Abstract

The rapid growth of the internet in China has been propelled by the Chinese government’s push to develop the country’s information infrastructure and its tight control over the internet. The most recent stage of internet development in China, however, has been driven by a three-way dynamic between the State, internet companies, and international finance capital. This relationship has yielded three internet giants—Baidu, Alibaba, and Tencent—that stand at the apex of the internet economy in China. They also rival their US counterparts like Google, Facebook, and Amazon, on several key measures. We examine annual reports and other financial documents to better understand these three companies’ character as ‘capitalist enterprises’ and the tight nexus that links them to international investment banks, venture capital funds, and other foreign investors. While these processes are now fundamentally shaping ‘the Chinese internet’, they have not yet been adequately explored in the scholarly literature, we argue.

Keywords

Introduction

Chinese internet companies have witnessed a meteoric rise in the past decade. In terms of revenue, the size of their user base, and stock valuations, three such companies—Baidu, Alibaba, and Tencent—have risen to the apex of the internet economy in China. By the end of 2016, these three internet giants were offering a vast range of online services to over 700 million internet users in China. On at least some measures, as this article shows, they now rival the ‘big six’ US-based internet giants: i.e., Google, Facebook, Apple, Amazon, Microsoft, and Netflix. Baidu, Alibaba, and Tencent have also been traded on stock markets since the early 2000s, and while still only one-half to two-thirds the size of their US counterparts based on market capitalization, their ownership, control, revenue, growth, and the very fact that they are listed on the New York Stock Exchange (Alibaba), NASDAQ (Baidu), and Hong Kong Stock Exchange (Tencent) at all, reveal their growing clout as well as their international and financialized character.

This is important because while the internet in China, as is well-known, is locked up behind the Great Wall, there is another side of this story that has been relatively neglected: namely, that the big three Chinese internet companies are also thoroughly integrated in the world economy in terms of the structure of capital, ownership, and control that stands behind them. While there is no doubt that the rapid growth of Baidu, Alibaba, and Tencent—and the internet overall—in China has been propelled by the government’s massive push to develop the country’s information/internet infrastructure, its protective information industry development policies, and the extraordinary policing, monitoring, and censoring powers that it has delegated to all internet companies operating in the country (Hong, 2017; Jiang, 2012), we also need to take stock of the fact that, first and foremost, these companies are ‘capitalist enterprises’ and tightly integrated with a variety of sources of international finance capital. To illustrate these points, this article draws on and analyzes the ‘Big Three’ Chinese internet companies’ annual reports and other financial documents that they have filed with Chinese financial market regulators and the Securities and Exchange Commission in the United States. It also draws on existing scholarship 1 as well as business news and data sources to provide a systematic and reasonably comprehensive view of the ‘big three’ Chinese internet firms along a handful of dimensions: (1) their operating profits, (2) how mergers and acquisitions have underpinned their expansion into new markets, (3) the rapidly rising debt that has come along with their ‘expansion-through-acquisition’ strategy, (4) the more concentrated market structure of the internet economy in China that has arisen because of these trends, and (5) the greater role of finance capital—domestic and international—in these companies’ ownership, control, and operations.

Ultimately, the upshot of our analysis is that the fortunes of Baidu, Alibaba, and Tencent not only depend on the heavy hand of the Chinese state in China, as per common understandings that are well-established in the literature, but increasingly on finance capital from abroad—by which we mean investment banks, venture capital funds, and other institutional investors. As we show, to better understand the Chinese internet, we must grasp not just the tight relationship between the state and business but the emergent three-way ties between the state, internet companies, and finance capital. This triangular relationship is fast becoming the pivot upon which the political economy of the internet in China turns. These linkages between finance capital and technology tightened considerably just as the commercial internet took off within China. Similar processes have been a feature of financial bubbles, crashes, and crises historically, including during the dot.com crisis that coincided with the commercial take-off of the internet in the Anglo European capitalist democracies (see, for example, Perez, 2002; Hodgson, 2015; Schumpeter, 1943/1996; Fitzgerald, 2012). Whether similar patterns will come to pass in China, however, it is too early to tell. Regardless of how these specific concerns turn out, examining the pieces of the puzzle taking shape will help shed more light on the political economy of the internet in China and to compare what we find with developments and events elsewhere either way.

Rise of Chinese internet companies

China was first connected to the internet in 1987. The first email was sent by Qian Tianbai, a professor from the Chinese Academy of Science to Germany, and it expressed a certain optimism about the potentials that lay ahead: ‘Across the Great Wall, we can reach every corner in the world’ (CNNIC, 2012). Seven years later, China established its first international dedicated line to the internet and was the 71st country to register onto the global computer network (CNNIC, 2012). The Chinese government has had a strong hand in constructing the telecommunications and internet infrastructures upon which the internet depends through various public policy and national development plans. The Informatization of the National Economy Program and the government’s 10th Five-Year Plan were particularly important because they set out the strategic significance that digital technologies were expected to play in national development (Dai, 2002). The rapid expansion of telecommunication infrastructure, in turn, brought about the fast expansion of internet development, especially its popular and commercial development.

While the growth of internet users remained tepid throughout the 1990s, by the early- to mid-2000s that changed. An explosive phase of commercial development and popular growth ensued, with the number of internet users multiplying nearly 20-fold from 1998 to 2001, from less than 1.2 million to 26.5 million (Dai, 2002: 151). Although media reform and marketization was well under way by the 1980s and 1990s in many areas of the economy, the commercialization of media and telecommunications accelerated when China joined the World Trade Organization in 2001. The Chinese government made several reforms at the time to comply with Western market norms, such as the promulgation of self-regulation rules for internet companies, who were expected to conscientiously promote the commercial use of the internet while achieving greater transparency in terms of the services they offer (Weber and Jia, 2007). More importantly, the WTO liberalized telecommunication markets in China and relaxed foreign ownership rules. Foreign investors can now own up to 50% of value-added telecommunications services according to Article 6 in the Administration of Foreign-funded Telecommunications Enterprises Provision. The most profound transformation in this era, as Zhao (2003: 61) argues, is the commercialization of the media sector and its transformation into a platform for capital accumulation—regardless of the national origins of capital.

China now has the world’s largest internet population with 710 million users at the end of 2016—a penetration rate of 52% (CNNIC, 2016). With just over half of the country connected to the internet, China is already a lucrative market for internet companies with lots of room to grow. As Schiller (2005, 2008) observes, the scale of Chinese developments and initiatives in the manufacture and distribution of communication and information technologies, content and services contribute significantly to the ongoing reconfiguration of the political economy of transnational capitalism. More recently, upon examining the political economy of Chinese social media (Baidu, Weibo, and Renren) in comparison to their US counterparts (Google, Twitter, and Facebook), Fuchs (2016) argues that the logic of commerce, capitalism, and advertising dominates both Chinese and US social media alike. As Fuchs sees things, Chinese social media companies now stand on the frontiers of capitalist expansion in China and have become poignant symbols of the country’s massive economic upheaval and transformation in recent decades.

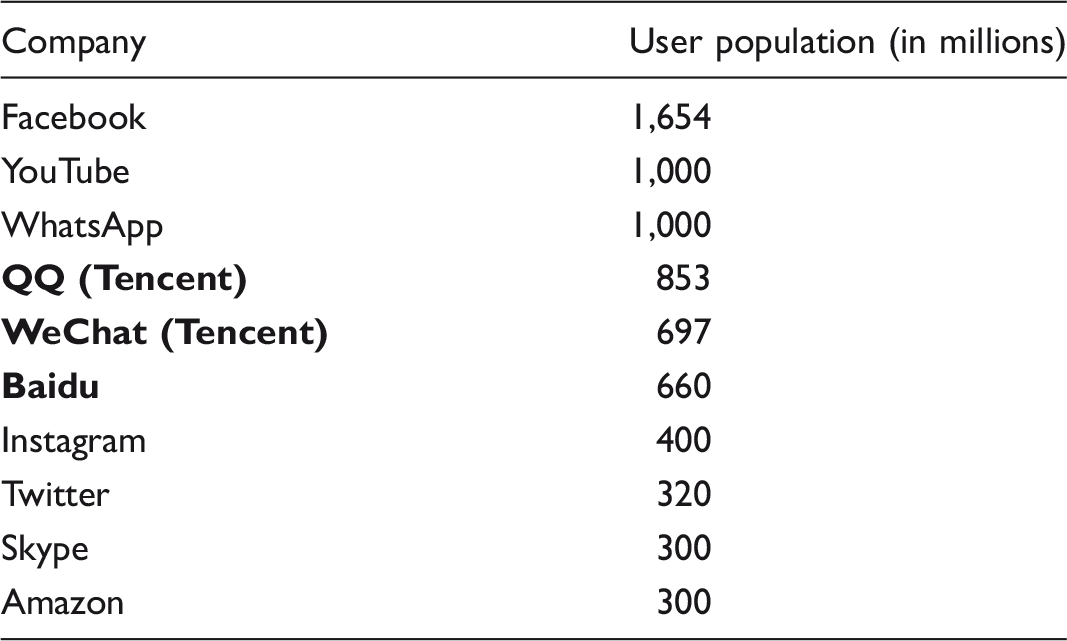

Top 10 internet companies in terms of user population (as of 2015).

Source: Compilation from company annual reports.

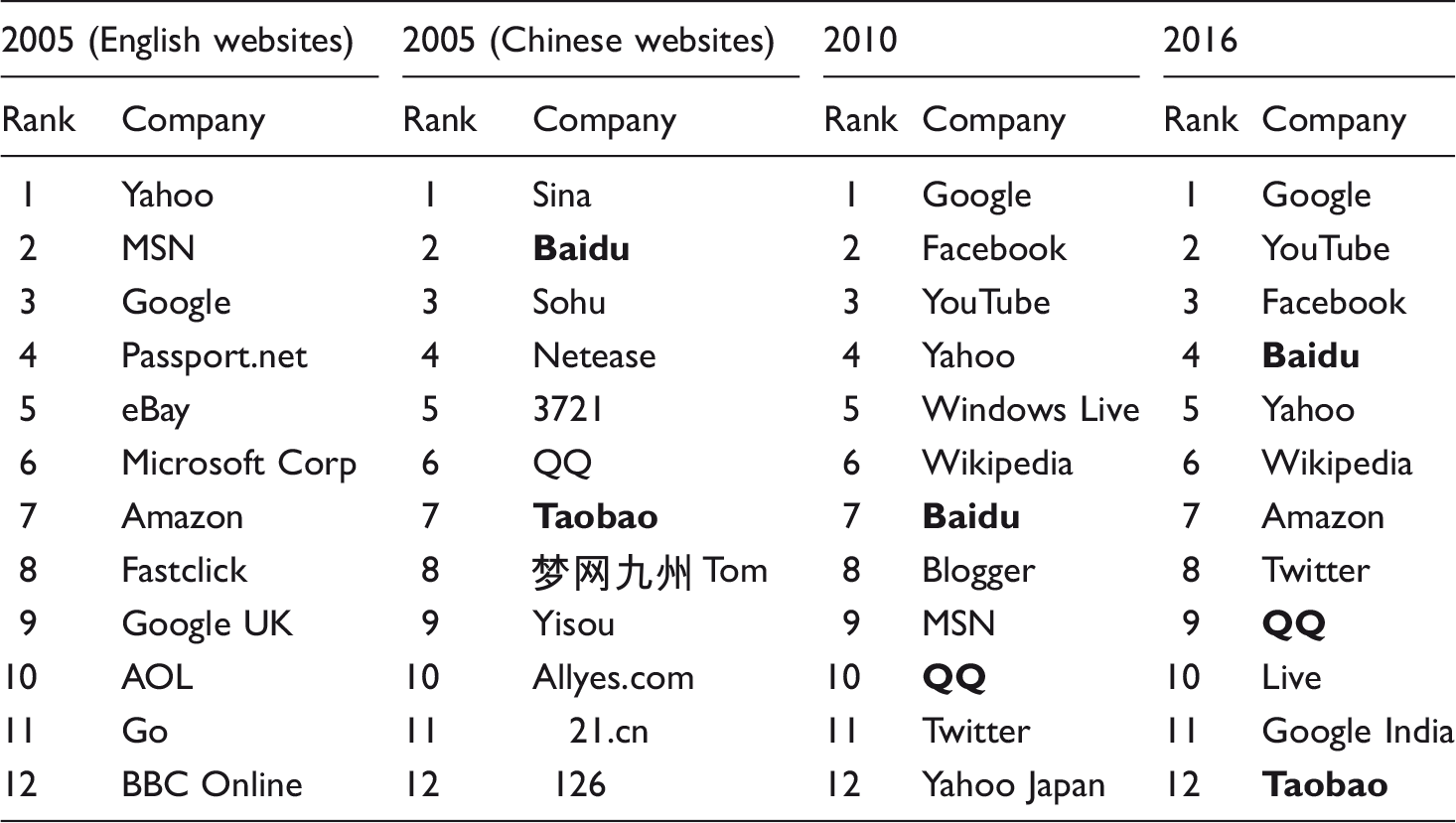

Top 12 internet companies by traffic, 2005, 2010, and 2016.

Source: Compiled from Alexa.

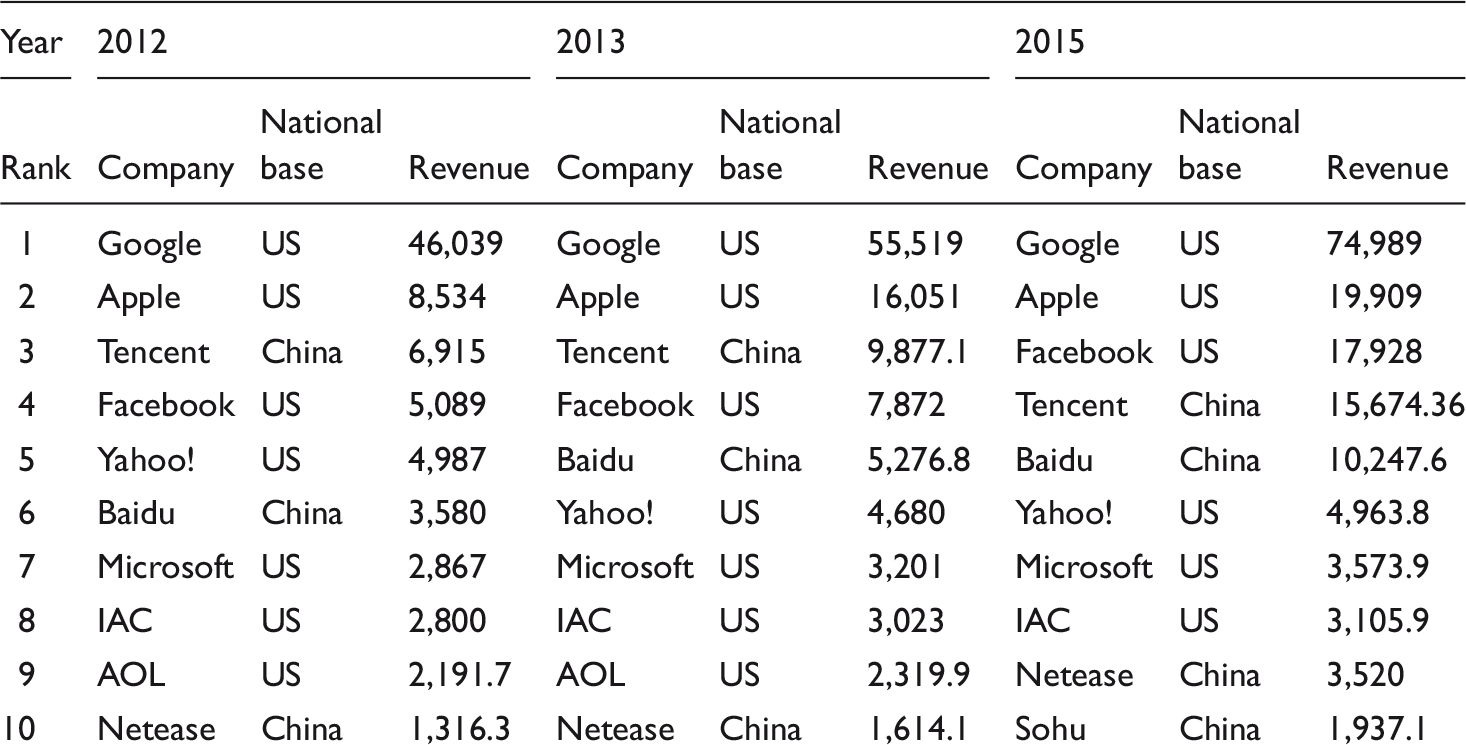

Top 10 internet companies by revenue (in million USD).

Source: Compilation from companies’ annual reports.

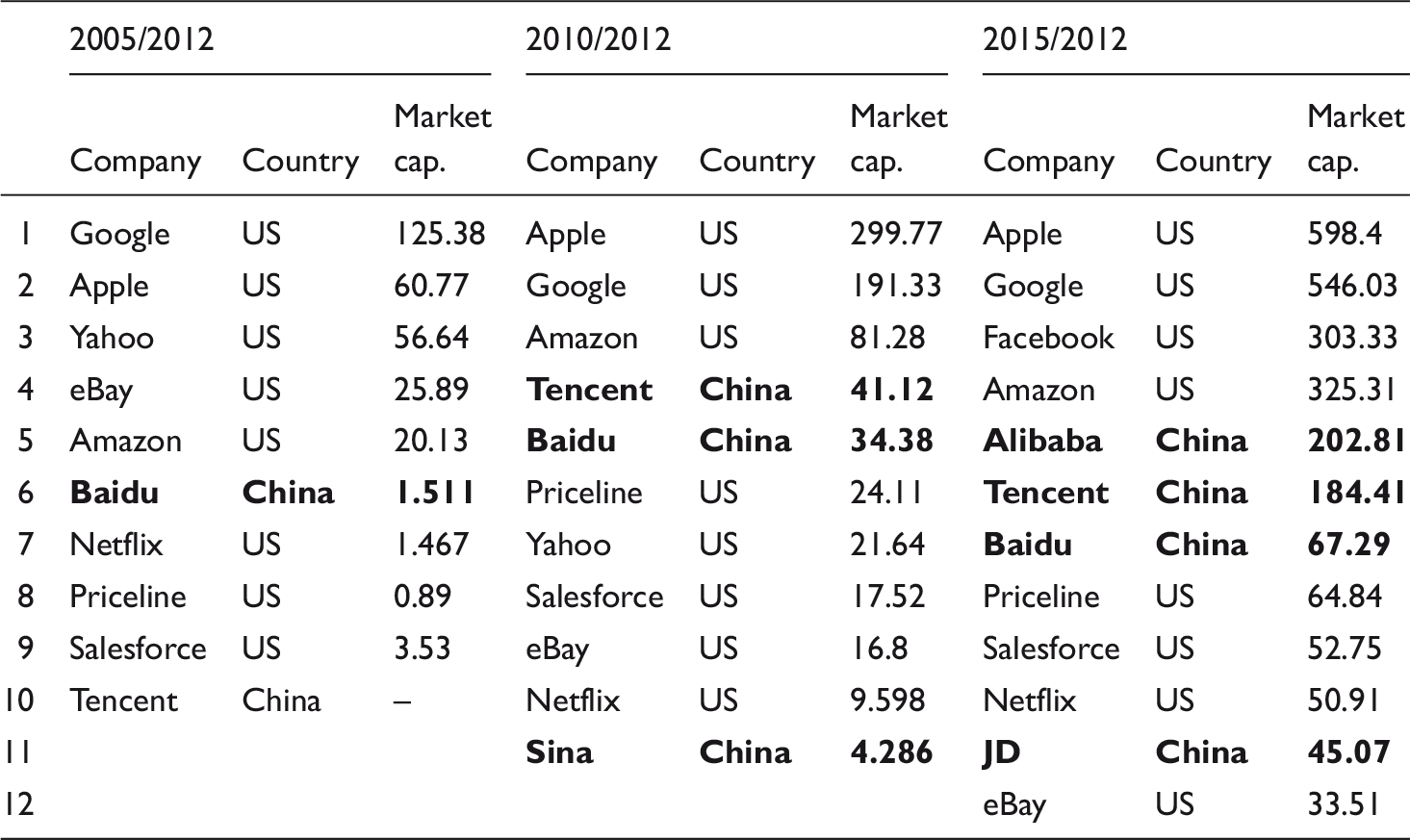

Top 12 internet companies by market capitalization (in billion USD).

Source: Compilation from companies’ annual reports.

Cap.: capitalization.

All of this is critically important because it shows that a handful of Chinese internet companies have emerged as some of the world’s top companies—not just in terms of user population and traffic but also revenue and market capitalization. Measured by these four metrics, Baidu, Alibaba, and Tencent are the ‘big three’ internet companies within China and amongst the top 12 such companies worldwide. Together, they challenge the US dominance of the commercial internet, with great potential to grow as the rest of the population becomes internet users. This also shows that the internet is becoming less-and-less US-centric as its locus shifts to other areas of the world, notably China and the rest of Asia, but also to the European Union and broader swathes of the Global South (Winseck, 2017). The largest Chinese companies will likely become a reference point for how others use the internet in the years ahead and for foreign internet firms that will likely come to mimic their business models. As a result, the private internet companies are shaping the evolution of the internet within China and beyond. Given this, they provide a crucial lens through which we can understand how economic forces can affect the evolution of new communication systems like the internet. On this point, we must always bear in mind that the media can never be understood without understanding the markets they operate in (Picard, 2008). The next section reviews some of the financialization literature and how that phenomenon has shaped the media industry generally and the Chinese internet specifically.

Financialization and the ascendant hegemony of finance

According to French economists Duménil and Lévy (2004), the rise of finance to its dominant, over-arching place in western capitalist economies can be traced back to the structural crisis at the end of the 20th century, when the rate of business profits had been steadily declining since the 1960s across Europe and the United States. Finance includes several major sectors (i.e., finance, insurance, and real estate, the ‘FIRE’ sectors) and the superior and active segments of the wealth owning and controlling classes. Financialization also denotes the extraordinary growth of the financial sector and financial assets relative to the industrial and other sectors of the economy over the past 25 years (Fitzgerald, 2012). These segments are also major owners of industry and assets (as creditors and shareholders). While typically not directly playing management roles at the ‘operational’, day-to-day level, financial interests wield ‘structural power’ because owners, equity holders, and creditors’ positions can give them a role on boards of directors where they can influence corporate policies and allocate resources in ways that affect companies’ activities over the long run, which markets they enter (or exit), the new technologies and services they pursue (or reject), their stance on government policy and legal measures, how many employees are maintained (laid off), and so forth (Duménil and Lévy, 2004: 208; Murdock, 1982).

Duménil and Lévy (2004) argue that financialization brings about a tight and hierarchical relationship between industrial capital and banking capital, basically elevating the latter while diminishing the former. The result is the hegemony of finance over business and industrial affairs. The liberalization of financial markets, the search for new modalities of capital accumulation, and efforts to reverse the declining rate of profit in the face of persistently low rates of economic growth are all enablers of the ‘rise of finance hegemony’, Duménil and Lévy (2004) state.

Duménil and Lévy (2004) also point out that the worldwide liberalization of capital exchanges and movements are fundamental components of financialization (9). William Milberg’s (2008) analysis further fleshes out the connection between the globalization of business value chains and financialization. Global value chains provide an opportunity for companies to reduce costs and derive profits from foreign input markets (421). In order to obtain higher returns on investment to realize shareholder values amidst a drawn-out phase of anemic economic growth, companies resort to two main strategies. First, they turn to the expanded global value chain to reduce costs. Second, given that the gap between the rate of return on manufacturing investment versus investments in financial assets is widening, businesses and investors have strong incentives to invest in finance rather than industry. Moreover, the profits obtained through cost-reduction do not get funneled back into investment in fixed assets and the ‘real economy’ but rather are used to pay dividends, for share buy-backs, and for merger and acquisitions. In this sense, heightened merger and acquisition activities reflect the processes of financialization and contribute to them as well. The result is the financialization of non-financial firms and of the economy in general.

The hegemony of finance institutionalizes its power in a variety of ways, including through ownership, boards of directors and by appointing executive managers. The result is an alliance, or fusion, of the interests of finance, ownership, and managerial elites (Duménil and Lévy, 2004: 17). As Duménil and Lévy (2004) also state, however, for capitalism to function well requires the harmonious and regular development of technological progress (which must concern capital and labor), steady wage growth, increased output, and productivity gains, and a growing workforce, as well as effective use of the institutional machinery of government to offset volatile swings in the economy (206). Financialization, on the other hand, tends to generate discordance between these activities. As business enterprises first and foremost, media firms are not only affected by financialization but also help to constitute such processes as well.

Financialization and media industry

The rapid development and commercialization of the media in China, including the internet, defined the 1990s and 2000s. With respect to the traditional mass media (e.g., television, newspapers, film, etc.), this was defined by increasing the role of the market and commercial forces, especially the role of advertising finance, while pushing the overt political role and agenda of the state more into the background. Thereafter, as the literature on Chinese media has well-established, the media were no longer yoked completely to a one-sided political and ideological agenda set by the state but forced to dance awkwardly between, as Zhao Yuezhi (1998) classically puts it, between ‘the party line and the bottom line’ (also see Hong, 2017; Jiang, 2012). The development of the internet was also similarly situated between these two poles, but given even greater weight in government policy because of its role as an infrastructural base for economic, political, social, and media development writ large (Hong, 2017; Jiang, 2012). In both cases, however, these processes were distinct from the processes of financialization that held sway in western capitalist democracies at the same time.

The role of finance and global finance networks in Chinese telecommunication and internet companies has only in recent years garnered scholarly attention. For example, Wójcik and Camilleri demonstrate how Chinese industrial policies and global financial networks 3 co-created one of the globally significant state-owned enterprises—China Mobile. Their study reveals how China Mobile, one of the world’s largest telecommunication companies in revenue and user population, was incorporated only weeks before its initial public offering, and consisted only of the assets of two regional mobile operators, and then sold successfully to international investors. They argue that American investment bankers and business service firms, with Goldman Sachs in the lead, played an indispensable and critical part in creating the company out of poorly managed assortment of provincial post and telecom entities and in selling the package to international fund managers as a national telecommunications giant (Wójcik and Camilleri, 2015). Wójcik and Camilleri’s study makes explicit the tight nexus between China Mobile and global finance network through detailed mapping of key actors involved. Fuchs (2015, 2016) has also examined systematically how logics of capitalism and commercialism have come to dominate internet companies in China by looking at the ownership structure, business models and strategies, products and services provided by several Chinese social media sites in comparison with their Western counterparts. A much more focused and detailed study of financialization and Chinese internet companies is conducted by Bingqing Xia and Christian Fuchs (2016). They note that Chinese internet companies are undergoing intense financialization as major internet companies are adopting acquisitions and investments as means to establish market domination. In particular, they argue that Baidu, Alibaba, and Tencent demonstrate characteristics of monopoly capitalism with their market dominance and acquisition of 75% of all successful start-up companies in the country and subsequently subsuming these companies under their pockets (Xia and Fuchs, 2016). They also highlight few key indicators of an internet bubble—the great divergence between profitability and the stock values of a handful of publicly listed Chinese internet companies—the stock value was 124.79 times higher than the average income (Xia and Fuchs, 2016). In such economic formation, Xia and Fuchs (2016) warn about the detrimental effects on productive capacity and the burden that falls on young workers. Hong (2017) also echoes the concerns about the increasingly financed character of Chinese internet economies and argues that Chinese government has gone the extra mile to legalize the overflow of transnational financial capital in controversial and restricted areas in her study of state-corporate relations of Foxconn, Qualcomm, and Alibaba.

According to Winseck (2011b), the telecoms, internet, and media industries were swept up in, and on the cutting edge of, the financialization of Anglo-European economies in the 1990s and at the turn-of-the-21st Century 4 (153). A key characteristic of this process, he observes, was a sharp spike in the number and value of mergers and acquisitions that swept the telecoms and media sectors from 1996 to 2000 and again, albeit more modestly, from 2003 to 2007 (150). These merger and acquisitions created huge media conglomerates and siphoned off profits into the financial market instead of, for instance, plowing them into investment in new technologies, content, and services, or in other words, the core functions of the media business that were needed more than ever to survive amidst the generalized upheaval brought about by the growing ubiquity of the internet, mobile connectivity, and digitization. Moreover, mergers and acquisitions came at the price of huge debts that had to be sustained (and paid back) amidst faltering economies. As the reality of protracted economic stagnation came crashing in, however, those debts often proved unsustainable. Thus, when the dot.com bubble burst in the early 2000s, of the $7 trillion reportedly lost at the time, $2 trillion could be laid at the feet of telecoms companies (Starr, 2002). The list of companies that failed, were broken up, or scaled back dramatically as a result is long indeed: e.g., AT&T, Adelphia, Bertelsmann, Canwest, Hollinger International, MCI Worldcom, Time Warner, Vivendi, etc. The vast ramping up of market capitalization and debt, followed by either the collapse of some companies or a steep loss of market capitalization for others, revealed the precarity of the forces of financialization and, in several cases, the outright folly of pursuing its dreams and dictates (Winseck, 2014).

Fitzgerald (2012) further develops this kind of analysis in relation to three major global media companies, notably Time Warner, Bertelsmann, and News Corporation. His analysis links macro- (transformations in the history of capitalism) and micro-level considerations (the inner workings of media enterprises). He argues specifically that three separate shifts characterized the financialization of the media industries: Firstly, the increasing centrality of financial institution as corporate shareholders; second, the extensive use of debt to finance growth and acquisition and the increasing salience of serving debt in corporate decision making and; third, the rise of a ‘financial’ conception of corporate assets in which the corporation is seen as a ‘portfolio’ of liquid subunits that must be continually restricted to maximize the share price. (391)

While the internet and broader information and communications technology revolution promised a new epoch of economic growth, and to revitalize democracy, the great paradox of the 21st Century has been that neither promise has come to pass. Instead, economic stagnation and what Schiller (2014) calls ‘digital depression’ have become the new norm while democracy is in retreat. Foster and McChesney (2011) similarly observe that the global economy has continued to stumble along at historically low rates of growth (or none at all), wealth inequality has grown starker, and people, while tweeting and uploading photos and videos to Facebook and Google more than ever, have become growingly disillusioned with democracy. In other words, the crises of capitalism have also begot a crisis of democracy.

The financialization of ‘the Chinese internet’? Analyzing the political economy of Baidu, Alibaba, and Tencent—The ‘BAT’ companies

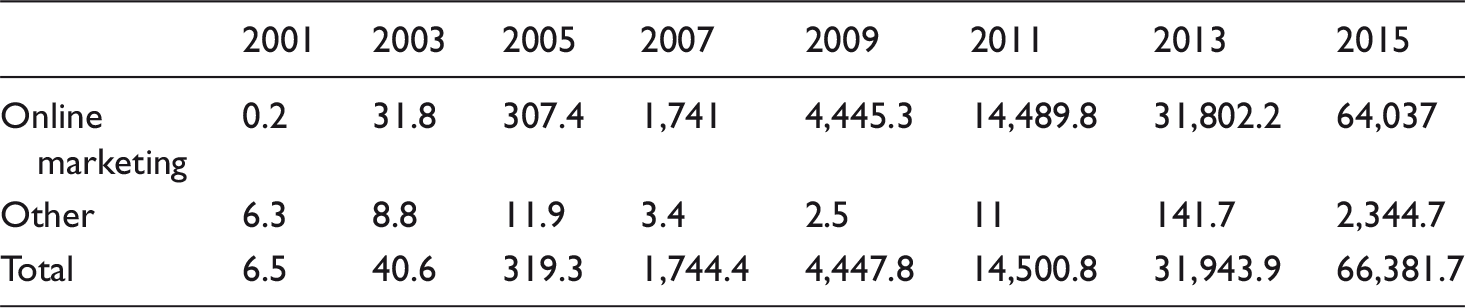

Baidu revenue by segment (in millions RMB).

Source: Company Annual Reports.

Alibaba revenue by segment (in millions RMB).

Source: Company Annual Reports.

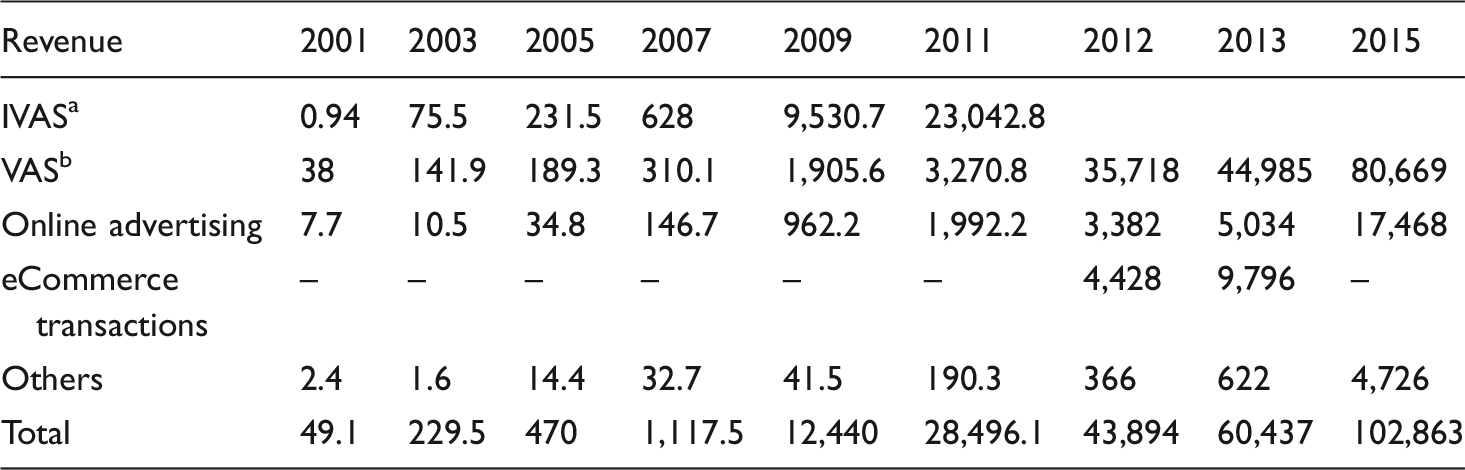

Tencent revenue by segment (in millions RMB).

Source: Company Annual Reports.

IVAS stands for internet value-added services, before 2012, Tencent’s method of reporting separated value-added services into IVAS and MVAS (mobile and telecommunication value-added service). After 2012, however, Tencent merged these two categories into VAS.

VAS stands for value-added services, such as games.

The following section provides a snapshot of the ‘big three’ Chinese internet giants along the following five dimensions, each of which helps fill in the empirical content of the financialization thesis: ownership structure, debt levels over time, mergers and acquisitions, board of directors, and linkages between owners and directors, on the one hand, and global finance networks, on the other. In particular, the analysis hones in on three major processes that Fitzgerald identified as the defining hallmarks of the financialization of media corporations:

increasing centrality of financial interests as corporate shareholders; increased debt leveraged to finance growth through mergers and acquisitions; the ‘financial’ conception of corporate assets as a ‘portfolio’ of liquid subunits, each of which must maximize its own value (Fitzgerald, 2012: 391).

Baidu

Baidu’s core business is online search. It was incorporated in 2000 and was listed on NASDAQ five years after that. As seen in Table 5, its main revenue stream derives from its core business: search tied to online advertising and marketing services. Compared to Alibaba and Tencent, Baidu also has the least diversified revenue structure, and it is smaller than Alibaba and Tencent based on revenue. After Google withdrew from mainland China in 2010, Baidu further cemented its place as the leading search engine in the country. The company also offers a bouquet of other internet services, such as an online map, payments, video streaming, and food delivery. In 2014, Baidu also made a major change to its board of directors that reflected its current foray into artificial intelligence and self-driving cars. Table 5, below, shows the 10-fold growth of revenue at Baidu between 2001 and 2015, and the company’s main lines of business operation.

At time of its public listing, Baidu’s CEO Yanhong Li owned 21.9% of the company’s share, while Draper Fisher Jurvetson ePlanet Ventures LP, a Silicon Valley venture capital firm, owned 15.6%, and Greg Penner, a member of Baidu’s Board of Director, directly owned 6.7% of its shares and another 6.5% through his Peninsula Capital Fund. Draper Fisher Jurvetson ePlanet Ventures and Greg Penner were no longer Baidu’s significant shareholders by 2015, however, while its majority and controlling owner continued to be its CEO, Li Yanhong (32% of shares), followed by the private Scottish asset management and investment trust, Baillie Gifford & Co. (7.25% of shares).

Alibaba

Ma Yun funded Alibaba in 1999. The company was listed on the Hong Kong Stock Exchange in 2007 and delisted in 2012. Alibaba launched another IPO in 2014, but this time on the NASDAQ in New York. It was valued at $25 billion USD when it went public—by then the biggest IPO for a Chinese company in history (Barreto, 2014). Its main revenue comes from its core business-to-business (B2B) and business-to-consumer (B2C) ecommerce services. As Alibaba’s Director and CEO Daniel Yong Zhang told attendees at the Nielsen Consumer 360 conference in Washington in 2015, however, ‘we are strong in ecommerce, but we never positioned ourselves as an ecommerce company only… we position ourselves as a data company, too’ (Liyakasa, 2015).The company is also a leading player in cloud computing business. Through vertical and horizontal integration, Alibaba has also expanded its reach into information infrastructure, which includes its investment in Singapore Post, logistics, cloud computing services, and big data services (Bloomberg News, 2016). Given the treasure trove of user data that the company gathers and processes through its ecommerce transactions, online payment system (AliPay), financial services and health care, Alibaba is also eyeing the opportunity to become the state’s appointed contractor in helping fight against crime using big data. Alibaba’s financial wing also developed the company’s Sesame Credit project as part of Chinese government’s national database and social credit scoring system, which is to be implemented in 2020 (Hatton, 2015). Both of these latter efforts illustrate the extent to which Chinese internet companies continue to cooperate closely with the Chinese government, and seem to relish the idea of being enrolled in the latter’s ‘law and order’ efforts. The efforts also suggest that the international investors behind such companies appear to be content to reap profits from their investments while facilitating the creation of a ubiquitous infrastructure of surveillance and social control that operates on behalf of the Chinese state.

Alibaba has also made important inroads into media content creation. It is the owner of Hong Kong’s English-language newspaper the South Morning China Post, which has a daily readership of 2.5 million. While the daily newspaper’s previous owners had maintained a pay wall a decade ago, it was dismantled after the newspaper was acquired by Alibaba in 2016 (Lhatoo, 2016). Alibaba has also invested heavily in ChinaVision, South Korea’s SM Entertainment, Huayi Brothers TV and movie production studio, and China’s largest online video site, Youku Tudou. Alibaba is owned by Ma Yun (7.8% of shares), Softbank (a Japanese based bank) (32% of shares), and Yahoo (15.4% of shares) (the well-known US-based internet company). Table 6, below, shows the near four-fold growth of revenue between 2012 and 2015 at Alibaba, and the company’s main lines of business operation.

Tencent

Tencent was founded in 1998 by Huateng Ma. The company was listed on the Hong Kong Stock Exchange in 2004. Its business is mainly based on online games and various mobile and internet instant messaging services. Tencent’s mobile chat program WeChat, for instance, has already gained a great deal of adoring attention from Western media, largely because it is seen as being on the ‘cutting edge of mobile tech’ and for having already surpassed Silicon Valley in this regard (Mozur, 2016). WeChat is designed as a fully integrated platform where chat is featured as the central function. Crucially, users do not need to exit WeChat at all to use other applications because the WeChat amalgamates access to an ever-widening range of apps, such as ride-hailing, online payment, flight ticket booking, and paying utility bills, for example—all through one application easily accessible via people’s mobile phones. Table 7, below, shows the fast-paced growth of Tencent over the 2001–2015 period. In short, WeChat epitomizes the reincarnation of the ‘walled garden’ approach, but on a grander scale than ever achieved in the heyday of that approach at the turn-of-the-21st Century in North America and Europe, and as best exemplified at that time by AOL Time Warner, an entity that also epitomized the excesses of the financialization processes at the heart of the dot.com bubble and its subsequent collapse.

In 2004 when Tencent went public, the company’s ownership structure was as follows: MIH QQ (subsidiary of South African media group Nasper): 35.62%; Advance Data Services Limited (wholly owned by Tencent’s CEO Huateng Ma): 13.14%; and ABSA Bank Limited (held by Nasper and wholly owned by Barclays through its holding company ABSA): 10.46%. In 2015, South African media group Nasper was still the biggest owner of Tencent, controlling a third (i.e., 33.5%) of its shares. The original founder, Huateng Ma, owns 9.1% of the company, while JP Morgan Chase owns 6.2% of the company’s shares. In September 2016, Tencent’s stock value surpassed that of China Mobile to become China’s most valuable publicly traded corporation (Chan, 2016). As Tencent’s largest shareholder, Nasper also saw a huge surge in its stock value, becoming Africa’s biggest company (Prinsloo and Hill, 2016). Table 7 below shows the growth of revenue between 2001 and 2015 at Tencent, and the company’s main lines of business operation.

Ownership, capital investment, boards of directors and power

In order to deepen our analysis of how Baidu, Alibaba, and Tencent have expanded and solidified their market power while simultaneously being integrated into worldwide circuits of capital as part of the financialization process, the remaining sections of this article examine the following six aspects of each company: i.e., ownership, directors, operating profits, debt level, mergers and acquisitions, and connections to broader global networks of capital, media and entertainment companies, ICTs, retailing, and the Chinese Government, amongst others.

In terms of the ownership of the big three Chinese internet companies, three things stand out. First, the

Second,

Third, and perhaps most surprising, is the extent to which

These ownership stakes have also been parlayed into positions on the companies’ boards of directors. Take Baidu, for instance. In addition to the positions held by the owner-founder, Robin (Yanhong) Li, the Bank of Japan and Greg Penner (an early investor) also have positions on its board. A major restructuring of the company’s board in 2014 also brought Lenovo’s CEO Yuanqing Yang and Brent Callinicos (who also holds similar positions at Uber, Google, and Microsoft), onto Baidu’s board of directors. Alibaba’s biggest institutional owners, Yahoo and Softbank, also have seats on its board, although its board also reflects the company’s ecommerce focus, with individuals from Pepsi, Intime Retail, and Walmart on it. As for Tencent, its biggest owner, Nasper, has long had board representation, and still does, as does Mail.ru, a Russian internet company that Tencent has invested heavily in. Each company also has interlocking relationships with various aspects of the Chinese Communist Party. As Arsenault and Castells (2008) observe, ‘media networks do not exist in a vacuum [but]… leverage connections with other critical networks: in finance, in technology, in cultural industries, in social networks, and in politics’ (731).

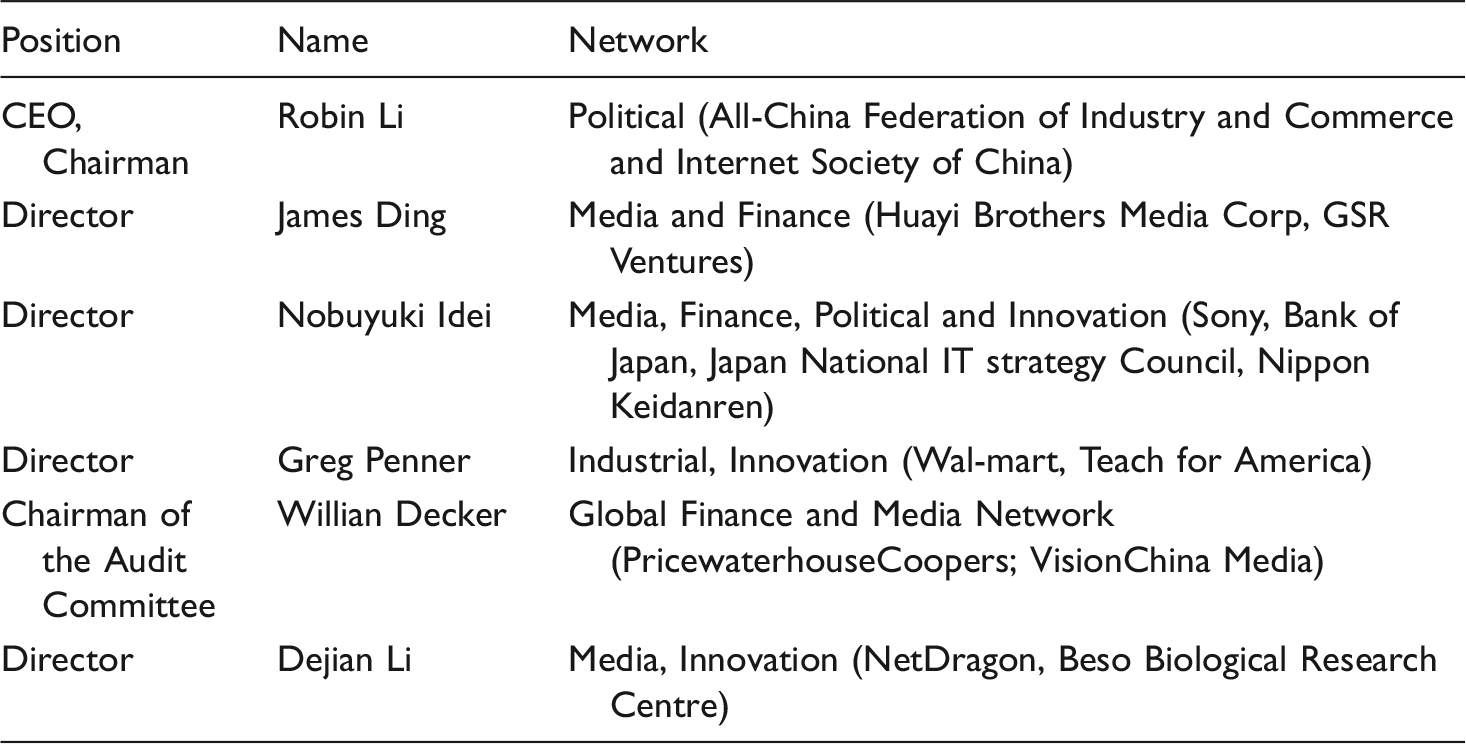

Baidu board of directors (2015).

Source: Baidu Annual Report 2015.

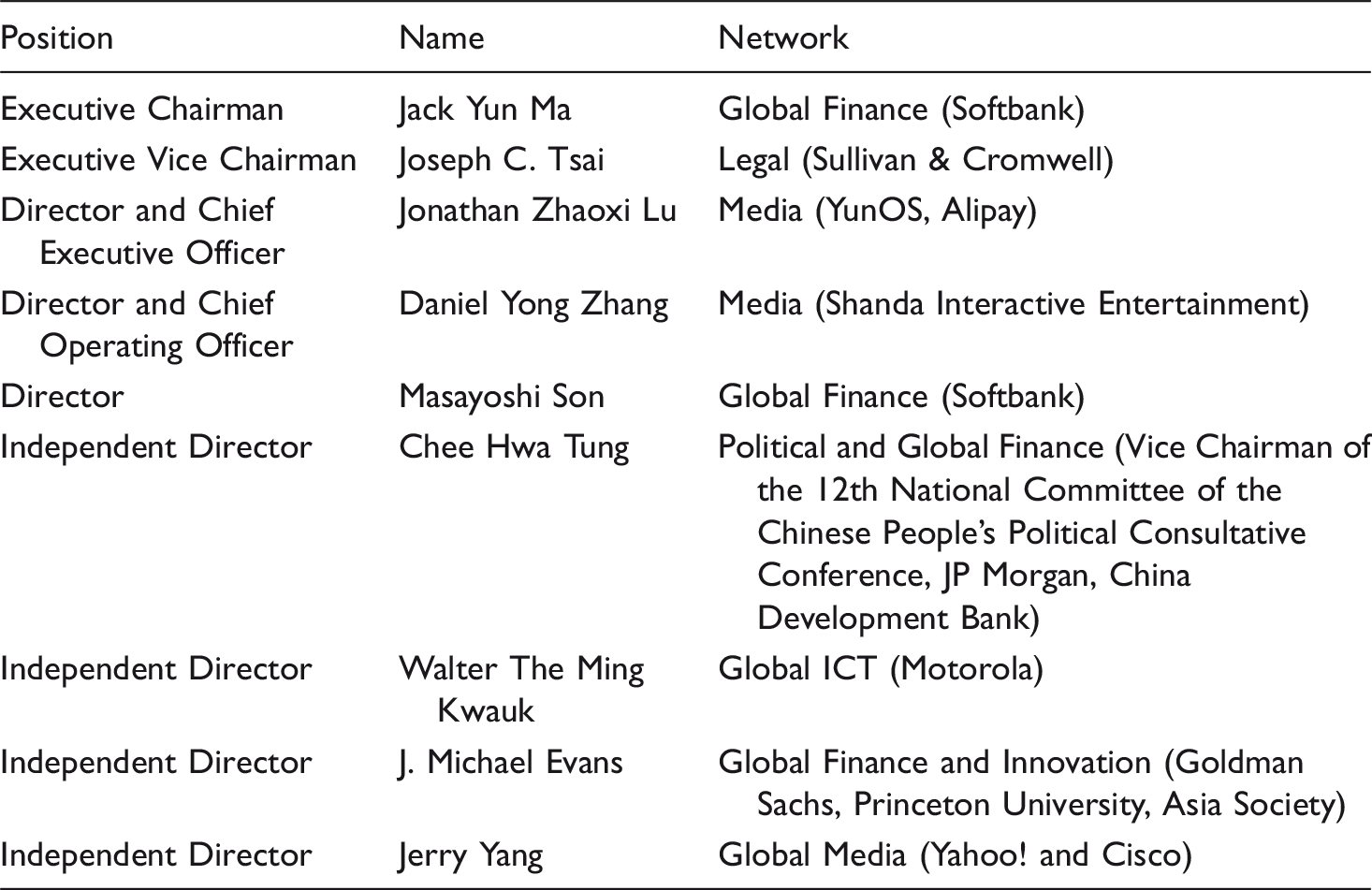

Alibaba board of directors (2015).

Source: Alibaba Annual Report 2015.

Tencent board of directors.

Source: Tencent Annual Report 2015.

Boards of directors are important because this is the juncture at which ownership can be turned into control (or power and influence). This is because boards shape the development of corporate policies and strategies, and the allocation of resources (e.g., money, technology, people, knowledge, etc.). These decisions affect the markets that the companies enter (or don’t) and their responses to new technologies and government policies, laws, and regulations—i.e., to embrace them enthusiastically, hesitantly, or not at all. This is a form of ‘structural power’. Being a director confers structural power because establishing long-term operating policies and allocating resources influences the direction that these companies take and, in turn, indirectly influence events from 1 day to the next. The ability to directly shape day-to-day events is a kind of ‘instrumental’ or ‘operational’ power. However, it is a weaker albeit not unimportant type of power because those who exercise it, e.g., managers, editors, engineers, etc., do so using the resources made available to them by directors and senior executives with ‘structural power’, and exercise whatever power they have within a framework of overarching corporate policies set by investors, owners, and directors (Arsenault and Castells, 2008: 743; Murdock, 1982).

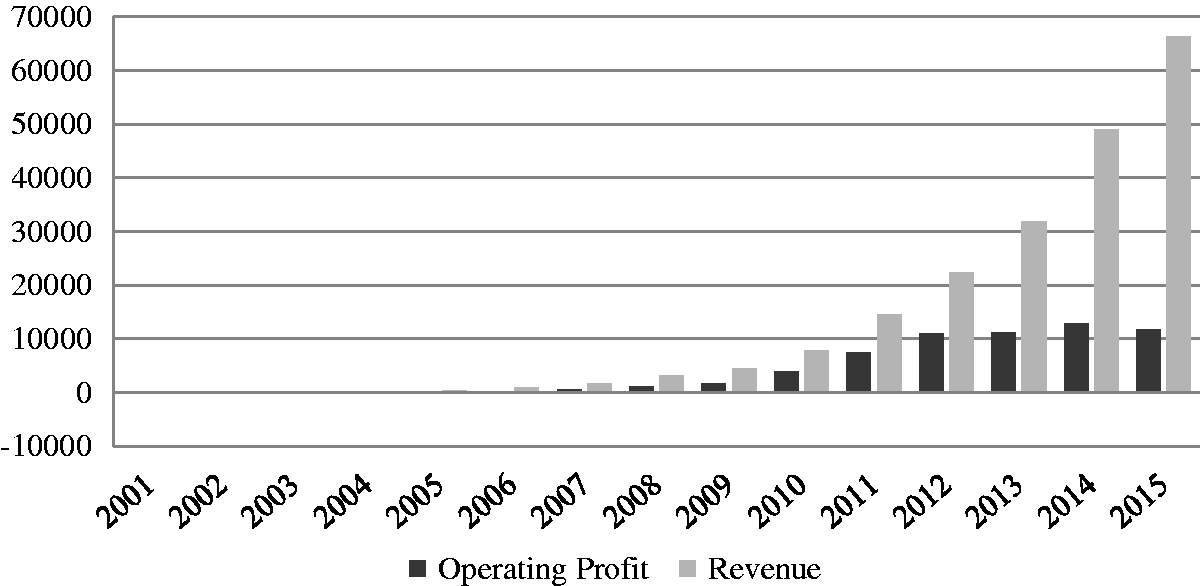

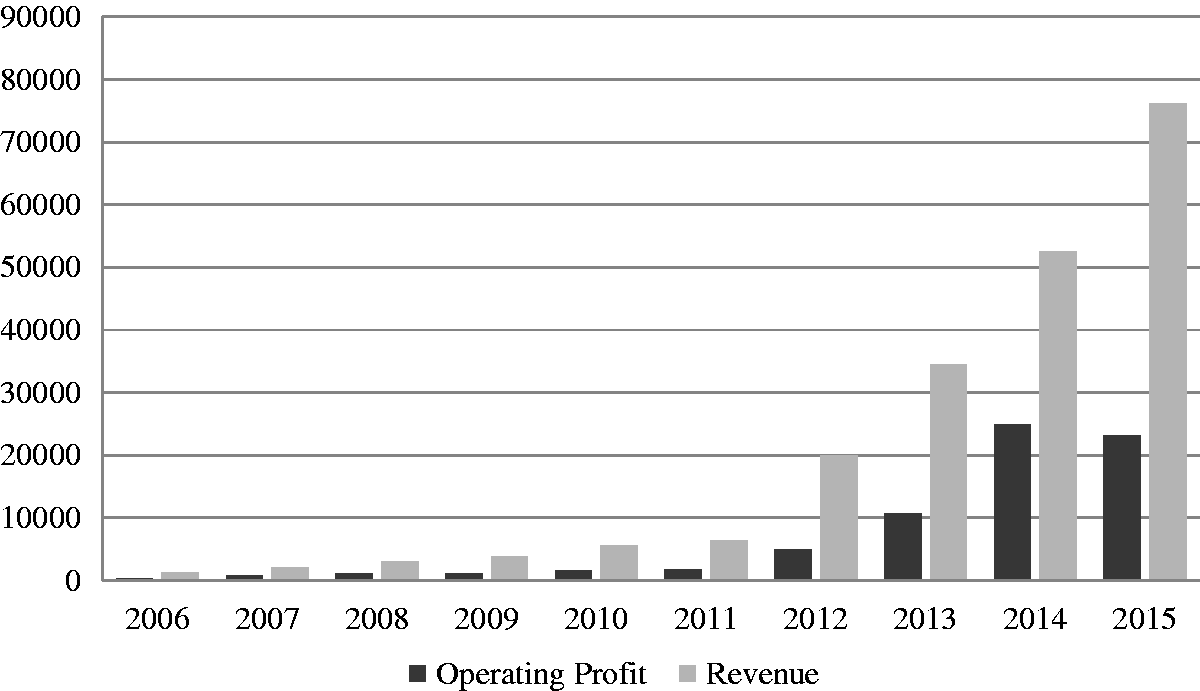

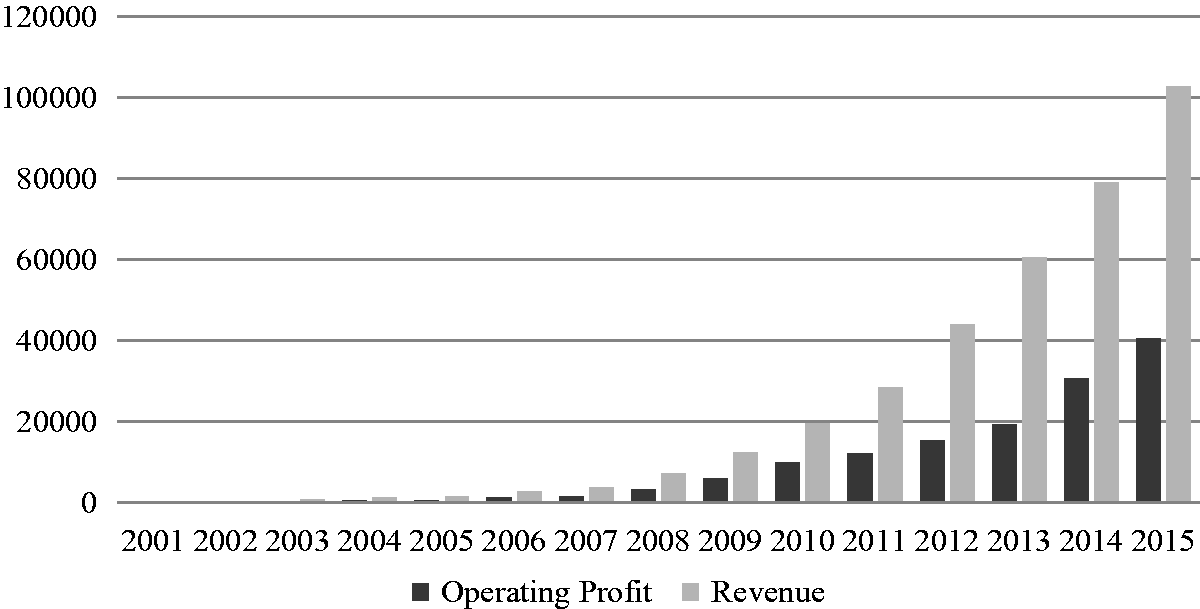

Operating profits

Operating profit is profit earned from a firm’s normal core business operation but excludes any profit earned from its investments and the effects of interest and taxes. It is also called earnings before interest and tax (EBIT). As seen in Figures 1 through 3 below, all three firms have achieved extremely lucrative profits over the periods covered in this article, averaging 31–32% for Alibaba and Baidu at the one end and an even more substantial 41% for Tencent. This is four- to five-, even more, times greater than the average level of operating profits for industry in China (7% in 2016) and multiple times higher than the US as well, where they were 10.3% last year (Damodaran, 2017a, 2017b). These lush profits are a key reason why the ‘big three’ Chinese internet companies have become magnets for capital investment from within China and international capital markets. It is further evidence in support of the financialization thesis as well.

Baidu operating profit (in million RMB). Alibaba operating profit (in million RMB). Tencent operating profit (in million RMB).

Mergers and acquisitions

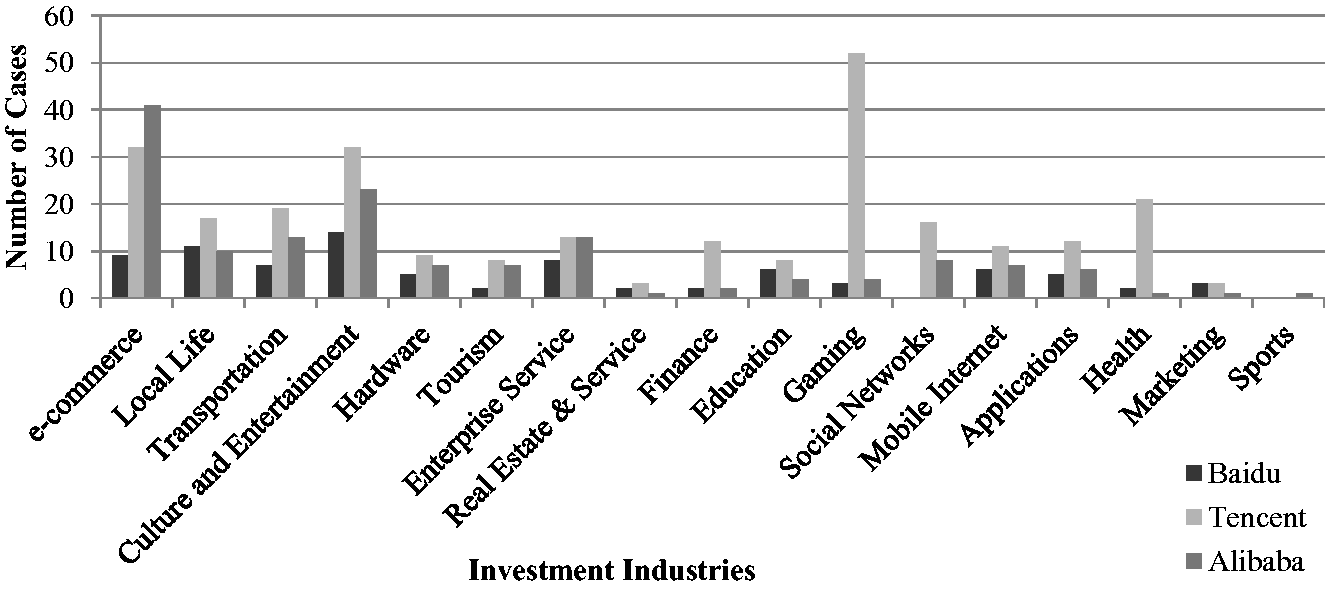

Consolidation is another leading indicator of the processes of financialization, and the order of the day amongst Chinese internet companies. Between 2014 and near the end of 2016, there were over 1,100 mergers and acquisitions (M&As) in the technology, media, and telecoms (TMT) sectors in China worth over $320 Billion (USD): 324 of those transactions worth $53.9 billion took place in 2014; 481 transactions valued at $156.8 billion occurred the next year; and there were 314 such deals worth over $110 billion in the first 9 months of 2016 (Perez, 2016a, 2016b). Figure 4 below charts the number and types of mergers, acquisitions, and investments completed by the BAT companies in 2014.

BAT mergers and acquisitions in 2014.

Baidu, Alibaba, and Tencent have been acquiring assets at a frenetic pace and are at the center of the processes of financialization rather than either innocent bystanders or its victims. Altogether, they made a combined $75 billion USD investment in acquisitions between 2013 and 2015 (Perez, 2016a, 2016b), and another estimated $80 billion USD in 2016—$155 billion (USD) in total. While the time frame doesn’t add up exactly since we don’t have figures for 2013 for mergers and acquisitions, the BAT companies’ acquisitions ($155 billion) equaled nearly half of the $320 billion (USD) in M&As that we do know of over the 2013–2016 period (Perez, 2016a). In short, they are at the center of such processes and in fact are leading them—consistent with trends that took place in North America and Europe around the turn-of-the-21st Century and, to a lesser extent, midway through the decade that followed (Fitzgerald, 2012; Winseck, 2014). Consolidation, in turn, has resulted in high levels of concentration in many core segments of the internet economy. While greater precision is needed, it is safe to say that the market for internet services in China is now a tight oligopoly, with Baidu, Alibaba, and Tencent occupying much of the field.

Baidu has been the least aggressive in terms of mergers and acquisitions, although its activities are still far from modest. Tencent, by contrast, topped the list in terms of the number and value of its investments in gaming, mobile internet, social network, and entertainment. In fact, it went on a buying spree in 2016, capped by its $8.6 billion USD purchase of an 84.3% stake in the Finnish mobile game developer Supercell from Softbank, which also owns nearly one-third of Alibaba (Chen et al., 2016). It was one of the biggest M&A cases in the country in 2016 (Perez, 2016b). Alibaba has invested and acquired mostly in ecommerce but it did branch out through its purchase of 82% of Youku Tudou for $3.7 billion USD in 2015. With its previously owned 18% share, Alibaba now wholly owns Youku Tudou, one of the dominant online video sites in China with a more than 21% market share (Forbes, 2016). Youku Tudou was previously traded on NASDAQ and struggled to be profitable amidst fierce competition with other rivals in the Chinese internet economy, and had lost $134.9 million USD in 2014 (Youku, 2014). The run of events at Tencent and Alibaba suggest that while the big three internet companies are consolidating their hold in markets that they have typically dominated, they are also diversifying into virtually all aspects of online business and making tentative forays into international markets.

Select acquisitions by Baidu, Alibaba, and Tencent, 2014–2016 (USD).

Source: Compilations from BAT annual reports and news sources.

Cap.: capitalization.

A stark example of the extent to which Baidu, Alibaba, and Tencent not only compete with one another but cooperate strategically is provided by Didi Chuxing—the Chinese ride-hailing service that now holds a monopoly in the market. Before Uber entered China, Tencent had vested interests in Didi Chuxing, while Alibaba owns 54.4% of another firm that was then dominating the ride-hailing market, Kuaidi. In February 2015, Kuaidi and Didi merged. At the same time, however, Baidu had a significant stake in Uber China. After finding the competition between Uber and Didi Chuxing too costly for both companies, Didi Chuxing bought Uber China in 2016, with Uber’s previous investors, including Baidu receiving a 2.3% ownership stake in Didi Chuxing (LA Times, 2016), after which the big three—Baidu, Alibaba, and Tencent—jointly owned the company. Drivers, for one, immediately felt the consequences, with their cut of the ride-sharing company’s fares slashed (He, 2016).

Mergers and acquisitions have also been used to globalize the big three companies’ businesses. Of course, there are those, like Gu and Frank (2006), for example, who point to how ‘foreign companies are increasingly buying Chinese assets as a way to tap into China directly’ (135). These authors use eBay and Amazon’s acquisitions of Chinese internet companies to illustrate their point. Equally important, however, is that Baidu, Alibaba, and Tencent are buying their way into foreign markets. For example, Tencent has made significant investments in Russia (Digital Sky Technologies, Mail.ru), India (Practo, Flipkart, Ola), the U.S. (Snapchat, Whisper, Epic Games), Canada (Kik Interactive), and South Korea (Kakao Talk). For its part, Baidu has launched search services directly in Japan, Thailand, Egypt, and Brazil. None of these efforts have yielded significant success, but undeterred Baidu also indirectly invested in Uber in the US, Israeli companies (e.g., Carmel Ventures, Pixellot, Tonara, Taboola, Outbrain), Japanese company PopIn, and Brazil’s Peixe Urbano.

Company debt level

Debt-to-equity value measures how much debt a company uses to run its business. In other words, it tells how much debt a company has for every dollar of equity it has. Technology business and research and development intensive companies will sometimes take on a heavy debt-to-equity of up to 2:1, but that is in exceptional circumstances. Melody (2007), for example, suggests that, as a general rule, the debt-to-equity ratio should stay below 1:1, and the lower the better. Take Apple and Google, for example. Both are fairly research intensive but both have very little debt. Google has had a debt-to-equity ratio that has consistently been less than 0.1 since 2001. Apple has a debt-to-equity ratio of less than 1.

BAT debt-equity ratio, circa 2001–2015.

Source: Authors’ compilation based on company annual reports.

As Table 12 illustrates, Baidu’s debt-to-equity ratio has risen steadily over the years. In simple terms, this means that the company has taken on more and more debt for every dollar of equity it owns. The same is true for Tencent. In 2014 and 2015 amidst a flurry of acquisitions, it took on more debt and its debt-to-equity ratio reached a high of 1.08 in 2014 and 1.5 in 2015. This was a result of its $1 billion USD investment in Dianping, a group-buying company in China, followed by its $770 million USD investment in Didi Dache, China’s ride-hailing application, and the purchase of one-fifth ownership stake in the online classified site 58.com’s stake for $836 million USD. As Table 12 also indicates, Baidu has had an average debt-to-equity ratio of 0.54 and Tencent 0.45 over the years, which means that both companies have maintained relatively modest levels of debt. On the other hand, Alibaba’s debt-to-equity ratio has fluctuated widely, temporarily soaring to its all-time high of 13.1:1 just before its reorganization in 2007. At the time, the company transferred its B2B services, Alibaba Hangzhou, to parent company Alibaba China in preparation for its stock listing that year. This demonstrated perfectly the rise of the ‘financial’ conception of corporate assets whereby the corporation is seen as a portfolio of liquid subunits each of which must be relentlessly pushed to maximize its own value as if it was traded as a separate, stand-alone entity (Fitzgerald, 2012). Overall, Alibaba’s average debt-to-equity ratio has consistently been higher than those of Baidu or Tencent.

Conclusion

This article has examined the capitalization and commercialization of the ‘big three’ Chinese internet companies and done so in line with the tenets of the financialization thesis: Baidu, Alibaba, and Tencent. In so doing, we have examined half-a-dozen characteristics that define these companies and the internet economy in China more generally. First, our analysis illuminates the centrality of financial institutions in the ownership of the companies. Founding owners still have a significant place in each of the companies, but they are always surrounded by major banks, venture capital funds, and institutional investors, a surprising degree of which is US, British, or Japanese in origin. Indeed, finance companies hold significant ownership stakes in BAT: the Scottish investment trust Baillie Gifford owns 7.25% of Baidu’s share, Softbank of Japan owns roughly a third of Alibaba, and JP Morgan Chase owns 6.2% of Tencent. Moreover, the scale of foreign investors ownership stakes in Alibaba (40%) and Tencent (45%) is extensive. The extent of foreign ownership has slipped over the years at Baidu from roughly a third 7.5% in recent years, but it is still significant. More to the point, the scale of foreign ownership in China’s three biggest internet companies contradicts conventional views that they are extremely insular due to the fact they have been deliberately created and cultivated as ‘national champions’ to counter the dominance of US-based internet giants such as Amazon, Facebook, and Google that the lion’s share of their operations takes place within China and the very tight regulation of their services by the Chinese government.

Second, the composition of the board of directors also reflects the ownership structure of each company and the role of financial institutions and investors. Indeed, banks and financial investors have director positions on the boards of all three companies. Given this, as Fuchs (2015) states, the capitalist information economy both in China and the West cannot be studied independently of finance capitalism. Publicly traded internet companies are listed on stock markets in both China and abroad in order to access capital, sell shares to investors, and to try and increase the value as measured by the metric of market capitalization. These are defining features of the internet economy and the companies that we have studied here and that others have examined elsewhere (Fitzgerald, 2012; Fuchs, 2016: 35; Perez, 2002; Winseck, 2014).

Third, Baidu, Alibaba, and Tencent have turned to capital-intensive mergers and acquisitions to consolidate their influence. While each company bases its operation on its core business—e.g., Baidu on search, Alibaba on e-commerce, and Tencent on value added content and online games—each is now striving to diversify by investing in companies in other areas. As Winseck (2011a) states, heightened waves of consolidation at the turn of the 21st Century and, to a lesser degree, midway through the next decade, in western capitalist democracies signaled that the telecoms, internet, and media sectors were at the forefront of the processes of financialization, accounting for far more mergers and acquisitions than their weight in the economy dictated (31). The slowing pace of the Chinese economy, coupled with the fact that the ‘Big Three’ Chinese internet have turned to a strategy of growth through acquisitions, suggests that the fit between the financialization thesis and the specificities of the Chinese case has tightened. While it is too early to draw firm conclusions one way or another on this point, our research suggests that this is a useful line of inquiry to pursue further and a useful complement to critical political economic scholarship that has already been done on the media and internet in China.

Fourth, however, Baidu, Alibaba, and Tencent have generally kept their debt levels in check—a point that runs counter to the financialization thesis. Ultimately, however, and fifth, regardless of whether events in China hew to the path cut by the western counterparts or chart a different course altogether, they have become tightly tied into the worldwide circuits of capital accumulation. Thus, while there is indeed be a distinctly ‘Chinese internet’ due to the heavy hand of the Chinese state, and the willingness of Chinese internet companies to play handmaiden to its efforts to regulate how people use the internet, our analysis suggests that a less parochial view is needed in light of the extent to which Chinese internet companies are tied tightly into global capitalism. This is a crucial insight and helps to illustrate why we need not just a politics of the Chinese internet but a political economy of that internet, which shines a bright light beyond the big shadow cast by the Chinese state. That is, we need a political economy of the internet under the conditions of autocratic Chinese capitalism that recognizes both the commonalities and distinctive characteristics of both.

Our article has tried to bring these features into clear view in order and to open new paths of inquiry that go beyond the well-established focus in the literature on the development of evermore sophisticated types of internet control by the Chinese government. We have tried to develop these insights with an eye to identifying both general trends but also the precise details and cross-cutting evidence that must inform the kind of political economic analysis that we are both trying to do and calling on others to pursue. While we want to stand back from drawing premature conclusions of what our observations mean, we agree with Mansell (2004) that there must be a central place for questions of power in any examination of the development, organization, ownership, control and uses of new media. This must be done by, among other things, examining different kinds of power and how they are embedded and expressed within specific conditions. To this end, we have focused on structural power, that is, the ability to use ownership and positions at the top of a business enterprise to frame what others throughout the rest of organization are able to do based on the resources they have been allocated and within the parameters set by the long-term corporate policies within which they must act (Murdock, 1982; Giddens, 1976/1993; Luke, 1974/2005). In this regard, we have shown how capital investors have parlayed their interests into key positions on BAT companies’ boards of directors and used the potential for influence that comes from such positions to allocate resources and develop corporate policies that give direction to Baidu, Alibaba, and Tencent’s operations over the long run. This is ‘structural power’. The course of development that they have set has been one of rapid growth through mergers and acquisitions. This has enabled Baidu, Alibaba, and Tencent to consolidate and diversify their roles in domestic markets while taking some steps to expand globally, albeit with only Tencent’s push into the online and mobile gaming industry constituting a major step in this direction. These are all ‘effects’, so to speak, but they don’t offer a ready-made basis for making judgments one way or another.

Private companies like Alibaba, Baidu, and Tencent have now become so prominent that we cannot fully understand China’s approach to internet governance and ongoing economic restructuring without understanding these companies (Shen, 2016; Hong, 2017). Ultimately, to understand the political economy of Chinese internet companies requires that we go further to understand the triangular relationship that exists between state power, private business, as well as domestic and international capital. Each of these entities acts and reacts in relation to the others, sometimes harmoniously and sometimes contradicting one another. And as China’s influence spreads to other countries which seek to emulate its ways, their influence is likely to grow.

How all this will play out in the long run, however, it is too early to tell. Nonetheless, we hope that our attempt to expand the analytical lens so as to bring the role of business enterprises, markets, and capital investment into sharper relief provides a useful contribution that others can build on.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.