Abstract

The use of online road freight transport exchanges (FTEs) in the EU-28 countries is widespread today, indicating a strong level of competition. Some exchanges attempt to distinguish themselves by developing new services, for example, warehousing services for logistics industries. In contrast, rail FTEs show a very low rate of success. Given the European Union policy goal on modal shift from road to rail and inland waterways for the next decade, there is a need to explore possibilities for improvement. This article, therefore, aims at specifying regulatory-, market-, technical- and operational success factors for implementing rail-based multimodal FTEs. It does so by exploring the success factors from established road FTEs and other successful network industries (energy and passenger transport) by performing a comparative analysis on the respective online exchanges. The theory on capability maturity development is applied, which assumes that actors engaged in a transition process steadily grow in terms of their capability to deal with various issues rising from the required transition goals. Based on the theory, a literature review and interviews, an initial capability maturity model (CMM) for FTEs is developed. Finally, learnings are summarized for the proposed multimodal FTE regarding rail and the regulatory topics for freight transport to serve as input for creating a generic CMM for online exchanges in subsequent steps of this research project. Similar research on maturity assessment of practices in online exchanges related to network industries could not be found.

Introduction

Digital platforms are emerging at a tremendous pace causing structural changes in market dynamics within and across economies worldwide. Thus, new ways are unfolding, both for producers and consumers for accessing the market, but more so for the intermediaries that are bringing these groups together by developing and offering innovative matching services. Most network industries are increasingly affected by such platforms. However, some industries are showing a higher maturity in adapting themselves than others, especially through offering new services, for example, multimodal services in the transport industry. (De)regulation in this regard appears to be an important vehicle to trigger and support such adaptations.

This article focuses on online exchanges as digital platforms of such network industries, including those within the freight industry. Within this scope, it aims to explore regulatory requirements, technical, operational and market-related practices from mature online exchanges. Resulting insights will, in a later stage of our research, constitute the input for developing and testing an innovative rail-based multimodal freight transport exchange (FTE). The trigger for this research is the observation that the freight industry is less mature in this respect as well as the belief, inspired by other network industries, that an improved rail-based multimodal FTE can support the European Union (EU) white paper policy goals to shift 30% of the long-distance road freight transport (beyond 300 km) to multimodal transport by 2030 and more than 50% by 2050. So far, little has been achieved in this context (European Commission, 2016). The share of rail freight in EU-28 countries (see Figure 1) has declined since 2011 and road freight continues to dominate. Hence, the EU policy has, so far, not been effective. One of the proposed explanations is that the matching between demand and supply in rail freight transport is not yet efficiently organized.

Freight transport in the EU-28: modal split of inland transport modes rail, inland waterways and road in % of total tonne-kilometres for 2011–2016. Source: Data retrieved from EUROSTAT (2018).

A brief characterization of developments in other selected network industries better highlights the state of rail freight regarding the development and use of digital platforms.

First, we look at industries different from freight where competition has strongly been stimulated. In postal and telecommunications services, email and messengers substituted paper-based letters, and Skype and WhatsApp enabled free calls on mobile phones. Further, an electricity power exchange platform provides a spot market for electricity, which matches demand and supply for each hour for market players (electricity generators, operators for long distance transmission or distributors for end-consumers, etc.), while providing a public price index (Boisseleau, 2004). Smart cities and smart home solutions connect passenger transport, telecommunications and energy industries further. Weiller and Pollitt (2013) suggest an electric vehicle aggregator as a platform service provider offering added value to consumers using electric (also named plugged-in) vehicles. In urban public transport (UPT), several transport companies are offering digital platforms for Mobility as a Service (MaaS) solutions. For example, a MaaS concept (Jittrapirom, Marchau, van der Heijden, & Meurs, 2018) was introduced as an integrative online platform for bundling information and offering booking and billing across different transport modes (private and public) for customers (both individual and businesses). This brief exploration indicates that various competitive network industries are maturing in service level by improving their business-to-business (B2B) markets or linking business-to-consumer (B2C) and B2B markets through the use of intermediaries, enabled by digitalization.

Regarding freight transport, nowadays hundreds of road FTEs are used within Europe (Jain & Bruckmann, 2017). Recently launched exchanges additionally offer transport of partial loads on their platforms. An exchange owner stated: ‘The general hypothesis is, that the long term customer relationships are gradually being replaced, the spot market continues to grow, and the B2B customers are increasingly behaving like B2C customers’ (Nallinger, 2018, para 13). Hence, in this research, we ignore the demarcation between B2B and B2C markets for drawing lessons about maturity in practices. The rise in road FTEs, which are able to merge different transport needs, is promising in reducing road congestion, pollution, noise and traffic accidents. To keep up with competition, some existing exchanges have evolved further by offering solutions in adjacent markets like warehousing. In contrast to road FTEs, one of the few rail-based exchanges closed its service recently in 2018 after a trial of 2 years, although its exchange for inland waterways continues to operate. This illustrates that a serious gap exists in bringing the rail freight industry from its current low level of maturity of (multimodal) services offered to a significantly higher level.

For exploring the possibilities to increase the level of maturity in (multimodal) transport services offered, we apply the following steps. First, a theoretical framework for online exchanges is specified. Next, relevant network industries for comparison are selected. We then briefly explain an initial capability maturity model (CMM) for maturity assessment of online exchanges as a starting point for elaborating a generic framework. The methodology section describes the data collection approach using semi-structured interviews with exchange service providers and experts and other data collection methods. In the section on capability maturity assessment, the data on regulatory, technical, operational and market-related practices related to online exchanges of network industries are qualitatively compared and assessed. The main focus is on exploring regulatory requirements for rail freight and multimodal transport, therefore only practices are described which lead to such requirements. Finally, conclusions on potential improvements of maturity through regulatory interventions will be presented.

Theoretical framework on online exchanges and network industries

To create a general framework for maturity assessment of two-sided platforms, key common principles in different definitions applicable to all digital platforms need to be identified. This is complicated by the variety of definitions of platforms (EU Committee, 2016). In this regard, the generalization of the theory of two-sided digital platforms by Rochet and Tirole (2003) is helpful, which states that the common underlying business model of platforms from seemingly uncommon industries is based on facilitating interaction between buyers and sellers.

In the freight industry, the terms ‘freight exchange’, ‘digital platforms’ and ‘online platforms’ are used interchangeably. O’Reilly and Finnegan (2005, p. 24) define online exchanges as: an organizational intermediary that electronically provides value added communication, brokerage and integration services to buyers and sellers of direct and/or indirect products and/or services in specific horizontal or vertical markets by supporting basic market functions, meeting management needs for information and process support, and/or operating the required IS/IT infrastructure.

The term ‘online exchanges’ is used in this article to understand and compare the overarching practices of online exchanges in network industries.

CMM framework

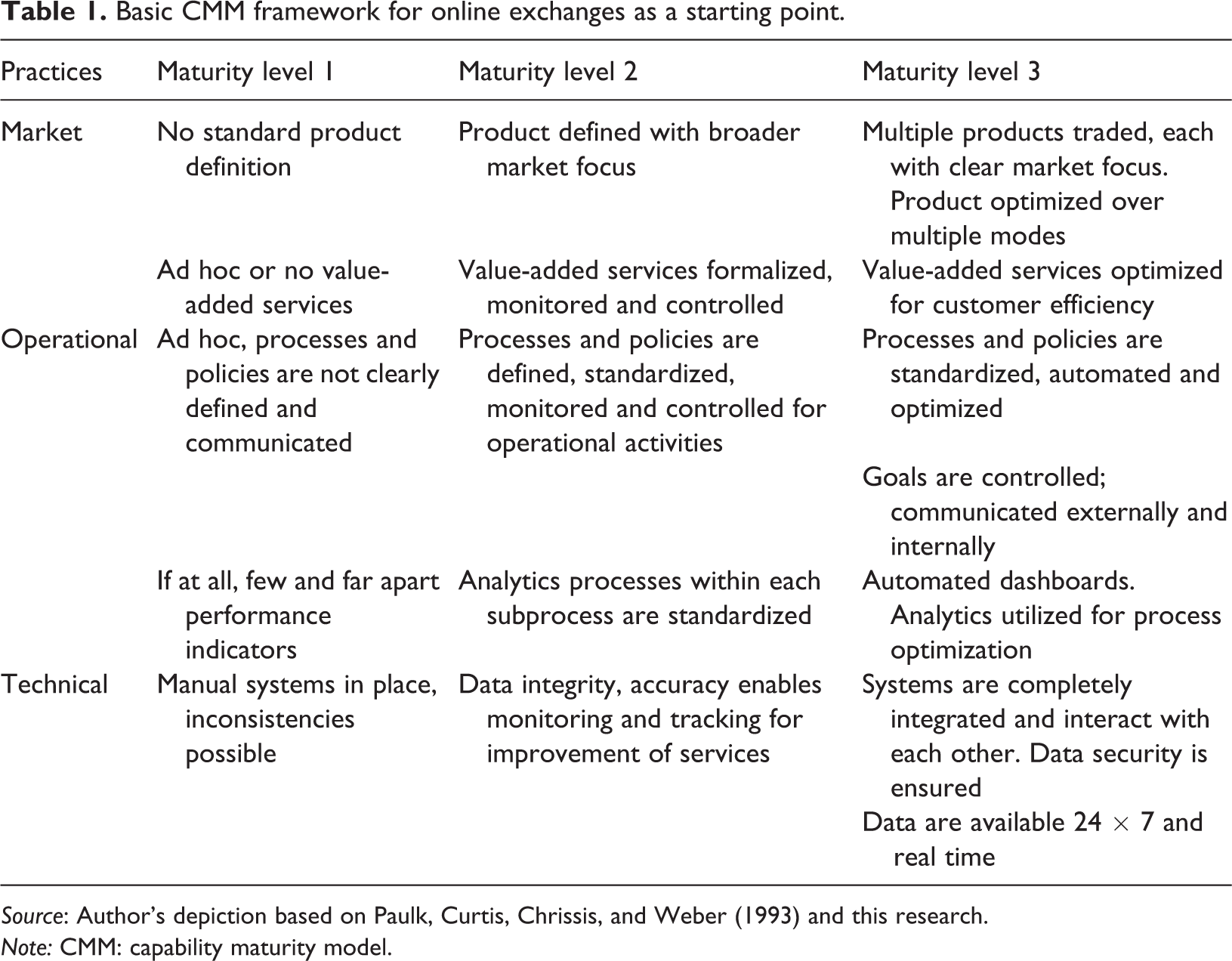

To be able to draw lessons for development of the rail freight industry, a supportive frame of thinking is needed. This article adopts the theoretical framework provided by the CMM framework for defining a transition path towards a rail-related multimodal online freight exchange. The CMM framework, originally formulated for the software industry, assumes that actors during a transition process, for example to the introduction of an innovation, steadily grow in terms of their capability to cumulatively deal with the various issues rising from that transition process. The framework describes and refines business development, operations and monitoring processes in terms of maturity stages, capabilities to achieve a maturity stage and activities to achieve a capability that contributes to a higher level of maturity regarding the coping with the challenges of the transition (Paulk, Curtis, Chrissis, & Weber, 1993). It is increasingly used to assess developments in industries other than the software engineering.

In this study, the challenge is to operationalize the theory on maturity growth for rail-based multimodal FTEs. Rose (2013) argues that specifying a CMM framework for any sector involves three steps: (a) determine the purpose of the model and its key process areas to be focused on, (b) determine the different maturity levels and (c) develop the expectations for (practices in) each key process area that contributes to a shift from the initial maturity level to the next maturity level. Following an explorative approach (Marshall & Rossman, 1989), using insights from literature and personal experiences, a basic CMM framework for comparing the rail FTEs to the selected comparable network industries is presented in Table 1.

Basic CMM framework for online exchanges as a starting point.

Source: Author’s depiction based on Paulk, Curtis, Chrissis, and Weber (1993) and this research.

Note: CMM: capability maturity model.

This framework makes a distinction between three levels of maturity to indicate different stages in mindset and acting regarding key processes. These are summarized and categorized as operational, technical and market-related practices linked to the existence, use and performance of online exchanges. The market practices relate to the expectations regarding clarity in strategy and market focus, the definition of products/commodities and the management of stakeholders that includes current and potential exchange participants. The operational practices relate to expectations regarding procedures and policies which must be communicated to participants, standardized and continuously optimized for running the exchange efficiently. Finally, the technical practices relate to expectations regarding data availability, data security and data integrity as well as the nature of the interface of the exchange with relevant systems of participants and partners.

The maturity levels of the basic CMM framework of online exchanges are defined as:

Exchanges at (low maturity) level 1 encompass ad hoc processes and policies with an unclear market focus and basic technical solutions in place (mainly for providing information). Operational practices of such exchanges are scattered or based on tailor-made, sometimes ad hoc, efforts to interact with specific customers to deliver dedicated services.

Exchanges at (intermediate maturity) level 2 have defined processes and an organized discipline to repeat certain practices manually. Routines and procedures with clients are largely standardized. The practices of such exchanges aim at solving current needs from the exchange participants and the customers in a fast and efficient manner.

Exchanges at (high maturity) level 3 have processes and systems that are automated and integrated with those of the involved partners. Processes and systems are in place to systematically monitor and control the exchange performance and its impact in market. They engage the stakeholders and the partners continuously and proactively to optimize processes, products, systems and services for higher customer efficiency and satisfaction.

Selection of relevant network industries for comparative analysis

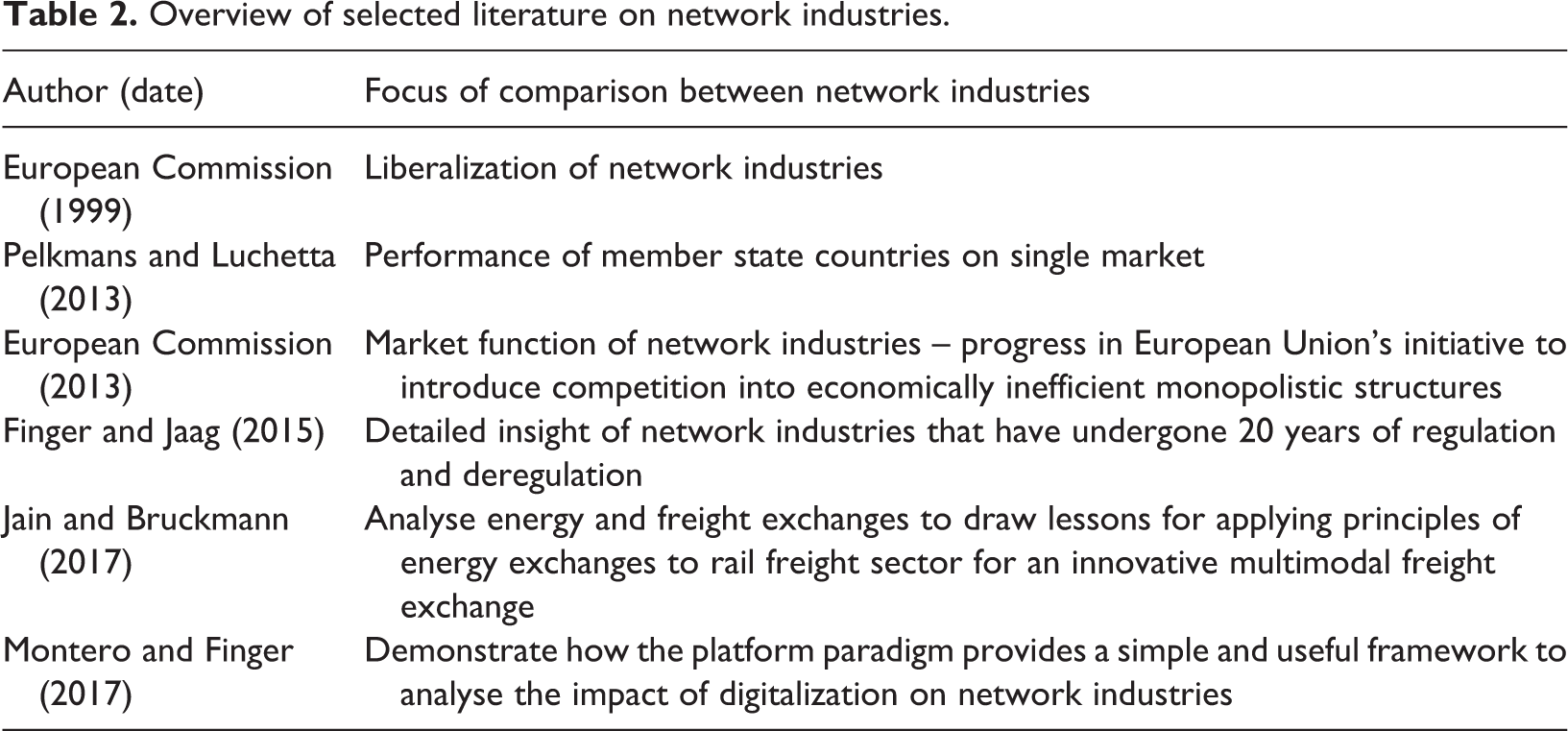

The literature search revealed that various comparisons of the characteristics of different network industries in the EU-28 countries and state of the industries in terms of liberalization, regulation and so on have been performed in the past two decades. Such industries include telecommunications and postal services, energy (electricity and gas), transport (rail, road, air, maritime) and water. The latter also includes UPT. Table 2 shows the relevant studies this article use to make a selection of the network industries later in this section. The aim is to select industries from which rail freight transport can draw lessons.

Overview of selected literature on network industries.

The current policy regulations, the key drivers of the industry (e.g. regulation/deregulation or very often technology development) and the evolution of the industry influence the current state of network industries. Thus, comparing the key influencing factors and current state of network industries is important for selecting relevant network industries to stimulate learning. Further, the commonalities in infrastructure characteristics form a basis for understanding the applicability of learnings drawn. First, we refer to the industries analysed by Finger and Jaag (2015), Montero and Finger (2017) and Jain and Bruckmann (2017), as summarized in Table 3.

Selection of network industries for comparison of online exchanges.

Source: Author’s depiction based on a Finger and Jaag (2015), Chapter 29, Table 29.1 and bauthor’s note.

As expressed in this table, the telecommunications, maritime and air services are far more competitive industries (and different infrastructure characteristics) than rail freight. Fresh water is politically influenced, therefore, yet to evolve. Hence, these industries are highly mature in an open market and are therefore not included for comparison. The energy industry operates in a highly regulated market (e.g. Finger & Jaag, 2015) and can offer learning for rail freight. From an economic point of view, the price in electricity fluctuates over time and between regions and is subject to fluctuation in demand and supply, including shortages and congestion on the network, thus making it non-homogenous and therefore comparable to transport (Jain & Bruckmann, 2017). Similarly, the standardization of consignments like Euro pallets or containers is a move towards homogeneity in transportation.

In terms of markets, energy exchange markets are organized on the basis of long-term contracts and short-term (spot) contracts. Whereas in electricity industry, liquidity is higher for long term contracts than for short-term contracts, the reverse is true for gas exchanges. In UPT (including MaaS) and long-distance passenger transport (LPT), tickets are either bought shortly before travel on exchanges or tickets are based on special long- and short-term offers. Due to various logistics development (e.g. Van Duin, 2012), the spot market on road freight exchanges is very liquid. However, exchanges have also started offering services based on long-term contracts making long-term and short-term markets increasingly complimentary. Today, rail freight operators are mainly focused on long-term, bulk haul contracts. Due to customization of production strategies (causing transport of smaller volumes), the spot market in road freight is increasing. Consequently, the long-term rail contract market decreases.

Next, we look at the commonalities in infrastructure characteristics of the industries from the perspective of applicability to rail freight. The energy (electricity and gas) and rail services have ‘natural monopoly’ characteristics caused by huge sunk costs in physical infrastructure (Pelkmans & Luchetta, 2013). Hence, little or practically no duplication of infrastructures exists for them, thus leading to concentrated and asymmetric market structures. Whereas road transport (private vehicles) is a strong substitute to rail and UPT services, a partial substitution occurs in energy industry (e.g. from privately produced renewables). Further, due to the high economies of scale, operators in network industries strive for achieving a critical mass (or liquidity) by offering products/services to users so that every new user brings benefits to all other users in their network (positive effects). In this regard, different mechanisms exist to overcome challenges related to bottlenecks in infrastructure (e.g. due to higher demand). Energy, UPT and rail passenger transport organizations thus optimize their capacity through assets sharing (e.g. facilitating multimodality) or connecting their networks by way of compatibility (or commoditization) and standardization of products and services. Rail freight transport has potential for improvements in this regard and, therefore, can learn from the three industries.

Finally, a comparison with road freight transport is indispensable since it dominates the transport in the EU-28 countries and is considered the largest competitor for rail freight transport.

Therefore, in this article, the selection of benchmark network industries to draw lessons from for rail transport is limited to the network industries that currently represent a ‘next step’ in development, hence the energy, road freight, long-distance passenger and UPT industries.

Methodology

For further elaborating the basic CMM framework, data for online exchanges of selected network industries were collected. In this article, only the first steps involved in the elaboration are discussed. The details will follow in a consecutive paper generalizing the complete CMM framework.

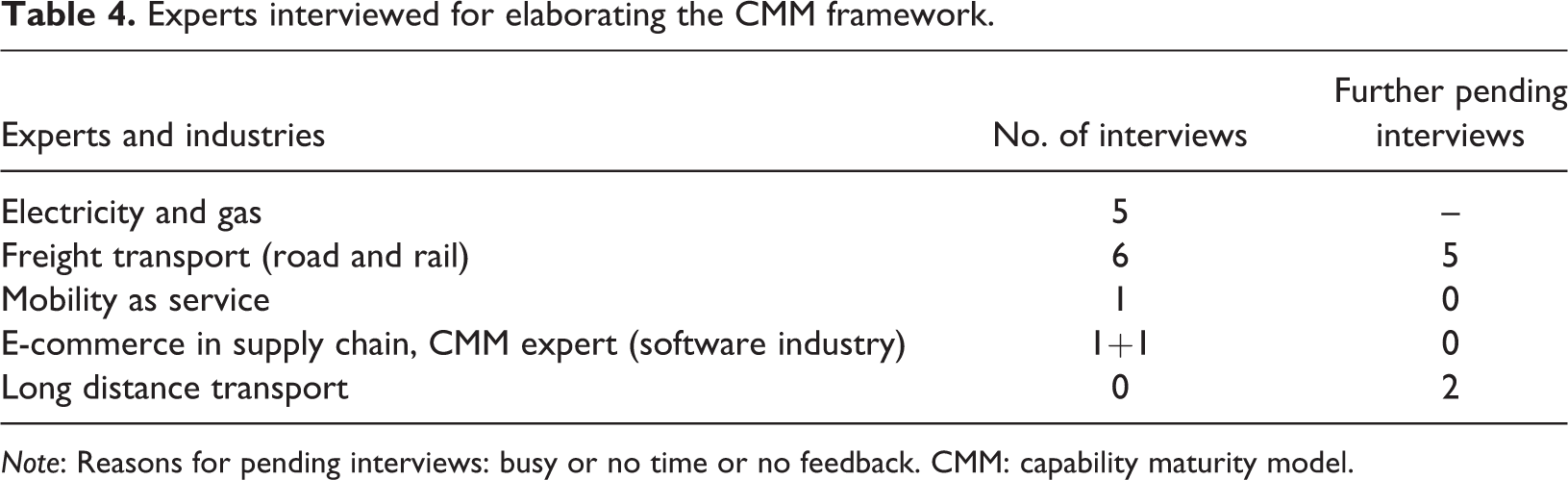

Data were collected through desktop research of the exchange websites, case studies and literature review. Experts who are representatives of online exchanges and independent subject matter experts from different network industries (Table 4) were selected for semi-structured interviews. These experts were questioned on infrastructure characteristics and the business model of online exchanges, together with the key processes and associated regulatory, technical, operational and market-related practices. The insights into maturity of exchange processes and practices were then used to refine the CMM framework. For example, market-related practices get broken down into further details. The interviewees agreed that technical practices like 24×7 availability, data security, accuracy and so on are basic conditions that all exchanges must fulfil. Therefore, these are prerequisites to operating exchanges and were not separately assessed.

Experts interviewed for elaborating the CMM framework.

Note: Reasons for pending interviews: busy or no time or no feedback. CMM: capability maturity model.

For the sake of readability, the analysis in the next section first describes selected exchanges and state of each industry. Based on this, the maturity level for each practice per industry is analysed using the elaborated CMM framework. Next, industries are compared to each other.

Maturity assessment of online exchanges in selected network industries

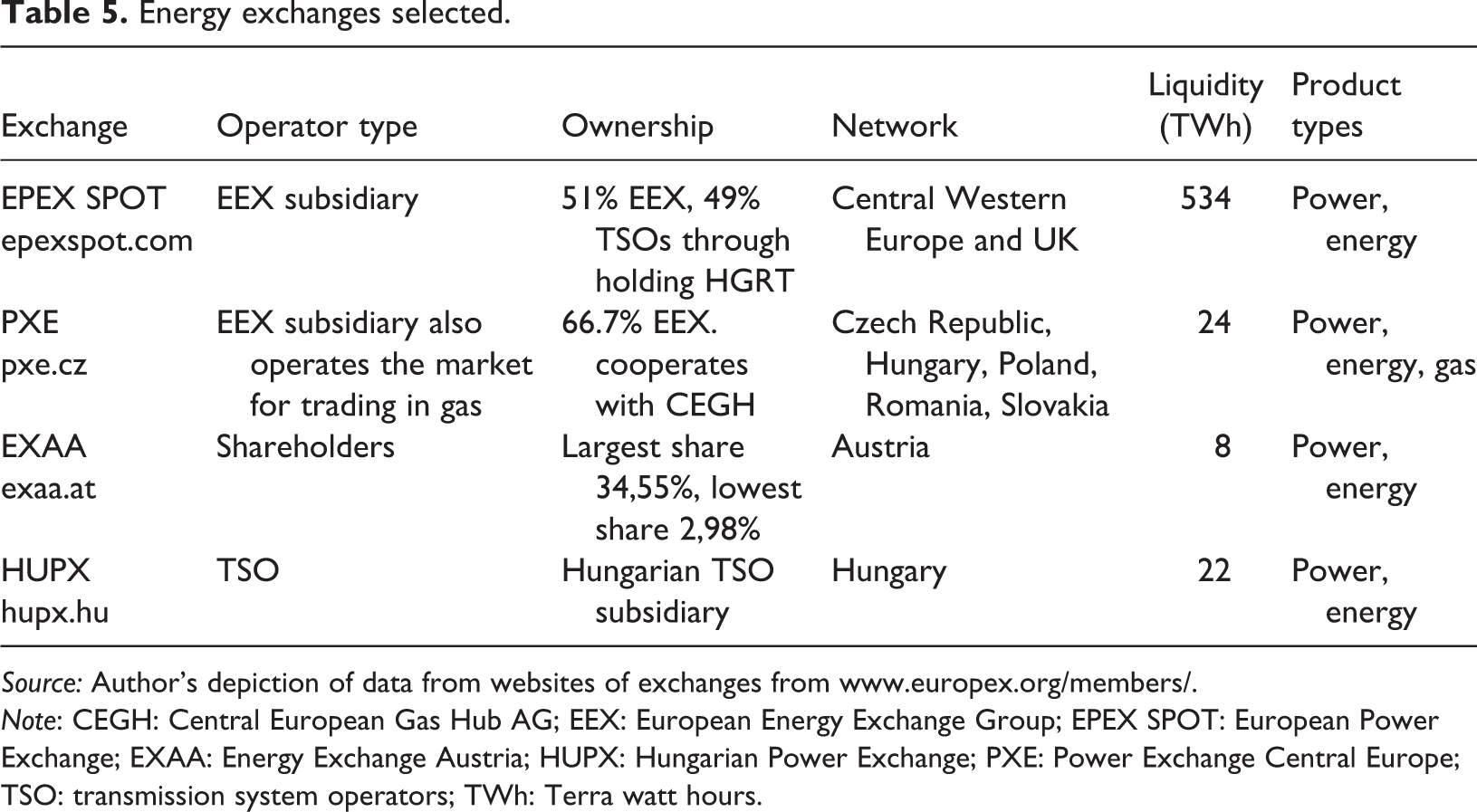

This section presents the findings from the interviews and the desktop research regarding the assessment of existing online exchanges and their practices. For this, the Tables 5, 6 and 7 show the selection of exchanges based on their company structures and network characteristics regarding (a) their geographical network that indicates the extent of market access, (b) liquidity or critical mass organized through the exchange(s) and (c) commodity (product type) through which standardization of services is achieved. First, we will explore major regulatory characteristics.

Energy exchanges selected.

Source: Author’s depiction of data from websites of exchanges from www.europex.org/members/.

Note: CEGH: Central European Gas Hub AG; EEX: European Energy Exchange Group; EPEX SPOT: European Power Exchange; EXAA: Energy Exchange Austria; HUPX: Hungarian Power Exchange; PXE: Power Exchange Central Europe; TSO: transmission system operators; TWh: Terra watt hours.

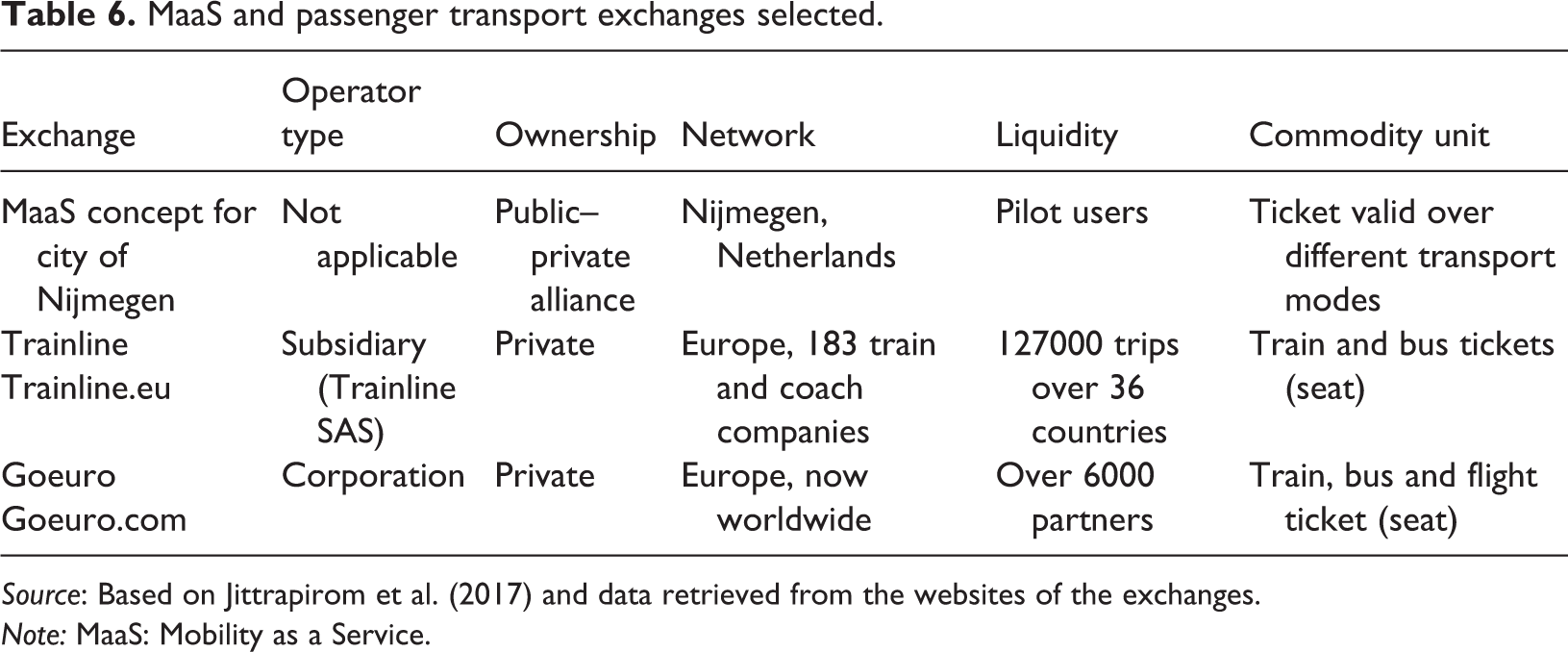

MaaS and passenger transport exchanges selected.

Source: Based on Jittrapirom et al. (2017) and data retrieved from the websites of the exchanges.

Note: MaaS: Mobility as a Service.

Freight exchanges selected.

Source: Based on selection from Jain and Bruckmann (2017), https://impargo.de/en/blog/top-10-freight-exchanges and https://www.tipeurope.com/top-10-europes-most-popular-freight-exchange-platforms/. Data from websites of the exchanges.

Note: C: customers; U: users; O: offers/day; TPA: trucks per annum; FTL: full truck load; LTL: less than a truck load.

Regulatory characteristics

Regarding energy, a competitive, internal energy market cannot exist without independent regulators who ensure the application of the rules (Market Legislation, n.d.). Within this framework, regulators must be independent, can issue binding decisions to companies and monitor data that must be submitted by operators, generators and suppliers. Regulators from different countries must also cooperate with each other to promote competition, to support opening of the market and to establish an efficient and secure energy network system.

Thus, the energy markets are highly regulated while infrastructure and services are unbundled. Due to these regulations, the ownership structure is moving towards balancing the expectations of transmission system operators (TSOs; focus, ensure security of supply) and the market participants, which are now major stakeholders in the exchanges. Most energy exchanges themselves do not own assets. In Table 5, representative examples of EPEX SPOT (electricity) and Power Exchange Central Europe (PXE) (gas) have been chosen.

Regarding transport, only licensed transport companies (passenger and freight) are allowed to offer services anywhere in the EU. Further, regulations (EC no. 1071/2009) in road freight transport exist regarding admission of road transport companies to the profession of road freight carrier and regarding access to the international road haulage market.

Also, online passenger transport exchanges (Table 6) are implemented for improving matching demand and supply. Trainline and GoEuro are private, online intermediaries without assets, which are offering multimodal passenger transport solutions. Most UPT services are organized and subsidized by (local or regional) authorities. The regulations regarding pricing are binding all subsidized service operators. These issues create serious challenges for the development and implementation of, for example, MaaS based on an independent platform.

The selection of the first four road FTEs, mentioned in Table 7, is based on an underlying analysis of hundreds of exchanges in Europe. A brief preview on their grouping of maturity precedes the selection of exchanges. Consensus exists between freight exchange experts that Timocom, trans.eu, Teleroute and Wtransnet are the top four road FTEs, given their geographical focus, number of users and transactions. Further, the developments of these exchanges for adjacent markets like warehousing and route exchange are also visible. Uber Freight is not active in Europe yet (Krigslund, 2018) and therefore not further discussed here. A list of six other exchanges (Raaltrans.cz, box24.de, 123cargo.eu, cargo.lt, lkwonline.de, schuettgut-boerse.com), mentioned at least once in interviews but not included in Table 7, builds a second important group of freight exchanges. However, their geographical coverage and their functionalities are already covered by the top four. Finally, the remaining hundreds of exchanges do not have mature practices similar to any of these top four (or ten) exchanges. Thus overall, the state of practices using exchanges varies considerably within the road freight sector. A major characteristic of these road freight exchanges is their status as third-party online intermediaries that do not own transport related assets.

Table 7 also includes the list of rail-focused exchanges. The multimodal freight exchanges, for example VIIA+, are asset owners (terminals) and operate four rail lines in partnership with European rail operators. For Freit-one and XRAIL, little relevant information could be found, making an assessment of its performance impossible. These exchanges, however, do not seem to be solving the main problem in the rail freight industry: the lack of direct access to customers, which the new market entrants are confronted with (Jain & Bruckmann, 2017). This problem can presently not be solved by the regulatory bodies, although their main task is to ensure a non-discriminatory access to the rail infrastructures (Article 10.7 of Directive 2001/12/EC, Articles 30 and 31 of Directive 2001/14/EC). Hence, there are differences in maturity between multimodal freight exchanges and the classic rail freight industry, and therefore they are separately assessed.

The conclusion is that the selected network industries have varying ownership structures for online exchanges and different regulations. The maturity of exchanges in organizing liquidity (number of offers and volume) in the energy sector and in road freight transport is higher than in rail freight transport. Regarding passenger transport, no clear conclusions can be drawn. Nevertheless, in all network industries, the issue of ownership structure appears to be significant. Especially, the preconditions that enable new entrants to a market are relevant.

The first step in the application of the CMM framework is to assess the emerged market-related practices for exchanges in the selected network industries. That will be followed by an assessment of the operational practices.

Assessing market-related practices in online exchanges

The market-related practices, on which data were collected in the interviews, were evaluated on the following criteria and their interpretation according to the initial CMM.

The first concerns strategic market management (a). This criterion focusses on the ability of exchanges to strategically align their goals to customer benefits, to societal goals and to regulatory requirements. The assumption is that standardization and automation enable growth in market. Further, a higher level of maturity is related to how exchanges seek higher benefits through understanding challenges exchange participants face outside the current exchange markets to integrate adjacent markets (b) covered by different participants in the exchange. This enhances the level of competition. As a consequence, the practices relating to design of products/commodities (as substitutes) (c), but also the design of algorithms for auctions (d) to organize liquidity on the exchanges, lead to differences in maturity. Here, practices related to subscription of products (e) and rebates to attract future participants and retain the existing ones are significant. The difference of maturity arises depending on whether the practices aim at continuously organizing and optimizing operations to increase market access. Consequently, this requires the assessment of maturity relating to market and stakeholder management (f) which measures how an exchange interacts with market players, shareholders, regulators and customers to be perceived as a reliable, fair and competitive partner. Finally, practices relating to defining and ensuring adherence to market (or behavioural) rules (g) must be evaluated to assess how exchanges are made safe and reliable for their participants.

In this analysis, we will focus on those practices whose assessment results in regulatory requirements. Therefore, we will not further discuss the practices related to subscription (e) and market and stakeholder management (f).

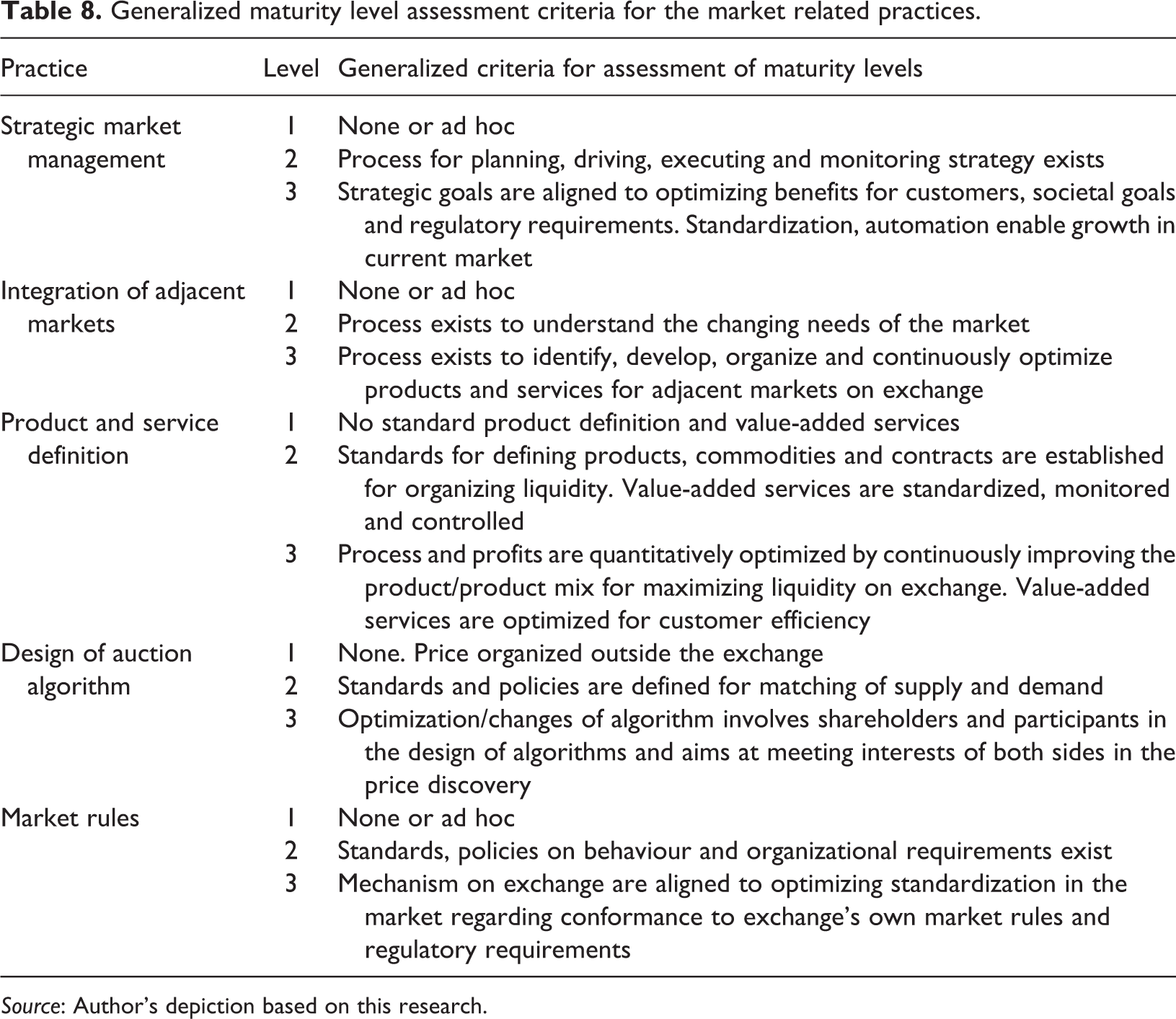

An overview of the generalized maturity level (1 = low; 3 = high) assessment criteria of the market practices is depicted in Table 8.

Generalized maturity level assessment criteria for the market related practices.

Source: Author’s depiction based on this research.

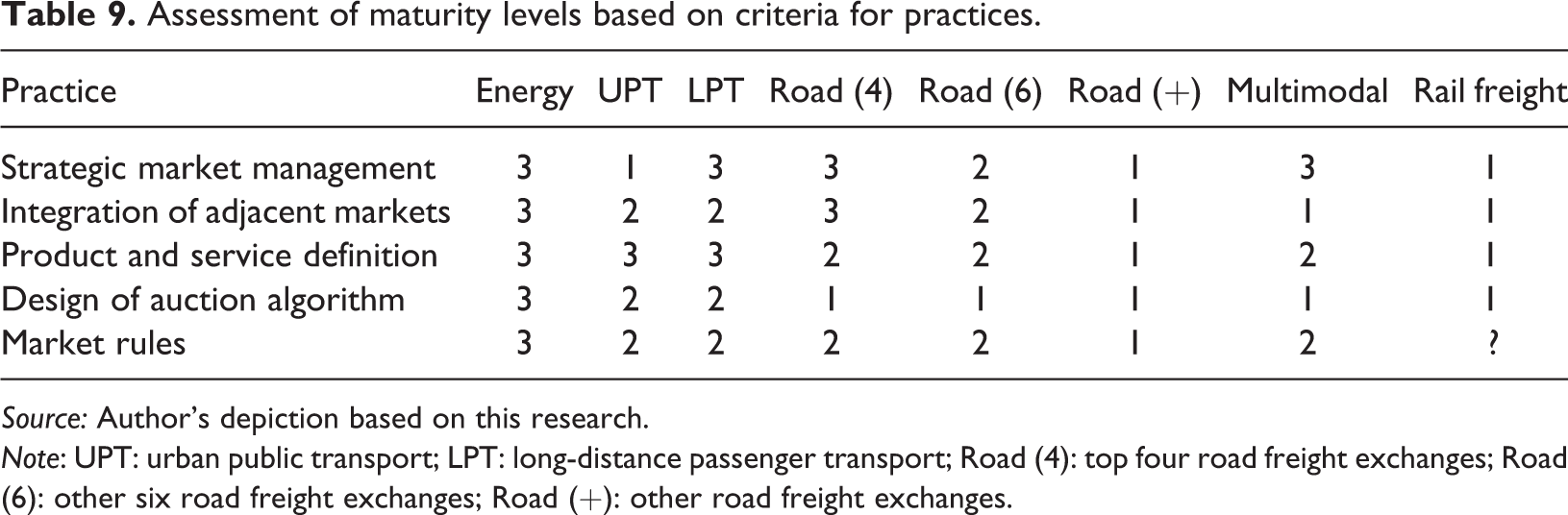

The assessment of maturity levels based on the criteria for each practice mentioned in Table 8 is depicted in Table 9. Next, the reasons for the assessment scores will be briefly explained.

Assessment of maturity levels based on criteria for practices.

Source: Author’s depiction based on this research.

Note: UPT: urban public transport; LPT: long-distance passenger transport; Road (4): top four road freight exchanges; Road (6): other six road freight exchanges; Road (+): other road freight exchanges.

Strategic market management

Energy exchanges align their strategic goals and operational processes consequently to the legislation and regulation regarding harmonization of rules and creation of internal market integration. By doing so, they improve liquidity through cross-border flows and reduce prices by accepting competition and complying with a high level of system security. They organize an easy market access, attracting new participants. For example the Energy Exchange group (EEX) has taken over several other exchanges (EPEX SPOT, PXE, Gaspoint Nordic (in Denmark) and some other exchanges (Members of EEX Group, n.d.). Further, the power derivatives operated by PXE are run on the EEX trading system (Power Exchange Central Europe, 2017). Exchanges are integrated and commoditization enables optimization over different products. Further, the EEX Group organizes compliance with regulations (‘One Platform – Three Regulations’, n.d.) for its exchanges. Overall, we consider such energy exchanges on the aspect of market management at maturity level 3.

In contrast, the implementation of MaaS in UPT is mainly in a stage of pilot projects, at a local level. Exchanges in this field have not matured yet. The practices relating to automation and using commoditization over different transport modes to organize multimodality may be in place in the pilots, but since structural, large-scale, policies are not yet in place, we consider them to be at maturity level 1.

In LPT industries, multimodal and door-to-door service is an unmet challenge (Montero & Finger, 2017). GoEuro and Trainline are now working on multimodal transport through commoditization and improved automation to optimize network benefits for their customers. For example, GoEuro sees extraordinary potential to transform travel booking by expanding their platform to the fragmented, mostly offline systems for managing transport globally (GoEuro, 2018, para 6). Trainline has also been expanding its business in Europe for train and bus travel. Further automation is being used for expanding market access between different exchanges (e.g. GoEuro with booking.com). Overall, we associate the selected transport exchanges with maturity level 3. This level may, however, be lower for other long-distance passenger exchanges, not addressed in this analysis.

Road FTEs show different maturity levels in regards to the practices of strategic market management. Goals for the top 10 exchanges appear to be aligned with customer benefits and societal goals related to carbon dioxide (CO2) emission. With a takeover of the Wtransnet exchange, the Alpega group (which also owns Teleroute and 123cargo.eu) chooses a strategy comparable to energy exchanges. However, a certain level of ad hoc management is needed (e.g. Terms and Conditions, 2019). Thus, there is still much room for improvement of automation. Timocom, on the other hand, expands its market reach by organizing tracking of transport orders through strategic cooperation with 245 telematics operators in Europe. Also, the multimodal freight exchange, VIIA+, increases its network services for rail and road transport by ‘putting all parties into contact, connecting them via a simple, safe solution’ (Multimodal Will Also Have Its Freight Exchange’, 2015, para 7). Consequently, multimodal services become possible through commoditization (e.g. intermodal transport units) and automation. These practices increase the market access. The maturity of the top four FTEs and multimodal FTE therefore is at level 3. Exchanges that cannot organize security but are ready to connect to other exchanges and have a strategy for market growth (e.g. the other six exchanges) are considered at maturity level 2. We recall that the majority of road FTE do not appear to have practices in place to expand their market access to ensure higher liquidity on the exchanges. They may succeed through individual (ad hoc) efforts (maturity level 1).

The rail FTE, XRAIL is restricted to the network of six partner railways. It aims to enhance the international wagonload with the implementation of international capacity booking (XRAIL Alliance, 2015). Since no further information regarding liquidity could be found, we consider its maturity to be at level 1.

The lesson to be learned for the freight transport industry concerns the setting of concrete goals regarding the market strategy (notably improving access to different markets) and developing multimodal transport services through the organization of a structural cooperation of involved freight transport companies. This should be supported by freight transport regulators. The alignment of organizations to the EU modal shift goals must accordingly be monitored and enforced (as in the energy industry). In this regard, interviewees emphasized the need for a political willingness to achieve such a state and that regulators both at state and EU levels must be able to function independently.

Integration of adjacent markets

Energy exchanges regularly focus on, for example, bilateral (over the counter) markets for identifying, developing and organizing new products and services on exchange to improve the efficiency for their existing and potential participants. For example, in the German market, a new product in the renewable energy market offers contracts on a 15-min basis instead of hourly basis (EPEX SPOT Intraday, 2014). In doing so, they improve liquidity and positive network effects for their participants. They do so by using a standardized project-oriented approach, for example, with the engagement of an exchange council (‘Role of the Exchange Council’, 2018). Once launched, the product is continuously optimized like all other products. This equals a maturity level 3.

Exchanges in UPT and LPT appear to be at a stage of organizing liquidity, working on the understanding of the changing needs of their customers. Increasingly, links to adjacent markets are pursued, for example in hotel booking, but such links are not yet made systematically. The sector starts bundling of online ticket booking over various transport modes and additional services for billing and payments. Maturity level in this aspect is hence assessed at level 2.

Some road FTEs appear to be understanding the changing needs of their customers and therefore have started to offer solutions like route exchange (Wtransnet) and warehouse exchange (Timocom) to identify and optimize efficient solutions for participants (maturity level 3). However, this practice is not standardized in all FTEs, like it is in energy exchanges. Overall, this practice for the top 10 exchanges matches maturity level 2 but is almost ready to move to level 3. Such a process is however absent, or ad hoc organized, in the majority of road FTEs (maturity level 1).

No mention of similar practices were found regarding XRAIL and VIIA+ (maturity level 1).

The lesson to be learned for rail freight is that it is extremely relevant to improve the understanding of the needs of customers, both in the core and adjacent markets, to make these needs leading in service provision. Further, to look for adjacent markets to increase the rail market share, an update in policies to stimulate multimodal transport is required. Finally, this might also be linked to other markets, for example, in warehousing or distribution. In terms of regulatory control, an (transport mode-) independent body for solving multimodal transport issues presently lacks.

Product and service design

All exchange experts stressed that a mature exchange standardizes the products and the contracts. Energy exchanges differ in that the products and commodities are clearly defined for long-term and short-term markets. Further, the contracts, which are organized by the exchange (except for bilateral contracts), are highly standardized and the practices are related to quantitatively optimizing the processes and profits through continuous improvement (as seen in the case of integration of adjacent markets) of the product (or product mix) to maximize the liquidity (volume or number of transactions) on the exchange (maturity level 3).

In UPT and LPT industry, the product is generally related to a free seat and the ticket as a contract is often standardized over all modes, therefore optimization on products (or product mix) takes place. Since high competition exists in the market for LPT, we associate these exchanges with maturity level 3. UPT is, in most cases, focused on societal goals, and therefore profit maximization is not the main focus. In particular, MaaS aims to provide an exchange with maturity level 3.

Most road FTEs appear to be load boards for road transport. Very few of them are involved in the finalization of contracts. The road haulage orders usually lead to spot or short-term deals and not often to long-term contracts (Nandiraju & Regan, 2008). For the top 10 exchanges, the products like less than a truckload (LTL) or full truck load (FTL) are well defined. Therefore, standards for defining products/commodities appear to exist to establish liquidity on exchanges. However, clear strategies for the optimization of LTLs to FTLs (i.e. optimization over multiple products) could not be found. At this point, an answer regarding contracting on exchanges cannot be fully provided. Further research is required in this area. We currently associate such exchanges with maturity level 2. Moreover, of the many hundred FTEs, many may not have a standardized product definition and they allow for all types of requests and ad hoc agreements (maturity level 1).

Regarding to rail freight transport, 19 wagon types with different characteristics were identified as a basis for the containerization of transport (Bruckmann, 2006), indicating a lack of standardized products. New customers also face obstacles when approaching the rail freight company for services since a customer-specific contract must exist before any transport takes place (Jain & Bruckmann, 2017). The related transaction costs create resistance to become an active partner in an exchange that should aim to easily match demand and supply of multimodal services. Therefore, we associate rail FTEs with a maturity of level 1. However, VIIA+ offers products like semitrailers, containers and swap bodies that are compatible to all modes. The focus on multimodality is evident in their mission statement to become ‘a neutral intermodal operator working for the road and with the road to provide a joint service suited to market needs’ (The Main Raison d’être of VIIA, 2016, para 6). This strategy should be associated with maturity at level 2.

Learning from energy exchanges, regulation at EU level regarding contract standardization (including enforcement and monitoring through regulators) for rail freight and multimodal transports could act as an enabler for an increased participation on FTEs and improve the potential for a modal shift. It is expected to lead to significant improvements in organizing transparency and multimodality of services offered by the exchanges. The example of VIIA+ illustrates this.

Design of auction algorithm

Energy exchanges involve shareholders and participants in the design of auctions and price building to meet the interests of both sides on exchange. Price coupling of regions is a crucial contribution to a harmonized European electricity market. The integrated European electricity market, enforced by Commission Regulation EU 2015/1222, is improving liquidity, efficiency and social welfare (PCR & EUPHEMIA Algorithm, 2017). Further, the auctioning focuses on price building and optimized matching of aggregated supply and demand. In this regard, energy exchanges are governed by regulatory requirements and ensure neutrality through anonymity of all participants during auctioning. Moreover, the prices on these exchanges (once finalized) are publicly communicated, therefore serving as a reference for price in bilateral markets. We therefore associate energy exchanges in this respect with a maturity of level 3.

In UPT and LPT, the matching of demand to supply is in the hand of the ticket buyer. Regarding MaaS, a pilot project Ubigo, a transport broker service in Gothenburg (Sweden), showed a reduction of the participants’ car use. Unfortunately, the revenues of the platform remained low because it was unable to increase the prices for public transport (Jittrapirom et al., 2017). So, although the MaaS platform provides a virtual matching mechanism, it is still tied to public policy influences on pricing and cannot enable a fully open and dynamic price discovery process. Hence, we consider them to be at maturity level 2. In regards to long-distance transport, Morris (2017, para 2) states: ‘Though a third party app allowing users to bid for upgrades (in rail) is new, a number of airlines already offer similar services’. Seatfrog, the exchange referred to here, plans to expand to the European rail network, Trainline and GoEuro do not yet provide this facility, but standards and strategies are in place to achieve a maturity level comparable to the air transport industry (maturity level 2).

Road FTEs mostly facilitate information exchange related to services and (negotiation for) contracting which then takes place outside the exchange. Hence, if standards and procedures are defined for auctioning, they are manually applied. In some interviews, it was mentioned that such mechanisms are relevant only when participants from both sides see the added value of, and hence desire for, such a functionality. In case of Wtransnet, offering route exchange services for regular routes, some automation of matching is possible (Route Exchange, 2019). Timocom, since 2017, also allows participants to electronically document their transport orders. Currently, very few of them publicly give information about organizing prices and capacity (Jain and Bruckmann, 2017): suppliers make different price offers during tendering procedures. More research is required regarding which information on prices the exchanges provide to the clients. Other interviewees stated that FTEs do not send price signals in the market since they do not have transparent price information (especially in case of spot markets). Therefore, we associate the current maturity of road FTEs with level 1.

In rail freight transport, the prices are non-transparent and get complicated for cross-border shipments (Endemann, 2016). Xrail does not organize the prices due to anti-trust regulations. We understand that XRAIL offers a capacity search service for single wagon loads triggered by specific demands. However, no fixed and transparent price component is involved (maturity level 1) and here also, more research is required. No information regarding price discovery was found for VIIA+ (as per general terms and conditions, this possibly takes place bilaterally). Thus, we associate the rail and multimodal FTE practices with maturity at level 1.

The lesson learned is that price transparency, price harmonization and a higher level of automation of contracting incentivize all stakeholders for cooperation. Regarding rail freight transport, it would contribute to more multimodal services and a better organization of risk and revenue sharing for such services. Independent regulatory bodies could contribute to the establishment of such transparency and harmonization.

Market rules

Energy exchanges perform regular analysis and reporting on conformance to market rules (behavioural rules). For example, REMIT introduces a legal framework for identifying and penalizing insider trading and market manipulation in wholesale energy markets across Europe (REMIT, 2017). Stringent quality checks support companies to achieve the highest data quality to the benefit of regulatory compliance (One Platform – Three Regulations, n.d.), the results of which are publicly reported. Both regulators and market participants benefit from this reporting. For example, extension of the VAT Directive recommended by the energy industry to protect energy and emission markets from VAT Frauds (Common Energy Sector Statement, 2018). The downside, according to the interviewees, is that the administrative tasks due to regulation have increased. Nevertheless, the maturity of the energy industry in this respect is perceived to be at level 3.

The UPT and LPT also have to comply with certain market rules especially if they want to provide international services. However, the research did not find coordinated practices related to standardization of rules in the industry to optimize the conformance to market rules (maturity level 2).

Regarding FTEs, the practices appear to be similar to passenger transport. Thus, each exchange defines its own market rules that evidently are in line with EU regulation. This implies that various sets of standards and market policies are applied. It was further observed that verification on conformance to regulation regarding minimum wage or working condition differs significantly between the top four (or even top ten) road FTEs and the rest. The top-level exchanges put higher effort in standardization of exchanges, since much problems result from different implementation of EU regulations in the member states and additional national regulations (CLECAT, 2017). Thus, we associate maturity of the road industry in this respect with level 1 for the majority of exchanges, where no standardization practice exists, and for top 10 exchanges at level 2. Practices in this respect for rail FTEs could not be found. In VIIA+, terms and conditions along with market rules for exchange exist, indicating standards and policies exist (maturity level 2).

The learnings from energy exchanges deal with standardization of market rules and public reporting of compliance to these rules. These practices can ensure better monitoring of unwanted actions that might jeopardize the business of exchange participants. Further, since regulators in the energy industry can mandate direct actions to companies, this may also be relevant for the multimodal freight transport industry. It is therefore concluded that additional market rules, possibly at EU level, will be required for multimodal freight exchanges.

Assessing operational practices of online exchanges

In line with the interviews, the maturity assessment of operational practices of online exchanges should focus on improving the efficiency of operations, hence customer efficiency.

The practices related to the adoption of an exchange by participants through registration (a) is the entry point for improvement in FTEs. Further, exchanges differ in maturity regarding how and why they organize services (b) with partner organizations, whether the focus is on standard operations or on optimizing customer satisfaction while expanding markets. Regarding expanding markets, practices related to the level of communication (c) are highly important. In the interviews, the need for operationalizing auctions (matching supply and demand) (d) was also recognized. The practice related to procedures for clearing and settlement (e) after the matching process must also be operated efficiently. Further, the need for organizational development (f) to manage changes and improve market-oriented services along with the ability to focus on process automation (g) using advanced Informations and Communications Technology (ICT) technology was identified. Finally, since all operations are based on data, practices related to data analytics and information sharing (h) must be necessarily assessed.

Since we discuss only practices with a clear link to regulatory requirements, we leave practices related to service organization (b), communication (c), operationalizing auctions (d), organizational development (f) and process automation (g) further undiscussed. Table 10 presents the assessment of maturity levels of the remaining selected operational practices of exchanges in the selected network industries.

Generalized maturity level assessment criteria for the operational practices.

Source: Author’s depiction based on this research.

The assessment of maturity levels based on the criteria for each practice mentioned in Table 10 is depicted in Table 11. Next, these associations will be briefly explained.

Generalized maturity level assessment criteria for the operations related practices.

Source: Author’s depiction based on this research.

Note: UPT: urban public transport; LPT: long-distance passenger transport; Road (4): top four road freight exchanges; Road (6): other six road freight exchanges; Road (+): other road freight exchanges; M.Modal: multimodal freight exchange; RF: rail freight.

Registration

Energy exchanges follow a strict registration procedure for their participants, including services to protect from frauds. Hence such practices (including charging registration fees) and verification procedures enable safe registration: they help to select only the serious customers to join the exchange. The operational efficiency of the registration process also facilitates the management of changes in the market access (e.g. when one exchange takes over the other) and compliance to regulatory requirements. We perceive this to be at maturity level 3.

In case of UPT (including MaaS) and LPT, standard processes and policies exist for registration using social media accounts, credit cards or other digital payment methods. These may be susceptible to possible frauds. We consider such practices related to maturity level 1.

In road FTEs, apart from the selected top four exchanges, most road FTEs offer simplified registration procedures for potential participants. Some FTEs offer the possibility of registration with an initial trial period for free or a lower price. The downside of these approaches is the relative lack of quality control and the possibility of fraud and offering of insufficient service levels. These processes are therefore associated with a maturity level 1. The selected top FTEs, in contrast, have started to introduce more checks and rules for registration. For example, Wtransnet’s quality assurance procedures filter new companies and continuously monitor their behaviour in accordance with the standards accepted at the time of their registration (The QAP System, n.d.). Thus, such exchanges exhibit a maturity at level 3. Such standards also include compliance to minimum wage policies under EU regulations for working conditions. In collaboration with the Romanian Road Authority, 123 cargo recently started the online service to verify the Transport and Forwarding license of all Romanian members (Real Time Check, 2018). Further, some of the top 10 FTEs adopted clear standards and policies regarding registration, however, do not yet perform similar quality assurance services like Wtransnet or 123cargo (maturity level 2). Again, such practices are not typical for a majority of FTES. Some interviewees emphasize that mature exchanges should handle such quality assurances during registration themselves, for which no regulations are required. Moreover, no knowledge of any reporting requirements surfaced in the interviews. We associate an absence of such practice to level 1. Finally, details regarding both VIIA+ and XRAIL could not be found. We, however, assume that some kind of registration process is in place. Further research is required in this regard.

Learning for freight transport focuses on the monitoring of the adherence to policies regulatory requirements in a standardized form at EU level. Due to international transport, more shared knowledge on fraudulent companies and practices can improve operational efficiency of all freight organizations. Building and sharing databases in this respect can help to track fraudulent companies and practices.

Clearing and settlement

Energy exchanges ensure that the trades are also delivered and paid via clearing agencies. Thus, European Commodity Clearing (ECC), a recognized partner of TSOs in many European countries (About ECC AG, 2019), ensures physical settlement of power, natural gas and emission allowances. It assumes that the counter party complies with regulatory standards (e.g. EMIR) thereby ensuring security of participants and improving efficiency (maturity level 3).

In MaaS and LPT, clear standards and policies are defined, for example, payments generally organized via credit cards or apps (maturity level 2).

Practices of road FTEs regarding clearance appear to be often organized by the exchanges individually. Research regarding risk management indicates that some mechanism of debt recovery on various road freight exchanges exists. For example, Timocom successfully helped 89% of all creditors to successfully recover their claims (Debt Collection International, n.d., para 1). Wtransnet guarantees the recovery of 90% of the invoice amount in trade relations established between companies from a European country it covers, whether EU or not (With a 90% Coverage, 2012, para 1). For this, it collaborates with the multinational company Coface, thus also indicating a focus on operational efficiency. This information indicates that such exchanges are themselves acting as regulators aimed at improving the operational efficiency. Further market efficiency through standardized policies and use of a central clearing agency (e.g. for Alpega) could be a possible next step for such exchanges. We assess the maturity of current practices in this respect at level 2. In the other top 10 road FTEs, the maturity level of this practice differs with the particular exchange. Some apply a mechanism for risk management, and others do not have such practices. Thus, whereas some exchanges can be associated with reaching level 2, the rest perform at level 1.

For VIIA+ general terms and conditions exist, however, no evidence of a clearing agency could be found. Similarly, details to XRAIL could not be found. Therefore, we associate both with maturity level 1.

The lesson learned is that if initial registration is strict, many risks may be reduced for consecutive processes on online exchanges. Further, a higher maturity stage of an exchange requires that insurance or prepayments are applied to reduce risks of counter parties. However, this is not a regulatory requirement. What, however, can be explored is how clearing agencies and standardizing reporting policies can improve the efficiency of freight exchanges in this respect by applying regulatory requirements uniformly, weeding out unserious participants.

Data analytics and information sharing

As mentioned earlier, practices in energy exchanges related to reporting on performance indicators are standardized and automated on all exchanges, including those for regulatory requirements. By doing this, they aim at achieving transparency. Results of auctioning of each product, including timings of process execution, price information, trends and so on, are transparently and publicly communicated. Processes and products can therefore be continuously optimized to organize liquidity and trust in exchange (maturity level 3).

Practices regarding data analytics in MaaS (dashboard on hubs and user requests) and LPT exchanges (e.g. most popular trains in each country) can be observed indicating that processes and policies exist for measuring and publishing operational efficiency. However, a standardized reporting of key performance indicators related to promised benefits especially regarding societal goals is not yet a common practice. The growth in user-related and other operational data is also not conclusive (maturity level 2).

In road FTEs, information on growth of users, improvements regarding CO2 emission and reduction in return trips is present, which indicates that some processes and policies for measuring (e.g. Timocom’s transport barometer) and publishing on performance exist; however, it is not conclusive. For example, 123cargo.eu states: ‘based on an algorithm that considers your (participants) scoring and activity on the platform, an indicator is calculated to help you better understand the type of activity of the collaborator you are consulting’ (Company Activity indicator, 2018). Hence, we associate such practices for top 10 exchanges with maturity level 2. Some interviewees also mention that the exchange participants should become more willing to understand the gains through data sharing in a relevant and secure fashion. No indication regarding the use of performance indicators for many other road FTEs and XRAIL was found (maturity level 1). VIIA+ shows scattered information which like the top 10 road FTEs shows information regarding the performance of the exchange; however, it is also not conclusive. It may be possible that these analytics are exclusively available to participants of the exchange (maturity level 2). More research is required in this regard for road FTE, rail and multimodal FTEs. It does appear though that when they function only as load boards, operational efficiency can be difficult to measure.

The learning for the freight transport industry is that some kind of regulation for freight exchanges at EU level to report on their contribution to the reduction of CO2 emissions can be helpful. Further, this information should be standardized to support comparison on service efficiency and relevant information should be publicly available, both at national and EU levels. This contributes to market efficiency enabling dispatchers and forwarders to better make trade-offs between two or three exchanges in their search for transport services. Also, standardization of freight papers and customs clearance can enhance process efficiency and improve the basis for data analytics.

Conclusion

In this article, the maturity of online exchanges in the rail freight transport industry is compared to those in passenger transport, road freight transport and energy supply. This comparison showed a relatively low level of maturity in modern service development in freight transport. Moreover, it suggests that regulation at EU level can play a significant role to improve the modal shift from road to multimodal freight transport, including rail services. The presented analysis involves an initial step towards a more detailed analysis in this respect. This then provides a basis for studying the steps required for transitioning the current practice in rail freight to a higher maturity level.

We interpreted the theory on capability maturity as follows. Exchanges of maturity level 1 appear to focus on some way of connecting the two sides of an exchange. The exchanges of maturity level 2 appear to focus on a more standardized and transparent way of organizing liquidity and understanding customer requirements to offer products and services that help them to better grow in the current markets. Exchanges at maturity level 3 appear to understand and systematically and dynamically deal with the markets and problems of their participants outside the markets. Thus, they focus on offering solutions in adjacent markets to retain and gain new customers. Moreover, at this level, procedures are highly standardized, fully automated, largely communicated to customers and the public, and the focus is on compliance to a set of jointly agreed rules. Assessments of practices along these different levels showed that energy exchanges, which are currently highly regulated, are at a maturity level 3. In contrast, such practices regarding multimodal freight exchange using rail and road are at a lower maturity level. Insights from the energy industry can, however, contribute to establish more mature practices in the freight transport industry.

The lesson is that regulation is important for organizing easy access to markets and increasing transparency in the achievement of goals. In this regard, some old rules have to be renewed. As observed in the interviews, the regulations for intermodal transport were made a quarter of a century ago and ongoing globalization and digitalization require an update of these regulations. Initiatives such as MaaS in passenger transport and similar concepts in freight transport underline that active policymaking is needed for implementing multimodal freight exchanges and creating a market setting that enables a significantly better cooperation between road and rail.

Footnotes

Acknowledgements

The authors are grateful to all the experts who have taken time to give an interview and provide examples and insights that were considered useful for this research.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.