Abstract

Congestion in infrastructure capacity is a barrier to entry to markets under liberalization. The Spanish rail infrastructure manager, ADIF AV, has implemented an innovative model to reduce such a barrier. ADIF AV optimized capacity by defining the schedule with the most efficient use of tracks, building packages with such track capacity and putting them for tender. Three railway undertakings, the incumbent and two newcomers, will compete in the high-speed market, increasing at least 55% the number of services. This model can be exported to other countries reforming the rail sector.

Keywords

Introduction

The Spanish railway infrastructure manager in charge of the high-speed network, ADIF AV (hereinafter ADIF), has implemented a new model of liberalization of the long-distance passenger railway market. In Spain, the management of railway infrastructure is fully separated from the provision of railway services. Renfe, a state-owned company, enjoyed exclusive rights to provide passenger railway services in Spain. ADIF has implemented a tender process to appoint three railway undertakings to sign framework agreements with ADIF, ensuring them infrastructure capacity in the main high-speed corridors for 10 years. In this way, an element of “competition for the market” has been introduced in the “open-access” “competition in the market” model designed by the European Union for the construction of the Single European Railway Area. This is a model of market opening which other countries can consider for the liberalization of railway services, particularly in countries with congested railway networks.

EU Directive 2012/34 imposed the liberalization of railway services in Europe by 14 December 2020 (Montero & Finger, 2020). “Competition in the market” is the preferred model for long-distance commercial passenger services, particularly high-speed services, as opposed to a “competition for the market” model for services under public service obligations. An unlimited number of railway undertakings can enter the market. However, the EU railway legislation does not define a concrete solution for the problem of allocation of scarce track capacity (Gibson, 2003). Capacity is allocated on a yearly basis, and access to infrastructure over a long term is not ensured. Certainly, the legislation does not define grandfather rights for the incumbents. However, no specific mechanism is imposed on the Member States to decide on the allocation of capacity in case of scarcity in order to favor market entry by newcomers. This is an important loophole in the legislation, and an important barrier to entry for newcomers (Nash & Preston 1992). ADIF has defined a model to solve this problem.

The Spanish infrastructure manager has opted for a tender to allocate track capacity. After informal and non-simultaneous consultation with potential newcomers, ADIF identified high interest in market entry on the part of a high number of railway undertakings (at least six). According to ADIF, the Spanish high-speed network could not accommodate all the services planed by the newcomers. The infrastructure manager’s engineers built an optimum cadenced timetable for the three busiest high-speed corridors in the country: northeast (Madrid–Barcelona), east (Madrid–Valencia & Alicante), and south (Madrid–Seville & Malaga). The predefined train paths designed for all three corridors were coordinated to produce maximum capacity.

The next step was to make 70% (legal maximum allowed by the EU legal framework) of this optimized capacity available for “framework agreements.” A framework agreement is an agreement setting out the rights and obligations of an applicant and the infrastructure manager in relation to the infrastructure capacity to be allocated and the charges to be levied over a period longer than one working timetable period. ADIF decided that framework agreements would last for 10 years, that three framework agreements would be concluded, and that they would be asymmetric, in the sense that each of them would provide access to a different amount of capacity: 60%, 30%, and 10% of the capacity made available for the respective framework agreements. Finally, as six applicants were interested in these three framework agreements, a competitive tender was arranged to appoint the three winners. On 27 November 2019, ADIF made public the winners of the three framework agreements: the Spanish incumbent Renfe, Trenitalia’s participant ILSA, and French incumbent SNCF. In this way, ADIF introduced a “competition for the market” element in what was designed as an “open access” model.

This model is in line with EU legislation, because further entry is not prohibited. On the contrary, 30% of the available capacity was originally reserved for the annual capacity assignment, making entry by further newcomers possible.

This paper analyzes this liberalization model. Liberalization and Tenders identifies the theoretical background of the capacity tendering model, then The Spanish High-Speed System identifies the drivers behind the strategy. Description of the Tendering Process describes the tendering process in detail. Economic Evaluation analyzes the economic pros and cons of the model, followed by conclusions in Conclusions.

Liberalization and tenders

There is a tradition in Europe and in Spain in particular, of controlling the process of introduction of competition in previously monopolized markets by tendering licenses to enter the market.

In the United Kingdom, a second license was granted in 1983 for the provision of telecommunications services in competition with the historic monopolist British Telecom (Pye et al., 1991). It was granted to Mercury, another state-owned corporation managing telecommunications networks in the former British colonies. Mercury was then privatized through a tender.

In Spain, following the United Kingdom precedent, a duopoly was established in 1996 for the operation of fixed telecommunications networks. A second license was granted to a state-owned corporation that owned the network for the transmission of television signals. This corporation was then privatized through a tender. A third license was put for tender in 1997. Full liberalization of the market took place in December 1998.

This model was considered in Spain for the liberalization of the railway industry. In 2014, the Spanish Government designed a tender to grant a second license for the provision of high-speed services in competition with Renfe, but only on the east corridor (Montero et al., 2016). The tender was finally abandoned, as the “Fourth Package” was adopted and the date of December 14, 2020, was fixed for the full liberalization of commercial services.

One of the first countries to liberalize railway passenger services in Europe, the United Kingdom, tendered licenses for the provision of the service in 1994. Services throughout the country were packaged in 23 franchises. The government then put out for tender the license for the provision of services in each franchise under monopoly rights. It was competition for the market, in the tender procedure, but no face-to-face competition in the market, as only one company was licensed for the provision of the service in each franchise (Geroski, 2003).

However, this was not the only option considered in the UK in the early 1990s for the introduction of competition in railway services. The option to tender more than one license in each franchise was also analyzed. In Starkie (1993), it was identified that inviting train companies to post bids for train paths would produce considerable overlap of preferred departure times. The conflicts could be resolved, but the processes would be complex, time-consuming and would not necessarily produce an optimum outcome. Starkie proposed to plan the optimum use of the existing infrastructure according to the timetable that would guarantee stability in terms of number of services and specific train schedules. In order to introduce competition, packages of services according to the optimum timetable can be defined and then put out for tender. In this way, an element of competition for the market, and for network capacity in particular, would precede competition in the market.

Specifically, the right balance had to be identified in the number of packages to be put out for tender. The more packages are made, the more competitors enter the market, but the higher the risk of inefficiencies derived from missing economies of scale and density and poor use of assets such as rolling stock. On the contrary, the lower the number of competitors, the higher the risk of collusion. However, Starkie advanced that the correlation between competition and concentration is not linear. Ian Jones suggested that “no more than three competing train companies are sufficient to obtain a competitive outcome in passenger railways competition” (Jones, 2001).

The debate reappeared 20 years later. In 2015 the UK Competition and Markets Authority opened a consultation to foster competition in railways, and Starkie argued again that “there would be two successful bidders for each franchise. Routes currently operated by one franchised [company] would be split so that two franchised [companies] could provide services. This option could be implemented in different ways. Services could be equally split, such that each operator serves many of the same destinations. Alternatively, the two franchised [companies] could be asymmetric, for example with a 60:40 (or greater) division between services. This would reduce the extent of on-rail competition between the franchised [companies] but would reduce the risk of collusive behavior. Another possibility would be for one of the operators to act as an ‘anchor franchisee’ with responsibility for the vast majority of unprofitable but socially valuable services, with the other operating primarily profitable services” (CMA, 2016).

The Spanish high-speed system

The liberalization strategy designed by the infrastructure manager was largely determined by two drivers of high-speed railway policy in Spain (Montero et al., 2019). On one hand, there was a need to increase the volume of passengers, which is lower than in other high-speed networks. On the other hand, there was a perception that newcomers would cherry-pick the Madrid–Barcelona route, cream-skimming the system. The tender organized by ADIF responded to these circumstances.

An opportunity to increase ridership

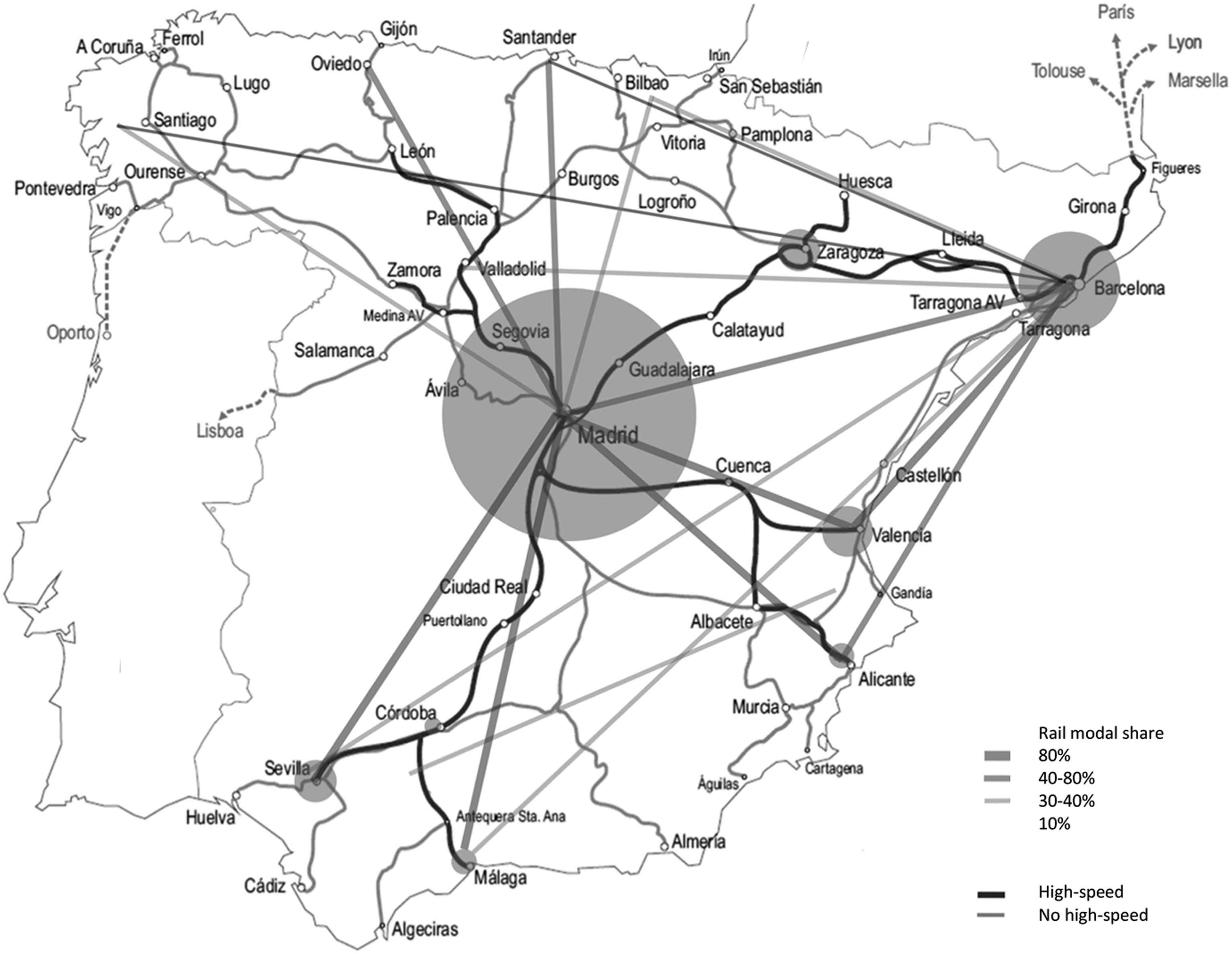

The Spanish authorities consider liberalization to be an opportunity to improve the intensity of the use of the high-speed network. Spain has one of the largest high-speed networks in the world, with a total distance of 2718 km. The network is hub-and-spoke, with its center in Madrid, the fifth most highly populated metropolitan area in Europe, located right in the center of the Iberian Peninsula. Four corridors depart from Madrid and become more capillary as they move to the coasts (García Álvarez, 2012): northeast to Barcelona, east to Valencia and Alicante, south to Malaga and Seville, and north, still under construction, even if some segments are already operative. Figure 1 Long-distance railway routes and their modal shares with aviation.

Track access charges for high-speed services in Spain are high compared with those of other countries (CNMC, 2018). The revenue generated for the use of the infrastructure (and other commercial activities) covers 56% of ADIF’s total costs (ADIF, 2018 p. 98). The development of the high-speed network has left ADIF highly indebted (€15 billion).

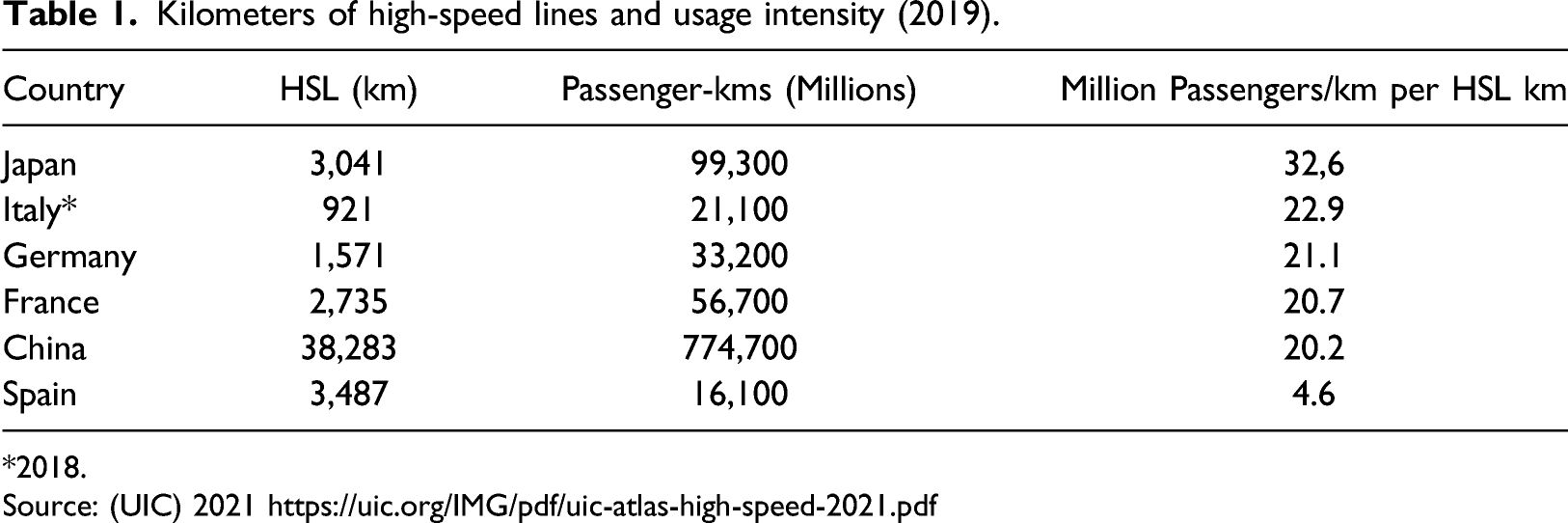

Kilometers of high-speed lines and usage intensity (2019).

*2018.

Source: (UIC) 2021 https://uic.org/IMG/pdf/uic-atlas-high-speed-2021.pdf

The stations in Madrid and Barcelona are bottlenecks that create congestion in the network. The high-speed network has been developed using the international gauge, while the rest of the rail network uses the traditional Iberian gauge. As a result, high-speed traffic is completely separate from the rest of the passenger and freight traffic. This is an advantage in the operation of the network, as high-speed services do not have to be coordinated with lower-speed services. However, the networks converge in the stations. This makes the management of stations more complicated, particularly those in the largest cities. In Madrid, the Atocha station—serving the northeast, east, and south corridors—has not been connected with Chamartin station—serving the north corridor and expected to grow to meet demand for all the corridors once it is connected with Atocha. In Barcelona, Sants station is particularly congested, and the new station, Sagrera, is only 40% complete, with no date for completion.

Risk of cream-skimming

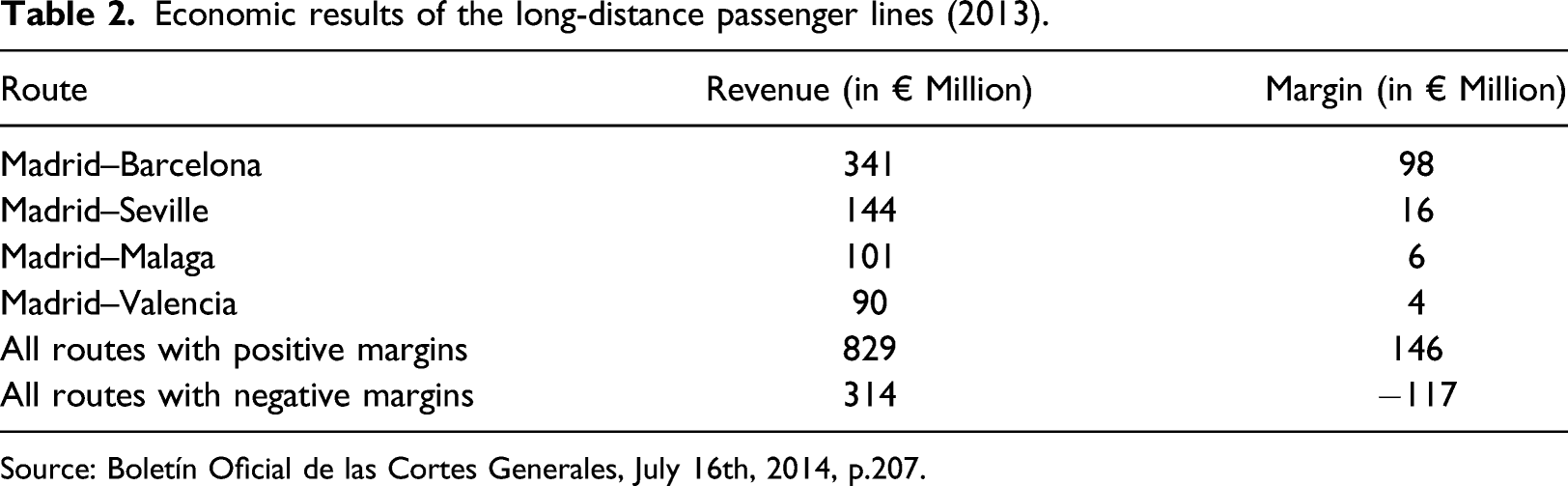

Another driver of the railway policy in Spain is the relevance of the Madrid–Barcelona route. The northeast corridor has the highest number of passengers, generates the most revenue, and is the most profitable as it presents the highest margins. It has traditionally generated most of Renfe’s profits, profits that have cross-subsidized the non-profitable long-distance routes.

Economic results of the long-distance passenger lines (2013).

Source: Boletín Oficial de las Cortes Generales, July 16th, 2014, p.207.

The east and south corridors connect Madrid with smaller metropolitan areas. Consequently, the number of passengers is smaller. This is the case even though high-speed services have attracted the highest share of passengers from air travel. In both the east and south corridors, railways have more than an 80% modal share, compared to less than 20% for aviation. The modal share of railways against aviation is lower on the Madrid–Barcelona route (66%). Cities in the east and south corridors have fewer business travelers than Barcelona. The distances are smaller, particularly in the east corridor, so cheaper road transport is competitive in same-day round trips.

Description of the tendering process

Key in the liberalization model is the tendering. However, the tendering object is not the licenses (the right to provide services), what would be prohibited by the EU legislation, but framework agreements granting the right to use track capacity.

Framework agreements

The model designed by ADIF took the form of the allocation of “framework agreements,” a term defined in EU railway legislation as “a legally binding general agreement […] setting out the rights and obligations of an applicant and the infrastructure manager in relation to the infrastructure capacity to be allocated and the charges to be levied over a period longer than one working timetable” (Art. 3 (23) Directive 2012/34/EU). Commission Implementing Regulation 2016/545 is specifically devoted to framework agreements (Warnecke, 2014).

Framework agreements enable railway undertakings to plan their activities beyond a mere annual assignment of rail path capacity. They were created to grant railway undertakings the necessary certainty for long-term investment in rolling stock and all the necessary assets, which have long maturity terms, certainly beyond 1 year. Framework agreements do not effectively grant access to rail infrastructure capacity. They do not even define train paths in detail. Specific train paths are still allocated on an annual basis by the infrastructure manager. However, preference is given to undertakings completing framework agreements.

Framework agreements could preclude the use of infrastructure by other applicants, so they are limited by EU legislation in duration (5 years with some derogation) and scope (no more than 70% of total capacity).

Competitive tendering

The point of departure for this procedure was the consideration of the high-speed rail infrastructure in Spain as congested. This might be surprising given it is the high-speed network with the lowest intensity of use in the world. However, the main stations in Madrid (Atocha) and Barcelona (Sants) might pose capacity constraints in the case of growth in demand due to liberalization. Works are underway to increase capacity in the existing stations, but the new capacity would not be available by December 2020 for the opening of the market.

ADIF decided to fully optimize the three main high-speed corridors. It decided to define an optimized timetable coordinating services throughout the day. ADIF determined the optimum departure stations (railway undertakings will not be allowed to initiate/terminate services to Valencia and Alicante at Atocha station but at Chamartin), the indicative departure time for each service, the speed, the time of arrival at the destination, the waiting time in the destination, the departure time for the return trip, and the optimum time to arrive back in Madrid and be ready for a new departure. In this way, the scarce capacity in Madrid (and also in Barcelona) will be used efficiently by railway undertakings, which must adapt to an optimized timetable of perfectly “cadenced” departure times throughout the day. Optimization increased the number of potential daily services, from the existing 119 to 189 daily services (60%).

ADIF decided to distribute the optimized capacity across three framework agreements. In order to meet the requirements in EU legislation, 30% of the optimized capacity was left for the annual allocation of capacity. The remaining 70% of the optimized capacity would be distributed in three framework agreements: Package A with 60% of the capacity, Package B with 30%, and Package C with 10%. This distribution was based on the business models communicated by the interested parties to ADIF. Package A seems to be suitable for the incumbent (Renfe), Package B for a newcomer with the ambition to compete head-to-head with the incumbent (Italo model in Italy), while Package C was presented as particularly suitable for “low-cost services.”

ADIF decided that each single framework agreement would include capacity in all three high-speed corridors. The alternative of separate framework agreements for each corridor was excluded.

Finally, ADIF decided that a 10-year period would be the optimum duration of the framework agreements, despite the 5-year term recommended in Directive 2012/34/EU. As a reference, framework agreements in Italy last for 7 years.

The assignment criteria

ADIF defined the most intensive use of infrastructure capacity as the parameter to prioritize the conflicting requests to conclude framework agreements. Agreements would be concluded with the candidates requesting the highest number of train paths included in each framework agreement in a sealed-bid auction. Only one package would be granted to a single railway undertaking, excluding capacity hoarding by the incumbent. Other possible allocation criteria (Stojadinovic et al., 2019) were not explored.

In the case of a tie, further parameters were defined: (i) commitments to reduce CO2 emissions; (ii) a lower percentage of employees with short-term labor contracts; (iii) a higher percentage of women employed; and (iv) a higher percentage of disabled employees.

The key parameter to appoint the winning bidders was the scale of operations in terms of the rail paths used. In this way, bidders were incentivized to ask for the maximum available capacity in each “package,” or as near as possible to the maximum as allowed by the availability of rolling stock. ADIF imposed an obligation to explain plans to acquire rolling stock and reserved for itself the possibility to judge how realistic these plans were.

ADIF defined penalties in case capacity is not used in the future (in line with the maximum contractual penalties admitted in Regulation 2016/545), and even fines for breaches of national railway legislation in such a scenario.

A fundamental element in the tender was the decision to evaluate the offers not separately for each corridor but combined as single offers covering all three corridors. The more services provided on the less popular routes, the higher the chances of being granted capacity on the Madrid–Barcelona route. Railway undertakings committing to use capacity only on the Madrid–Barcelona route would, in practice, be excluded from the Spanish market.

The tendering process

ADIF invited railway undertakings that were potentially interested in framework agreements to submit their proposals before 31 October 2019. Railway undertakings could define their capacity needs according to their business plans. It was not compulsory to adapt the request to the optimized capacity structure defined by ADIF, or according to the structure in three packages designed by ADIF.

Only if the capacity requests by all railway undertakings exceeded the available capacity would the tender actually take place. In case the tender would be necessary, participants would not be able to submit a new offer, but the original capacity requests already submitted would be considered the bidding offer to compete in the tender and to be evaluated according to the criteria defined by ADIF.

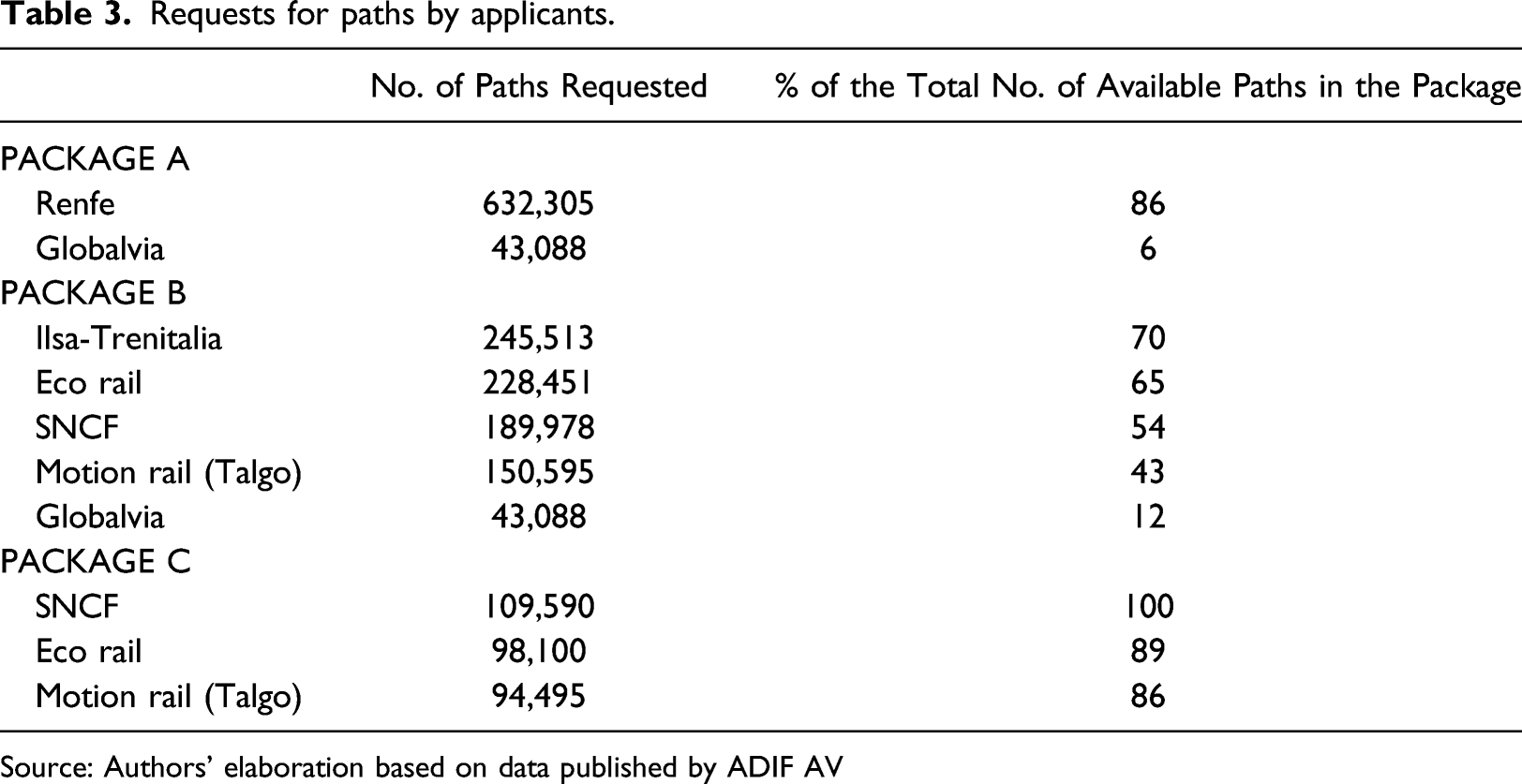

Requests for paths by applicants.

Source: Authors’ elaboration based on data published by ADIF AV

ADIF made the results of the tender public on 27 November 2019. As expected, Renfe was assigned Package A; that is, the package with 60% of the capacity in the three leading high-speed corridors. In fact, Renfe did not bid for all the available capacity, only for 86% of it. This means it will operate around 100 return services a day in all three corridors (10% more than before the tender).

ILSA-Trenitalia was assigned Package B. ILSA is a corporation controlled by Spanish regional airline Air Nostrum, with a 45% stake owned by Trenitalia, the Italian railway incumbent. ILSA committed to make use of 70% of the available capacity in Package B (close to 40 return services a day) starting in January 2022. ILSA announced that it will operate with 23 Bombardier Zefiro trains provided through leasing by Trenitalia.

SNCF, the French railway incumbent, was assigned Package C. SNCF committed to fully operate all the available capacity (around 13 return services a day), starting in May 2021.

The three candidates excluded were Eco Rail, a local consortium that bid to use 65% of the capacity in Package B, close to the offer made by ILSA, Talgo, a rolling stock manufacturer, and Globalvía, a worldwide infrastructure concession management leader.

The railway undertakings committed to use the capacity with contractual penalties and even to impose fines if they do not meet their commitments. Additionally, they committed to use specific rolling stock and to follow the model predefined by ADIF in terms of stations, timetables, stops, etc. They can exploit further services, but they cannot reduce the minimum number of services in each corridor, or transfer services from one corridor to another, unless force majeure justifies it.

Overall, the three competitors committed to exploit on average 55% more services than those Renfe provided before liberalization. The newcomers will exploit around 35% of the capacity assigned in framework agreements. In financial terms, ADIF has estimated a €2 billion increase in revenue over a 10-year period.

The signature of the framework agreements took place in May 2020, with some delay due to the COVID-19 crisis.

Economic evaluation

The liberalization model designed by ADIF aims to solve a loophole in EU regulation, namely, the entry barrier derived from congestion in rail infrastructure. However, it requires more centralized planning than in other liberalization models, and some governmental intervention in the definition of the tender conditions. An evaluation of these parameters is necessary.

Regulating congestion

The Spanish infrastructure manager has defined a new model to allocate track capacity in case of congestion, reducing barriers to entry to newcomers while enabling the incumbent to continue operations without surrendering track access rights.

ADIF could have followed the example of other European countries and just waited for railway undertakings to ask for capacity in the annual procedure for the allocation of capacity. This was the procedure in Italy and is going to be the procedure in other countries with extensive high-speed networks, such as France. Both of these networks, especially the Rome–Milan and Paris–Lyon sections, are more congested than the Spanish network.

However, network congestion is a barrier to entry for newcomers. High-speed networks are highly congested in Europe, even when they are used by a single railway undertaking with exclusive rights. While no grandfather rights are defined for track access, as it is the case with airport slots, newcomers cannot take for granted the availability of stable train timetables to conform a coherent, viable competitive schedule of services in the densest routes.

Directive 2012/34/EU imposes a procedure to adopt a formal capacity analysis to ascertain the reasons of the congestion and the measures to manage congestion, as well as a capacity enhancement plan to put an end to congestion (Art. 50). The formal declaration of an infrastructure as congested makes it possible for infrastructure managers to apply priority criteria to exclude track access applicants (Art. 47). However, each Member State had to be left some latitude in this subject. Each national legislation defines the priority criteria (IRG, 2019).

Other way to manage congestion is by introducing congestion charges as a response to congestion. Articles 31 (4) and 47 of Directive 2012/34/UE allow Member States to increase access charges to provide incentives for better use of capacity (Ait & Eliasson, 2019). This could be an option to ease congestion and to identify the priorities of the railway undertakings for the use of the scarce capacity and to exploit capacity more efficiently. Even auctions could be considered (Affuso, 2003). However, such a charge would increase the price of the railway services, making them less competitive against road transport, and is very complicated to calculate.

ADIF has triggered an intensive entry in a short period of time. Indeed, the winner of a package is the candidate that is willing to demand more capacity, which means that it is willing to invest more and in a shorter period in rolling stock than its competitors. Thus, ADIF generates a supply push by significantly increasing pre-existing frequencies.

This drives demand, which takes advantage of economies of scale and density, which reduces operator costs and ADIF’s costs. These lower unit costs allow subsequent price reductions and increases in supply, which drive demand again. Thus, a virtuous circle is generated. It is similar to what happened in Italy (Beria & Bertolin, 2019), except that it is caused here by ADIF and with positive results in a shorter period of time.

The model designed by ADIF provides a good precedent for the management of congestion in railway networks, particularly in the moment of market opening and the promotion of railways throughout Europe. However, some specific adjustments can improve it.

First, it is advisable to implement the model only after the capacity analysis and the capacity-enhancement plans are completed. These documents require the participation of railway undertakings, potential newcomers in particular, in order to identify the future development of traffic. Formal analysis provides the objective basis to justify the restrictions to be imposed in the form of an optimized timetable and priority criteria excluding interested undertakings, as well as the duration of such restrictions. In Spain, this process was informal due to time constraints, and the results were never published.

Second, the criteria for the adjudication of capacity rights in the tender can be improved in order to incentivize efficiency. The main criterion in Spain was intensity in the use of the infrastructure. The tender would be awarded to the railway undertakings offering the highest number of services in each package. Congestion might be a self-fulfilling prophecy, as bidders were encouraged to make offers for the highest number of operations over the 10-year period. Alternative criteria can be considered, such as the most efficient use of the infrastructure (use of larger trains with more seats, double trains, etc.). For example, bids could be based in train paths and seat.km circulated, instead of only train paths.

Planning versus market

The main feature of the Spanish model is the planning of the optimal timetable to be implemented and the number and characteristics of the packages to be put for tender, just as Starkie proposed in the 1990s. This feature certainly reduces the railway undertakings’ ability to define their business models, and the role of the market to determine the structure of the industry. It can be argued that this is a dirigiste option—as the planners in the infrastructure manager openly admitted when they identified the objective of “favouring the introduction of service competition in an orderly and gradual manner” (ADIF, 2019A).

However, free market mechanisms face limitations when infrastructure is congested and the scarce capacity available is already in use by an incumbent benefiting from decades of exclusive rights. The outcome of the annual allocation of capacity might not ensure the optimum use of the available operator’s fleet. The barriers to entry derived from congestion affect the newcomers asymmetrically, as the incumbent is already active in the market.

Furthermore, planning is intrinsically linked to railways. All services making use of the rail tracks must be coordinated so they do not collide. Timetables are defined months in advance. Planning the timetable to optimize the available capacity ensures that the expensive and rigid infrastructure is exploited as intensively as possible.

Certainly, the centralized definition of the timetable determines the business model of the railway undertakings. However, the business model of the railway undertakings is mostly shaped by the rigidity of the industry. The routes are rigid, as rolling stock cannot be moved from one market another as they can in aviation. Traveling times are rigid, as they have to be determined by the availability of track paths for all the services. The very same schedule of services to be designed by a company is rigidly predetermined by these features. In networks with limited routes and type of services, such as high-speed networks, the options to innovate are limited.

Consequently, the centralized definition of the optimized timetable for a high-speed network has a rather limited impact in the freedom of the railway undertakings to determine their services. The downside can be balanced by the efficiency gains in terms of optimized use of the infrastructure.

On the contrary, the Spanish model has a more profound impact on the market in terms of the definition of the packages. It affects: (1) the scope of the packages in terms of routes, (2) the number of packages, (3) the relative size of the packages, and (4) the duration of the agreements.

First, packages can be defined for one route or for more than one route. In the case of the Spanish high-speed services, packages could have been defined for each corridor, but the option was to make packages for all the three largest corridors combined, to be put for tender together. The objective was to avoid cherry-picking and incentivize the provision of services not only in the Madrid–Barcelona route, but in all three corridors.

Second, the number of packages determines the future of competition in the market. A low number of packages, and therefore competitors, facilitate collusion, which could easily be the case in a duopoly. A higher number of packages and competitors ensure a more intense competition, but also potential inefficiencies derived from not exhausting economies of scale and density.

Third, the relative size of the packages has a high impact in terms of shaping competition: asymmetrical packages make collusion more complex and therefore foster competition in the market. The experience in aviation proves that, in oligopolistic routes, the presence of low-cost carriers reduces fares in a statistically significant way when airports expand capacity (Fageda & Fernández-Villadangos, 2009).

Fourth, the duration of the framework agreements is also relevant. Thirty years ago, Starkie advanced that ossification is an important risk in this model. The timetable and the market structure are predetermined for the duration of the rights granted by the tender. The smaller the margin to modify the conditions in the offer, the more rigid the market becomes. A long duration of the right amplifies the rigidity. The 10-year duration of the framework agreements in Spain is a long period, during which changes in the conditions of supply and especially of demand can occur at any time. One example is the current uncertainty about the evolution of demand as a consequence of COVID-19. The virus is introducing new risk, both in supply and demand. This uncertainty will most likely lead to renegotiations of the terms of the framework agreement.

It can be argued that an infrastructure manager is not the optimal entity to determine all the parameters in the model. The infrastructure manager can determine the existence of congestion, as it has the best knowledge of the infrastructure and the available capacity. It can also define the timetable to optimize capacity, as no other entity has a better knowledge of the infrastructure. However, the infrastructure manager is not in the best position to define the tender conditions, and particularly the definition of the services to be included in each package, the number of packages, the potential asymmetry in the packages, and the adjudication criteria. The infrastructure manager has a conflict of interests, as it has the incentive to maximize the use of the network and its revenue. Certain policy options (promoting certain corridors and services over others) might be valid policy options, but they should be decided by a governmental authority. In any case, close supervision by the independent regulator is advisable.

Regulating competition

The conditions defined in the tender have a large influence on the competition to be introduced in the market. The number of packages, the asymmetric volume of the packages, and the incentive to increase the number of services determine the intensity of the competition that can be expected.

Literature suggests that liberalization delivers the best results when there is market potential; that is, the possibility for the market to grow in volume (Preston et al., 1999). In other words, competition is welfare-improving if it generates enough new passengers (Alvarez et al., 2016). Otherwise, price competition with homogenous services will merely trigger a devastating price war (Villemeur et al., 2003).

Liberalization has led to sharp increases in the supply of services in all the countries that have already liberalized their railway services. On the Rome–Milan route, frequencies increased by 56.4% between 2010 and 2013 (Bergantino, 2015). In the Czech Republic, on the Prague–Ostrava route, the number of frequencies increased from 20 in 2010 to 35 in 2014, but the number of seats per train was simultaneously reduced, from 465 in 2010 to 333 in 2014 (Tomes et al., 2016). In Austria, the number of frequencies on the Vienna–Salzburg route increased significantly. New-entrant Westbahn initially offered 15 connections a day and announced an increase to over 30 in 2018, while ÖBB offered 33 daily connections (Finger et al., 2016). In all these cases, infrastructure became congested. In this sense, competition in quantities (Cournot competition) seems a common strategy in long-distance railways intramodal competition (Laroche & Lamatkhanova, 2021).

In Spain, the railway undertakings have committed to an increase of 55% in frequencies. This increase is not limited to the Madrid–Barcelona route but applies to all three high-speed corridors. In fact, daily frequencies might even double on the less attractive route (Madrid–Alicante). This is the main difference between the model implemented in Spain and the liberalization in other European countries, where expansions of services are being freely decided by railway undertakings, with service expansion being very conservative, limited to the most profitable services, and implemented gradually.

It is often stated that competition leads to growth in patronage, particularly in high-speed services. In Italy, the number of high-speed passengers grew from 23.4 million in 2011 (before NTV entry) to 40.3 million in 2015 (of which the incumbent had a market share of 77.4%). On the Prague–Ostrava route, a 92% ridership increase was observed between 2010 and 2015 and the incumbent had a market share of 41% in 2015 (Tomeš & Jankova, 2017). On the Vienna–Salzburg route, demand increased by 25% between 2013 and 2016 (Finger, Montero & Kupfer, 2016). Overall, the market share of the incumbent ÖBB on all passenger routes in Austria is around 88%.

The Italian example is often cited. However, competition in high-speed services in Italy coincided with the completion of the high-speed infrastructure between Milan and Rome (Desmaris, 2016). It has been argued that growth in demand in Italy can be explained by the availability of the high-speed infrastructure rather than by the introduction of competition. In fact, ridership growth in Italy when the high-speed infrastructure was introduced mirrored growth in France, where no high-speed competition existed (Bacares et al., 2019).

Growth in ridership in Italy, as in France, is explained by the transfer of passengers from aviation to railways. Competitive travel times made possible by the high-speed infrastructure and cheaper fares have led to high-speed services reaching a modal share of over 80% (against aviation below 20%) on the most popular routes in Italy (Milan–Rome), but also in France (Paris–Marseille), where no competition exists yet. However, it has been observed that high-speed services have not attracted a substantial number of private car users in Italy (Borsati & Albalate, 2019), and in France car-pooling is actually detracting passengers from high-speed services.

On the Madrid–Barcelona route, high-speed has a modal share of 66% against air transport. This low share can be explained by high prices—to cross-subsidize other loss-making services—and capacity constraints due to scarcity of rolling stock. Therefore, there is room for growth, but this room is limited, as the modal share is not as low as it was in Italy when high-speed was introduced (41%).

The situation is different in the other corridors. High-speed railways already have a modal share of over 80% in the east and south corridors in Spain. No major increase in ridership can be expected from a modal shift from air to rail in these corridors. New demand can only be induced with more aggressive marketing techniques. Some passengers can be attracted from road transport, particularly from coach services, which are very popular in Spain among low-income individuals such as students, young professionals, and retired people. Induced demand would be another source of demand, especially for low-cost services offered in packet C.

It will be difficult to substantially increase ridership when air passengers—the low-hanging fruit—have already migrated to high-speed services. The shock in supply might not be met by a parallel increase in demand. Furthermore, the current sanitary crisis has introduced more uncertainty. COVID-19 might make it more challenging to attract traffic currently traveling by private car.

Furthermore, the decision to have three competitors raises some questions about the competitiveness of the newcomers. The incumbent will have access to 2.5 times the capacity of the second competitor. The newcomers might have difficulty reaching the necessary economies of scale and density to compete with the incumbent. The two newcomers will be exploiting around 18 million and 1 million train-km per year, respectively, in a network of 1900 km, which might not be enough to reach the necessary economies of scale and density (Wheat & Smith, 2015).

The need to increase demand to meet the committed increase in supply is expected to lead to aggressive competition between the three competitors, particularly in the east and south corridors. Rates can be expected to be drop sharply in all the corridors. This has been the experience in competitive rail markets. The Italian incumbent reduced high-speed fares by an average of 31% just before competition started (Cascetta & Coppola, 2014). These prices have been calculated to be around 30–35% higher than those of the new entrant (Bergantino et al., 2015). In the same way, in the Czech Republic fares went down by 46% on the Prague–Ostrava route between 2011 and 2014 (Tomeš et al., 2016). In Sweden, prices on the Stockholm-Goteborg route went down by 12.8% in the period between March 2015 and June 2016 (Vigren, 2016). After Westbahn’s market entry in Austria, prices for long–distance connections were reduced overall (the new entrant offered tickets on the Vienna-Salzburg route at 50% of the incumbent ÖBB’s standard). This was followed by a shift towards a more sophisticated pricing regime at ÖBB, with better rates for early bookings and higher discounts for owners of loyalty cards (Finger et al., 2016). This is in line with economic models (Broman & Eliasson, 2017; Ruiz & Palacin, 2013).

Prices tend to stabilize after a period of competition, particularly when there are only two competitors in the market (Montero et al., 2016). However, economic theory predicts that in markets with a higher number of competitors, particularly when they have asymmetric market shares and there is a maverick, equilibrium is often not reached, and prices tend to fall to the level of variable costs. In this respect, the C-package operator in Spain can play the role of the maverick.

This effect is reinforced when substantial barriers to exit are introduced, which is the case in Spain, as ADIF has introduced heavy penalties in the case that an applicant misses its commitments to make use of the infrastructure. We should remember that these commitments have been made for a period of 10 years. Operators can be expected to differentiate their products. If they are successful, product differentiation can reduce constraints on prices.

Conclusions

The Spanish infrastructure manager has proactively designed a new model to introduce competition in the passenger railway service. Once it was identified that existing capacity could not accommodate newcomers interested in the market, a tender of capacity was organized. First, infrastructure capacity was optimized through the definition of the timetable of services. Second, capacity was distributed into three asymmetric packages covering the three main high-speed corridors. Third, the capacity packages were put out for tender, in the form of the right to conclude framework agreements for capacity with a duration of 10 years. Finally, the criterion for adjudication was the intensity of use of capacity.

This model provides a viable solution to the fundamental challenge of allocating infrastructure capacity when the infrastructure is congested. This is particularly relevant when the market is opening to competition, an incumbent monopolizes the use of capacity, and capacity becomes a barrier to entry to the market. The model is based on solid economic grounds and can be implemented in other jurisdictions.

Some adjustments in the model might improve it. First, a formal description of the congestion, in terms of available capacity, forecast demand, and duration of the congestion by the infrastructure manager would facilitate the definition of proportionate restrictions in the form of an optimized timetable, definition of the packages, and adjudication criteria. Second, these conditions should be defined not by the infrastructure manager, but by a governmental authority, in order to avoid conflicts of interest and provide the necessary legitimacy to the political decisions that shape the industry. The role of the independent regulators should also be enhanced. Third, the allocation criteria should take into consideration efficiency in the use of infrastructure, and not just the most intense use of it, which increases congestion.

As a result of the model implemented by ADIF, high-speed railway services will be provided under competitive conditions in Spain. Barriers to entry have been reduced to newcomers. The tender procedure has ensured a sharp increase in services and promotes effective competition. Passengers will certainly benefit from more frequencies and lower prices.

However, the winning railway undertakings will be subject to rigid commitments for the next 10 years in terms of the routes they will operate, their frequencies, and the timetables. Such rigidity for such a long period might be an obstacle to supply adapting to demand and might pose a risk to the viability of these railway undertakings in the long term. Rigidity in ambitious commitments might be the winners’ curse.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.