Abstract

This study investigates the link between board gender diversity (BGD) and firm performance (FP). The analysis is conducted using Fortune 500 firms in the Science, Technology, Engineering, Mathematics, and Finance (STEM&F) sectors covering a period of seven years, from 2007 to 2013. The theoretical framework combines several theories that give shape to the critical mass effect of BGD on FP. This shape shows that below the critical mass threshold, BGD may represent a disadvantage to the board as it may facilitate the formation of subgroups, dysfunctional conflicts, and distrust. However, at or above the critical mass threshold, BGD facilitates better monitoring of management, greater resource provisions, and divergent thinking. To ensure sound results, this study addresses endogeneity concerns regarding omitted variable bias, reverse causality, and dynamic endogeneity. These results support a significant U-shaped relationship between the number of female directors and FP in the STEM&F sectors. That is, BGD yields higher FP when there is a critical mass of women on the board. This finding remains robust when alternative proxies for BGD and FP are employed and is consistent with the predictions of our theoretical framework. Our analysis also reveals that the positive effect of BGD on FP increases when there is at least a critical mass of 30% of women on a corporate board. This finding suggests that boards that have reached a critical mass of 30% of women present a favorable environment to capitalize on innovative ideas arising from BGD.

Corporate boards influence not only the lives of millions of employees and consumers but also play a major role in determining the policies and practices in the global marketplace (Rhode & Packel, 2014). Gender diversity on corporate boards has historically focused on the social justice aspects of female representation as the goal. Rightly so. Women represent 49.6% of the world population and 34% of the nonagricultural worldwide workforce (Population Reference Bureau, 2015; United Nations, 2015). Thus, from a social justice perspective, women should be proportionately represented on corporate boards. However, while the social justice argument is strong and substantial, it could easily fall on deaf ears in the current economic climate. During more recent years, and particularly after the 2008 Global Financial Crisis (GFC), there has been a shift in focus to the business case for women on corporate boards (WOCBs). Rather than argue for the appointment of female directors based on equal opportunity and fairness, the arguments for their inclusion have been increasingly presented regarding a business case (Burgess & Tharenou, 2002; Carter, D’Souza, Simkins, & Simpson, 2010). Yet the academic literature supporting a business case for WOCBs has not yet given a clear answer to the nature of the relationship between gender-diverse boards and firm performance (FP; Joecks, Pull, & Vetter, 2013).

Linear empirical studies show that female directors are associated with positive, negative, and neutral effects on FP (for a review, see, e.g., Post & Byron, 2015). However, these studies fail to deal with the effects of tokenism or the existence of a critical mass (Post & Byron, 2015). The current studies exploring the role of a critical mass reveal that the mere presence of women on boards (WOBs) does not guarantee desirable levels of influence on board decisions or improvements in FP. Rather, to mitigate tokenism, it may be necessary to have WOBs in sufficient numbers (Joecks et al., 2013; Strydom, Au Yong, & Rankin, 2016). These studies are just beginning to show how board gender diversity (BGD) leads to greater social performance (Post, Rahman, & Rubow, 2011), innovation (Torchia, Calabro, & Huse, 2011), and FP (Joecks et al., 2013).

Our study adds to the debate on the relationship between BGD and FP by further exploring the critical mass theory (CMT). It adds to the recent stream of literature exploring whether the association between BGD and FP is U-shaped, rather than linear. In addition, it advances the analysis of the CMT, by testing the moderating effect of reaching a critical mass of 30% of female directors on the BGD–FP relationship. While doing so, this study addresses and expands on the three main issues in the existing literature on the BGD–FP nexus: (a) measuring diversity, (b) addressing causality between diversity and performance, and (c) investigating the CMT (Lückerath-Rovers, 2013). Our study uses two measures rather than one measure of gender diversity. It addresses causality by using a two-step system generalized method of moments (GMM) estimator, and it explores the CMT both theoretically and empirically. In particular, our contribution expands on Joecks et al. (2013) by using a larger number and more widely used FP measures, a longer and more recent time span, and more robust econometric techniques.

Furthermore, to our knowledge, there are no empirical studies that have tested the effect of a critical mass of women directors on U.S. boards. This current research is the first to empirically explore the curvilinear link between BGD on Fortune 500 boards and FP. We specifically selected the STEM&F (Science, Technology, Engineering, Mathematics, and Finance) sectors as the positive effects of greater BGD on FP may be more pronounced in firms predominantly characterized by complex tasks and innovative output (Adams & Kirchmaier, 2016). Choosing the right context when modeling the BGD–FP relationship may have an important effect on strengthening the results, and yet many studies fail to consider it (Johnson et al., 2013; Post & Byron, 2015; Pye & Pettigrew, 2005). We propose that an increased number of women in boardrooms, and specifically in the STEM&F industries, significantly improves FP after reaching a critical ratio (at least 30% of female directors). Also, we examine different theoretical perspectives that address the advantages and disadvantages of gender diversity. Our theoretical framework gives support to a curvilinear (i.e., U-shaped) relationship between BGD and FP, presenting the “critical mass” as a decisive moderator of the BGD–FP relationship.

The article is structured as follows. The next section summarizes prior literature, discusses the theoretical background, and develops the research hypotheses. The third section describes the context, data, and method. The fourth section shows the statistical analyses and provides a discussion of the results. The last sections present the conclusions, practical implications, limitations, and future research.

Theory and Hypotheses

Recent Studies on Board Gender Diversity and Firm Performance

The empirical evidence is ambiguous concerning the effect that BGD has on FP. One stream of empirical findings points to the idea that a higher representation of women on the board is related to improved profitability (Erhardt, Werbel, & Shrader, 2003), higher firm value (Campbell & Mínguez-Vera, 2008; Carter, Simkins, & Simpson, 2003), and higher abnormal returns (Francoeur, Labelle, & Sinclair-Desgagné, 2008). However, other empirical findings point toward a negative association. In a study of U.S. firms during 1996 to 2003, Adams and Ferreira (2009) found that BGD had a negative effect on FP as measured by Tobin’s Q and ROA. Similarly, Haslam, Ryan, Kulich, Trojanowski, and Atkins (2010), in a study of the FTSE 100 companies during 2001 to 2005, found that gender diversity had a negative influence on profitability, that is, ROA and ROE. Other studies found that BGD is unrelated to firm value, i.e., Tobin’s Q (Carter et al., 2010; Rose, 2007) or firm profitability, i.e., ROS, ROA, ROI, and ROE (Shrader, Blackburn, & Iles, 1997). In an effort to reconcile these inconsistent findings, Post and Byron (2015) conducted a meta-analysis using 140 studies from 35 different countries and found that BGD was positively related to higher accounting returns (i.e., ROA, ROE, and ROIC), but unrelated to market performance (market-to book ratio, Tobin’s Q, stock performance, and shareholder returns). The authors contend that their finding of a positive relationship between female directors and accounting returns supports the critical mass argument. For instance, under conditions of non-tokenism, women exert a greater influence on FP. However, this article has two major shortcomings: specifically, the inability to determine a causal relationship (Rhode, 2016) and to empirically test the critical mass role.

Given the inconclusive evidence from linear studies, some researchers have recently tested this concept (the BGD effect on FP after a critical mass is attained). This involved two different legal environments, that is, in countries with and those without mandatory board gender quotas. Ahern and Dittmar (2012) and Matsa and Miller (2013) explored the effects of Norway’s 2006 quota (i.e., 40%) and reported that after the firms adopted the quotas, there was a significant drop in firm value (i.e., Tobin’s Q) and in operating (short-term) profits. Specifically, they argue that the abrupt increase of the female directorships, from 18% to 40% in 3 years, led to younger and less experienced boards that deteriorated the performance of Norwegian corporations (Ahern & Dittmar, 2012).

Conversely, in countries where a critical mass is attained without enforcement of gender quotas, a critical mass of WOBs is associated with better corporate governance practices and higher FP. Kramer, Konrad, Erkut, and Hooper (2006) carried out a qualitative study through interviews and discussions with 50 women directors, 12 CEOs, and seven corporate secretaries from Fortune 1000 companies. Their research revealed that a critical mass of three or more women could cause a fundamental change in the boardroom and enhance corporate governance. The more recent research employed quantitative approaches to explore the link between BGD and earnings quality or FP and their curvilinear nature. For example, Strydom et al. (2016), in an analysis of Australian firms in the years 2005 to 2013, suggested the existence of a U-shaped relationship between BGD and earnings quality and indicated “30%” as a tipping point at which the benefits of a critical mass of women emerge. Joecks et al. (2013) in an empirical study of 151 German stock exchange companies during the years 2000 to 2005 found that tilted boards, that is, boards with three or more women directors serving simultaneously are associated with higher FP (i.e., ROE) in comparison with all-male boards. Furthermore, Joecks et al. (2013) observed that this association represented a U-shaped form.

Main Theoretical Frameworks

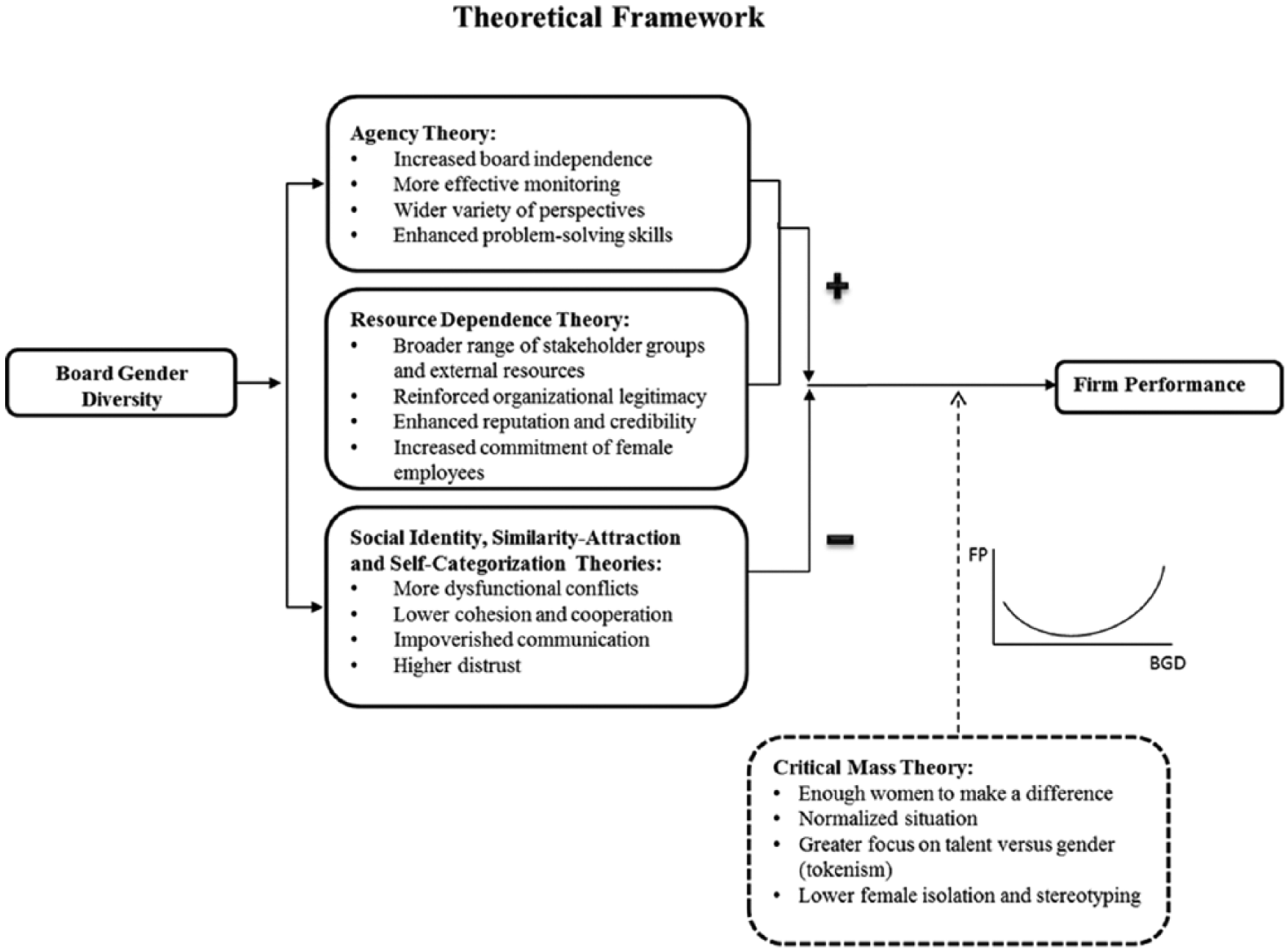

The benefits of greater BGD are generally derived from the agency theory (AT) and resource dependence theory (RDT) which denote boards that provide strong, sound, and timely advice to the executives and as such provide guidance, legitimacy, and access to essential resources. The drawbacks of BGD are explained through related theories such as the social identity theory (SIT), similarity–attraction theory, and self-categorization theory, which denote a board with dysfunctional group dynamics. To reconcile these conflicting results, the CMT conjectures that to realize the benefits of gender diversity, there should be more than superficial diversity (Barroso, Villegas, & Pérez-Calero, 2011; Hillman & Dalziel, 2003; Johnson, Daily, & Ellstrand, 1996). These benefits and drawbacks are shown in the theoretical framework in Figure 1 and further discussed in the sections that follow.

Theoretical framework for the board gender diversity–firm performance.

Advantages of Board Gender Diversity

The agency theory (AT) asserts that when ownership and control are separated (as they are in most modern corporations), managers may pursue their self-interest at the expense of profit maximization, thereby creating “agency” costs. One of the potential remedies for reducing these agency costs and improving financial performance is the board (Dobbin & Jung, 2011; Fama & Jensen, 1983; Hillman & Dalziel, 2003). Drawing on this theory Carter et al. (2003) suggested that a more diverse board may entail better monitoring of managers and may foster a more ethical corporate culture that reduces fraud and lowers agency costs. Therefore, the argument underlying the agency framework proposes gender diversity as an instrument to help increase the monitoring effectiveness of the board and offers the possibility that the improved monitoring brings a positive impact on FP.

The improvement on board monitoring relies on (a) expanding the perspectives around the table, (b) increasing board independence, (c) eroding the male “group think” phenomenon, and (d) improving the attendance behavior of the board. Empirical research has found supportive evidence of a positive effect of women on the board monitoring function. For example, directors of a different gender or cultural background might ask unique questions (Campbell & Mínguez-Vera, 2008) and more often, bring and integrate a wider variety of perspectives that improve the board’s decision making (Rosener, 1990) and increase board independence (Carter et al., 2003). Kanter (1977) argued that the role of managers is profoundly masculinized since rationality and efficiency are the raison d’être for managerial control. Women on the board represent more heterogeneity of opinions which may help erode the boardroom hazard of masculine “group-think” (Burgess & Tharenou, 2002). Bart and McQueen (2013) found that female directors employed innately superior decision-making frameworks and process skills (i.e., considered everyone’s point of view), and were better able to fulfill the board’s fiduciary responsibility to shareholders. In addition, based on results from probit and fixed-effect OLS regressions on data from 86,714 directorships in the United States, Adams and Ferreira (2009) suggested that female directors have a better attendance record than their male colleagues, are less prone to miss board meetings and are more likely to join monitoring committees. Furthermore, Huse and Solberg (2006) using a qualitative analysis, collecting stories from eight women directors about their experiences from more than 100 corporate boards found that female directors are better prepared for board meetings than male directors and thus, female representation may improve board behavior and effectiveness. These boards that the women directors were associated with ranged from voluntary organizations and small partnerships to large multinational corporations.

The RDT attributes to corporate boards the essential role of managing the external environment, securing the necessary external resources, reinforcing organizational legitimacies, and preserving the image of the company. The basic tenet of RDT is that companies must effectively manage uncertainty in their environments. Consequently, they need board members with networking and coalition capabilities to engage agreements and secure resources that otherwise would be unobtainable or obtainable albeit at higher costs (Dalton & Dalton, 2010). By having women on their boards, firms may gain access to a broader range of stakeholder groups (Siciliano, 1996), may boost organizational legitimacy (Hillman & Dalziel, 2003) and information exchange (Larcker, So, & Wang, 2013), and, in turn, enhance customer and employee relations (Hillman, Shropshire, & Cannella, 2007). This might also enhance a firm’s reputation and credibility with stakeholders (investors and customers), subsequently increasing FP, that is, firm profitability and value (Carter et al., 2003; Erhardt et al., 2003; Roberson & Park, 2007). Perrault (2015) found that by enhancing perceptions of a board’s legitimacy, women contribute to the perceptions of board’s trustworthiness which potentially generates higher FP regarding firm value, that is, Tobin’s Q. Hillman et al. (2007) extended the application of board reputation by arguing that the presence of female board members increases commitments from female employees reducing turnover costs and thus increasing firm profitability.

Disadvantages of Board Gender Diversity

Several related theories on intergroup relationships such as SIT (Tajfel & Turner, 1986), similarity-attraction theory (Berscheid & Walster, 1969; Byrne, 1971), and the self-categorization theory (Turner, Hogg, Oakes, Reicher, & Wetherell, 1987) predict that diversity might have a disruptive role in group dynamics. According to the SIT (Tajfel, 1978), individuals try to maintain a positive self-identity by surrounding themselves with similar others. Social identity processes maximize conformity within in-group individuals (similar others) and discrimination against out-group individuals (dissimilar others) to enhance this positive self-identity. Similarity–attraction theory (Byrne, 1971) proposes that individuals are positively inclined toward similar others. Similarity is likely to enhance social interaction (Ibarra, 1993) and the formation of coalition among similar individuals (Byrne, 1971), but leads to more conflicts between or across individuals which fall in different groups (Hogg, Turner, & Davidson, 1990). The self-categorization theory (Turner et al., 1987) assume that people create social categories based on visible characteristics, for example, gender, which foster the creation of in-group and out-group distinctions. On a board of directors, the social categorization processes may give rise to the formation of gender-based subgroups, where members belong either to the in-group (“us”) or out-group (“them”), and tend to like and trust “us” more than “them” (Brewer, 1979; Jones, Hillier, & Comfort, 2013; Turner et al., 1987). This subgrouping elicits dysfunctional conflicts, reduces cohesion and cooperation, hinders communication, and generates distrust across female and male board directors (Jehn, Northcraft, & Neale, 1999; Milliken & Martins, 1996). When these negative processes (e.g., conflicts and miscommunication) materialize, the benefits of diversity are more likely to be diluted and FP is likely to be negatively affected.

The women’s underrepresentation on the board of directors has led some researchers to see female directors as “tokens,” who are highly visible and marginalized for being unique. As tokens, female directors may be perceived negatively and are often doubted or not trusted (Torchia et al., 2011) and as a result, they may feel uncomfortable, isolated, or hold self-doubt (Kanter, 1977), which may interfere with their performance (Powell & Graves, 2003). Female directors may not be listened to or taken seriously, and they may, therefore, sense a lack of support and in such a situation, not perform to their fullest potential.

Critical Mass Theory

The CMT refers to the particular number of personnel needed to affect policy and to make a change, not as a token; but, as an influential body (Kanter, 1977). As such, it addresses the issue of having the “right” number of WOCBs (Konrad, Kramer, & Erkut, 2008; Torchia et al., 2011). According to Kramer et al. (2006), when there is only one woman on the board, she may experience the bias and limitations of tokenism. Having three women on a board normalizes the situation and removes the focus from gender to talent (Konrad et al., 2008) resulting in lower out-group bias for female members (Torchia et al., 2011). With at least three women on the board, they are more comfortable to indicate their concerns, less pressured to prove themselves, and more confident of their talent (Kramer et al., 2006). CMT postulates that unless a certain threshold or critical mass of WOCB is reached, gender barriers are not broken down, and the benefits of gender diversity do not appear.

Hypotheses

From AT and RDT, a positive linear relation is predicted; from intergroup relationship theories a negative linear relationship is expected, while a U-shaped form is obtained from the integration of these theories under the CMT framework. In this context, some authors have identified a curvilinear relationship between BGD and FP. For example, Joecks et al. (2013) postulate that there is a U-shaped curvilinear relationship between BGD and FP. Only when boards reach a critical mass of women of about 30% or above (i.e., three women), the FP of gender diverse boards exceed that of an entirely male board. Other researchers also suggest the existence of a curvilinear relationship with inflection points at high and low levels of female representation. These studies, however, are empirically limited by the rare occurrence of boards with high levels of female directors (i.e., female-dominated boards). For example, Nguyen, Locke, and Reddy (2015) suggest that in female-dominated boards (i.e., 80% are women), the costs of diversity may outweigh its benefits, as it may happen in the situation of a male-dominated board (i.e., 20% are female). They, however, explicitly state their impossibility to prove this statement empirically. Schwab, Werbel, Hofmann, and Henriques (2016) indicate that “too little” or “too much” of either gender in management triggers dysfunctional group processes that impede the attainment of performance benefits. However, they use male-dominated firms as a proxy for female-dominated firms, given the scarce availability of the latter.

The CMT gives ground to understanding that a curvilinear relationship is theoretically possible. This relationship is circumscribed to boards having predominantly more men than women and supports our testing the CMT. It is impractical to test the relationship in reverse since it is rare to find all-female boards or boards where females are predominant (Nguyen et al., 2015; Schwab et al., 2016). Under these conditions, we anticipate that the BGD–FP relationship will follow a U-shaped form, where, above a certain threshold, gender diverse boards are associated with considerable financial gains, and below that threshold, gender diverse boards are associated with practically no gains or even losses. The proposed U-shaped association could explain the existing conflict in the empirical findings in prior research, given previous research mostly explored linear associations (Adams & Ferreira, 2009; Campbell & Mínguez-Vera, 2008; Carter et al., 2010; Rose, 2007). Therefore, Hypothesis 1 is stated as follows:

Along with the curvilinear nature of the BGD–FP relationship, and in line with the predictions of the CMT, we analyze the moderating effect of the existence of a critical mass of 30% of women on the BGD and FP relationship. We anticipate that the women’s contribution to FP will be more accentuated in boards that reach at least the 30% threshold. The critical mass is predicted to be about 30% (Cohen, Broschak, & Haveman, 1998), or about three female directors in an average board of 10 directors (Kramer et al., 2006). Joecks et al. (2013) argue that if there is a critical mass of female directors that positively affects FP, this lies in the rage of 20% to 40% female directors. More specifically, they point to 30%—or about three women—as the critical mass point to effect a positive change. Kanter (1977) also suggested that the threshold (i.e., critical mass) for minorities (e.g., women) to influence the culture of the organization was approximately one-third of the group. Kramer et al. (2006), using absolute numbers of female directors, argues that below the critical mass, one or two women may have no impact or even a negative impact on governance. Once the critical mass is achieved, the impact of WOBs decisions becomes more pronounced. Dahlerup (2006) identified 30% as the critical mass at which “a large minority can make a difference, even if still a minority.” Based on this, we hypothesize that BGD will be more positively related to FP in boards with, at least, a critical mass of women of 30%, that is, in boards where women are able to influence the content and process of board discussions more substantially (Kramer et al., 2006). Therefore, Hypothesis 2 is stated as follows:

Context, Sample, Data Sources, Measures, and Method

Context

In this study, we use two contextual factors that have the potential to positively influence the effect BGD has on FP. The first contextual factor is the use of STEM&F companies. These companies need leaders who can respond to disruptive variations in the environment and sustain and generate continuous innovation (Makri & Scandura, 2010). Establishing a board with the right skills is crucial to having the competency to ensure the firms’ survival and success. In this context, empirical studies show evidence that BGD is associated with superior handling of nonroutine tasks (Hillman et al., 2007), a greater likelihood of creating new products and services (Østergaard, Timmermans, & Kristinsson, 2011), and greater firm innovation. Innovation is generally accepted to be positively related to FP and, is an essential component to the firm’s survival (Hull & Rothenberg, 2008; Miller & Triana, 2009; Torchia et al., 2011), especially in the STEM-intensive sector. In an analysis of workforce diversity and firm productivity across industries in Belgium, Garnero, Kampelmann, and Rycx (2014) found empirical evidence that gender diversity generates significant gains in high-tech/knowledge-intensive sectors than in more traditional industries.

Another contextual factor is the selection of a time period for the study. We chose recent years, that is, 2007 to 2014, including the 2008 GFC, where boards were more prone to opening their doors to women. The 2008 GFC exposed the hypermasculine composition of boards and senior leadership teams across most U.S. firms (McDowell, 2011). A debate regarding whether greater gender diversity could have prevented certain masculine behaviors allegedly behind the crisis ensued (Van Staveren, 2014) and motivated the emergence of voluntary efforts, investor-driven initiatives, regulatory actions, and more public scrutiny on board composition. Concomitant with these, the overall proportion of Fortune 500 board seats occupied by women went up slightly from 11.7% in 2000 to 14.8% in 2007, and 18.0% in 2013 (Catalyst, 2013; Gero & Sonnabend, 2015). The boardroom dynamics also began to change from a male-dominated culture to a more gender-inclusive one, where female and male directors held similar board roles (Jonsdottir, Singh, Terjesen, & Vinnicombe, 2015); female directorships were more likely to be accepted (Ryan & Haslam, 2007); and boards were more inclined to overcome their gender biases in order to improve decision making and ethicality (Sun, Zhu, & Ye, 2015).

Sample and Data Sources

Previous U.S. studies investigating the BGD–FP nexus did so across all Fortune 500 firms with sample sizes ranging from 112 companies over a span of 1 year (Erhardt et al., 2003) to 353 firms for each year of a 4-year analysis (Carter, D’Souza, Simkins, & Simpson, 2007). This current study focuses on Fortune 500 firms in the STEM&F sectors where women may potentially have a greater impact. Other such studies used years that did not align with the potential for identifying gender-related contributions on corporate boards. The present study targets a particular period where there were sufficient and increasing numbers of WOCBs and focuses on the years of the GFC and beyond as a period when there might be a greater openness to different perspectives from diverse board members.

Two datasets were used to examine our hypothesis. One dataset is the Institutional Shareholder Services Directors Data, which includes corporate governance data on each director of the Standard & Poor’s 1500 (S&P 1500) for the years 2007 through to 2013. For this dataset, we used firms that were included in the Fortune 500 list during the years 2007 to 2014, and those operating in the STEM&F sectors. 1 The other data resource was Mergent Online, which covers financial data for the same companies from 2008 to 2014. When both databases were merged, we obtained an unbalanced sample of 1,605 firm-year observations representing 236 Fortune 500 firms in the STEM&F sectors.

Measures

Independent Variables

This study estimates BGD (Board Gender Diversity) using the exact number of women on the board of directors (Carter et al., 2010; Dobbin & Jung, 2011) and its square (Board Gender Diversity2). The variable Board Gender Diversity allows us to examine whether a greater number of WOCB has an impact on FP, whereas the quadratic term makes it possible to check for curvilinearities in such a relationship, for example, the existence of a critical mass of WOCBs. Also, we use alternative proxies for BGD to test the robustness of our findings. These include the proportion of female directors (the Pct. Board Gender Diversity; Adams & Ferreira, 2009; Nguyen et al., 2015) and its square (Pct. Board Gender Diversity2) (Ntim, 2015).

Dependent Variables

Following earlier studies (Adams & Ferreira, 2009; Carter et al., 2003; Carter et al., 2007; Carter et al., 2010; Nguyen et al., 2015), we employ a market-based measure, Tobin’s Q, as a proxy of FP. Tobin’s Q is an indicator of a firm’s stock performance and is widely considered as the best measure of a firm’s market value (Dobbin & Jung, 2011). It is the firm’s current market valuation divided by the replacement costs or book value of the firm’s assets. As in Nguyen et al. (2015), we transform Tobin’s Q into a natural logarithm to mitigate the potential effects of outliers which commonly tag this measure. When compared with using the raw measure, this transformation evidences better statistical distribution properties (Hirsch & Seaks, 1993). In addition, for robustness and comparisons with earlier studies, we employ two additional accounting-based measures of FP: (a) ROA—return on assets (Dobbin & Jung, 2011; Farrell & Hersch, 2005; Shrader et al., 1997), and (b) ROI—return on investments (Miller & Triana, 2009; Zahra & Stanton, 1988).

Moderating Variables

Following research on critical mass, we propose a critical mass of 30% of WOCB as a moderating variable in the BGD–FP relationship. For example, Joecks et al. (2013) followed Kanter (1977) in categorizing the gender composition of work-groups and pointed out 30% (i.e., a representative figure for tilted boards) as the starting point to unlock women’s positive contribution to FP. Other studies use the raw number of women, for example, three or more women, to establish a critical mass (Konrad et al., 2008; Post et al., 2011). However, we believe that such a ratio encapsulates the effect of male–female board balance, given the large dispersion of the board size in our sample (i.e., a minimum of six directors, maximum of 19 directors). Thus, the 30% threshold combines the magic number of “three women” on a 10-member board and is often used as a catalyst for improving group dynamics. This variable is a dummy variable that takes the value “0” when firms have a ratio less than 30% and “1” when firms have a ratio of 30% or more women.

Control Variables

We include controls for several widely used firm and board characteristics that are deemed to have an impact on our dependent variable, that is, FP. These consist of two sets. The first set comprises firm characteristics: firm age (Miller & Triana, 2009; Nguyen et al., 2015) measured as the number of years since the company was founded; firm size (Adams & Ferreira, 2009; Carter et al., 2010) measured as the logarithm of total assets; the degree of firm internationalization (Masulis, Wang, & Xie, 2012; Oxelheim, Gregorič, Randøy, & Thomsen, 2013) calculated as the percentage of foreign sales; and the number of business segments (Adams & Ferreira, 2009; Sila, Gonzalez, & Hagendorff, 2016) tabulated by the four-digit SIC code classification.

The second set of variables are governance variables and involve the characteristics of the board and its members. These include Chairperson of the Board (COB) and Chief Executive Officer (CEO) duality, that is, COB & CEO duality (Bhagat & Bolton, 2008; Holm & Schøler, 2010; Singla, George, & Veliyath, 2010); board size (Rose, Munch-Madsen, & Funch, 2013; Sanders & Carpenter, 1998; Zahra, Priem, & Rasheed, 2007), measured as the number of directors on the board; board independence (Musteen, Datta, & Herrmann, 2009; Pérez-Calero Sánchez, Villegas-Periñán, & Barroso-Castro, 2013; Sila et al., 2016), calculated as the proportion of independent directors to board size; board ownership (Bhagat & Bolton, 2008; Carter et al., 2010), measured as the sum of the shares held by the board directors divided by the firm’s outstanding shares; and additional directorships (Carter et al., 2010), measured as the average number of all the extra board seats held by the firm’s board members. Also, included in the second set are board financial expertise or financial independent experts on the audit committee (FIEA; Bédard, Chtourou, & Courteau, 2004; Güner, Malmendier, & Tate, 2008), measured as the total number of independent directors with financial expertise and who sit on the audit committee, and foreign independent director (FID Indicator; Masulis et al., 2012; Oxelheim et al., 2013), measured as a dummy variable that equals one if the firm has at least one foreign independent directors, that is, independent directors domiciled outside the United States and zero otherwise. Finally, we analyzed two other board characteristics including director’s age and director’s tenure (Alderfer, 1986; Carlsson & Karlsson, 1970; Masulis, Wang, & Xie, 2007; Vroom & Pahl, 1971).

Method

Method Development

Our goal is to explore how women directors affect FP. This relationship, as suggested by Hermalin and Weisbach (2001), is prone to endogeneity biases. For example, high-performing boards may be noted for bringing women on their boards, making it difficult to ferret out whether to attribute the advances in FP to the number of women on their boards (Farrell & Hersch, 2005) or other factors, such as high-performance practices. Thus, studies examining how female directors affect FP should control for the endogenous nature of this relationship to obtain reliable estimates and to correctly infer causality (Adams & Ferreira, 2009; Carter et al., 2010; Dezsö & Ross, 2012; Hermalin & Weisbach, 2001). The three primary sources of endogeneity include Omitted Variable Bias (OVB), reverse causality, and dynamic endogeneity. OVB occurs when a model is created and incorrectly omits one or more important factors. Reverse causality occurs when the model includes endogenous explanatory variables (Adams & Ferreira, 2009; Hermalin & Weisbach, 2001), and dynamic endogeneity (Wintoki, Linck, & Netter, 2012) occurs when there are intertemporal effects between governance variables and FP.

Most of the previous empirical studies on this topic suffer from one, two, or all three endogeneity biases. Indeed, the statistical examinations carried out by Zahra and Stanton (1988); Erhardt et al. (2003); Shrader et al. (1997); Farrell and Hersch (2005); and Desvaux, Devillard-Hoellinger, and Baumgarten (2007) used univariate tests that did not control for either type of endogeneity. Other studies such as those by Adams and Ferreira (2009); Anderson, Reeb, Upadhyay, and Zhao (2011); Carter et al. (2010); Carter et al. (2003); and Sabatier (2015) only attempted to control for two endogeneity biases: OVB and reverse causality using an instrumental variable technique along with fixed effects. In the present study, we apply the dynamic panel GMM estimator proposed by Arellano and Bover (1995) and Blundell and Bond (1998). The GMM technique allows us to simultaneously address the three key endogeneity biases that can influence the BGD–FP nexus.

First, it addresses reverse causality by instrumenting the endogenous explanatory variables through their lagged values (Blundell & Bond, 1998). The reliability of these instruments is tested with the Hansen (1982) test of overidentifying restrictions and the Arellano and Bond (1991) test for second-order autocorrelation in the first-differenced errors. Second, it controls for the potential impact of performance persistence (i.e., dynamic panel bias) by adding lags of each dependent variable (Roodman, 2009; Wintoki et al., 2012). Third, it helps to mitigate OVB bias through a fixed effect approach (Nguyen et al., 2015). Additionally, the GMM estimator has proven to be the best-performing estimator for dealing with endogeneity in the field of corporate governance (Chapple & Humphrey, 2014; Nguyen et al., 2015; Sila et al., 2016; Wintoki et al., 2012) and specifically for panel datasets like ours. Such panel datasets are (a) short with (b) endogenous explanatory variables, and (c) dynamic dependent variables (Flannery & Hankins, 2013; Zhou, Faff, & Alpert, 2014)

Model Specification

Following Wintoki et al. (2012), our dynamic model specification for estimating the BGD–FP relationship takes the following form:

where FP is the firm performance variables; CG is the corporate governance variables; and FC is the firm characteristic variables. The i index refers to each firm and the t index to each year. φ, β, and δ are vectors of coefficients on FPi,t-1, CVi,t-1, and BGDi,t-1. Yeari represents year dummies, ηi is a firm-specific effect representing unobserved time-invariant characteristics of the firm influencing its performance, and εi,t is the error term. We lag all control and independent variables that appear on the right-hand side of our regression models to minimize endogeneity problems (Carter et al., 2010; Ntim, 2015; Yermack, 1996). We include the first lag of our dependent variable on the right-hand side of our BGD–FP equation to control for the persistence of performance differences between firms. We find that including the first lag of our dependent variable in the regression equations is sufficient to accomplish this goal, as the second lag of our dependent variables is statistically insignificant. This technique was similarly reported in recent empirical studies in the governance literature (Delis, Gaganis, Hasan, & Pasiouras, 2017; Nguyen et al., 2015). All the explanatory variables except year dummies and firm age are included in the regressions as endogenous variables (Schultz, Tan, & Walsh, 2010; Wintoki et al., 2012).

The hypothesis proposed in this research were studied using GMM regression analysis with year fixed effects and firm-cluster robust standard errors, small-sample adjustments, and orthogonal deviations, and using a set of different models to assess robustness. The different models considered FP as the dependent variable, BGD as the independent variable and the squared term of BGD and Critical Mass as moderating variables. Furthermore, three sets of control variables were introduced in a step by step fashion. Before estimating the model, we confirmed that the data used for the estimation fulfilled the assumptions required for regression analysis concerning normality and multicollinearity.

Empirical Results

Descriptive Analysis

Table 1 shows the descriptive statistics for all variables. The average number of female directors in our data sample was 1.88, which corresponds to an average of 17% female board members. In comparison, this figure is almost twice the proportion of WOCB in previous research studies (Adams & Ferreira, 2009; Carter et al., 2010; Farrell & Hersch, 2005). It indicates that women still represent a small share of the total U.S. board seats and often do not occupy enough board seats to constitute a critical mass (e.g., three or more women). Of all the Fortune 500 firms, only 23% have three or more women on the board. Having two women on the board is the most popular board gender configuration. Slightly more than 40% (i.e., 41% of firms) exhibit this pattern. While these numbers are small, they are higher than those reported by recent empirical studies on critical mass (Joecks et al., 2013; Torchia et al., 2011).

Descriptive Statistics of the Sample.

Note. For comparison purposes, Tobin’s Q is reported as raw numbers.

Regression Analysis

Table 2 presents the results for Hypothesis 1 which proposed that BGD would have a U-shaped relationship with FP. To test this relationship, we use the number of female directors alone and in conjunction with its squared term. The model was developed in three steps. The firm control variables were entered in Step 1, the board characteristics of the firms were entered in Step 2, and additional characteristics of the directors were entered in Step 3. Model 1(a)/(b)/(d) use the squared term of Board Gender Diversity, whereas Model 1(c) only uses the linear term. A significant positive coefficient for this squared term would be consistent with the expected curvilinear effect.

Dynamic Panel GMM Regressions: The Effect of Board Gender Diversity on Firm Performance—Linear and Nonlinear Effects.

Note. aFID = foreign independent director; FIEA = financial independent expert on the audit committee.bUnstandardized regression’s estimates are shown along with the robust firm-clustered standard errors, in brackets.

cLag 1 of the dependent variables is included in all models. All independent and control variables are treated as endogenous except the year dummies and firm age. The board diversity and control variables are instrumented by their Lags 2-3. The dependent variable, that is, Ln (Q)—natural logarithm of Tobin’s Q, is instrumented by Lag 2.

dThe null hypothesis for the Hansen test is that the overidentifying restrictions are valid.

eArellano–Bond test for AR(2), p-value refers to second-order autocorrelation in first-differenced errors.

fYears are controlled for by using dummy variables but not reported.

p < .10. *p < .05. **p < .01.

The results in Table 2 indicate that the squared term of BGD, that is, Board Gender Diversity2 is positively and statistically related to Tobin’s Q at the p < .1 level (Model 1[b]) and p < .05 level (Model 1[d]), indicating the existence of a curvilinear U-shaped effect, as suggested in Hypothesis 1. The results show that in general, adding control variables does not change the coefficient of the independent variables significantly. As shown in Table 2 Model 1(a) to 1(d), the linear effect of BGD is not significant. These results prove that, in general, a potential U-shaped relationship may exist between BGD and FP. For instance, this could mean that adding women to the board at low levels of BGD (e.g., less than three women) do not generate benefits or is detrimental to board dynamics. However, when a critical mass of women is reached, women start to create benefits that translate into superior financial performance. This is in line with Joecks et al. (2013) finding of a U-shaped effect of BGD on FP.

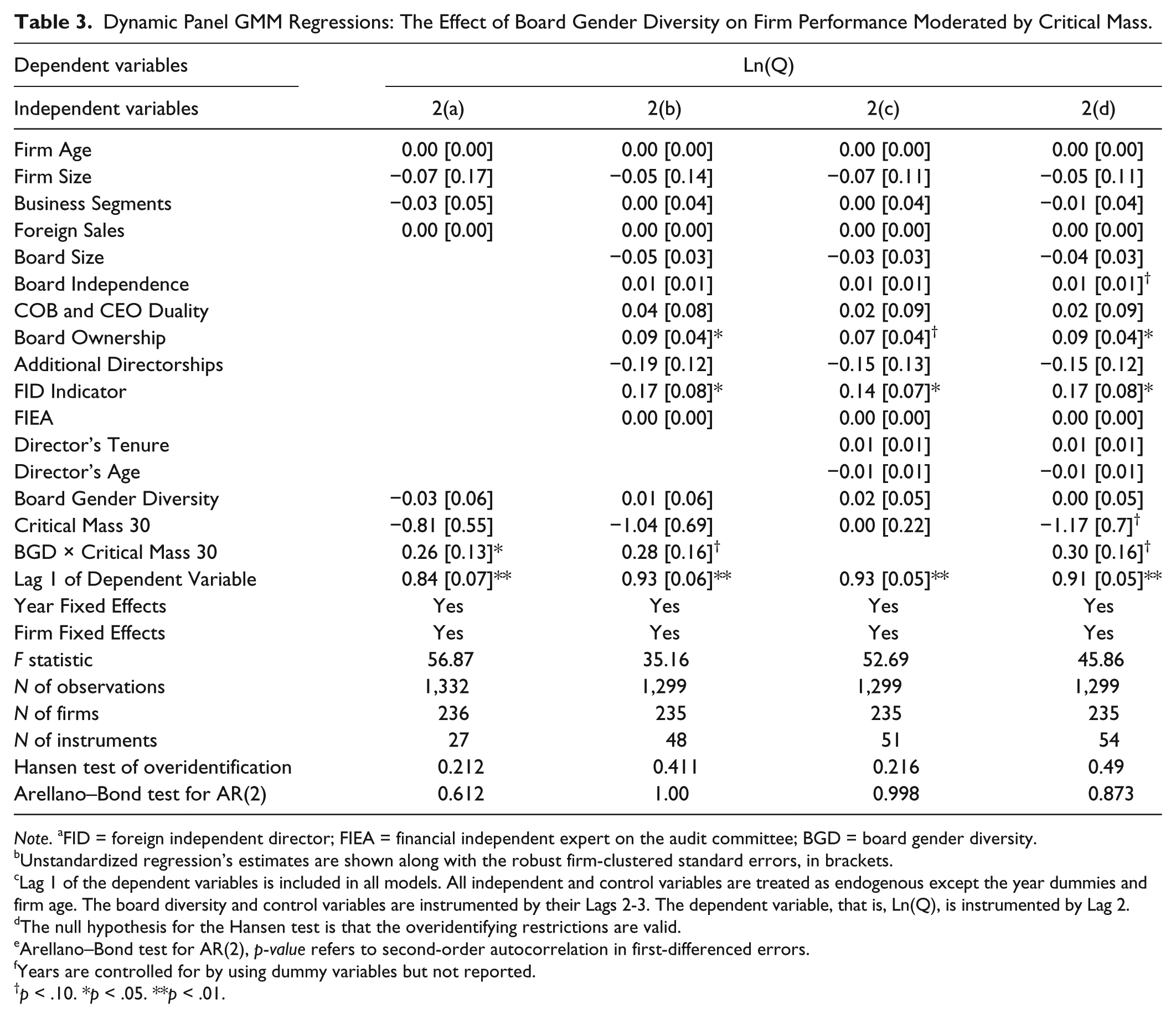

Table 3 presents the results of the GMM regressions for Hypothesis 2. Hypothesis 2 proposed that the BGD and FP relationship is moderated positively by a critical mass of 30%. We followed the same approach used before (Model 1[a]-1[d]), and developed the models in three steps. In this table, Model 2(a)/(b)/(d) use the interaction term of BGD and Critical Mass of 30%, whereas Model 2(c) does not. The results show that the coefficient of the interaction term, BGD × Critical Mass 30, is statistically significant at the p < .05 level (Model 2[a]) and p <.1 level (Model 2[b]/[c]) with a positive sign. Furthermore, the coefficient for the variable, Board Gender Diversity, maintains that it is not statistical significant for any of the Models, showing the absence of a BGD direct effect on FP. This result confirms Hypothesis 2 concerning the moderating effect of a critical mass, suggesting that the variable Board Gender Diversity has a significant and positive effect on FP when a critical mass of 30% of women is present on the board.

Dynamic Panel GMM Regressions: The Effect of Board Gender Diversity on Firm Performance Moderated by Critical Mass.

Note. aFID = foreign independent director; FIEA = financial independent expert on the audit committee; BGD = board gender diversity. bUnstandardized regression’s estimates are shown along with the robust firm-clustered standard errors, in brackets.

cLag 1 of the dependent variables is included in all models. All independent and control variables are treated as endogenous except the year dummies and firm age. The board diversity and control variables are instrumented by their Lags 2-3. The dependent variable, that is, Ln(Q), is instrumented by Lag 2.

dThe null hypothesis for the Hansen test is that the overidentifying restrictions are valid.

eArellano–Bond test for AR(2), p-value refers to second-order autocorrelation in first-differenced errors.

fYears are controlled for by using dummy variables but not reported.

p < .10. *p < .05. **p < .01.

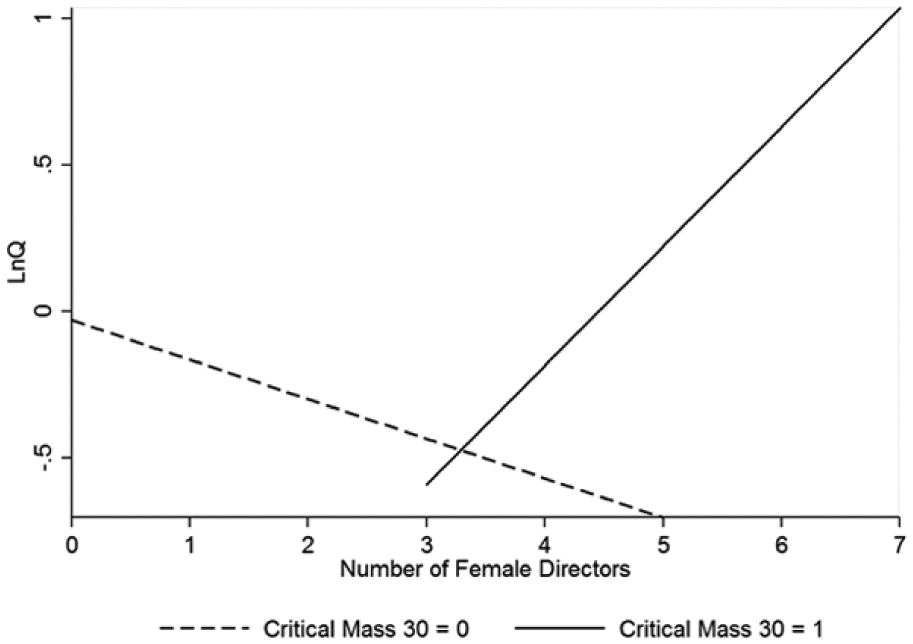

To provide a more visual representation of the moderating effect of a critical mass on the BGD–FP relationship, we have illustrated the interactions of Model 2(d) in Figure 2. Figure 2 shows that the BGD–FP relationship is different depending on whether boards do or do not reach a critical mass of 30% of women. Specifically, the BGD–FP relationship is positively sloped for boards with a critical mass of 30% of women or more and negatively sloped otherwise. Thus, boards reaching or surpassing the 30% threshold reflect a better scenario for women to be able to contribute to enhancing FP.

The moderating effect of critical mass on the BGD–FP relationship.

A post hoc analysis on the overlap area of Figure 2 revealed that boards that have four women and are below the 30% critical mass were significantly less likely to improve FP (i.e., LnQ) than boards that have four women and have reached the 30% critical mass. However, no significant differences were found for boards with three women regardless as to whether they attained the 30% critical mass. No post hoc analysis was performed for boards with five women given the small sample size of this group. 2 It is worth noting that the limited availability of boards with five women is representative of the rarity of female-dominated boards (Schwab et al., 2016). The post hoc results provide a greater insight into Figure 2 suggesting that when boards reach four women, the moderating effect of a 30% critical mass is instrumental in improving FP. These results are not tabulated for brevity.

Robustness Checks

Robustness to Alternative Proxies for Gender Diversity

To challenge our results, we apply the same two-step system GMM estimation on the same specification models developed in Model 1(a)-(d) but using an alternative proxy for BGD, that is, Pct. Board Gender Diversity (Pct. BGD) and its square. These new variables allow us to check whether an increase in the proportion of female directors on boards leads to their having a greater influence on FP and if that influence is U-shaped. The results displayed in Model 3(a)/(b) and (d) in Table 4 indicate that Pct. Board Gender Diversity2 is positively and statistically related to Tobin’s Q at the p < .1 level (Model 3[a]) and p < .05 level (Model 3[b] and 3[d]). Thus, a U-shaped relationship between BGD and FP remains significant, even after employing alternative proxies for gender diversity. Again, no significant linear relationship is found in any of the models (Model 2[a]-[d]). In sum, the results appear to consistently point to a BGD–FP relationship accommodating U-shaped effects.

Dynamic Panel GMM Regressions: Robustness Checks With Proportion of Female Directors as Proxy for Gender Diversity—Linear and Nonlinear Effects.

Note. aFID = foreign independent director; FIEA = financial independent expert on the audit committee. bUnstandardized regression’s estimates are shown along with the robust firm-clustered standard errors, in brackets.

cLag 1 of the dependent variables is included in all models. All independent and control variables are treated as endogenous except the year dummies and firm age. The board diversity and control variables are instrumented by their Lags 2-3. The dependent variable, that is, Ln(Q), is instrumented by Lag 2.

dThe null hypothesis for the Hansen test is that the overidentifying restrictions are valid.

eArellano–Bond test for AR(2), p-value refers to second-order autocorrelation in first-differenced errors.

fYears are controlled for by using dummy variables but not reported.

p < .10. *p < .05. **p < .01.

To provide a more visual interpretation of these results, we plotted a quadratic prediction graph for the Ln(Q) on Pct. BGD in Figure 3. The predicted values for the Ln(Q) were estimated in Model 3(d). As expected, the graph favors a model with a U-shaped effect of Pct. BGD on FP. As can be seen in Figure 3, the inflection point, where FP (i.e., LnQ) is minimized takes place at 20% of women. From this point, the curve slope starts to become predominantly upward trending. However, it is not until boards surpass the 30% threshold, that gender diverse boards start outperforming all-male boards. This indicates that the critical mass is around that threshold. According to Kanter’s classification, 3 this means that tilted boards (i.e., boards that are 20%-40% women) outperform skewed boards (20% women or less) and that balanced boards (i.e., boards that are 40%-50% women) seem to outperform all the others. These findings are in line with Joecks et al. (2013) which builds on Kanter (1977) influential work and suggests that in tilted boards, female directors are still perceived as a minority whereas male directors are considered majority. It is not until boards become balanced on gender that the majority and minority turn into potential subgroups with a focus on talents rather than gender-specific differences (Kanter, 1977). Such a turn enables the overall board to make high-quality decisions that improve FP.

U-shaped relationship between Ln(Q) and Pct. Board Gender Diversity.

A caveat worth noting about the graphical representation of Model 3(d) in Figure 3 is the small proportion of balanced boards used in this sample. These proportion although higher than in previous studies, for example, Joecks et al. (2013), it is both limited by and representative of what is imposed by the business world in terms of the representation of WOCBs (Joecks et al., 2013; Nguyen et al., 2015; Schwab et al., 2016). However, this limitation may make the graphical representation of the U-shaped BGD–FP relationship to be particularly sensitive to small variations in the FP of companies with balanced boards, yet would not fundamentally alter the finding of an empirical U-shaped relationship. Our empirical finding of a U-shaped relation between BGD and FP proves to be robust on different robustness tests, for example, for different FP proxies such as ROA and ROI, for different BGD proxies, and for different sets of controls. In addition, the finding of a U-shaped relationship between BGD and FP is also supported by recent empirical literature on critical mass, for example, Joecks et al. (2013) and anticipated by the critical mass framework.

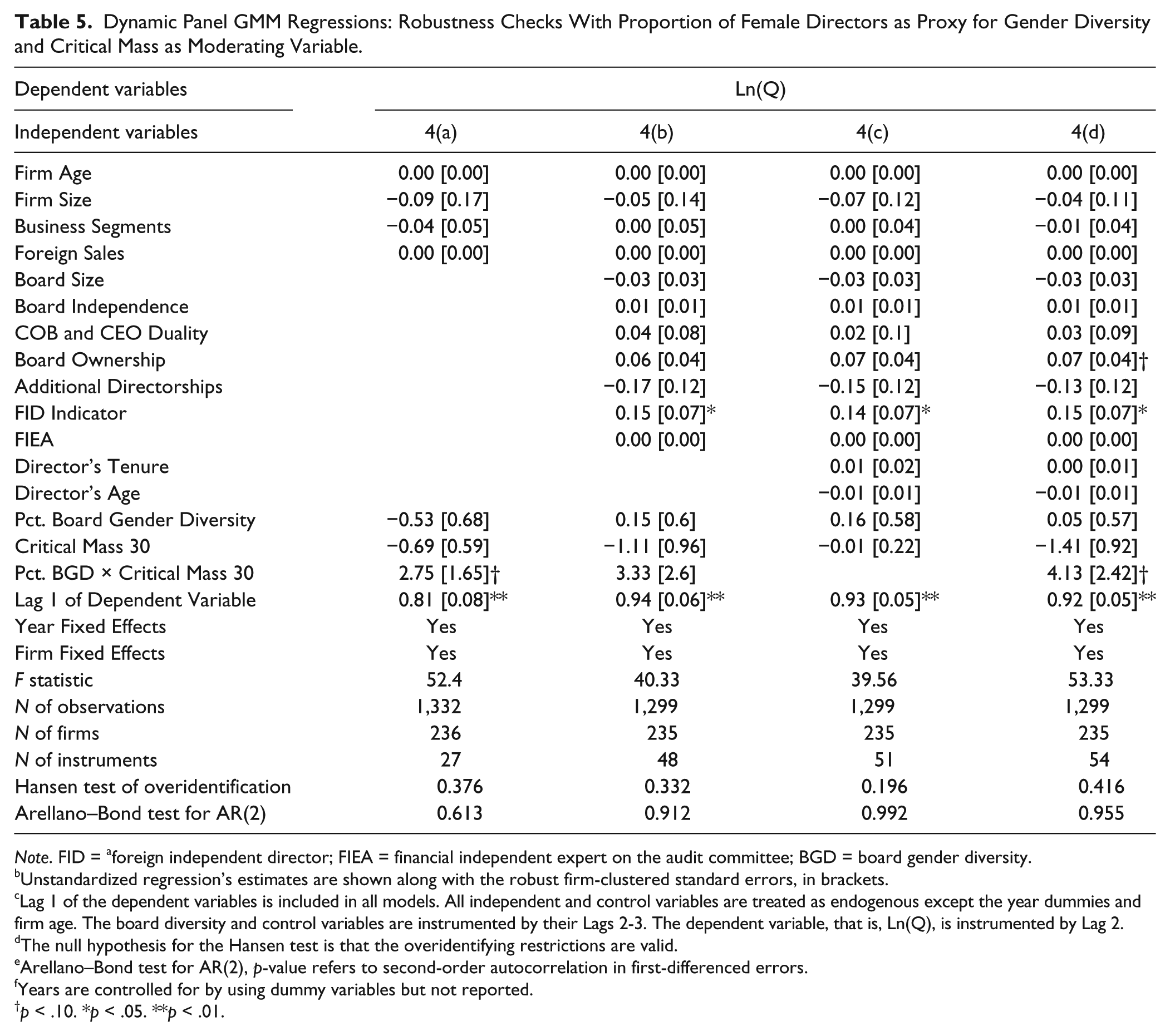

We also employed the proxy for BGD, that is, Pct. Board Gender Diversity and its interaction term, Pct. BGD × Critical Mass 30, to test the robustness of the results obtained in Models 2(a)/(b)/(c)/(d). Two (Model 4[a]/[d]) of the three models (Model 4[a]/[b]/[d]) in Table 5 indicate that the interaction term is positively and statistically related to Tobin’s Q at the p < .1 level. Thus, it supports the positive moderating effect of critical mass on the relationship between female representation and FP. Again, no significant linear relationship is found in any of the models (Model 4[a]-[d]). These results, in general, support Hypothesis 2 and indicate that for female directors to have a positive impact on FP; boards need to be at least 30% women.

Dynamic Panel GMM Regressions: Robustness Checks With Proportion of Female Directors as Proxy for Gender Diversity and Critical Mass as Moderating Variable.

Note. FID = aforeign independent director; FIEA = financial independent expert on the audit committee; BGD = board gender diversity. bUnstandardized regression’s estimates are shown along with the robust firm-clustered standard errors, in brackets.

cLag 1 of the dependent variables is included in all models. All independent and control variables are treated as endogenous except the year dummies and firm age. The board diversity and control variables are instrumented by their Lags 2-3. The dependent variable, that is, Ln(Q), is instrumented by Lag 2.

dThe null hypothesis for the Hansen test is that the overidentifying restrictions are valid.

eArellano–Bond test for AR(2), p-value refers to second-order autocorrelation in first-differenced errors.

fYears are controlled for by using dummy variables but not reported.

p < .10. *p < .05. **p < .01.

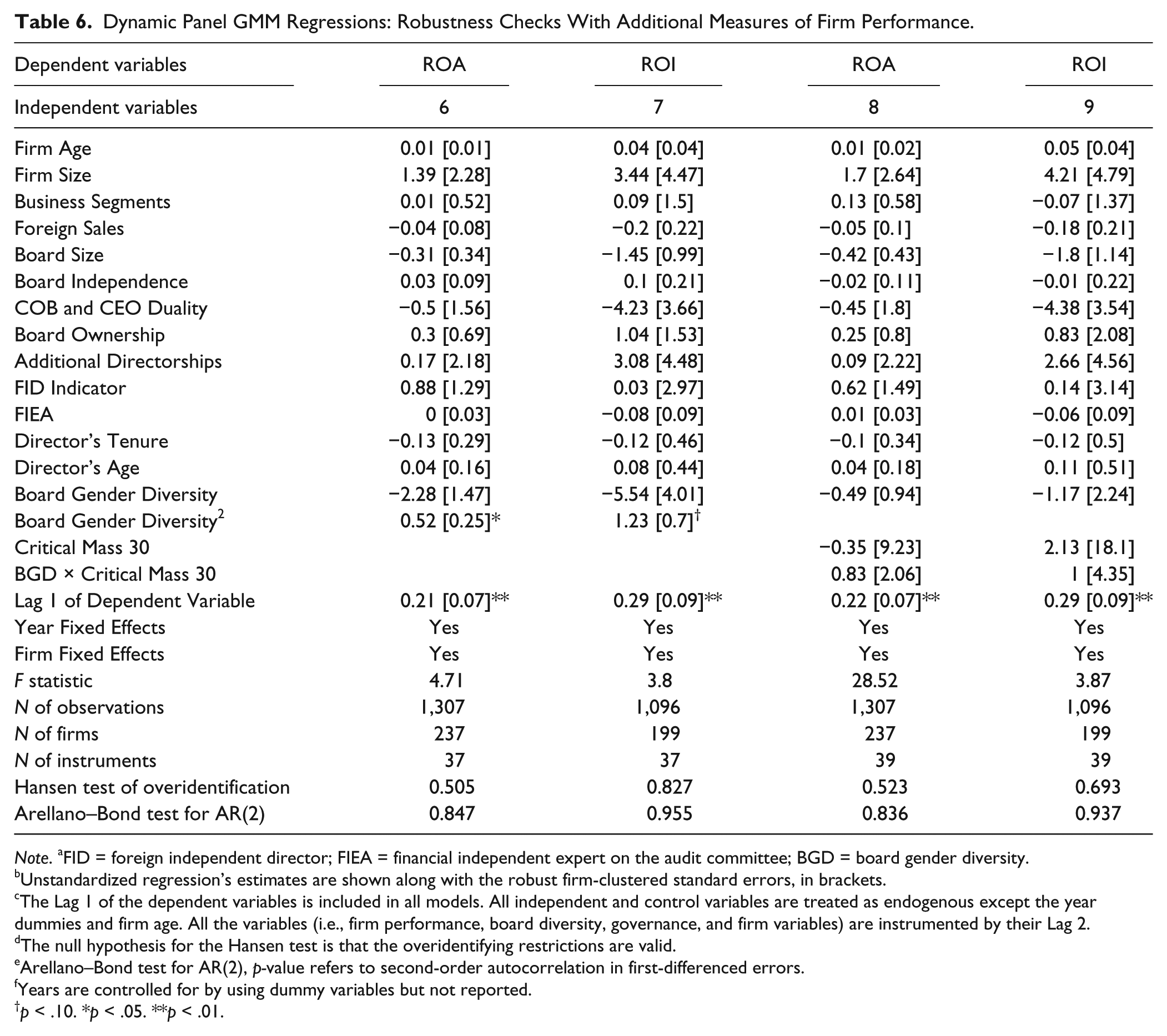

Robustness to Alternative Proxies for Firm Performance

To check the robustness of the estimations reported in Model 1(d) and Model 2(d) of Table 2, we employ two alternative proxies for FP (i.e., ROA and ROI). The results reported in Model 6 and Model 7 of Table 6 show that the square term of BGD is positively related to firm profitability, that is, ROA at the p < .05 level and ROI at the p < .10 level. Therefore, it seems that BGD has a U-shaped effect also on firm profitability, yielding stronger evidence that the U-shaped effect exists (Hypothesis 1).

Dynamic Panel GMM Regressions: Robustness Checks With Additional Measures of Firm Performance.

Note. aFID = foreign independent director; FIEA = financial independent expert on the audit committee; BGD = board gender diversity. bUnstandardized regression’s estimates are shown along with the robust firm-clustered standard errors, in brackets.

cThe Lag 1 of the dependent variables is included in all models. All independent and control variables are treated as endogenous except the year dummies and firm age.

All the variables (i.e., firm performance, board diversity, governance, and firm variables) are instrumented by their Lag 2.

dThe null hypothesis for the Hansen test is that the overidentifying restrictions are valid.

eArellano–Bond test for AR(2), p-value refers to second-order autocorrelation in first-differenced errors.

fYears are controlled for by using dummy variables but not reported.

p < .10. *p < .05. **p < .01.

Again, we used the same proxies of FP to test the robustness of the results obtained for Hypothesis 2. The results reported in Model 8 and Model 9 of Table 6 show that the interaction term of BGD and Critical Mass is positive but insignificantly related to firm profitability, that is, ROA and ROI. Therefore, the findings suggest that a critical mass does not moderate the relationship between BGD and firm profitability and thus do not provide further robustness to Hypothesis 2. This lack of robustness can be explained by the low percentage of boards with 30% or more women (i.e., only 10% of the overall sample), which may make the results vulnerable to causality bias.

Conclusions

This article estimates the curvilinear effect of BGD on FP in the STEM&F sectors in the United States. It makes several contributions to the existing literature as it is the first study that provides empirical evidence of the U-shaped effect of BGD on FP in U.S. firms in the STEM&F sectors. Furthermore, our theoretical framework is complex. It incorporates the positive and negative effects of female directors on the board and discusses how these effects are moderated by the existence of a critical mass. This contributes to the gender diversity debate and provides a better understanding of the fundamental role of a critical mass on corporate boards. Our results stress the importance of reaching a critical mass threshold to facilitate women’s influence on boards. We examined two interesting contextual factors that may affect the representation of WOCBs and their influence on board decisions. The first contextual factor is the time period, that is, 2007 to 2013; and the second is the focus on the STEM&F sectors. The STEM&F sectors require more creative and innovative thinking, thus divergent perspectives, to survive. The time span reflects a period in which there were greater internal and externals pressures to gain more WOCBs.

Our findings show that BGD is beneficial for FP in the STEM&F sectors when there is a critical mass of WOCB. The benefits of gender diversity are found to be subject to the existence of a critical mass, as delineated by the U-shaped significant relationship. Below that critical mass, there are “too few” women in the boardroom to be treated as “in-group” individuals. Once the token level is passed the benefits theorized by the agency and resource dependence literature are unleashed. Above the critical mass point, gender diversity contributes to performance as it increases the heterogeneity of experiences, ideas, beliefs, and attitudes among the board members and encourages the exchange of new information and know-how. Also, it provides unique social and professional connections. Together, these lead to improvements in board dynamics that are likely to have a positive impact on FP. Further analysis of the critical mass suggests that there is a positive moderating effect of critical mass, that is, 30% WOCB, on the BGD–FP relationship. This finding is consistent with the hypothesis that female directors need to be fairly represented at the board level and provides evidence that 30% is a potential “magic ratio” to break through gender barriers, as also suggested by earlier studies (Jia & Zhang, 2013; Joecks et al., 2013; Strydom et al., 2016; Torchia et al., 2011).

Practical Implications

This study has several practical implications regarding WOCBs. While few women are in leadership roles in the STEM sectors, our findings provide an economic rationale to support a critical mass of women (i.e., 30%) in the boardroom in the STEM&F sectors. Specifically, our analysis points to 30% or more WOCBs as the ratio needed to enhance FP. Currently and in the past, the disclosure requirements and the encouragement of voluntary gender targets have facilitated women gaining access to boardrooms. However, most companies are still below the critical mass point. The companies that are slightly below the critical mass point are in the best position to gain an observable advantage on FP. These companies already have the traction to move to the critical mass point. A relatively small investment in gender diversity would bring substantial improvements in FP. In contrast, companies with zero or little diversity (e.g., 0-1 WOBs), would require a considerable investment to break through the “too little” point. Even so, their substantial investment might enable them to experience significant performance improvements. For such companies, more aggressive and customized interventions are necessary to catalyze their move toward reaching the critical mass point and addressing any current casual or deep-rooted gender biases and structural barriers against WOCBs.

Given the sparse evidence of positive results from enforced quotas, the use of additional voluntary and regulatory efforts could provide a better solution to mitigate the dearth of WOCBs. For example, companies could incentivize and provide sponsorships to promote women’s advancement in the senior leadership to board pipeline. Research shows that sponsorship is key to retaining and advancing women within the firm, especially in the STEM sectors (Hewlett & Sherbin, 2014). In this context, the exposure of female managers and professionals to corporate leaders may prepare women in the early and middle of their careers for future board membership, fostering new experiences and facilitating meaningful career trajectories. In addition, to bring more qualified WOBs over the short run, companies could expand their directors’ searches to nontraditional pipelines, for example, government, academia, and nonprofit organizations; and promote the advancement of women into traditional pipelines, for example, CEO and board experiences.

To attract and retain female directors and to alleviate the cultural norm of inequality in the corporate context, companies could promote compensation parity between men and women, thereby signaling their equal value and contribution. Gender differences in salary seem to persist and even to increase on more male-dominated boards (Elkinawy & Stater, 2011). The company’s advancement toward greater diversity should be tracked and monitored through metric systems and integrated into existing or new recognition and award programs both within and outside the organization. These parameters may cause companies to feel higher scrutiny and motivate them to undertake further steps to diversify the board. Finally, improvements in the regulatory requirements such as the December 2009 SEC rule requiring more precise and standardized information on each director (e.g., director’s gender, race, and ethnicity) could enhance transparency and reveal a corporation’s real commitment to diversity at the top. Currently, public companies are only required to disclose certain information on board diversity subject to their own interpretation (U.S. Government Accountability Office, 2015).

Limitations and Future Research

Future studies should continue to empirically explore the effect that female directors have on board processes, dynamics, and behaviors in addition to financial outcomes. Our research evidences “what” matters, that is, that a critical mass of WOBs at and above the 30% threshold matters to FP. Future research might explore “how” a critical mass of WOCBs matters. This requires both using and going beyond the demographic proxies of board diversity to explore heterogeneity across boards of directors in leadership styles (Nielsen & Huse, 2010; Rosener, 1990) and preferences in risk-taking (Adams & Funk, 2012).

In particular, future research might consider exploring more “substantive heterogeneity constructs” such as psychographic differences (Priem, Lyon, & Dess, 1999) of boards as a way to get inside the proverbial black box. This would result in both going beyond the demographic proxies used in our study and expanding on our research. While we have used demographics as one way to study the impact gender on FP, we understand that this may not capture the deeper levels of diversity that require, not only controlling for demographics; but also applying a psychographic approach. For example, this would enable us to gain a greater understanding of “how” differences in psychographics may not only impact FP; but “how” these variances are silenced or promoted in various contexts, that is, when boards are under, at, or above a critical mass. Using qualitative research to explore substantive heterogeneity such as psychographic variances may in fact provide important insights that contradict demographic results (Priem et al., 1999). Nevertheless, gaining clarity regarding the impact of psychographics could potentially provide valuable explanations for demographic-based findings (Priem et al., 1999) concerning WOCBs. Following this, it might result in building a framework for potent, prescriptive recommendations regarding effective board composition vis a vis FP or specific business goals such as innovation.

In addition, an analysis of the female directors’ human and social capital (board capital) could potentially reveal what specific attributes female directors bring to boards and how such attributes enhance board functioning in the context of particular events, environmental circumstances, and firm strategies to add value. Specifically, female directors seem to strengthen the FP of companies that require higher levels of creativity, innovation, and critical thinking. Thus, further context-specific investigations of the relationship between WOCB and FP should take care to select specific environments where gender diversity benefits are fully utilized.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.