Abstract

Top management team (TMT) heterogeneity research has not yet clearly revealed whether surface-level diversity (i.e., national culture, gender, age) contributes to or detracts from a firm’s financial performance and has not focused on how strategic change frequency (number international diversification or refocusing activities) serves as an intervening mechanism. Based on a sample of 1,993 firms between 2003 and 2015, we examine the mediating role of strategic change frequency in the relationship between surface-level diversity and long-term firm performance. Grounded in the upper echelons perspective, we find that TMT surface-level diversity increases rather than decreases strategic change frequency. Furthermore, our results are consistent with our hypothesized positive relationship between strategic change frequency and long-term firm performance. More important, we also find support for a longitudinal-based mediation model in which strategic change frequency in terms of diversification/refocusing actions (Time 2) transmits the positive effect of TMT surface-level diversity (Time 1) to long-term financial performance (Time 3) without accounting for any moderated conditions suggesting that mediation models warrant more utilization in the upper echelons research and internationalization research domains. Implications for the upper echelons theory in a more global world as if relates to the often unexplored surface-level diversity are offered.

Keywords

Introduction

Although workforces are becoming more diverse in terms of dimensions such as national culture, gender, and age, the evidence does not show that such diversity is represented in the upper echelons of corporations as abundantly as it is at lower levels of the hierarchy (Anonymous, 2014; Baxter & Wright, 2000; Zhang & Qu, 2016). For this reason, it appears that we know little about whether companies with more diverse top management teams (TMTs) with more national culture, gender, or age diversity (i.e., heterogeneity) perform differently from those whose management is more homogeneous. Of particular interest would be the frequency of changes in strategy where companies execute strategic change internationally involving diversification and/or refocusing. There has been scholarly work on the relationship between TMT heterogeneity on so-called task-related dimensions such as functional background (Qian, Cao, & Takeuchi, 2013) and also on conditions that moderate such effects (Boone & Hendriks, 2009; Buyl, Boone, Hendriks, & Matthyssens, 2011; Cannella, Park, & Lee, 2008; Carpenter, 2002), but is there any relationship between surface-level diversity and strategic change given the global trend toward more cultural, age, and gender diversity in TMTs?

Organizational behavior scholars and social psychologists who espouse social identity theory might point to the research on work teams. It reveals that surface-level diversity often results in social categorization and tension among team members (Jehn, Northcraft, & Neale, 1999; Tajfel & Turner, 1979; Webber & Donahue, 2001; Williams & O’Reilly, 1998). There is, however, an alternative categorization-elaboration model (CEM) which proposes that diversity promotes information and decision-making advantages through better elaboration of task-relevant information among team members (van Knippenberg, De Dreu, & Homan, 2004). The CEM asserts that surface-level diversity does not always impair performance. Such CEM ideas fit nicely with the upper echelons theory, which emphasizes how diversity in a TMT, even in terms of surface-level attributes, can improve an organization’s effectiveness (Carpenter, 2002; Cooper, Patel, & Thatcher, 2014; Hambrick, 2007; Hambrick & Mason, 1984; Opstrup & Villadsen, 2015; Richard & Shelor, 2002).

This study investigated the following process-based theoretical model which link’s diversity in some surface-level characteristics of the members of a firm’s TMT to long-term firm performance through the frequency of changes in the firm’s strategies. The investigation focused particularly on changes entailing diversification or refocusing.

The model has an action theory component and a conceptual theory component (D. P. MacKinnon, Coxe, & Baraldi, 2012). Action theory links the TMT’s diversity to the frequency of strategic change. The conceptual theory of Figure 1 in fact suggests that more frequent changes in strategy tend to improve a firm’s long-term performance. This is supported by research findings (Amburgey & Miner, 1992; Burgelman & Grove, 2007; Feldman & Pentland, 2003; Klarner & Raisch, 2013). This study differed from prior scholarly work on these topics in that it focused on surface diversity rather than demographics such as functional background that were the subjects of prior research. This is particularly relevant to China today. Although the TMT’s obligations and functions in Chinese firms are similar to those of firms based in the West (Cumming, Leung, & Rui, 2015; Xie, Wang, & Qi, 2015), most upper echelons research has been conducted using U.S. samples (e.g., Dezsö, Ross, & Uribe, 2016; Post & Byron, 2015; Triana, Miller, & Trzebiatowski, 2014). What about China, now the world’s second largest economy? U.S.-based research on upper echelons diversity has generally concluded that the benefits of TMT diversity outweigh its costs (Andrevski, Richard, Shaw, & Ferrier, 2014; Hambrick, Cho, & Chen, 1996). China, though is a more culturally homogeneous, male-dominated setting which may have greater divisions between older and younger employees. These differences from the United States offer an opportunity to examine to what extent TMT diversity matters for firm performance more generally.

A conceptual model linking top management team surface-level diversity to long-term firm performance.

Second, previous upper echelons research has only rarely considered diversification or refocusing. Both can be essential for firms seeking to compete internationally. Firms can gain competitive advantage if they are able to diversify outside of their home countries successfully, but in other cases if they can successfully refocus by moving out of a foreign market. Chinese businesses today frequently face such challenges.

Most research on TMTs, indeed on work teams in general, has sought factors which might reveal under what conditions TMT heterogeneity is most likely to affect a firm’s performance (Carpenter, 2002; Joshi & Roh, 2009; Nielsen & Nielsen, 2013; Roberson, Holmes, & Perry, 2017). That concentration on moderators has provided much insight into the workings of upper management, but identifying mechanisms that might link TMT diversity to firm performance has received less attention (Barrick, Bradley, Kristof-Brown, & Colbert, 2007; Hambrick, 2007; Joshi, Liao, & Roh, 2011; Smith et al., 1994). Indeed, theories linking TMT diversity with performance sometimes appear theoretically unconvincing and sometimes little empirical support has been observed (Hayes, 2009; Rodriquez & Nieto, 2016). A tendency to concentrate on narrow contingency conditions (e.g., munificent environments, service industries) in which TMT diversity can show a positive relationship with performance (e.g., Richard, Murthi, & Ismail, 2007) is unhelpful for the great majority of organizations for which those conditions do not exist. Manufacturers and firms in resource-scarce environments are also potentially affected, but through different routes (Hayes, 2009; Shrout & Bolger, 2002; Zhao, Lynch, & Chen, 2010). Statistical evidence of a process-based relationship even in cases in which no direct relationship between TMT diversity and firm performance can be demonstrated is badly needed (MacKinnon et al., 2012). This study investigated the frequency of strategy changes as a mediating mechanism or linchpin connecting surface-level TMT diversity with long-term firm performance. The model of Figure 1 was tested with 14,035 firm-years observations of 1,933 Chinese firms during the 2003 to 2015 period.

Prior Scholarship and Hypotheses

Action Theory: TMT Surface-Level Diversity and Strategic Change Frequency

Upper echelons theory posits that a firm’s major actions emanate from the decisions of its TMT. The team’s members apply their own filters in interpreting the business environment and make strategic decisions designed to help the firm compete successfully (Hambrick & Mason, 1984). The filtering process involves TMT members using their individual cognitive bases, values, perceptions, and interpretations to formulate and implement strategy. Upper echelons theory rests on the assumption that TMTs have a more powerful impact on strategic choices than any one member, including the chief executive. Strategic choices are a shared activity and a result of iterative information exchange among the TMT’s members (Carpenter & Fredrickson, 2001; Michel & Hambrick, 1992; Murray, 1989). Diverse perspectives in the team then allow for more comprehensive searching considering a variety of strategic alternatives (Eisenhardt & Schoonhoven, 1990; Hambrick, 2007; Pitcher & Smith, 2001; Wiersema & Bantel, 1992). Diversity also confers a broader range of knowledge bases, facilitating thinking “outside the box” (Cooper et al., 2014; Cox, Lobel, & McLeod, 1991; Jackson, 1992; Opstrup & Villadsen, 2015). However, we know very little about how diversity in terms of national culture, gender, and age might influence such decision making. This study investigated the idea that it might affect the frequency of strategy changes, specifically changes related to diversification and/or refocusing (Klarner & Raisch, 2013).

Chinese culture places value on individuals developing strong and enduring interpersonal relationships (guanxi) and avoiding aggressive behavior that could result in unhealthy conflict. That should promote cohesion within Chinese TMTs despite any cultural, gender, or age diversity (Qian et al., 2013; Tjosvold, Poon, & Yu, 2005). Qian et al. (2013) have explained how the unit of opposites in Chinese philosophy stresses cooperation and appreciation of perspectives that differ from one’s own, a presumably useful value in a diverse TMT. In Chinese TMTs, therefore, the disruptive social-categorization processes often said to operate in diverse teams leading to conflict and diminishing cohesion may be less important than elsewhere. That should promote the smoother elaboration of task-relevant information among diverse TMT members (van Knippenberg et al., 2004).

National culture does help explain difference in executive decision making (Crossland & Hambrick, 2011; Elron, 1997; Nielsen & Nielsen, 2013). Work team research conducted by Watson, Kumar, and Michaelsen (1993) has shown that culturally diverse teams over time (if not initially) generate a wider range of creative alternatives than a homogenous team. This result is not surprising, and it might be extended to suggest that an executive’s country of origin influences his or her worldview and interpretation of strategic issues. Nielsen and Nielsen (2013) have proposed that culturally diverse TMTs are more prone to deliberate in depth broad-based ideas, which bolsters creativity and innovation. They have identified in their study more thorough information processing and higher quality decision making as the unmeasured mechanisms linking diverse nationality in a TMT to firm performance. Whether strategic decision-making processes are truly the mechanism that explains such findings has yet to be explored in a rigorous way. This study tested the idea that multiple national cultures in a TMT influences the frequency of strategy shifts related to diversification or refocusing.

As might be expected, gender diversity in the workplace has received more scholarly attention. However, most previous gender research has not investigated TMTs. Findings based on boards of directors (Post & Byron, 2015) or women in general management (Richard, Kirby, & Chadwick, 2013) may or may not be generalizable. Dezsö and Ross (2012) did study gender diversity in TMTs, and they found that it stimulates creativity and improves the quality of decisions. They attributed that to more detailed discussion and broader perspective taking, but they did not study strategy shifts nor their frequency. There is, however, work by Triana et al. (2014) gender diversity in boards of directors that did consider strategy change. Their findings suggest that a more gender-diverse TMT has access to a broader range of information which should spark strategy change when it is needed in a rapidly changing environment. In fact, gender research in general documents that gender diversity results in a wider range of perspectives in information search, more diverse socialization experiences, and more extensive social networks. All of these perspectives should in theory foster greater depth and breadth in strategic decision making (Brennan & McCafferty, 1997; Burgess & Tharenou, 2002; Hillman, Shropshire, & Cannella, 2007; Manolova, Carter, Manev, & Gyoshev, 2007). In fact, Welbourne, Cycyota, and Ferrante (2007) have shown gender diversity in a TMT increases its problem-solving capabilities. It stands to reason that all of these processes should affect the frequency of strategy changes, and the volatile Chinese economy is one setting where such changes may be particularly important.

The empirical results with regard to age diversity in TMTs have been distinctly mixed (Backes-Gellner & Veen, 2013; Cannella et al., 2008; Jackson & Joshi, 2004; Richard & Shelor, 2002). Theoretically, scholars propose that having employees that span generations contributes to creativity and effective decision making (Cox & Blake, 1991). Goll, Sambharya, and Tucci (2001) have shown that age diversity in a TMT is related to more progressive decision making, but Olson, Parayitam, and Twigg (2006) found that it is negatively related to strategic change. So, age diversity should be considered along with national culture and gender diversity as a factor potentially influencing the frequency of strategy changes.

Conceptual Theory: The Mediating Role of Strategic Change Frequency

Strategic change involves reallocating an organization’s assets in a way that is expected to improve its competitive position in the long run (Finkelstein & Hambrick, 1990). Some scholars emphasize that such changes weaken a firm’s current strategic position (Amburgey & Miner, 1992). They do, however, prevent inertia (Burgelman & Grove, 2007; Hannan & Freeman, 1984). Certainly, a firm that is not adapting its strategy to a changing environmental context should expect its performance to deteriorate (Burgelman & Grove, 2007). There is ample evidence that a change in strategy can have a direct and positive association with a firm’s long-term performance (Brown & Eisenhardt, 1997; Galunic & Eisenhardt, 1996; Naranjo-Gil, 2015). Brown and Eisenhardt (1997) also found that firms which prioritize regular communication and design flexibility make more frequent strategy changes. While such changes can disrupt business operations in the short term (Hambrick, Finkelstein, & Mooney, 2005; Klarner & Raisch, 2013), they should benefit a firm in the long term

One of the uncertainties in the findings of upper echelons research is about what processes connect TMT diversity to firm performance (Hambrick, 2007). Figure 1 proposes the frequency of strategy change for this role. Action theory proposes that TMT diversity increases the frequency of strategy change, the proximal mediator. Conceptual theory proposes a positive relationship between change frequency and long-term performance (McDougall & Oviatt, 1996; Zajac, Kraatz, & Bresser, 2000; Zhang & Rajagopalan, 2010). A TMT’s major goal is improving firm performance, and the frequency of strategy changes is an important proximal mediator. That is why diversity in a TMT’s surface-level characteristics may predict long-term firm performance indirectly through the frequency of strategy changes. Figure 1 is thus an action and conceptual theory mediation model.

Method

Data

These ideas were tested using data panel data covering Chinese publicly listed firms from multiple sources. The firms were listed on either the Shanghai or Shenzhen stock exchange (or both). Their TMTs’ demographic characteristics during the 2003 to 2015 period were extracted from the database published by China Stock Market and Accounting Research (CSMAR), specifically the Corporate Governance Database component. CSMAR is considered a reliable data provider focusing on Chinese companies which are publicly listed. TMT membership was defined as the CEO and those managers that report to him (very rarely her) directly. On average, the TMTs had six members.

The CSMAR database provided information on each firm’s return on equity (ROE), return on assets (ROA), number of employees, domestic or foreign ownership, and state ownership annually. The firm’s annual reports for 2003 to 2015 were also studied (Piperopoulos, Wu, & Wang, 2018; Wu, Wang, Hong, Piperopoulos, & Zhuo, 2016). ROA and ROE were calculated over one-, two- and three-year periods, which were adjusted (normalized) by the industry average. Those calculations limited the applicability of the last 2 years of the data.

Data on the frequency of strategy change were extracted from the annual reports using a predefined coding developed by Klarner and Raisch (2013). Changes in the scope of a firm’s operations were considered as changes in strategy. Changes involving diversification or refocusing were enumerated (Wischnevsky, 2004).

Industry munificent and industry dynamism were also quantified. Each industry’s gross output was extracted from published statistics. We then matched different databases based on unique stock-code identifiers.

The final sample was an unbalanced panel (due to some firms entering after 2010) covering 1,933 firms and 14,035 firm-year observations. On average, each firm contributed seven observations.

Measures

The industry-adjusted ROE was the dependent variable in the analyses. It indicates to what extent a company used its resources efficiently (Keck & Tushman, 1993; Wischnevsky, 2004). It was calculated as net income divided by average equity over the year (Keck & Tushman, 1993). Adjusting for industry effects involved subtracting average industry ROE from the firm’s ROE in the same year (Tushman & Rosenkopf, 1996; Virany, Tushman, & Romanelli, 1992). The average industry ROEs were computed as the annual mean ROE of all the companies in the sample operating in the same industry (Klarner & Raisch, 2013).

Even though single changes in strategy usually penalize short-term performance, the study’s emphasis was on the accumulated, long-term performance effect of an entire set of repeated strategy changes. As in previous studies, performance was measured 2 years from the end of each change period (Klarner & Raisch, 2013). Since the analysis covered strategy changes initiated between 2003 and 2013, long-term performance was measured for 2005 to 2015.

Mediator

To derive change-event sequences for each firm, we coded strategic changes from the annual reports. Changes in corporate strategy were defined in terms of changes in a firm’s scope of operations and examined along the diversification-refocusing dimension (Wischnevsky, 2004). A diversification event was coded if a company had entered a new country or a new business segment; a refocusing event was coded if a company departed from a country or a business segment (Klarner & Raisch, 2013; Vermeulen & Barkema, 2001; Webb & Pettigrew, 1999). Change frequency was the total number of such changes within a year. A natural logarithm transformation was applied to normalize the original, skewed distribution (Waller, Huber, & Glick, 1995). The average frequency was 0.93 with a minimum of 0 (as one would expect) and a maximum of 3. To deal with the incidence 0s, 1 was added to the frequencies before taking the logarithm.

Independent Variables

The independent variables were TMT national culture diversity, TMT gender diversity, and TMT age diversity. The national culture variable was assigned based on an analysis of each firm’s annual report (Nielsen & Nielsen, 2013). In China, listed firms are required to include the nationalities of their top executives in their annual reports. There were 19 national cultures represented in the data set: China, Japan, South Korea, Australia, Germany, Canada, Belgium, France, the United Kingdom, India, Italy, Hong Kong, Taiwan, 1 Malaysia, New Zealand, Singapore, Turkey, Ukraine, and the United States. Following the lead of prior studies (Zenger & Lawrence, 1989), Blau’s index of heterogeneity (Blau, 1977) was used to quantify TMT cultural diversity. Specifically, Β = [1 − Ʃ(p i )2], where p i is the percentage of members with the ith nationality. Blau’s index was computed to quantify TMT gender diversity in the same way. The Βs were very small, as TMTs with more than one non-Chinese or more than one woman were rare. As in prior studies on TMT age diversity (Nielsen & Nielsen, 2013), it was quantified with a coefficient of variation.

Several sets of control variables were also considered in the analyses. Change magnitude distinguished large from small-scale changes (Amburgey & Dacin, 1994). A large-scale change was one which affected more than 5% of a firm’s turnover (typically exiting a market). The data were obtained from the firms’ annual reports—segment reporting, notable events, and notes—as well as from the news and deals sections of the Thomson One Bankers database. The change magnitude variable was the number of large-scale changes between 2003 and 2013 divided by the total number of changes in that period. A change mode variable distinguished acquisitions from internal development, since research reveals that acquisitions almost always affect performance (Karim & Mitchell, 2000; Laamanen & Keil, 2008) and internal development is difficult to track. The value of change mode was the total number of a firm’s acquisitions between 2003 and 2013 divided by the total number of its strategic changes during that period. The change median variable was another control. It represented the fact that more recent changes may have a stronger effect on performance than earlier ones. Change median was the median year of each firm’s changes during the period from 2003 to 2013. Higher values indicated an accelerating pace of strategy changes (the changes were back loaded) (Klarner & Raisch, 2013).

Firm size was the logarithm of the number of a firm’s employees, as size presumably influences the impact of strategy changes (Jayaraman, Khorana, Nelling, & Covin, 2000). Firm age was the number of years since a firm’s inception, often found in previous studies to affect performance (Barron, West, & Hannan, 1994). Debt ratio was another control, measured as total long- and short-term debt as a percentage of total capital. Sales growth was the percentage increase or decrease over the entire period studied (Klarner & Raisch, 2013). In China, ownership structure seriously affects firm performance (Wu, 2011), so two ownership controls were included representing foreign ownership and state ownership. Foreign ownership was foreign-owned equity capital as a proportion of total capital. State ownership was state-owned equity as a proportion of total capital.

The extent to which an industry’s environment can support sustained growth would be expected to affect the frequency of strategy changes (Dess & Beard, 1984). To take account of this, industry munificence was another control variable. It was the coefficient of a regression of each industry’s annual average sales against time divided by the mean value of a firm’s sales during the study period. In addition, firms competing in more dynamic industries will be more likely to segment homogeneous elements of their environments (Simon & March, 1958). Industry dynamism was quantified using the standard error of the slope coefficient of a plot of industry sales against time divided by the mean value of industry sales (Dess & Beard, 1984; Keats & Hitt, 1988).

Another control was TMT average tenure, computed using data from the annual reports. TMT average education level was quantified by assigning a value of 1 for each TMT member with only a primary school education (approximately 6 years), a 2 for each member completing primary school but not high school (approximately 9 years), a 3 for completing high school or technical school, 4 for a bachelor degree, 5 for a master’s, and 6 for a PhD. The TMT functional background diversity variable was computed similarly by assigning a 1 for each member with a finance background, 2 for engineering, 3 for law, 4 for human resources (a role often assigned to otherwise unqualified Communist Party Secretaries in Chinese firms), 5 for a marketing background, 6 for operations management, and 7 for production. A Blau index was computed to quantify a TMT functional background diversity value for each firm. Year and industry dummy variables were also defined. Seventeen industries were represented in the data. Given that the sampled firms are from 17 industries ranging from chemical Industry (C26), pharmaceutical industry (C27), and equipment manufacturing industry (C34), and so on, we included a set of industry dummy variables to control industry effects.

Modeling

The data constituted a panel of firm-year observations. Fixed- and random-effects models are the formulations most commonly used to control for unobserved effects and partially alleviate endogeneity concerns. This study’s basic model was of the form

Omitted variables such as government policy changes or economic downturns may also affect strategic change decisions and firm performance (Certo & Semadeni, 2006). The time dummy variables in the models with a large number of firms and short time periods helps reduce such extraneous correlation (Certo & Semadeni, 2006). Using the random-effects formulation also helps deal with any omitted variables (Baltagi, 2013).

Change frequency would be expected to affect TMT diversity. An acquisition, for example, might add TMT members who differ from the current cohort in various ways. To help overcome such circumstances, all the explanatory variables were lagged to help account for any reverse causality. In testing for a relationship between TMT diversity and change frequency, the three diversity variables and the control variables at year t were regressed against the dependent variable, change frequency, in year t + 1. In testing for mediation, ROE in year t was related to change frequency at t − 1 and the independent and control variables at t − 2.

Endogeneity arises when the true values of the independent variables are not observed (errors), a variable which correlates with both the outcome and one or more of the explanatory variables is not included in the model, or the dependent variable causes the values of the independent variables. Because the explanatory variables came from annual reports or the CSMAR’s Corporate Governance Database, the errors-in-variables issue would appear to be not too serious. Also, the models controlled for several alternative explanations, so omitted variable bias may have been avoided. Nevertheless, the models could potentially suffer from simultaneous causality.

Cooper et al.’s (2014) approach was applied in assessing the endogeneity of the TMT diversity measures. A Durbin–Wu–Hausman test was conducted using the xtivreg2 routine in the STATA software suite. The null hypothesis predicted that the measures would appear exogenous. Nonsignificant chi-square statistics in the Durbin–Wu–Hausman test would suggest that the three TMT diversity measures are exogenous and that their unbiased estimates can be reported. In the analyses, the null hypothesis could not be rejected (F-test: χ2 = 0.312, p = 0.65), suggesting that the three TMT diversity measures are exogenous. In addition, two instrumental variables were included to further address endogeneity concerns. Prior studies have suggested that the percentage of institutional ownership is a good instrumental variable for TMT diversity (Cooper et al., 2014) as it is correlated with diversity but has little impact on firm-level outcomes.

Results

Table 1 presents statistics describing the variables and their intercorrelations. The maximum variance inflation factor was 1.97, and the minimum was 1.02, with a mean variance inflation factor of 1.26. In addition, an examination of the correlations shows that multicollinearity was not a notable problem.

Correlation Matrix, Means, and Standard Deviations.

Note. ROE = return on equity; TMT = top management team. n = 14,035. Industry and year are omitted. Numbers with an absolute value >.0156 are significant at the 95% level of confidence.

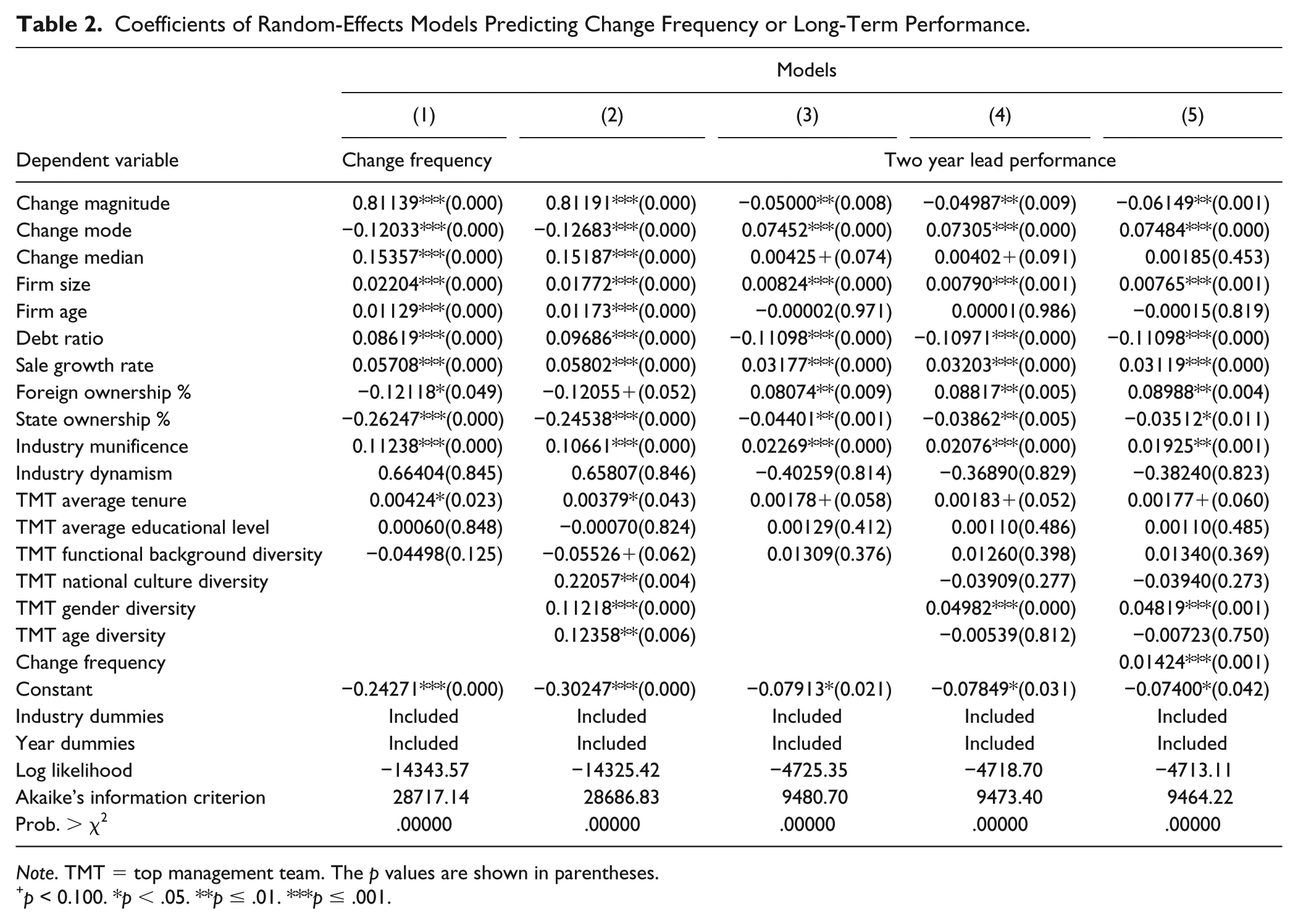

Table 2 reports the results test Hypothesis 1. Model 1 includes only the control variables to show their relationship alone on change frequency. Model 2 also includes the three TMT diversity measures. Models 3 through 5 predict two-year-lagged and industry-adjusted ROE rather than change frequency. Model 3 uses just the control variables. Model 4 uses the control variables plus the three TMT diversity measures. Model 5 adds change frequency as a mediator.

Coefficients of Random-Effects Models Predicting Change Frequency or Long-Term Performance.

Note. TMT = top management team. The p values are shown in parentheses.

+p < 0.100. *p < .05. **p ≤ .01. ***p ≤ .001.

Hypothesis 1 predicts that TMT cultural, gender, and age diversity are all positively related to the frequency of strategy change. In Model 2 of Table 2, the coefficients of all three diversity terms are positive and statistically significant, culture and age at the 1% level of confidence and gender at the 0.1% level. These results support Hypothesis 1.

Hypothesis 2 proposes that more frequent strategy changes predict better long-term performance. In Model 5, the coefficient of the strategic change frequency term is positive and significant, supporting Hypothesis 2.

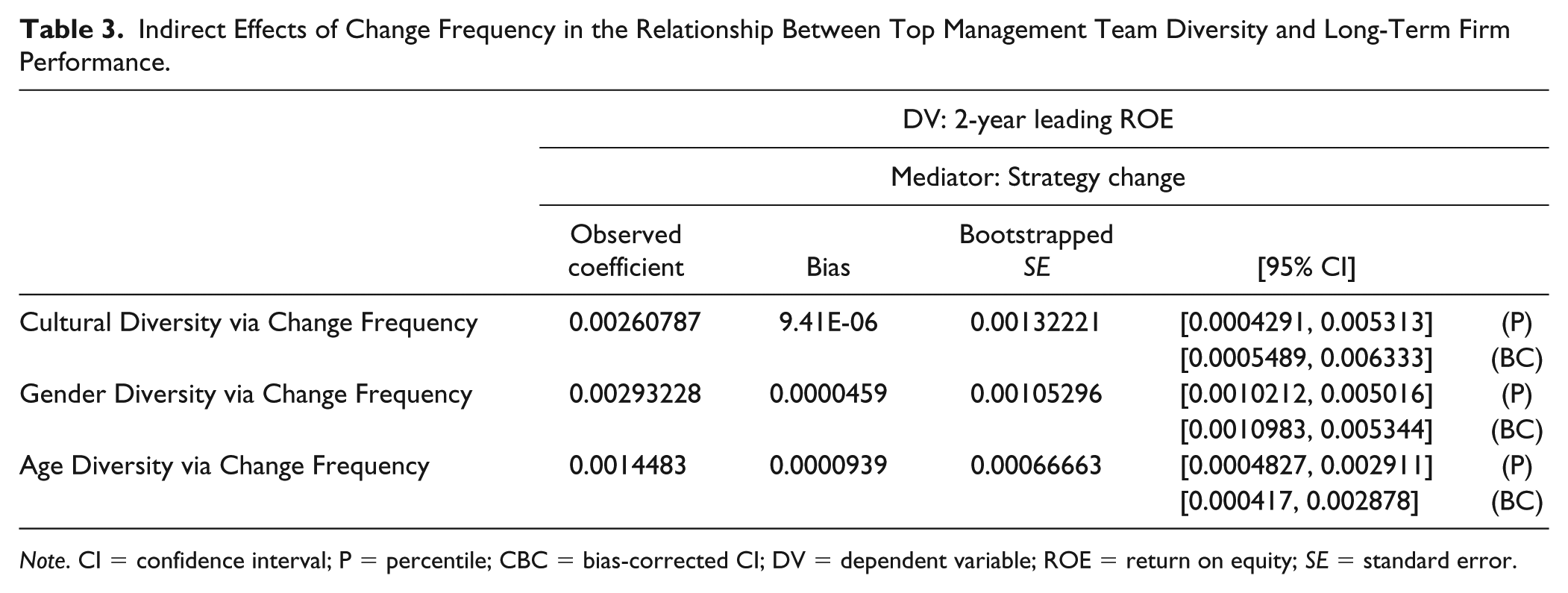

Hypothesis 3 proposes that the frequency of strategy changes mediates in the demonstrated relationships between the TMT diversity variables and long-term firm performance. Model 5 in Table 2 does reveal that change frequency positively predicts ROE. Table 3 reports the results for all three of the TMT diversity measures. Based on 1,000 bootstrapped samples using a 95% percentile confidence interval, all three diversity measures show evidence of mediating in the relationship between change frequency and ROE. So Hypothesis 3 is also supported.

Indirect Effects of Change Frequency in the Relationship Between Top Management Team Diversity and Long-Term Firm Performance.

Note. CI = confidence interval; P = percentile; CBC = bias-corrected CI; DV = dependent variable; ROE = return on equity; SE = standard error.

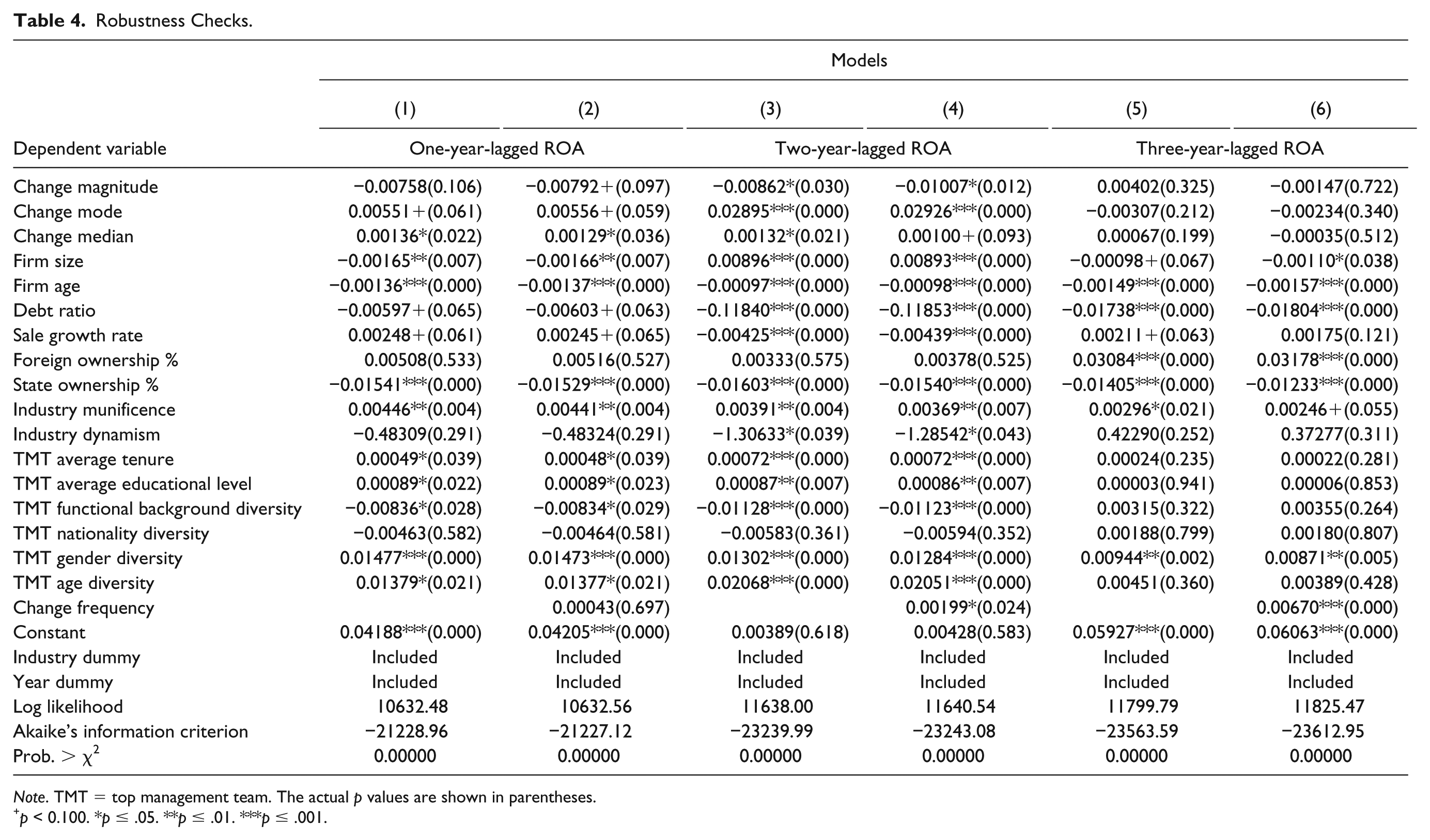

To check the robustness of these results, ROA replaced ROE as the performance measure. One-year-lagged, two-year-lagged, and three-year-lagged industry-adjusted ROA were tested, with the results reported in Table 4. The alternative financial performance measure did not change the results materially. Nor did the different lag periods. Three-year industry-adjusted ROE was also tested, but the results again were not substantially altered (albeit weaker due to the loss of observations). These findings support strong predictive validity for the hypothesized effects.

Robustness Checks.

Note. TMT = top management team. The actual p values are shown in parentheses.

+p < 0.100. *p ≤ .05. **p ≤ .01. ***p ≤ .001.

The fact that the three TMT diversity measures are moderately correlated with functional background diversity (γ = 0.10) could violate the assumption that the explanatory variables are independent of each other. To resolve this concern, the analyses were rerun excluding the functional background variable. The results remained consistent with those reported in Table 2.

Another robustness test involved reconfiguring the national culture categories by classifying Hong Kong and Taiwanese managers as Chinese. That reduced the number of categories to 17. The analyses were rerun with the TMT national culture diversity quantified on that basis and the results were again highly consistent with those using 19 categories. Using continents rather than economies, however, generated no significant relationship. The original TMT national culture diversity measure which distinguished China from Hong Kong and Taiwan had the best predictive power.

Discussion

Given the trend toward more internationalization of companies into new markets away from simply operating in domestic markets as well as refocusing by retreating from some foreign markets, Nielsen and Nielsen (2013) called for research to explore to what extent and in what way diversity among a TMT’s nationalities influences firm performance. That was explored in this study along with gender and age diversity. Their relationship with the frequency of diversifications and withdrawals was investigated along with their relationship with long-term performance. The aim was to place diversity squarely within the ambit of upper echelons studies and reveal any associated predictive power. That extends the field beyond consideration of the functional backgrounds normally studied.

The findings show that the frequency of strategy changes acts as a mediator linking all three types of diversity studied to firm performance. But without that mediator neither national culture nor age diversity usefully predicts firm performance. This exemplifies the advantage of using a process model to detect relationships when no main effects are significant and theory suggests no moderating factors (Hayes, 2009). Thus, we hope the action and conceptual theory framework used in this study find its way into more international business, strategic management, upper echelons, and workforce diversity research.

Theoretical Implications

From a theoretical perspective, there is a need to open a “black box” within upper echelons theory (Hambrick & Mason, 1984) and more fully explain the how diversity contributes to or detracts from firm performance. This study made some progress in that direction using surface-level diversity descriptors, but a need remains to explore deeper, less salient diversity dimensions. Surface-level diversity has been at center stage recently (Dezsö & Ross, 2012; Nielsen & Nielsen, 2013; Nishii, 2013; Triana et al., 2014).

The finding that surface-level diversity in a TMT relates to long-term firm performance through the frequency of strategy change as a mediating mechanism has important theoretical implications. It suggests that attention should be paid to the “how” as well as the “when” in moderation research. In fact, those seeking contingencies which determine when diversity matters should adopt this study’s approach because, at least for cultural and age diversity in a TMT, the frequency of strategy shifts reveals not only how diversity affects firm performance but also when. Indeed, only when change frequency is included in the action and conceptual theory model were any significant effects observed. This is an observation important for future research in which mediating linkages might exist but main effects do not. As the saying goes, “There is more than one way to skin a cat.” When no main effect is evident, an alternative to finding a moderator that reveals a narrow condition in which an effect emerges is to identify a proximal mediator that forcefully links a study’s predictor and predicted variables.

Decades ago, Hambrick and Mason (1984) showed the influence of managers’ ages, organizational tenure, functional backgrounds, education levels, and socioeconomic status on firm outcomes. This study supports and extends their findings to national culture and gender. Both usefully predict the frequency of strategic changes and subsequent firm performance. This more process-oriented approach aligns with the original theory, since TMT characteristics influence a firm’s outcomes, including changes in strategy and of course performance. This study’s findings extend upper echelons theory by taking a finer-grained approach to explaining how characteristics of a firm’s TMT affect its long-term firm performance as depicted in Figure 1’s action and conceptual theory model.

The study focused exclusively on surface-level diversity dimensions of national culture, gender, and age diversity because of lack of published research on how these relate to strategic decision making and performance (Cox & Blake, 1991; Menz, 2012; Richard & Shelor, 2002; Williams & O’Reilly, 1998). Not surprisingly, scholars have described surface-level diversity as a double-edged sword whose positive effects are often offset by negatives (Milliken & Martins, 1996). The findings here support the information and decision-making perspective and reveal that elaboration of task-relevant information likely outweighs any negative social categorization (van Knippenberg et al., 2004).

Limitations and Future Research Directions

Future research might fruitfully consider other proximal mediating mechanisms linking TMT diversity to firm performance (Phelps, Heidl, & Wadhwa, 2012). For example, Andrevski et al. (2014) have shown that the intensity of a firm’s competitive activity mediates in relationships between management diversity (at all levels) and firm performance. Other process variables such as elaboration of task-relevant information and innovations seem promising as other mediating mechanisms (Miller & Del Carmen Triana, 2009).

In addition, although this study did not account for contingency factors, research should continue to consider moderating factors. For example, one could consider whether or not properties of social networks (such as holes, network tie strength, network tie diversity, network partner diversity) might be potential moderators of the observed TMT diversity–change frequency relationship (Phelps et al., 2012). Beyond that, board composition might be another moderator to consider in the same way (Miller & Del Carmen Triana, 2009). For example, would it be more effective if the TMT’s diversity (or lack of it) mirrored that of the board of directors? Or should they complement one another by having contrasting demographic makeup?

Personnel management systems, specifically diversity management practices, might be an important component to include in future research exploring diversity’s effects. For example, systems that include participative job arrangements and promote empowerment foster an environment of collaboration, inclusiveness, and sharing of information (Nishii, 2013; Richard et al., 2013; van Knippenberg & Schippers, 2007) should be particularly useful for effective interactions within a diverse TMT. Nishii (2013) has shown that an inclusive climate reduces the social categorization often associated with diversity. Such a climate might also positively moderate the observed relationships between TMT diversity and the frequency of strategy changes. Future research should also consider second-stage moderation within a moderated mediation framework (Edwards & Lambert, 2007).

And of course, these findings need to be extended to other societies and their economies. China is in many respects and outlier both socially and economically. Some have suggested that executives have more discretion without a party secretary acceding to all their decisions. Surface-level diversity might then exert even stronger predictive power. Scholars pursuing this line of enquiry might usefully embed power distance, collectivist predilections, and other cultural dimensions when crafting their hypotheses (Rabl, Jayasinghe, Gerhart, & Kühlmann, 2014). This study used a large sample of China firms, but its findings may nevertheless be culture specific.

These findings nevertheless make an important contribution to international business scholarship by revealing the importance of cultural diversity in a firm’s TMT. They certainly have important implications for companies headquartered in China but seeking global competitiveness. Beyond task-related dimensions of diversity such as functional background, competitive advantage is also to be had from seemingly superficial factors such as diversity in national culture, gender, and age. Such factors deserve more scholarly attention.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.