Abstract

We employ a Cournot model with interdependent demands to explore the interaction between demand and cost complementarities in mitigating upward pricing pressure, post-merger. The analysis reveals that even substantial increases in the HHI post-merger need not raise competitive concerns when output is redistributed from single-market to multi-market providers. Furthermore, the numerical simulations indicate that there is a wide range of demand and cost complementarity parameters over which even monopolization of the market would not be expected to result in higher prices. These findings may constructively inform merger policy and provide useful context for application of the DOJ/FTC horizontal merger guidelines in an increasingly digitized (network) economy.

Introduction

A merger that simultaneously increases both market concentration and multi-market participation gives rise to countervailing effects. 1 The first effect is an increase in market concentration that places upward pressure on market price. 2 The second effect is an increase in multi-market participation that exerts downward pressure on market price when demands are complementary. This second effect is compounded in the case of cost complementarities (i.e., efficiencies that derive from multi-market participation). Complementary demands are common in network industries because increased traffic flows from one node to another node on a telecommunications or transportation network generate increased traffic flows in the reverse direction and to other nodes on the network (Larson et al., 1990; Weisman, 2005). 3,4

Williamson (1968) derives the critical level of cost savings necessary for a merger to be welfare-neutral. He finds that even modest merger efficiencies can dominate significant increases in market power in producing net welfare gains, post-merger. 5 Weisman (2003, 2005) employs a model of Cournot oligopoly to examine the effects of mergers and multi-market participation on pricing behavior but does not explore the interaction between cost and demand complementarities or measure the empirical significance of these effects. The interaction between cost and demand complementarities is likely to play an increasingly prominent role in the application of antitrust to a digitized economy.

This article builds upon previous research in three important respects. First, we formally model the tradeoffs between cost and demand complementarities in mitigating upward pricing pressure, post-merger. 6,7 Second, the numerical simulations complement the theoretical findings by delineating the various combinations of cost and demand complementarities that refute the contention that “Mergers resulting in highly concentrated markets that involve an increase in the HHI of more than 200 points will be presumed to be likely to enhance market power.” 8 Finally, the analysis identifies combinations of demand and cost complementarities that may contest the view that “Efficiencies almost never justify a merger to monopoly or near-monopoly.” 9

The main findings of this article are as follows. First, mergers that increase both market concentration and multi-market participation need not result in upward-pricing pressure, even in the absence of cost complementarities. Second, there is an increasing tradeoff between demand and cost complementarities in mitigating upward-pricing pressure, post-merger. Third, cost and demand complementarities interact to negate the presumption of upward pricing pressure that would typically accompany significant increases in the HHI post-merger. 10 These effects are likely to be particularly important in a digital economy wherein cost and demand complementarities can interact to engender mergers that increase market concentration while decreasing prices. The larger footprint of the combined firms, post-merger, allows for demand externalities to be internalized. Finally, the numerical simulations indicate that even a doubling of the HHI post-merger need not be dispositive of competitive concerns.

The format for the remainder of this article is as follows. Section 2 introduces the notation and the formal model. The main findings are presented in Section 3. Section 4 discusses the numerical simulations. The implications of this analysis for the Department of Justice and Federal Trade Commission Horizontal Merger Guidelines (HMG) are reviewed in Section 5. Section 6 concludes.

The model

To investigate the problem of interest, we employ a Cournot model with linear, complementary demands in which single-market providers (SMPs) and multi-market providers (MMPs) may serve the market simultaneously. 11 The linear functional forms facilitate both closed-form expressions for the key variables and the numerical simulations. There are two symmetric markets identified as market A and market B. The inverse market demand functions for these two markets are given by:

and

where α > 0 and

and

The main findings

Recognizing that

and

To explore the relationship between own and cross-effects, let

The first proposition establishes the equilibrium outputs for the SMPs and MMPs.

Proof: Solving (5) and (6) simultaneously yields

and

where

Proof: Computing the difference between (8) and (7) and simplifying yields the result.

The rationale for Corollary 1 is that the SMP does not consider the effect of its output choice in market A on demand in market B and therefore puts less output on the market in comparison with the MMP. This explains why substituting MMPs for SMPs yields lower prices as shown in Proposition 2. Note also that the difference in the output levels of the MMP and the SMP vanishes in the limit as the complementarities approach zero or

Substituting (7) and (8) into (1) or (2) and omitting superscripts since the markets are identical yields the equilibrium market price, or

Corollary 2 establishes that (i) cost complementarities decrease the equilibrium price when the market is not served exclusively by SMPs; and (ii) these price decreases are larger with stronger demand complementarities when the market is not served exclusively by MMPs.

Proof:

The next proposition examines the tradeoff between SMPs and MMPs. Specifically, holding the number of market providers (n) constant, a one-unit decrease in the number of SMPs (n − k) coupled with a one-unit increase in the number of MMPs (k) causes the equilibrium price to decrease. Cost complementarities

(i)

Proof: To prove part (i), partially differentiate (9) with respect to k to obtain

since

The proofs of parts (ii) and (iii) are straightforward and are therefore omitted.

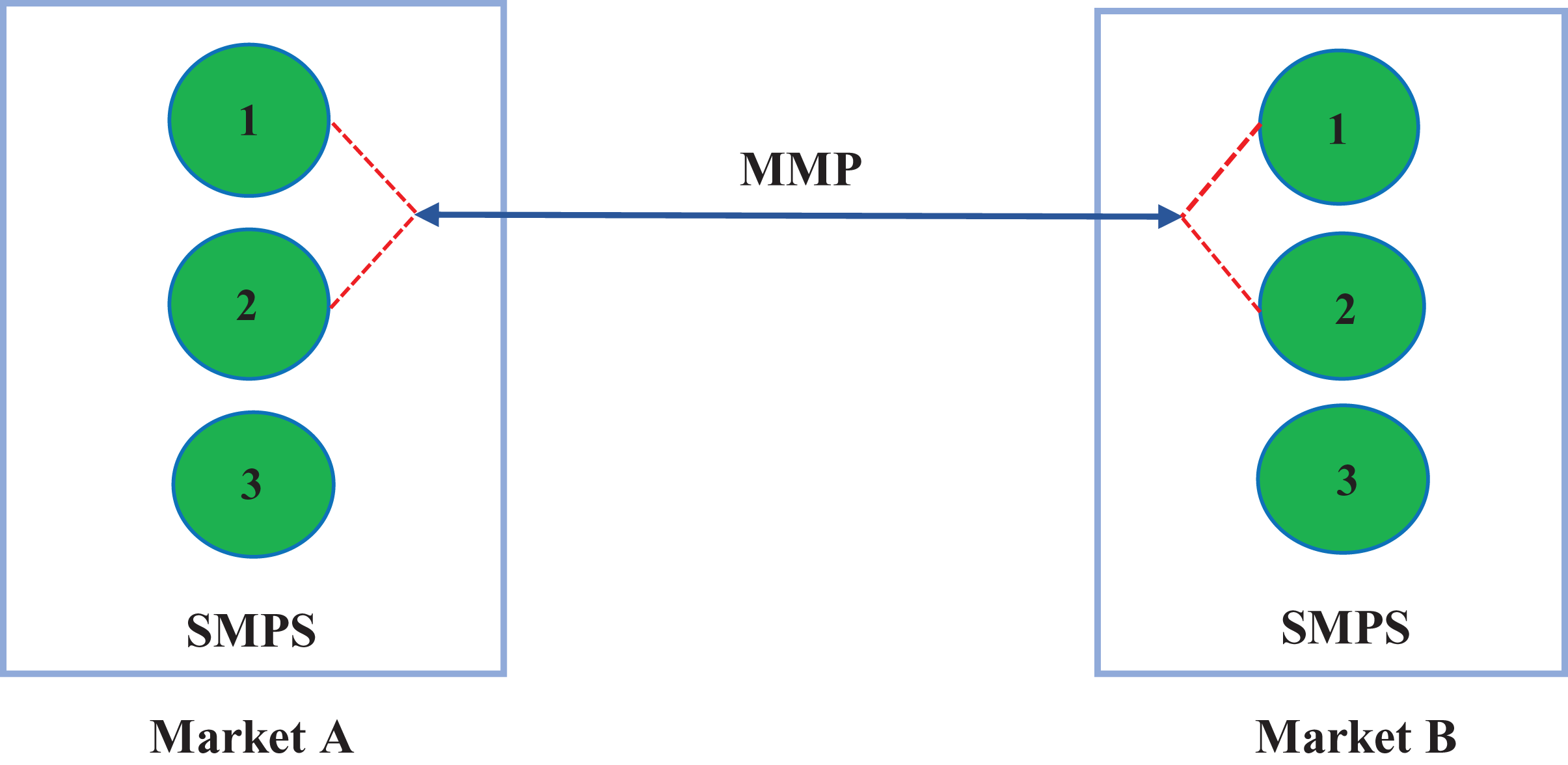

We now derive the conditions under which a merger that simultaneously reduces the number of market providers and SMPs, while increasing the number of MMPs satisfies the non-increasing price condition (NIPC). This is illustrated in Figure 1 in which there are 3 SMPs in each market pre-merger and 1 SMP and 1 MMP post-merger. 15

Pre-merger: 0 MMPs and 3 SMPs – post-merger: 1 MMP and 1 SMP.

Proof:

Definition 1. The critical value of

It follows from (14) that

Proof:

and

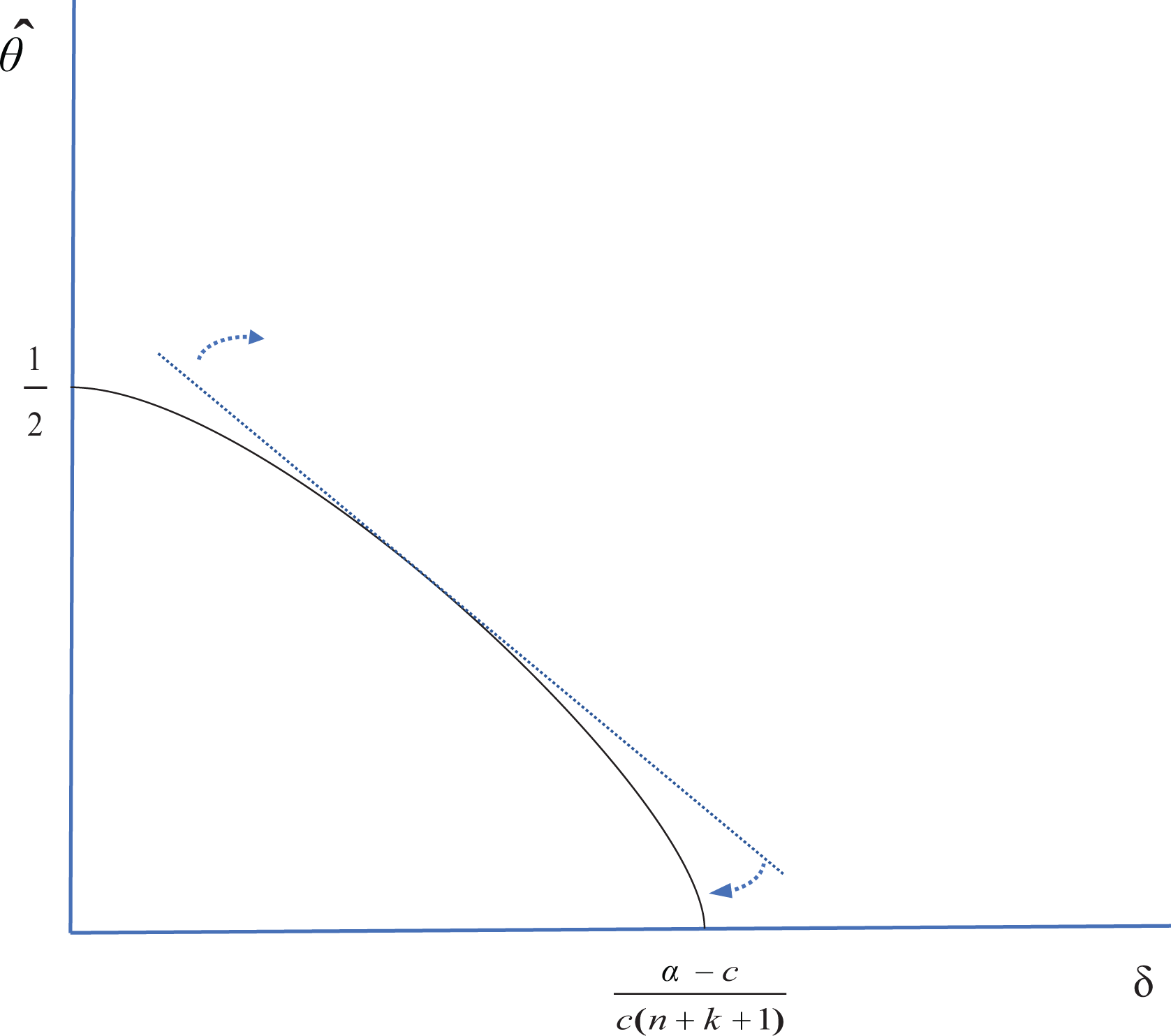

The increasing tradeoff between

The increasing tradeoff between

At the vertical intercept in Figure 2, there are no cost complementarities

The next proposition reveals that the critical value of demand complementarities is decreasing in both the number of SMPs and MMPs when cost complementarities are present, ceteris paribus.

17

There is a tradeoff or substitutability between the critical value of demand complementarities and the number of SMPs (or MMPs) in satisfying the NIPC. Since increasing demand complementarities or the number of market providers (n or k) both decrease P*, increasing one permits a decrease in other while satisfying the NIPC. Similar logic applies to the case of

Proof:

The next proposition indicates that the critical value of demand complementarities is increasing in the ratio of the reservation price to marginal cost when cost complementarities are present, ceteris paribus. Since the equilibrium price is increasing in z, ceteris paribus, an increase in demand complementarities is required to offset the upward pricing pressure associated with an increase in z so that the NIPC is satisfied.

Proof:

Numerical simulations

This section reports the numerical simulations to complement and expand upon the theoretical findings in Section 3.

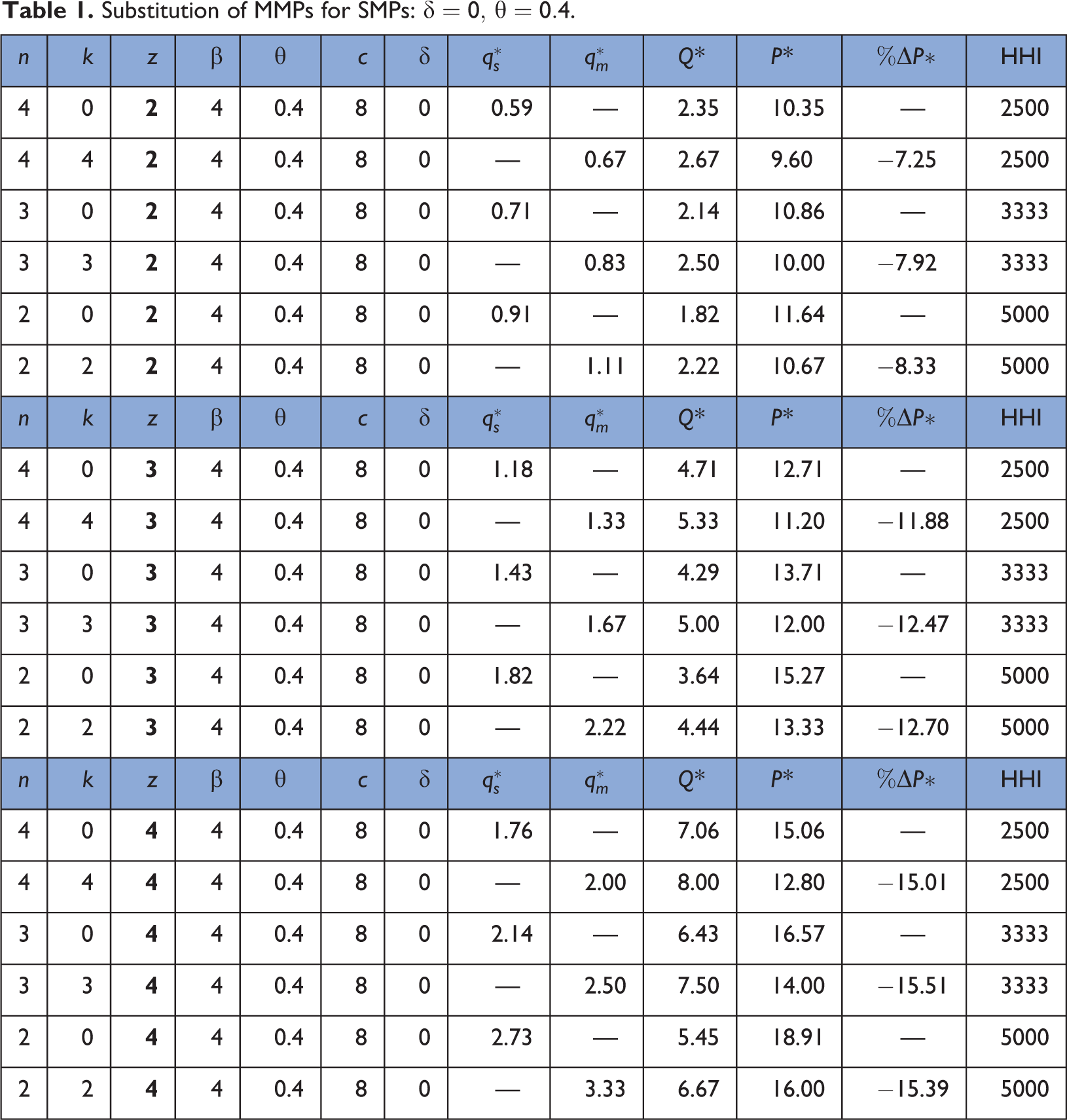

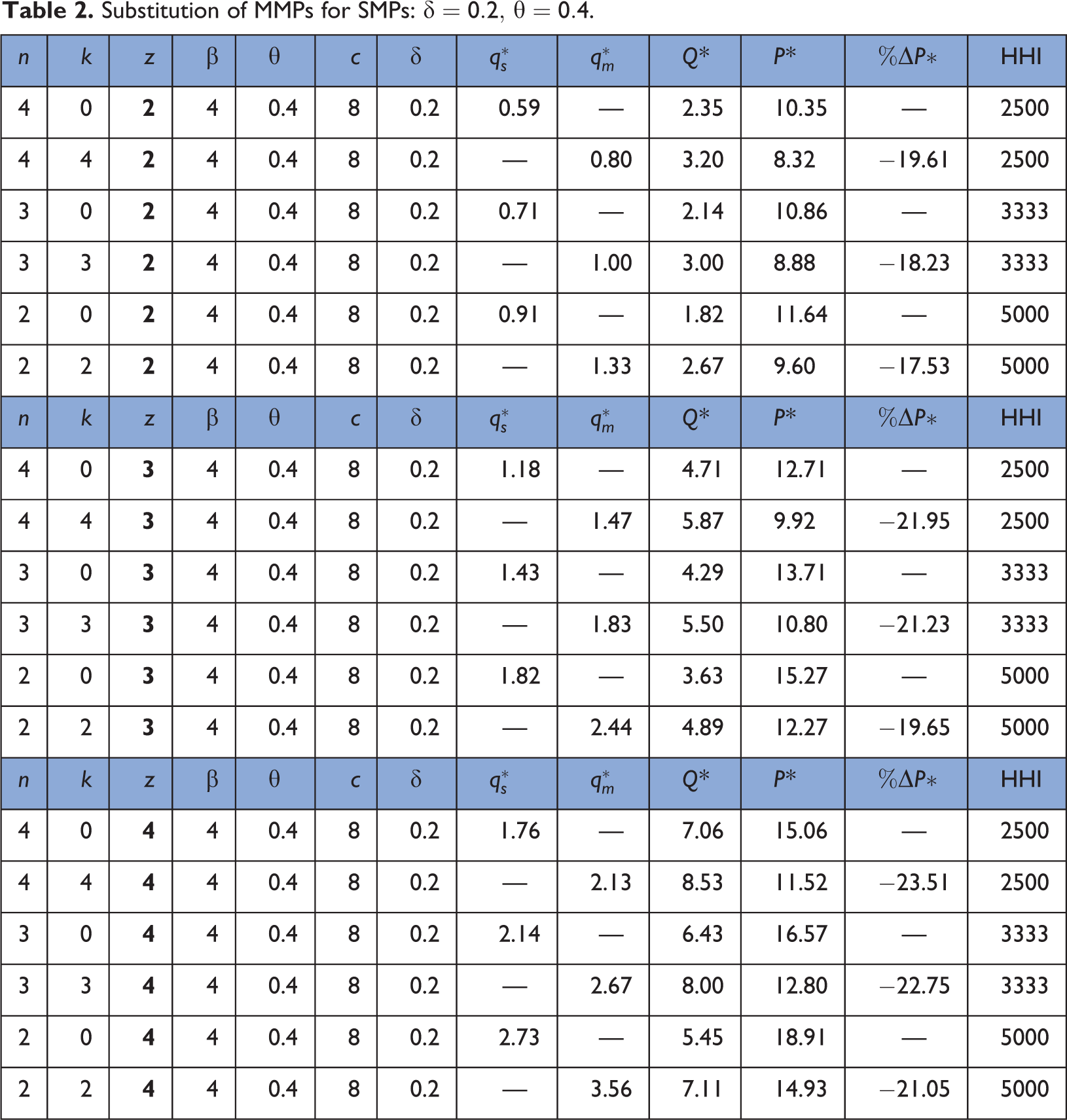

The first set of simulations, corresponding to Tables 1

to 4, explores changes in market structure, substituting MMPs for SMPs, along the lines of Proposition 2 for various cost and demand complementarity two-tuples

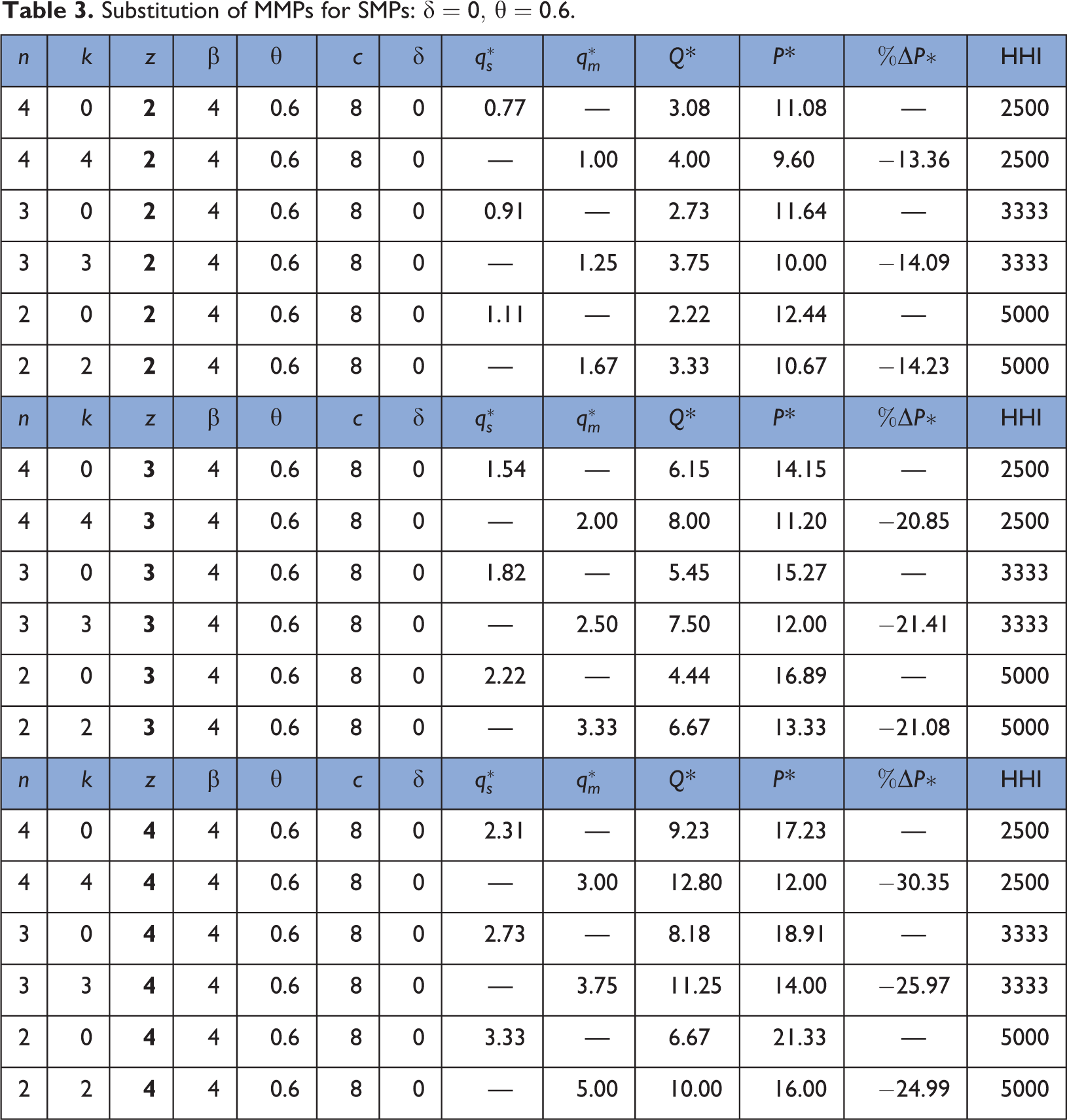

Substitution of MMPs for SMPs:

Substitution of MMPs for SMPs:

Substitution of MMPs for SMPs:

Substitution of MMPs for SMPs:

The following observations are noteworthy. First, the substitution of MMPs for SMPs leads to pronounced price reductions even in the absence of cost complementarities (Proposition 2(i)). Second, cost complementarities further augment the magnitude of these price reductions (Proposition 2(ii)). Third, the price reductions associated with the substitution of MMPs for SMPs are increasing in the ratio of the reservation price to marginal cost (z) (Proposition 2(iii)). Finally, except for the simulations reported in Table 1, the substitution of MMPs for SMPs results in lower prices despite a doubling of the HHI.

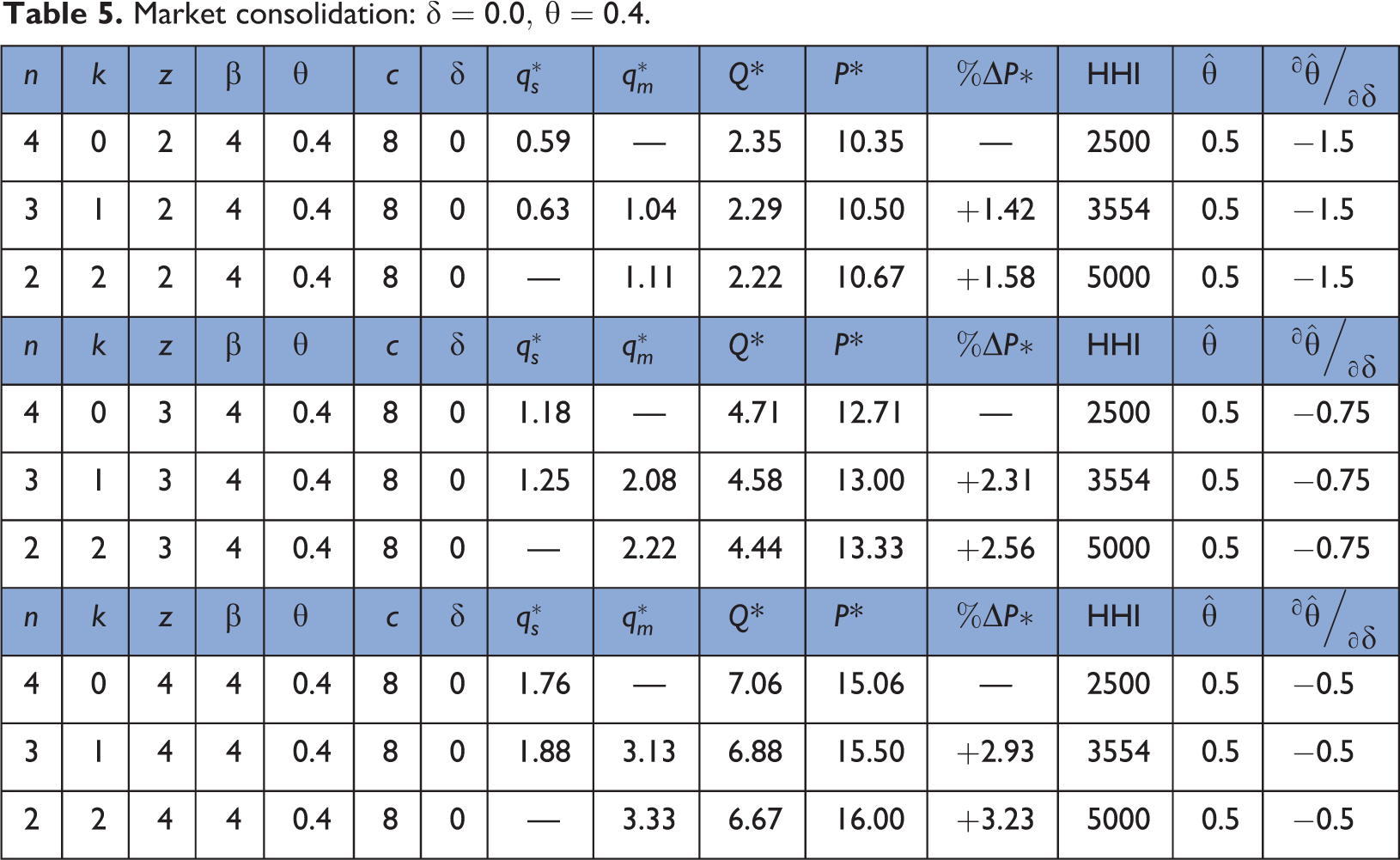

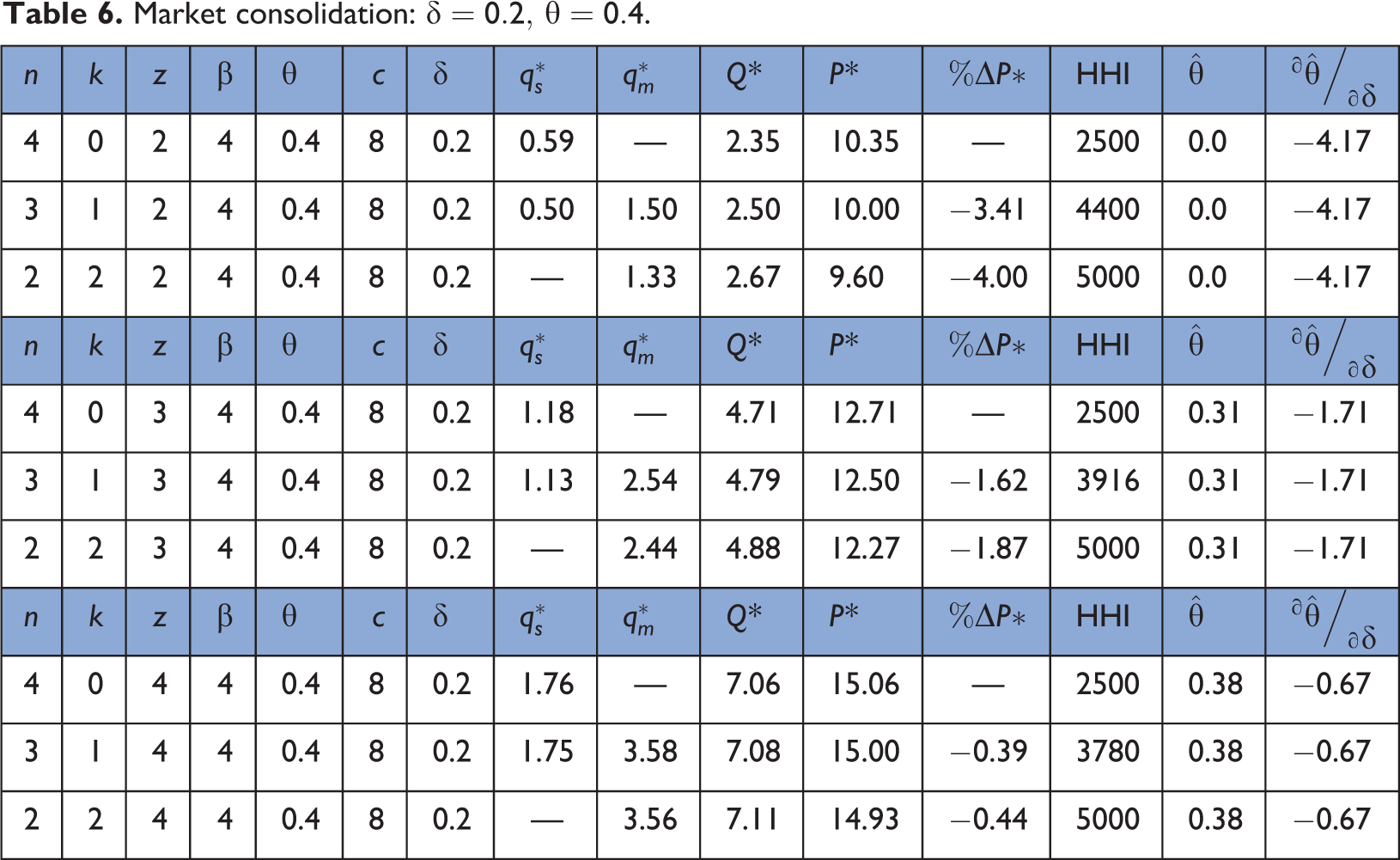

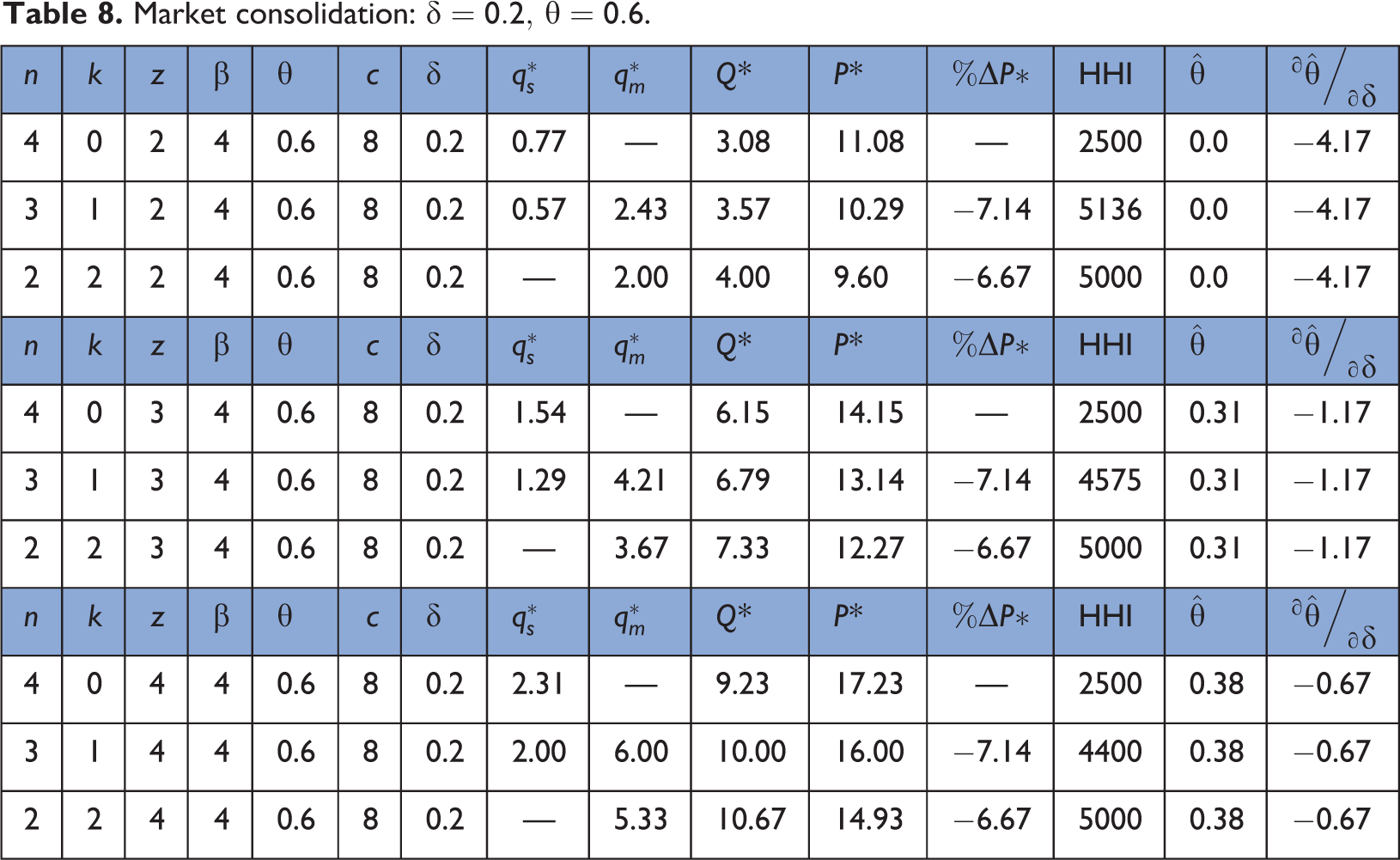

The second set of simulations, corresponding to Tables 5

to 8, explores the effects of industry consolidation (ΔSMPs = −2 and ΔMMPs = +1) for the specified cost and demand complementarity two-tuples

Market consolidation:

Market consolidation:

Market consolidation:

Market consolidation:

Selected findings from the simulations are highlighted. First, except for Table 5 in which

Implications for horizontal merger guidelines

Market consolidation

Market concentration and changes in market concentration figure prominently in the HMG. For example, the HMG consider a market to be moderately concentrated if the HHI is between 1500 and 2500 and highly concentrated if the HHI is greater than 2500.

20,21

In the former, “Mergers resulting in moderately concentrated markets that involve an increase in the HHI of more than 100 points potentially raise significant competitive concerns and often warrant scrutiny.”

22

In the latter, “Mergers…that involve an increase in the HHI of more than 200 points will be presumed to be likely to enhance market power.”

23

In this case, the HMG duly observe that this “presumption may be rebutted by persuasive evidence showing that the merger is unlikely to enhance market power.” The HMG explicitly recognize the inherent limitations of an exclusive focus on market concentration. The purpose of these thresholds is not to provide a rigid screen to separate competitively benign mergers from anticompetitive ones, although high levels of concentration do raise concerns. Rather, they provide one way to identify some mergers unlikely to raise competitive concerns and some others for which it is particularly important to examine whether other competitive factors confirm, reinforce or counteract the potentially harmful effects of increased concentration. The higher the post-merger HHI and the increase in the HHI, the greater are the Agencies’ potential competitive concerns…

24

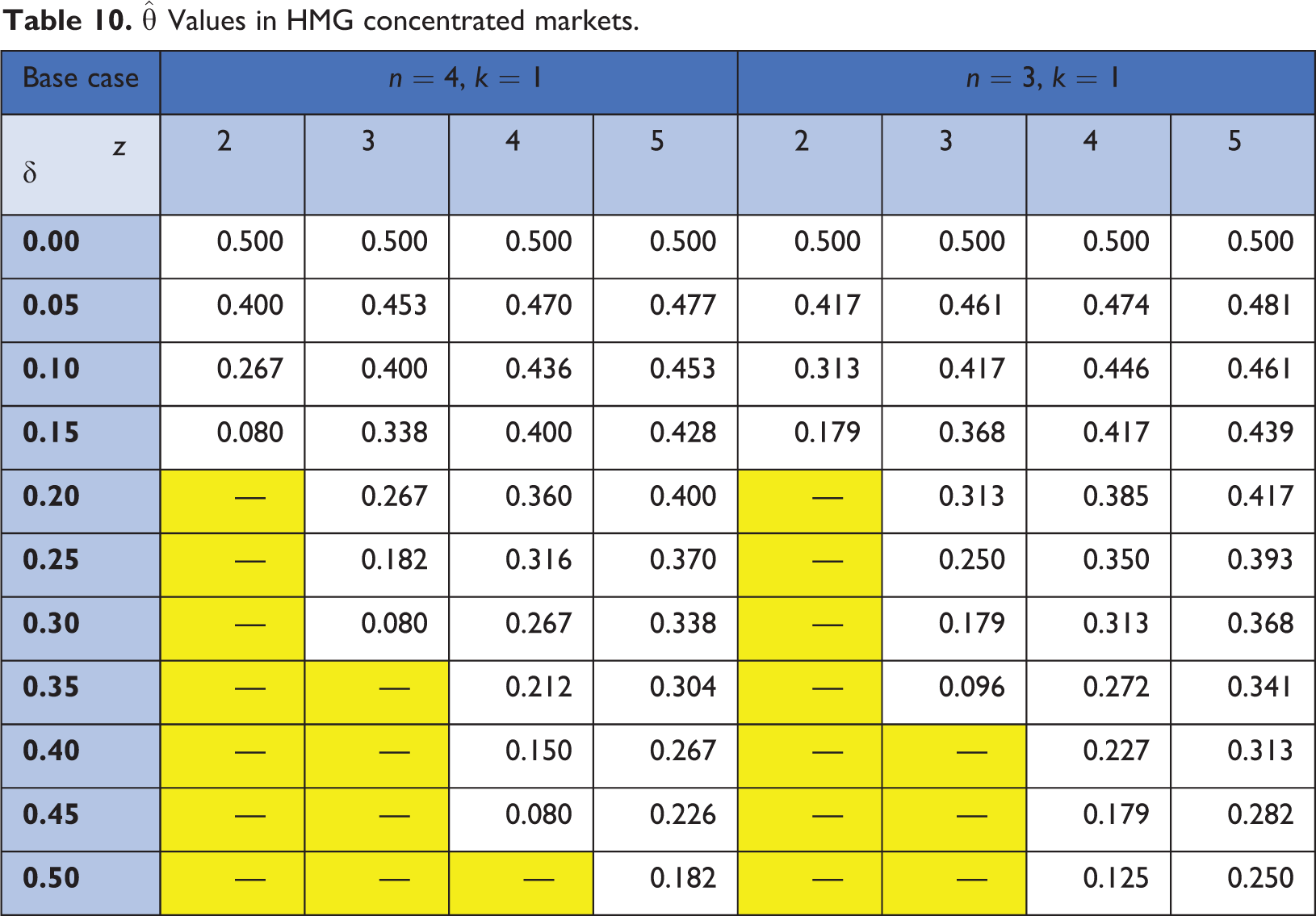

From (14) and Definition 1, the critical value of the demand complementarity parameter is given by

Substituting n = 3 and k = 0 in (20) yields

Substituting n = 4 and k = 0 in (20) yields

The critical values of the demand complementarity parameter

The following observations are noteworthy. First,

We now explore the effects of an MMP operating in a concentrated market prior to consolidation and how this change in market structure changes the

Substituting n = 3 and k = 1 in (20) yields

Substituting n = 4 and k = 1 in (20) yields

The critical values of the demand complementarity parameter

In general, the

Merger to monopoly

The HMG observe that The elimination of competition between two firms that results from their merger may alone constitute a substantial lessening of competition. Such unilateral effects are most apparent in a merger to monopoly in a relevant market…

26

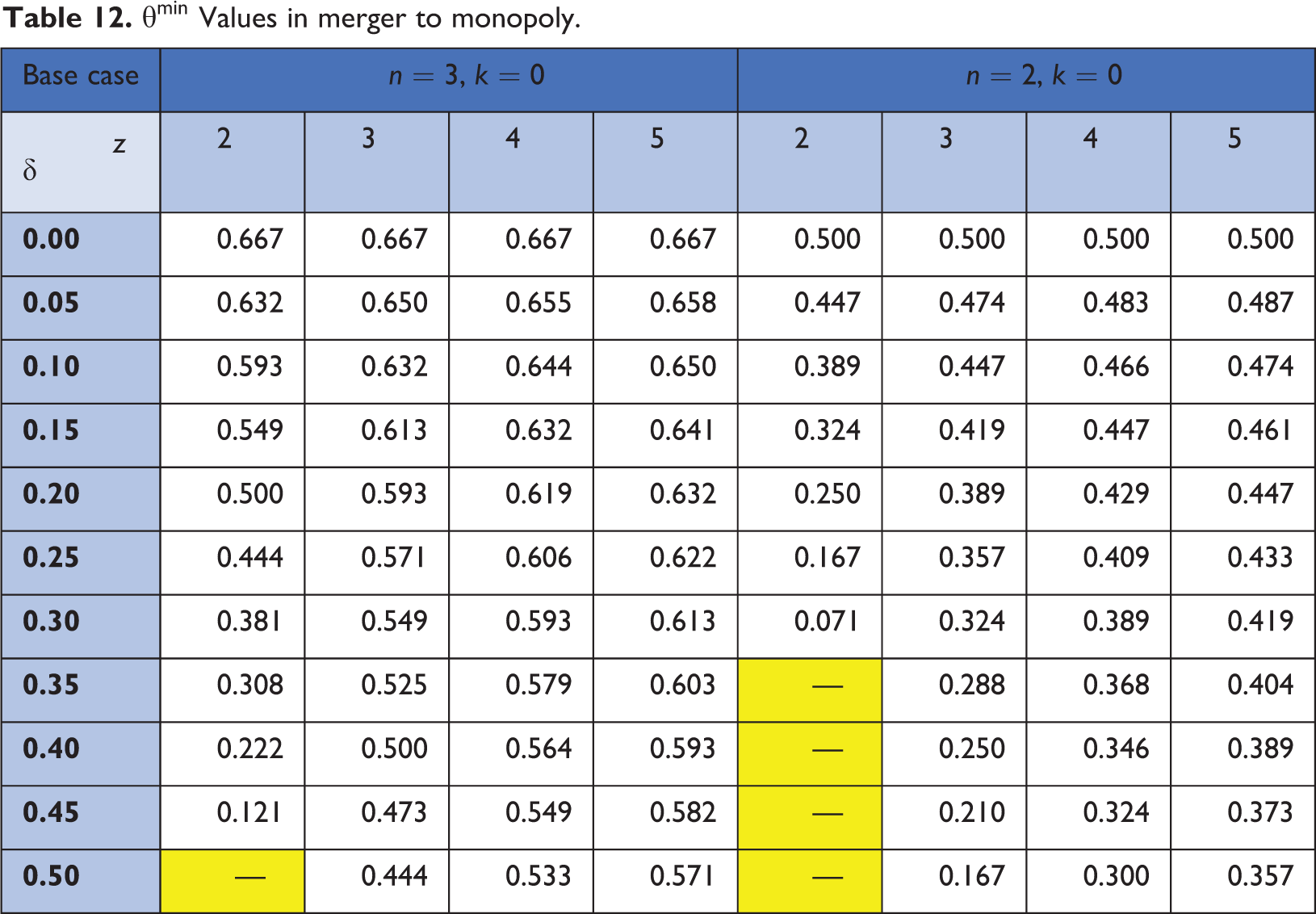

In this subsection, we investigate the various combinations of cost and demand complementarities that are sufficient to negate the HMG concerns regarding monopolization. Specifically, we determine the values of the demand complementarities for which MMP monopolization of the market satisfies the NIPC.

Proof: Setting

Solving (25) as an equality yields the minimum level of demand complementarities

Proof: Setting

Expanding (27) and simplifying the resulting expression yields

Corollary 3 implies that a market in which an MMP is present cannot be monopolized and still satisfy the NIPC.

The final proposition establishes that (i) more concentrated markets necessitate smaller values of

(i)

Proof:

The minimum values of the demand complementarity parameter

Conclusion

This article explores the trade-off between market concentration and multi-market participation in a Cournot model with complementary demands. A key finding is that mergers that increase both market concentration and multi-market participation can satisfy the NIPC even in the absence of cost complementarities. 31 Cost complementarities further augment these price reductions. In addition, there is a pronounced tradeoff between demand and cost complementarities in satisfying the NIPC.

These findings may have special significance for consolidation trends in an increasingly digitalized economy that encompasses network industries, including telecommunications and transportation, that are characterized by demand complementarities, cost complementarities and multi-market participation. These are properties that may introduce a negative bias into traditional merger analysis. A key policy finding is that antitrust practices that place significant weight on market concentration as specified in the HMG, particularly in network industries, can lead policymakers to block mergers that may be expected to yield lower prices. Notably, even in concentrated markets significant increases in the HHI, post-merger, are not dispositive of competition concerns.

There are three limitations of this analysis that caution against drawing broad policy conclusions and further serve to identify potentially promising areas of inquiry. First, relaxing the assumption of symmetric markets would allow SMP and MMP outputs as well as the number of SMPS to vary across the two markets. This change in market structure is not expected to alter the key qualitative findings of the analysis. Second, relaxing the assumption of linear demand and cost functions may provide insight into the generality of these findings, albeit at the cost of analytical tractability.

Finally, the HMG specifically recognize that market share and concentration analyses “are used in conjunction with other evidence of competitive effects.” 32 This other evidence includes product differentiation and prices (vis-à-vis quantities) as the strategic choice variable. As a result, the findings of this analysis should be considered suggestive rather than conclusive in the crafting of merger policy generally and in assessing the merits of any proposed merger specifically.

Footnotes

Acknowledgements

The author is grateful to Dong Li, Glen Robinson and David Sappington for helpful discussions. The author would also like to thank the managing editor, Deniz Ece Dalgic, and two anonymous reviewers for helpful comments and constructive suggestions for revision that improved the manuscript. The usual caveat applies.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.