Abstract

This article assesses an overview of the media industries in North America after 20 years of NAFTA, 1994–2014. The study addresses three research questions: (1) How have the communications acts been reformed: according to which logic and with what objectives? (2) How have the communication regulatory bodies performed? (3) To what extent has concentration on the media and telecommunication industries increased? It explores these issues from a structural historical analysis to understand how the media systems in North America have been re-shaping in the three countries (Canada, Mexico, and the United States) during the last 20 years, focusing in three observable paths: Media policy reform and policy-making; the performance and leeway of the regulatory institutions; and the level of concentration in the three countries in media and telecommunications sectors.

Keywords

Introduction

The North American Free Trade Agreement (NAFTA) has raised concerns with many people: politicians (both conservative and progressive), labor unions, environmental groups, non-governmental organizations (NGOs), intellectuals, academics, and even with interested industries in the affected countries. This is for three main reasons: (1) the economic inequalities among the three countries (Canada, Mexico, and the United States (US)) and its regions, particularly with Mexico and the loss of jobs in the US, (2) the asymmetrical bilateral relations with the US as a super power and dominant economy in the world, and (3) the agreement articulates the integration of North America solely under the logic of a free market, in opposition to the European Union or Mercosur models.

The issues related to the communication and cultural industries were very questionable as well (Galperin, 1999; McAnany and Wilkinson, 1995), particularly in the case of Mexico, because it included cultural and communication products in the agreement between Mexico and the US—we have to recall that the Canadians applied the cultural exception clause 1 (Mosco, 1990). At the same time, the NAFTA framework has invited criticism, apart from plurality and diversity issues, concerning the idea of articulating the media systems under the logic of a free market and whether this frame could generate and guarantee plural public sphere and cultural diversity by itself (Crovi, 1995; Guevara Niebla and García Canclini, 1992; Mosco and Schiller, 2001).

Twenty years after this agreement, this article re-visits the criticisms of NAFTA and analyses the implications of the free market logic, particularly with communication industries in the three countries. To accomplish this objective, three main research questions are formulated as points of entry to establish how NAFTA is re-shaping the media systems in the region: (1) How have the Communications Acts been reformed: according to which logic and with what objectives? (2) How have the communication regulatory bodies (such as Canadian Radio-television and Telecommunications Commission (CRTC), Federal Communication Commission (FCC), and Cofetel/Ifetel) performed? (3) To what extent has concentration on the media and telecommunications industries increased?

The article aims, therefore, to establish the different particularities of NAFTA's members and to consider how the three signatory countries have addressed the communication industries in relation to the balance between public power and corporate capital (Golding and Murdock, 2000). In other words, how has NAFTA structured the social relations of power in the communications sector (Mosco, 2009) during the last 20 years? This article addresses this research from a structural historical analysis (Wasko, 2004).

In addition, it is important to note that comparative studies can be classified as ‘case-oriented’ or ‘variable-oriented’. In the first case, it seeks to adopt a historical/institutional type approach with emphasis on the differences of the cases presented, while the second focuses its analysis on the similarities and tries to present generalizations (Imbeau et al., 2000). This article adopts the two approaches because it could provide a broad and critical overview of the issues posed in the research, and to a certain extent, link them with a structural analysis. Nevertheless, the research is aware of the possible problems implied by including both analyses.

In the same historical trajectory of NAFTA, the process of convergence (Murdock, 2003) has challenged and changed both the design of communications policy (Van Cuilenburg and McQuail, 2003) as well as the dynamics of production, distribution, and circulation of the communication services and their consumption in multi-screen, multi-platform, and mobile scenarios (Hesmondhalgh, 2013).

At the same time, note that this article understands NAFTA as a significant accelerator and tool of the marketization process (Murdock and Wasko, 2007), particularly in relation to public communication policies and provides inputs for how these free trade agreements structure global communication and the cultural field under the conditions where the hegemonic transnational industries could continue growing in accordance with global capitalism. Is it central to say that the free trade agreements are just one component, albeit a central one, of the complex economic relations among the three countries and the world economy.

Thus, NAFTA generates a complex system and dialectical system of observation (Gómez, 2012) for thinking conceptually and practically about the problems, struggles, inequalities, and contradictions of global capitalism, where the Global North and Global South are in continuous tension.

Overview of NAFTA and its members

Since NAFTA took effect in 1994, there have been a number of disputes, and different sectors of the three countries have complained about different issues. In addition, economic interdependence has grown, while investment and migration flow among the three countries have increased (Fernández-Kelly and Massey, 2007). Above all, there has been rising economic interdependence between the US and Canada and between the US and Mexico, while the Canada-Mexico trading relationship continues to be of little significance (Weintraub, 2004).

Another important issue to establish is that the Mexican administration was a key player in the design of the agreement, because they strongly believed that this agreement could modernize the Mexican economy (Gómez, 2007). In this regard, Fernández-Kelly and Massey (2007: 101) point out ‘that NAFTA's architects are found on both sides of the US-Mexican border.’ Another remark to underscore is that after 11 September 2001, the security demands changed the bilateral relations between the US and Mexico, particularly in relation to borders and immigration (Coleman, 2007). At the same time, Canada changed its immigration policy for Mexico in July 2009 restricting the entry of Mexican citizens to Canada without a visa.

During the last 20 years, commodities, capital, and companies have had comparatively free access to each country. However, the US governments permit neither free exchange of labor nor free transit for Mexican citizens, even though the US relies heavily on Mexican labor. Meanwhile, Mexico's rural base has been undermined by prohibitions on subsidies during a time when crime-related drugs and violence displace vast groups of people. This issue has motivated an important flux of people northwards in the last two decades as the number of Mexican migrants, with or without papers, has reached at least seven million—the Mexican government says 12 million of its citizens reside in the US (Consejo Nacional de Población (CONAPO), 2012).

The marked inequalities among the three NAFTA members may not be surprising, particularly in socioeconomic terms. For example, while the 2012 per capita Gross Domestic Product of the US was $51,703 dollars and Canada was $47,708, in Mexico it was barely $10,058 dollars. 2 In the same vein, if we review the human development index of the United Nations Development Program (UNDP), Mexico is ranked 58, while Canada and the US are in the 11th and 3rd places worldwide, respectively (UNDP, 2013).

In the case of Mexico's progress, NAFTA has clearly been inefficient in addressing its long-run development goals: 40% of its population lives in poverty and well below its estimated potential economic growth rate (Hufbauer and Schott, 2005: 3). This performance contrasts with the important economic development and growth that have been experienced in the same period of time in other Latin American countries like Argentina and Brazil.

The objective of the Mexican administration under President Carlos Salinas (1988–1994) was that NAFTA would accelerate the modernization of Mexico by means of private investment, both national and foreign, to create a large number of sources of jobs and developmental improvement. Thus, NAFTA can be thought of as an accelerator of the structural changes promoted in Mexico since the beginning of the 1980s based on neoliberal policies, 3 orchestrated by the US administration and endorsed by the Mexican government and its business elites (Gómez, 2007). It should also be indicated that this frame of reference includes resistance, struggles, and tensions within and among different social agents in the three countries.

In terms of its media systems (Hallin and Mancini, 2004), Canada and the US have been characterized by a liberal model. Canada has been identified as one of the most progressive systems in the world in the orbit of the liberal model and the US is clearly the example of that model (Hallin and Mancini, 2004). Mexico has been identified under the guidelines of the clientelism model (Hallin and Papathanassopoulos, 2002) in the context of emerging democracy (Hughes and Lawson, 2004).

NAFTA's background: Cultural exception and digital integration

The focus here is on communication and cultural policy which, before the signing of NAFTA, created intense and significant debates in Mexico. This was mainly because the Mexican government did not resort to the cultural exception clause that the Canadian government had incorporated into the Canada–US Free Trade Agreement (CUSTFA) 5 years before (Mosco, 1990: 46). Therefore, the Canadians were able to protect, partly, 4 their communication and cultural industries, excluding them from the free flow of commodities and investments. For Canadians, ownership and control of media have been thought of as key to cultural sovereignty and cultural identity (Tremblay, 1992).

Vincent Mosco understood the CUSTFA as a discourse. That is to say, ‘in itself, it is a cultural product with visions and a language that reflect the culture of American capitalism. Essentially, the FTA is a cultural export from the US to Canada, which, if successful, will be exported to other countries’ (Mosco, 1990: 45). In this regard, it can even say that it is precisely from this perspective that this article understands some of the problems, distortions, and contradictions that have weighed on NAFTA after 20 years. In addition, it could be read as the naturalization of the free market culture as normative in the three countries.

Returning to the Mexican government regarding the possibility of a cultural exception, it did not display a special interest in struggling for the exception because, according to its vision, the millenarian Mexican cultures and identities were sufficiently solid to withstand any foreign cultural infiltration, especially that of the US. In addition, the Mexican government believed that having a different language would serve as a natural barrier (Lozano, 2006; Wilkinson, 2006). In contrast, the Mexican academic and intellectual sectors warned that the agreement would include provisions that could directly endanger the capacities of Mexico to defend, consolidate, and promote Mexican cultural identity and a sense of nationhood (Crovi, 1995; Guevara Niebla and García-Canclini, 1992). At the same time, they argued that NAFTA could present a genuine opportunity if the government was willing to take the democratic challenge to build a plural media system. This would involve the possibility of having a public broadcasting service (Toussaint, 1993), breaking the television monopoly of Televisa, fostering competition (Sánchez-Ruiz, 1995) and changing professional journalism practices in the country (Adler, 1993).

In addition, the copyright requirements in NAFTA were problematic as they addressed cultural intellectual property from an Anglo-Saxon law's liberal logic (Guevara Niebla and Garcia Canclini, 1992). In contrast, the dominant players in the telecommunications and media in Mexico did not oppose NAFTA. In fact, they strongly supported the government reforms and every single FTA that Mexico has signed since then. At the same time, discussions and debates about the possible negative implications of NAFTA in Mexico were not covered by the principal media, especially by Televisa, the major television group and audience leader. This issue clearly showed the lack of plurality of voices in Mexican television in those years and the necessity of transforming that system to shape a democratic public sphere (Toussaint, 1998).

The winners after 20 years of increased audiovisual flows involving the signatory countries are the big conglomerates in the US, some Canadian audiovisual producers (Tinic, 2010), and Mexico's Televisa and TV Azteca, that import large quantities of US audiovisual content and sell content in the US to the Latin@ TV networks (Gómez et al., 2014).

In terms of digital terrestrial television (DTT) standards, the North American region adopted the US technology, Advanced Television System Committee (ATSC), as its digital standard; Canada and the US achieved their digital television transitions in 2011 and 2009, respectively. In the case of Mexico, the transition is expected to be complete by the end of 2015.

Additionally, despite the fact that all three countries have been governed by different political parties both right-wing conservatives—conservative republicans, and national action party (PAN)—and centrist liberals—labor, democrats, and institutional revolutionary party (PRI)—during the last 20 years, none of them have challenged, inhibited or even adjusted the free market logic, at least, in the communication and cultural policies.

Media policy in North America

During the last two decades (1994–2014), the communication acts in the three countries have suffered important market-driven (Gómez, 2007; Horwitz, 2005; Skinner et al., 2005) re-regulations (Murdock, 1990). From the article's perspective, two main processes furthered those changes. First, neoliberal policies have driven the marketization of the communication and cultural sectors (Murdock, 2003). Second, but closely related, digitization sets up possibilities for the re-organization of the radio electric spectrum, while the Internet opens possibilities for interaction among broadcasting, telecommunications, and information in terms of production, distribution, and consumption. Nevertheless, we have to say that even if we could maintain this generalization in the three countries regarding the prominence of the interactions among the processes of structuration (Mosco, 2009), marketization, and convergence, there are some specificities with the different logics and interactions of the political systems, media systems, media policy traditions, and political cultures of each country. In that regard, it has to be said that the three media systems are complex and multivariable (Raboy and Taras, 2004; Sánchez-Ruiz, 2001).

Canadian media policy and the centrality of the CBC

In the case of the Canadian media system, this is articulated from the core of its public broadcasting service, Canadian Broadcasting Corporation (CBC), and is characterized as a mixed model where a strong public service coexists with nine privately owned media conglomerates (Raboy and Taras, 2004; Winseck, 2011). As we know, this media system has two major languages: English and French. While the Quebec province is one of the principal promoters, in terms of cultural diversity and positive content regulation in media policy, Canadian regulation includes a significant contribution from the Canadian independent audio-visual production sector (Lozano, 2006).

In terms of communications policy, Canada has strong provisions to protect its media system. For example, the federal government has exclusive jurisdiction in communications, and broadcasting outlets must be owned and controlled by Canadians. At the same time, its communication policy-making is considered to be one of the most open in terms of discussions, participation, transparency, and accountability (Raboy and Taras, 2004). These achievements make Canada an important reference in terms of best international practices in communication policies. Nevertheless, even with the strong normative perspective, provisions, and participatory policy-making by Canadians, some scholars have argued that its communication policies have been guided, little by little, toward a market-driven and corporate logic since the 1990s (Regan, 2005; Rideout and Reddick, 2001; Schultz, 2003).

A key change in Canadian communication policies, in that respect, was altering the rules related to cross-ownership, which was implemented by the ‘Convergence Policy Statement’ in 1996. That statement gives telecommunication carriers the ability to hold broadcasting licenses on its competition chapter. This amendment in the Bell Canadian Act and Telecommunications Act opened the door to important mergers that have fostered attention on the Canadian Communication System. At the same time, this reform allows these entities to own newspapers challenging the plurality of the news outlets (Skinner et al., 2005).

In 2012, the Canadian government announced a further important potential change, raising the current limit for foreign investment in small telecommunications operators, which was previously set at 47.6% (Economic Action Plan, 2012).

Another indicator that we need to be reminded of, in the logic of market prominence as a public policy, is that during the last two decades, the cuts in terms of funding to CBC had been significant in value, particularly in the last years. For example, from 2012 to 2014, the CBC had lost over $115 million in funding by the cuts of the federal government (Drimonis, 2014).

US communication policy and ‘fin-syn’ rules 5

In the case of US communication system and its communication policies, there have been major changes, qualitatively speaking, during the last 20 years that have modified this complex system in different ways. As in the Canadian case, the media cross-ownership regulations have been reduced over time, and this is the main change that is re-shaping the US communication system in terms of concentration, consolidation, competition, and diversity (Freedman, 2006; Horwitz, 2005; McChesney, 2004). However, at the same time, the emergence of Spanish Language Media (Piñón and Rojas, 2011) must be underscored as an important subsystem of US communication system. In fact, while the traditional networks ABC, CBS, and NBC and their audiences are decreasing (Lannett et al., 2011), the number of Spanish language television media and Latino/Latina audiences are increasing. On the one hand, this is mainly a result of the growing Hispanic population in the US and its respective purchasing power as well as its political weight in elections (Dávila, 2012), and on the other, because the US communication system is fragmented by the options of different digital platforms that offer audiovisual contents to the English-language audience-users (Lannett et al., 2011).

Since NAFTA, communication policies in the US have been reformed and important rules have been rescinded. First, the Telecommunication Act was issued in 1996 which rules communications in the US. This act was designed with a clear impromptu of market-driven logic, and with the principal mandate to foster competition. In that respect, ‘the act eliminated the legal basis for protected monopoly in telecommunication and encouraged mergers and vertical integration to facilitate what's termed “cross-platform” competition, that is, competition between previously separate industries to provide the same service…’ (Horwitz, 2005: 30). An example of this is the 2003 FCC recommendation to increase the national broadcasting ownership cap from 35% to 45% of the total audience (Horwitz, 2005). In this regard, the FCC eliminated some media ownership rules by the end of 2007, including a statute that forbids a single company to own both a newspaper and a television or radio station in the same city (FCC, 2007).

Referring to the US re-regulation process since the change of the fin-syn rules in the 1980s and its consolidation with the 1996 Telecommunications Act, Robert McChesney has argued that ‘Deregulation has led to the worst of both worlds: fewer enormous firms with far less regulation. To top it off, the political power of these firms in Washington and state capitals has reached Olympian heights’ (2013: 210–211). It is important to underscore the large amount of money spent by telecommunications companies on lobbying in Washington DC. This is a key concern that has been increasing during the last 20 years as Crawford (2013) and Freedman (2008) have documented.

Another aspect to highlight is the issuance of the Local Community Act of 2011 because it runs opposite the commodification of the communication policies. It is important to point out that this change resulted in part to the prominent role that the Free Press organization and other social agents are playing in the policy-making process of the communication policies in the US, as a counter balance to the structuralization process under the dominance of free market and corporate logic. However, this aim of the civil society is marginal, if it is compared with the growth and consolidation of corporate media, thanks to re-regulation in the last 20 years.

Mexican media policy and the vulnerability of emergent democracy

The Mexican communication system since NAFTA has maintained and reinforced the power of the dominant players. In the TV sector, Televisa and TV Azteca are a duopoly, and in the telecommunications sector, Telmex 6 is the dominant player by far in the Internet, mobile, and fixed telephone services. This configuration generates ‘telecom wars,’ in the context of convergence and public institutional reform, mainly between Televisa and Telmex (Gómez and Sosa, 2013).

Mexico has also made significant reforms in its communications policies during this period. The 1995 Federal Telecommunications Act is a clear example of re-regulation (Murdock, 1990) built upon the neoliberal logic, distinguished by its technical nature, giving priority to the logic of the free market and without social commitment from the public service (Gómez, 2007). Its focus was promoting private national, foreign investment evidenced by the re-regulation accepting 50% of foreign investment and to foster investment in the pay-TV subsector (Casas, 2006).

Another important adjustment in this period was the controversial reforms to the Federal Radio and Television Act and to the Federal Telecommunications Act in 2006. The need to modify the Radio and Television Act of 1960, in effect up to that time, was imperative for the Mexican communication system. However, the bill, approved by the Chambers of Deputies and Senators, contained various omissions, and in particular, continued to respond to the needs of the Mexican TV duopoly—Televisa and TV Azteca. In fact, the bill was known as ‘the Televisa Act’ (Esteinou and Alva de la Selva, 2009). By contrast, the elements excluded from the amendments were the access to licenses for community media, the inclusion of public service provisions, and ownership concentration safeguards and caps. At the same time, during the amendments, there was a lack of inclusion and participation of civil society organizations (for a thorough discussion, see Esteinou and Alva de la Selva, 2009).

In 2013, after a competitive presidential election in 2012, the emergence of students’ social protest for the democratization of communication (Guillén, 2013) and the return of the Institutional Revolution Party (PRI) to the Mexican presidency, the federal government, in alliance with the three major parties, signed a pact that fostered many ‘structural modifications’ under the name of Pact for Mexico—Pacto por México. In the case of the telecommunications sector, in June of 2013, the constitution was amended following the pact. Those reforms it could be highlighted as follows: (a) Raise or eliminate limits on foreign investment: they allow foreign broadcast firms to have as much as a 49% stake and give blanket permission for total foreign ownership of all telecommunications and satellite TV services—with a clause of reciprocity. (b) Compromise to launch two new tenders for national digital television networks in 2014 and to start to operate in 2016. (c) Include broadcasting licenses to community and social actors. (d) Create a new national public broadcasting system. (e) Have ‘convergence’ licenses: voice, data, and broadcasting. (f) Lastly, launch new constitutional independent regulatory commission (Instituto Federal de las Telecomunicaciones (IFT)) following the guidelines of the FCC in the US, with the power to unilaterally punish non-competitive practices, including corporations’ licenses. The new independent commission is able to order firms to sell off assets to reduce their market dominance, which was established as 50% of the market share by sector.

After a difficult process of lobbying in the chambers, the new Act was issued in July 2014. In retrospect, the reform did not succeed in addressing all the issues facing media industries particularly in: (a) community media, because of the marginal conditions it holds; (b) there is not equitable treatment of/by the main dominant players in the broadcasting and telecommunication sectors; (c) the public service Act, as it does not establish public service provisions in terms of autonomy; and (d) there is not support for independent audiovisual producers, among other controversial issues (see further details at Trejo, 2014).

Regarding the conditions in which the re-regulations of the cited Acts were carried out, two main aspects must be highlighted: the economic centrality from which the amendments were prepared and the power of lobbying by large media companies—especially Televisa and TV Azteca—within the legislative chambers, the federal government, and the political parties. These reforms also took place leading up to major election cycles.

The Mexican case has set an example of a second generation of the commodification of communications policies. This is illustrated by the new Act of 2014 that mandates (a) a convergent Act that has to consider the idea of a convergent license—data, voice, and broadcasting contents—and (b) setting a cap for telecommunication and broadcasting sectors' market share at 50% without cross-ownership restrictions. However, it is important to underscore that the constitutional reforms show a slight positive improvement in Mexico because it finally tackled some concerns and issues that were avoided in the past and certainly, could help re-organize the Mexican communication system.

The role of regulatory agencies: CRTC, FCC, and Federal Telecommunications Institute (Cofetel/IFT)

The regulatory bodies in the three countries are important independent institutions that govern or have the legal authority to regulate and supervise their communication systems with strong safeguards and regulatory power. In the case of the CRTC and FCC, they have been historical international referents in this matter. In the case of Mexico, the Federal Telecommunication Commission (Cofetel) and the new IFT are starting to have centrality in recent years, but it is still in a young stage in terms of transparency, accountability, and autonomy on a practical level.

One aspect that has to be underscored is the intrinsically associated relationship between the market and regulatory trends, which sets the context within which these agencies operate. The regulatory challenges faced by the agencies are related to the rapid process of convergence that is taking place between media and telecommunications. Such convergence presents new regulatory challenges that are difficult to grasp. For example, the debates about net neutrality in the United States were specifically focused on whether Internet Service Providers (ISPs) should be reclassified and treated similarly to telecommunications providers. These challenges are intertwined with broader market trends toward concentration, consolidation and cross-ownership, which is a global tendency within telecommunication, information services, and content providers (International Telecommunications Union, 2014).

Because of this key role in their communication systems, these agencies have been at the center of debates for their decisions in the last two decades. In particular, resolutions related to accepting significant cross-ownership mergers, takeovers, and joint ventures in the three countries have been crucial. In many ways, those resolutions continue to re-shape their communication system towards both concentration and commodification.

In what follows, it will be present major examples of how the three regulatory agencies have performed in front of important mergers, takeovers, and joint ventures or general resolutions, for the purpose of analyzing some challenges that the agencies have faced during the last 20 years.

CRTC and the convergence of the media and telecommunications markets

In the case of Canada, the most controversial decisions of the CRTC were to accept the acquisitions or mergers of important Canadian Communication Groups, for example (1) the acquisition of Canadian Television Network (CTV) and the Global and Mail by Bell Canada Enterprises (BCE) in 2000 ($3.4 billion); (2) the purchase of Vidéotron, Téléviseursassociés (TVA) and the Sun ‘Media’ newspaper chain by Quebecor ($7.4 billion) between 1998 and 2001; and (3) the purchase of Western International Communications ($800 million) in 1998, the Hollinger newspaper chain and the National Post ($3.2 billion) in 2000, and Alliance Atlantis ($2.3 billion) by Canwest with the support of Goldman Sachs in 2007 (Winseck, 2011: 151–154). The other main players in the private Media and Telecommunications sector are Rogers Communications, Telus, and Shaw. With these mergers or purchases since the change of the ownership rules in 1996, the Canadian Communication system has become controlled by privately owned media conglomerates marked by horizontal, vertical, and cross-ownership integration that includes radio and TV stations, satellite services, cable operations, magazines, and newspapers. Furthermore, Winseck (2011: 152–158) has clearly established how this acquisition and concentration process is related with the financialization of the communications industries in Canada with the complacence and approval of CRTC.

In favor of the CRTC, it has to be said that the trends in regulation and the convergence policies during the mid 1990s allowed or opened the door in many ways to accepting merger decisions. However, there are specialists that argue that there could be more safeguards or disinvestment conditions in those resolves because the Canadian communication system has experienced high levels of concentration nationally and in many regional and local markets (Sullivan and Beaty, 2003; Winseck, 2011). Finally, still related to CRTC, it is significant to highlight its decision to deny the BCE control of Astra Media, because in some ways, it restrains the expansion of BCE. Consequently, in some sense, this CRTC resolution (CRTC, 2012) could be seen as a contentious warning to the big Canadian conglomerates.

FCC and the Comcast dilemma

In the case of the FCC, the Comcast-NBC/Universal acquisition decision is by far the most controversial example in the US. For many academics and specialists, from different fields and political approaches, the merger represents a step back for the US communication system and particularly for the FCC, because it allowed a big telecommunications carrier to concentrate many communication services in detriment to users–consumers–audiences and could undermine the quality of internet services, and could also generate barriers of entry to new players in different media and telecommunications subsectors (Crawford, 2013; Lannett et al., 2011; McChesney, 2013).

The case of Comcast/NBC could be established as paradigmatic, because by international standards, it is one of the global examples that it is closer to accomplishing ‘total convergence.’ At the same time, the acceptance of the merger of Comcast-NBC/Universal is just one of many cases that follows the FCC's tendency to allow cross-ownership conglomeration, especially if we review the different takeovers, mergers, and acquisitions during the last 20 years (Hesmondhalgh, 2013: 191–2). Susan Crawford pointed out that ‘Comcast is the communication equivalent of Standard Oil. It is a mammoth enterprise… considering a media and entertainment colossus with sweeping power to decide what Americans watched and read’ (Crawford, 2013: 5).

If we review the major players of US communication systems, we could confirm how the historical TV networks and Hollywood major firms are part of the most profitable global communication conglomerates (Hesmondhalgh, 2013: 193). In this part, it is important to say that this circumstance and decision allow US communication industries not just to grow nationally and locally, but these mergers have global implications that give more muscle, scope, and scale to perform globally in hegemonic terms to those firms. Furthermore, it has to be underscored that the FCC resolutions do not just have national implications; these have to be read at global scale.

We have to recall that the major tool to allow mergers and acquisitions was the issue of the Telecommunications Act in 1996 in the context and logic of NAFTA and WTO policies related with communication and cultural services such as General Agreement on Trade in Services (GATS) and Trade-Related Aspects of Intellectual Property Rights (TRIPS) (Freedman, 2006). However, the Act requires that the FCC review its media ownership rules every four years to determine ‘whether any of such rules are necessary in the public interest as a result of competition’ and to ‘repeal or modify any regulation it determines to be no longer in the public interest’ (Telecommunication Act, 1996). There is no doubt that these corporate activities are risky or could fail on their own terms, because as we know, some media conglomerates have collapsed or broken up since 1994. The issue here is that the regulator allowed several vertical, horizontal, and cross-ownership concentrations and those decisions were detrimental to public interest and the entrance of new players and the quality of services (Crawford, 2013; McChesney, 2013).

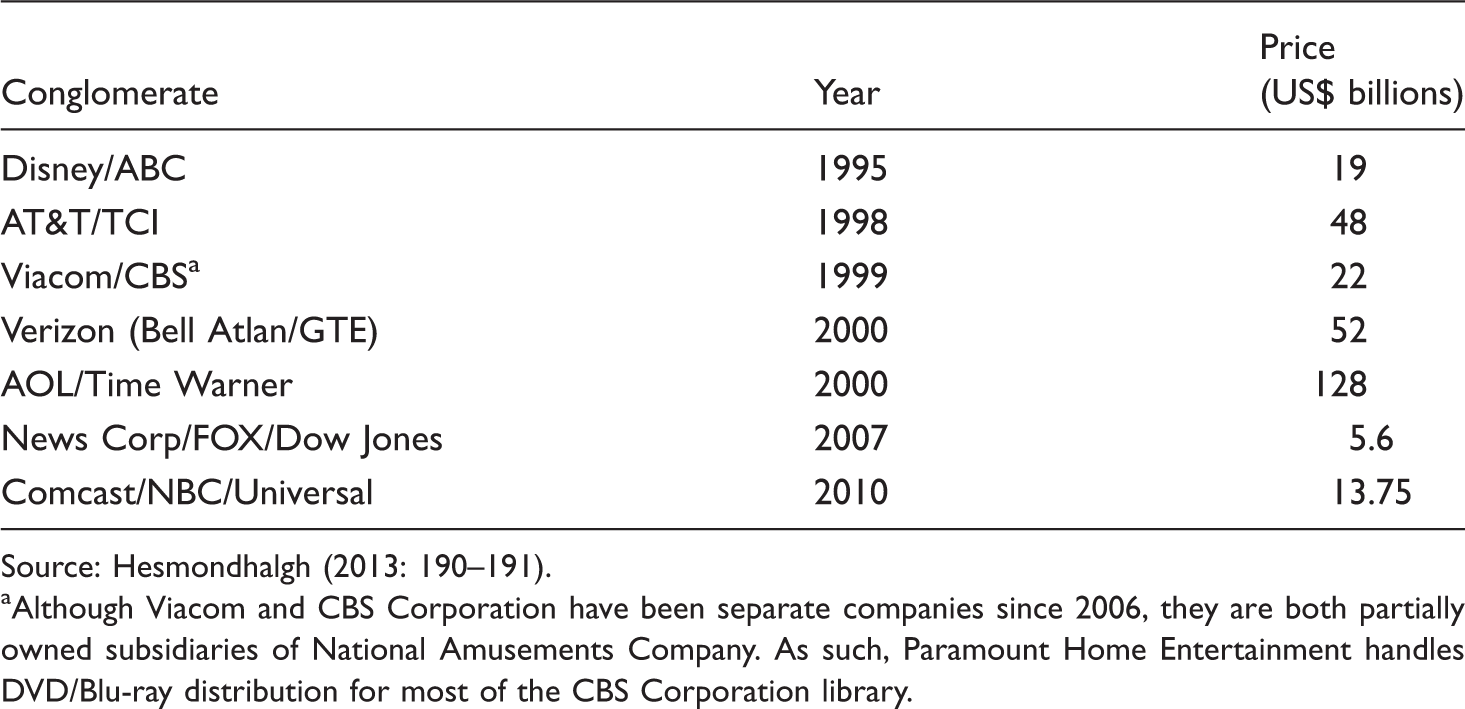

In favor of the FCC resolutions, it has to be remembered that they decided to block a proposed purchase of T-Mobile (fourth largest operator) by AT&T (second one) in 2012. However, from some points of view, there was no doubt it would be rejected, because it was a clear horizontal merger, and would harm competition and would not be in the public interest (FCC, 2011). However, with the antecedent of Comcast/NBC, there were doubts about the resolution of the FCC. This example gives an opportunity to clarify and recognize the important and complicated role of the FCC and these agencies in their resolutions. At the same time, it is well known that these decisions are not simple or easy. The argument that the article wants to claim here is that the crucial resolutions in the last 20 years have been in favor of the big players as the evidence shows (Table 1).

The Mexican young regulatory institutions in front of the media and telecom giants

In the case of Mexico, we have to add another entity to recall a controversial example in terms of mergers or alliances because, before the constitutional amendments of 2013, the regulatory body that evaluates the economic media mergers and alliances was the Federal Commission of Economic Competence (Cofeco).

Cofeco accepted in June of 2012 the alliance between Televisa and TV Azteca in the telecommunications company ‘Iusacell,’ whereby Televisa purchased ($1.6 billion) half of the company, TV Azteca, its ‘rival’ in the TV sector. The first resolution for this alliance was rejected by the agency in January 2012 but, after an appeal by Televisa, 6 months later, the antitrust agency changed its decision to allow the joint venture.

The concerns against this joint-venture alliance regarded competition and potential collusion in the free-to-air and pay-television markets, while acknowledging the benefits for competition in mobile-phone service. The move for Televisa in this acquisition was clearly to enter the mobile-phone subsector, get spectrum, and take advantage of the possible synergies to offer its audiovisual contents in that platform. Cofeco, in accordance with Federal Commission of Telecommunications (Cofetel) and Ministry of Finance, approved the joint venture under certain conditions (Cofeco, 2012). The big issue here was that Televisa kept growing in every market in the media and telecommunications sectors. Televisa is Mexico‘s largest television broadcaster with four TV networks, four cable TV units—that offer triple play services—making it an audiovisual content powerhouse, which also owns the country‘s largest satellite TV service (Huerta-Wong and Gómez, 2013).

During the last 20 years, the Cofetel clearly started to have, little by little, some presence in the organization of the sector as a young institution, but because of digitization and its economic implications, the agency became more visible since the mid 2000s and with the new agency, IFT in 2013, it is expected to increase its role in the re-configuration of the Mexican communication system in the next years. At the same time, its performance is a test in relation to the democratization, mainly in terms of accountability and autonomy from the federal government and economic agents. The biggest challenges are forthcoming, after IFT declared Telmex and Televisa as dominant agents in their respective markets in March of 2014, it could finally boost competition, and the entrance of new players and investments are expected—a possible positive circumstance for competition in the Mexican communications industries.

Concentration in North America: A convergent path

The landscape of North American communications industries has experienced important levels of concentration in the three countries since 1994. However, this progression has had highs and lows in some subsectors, from moderately concentrated to highly concentrated, according to the Herfindahl Hirschman (HHI) and Concentration Radio 4 (CR4) indices. These methods of measurement were chosen because they give a clear picture of time in economic standards, on the one hand, and because they were used as reference by the regulatory bodies as an indicator or tool to evaluate and compare their markets, on the other.

In Canada, nine companies are growing in size and scale both nationally and regionally. The big US conglomerates have not stopped growing in vertical, horizontal, and cross-ownership and are the leaders in the top 10 global communication industries (European Audiovisual Observatory, 2014). The dominant Mexican players have maintained and expanded their supremacy and control. Both Televisa and Telmex dominate the national markets and they are leaders in their respective Iberoamerican markets (Mastrini and Becerra, 2011).

In this part, is presented some results on the standard concentration indices, HHI and CR4, of the three countries to show the concentration progression during the last 20 years, particularly in Canada and the US. In the case of Mexico, it is important to remember that the fixed telephone services and open-air TV was operated by monopolies, Telemex until 1995 and Televisa until 1993, respectively. This structure reflects the highest levels of concentration in those markets (Figures 1 and 2).

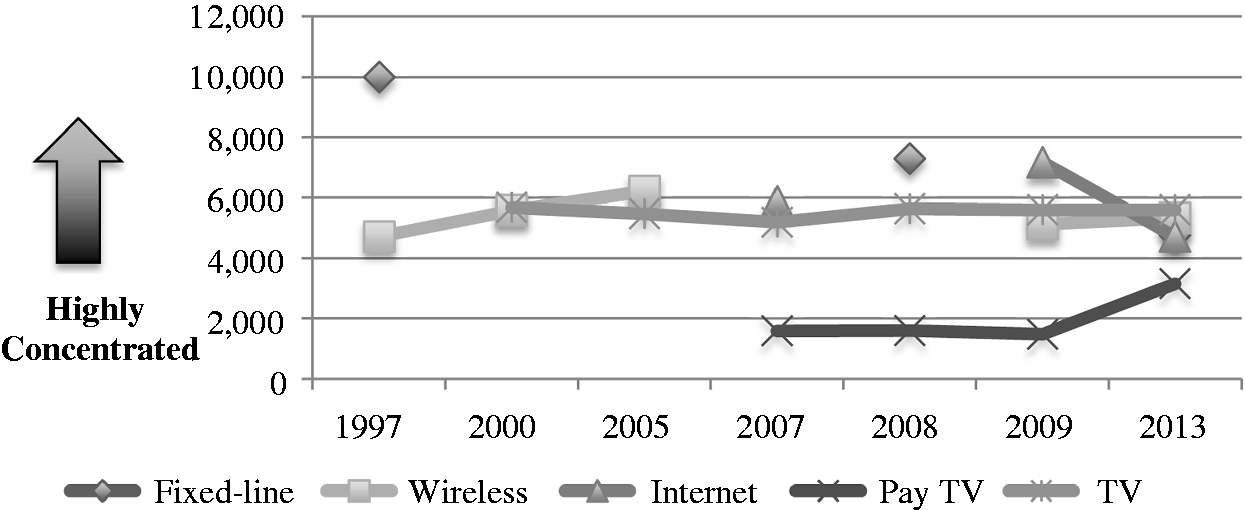

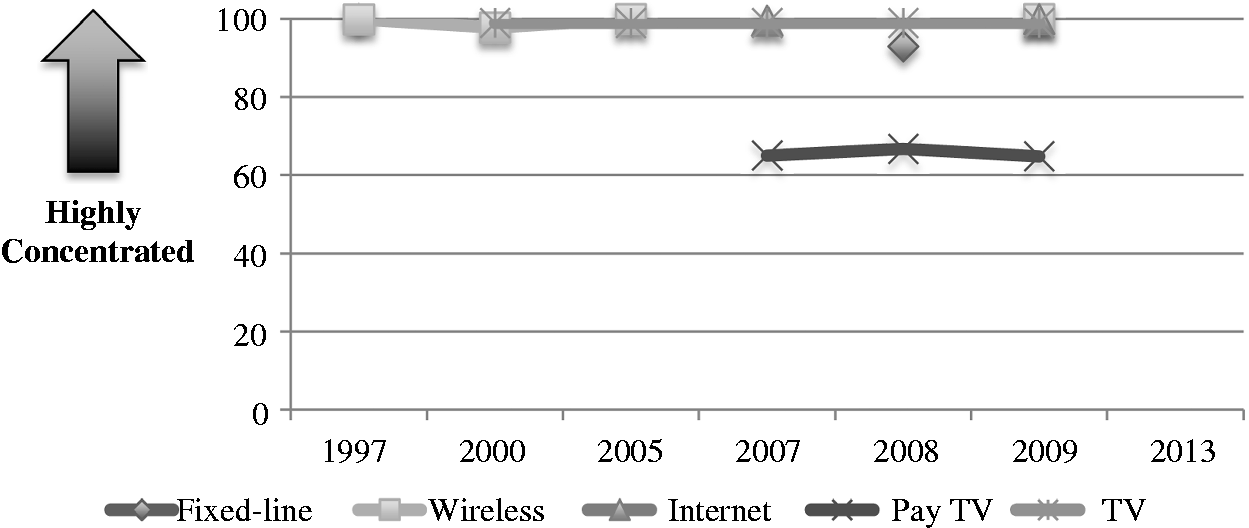

HHI Index Mexico 1997–2013. Source: Huerta-Wong and Gómez (2013: 125,129,138, 142). CR4 Index Mexico 1997–2010. Source: Huerta-Wong and Gómez (2013: 125,129,138, 142).

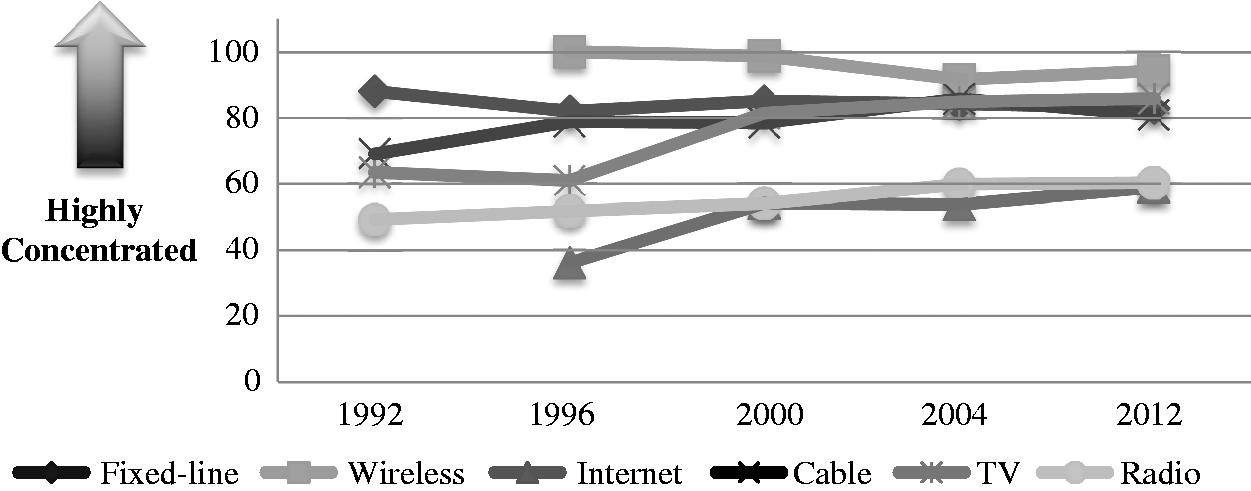

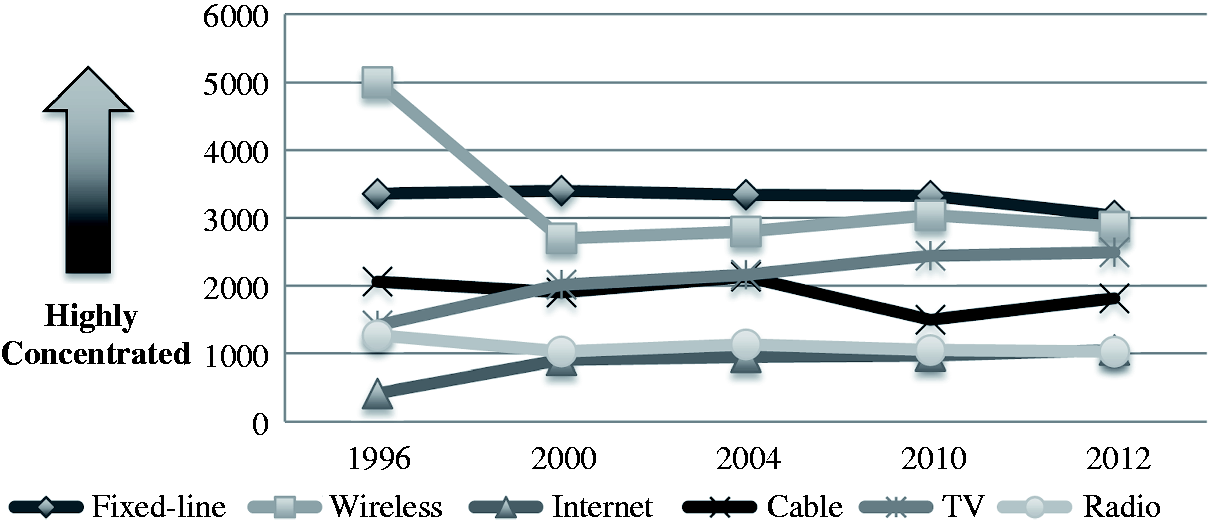

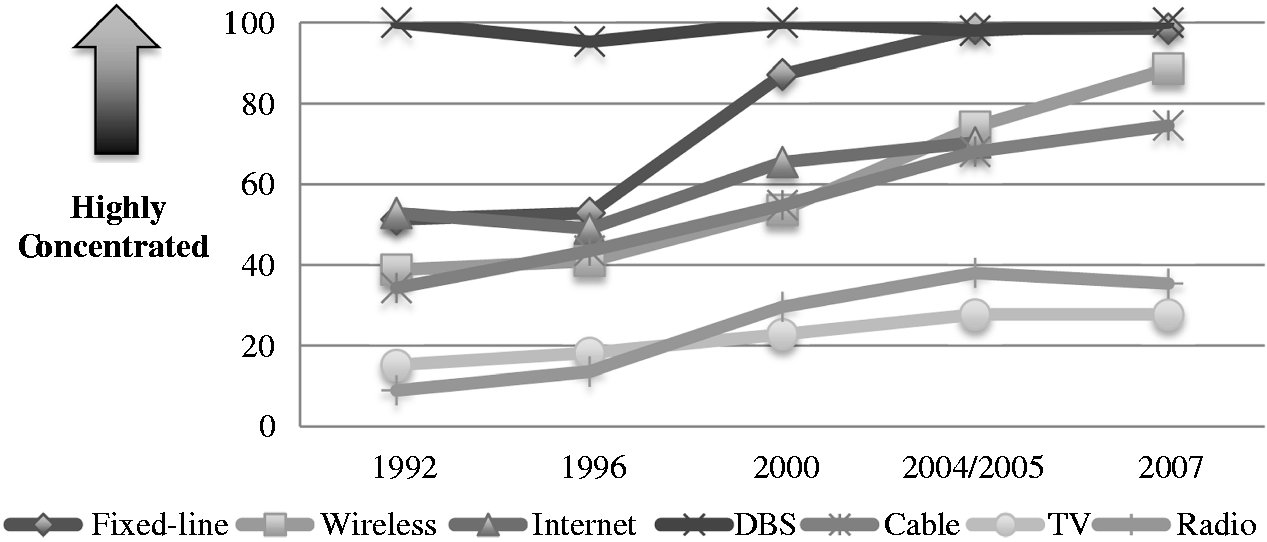

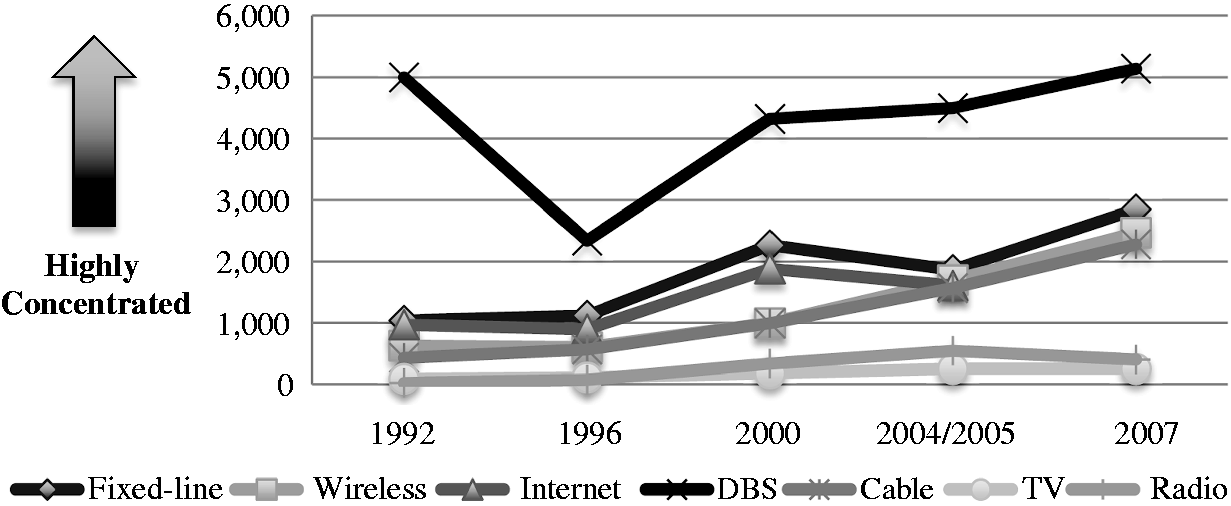

Thus NAFTA, for the Mexican Communication system, provides the possibility to start and experience some grades of ‘competition’ in those markets, or at least that was the discourse of the NAFTA proponents. In the case of Canada, according to the Winseck data, the tendency towards media and telecommunications concentration is clear during the last 20 years (Winseck, 2011: 157). In fact, it could be observed that the wireless, fixed phone, and TV markets are the most concentrated (Figures 3 and 4), particularly in the CR4 index, that tendency is acute (Figure 3).

CR4 Index Canada 1992–2012. Source: Winseck (2011: 152) and CMCRP, 2013. HHI Index Canada 1992–2012. Source: Winseck (2011: 152) and CMCRP, 2013.

The US media and telecommunications market concentration results (Noam, 2009: 251, 298, 304) reflect less concentration in comparison with their two neighbors, but its own historical progression shows the increase of concentration as clear, sharp, and constant (Figures 5 and 6), particularly in the radio, internet, fixed-phone lines, and pay-TV markets. In the last five years, Clear Communication, Verizon, and Comcast are the emergent players in their respective subsectors and the big five—Disney, News Corp, Viacom, Time Warner, and Comcast/NBC (still in a consolidation process) (Winseck, 2011).

CR4 Index US 1992–2007. Source: Noam (2009: 251, 298, 304). HHI Index US 1992–2007. Source: Noam (2009: 251, 298, 304).

In the case of Mexico, the levels of concentration are too high and the TV, pay-TV, wireless, Internet, and fixed telephone lines markets have dominant agents. Televisa controls the TV subsectors and Telmex, the other three. In this regard, the alleged positive effects of the free market related with competition, better services, lower prices to consumers and the assumptions to have more players, and thus, a plural ‘marketplace of ideas’ are not happening in these Mexican markets after 20 years of NAFTA. The subsectors that have been experiencing some relative changes in terms of competition during this period are the newspapers, radio, and pay television. Nevertheless, pay television has experienced, in recent years, several acquisitions by Televisa (Huerta-Wong and Gómez, 2013).

The evidence suggested by the concentration indices presented, that at least during the 20 years of NAFTA, is that there are no signs of de-concentration of the communication and telecommunications markets in the three countries. The results indicate that free market logic has not helped in having a diversity of sources, even though it is clear that more than ever, there are more channels and contents, but they are concentrated in a few hands. This structure has implications particularly in terms of ‘influence on our thinking about their operations, about all other industries and, indeed, potentially, about all aspects of life’ (Hesmondhalgh, 2013: 31).

Final remarks

As the article has established, Canada, the US, and Mexico have relaxed their communication ownership rules in the last 20 years. In particular, the re-regulations of the Telecommunications Acts in the 1990s have been the major tools in that direction, and at the same time, clearly reflect the free market logic that was institutionalized by NAFTA in those years. In fact, North America after 20 years, as a region, is a clear example of the marketization of communication policies on a global scale. Nevertheless, this general appreciation has particularities in the three countries.

The three regulatory entities have been under pressure dealing with big issues and resolutions during the last 20 years, regardless of mergers, acquisitions, and alliances. The research just highlights the major resolutions to illustrate the complicated trends and significant roles that are affecting these agencies to regulate and organize their communication systems in the three countries. At the same time, to a greater or lesser extent the lobbying power of the major media and telecommunications players and the politics of the media policy (Freedman, 2008) are important variables that are affecting any resolution related to the agencies in the three countries. These conditions relegate or, at least, put citizens and civil society advocates in a disadvantageous position to influence both policy-making and regulatory resolutions.

Within these disadvantageous circumstances, however, many activist groups, citizen collectives, NGOs, and individuals have raised their voices more than ever to try to confront the neoliberal logic as a way to participate in the policy-making process of communication policies and regulation. These groups have the potential to offer alternative narratives and perspectives, especially through the use of new media spaces and social media. During the 20 years of NAFTA and, particularly since 2009, there are examples that are challenging the governments, congresses, regulatory entities, and transnational companies to try to counterbalance the social relations of power at play in three communication and political systems. Nevertheless, these movements remain largely marginalized in their efforts to effect structural change.

In terms of concentration, it is clear that media consolidation has been experienced in the region. At the same time, the financialization process occurring in the communication industries together with concentration must be underscored. These national monopolistic and oligopolistic market conditions allow the dominant communication companies to have better circumstances to compete at a global level, especially the US companies as the hegemonic global audiovisual producer and powerhouse distributor. In the case of the Mexican dominant players, concentration gives the possibility to be the leader in audiovisual content in the Hispanic geo-linguistic zone, in the case of Televisa, and the telecommunications leader in Latin America with convergent and global aspirations, in the case of Telemex. The concentration in Canada is re-drawing its communication system in terms of undermining its rich and solid public broadcasting system as a key entity.

To summarize, this article has shown how the free market (NAFTA) logic is prevailing in the three countries in their communications policies, and after 20 years of this rationality, North American communication systems are more concentrated, its regulatory entities have less leeway to resolve public interest goals, and the different communication conglomerates are growing both in economic and political power. At the same time, the structural condition pushed forward by the marketization process that is leading the convergence process is naturalizing this rationality as the hegemonic idea to shape the communication and cultural systems.

Major communications industry mergers and acquisitions 1994–2014 in US.

Source: Hesmondhalgh (2013: 190–191).

Although Viacom and CBS Corporation have been separate companies since 2006, they are both partially owned subsidiaries of National Amusements Company. As such, Paramount Home Entertainment handles DVD/Blu-ray distribution for most of the CBS Corporation library.

Footnotes

Acknowledgement

I would like to thank Ben Birkinbine to his comments and English editing.

Declaration of Conflicting Interest

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Fulbright-Garcia Robles Research Grant from 2013-2014, and Conacyt Estancias Sabáticas 2013-2014.