Abstract

Government efforts to regulate sustainability depend on the quality, comparability, and verifiability of information flows from regulated organizations to oversight bodies. In many emerging economies, ESG reporting is still produced through spreadsheets, surveys, or stand-alone disclosure tools outside authoritative accounting systems, weakening auditability, increasing reconciliation costs, and limiting transaction-level verification. Drawing on digital government research on regulatory information infrastructures, machine-readable regulation, and data-driven regulatory delivery, this paper argues that ESG oversight is fundamentally an information-governance problem: enforceability depends on standardized semantics, controlled provenance, and interoperable reporting pipelines that support automated validation and traceable auditing. The paper develops a conceptual design synthesis integrating (i) digital government and regulatory information infrastructure scholarship, (ii) sustainability accounting and environmental management accounting (EMA), and (iii) ERP and management accounting change. It specifies an implementable Enterprise Resource Planning (ERP)-to-regulator architecture and derives three analytical propositions concerning embedding depth, traceability, and scope conditions. Using SAP FI/CO as an illustrative example, the framework embeds sustainability attributes within routine accounting objects and control processes. It operationalizes this through three levers: (1) an ESG chart-of-accounts addendum, (2) carbon and energy sub-ledgers for cost-object and asset-level attribution, and (3) machine-readable ERP-to-regulator reporting (API/XBRL-style) with validation rules, access controls, provenance logging, and exception workflows. Bangladesh is used as an illustrative policy context rather than an empirical case study. The paper's contribution is a regulator-ready conceptual architecture that links ERP-based accounting infrastructure to ESG auditability and regulatory enforceability, offering a pathway to scale sustainability assurance in ERP-mature sectors without creating parallel reporting stacks.

Keywords

Introduction

For public managers, regulators, and utility finance teams in emerging economies, a central challenge is generating reliable, auditable ESG information without creating parallel reporting systems or imposing unsustainable administrative burdens on capacity-constrained institutions. Over the past two decades, accountability in both corporate and public sectors has expanded from narrow financial compliance toward sustainability-oriented disclosure aligned with the Sustainable Development Goals (SDGs). This shift has been institutionalized through global reporting architectures, including the GRI Universal Standards (Global Reporting Initiative, 2021), IFRS S2 Climate-related Disclosures (IFRS Foundation, 2023), and the Integrated Reporting Framework (IFRS Foundation, n.d.). Together, these frameworks elevate expectations for comparability, assurance, and transparency, while intensifying pressure on accounting systems to produce non-financial information with financial-grade reliability.

Despite the expansion of sustainability disclosure requirements, the accounting infrastructure for generating ESG information remains fragmented in many emerging economies. Sustainability data are frequently assembled using spreadsheets, consultant-managed surveys, or stand-alone reporting tools that operate outside core financial systems. These arrangements weaken auditability, increase reconciliation costs, and limit regulators’ ability to verify ESG claims at the transaction level. As a result, sustainability reporting often functions as an ex post compliance exercise rather than as an integrated component of financial management and public accountability.

From a digital government perspective, this fragmentation reflects a deeper information-governance problem. Regulators can enforce ESG rules only to the extent that ESG data flows through standardized, controlled, and verifiable information pipelines. Digital government research emphasizes that public accountability depends not merely on disclosure mandates but on how information is structured, standardized, transmitted, and verified across organizational boundaries (Janssen & van den Hoven, 2015; Mergel et al., 2019). Where regulatory data flows lack standardized semantics, controlled provenance, and system-level validation, enforcement capacity erodes even when formal reporting requirements exist.

Research published in Government Information Quarterly further demonstrates that information systems used for public oversight are not neutral technical channels but policy instruments that embed governance logics into data schemas, validation rules, and interoperability arrangements (Cordella & Paletti, 2019; Klievink et al., 2016). When sustainability data are produced outside authoritative operational systems—such as through spreadsheets or consultant-managed portals—regulators face structural information asymmetries, delayed oversight, and high reconciliation costs, undermining effective supervision and comparability across regulated entities. In such settings, the state's information advantage collapses: supervisors receive disclosures but cannot validate them at the transaction level, consistently compare entities, or automate anomaly detection.

Recent digital government research highlights the growing importance of machine-readable regulation, in which regulatory requirements are operationalized through structured, computable data and automated validation mechanisms (Mohun & Roberts, 2020; OECD, 2021; van Ooijen et al., 2019). Under this paradigm, accountability shifts from ex post narrative justification toward compliance-by-design, where regulatory intent is embedded directly into information infrastructures. Nevertheless, much of the existing literature treats sustainability governance, digital regulation, and enterprise information systems as separate domains, leaving unresolved the question of how ESG accountability can be institutionalized within routine accounting infrastructures.

This paper addresses that gap by positioning ERP financial systems as a public-interest regulatory information infrastructure. It is a conceptual design paper rather than an empirical case study, and it uses Bangladesh as an illustrative policy context to motivate feasibility, scope conditions, and governance design choices rather than to support causal inference.

By conceptualizing ERP-to-regulator data pipelines as instruments of digital government, the paper reframes sustainability accounting as an information-policy problem central to regulatory enforceability, auditability, and scalable public accountability in emerging economies.

Enterprise Resource Planning (ERP) systems increasingly constitute the authoritative accounting infrastructure through which both financial and non-financial information must flow. By integrating general ledgers, asset accounting, cost centers, and profitability analysis, ERP systems connect operational activities to formal financial records and reporting outputs (Dumitru et al., 2023; Granlund & Malmi, 2002; Scapens & Jazayeri, 2003). Foundational accounting research shows that ERP adoption reshapes management accounting practices by standardizing data structures, routines, and control mechanisms (Granlund & Malmi, 2002; Kanellou & Spathis, 2013; Scapens & Jazayeri, 2003). More recent scholarship extends these insights to environmental management accounting (EMA) and sustainability performance measurement, highlighting the growing relevance of ERP systems for capturing environmental and social information within accounting processes (Cao et al., 2025; Masanet-Llodra, 2006; Swalih et al., 2024).

However, much of the ERP literature continues to emphasize operational efficiency, integration, and control, under-theorizing the potential of ERP systems as a sustainability accounting infrastructure capable of supporting governance and accountability outcomes (Anaya & Qutaishat, 2022; Anaya et al., 2025). Similarly, sustainability accounting research has focused extensively on disclosure standards, indicators, and reporting outcomes, often treating information systems as a secondary implementation concern rather than as a central determinant of data quality and assurance. This disconnect leaves a conceptual gap between what sustainability frameworks require and what accounting systems are structurally capable of producing.

To address this gap, the paper develops a conceptual sustainability accounting architecture that leverages ERP financial-control systems as the primary vehicle for generating ESG data. Using SAP FI/CO as an illustrative implementation, the paper reframes ERP financial modules not merely as compliance tools but as public-sector sustainability accounting infrastructure. The integrated ledgers inherent to ERP systems—general ledger, asset accounting, cost centers, and profitability analysis—generate continuous audit trails that support SDG-aligned accounting instruments, including carbon-cost attribution, green procurement tracking, and social-impact budgeting (Huynh & Nguyen, 2024). When sustainability variables are embedded directly into routine financial postings, ESG accountability becomes endogenous to financial management rather than layered on as a parallel reporting exercise.

The argument is grounded in institutional and socio-technical perspectives. From an institutional standpoint, organizations internalize sustainability disclosure norms in response to coercive and normative pressures from regulators, standard-setters, and capital markets (DiMaggio & Powell, 1983). From a socio-technical perspective, ERP platforms function as infrastructural mediators of institutional change, embedding governance logics into everyday accounting practices (Geels, 2002; Geels, 2011). In developing-country contexts—where institutional capacity and enforcement vary widely—the configuration of accounting infrastructure plays a decisive role in determining whether sustainability standards translate into substantive accountability or remain symbolic.

Bangladesh provides a particularly instructive policy context for examining this transformation. Sustainability disclosure requirements are being consolidated through regulatory guidance and supervisory review led by Bangladesh Bank (Bangladesh Bank, 2023; Bangladesh Bank, 2025). At the same time, sector-specific literature indicates ERP adoption and implementation challenges in parts of the Bangladeshi economy, including the healthcare sector, while broader developing-country research suggests that compliance pressure often shapes ERP uptake and performance under constrained institutional conditions (Hawari & Heeks, 2010; Heeks, 2002; Karim et al., 2025). Nevertheless, digital finance systems and ESG governance frameworks have largely evolved in parallel, limiting the verifiability and comparability of sustainability data. Drawing on insights from the information systems and development literature (Hawari & Heeks, 2010; Heeks, 2002), this paper proposes policy-oriented accounting mechanisms to integrate ERP financial modules with national ESG reporting architectures, thereby transitioning sustainability accounting from fragmented compliance toward institutionalized public accountability.

The proposed architecture is particularly applicable to critical infrastructure sectors, notably electricity, gas, and water utilities, where tariff regulation, fiscal transfers, and service obligations require verifiable financial and sustainability information within a unified accounting system. Accordingly, the paper asks: How can ERP financial-control systems be configured as a regulatory information infrastructure to enable machine-readable ESG oversight with transaction-level traceability in emerging economies?

The paper makes four contributions. First, it reframes sustainability reporting as a digital government information-infrastructure problem defined by standardized semantics, controlled provenance, and interoperable data flows that shape enforceability (Cordella & Paletti, 2019; Klievink et al., 2016). Second, it specifies the causal mechanism through which ERP-to-regulator pipelines can operationalize compliance-by-design by embedding sustainability attributes within authoritative accounting objects, controls, and reporting interfaces (Janssen et al., 2012; van Ooijen et al., 2019). Third, it develops three analytical propositions linking transaction-level embedding, traceability, and ERP maturity to ESG auditability and regulatory enforceability. Fourth, it offers a regulator-oriented conceptual architecture for ERP-mature sectors—particularly banking and utilities—to scale ESG accountability without constructing parallel reporting stacks.

Literature Review: ERP Systems, Sustainability Accounting, and Regulatory Accountability

This paper adopts a conceptual, policy-oriented design synthesis that integrates three streams of scholarship: (i) digital government and regulatory information infrastructures, including interoperability, machine-readable regulation, and public value; (ii) sustainability accounting and environmental management accounting (EMA); and (iii) ERP systems and management accounting change. This literature is combined to derive an implementable ERP-to-regulator regulatory information architecture. The architecture maps regulatory disclosure requirements—such as sustainability classifications, assurance, and traceability—onto ERP accounting objects and controls, including chart-of-accounts structures, cost objects, asset master data, authorizations, and audit trails. It links these to an interoperability layer (API/XBRL-style submissions) that preserves traceability from reported ESG values back to source transactions. The scope conditions are emerging-economy regulators and ERP-mature sectors, notably banking and utilities, where financial-control systems already structure compliance routines and therefore offer leverage points for ESG enforceability.

ERP Systems and Management Accounting Transformation

The relationship between ERP systems and management accounting has been a central concern of accounting research for more than two decades. Early studies examined whether ERP adoption produced incremental adjustments or more fundamental transformations in accounting practice. Granlund and Malmi (2002) documented a moderate but persistent impact, showing that ERP systems standardize data structures and routines while leaving elements of managerial interpretation unchanged. Similarly, Scapens and Jazayeri (2003) observed that ERP implementation restructures accounting processes and information flows, enhancing organizational integration while simultaneously constraining flexibility through standardized procedures.

Subsequent research reinforced these insights by highlighting the effects of ERP systems on information quality, traceability, and control. Kanellou and Spathis (2013) demonstrate that user satisfaction in ERP environments is closely associated with improvements in accounting accuracy, timeliness, and organizational integration. Collectively, this literature positions ERP systems not as neutral IT tools but as foundational accounting infrastructure shaping how financial information is generated, validated, and used within organizations.

In developing- and emerging-economy contexts, ERP implementation is further conditioned by institutional and capacity constraints. Huang and Palvia (2001) identify persistent differences between advanced and developing countries, including skills shortages, localization challenges, and governance weaknesses. Heeks (2002) and Hawari and Heeks (2010) similarly show that information systems in developing countries frequently underperform when institutional realities are misaligned with system design. These findings highlight that ERP configuration is inseparable from governance context and regulatory objectives—an issue of particular importance when ERP systems are repurposed to support sustainability accountability rather than financial compliance alone.

Environmental Management Accounting and Sustainability Disclosure

In parallel, sustainability accounting research has evolved around environmental management accounting (EMA) and ESG disclosure. Early EMA studies emphasized the strategic importance of integrating environmental costs into accounting systems. Masanet-Llodra (2006), for example, shows that systematic identification and allocation of ecological costs can support environmentally innovative strategies.

More recent research links EMA practices to institutional pressures and sustainability performance outcomes. Cao et al. (2025) finds that environmental management accounting plays an important role in enabling organizations to respond to institutional sustainability pressures. Systematic reviews by Swalih et al. (2024) further demonstrate that EMA improves strategic decision-making by increasing visibility over environmental costs, risks, and opportunities. Huynh and Nguyen (2024) likewise show that EMA contributes positively to sustainability performance when embedded within organizational control systems.

However, much of this literature implicitly assumes the existence of appropriate data infrastructures and devotes limited attention to how environmental information is actually generated, governed, and assured within core accounting systems.

At the same time, ESG disclosure research has examined the influence of reporting frameworks and disclosure innovation. Sun (2024) finds that integrated reporting can improve ESG performance but notes persistent concerns regarding data credibility and verification. Dumitru et al. (2023) similarly argue that ERP automation creates new opportunities for sustainability accounting and reporting, while documenting uneven empirical implementation across organizations. Taken together, these studies suggest that the effectiveness of sustainability disclosure depends not only on reporting standards or indicator design, but also on the robustness of the underlying accounting infrastructure that produces the data.

Institutional and Socio-Technical Perspectives on Accountability

Institutional theory provides a useful lens for understanding why sustainability accounting practices diffuse unevenly across organizations and countries. DiMaggio and Powell (1983) explain how coercive, normative, and mimetic pressures generate organizational isomorphism, encouraging firms to adopt similar structures and practices. In the context of sustainability reporting, global frameworks such as the Global Reporting Initiative Standards and IFRS S2 create coercive and normative pressures, while peer adoption reinforces mimetic dynamics across industries.

However, institutional pressures alone do not guarantee substantive accountability. Geels’ (2002, 2011) multi-level perspective highlights the role of socio-technical systems in mediating institutional change. From this perspective, ERP platforms function as infrastructural regimes that translate governance logics into everyday operational practices. Where accounting infrastructures are poorly aligned with sustainability objectives, disclosure may remain symbolic rather than substantive.

This interaction is particularly important in emerging economies, where regulatory capacity and enforcement vary widely. ERP systems embedded in public-sector finance and utility management can therefore serve as critical leverage points for institutionalizing sustainability accountability. However, existing literature has not sufficiently theorized how ERP financial-control modules can be configured as a sustainability accounting infrastructure capable of producing audit-grade, regulator-verifiable ESG data.

Digital Government, Regulatory Information Infrastructure, and Enforceability

Digital government research emphasizes that public accountability is conditioned by the information infrastructures through which regulatory data are generated, exchanged, and verified across organizational boundaries. In regulated domains, data fields, reporting schemas, interoperability standards, and validation rules are not neutral technical choices; they shape what can be monitored, compared, and enforced at scale (Cordella & Paletti, 2019; Janssen et al., 2012; Klievink et al., 2016). Earlier work on regulatory information infrastructures established that fragmented reporting architectures undermine comparability, increase reconciliation costs, and weaken risk-based supervision (Janssen & van den Hoven, 2015; Klievink et al., 2016; van Ooijen et al., 2019).

More recent work sharpens this insight by treating regulation itself as increasingly computable. Rules as Code proposes that governments create an official machine-consumable version of rules so that legal requirements can be understood and actioned consistently by digital systems (Mohun & Roberts, 2020). Related work on automation in governance similarly shows how discretion and control can be reconfigured through digital rule environments (Zouridis et al., 2020). In parallel, work on data-driven regulatory delivery argues that regulatory effectiveness increasingly depends on digitally enabled supervision, structured data, and information-rich risk targeting rather than purely document-based compliance review (OECD, 2021). These developments suggest that enforceability depends not only on the substantive content of rules, but also on whether those rules can be translated into operational data structures and validation logic.

These developments are no longer confined to abstract RegTech debates. In sustainability reporting, digital taxonomies now translate disclosure standards into machine-readable structures. The IFRS Foundation published the IFRS Sustainability Disclosure Taxonomy 2024 to reflect IFRS S1 and IFRS S2, thereby enabling digital comparability around the ISSB standards (IFRS Foundation, 2024). EFRAG has likewise developed the ESRS Set 1 XBRL Taxonomy to support the digital tagging of ESRS statements (EFRAG, 2024). Global Reporting Initiative has also launched its Sustainability Taxonomy, a machine-readable architecture designed to improve the accessibility, comparability, and quality of sustainability data reported using the Global Reporting Initiative Standards (Global Reporting Initiative, 2025).

Digital supervisory reporting infrastructures show the same pattern. ESMA's electronic reporting regime treats digital reporting as a means of improving accessibility, analysis, and comparability of corporate disclosures (European Securities and Markets Authority, n.d.). Similarly, the EBA's reporting frameworks rely on a structured data point model, XBRL taxonomies, and validation rules to standardize supervisory submissions and data exchange (European Banking Authority, n.d.). Together, these developments show that digital regulation increasingly depends on structured reporting logics rather than unstructured documentary compliance.

However, this literature still concentrates primarily on the machine-readability of disclosure outputs or supervisory submissions. It says much less about the upstream accounting architecture through which sustainability data are generated in the first place. This is the unresolved problem for ESG governance in emerging economies: even when machine-readable reporting standards exist, disclosure remains weak if the underlying data are still assembled through peripheral spreadsheets, consultant-managed templates, or non-authoritative systems. The analytical gap, therefore, is not only about how to digitize reporting, but also about how to institutionalize the generation of regulator-verifiable sustainability data within routine accounting infrastructures.

Research Gap and Contribution

The literature reveals three interrelated gaps. First, ERP research has focused predominantly on efficiency and control, with limited attention to sustainability accounting and regulatory accountability. Second, sustainability accounting and EMA studies emphasize disclosure practices and performance effects without adequately theorizing the role of accounting infrastructure in producing credible, auditable data. Third, institutional and socio-technical perspectives have seldom been integrated into a coherent framework for ERP-enabled sustainability accountability in emerging economies.

This paper addresses these gaps by developing a conceptual ERP-native regulatory information architecture that links management accounting systems, institutional pressures, and public-sector accountability. Taken together, the literature suggests that ESG oversight fails less because of missing indicators than because of weak regulatory data architectures—unclear semantics, absent provenance, and limited interoperability. This motivates the paper's central claim: ERP financial-control modules are a practical leverage point for ESG enforceability because they already encode classification rules, approvals, and audit trails at the transaction level.

Analytical Propositions

The foregoing synthesis supports three analytical propositions.

When ESG attributes are embedded at the point of transaction posting within ERP ledger logic, ex post reconciliation effort declines, and the likelihood of first-pass audit acceptance of sustainability disclosures increases.

Observable implications include fewer manual period-end adjustments, fewer ledger-to-disclosure mismatches, and fewer audit exceptions.

ERP-native ESG reporting improves regulatory enforceability when machine-readable submissions preserve traceability from reported sustainability values back to source transactions, cost objects, asset records, and approval histories.

The governance benefits of ERP-native ESG reporting are strongest in ERP-mature, highly regulated sectors and weaker where firms lack integrated accounting infrastructure, implementation capacity, or interoperable supervisory standards.

For the purposes of this paper, ERP maturity refers to a minimum threshold comprising an integrated general ledger, cost-object accounting (for example, cost centers and internal orders or their equivalents), asset/master-data linkage, period-close controls, and role-based authorization/audit-trail functionality sufficient to preserve transaction-level provenance.

Together, these propositions shift the paper from descriptive synthesis toward a mid-range theoretical argument linking information architecture to accountability outcomes under identifiable scope conditions (DiMaggio & Powell, 1983; Geels, 2002, 2011; Klievink et al., 2016; Scapens & Jazayeri, 2003).

Enterprise Resource Planning (ERP) systems standardize financial and operational data structures, thereby shaping organizational control, accountability, and compliance routines (Granlund & Malmi, 2002; Scapens & Jazayeri, 2003). Within this architecture, ERP financial control modules—illustrated here with SAP FI/CO—serve as a ledger-based information infrastructure that integrates the general ledger, cost centers, internal orders, asset accounting, and profitability analysis. This integration enables granular traceability of transactions across financial and operational activities, strengthening internal consistency and improving the auditability of reporting outputs (Huynh & Nguyen, 2024; Kanellou & Spathis, 2013).

Although ERP systems have traditionally been deployed to satisfy financial compliance and statutory reporting requirements, recent research shows that the same ledger architecture can support environmental and social accountability when sustainability attributes are embedded directly into routine accounting processes, extending environmental management accounting (EMA) within ERP environments (Cao et al., 2025; Dumitru et al., 2023; Masanet-Llodra, 2006; Sun, 2024; Swalih et al., 2024).

The core mechanism advanced in this paper is that ESG oversight becomes credible and enforceable when ESG data are generated within the same authoritative infrastructure that governs financial accountability. In practical terms, this requires relocating ESG data production from peripheral spreadsheets and ad hoc disclosure tools into the ERP's internal logic. When sustainability variables are recorded through ERP transactions, they become subject to established internal controls—authorization, documentation, classification rules, reconciliation procedures, and audit trails.

Three complementary design levers operationalize this shift: an ESG chart-of-accounts (CoA) addendum that standardizes classification, carbon and energy sub-ledgers that enable transaction-level attribution, and ERP-to-regulator machine-readable reporting that supports automated validation and regulatory assurance.

From a digital government perspective, these levers function as information-policy instruments. The ESG CoA addendum defines regulatory semantics; carbon and energy sub-ledgers establish controlled provenance; and ERP-to-regulator reporting pipelines enable interoperability and automated rule checking. Together, they operationalize principles of machine-readable regulation by embedding regulatory intent directly into enterprise information systems, enabling rule-based supervision rather than discretionary disclosure review (Janssen et al., 2012; Klievink et al., 2016; van Ooijen et al., 2019).

The causal logic can be stated directly. Institutional pressure creates demand for comparable ESG disclosure, but disclosure remains weak when sustainability data are produced outside authoritative accounting systems. Embedding ESG attributes within ERP posting logic changes this by standardizing classification at the point of entry, attaching sustainability variables to recognized accounting objects, preserving provenance through routine controls, and generating machine-readable outputs that regulators can validate systematically. Regulatory enforceability, therefore, rises not simply because disclosure standards exist, but because compliance information is produced within a controlled infrastructure that links reported values to source transactions (DiMaggio & Powell, 1983; Geels, 2002, 2011; Janssen et al., 2012; van Ooijen et al., 2019).

The first lever is an ESG chart-of-accounts addendum—an extension of existing account structures that creates standardized categories for sustainability-related transactions (Global Reporting Initiative, 2021; IFRS Foundation, 2023; IFRS Foundation, n.d.). From a governance standpoint, the chart of accounts is not merely a coding device; it is a control instrument that determines what is countable, how expenditures are classified, and which transactions can be aggregated into auditable disclosure statements.

In many emerging-economy settings, ESG reporting is weakened by inconsistent classification practices—for example, environmental capital expenditures recorded under generic maintenance accounts or social expenditures dispersed across discretionary cost centers. An ESG CoA addendum addresses this weakness by specifying a minimum set of ESG-linked accounts or account attributes that align transaction classification with regulatory disclosure requirements.

This approach strengthens auditability in two ways. First, it reduces reliance on ex post interpretation by requiring sustainability-relevant transactions to be recognized at the point of posting, within the same rules-based environment that governs financial reporting (Granlund & Malmi, 2002; Scapens & Jazayeri, 2003). Second, it facilitates reconciliation between sustainability disclosures and financial statements by ensuring that ESG totals can be traced directly to the general ledger and associated cost objects, thereby improving comparability and assurance across regulated entities (Huynh & Nguyen, 2024; Kanellou & Spathis, 2013). In effect, the ESG CoA addendum converts sustainability classification into an internal control routine rather than a discretionary narrative exercise.

Carbon and Energy Sub-Ledgers: Attribution Rather Than Estimates

The second lever is the creation of carbon and energy sub-ledgers within ERP financial and asset modules to attribute emissions and resource use to cost centers, internal orders, and asset classes (Cao et al., 2025; Masanet-Llodra, 2006; Swalih et al., 2024). Much sustainability disclosure currently relies on aggregated estimates, manual conversion factors, or consultant-managed spreadsheets that cannot be audited back to source transactions. Sub-ledgers address this limitation by embedding sustainability attributes as structured data linked to recognized accounting objects.

In practice, energy purchases and emissions-relevant inputs can be tagged at the time of posting with attributes that map to specific cost centers, production lines, project orders, or asset identifiers. Asset accounting can store energy-relevant metadata for major equipment, allowing depreciation, maintenance, and energy-consumption profiles to be linked for assurance and performance analysis. These configurations generate transaction-level traceability between financial postings and sustainability variables.

From an EMA perspective, sub-ledgers enable routine cost attribution: sustainability variables become traceable components of the cost structure rather than external indicators appended after financial closing (Huynh & Nguyen, 2024; Masanet-Llodra, 2006; Swalih et al., 2024). This also enhances managerial decision support by allowing internal carbon prices or carbon-cost proxies to be represented as cost elements within controlling and profitability analysis, making carbon exposure visible in the same reports used for operational control (Anaya et al., 2025). By surfacing exposure to carbon taxation, energy price volatility, and compliance penalties in routine accounting outputs, sub-ledgers strengthen organizational risk resilience (Sun, 2024). Moreover, transaction-level attribution can increase the credibility of ESG claims for external stakeholders by reducing reliance on qualitative or weakly reconciled disclosures (Cao et al., 2025; Sun, 2024).

ERP-to-Regulator Reporting: Regulatory Assurance Through Traceability

The third lever is automated, machine-readable reporting from ERP systems to regulators through API- or XBRL-style submissions, designed to strengthen regulatory assurance while reducing reporting burden (European Banking Authority, n.d.; European Securities and Markets Authority, n.d.; EFRAG, 2024; IFRS Foundation, 2024). In Bangladesh, the relevant immediate point is not that such a machine-readable architecture is already fully deployed for ESG reporting, but that domestic disclosure guidance now creates a policy basis on which more structured supervisory reporting could be layered over time (Bangladesh Bank, 2023; Bangladesh Bank, 2025). ERP-to-regulator reporting reduces this friction by generating standardized submissions directly from the ledger environment, where controls, approvals, and documentation are already embedded.

This mechanism supports regulatory assurance in three ways. First, it enables structured validation checks: regulators can require standardized data fields, metadata, and reporting periods, reducing ambiguity and discretionary interpretation (Bangladesh Bank, 2023; Bangladesh Bank, 2025). Second, it improves auditability by preserving traceability from reported ESG values back to underlying postings, cost objects, and accounting periods, enabling auditors and supervisors to apply familiar audit procedures. Third, it limits opportunistic reporting by constraining late-stage spreadsheet manipulation; reported ESG totals become a function of ledger postings and configuration rules rather than discretionary narrative reporting. This aligns with research emphasizing that the credibility of ESG disclosures depends on the quality of the underlying accounting information infrastructure (Dumitru et al., 2023; Sun, 2024).

Because these data flows operate in public administration contexts, governance and protection are essential. ERP-to-regulator pipelines should incorporate role-based access controls, segregation-of-duties alignment, and logged provenance to ensure that (i) regulated entities cannot modify sustainability attributes post hoc without audit signals, and (ii) regulators can perform validation without gaining unnecessary access to sensitive operational data. In practice, this requires specifying minimum required ESG fields, allowable transformations, validation checks, and exception workflows so that ESG reporting functions as

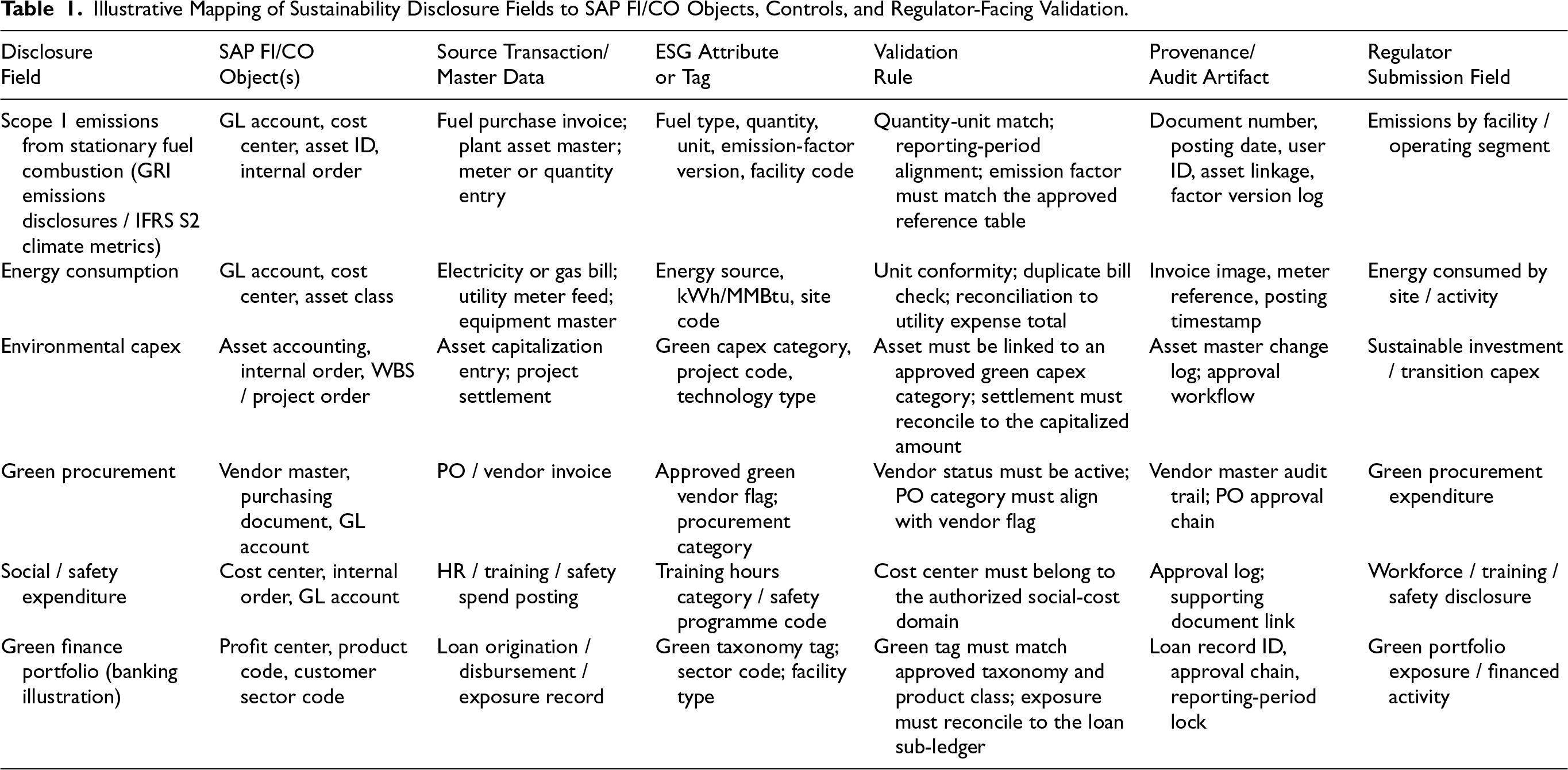

As shown in Table 1, the ERP-specific logic of the framework can be made explicit by mapping selected sustainability disclosure requirements onto SAP FI/CO objects, validation rules, and provenance controls, thereby showing how ledger-based controls can support machine-readable supervisory reporting (Dumitru et al., 2023; Global Reporting Initiative, 2021; Global Reporting Initiative, 2025; Huynh & Nguyen, 2024; IFRS Foundation, 2024).

Illustrative Mapping of Sustainability Disclosure Fields to SAP FI/CO Objects, Controls, and Regulator-Facing Validation.

Illustrative Mapping of Sustainability Disclosure Fields to SAP FI/CO Objects, Controls, and Regulator-Facing Validation.

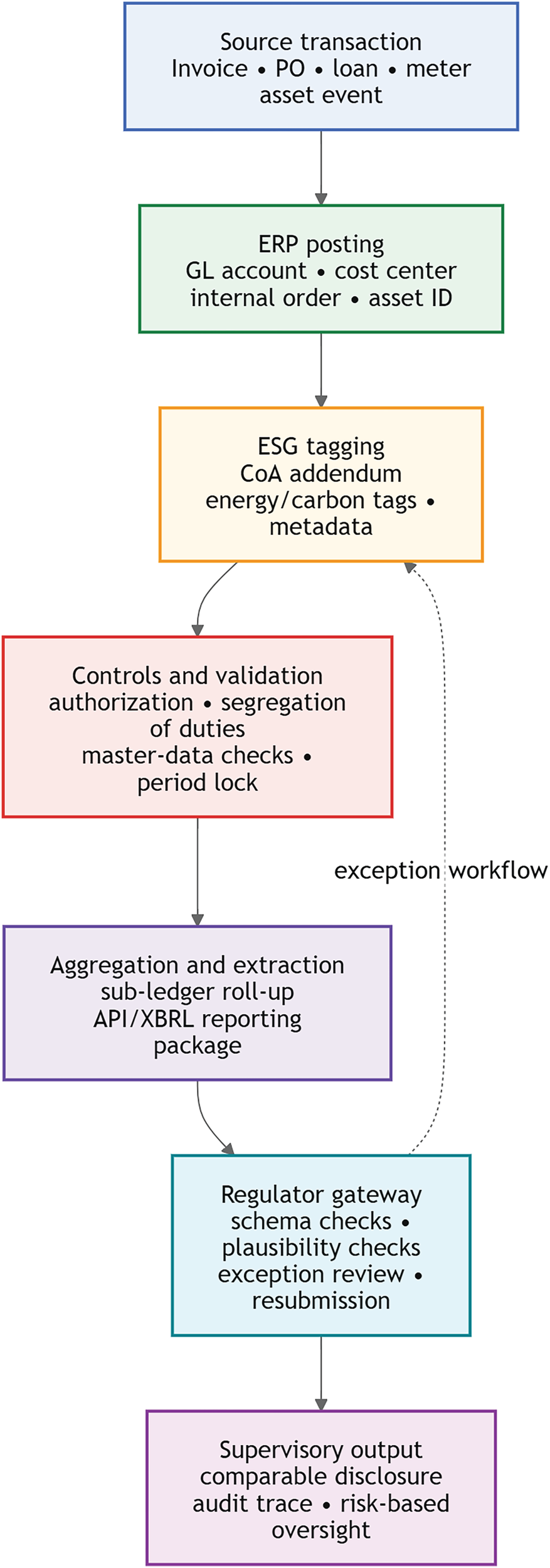

Figure 1 illustrates that regulatory assurance depends not only on final disclosure outputs but on the integrity of the upstream chain linking source transactions, accounting objects, ESG tagging, control routines, machine-readable extraction, and regulator-side validation (European Banking Authority, n.d.; European Securities and Markets Authority, n.d.; IFRS Foundation, 2024).

Data provenance flow (from ERP transaction posting to regulator submission).

Embedding ESG attributes within ERP financial ledgers produces three policy-relevant outcomes. First, operational efficiency improves when sustainability variables—such as internal carbon prices—are treated as cost elements within controlling and profitability modules, thereby enhancing visibility into resource use and supporting waste reduction through routine variance analysis and cost control (Anaya et al., 2025). Second, risk resilience is strengthened as ESG-linked cost structures reveal exposure to carbon taxation, energy price volatility, and compliance penalties in routine financial reporting, enabling ex ante risk management rather than reliance on ex post disclosure narratives (Sun, 2024). Third, investor and lender confidence is enhanced through automated, transaction-level audit trails that improve the credibility and comparability of sustainability disclosures (Annosi et al., 2024; Cao et al., 2025).

Together, these outcomes shift sustainability accounting from external compliance toward institutionalized accountability, where ESG performance becomes an endogenous feature of core accounting processes rather than an add-on reporting obligation. Green procurement criteria, for example, can be operationalized through vendor master data and purchasing classifications that feed directly into financial postings, while carbon and energy sub-ledgers classify emissions-linked expenditures within cost centers and internal orders. These configurations connect sustainability performance to enterprise cost structures, asset management, and financial outcomes, reinforcing accountability through established accounting controls (Granlund & Malmi, 2002; Kanellou & Spathis, 2013; Scapens & Jazayeri, 2003).

Theoretical Consistency: Institutionalization and Socio-Technical Embedding

This mechanism is consistent with institutional theory, whereby organizations internalize global sustainability disclosure standards and related digital reporting architectures—such as the GRI Universal Standards, IFRS S2, and the IFRS Sustainability Disclosure Taxonomy—in response to coercive and normative regulatory pressures (DiMaggio & Powell, 1983; Global Reporting Initiative, 2021; Huang & Palvia, 2001; IFRS Foundation, 2023, 2024). It also reflects a socio-technical transition in which ERP platforms function as infrastructural mediators of governance change, embedding sustainability logics into everyday accounting practices rather than treating them as separate reporting initiatives (Geels, 2002; Geels, 2011; Hawari & Heeks, 2010; Heeks, 2002). In emerging economies, where enforcement capacity and reporting quality vary widely, the configurability of ERP systems can determine whether sustainability standards translate into substantive accountability or remain symbolic.

In Bangladesh, this mechanism is policy-relevant because sustainability disclosure expectations are increasingly being formalized through Bangladesh Bank guidance and supervisory review, while sector-specific evidence points to ERP adoption and implementation challenges in parts of the economy rather than demonstrating uniform cross-sector ERP maturity (Bangladesh Bank, 2023; Bangladesh Bank, 2025; Hawari & Heeks, 2010; Heeks, 2002; Karim et al., 2025). Embedding ESG accounting within ERP financial modules, therefore, represents a plausible regulator-oriented pathway for improving the structure, auditability, and comparability of sustainability information in integrated accounting systems.

SAP FI/CO functions not merely as a compliance tool but as a socio-technical accounting infrastructure for sustainable competitiveness, enabling emerging economies such as Bangladesh to align routine financial management with global sustainability standards. In digital government terms, the architecture operationalizes three complementary enforcement functions. The ESG chart-of-accounts addendum provides regulatory semantics by standardizing the definition of an ESG-relevant transaction. Carbon and energy sub-ledgers establish controlled provenance by attaching ESG attributes to recognized accounting objects under existing controls. The ERP-to-regulator reporting layer ensures interoperability, producing machine-readable submissions that regulators can validate automatically and audit back to source postings. Together, these elements transform ESG reporting from narrative disclosure into infrastructure-enabled, compliance-by-design accountability.

Bangladesh Case Context

Bangladesh provides a policy-relevant and institutionally rich context for illustrating ERP-enabled sustainability accountability amid concurrent advances in digital financial reform, state-led regulation, and rising ESG disclosure pressures in an emerging economy. The discussion is illustrative rather than evaluative: it motivates feasibility and governance-design choices for ERP-native ESG oversight rather than testing causal impacts. Bangladesh combines growing regulatory demand for sustainability disclosure with uneven ERP maturity and persistent gaps in sustainability data integration, making it a useful context for examining ERP-to-regulator architectures for ESG accountability.

ERP Diffusion, Banking Regulation, and Accounting Infrastructure

Over the past decade, Bangladesh has experienced increasing pressure for more structured financial and sustainability disclosures, particularly in the banking and finance sector, through guidance issued by Bangladesh Bank (Bangladesh Bank, 2023; Bangladesh Bank, 2025). This makes Bangladesh a relevant context for considering ERP-native ESG reporting architectures, especially where regulated entities already rely on formal accounting and reporting systems. At the same time, the currently cited sector-specific ERP literature for Bangladesh is narrower than the full regulatory landscape considered in this paper: published evidence directly verifies ERP adoption and implementation challenges in healthcare, while broader developing-country research indicates that ERP outcomes are strongly shaped by institutional capacity, governance alignment, and compliance pressures (Hawari & Heeks, 2010; Heeks, 2002; Karim et al., 2025). For this reason, Bangladesh is used here primarily as an illustrative policy setting in which disclosure regulation is advancing faster than the development of an integrated ESG data infrastructure.

A Dual Accounting Landscape: ERP-Mature Versus Lagging Firms

Despite this diffusion, ERP adoption remains uneven in depth and configuration. Where banks, regulated utilities, and large conglomerates operate integrated ERP modules, these systems can generate audit-ready financial data and standardized management reports. In contrast, many small and medium-sized enterprises (SMEs) and unregulated firms continue to rely on fragmented accounting software or spreadsheets with limited data governance and weak audit trails (Hawari & Heeks, 2010; Heeks, 2002; Huang & Palvia, 2001).

This divergence has produced a dual accounting landscape. ERP-mature organizations can generate transaction-level, system-controlled data suitable for reconciliation and audit. In contrast, lagging firms often treat sustainability reporting as an external compliance exercise mediated by consultants and detached from routine accounting processes. From a regulatory perspective, this asymmetry creates information blind spots: supervisors may receive formally compliant ESG disclosures that remain substantively non-comparable because underlying accounting infrastructures differ across reporting entities. Embedding ESG reporting requirements within authoritative ERP systems that already govern financial accountability, therefore, offers a more robust alternative to layering sustainability portals on top of heterogeneous accounting practices.

ESG Policy Drivers: Banking Supervision, Utilities, and Export Markets

ESG disclosure pressures in Bangladesh are intensifying through several overlapping channels. At the regulatory level, the Bangladesh Bank Guideline on Sustainability and Climate-related Financial Disclosure for Banks and Finance Companies aligns domestic expectations with international sustainability and climate disclosure frameworks, including IFRS S2, while sustainability reporting assessments also indicate growing disclosure uptake alongside persistent problems of consistency and assurance in Bangladesh (Bangladesh Bank, 2023; Global Reporting Initiative, 2024; IFRS Foundation, 2023). Banks are increasingly expected to disclose climate-risk exposures, green financing portfolios, and environmental performance indicators as part of supervisory review processes.

At the same time, public utilities and state-owned enterprises face increasing scrutiny over tariffs, subsidies, and fiscal transfers. Energy pricing, capacity payments, and fuel subsidies carry substantial fiscal implications, and sustainability-related inefficiencies increasingly translate into budgetary risks. However, many utilities lack accounting systems capable of attributing energy losses, emissions-related costs, or environmental expenditures at the asset or cost center level, thereby limiting regulators’ ability to assess sustainability performance beyond aggregate financial outcomes.

A third driver arises from international market pressures, particularly in export-oriented sectors such as the garment industry. International buyers, lenders, and development finance institutions increasingly require ESG disclosures as conditions for market access and financing. The Global Reporting Initiative (2024) assessment of sustainability reporting in Bangladesh documents rising disclosure uptake among large exporters but also identifies persistent weaknesses in data consistency, assurance, and comparability—limitations closely tied to underlying accounting infrastructures.

Accounting Infrastructure Gaps and ERP-Based Integration

While ESG frameworks specify disclosure outcomes, a critical gap persists in the accounting infrastructure for generating sustainability data. Many organizations lack systems capable of capturing energy use, carbon cost allocation, or social expenditures at the transaction level, forcing reliance on estimates and manual reconciliation. These weaknesses are particularly pronounced in utilities and infrastructure projects, where capital intensity and long asset lifecycles require robust attribution mechanisms.

Configuring ERP financial modules—illustrated here with SAP FI/CO—to embed carbon-cost elements in cost centers and energy-related metadata in asset accounting provides a practical pathway for operationalizing ESG disclosure requirements within routine accounting processes (Cao et al., 2025; Dumitru et al., 2023). By aligning sustainability attributes with existing accounting objects, ESG data becomes subject to established controls, documentation standards, and audit procedures, strengthening regulatory assurance without creating parallel reporting systems.

Illustrative Scenario A: Utility Asset Posting to Regulator-Ready Emissions Reporting

To make the mechanism concrete, consider an illustrative utility scenario involving a BPDB-type thermal generation asset. A fuel purchase is posted in SAP FI against the relevant expenditure account and assigned to a plant cost center, while the associated generating unit is identified in asset accounting. At the time of posting, the transaction receives structured sustainability attributes: fuel type, physical quantity, unit of measure, facility code, and approved emission-factor reference. These values are then carried into a carbon or energy sub-ledger linked to the same cost center and asset identifier.

During period closing, the system aggregates fuel use and calculates emissions by asset, plant, and reporting period. A regulator-facing extraction layer packages the resulting values into a machine-readable reporting file, along with metadata on the calculation method, source-document keys, and posting dates. Regulator-side validation can then test whether the reported emissions reconcile with fuel purchases, reporting period boundaries, and asset-level activity data. In this configuration, an emissions disclosure is no longer a stand-alone estimate; it is a traceable derivative of routine accounting postings and approved calculation rules (Global Reporting Initiative, 2021; IFRS Foundation, 2023; Janssen et al., 2012; van Ooijen et al., 2019).

The analytical point is not that Bangladeshi utilities currently report in this way, but that ERP-native configuration would make such reporting institutionally plausible in sectors where cost centers, asset registers, and reporting controls already exist (Bangladesh Bank, 2023, 2025; Hawari & Heeks, 2010; Heeks, 2002).

Illustrative Scenario B: Banking-System Posting to Green-Finance Supervisory Reporting

A second scenario can be drawn from banking supervision. Consider an illustrative green-finance loan to a solar or energy-efficiency project. At origination, the facility is recorded in the bank's core accounting and loan systems and linked to product code, sector classification, customer identifier, approval history, and exposure amount. If the bank maintains an ERP-integrated sustainability tagging layer, the facility can also receive a structured green-finance classification linked to an approved internal or regulatory taxonomy.

At the reporting date, the system aggregates tagged exposures across product classes, sectors, and business units and generates a machine-readable supervisory return. Validation rules can test whether the green tag is consistent with the approved product category, whether the reported exposure reconciles to the loan sub-ledger, and whether late-stage reclassifications have occurred outside authorized workflow. This improves supervisory assurance by reducing reliance on manually curated sustainability templates and by preserving traceability from reported portfolio figures back to loan-level records (Bangladesh Bank, 2023, 2025; European Banking Authority, n.d.; OECD, 2021).

As with the utility illustration, the value of the scenario lies not in claiming empirical implementation, but in demonstrating how ERP-native disclosure logic can transform supervisory reporting from document submission into infrastructure-mediated verification.

Implications for Development and Analytical Scope

These illustrative scenarios clarify Bangladesh's analytical role in this paper. Bangladesh is not used here as an empirical test case, but as a policy context in which regulatory demand, uneven ERP maturity, and rising ESG disclosure pressure coexist. The case, therefore, serves as a bounded illustration of where ERP-native ESG oversight is most plausible: sectors that are already regulated, digitally administered, and dependent on auditable financial control systems (Bangladesh Bank, 2023, 2025; Geels, 2011; Heeks, 2002). The argument is therefore institutional and design-oriented, rather than a claim that cross-sector ERP maturity has already been empirically demonstrated in Bangladesh, based on the sources used here. In this sense, Bangladesh helps identify both the opportunity and the scope condition of the framework. The opportunity is that sustainability governance can build on existing accounting infrastructures rather than proliferating parallel portals. The scope condition is that this pathway is most viable where ERP adoption, supervisory leverage, and basic data governance capabilities are already in place.

Discussion

This paper advances sustainability accounting and digital government research by reframing ERP financial systems—illustrated through SAP FI/CO—not merely as operational or compliance tools but as institutional accounting infrastructure capable of embedding ESG accountability within routine financial processes. Rather than treating sustainability reporting as an external disclosure exercise, the framework positions accounting systems themselves as the primary locus for generating, governing, and enforcing ESG information. This discussion outlines the implications of this reframing for sustainability accounting theory, public-sector accountability, and regulatory design in emerging economies. It clarifies how the proposed approach differs from stand-alone and consultant-driven ESG reporting models.

Implications for Sustainability Accounting Theory

The primary theoretical contribution is a shift in analytical attention from disclosure outputs to accounting infrastructure. Much sustainability accounting research emphasizes indicators, reporting standards, and performance outcomes, often treating information systems as secondary implementation concerns. By contrast, this paper foregrounds ERP financial modules as the institutional sites where sustainability data are classified, attributed, controlled, and assured, reconnecting sustainability accounting with core management accounting concerns—classification, cost attribution, internal control, and auditability—identified in foundational ERP research (Granlund & Malmi, 2002; Scapens & Jazayeri, 2003).

The framework extends environmental management accounting (EMA) by embedding environmental and social attributes directly within ledger logic rather than treating them as parallel analytical overlays or post hoc calculations (Cao et al., 2025; Masanet-Llodra, 2006; Swalih et al., 2024). When sustainability variables—such as carbon costs or energy use—are recognized at the point of posting and linked to established accounting objects (e.g., cost centers and assets), they become endogenous to accounting processes. This shifts sustainability accounting away from symbolic or narrative compliance toward procedural accountability, where ESG information is subject to the same routines, controls, and reconciliation practices as financial data.

Institutional theory further clarifies this contribution. While global frameworks such as the GRI Universal Standards and IFRS S2 exert coercive and normative pressures on organizations (DiMaggio & Powell, 1983; Global Reporting Initiative, 2021; IFRS Foundation, 2023), substantive accountability depends on how these pressures are internalized within accounting systems. By positioning ERP configuration as the mechanism that translates institutional pressures into operational practice, the paper bridges sustainability accounting and socio-technical transition perspectives (Geels, 2002; Geels, 2011), explaining why reporting outcomes vary among organizations facing similar disclosure mandates.

Framed this way, the paper's theoretical contribution is not merely that ERP systems matter for sustainability reporting, but that they matter in specific and researchable ways. Proposition 1 links transaction-level embedding to auditability; Proposition 2 links traceable machine-readable reporting to regulatory enforceability; and Proposition 3 specifies that these effects are conditional on ERP maturity and regulatory capacity. The contribution is therefore a bounded theoretical account of how information architecture conditions ESG accountability outcomes (DiMaggio & Powell, 1983; Geels, 2002, 2011; Klievink et al., 2016).

Implications for Public-Sector Accountability

The framework has direct implications for public-sector accountability, particularly in emerging economies where regulatory capacity, audit resources, and enforcement capabilities are uneven. Public accountability depends not only on transparency but on the verifiability and traceability of reported information. When sustainability data are generated outside core accounting systems—through spreadsheets or stand-alone disclosure tools—regulators face persistent challenges in validating claims, reconciling ESG disclosures with financial statements, and enforcing compliance.

Embedding ESG attributes within ERP financial modules aligns sustainability reporting with established public-sector accounting controls in regulated sectors such as banking and utilities. ERP systems already structure budget execution, tariff calculations, asset management, and supervisory reporting. Extending these systems to capture sustainability attributes allows regulators to assess ESG performance using familiar audit techniques rather than bespoke verification processes. This is particularly important in utility sectors, where sustainability inefficiencies frequently translate into fiscal risks via subsidies, tariff adjustments, or capital transfers. The Bangladesh context illustrates how ERP-native sustainability accounting can support a co-evolution of regulation and market practice, shifting ESG oversight from episodic compliance toward embedded accountability.

Implications for Regulatory Design, Scope Conditions, and Limitations

For regulators, the framework implies a reorientation from proliferating disclosure portals toward infrastructure-based governance. Three design principles emerge from the analysis. First, sustainability semantics should be stabilized as close as possible to the point of transaction classification, for example, through ESG chart-of-accounts addenda, approved taxonomies, and standardized master-data fields. Second, attribution should occur through recognized accounting objects—such as cost centers, internal orders, asset records, and product classes—so that sustainability variables remain connected to financial responsibility. Third, regulator-facing reporting should be machine-readable and validation-ready, preserving traceability from reported values back to source transactions while allowing schema checks, plausibility testing, and exception-based supervision (European Banking Authority, n.d.; European Securities and Markets Authority, n.d.; Mohun & Roberts, 2020; OECD, 2021).

These implications should, however, be interpreted within clear scope conditions. The framework is most applicable in ERP-mature, highly regulated sectors such as banking, utilities, and large infrastructure organizations, where financial-control systems already structure compliance routines. It is less applicable in fragmented organizational environments where accounting remains distributed across spreadsheets, low-end software, or disconnected operational systems. The paper, therefore, does not claim universal applicability across all firms or all developing-country settings (Hawari & Heeks, 2010; Heeks, 2002; Huang & Palvia, 2001).

A first limitation concerns vendor dependence and system heterogeneity. Although SAP FI/CO is used illustratively because it clearly exposes ledger objects, controls, and reporting interfaces, many organizations operate Oracle, Microsoft, Finacle, local ERP variants, or hybrid landscapes. The conceptual mechanism should travel across platforms, but implementation costs, data models, extensibility, and audit affordances can differ significantly by vendor and configuration. Moreover, the use of ERP-native sustainability architectures may deepen lock-in if regulators implicitly design reporting logic around the affordances of large enterprise platforms. Future comparative work should therefore examine how the proposed architecture translates across non-SAP and mixed-system environments.

A second limitation concerns the political economy of infrastructure-based oversight. The framework assumes that organizations and regulators will welcome stronger traceability and more standardized supervisory visibility. In practice, however, infrastructure-mediated oversight redistributes informational power. Managers may resist greater internal visibility over energy losses, environmental expenditures, or green-finance classification decisions. Firms may also resist regulator access to more structured and auditable data if such access increases enforcement risk, narrows interpretive flexibility, or exposes inconsistencies between sustainability narratives and internal records. Regulators themselves may face incentives to preserve discretionary, document-based review rather than invest in more rule-bound and transparent infrastructures (Cordella & Paletti, 2019; Mohun & Roberts, 2020; OECD, 2021).

A third limitation concerns inclusion and proportionality. The framework is designed around ERP-mature entities, which means SMEs and less-digitalized firms are likely to fall outside its immediate reach. This is not a trivial side issue. If infrastructure-based ESG reporting becomes the dominant regulatory model, it could unintentionally privilege larger firms with integrated systems while imposing transition costs that smaller entities cannot absorb. A proportionate regulatory strategy may therefore require tiered obligations, phased adoption, shared reporting utilities, or lighter-weight digital templates for firms operating below ERP maturity thresholds (Hawari & Heeks, 2010; Heeks, 2002).

A fourth limitation concerns data sovereignty, confidentiality, and the risk of cross-border reporting. Machine-readable ERP-to-regulator pipelines increase comparability and validation capacity. Still, they also intensify questions about who controls sensitive operational data, where it is stored, which metadata are exposed, and how cross-border reporting or cloud-based ERP environments interact with domestic regulatory authorities. Even when regulators lack access to raw transactional details, structured reporting architectures may still reveal commercially sensitive operational patterns. For this reason, the framework should be read as requiring careful institutional design around access control, role separation, permissible transformations, retention rules, and legal authority over digital reporting infrastructures (European Banking Authority, n.d.; European Securities and Markets Authority, n.d.; Mohun & Roberts, 2020).

Finally, the framework remains conceptual and does not empirically assess implementation outcomes. Future research should test the propositions through comparative ERP cases, pilot reporting architectures, interviews with regulators and firms, and cross-country analyses of how institutional capacity, market structure, and platform maturity condition adoption. The framework's contribution is therefore best understood as a bounded theoretical and design-oriented account of how ESG enforceability can be strengthened through accounting infrastructure, not as a claim that implementation is frictionless or universally desirable.

Conclusions

This paper reconceptualizes ERP financial controlling systems—illustrated through SAP FI/CO—not as peripheral compliance tools but as sustainability accounting infrastructure capable of generating transaction-level, auditable ESG information within routine financial processes. Much RegTech and digital reporting research concentrates on digitizing reporting interfaces or automating downstream compliance checks. By contrast, this paper locates regulatory enforceability upstream in the internal accounting architecture through which sustainability data are classified, attributed, and made auditable (Mohun & Roberts, 2020; OECD, 2021).

The analysis advances sustainability accounting scholarship by shifting attention from disclosure outputs to accounting infrastructure. By embedding ESG attributes directly within ledger logic, the framework extends environmental management accounting. It connects sustainability reporting to the core mechanisms of management accounting—classification, cost attribution, internal control, and auditability. Integrating institutional theory with socio-technical perspectives further clarifies how global sustainability disclosure standards become operationalized within organizational accounting systems in emerging-economy contexts.

From a digital government perspective, the framework demonstrates how regulators can strengthen ESG assurance while simultaneously reducing reporting burdens. By leveraging authoritative ERP-based accounting systems, regulators can stabilize sustainability semantics through ESG chart-of-accounts extensions, establish controlled provenance through carbon and energy attribution linked to accounting objects, and enable machine-readable regulatory submissions that support automated validation and traceable auditing.

The Bangladesh context illustrates how digital finance reform and sustainability governance may co-evolve in emerging economies. In sectors where formal accounting systems and supervisory reporting structures are already in place, fragmented sustainability data infrastructures still constrain regulatory oversight and comparability. Treating ERP systems as public-interest accounting infrastructure, therefore, offers a practical pathway from compliance-driven sustainability disclosure to more scalable, credible, and enforceable ESG accountability.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

AI Disclosure Statement

The author used generative AI tools only for language refinement and structural editing; all substantive arguments, analysis, and interpretations are the author's own.