Abstract

This study focuses on a two-stage hybrid framework for dynamic portfolio optimization. While existing two-stage approaches often rely mainly on price data, symmetric downside measures, or static allocation, they provide limited insight into fundamental efficiency and how assets behave during severe market downturns. In the first stage, Data Envelopment Analysis (DEA) is used to pre-select efficient stocks based on fundamental financial indicators. In the second stage, several risk-based allocation strategies are applied to the selected assets, including mean-standard deviation, semi-deviation, conditional value at risk, maximum Sharpe ratio, and a proposed mean-asymmetric downside risk model. This proposed model introduces an exponential penalty function to emphasize larger losses and better capture downside risk during market downturns. Portfolio performance is evaluated using a rolling-window approach with weekly rebalancing over a 65-week out-of-sample period. The DEA-based selection effectively reduced the investment universe from 36 to 9 efficient stocks. Empirical results show that the simple DEA+1/N portfolio outperformed the SET50 benchmark, and the proposed DEA+mAsymRisk delivered higher returns with lower downside risk compared to alternative strategies. These findings highlight that combining fundamental screening with downside-sensitive allocation strengthens portfolio robustness and offers practical value for dynamic risk management in financial markets.

Keywords

Introduction

Portfolio management is a study of selecting and managing a combination of financial assets to meet specific investment goals while managing risk (Reilly, 2002). Two essential components of portfolio management are portfolio selection and optimization. The former concerns choosing a diversified set of assets based on investor preferences, while the latter focuses on allocating weights to these assets in a manner that balances return and risk. The classical mean-variance (MV) model introduced by Markowitz has long served as the foundational framework for portfolio management, where variance is used as a measure of risk and expected return as a proxy for performance (Kolm et al., 2014).

Despite its strengths and popularity among researchers and practitioners, the MV model has known limitations. In practice, investment decisions often depend not only on historical return data but also on the fundamental characteristics of firms, such as profitability, leverage, and earnings stability (Peykani et al., 2020; Zhang, 2024). To better capture such multidimensional information, researchers have explored combining optimization models with multiple-criteria decision-making (MCDM) techniques (Hallerbach & Spronk, 2002).

Among these, Data Envelopment Analysis (DEA) has demonstrated effectiveness as a non-parametric method for evaluating the relative efficiency of assets based on multiple inputs and outputs (Charnes et al., 1978). Arasu et al. (2021) successfully applied the DEA model to the Indian stock exchange to identify high-performing stocks based on financial ratios and performance indicators. Similarly, Siew et al. (2017) conducted an empirical investigation on the efficiency of financial companies in Malaysia using the DEA model from 2010 to 2015, identifying nine companies as efficient based on their optimal control of inputs to generate maximum outputs. Expanding on these applications, Safari et al. (2024) integrated DEA with Recurrent Neural Networks (RNNs) in the Thai stock market. This ensemble model combined DEA’s ability to filter stocks based on fundamental ratios with RNNs’ predictive power for stock prices, enhancing decision-making.

Certain studies have extended the application of DEA beyond just serving as an efficiency measurement instrument. They have incorporated it into portfolio optimization models to address dimensionality reduction issues and facilitate asset selection based on multiple performance criteria. Hosseinzadeh et al. (2023) proposed a DEA-based framework that evaluates assets using a broad set of market-derived risk and return indicators, and applied three portfolio optimization models, all built around Markov Scenario Generation performance ratios. Their approach performs well on large datasets. However, it relies mainly on price data and ignores firm-level information and parameter uncertainty, which can reduce robustness in dynamic markets. This observation aligns with prior research (Brandt et al., 2009; Hand & Green, 2011; Lyle & Yohn, 2021), which demonstrates that combining fundamental characteristics with market data can enhance portfolio performance in parametric optimization frameworks.

Peykani et al. (2020) proposed a robust two-phase model has been introduced that combines DEA with robust mean-risk-liquidity optimization techniques. Although this model improves resilience under uncertain data conditions and integrates financial ratios, it applies static optimization and lacks mechanisms for dynamic portfolio adjustment over time. Rotela Rotela Junior et al. (2017) combined DEA with entropy-based diversification within a simplified Sharpe optimization framework. While this approach introduces diversification benefits, it limited input-output selection to earnings per share (EPS) and price-to-earnings (P/E) ratio, assumes no asset correlation, and does not consider portfolio rebalancing. Similarly, Pätäri et al. (2012) combined DEA with value and momentum investing by forming three quantile-based portfolios according to DEA efficiency scores and assigning equal weights to the selected assets. However, their approach relied on a fixed, equal-weighting strategy without incorporating any rebalancing over time.

Building on existing two-stage portfolio frameworks, this study proposes a dynamic hybrid approach that integrates firm-level asset selection with downside-sensitive allocation. In the first stage, DEA is used to screen efficient stocks using a diverse set of fundamental indicators, including profitability, liquidity, and operational performance, to reflect intrinsic financial strength rather than just historical returns. In the second stage, selected assets are passed through multiple allocation strategies, including equal-weighting (

Tail-risk models such as CVaR and semi-deviation have been widely used in portfolio optimization to better capture downside risk exposure (Ghanbari et al., 2023; Rockafellar & Uryasev, 2000). These models aim to address the limitations of variance-based measures by focusing on extreme losses. However, they often apply symmetric or linear penalization. Building on this foundation, we introduce the mAsymRisk model, which incorporates an exponential penalty for large losses and a downside covariance matrix to better reflect co-movement during market downturns.

Furthermore, unlike previous studies that assume static weights or simplified assumptions, this study applies weekly rebalancing over a 65-week out-of-sample period, enabling the evaluation of model robustness under realistic, volatile market dynamics. The framework is empirically validated on the Thai stock market, offering insights from an emerging market context where volatility and risk asymmetry might be more pronounced.

The paper is organized as follows. The Methodology section outlines the approach used, including the DEA model for stock selection and the portfolio optimization strategies. The next section presents the empirical results and evaluates the performance of the proposed models. Finally, the last section offers concluding remarks, discusses key findings and their implications, and suggests directions for future research.

Methodody

This section breaks down the two-stage hybrid approach to dynamic portfolio optimization proposed in this study. The first stage involves the use of the DEA method for efficient asset preselection, while the second stage focuses on portfolio optimization using various risk measures, including our proposed mAsymRisk model. We then describe the performance evaluation metrics and the dynamic rebalancing strategy employed in our empirical analysis.

Data Envelopment Analysis

Data Envelopment Analysis (DEA), initially introduced by Charnes et al. (1978), is a nonparametric method for evaluating the efficiency of Decision-Making Units (DMUs) with similar inputs and outputs. Building on Farrell’s efficiency concept (Farrell, 1957), the initial DEA model, referred to as the CCR model. It assumes constant returns to scale (CRS), meaning that proportional increases in inputs lead to the same proportional increases in outputs. Later, Banker et al. (1984) extended the CCR framework and proposed the BCC model. This model assumes variable returns to scale (VRS), allowing efficiency to change with the scale of operations, where input–output proportions may increase or decrease at different rates.

In this study, each DMU represents an individual stock, with firm-level financial indicators used as inputs and outputs to evaluate their relative efficiency. The inputs employed to assess stock efficiency are:

The financial indicators considered as outputs in this study are as follows:

DEA models are generally categorized as input-oriented or output-oriented: the input-oriented model minimizes the level of inputs needed to produce a given output, whereas the output-oriented model maximizes outputs given fixed inputs. In this study, both the input-oriented CCR and input-oriented BCC models are applied, as presented below.

These models employ standard linear programming techniques for DMUs by optimizing input and output weights to maximize each DMU’s efficiency score (Camanho & D’Inverno, 2023). The efficiency score is calculated as the weighted sum of outputs relative to the weighted sum of inputs. A score of one is considered to be efficient, while a score below one indicates inefficiency. In this study, the CCR and BCC models provide valuable insights into how various fundamental metrics influence a stock’s overall efficiency. The weights derived from these models are crucial for refining each DMU’s efficiency assessment. However, in line with our research objective, we focus solely on the final stock scores rather than the metric weights, as our primary goal is to identify the most qualified stocks in the portfolio optimization stage. Therefore, we retained only frontier units—stocks with an efficiency score = 1.00 in both CCR and BCC for the allocation stage, which yielded 9 stocks.

Portfolio Optmization Models

The mean-standard deviation model (Markowitz, 1952) aims to minimize the portfolio risk

The mean-semi-deviation model (Ang et al., 2006) aims to minimize the portfolio’s semi-volatility

The mean-conditional value at risk (mCVaR) model aims to minimize potential losses in the worst-case scenarios by measuring the expected loss given that it exceeds a specified value at risk (VaR) threshold (Rockafellar & Uryasev, 2000). The mCVaR model is defined as:

The maximum Sharpe ratio (maxSharpe) model (Sharpe, 1994) aims to maximize the portfolio’s Sharpe ratio, which is the ratio of the portfolio’s excess return to its total risk. The maxSharpe model seeks the optimal balance between return and risk to obtain the highest possible reward per unit of risk. It is expressed in a typical single-objective optimization as follows:

All portfolio optimization models and performance evaluations were conducted using our custom-developed CMU library, which implements the Sequential Least Squares Programming (SLSQP) algorithm for consistent constraint handling across all risk measures.

1

The library ensures reproducible results through standardized parameter settings: target return

In this section, we propose mean-asymmetric downside risk (mAsymRisk) which minimizes portfolio risk by emphasizing the severity and co-movement of losses during adverse periods. Unlike standard risk models such as mean-variance or mCVaR, which either use unconditional variance or treat all losses above a threshold equally, mAsymRisk focuses on two key aspects:

The correlation structure of asset returns during market downturns, and The asymmetry in loss magnitude, where larger losses are penalized more severely.

In addition, two main elements for measuring the risk are considered:

Combining these two risk measurements, the optimization problem can be defined as:

By integrating both

To obtain an optimal solution of eqs. (13) and (14), we apply Lagrange multipliers. Firstly we reformulate the objective function as Stationarity condition:

Primal feasibility: the optimal solution Dual feasibility: the Lagrange multipliers for the inequality constraints, that is, Complementary slackness: each inequality constrain satisfies complementary slackness, that is,

Note that the full analytical solution is non-trivial because of the complementary slackness conditions for the non-negativity constraints. In this case, we use numerical optimization algorithms, that is, interior-point methods, which are designed specifically to find the optimal solution

The proposed measure conditions on downturn returns and explicitly models joint extreme losses. Mean–variance uses the unconditional covariance of returns and penalizes upside and downside symmetrically; semi-deviation is a linear lower-partial variance that does not magnify very large negatives; and CVaR summarizes the average tail loss beyond VaR without modelling cross-asset co-movement. The mAsymRisk instead conditions on market downturns and augments risk with

Several risk and return metrics were employed to evaluate the performance of these portfolio optimization models. The annualized return measures the geometric average return of the portfolio, assuming that returns are compounded. The formula for annualized return is defined as follows:

Annualized volatility represents the total risk of the portfolio, scaled to an annual timeframe. The formula adjusts the standard deviation of periodic returns to account for the number of periods in a year:

Maximum drawdown (MDD) measures the largest peak-to-trough decline in the value of a portfolio over a given time period. The MDD captures the maximum observed loss from a historical high to the lowest point before a subsequent recovery:

Conditional Value at Risk (CVaR), also known as Expected Shortfall, measures the expected portfolio loss conditional on losses exceeding the Value at Risk (VaR) at a given confidence level

The Sharpe ratio evaluates excess return per unit of total risk and is defined as:

The Sortino ratio refines the Sharpe ratio by considering only downside risk instead of total volatility:

Finally, the Information ratio (IR) measures portfolio return relative to its total volatility, providing another indicator of the risk-return trade-off:

In this section, we present the results of the proposed two-stage hybrid approach to dynamic portfolio optimization. In the following subsections, we will first present the results of the initial stage, which involves using the DEA method for selecting the top

Case Study and Datasets

This study focuses on the Stock Exchange of Thailand (SET), particularly the SET 50 index 2 . As of January 2024, the SET has a capitalization of over $1.2 billion. Foreign investment accounted for 30.50% of total market capitalization as of August 2023, highlighting SET’s significance as a leading equity market within ASEAN and one of the top emerging markets in the world.

For the DEA method, we considered stocks that were part of the SET 50 index before 2017 and excluded stocks in the financial sector due to missing inventory ratio data in their financial reports. Thus, we collected fundamental data from 36 companies from the first quarter of 2017 to the third quarter of 2022.

Regarding the portfolio optimization stage, there are several options for the frequency of price data, including high-frequency data such as hourly and daily, moderate frequencies like weekly, and lower frequencies such as monthly. While high-frequency data is often abundant, it tends to capture excessive noise and incurs higher transaction costs due to the need for frequent rebalancing (Bakry et al., 2021; Platanakis & Urquhart, 2019). In addition, monthly prices lack the granularity and timeliness required to effectively capture short-term market movements and trends. Therefore, following the suggestions of previous studies (Click & Plummer, 2005; Nguyen & Huynh, 2019), we used weekly adjusted closing prices to ensure data consistency, balance, and completeness, while minimizing the impact of noise and transaction costs.

Therefore, the study employed weekly adjusted closing prices of the top stocks resulting from the initial stage, from January 2018 to September 2022. The optimization models were trained on this dataset and evaluated using an out-of-sample test period covering 65 weeks from October 2022 to December 2023. We implement a weekly, expanding rolling window: each out-of-sample week we recompute the expected-return vector and risk measures using all data up to the prior week, re-optimize weights under full-investment and no-short-selling constraints, rebalance and hold for one week, then extend the window by one week and repeat.

Data Envelopment Analysis Results

In the first stage, portfolio selection was conducted using the CCR and BCC models, which rely on inputs and outputs derived from companies’ financial reports. The efficiency scores of stocks in Table 1 show that nine out of 36 stocks were considered fully efficient, as they achieved a score of one in both CCR and BBC models. Thus, these nine stocks will proceed to the next stage of portfolio optimization. Six stocks obtained a score of one in the BCC model, and the rest of the stocks had scores lower than one.

Efficiency Values of the CCR and the BCC Models on Stocks.

Efficiency Values of the CCR and the BCC Models on Stocks.

As discussed earlier, the CCR model, which assumes constant returns to scale, evaluates efficiency by assuming that output changes in direct proportion to input. Conversely, the BCC model, which accounts for variable returns to scale, is more flexible and allows for cases where output does not change at a constant rate relative to input variations. This flexibility explains why certain stocks such as CPF, DELTA, LH, RATCH, SCC, and IRPC were classified as efficient under the BCC model but not under the CCR model. In contrast, ADVANCE, BH, EGCO, GULF, INTUCH, PTTEP, PTTGC, TOP, and TU stocks, which achieved a score of one in both models, indicate consistent efficiency across different scale assumptions.

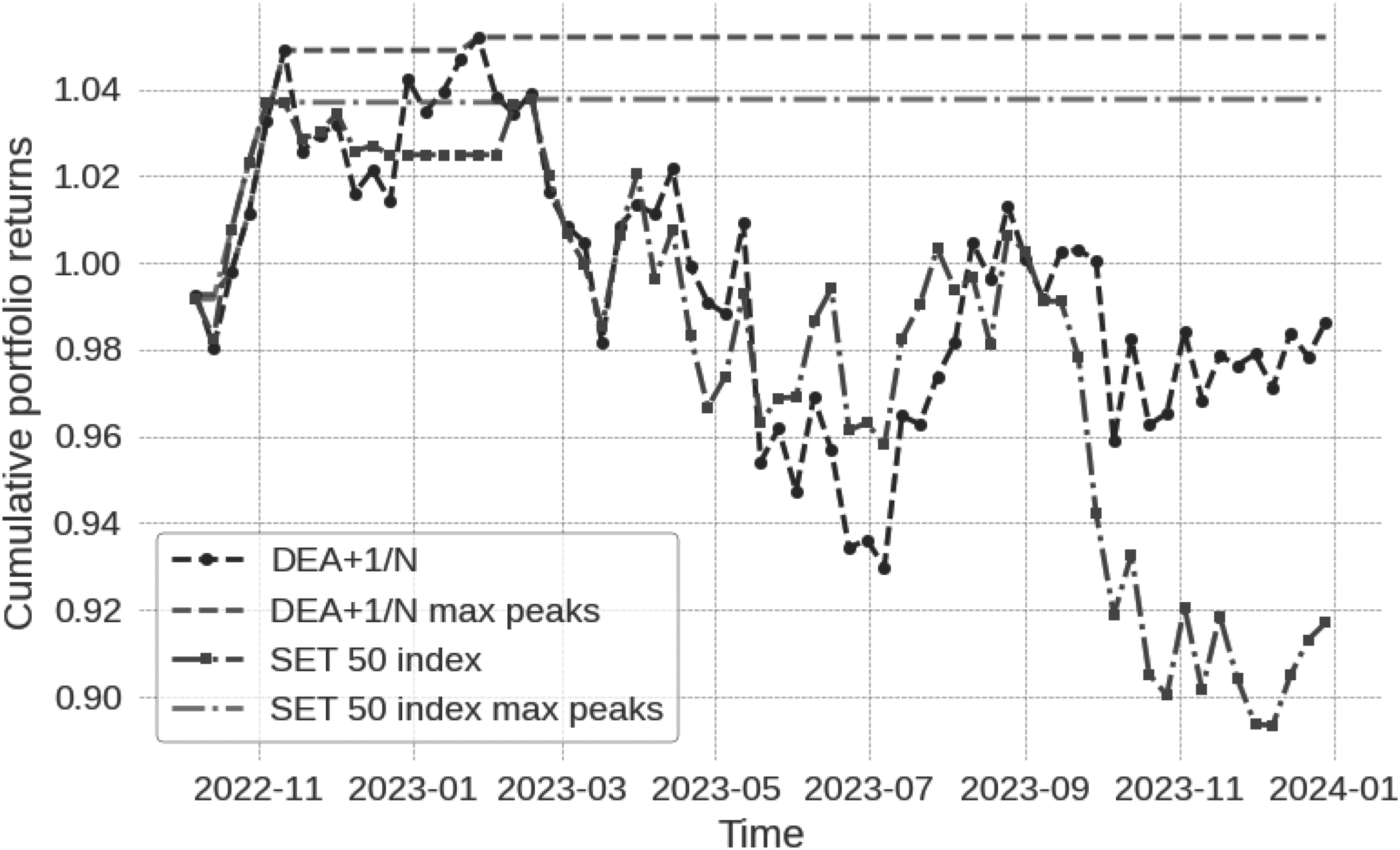

To evaluate the effectiveness of the DEA-based portfolio selection, we compared the performance of the Equal-Weight DEA (DEA+1/N) portfolio against the SET 50 index, a widely used benchmark representing the top 50 companies in the Thai stock market. This comparison highlights how the DEA+1/N portfolio, which allocates equal weights to the 9 top stocks deemed efficient by the DEA models, performed relative to the broader market. Figure 1 illustrates the cumulative returns of DEA+1/N and the SET 50 index using out-of-sample data from October 2022 to December 2023. The DEA+1/N portfolio consistently achieved higher cumulative returns, especially during periods of market stress. For example, between October 2023 and January 2024, the DEA+1/N portfolio maintained an upward trend consolidation, while the SET 50 index experienced a downward trend.

Cumulative Returns of DEA+1/N Portfolio and SET 50 Index.

Furthermore, Table 2 indicates a detailed risk-return analysis. The DEA+1/N portfolio achieved an annualized return of

Annualized Return and Risk Values in Percentages for DEA+1/N Portfolio and SET 50 Index.

Overall, the results showed that incorporating fundamental analysis into financial decision-making for portfolio selection gave a better investment performance. The next section will allocate the investment properties of the selected stocks, with the DEA+1/N portfolio and SET 50 index as benchmarks for comparison.

The objective of this stage is to allocate the optimal size for the 9 top stocks deemed efficient by the DEA models for the investment portfolio. We employed various hybrid models, that is, DEA+mean-standard deviation, DEA+mean-semi-deviation, DEA+mCVaR, the proposed DEA+mAsymRisk models, and DEA+maxSharp as a risk-adjusted model. The performance of the models is evaluated over a 65-week out-of-sample period using a rolling window approach for weekly rebalancing.

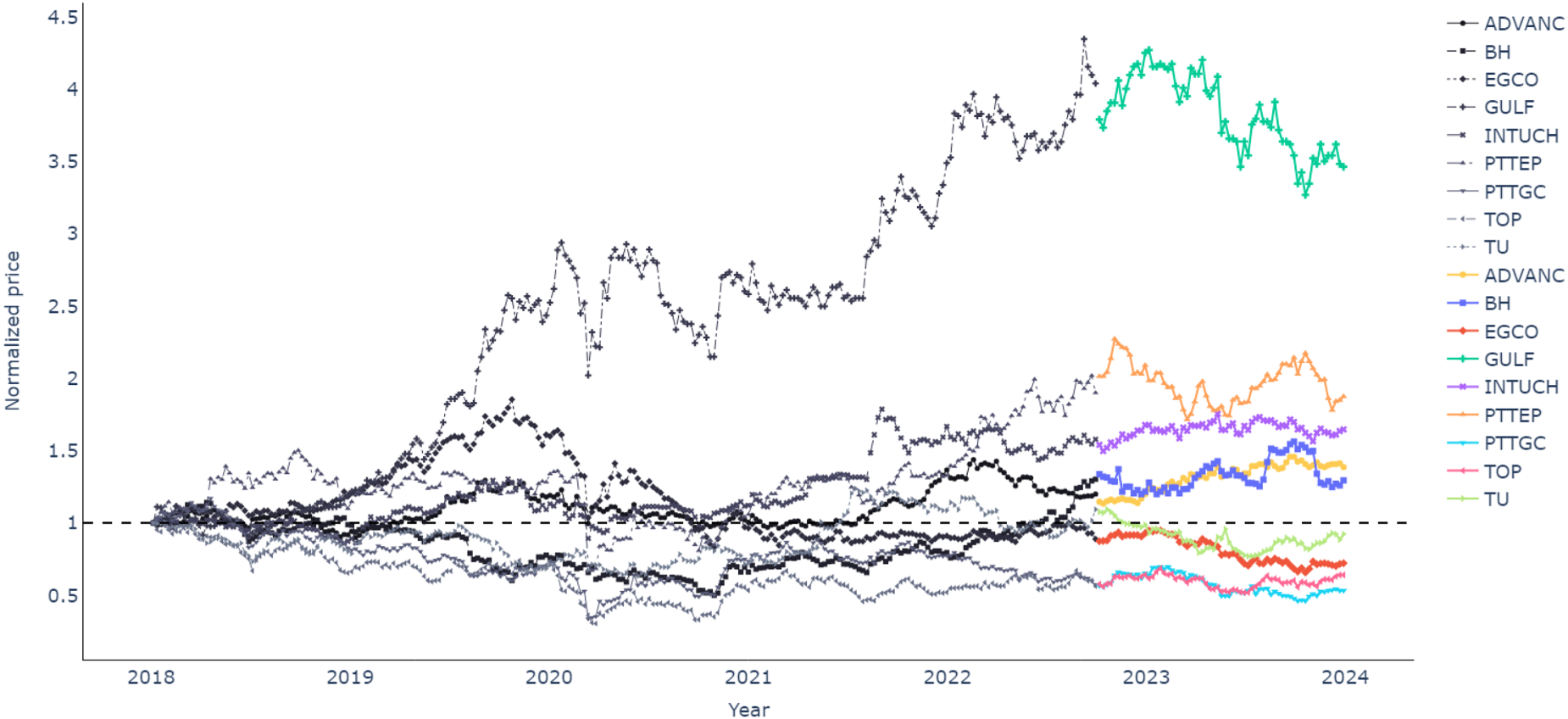

Figure 2 presents an overview of stock performance trends over time. Stocks such as GULF and PTTEP demonstrate consistent and significant growth throughout the period, while INTUCH, BH, and ADVANC exhibit moderate growth and stability. By contrast, EGCO, TU, and TOP displayed bearish trends, with normalized prices remaining below one for much of the period. Volatility across most stocks spiked in 2020, reflecting the global economic uncertainty caused by the COVID-19 crisis. This period is ideal for our study as it captures both systematic and unsystematic risks, offering a valuable opportunity to assess risk mitigation strategies.

Stock Performance Trends During the Training Set (Gray Lines) and Out-of-Sample Test (Bright Lines).

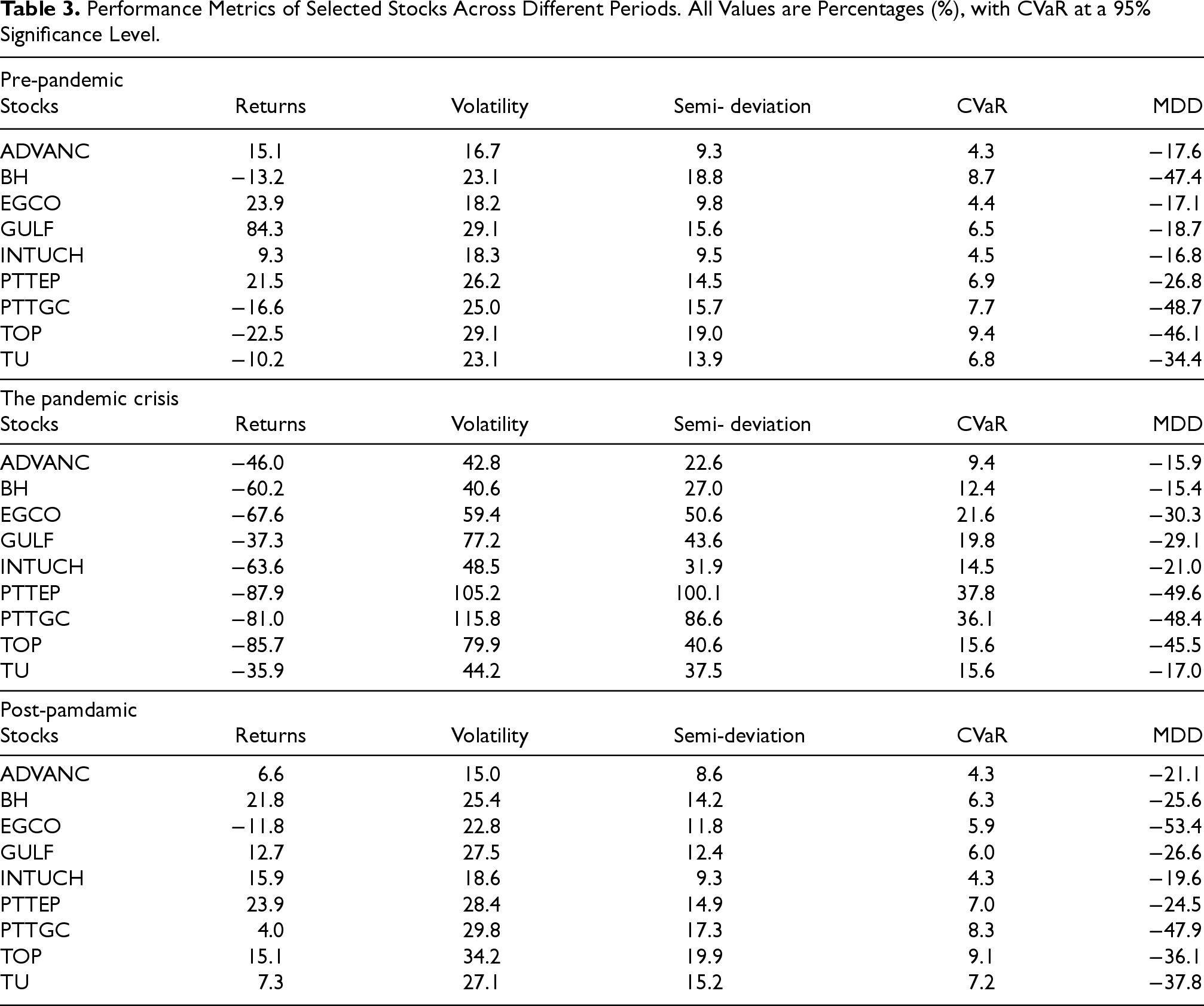

Table 3 indicates the risk-return profile of stocks across three periods: pre-pandemic (December 2017 to January 2020), pandemic crisis (January to April 2020), and post-pandemic (May 2020 to December 2023). During the pre-pandemic period, GULF showed remarkable growth with an annualized return of

Performance Metrics of Selected Stocks Across Different Periods. All Values are Percentages (%), with CVaR at a 95% Significance Level.

The pandemic caused a sharp market downturn, particularly affecting energy stocks such as PTTEP, TOP, and PTTGC. These stocks saw their annualized returns drop to

During the post-pandemic recovery period, the market witnessed an improvement in the return-risk profiles of several stocks. BH and PTTEP reported annualized returns of 21.8% and 23.9%, respectively. In contrast, EGCO continued to underperform, yielding an annualized return of

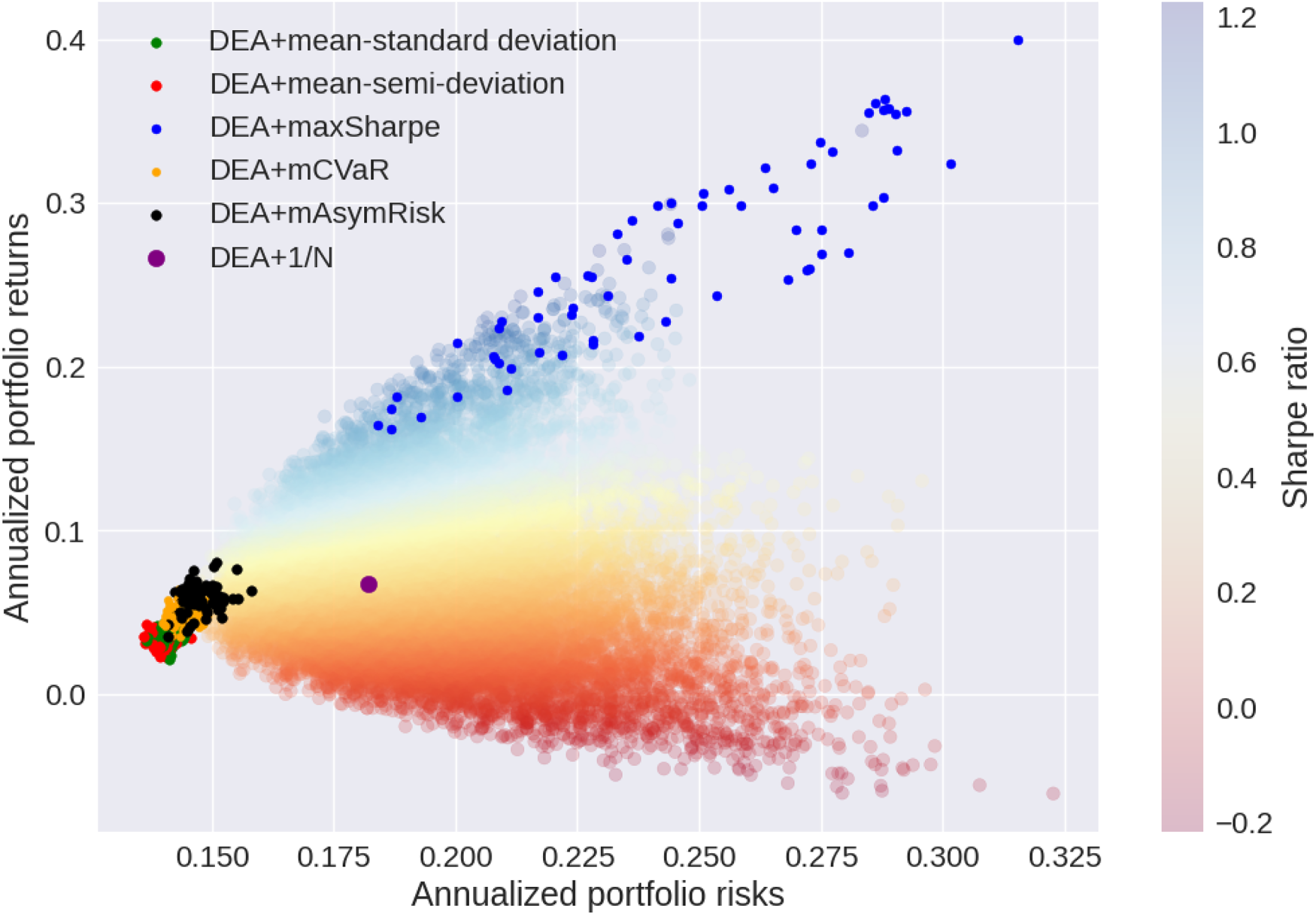

Risk-return Profiles of Portfolios Rebalanced Over Time, with Monte Carlo Simulations.

Effective portfolio construction involves periodic rebalancing to monitor risk-return profiles and maintain desired asset allocations. The methodology in this study employs a rebalancing strategy using an expanding window approach, where the training period extends over time.

Figure 3 visualizes the risk-return profiles of portfolios that were rebalanced over a 65-week test period for each model. To provide an understanding of the model’s performance, we generated 20000 portfolios using Monte Carlo simulations as a background reference. The simulated portfolios form a distinctive shape, with the upper boundary representing the efficient frontier. This curve demonstrates the theoretical optimal portfolios that offer the highest expected return for a given level of risk. Each model is represented by a cluster of points, reflecting the risk-adjusted returns of portfolios recommended by the models throughout the 65-week test period. The dispersion and closeness of points within each cluster reflect the evolution of the portfolios and their stability over time.

Based on the results in Figure 3, the DEA+mean-standard deviation, DEA+mean-semi-deviation, and DEA+mCVaR models tended to be positioned towards the tip of the efficient frontier curve, indicating low risk but correspondingly lower returns. DEA+mean-semi-deviation and DEA+mCVaR achieved slightly higher returns than DEA+mean-standard deviation for similar risk levels, suggesting a benefit in focusing on downside risk. DEA+maxSharpe forms a distinct cluster on the efficient frontier, representing higher returns for moderate risk levels, though with more variability over time. The proposed DEA+mAsymRisk strategy competes with DEA+maxSharpe in terms of returns but shows potentially lower risk, suggesting an effective balance between capturing upside potential and mitigating downside risk.

Finally, Figure 4 illustrates the dynamic shifts in portfolio weights over time across portfolio optimization models, with weekly adjustments during the 65-week period. The risk-minimizing models (DEA+mean-standard deviation, DEA+mean-semi-deviation, DEA+mCVaR, and DEA+mAsymRisk) show some consistent patterns and notable differences. ADVANC emerges as a primary component across all these risk models, indicating its perceived stability and favourable risk-return profile. Interestingly, DEA+mean-standard deviation and DEA+mean-semi-deviation allocated more weight to TU compared to DEA+mCVaR and DEA+mAsymRisk, while the latter two models showed a stronger preference for BH. This suggests that CVaR and asymmetric risk measures may be capturing different aspects of risk that favour BH’s characteristics. Notably, the DEA+mAsymRisk model demonstrated a lower tendency to select EGCO compared to other risk measures, potentially indicating that EGCO exhibits risk characteristics that are particularly penalized by the asymmetric risk framework.

In contrast, the DEA+maxSharpe model shows a significant divergence in its portfolio composition, frequently allocating heavily to energy stocks like GULF and PTTEP. This difference represents DEA+maxSharpe’s goal of maximizing risk-adjusted returns. The risk-minimizing models, on the other hand, maintain more stable allocations overall, consistently favouring telecommunication stocks such as ADVANC and INTUCH. This stability reflects their primary objective of ensuring lower volatility and consistent performance, even if it means potentially sacrificing some upside potential.

Portfolio Performance Evaluation

According to Table 4, the proposed DEA+mAsymRisk model is the best performance among these models in terms of annualized returns, achieving 3.75%, compared to

Dynamic Shifts in Portfolio Weights Over 65 Weeks Across Optimization Models. (a) DEA+mean-standard deviation, (b) DEA+mean-semi-deviation, (c) DEA+mAsymRisk, (d) DEA+mCVaR, (e) DEA+maxSharpe and (f) DEA+1/N.

Performance Metrics for DEA+models.

The CVaR model also performed well, ranking second in annualized returns at 0.89%. This model exhibited a low semi-deviation (7.18%), which was comparable with that of the SET 50 index but with significantly better returns. Although the DEA+mean-semi-deviation and DEA+mean-standard deviation models were not as effective as DEA+mAsymRisk or DEA+mCVaR, they still outperformed the benchmarks in terms of returns while maintaining lower volatility. This suggests that even conservative risk-minimization models can achieve better outcomes than passive indexing or equal-weighting of DEA-efficient stocks. Note that the DEA+maxSharpe strategy, despite its theoretical appeal, underperformed during the evaluation period, generating a low annualized return of

The MDD metric further underscores the risk-mitigation advantages of our portfolio optimization models. The DEA+mCVaR exhibited the lowest MDD at

Figure 5 illustrates the cumulative returns of various portfolio optimization models. The DEA+mAsymRisk model achieved the best overall performance, reaching a peak cumulative return of about 1.15% in late 2023 before settling around 1.05% by January 2024. Other optimization models like DEA+mean-standard deviation, DEA+mean-semi-deviation, and DEA+mCVaR also outperformed the benchmark, clustering between 1% and 1.05% by the end of the period. The DEA+1/N portfolio closely tracked these models but with slightly lower returns.

In contrast, the SET 50 index and DEA+maxSharpee model underperformed significantly. The DEA+maxSharpee showed the most volatility, dropping to about 0.85% in late 2023 before partially recovering. The SET 50 index consistently lagged behind risk-minimizing models, ending the period with a low cumulative return of approximately 0.92%. This finding suggests that risk-minimizing models, particularly those accounting for asymmetric risk, were more effective in this market environment than the market index or the DEA+maxSharpe approach.

Cumulative Returns of Portfolio Optimization Models Over Evaluation Period.

This study applied a two-stage hybrid approach for dynamic portfolio construction to address uncertainties in financial markets, conducted a comprehensive evaluation of stocks based on various financial criteria, and managed risks in volatile markets. Specifically, the approach combined DEA models for initial stock selection with various risk-based optimization models, that is, DEA+mean-standard deviation, DEA+mean-semi-deviation, DEA+mCVaR, the proposed DEA+mAsymRisk models, and DEA+maxSharpe as a risk-adjusted model. Our findings showed the efficacy of this hybrid approach in enhancing portfolio performance within the context of the Thai stock market, specifically the SET 50 index.

Similarly to some studies (Hamdi et al., 2022; Hosseinzadeh et al., 2023; Peykani et al., 2020), the DEA-based stock selection process effectively identified nine qualified stocks out of thirty-six stocks based on fundamental financial metrics, providing a robust foundation for subsequent optimization. This initial screening proved valuable, with the DEA+1/N portfolio outperforming the SET 50 index during a 65-week out-of-sample test, recording an annualized return of

Furthermore, other risk-minimization strategies, including DEA+mCVaR, DEA+mean-semi-deviation, and DEA+mean-standard deviation, could outperforme the benchmarks while maintaining lower volatility. This consistency across various risk measures reinforces the robustness of our two-stage approach and its ability to generate superior risk-adjusted returns. However, the DEA+maxSharpe model underperformed during the evaluation period, generating a low annualized return (

Our research contributes to the growing body of literature on portfolio optimization in emerging markets. By demonstrating the effectiveness of combining fundamental analysis via DEA with advanced risk measures, we provide a framework that can potentially enhance investment strategies in these markets. The superior performance of DEA+mAsymRisk could suggest that incorporating asymmetric risk preferences and correlation effects during downside events can lead to more robust portfolio outcomes.

However, it is important to acknowledge the limitations of this study. While the proposed DEA+mAsymRisk framework offers improved risk-adjusted performance, its relative model complexity may present implementation challenges, and despite the use of an out-of-sample rolling-window design, the possibility of overfitting to historical patterns cannot be entirely excluded.

Our focus on the Thai stock market and the specific time period, which included the COVID-19 pandemic, may limit the generalizability of our findings. Therefore, future research could extend this approach to other emerging markets or asset classes to validate its broader applicability. Additionally, although we did not account for transaction costs in this study, incorporating these costs could enhance the practical relevance of the proposed framework. Exploring the impact of transaction costs in future work will provide a more comprehensive understanding of the real-world feasibility of these strategies without diminishing the theoretical insights this study offers.

Footnotes

Acknowledgements

This work is supported by a PhD Program in Applied Statistics, Faculty of Science, Chiang Mai University, under the CMU Presidential Scholarship. This work is supported by Chiang Mai University.

Ethical Considerations

Not applicable.

Consent to Participate

Not applicable.

Consent for Publication

Not applicable.

Author Contributions

Funding statement

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interest

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability

The data that support the findings of this study are available from the corresponding author upon reasonable request.