Abstract

As the financial information of electric power enterprises becomes more and more complex, the method of processing original financial data is no longer applicable to continuous financial management. Enterprise Resource Planning (ERP) improves the efficiency of financial information processing and the quality of information management by coordinating and comprehensively managing all company departments. In the fierce market competition, although electric power enterprises may have some competitiveness, there are still many defects in the core financial management of electric power enterprises due to the low level of financial information. Therefore, this paper studied the application prospect of ERP in power financial informatization by analyzing the challenges and impacts of power financial informatization. Finally, according to the problems in the application, the adaptive computing model was used to solve them, and the corresponding solutions were proposed. Through experimental analysis, it was found that the enterprise informatization level under the new financial model was 12.3% higher than the traditional model, and the financial risk level was 36.6% lower than the traditional model. It could be seen that ERP could promote the development of power financial informatization and the accuracy of adaptive index calculation.

Keywords

Introduction

As the engine of the national economy, electric power enterprises have a major responsibility for promoting socially sustainable development. In the era of continuous progress in information technology, the financial management of electric power enterprises has gradually become informationized, and the management efficiency and level have been greatly improved. Electric power enterprises implement financial informatization, which effectively improves the efficiency of asset management. Proper capital allocation can stimulate energy supply. Enterprises can explore better business models, and create more profit space, to promote comprehensive economic development. The use of ERP systems in power enterprises has had a significant impact on improving financial information management. Therefore, this paper integrated ERP into the financial management of power enterprises to promote financial informatization and improve the calculation accuracy of adaptive indicators.

Intelligence of financial information is of great significance to the quality of financial management. Chen Sophia studied the prediction ability of financial variables to macroeconomic variables. Financial variables such as credit growth, stock price, and house price had considerable predictive power for macroeconomic variables. 1 Schinckus Christophe discussed the increasing computerization of financial markets and the impact of this process on the ability to collect financial price information and analyzed the increasing computerization of the financial sector. 2 Asandimitra Nadia compared the impact of financial information, financial self-efficacy, and emotional intelligence of female lecturers in public and private universities on financial management, which would generally benefit financial institutions and governments that held education and training programs for customers. 3

In addition, Cordazzo Michela tried to investigate whether this change would affect the value relevance of non-financial information, which was related to the environmental, social, and governance disclosure requirements of the Directive. 4 Lev Baruch believed that the deterioration of the usefulness of financial information was because the accounting standard setters abandoned the traditional income statement model and adopted the balance sheet model. 5 Jebe Ruth consolidated sustainable development and financial information by using the definition of importance. This use of financial importance conflicted with the non-interference attitude of the Accounting Standards Committee and the Securities and Exchange Commission on governance reporting. 6 Through experiments, Gold Anna examined whether the implementation of key audit items in the audit report would affect the reporting behavior of managers. 7 The above studies all described the importance of financial information management, but they were not analyzed and studied in combination with ERP.

ERP can promote the self-adaptation of enterprise information intelligence. Roszkowska Paulina discussed the reasons related to the audit of financial scandals and made suggestions on how emerging technologies could provide solutions. 8 Al-Dalabih F. A determined the impact of the use of the accounting information system on the quality of financial data of Amman Securities Market Service Company. The nature and security of the accounting information system had a statistically significant positive impact on the quality of financial data. 9 Liu Qian proposed a new method of intelligent control of accounting information based on multi-objective evolution and adopted a multi-objective evolution algorithm to build an accounting information control system, to realize intelligent control of accounting information. 10 Jayeola Olakunle determined the impact of the successful implementation of cloud ERP on the financial performance of small and medium-sized enterprises and found that policymakers and practitioners could promote the management of financial information by improving the implementation of cloud ERP strategies. 11 To sum up, the financial information of enterprises could not be separated from ERP, but there were still some deficiencies in intelligent adaptive indicator calculation.

To solve the obstacles and problems of current power enterprise financial informatization, this paper analyzed the challenges and limitations of power enterprise financial informatization through an adaptive calculation model and then studied the confidence level and adaptive calculation output value of power enterprise under ERP. Finally, it was found that ERP had a positive impact on the financial information development of power enterprises, and could also improve the competitiveness and decision-making level of power enterprises. Compared with the research of the above documents, this paper mainly analyzed the application of ERP in the electric power financial informatization to compare with traditional financial management and found that the accuracy of the calculation of adaptive indicators of financial informatization increased significantly.

Challenges and impact evaluation of power financial informatization construction

Impact of power financial informatization on enterprises

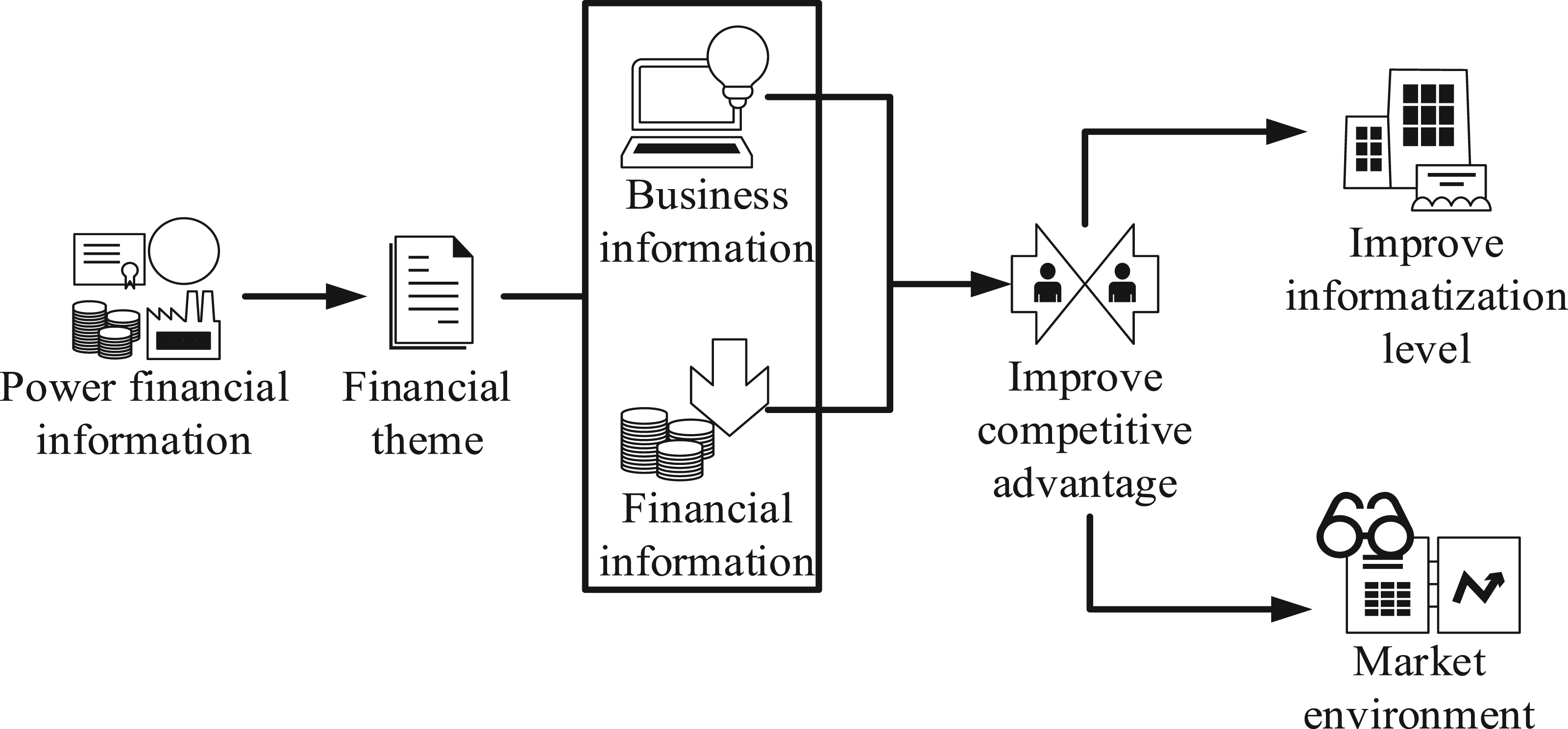

Power financial informatization mainly includes the following aspects, as shown in Figure 1. Subject of financial information: Information about electric power enterprises includes commercial and financial information. However, many people are unable to distinguish between business and financial information, which makes it easy to confuse the purpose of financial information. The main component of electric power financial informatization is financial information. The implementation of information aims to improve the management and decision-making level of power enterprises, especially the implementation of financial information. The monitoring of internal financing of power enterprises is strengthened, and the company's decision-making and macro-supervision capabilities are improved.

Impact of power financial informatization on enterprises.

The realization of financial informatization of electric power enterprises can improve the core competitiveness of enterprises and adapt to the market development trend and market competition environment. The introduction of the financial information of the power company can effectively alleviate the company's difficulties, and save more unnecessary human resources. It can link the investment with the daily operation of the power company, thus reducing the investment cost and improving the cost-effectiveness. Digital financial services allow people without bank accounts to obtain financial services through digital technology. 12 The implementation of financial informatization in power enterprises can improve the cash flow of enterprises and even subsidiaries, and enhance the efficiency of capital utilization.

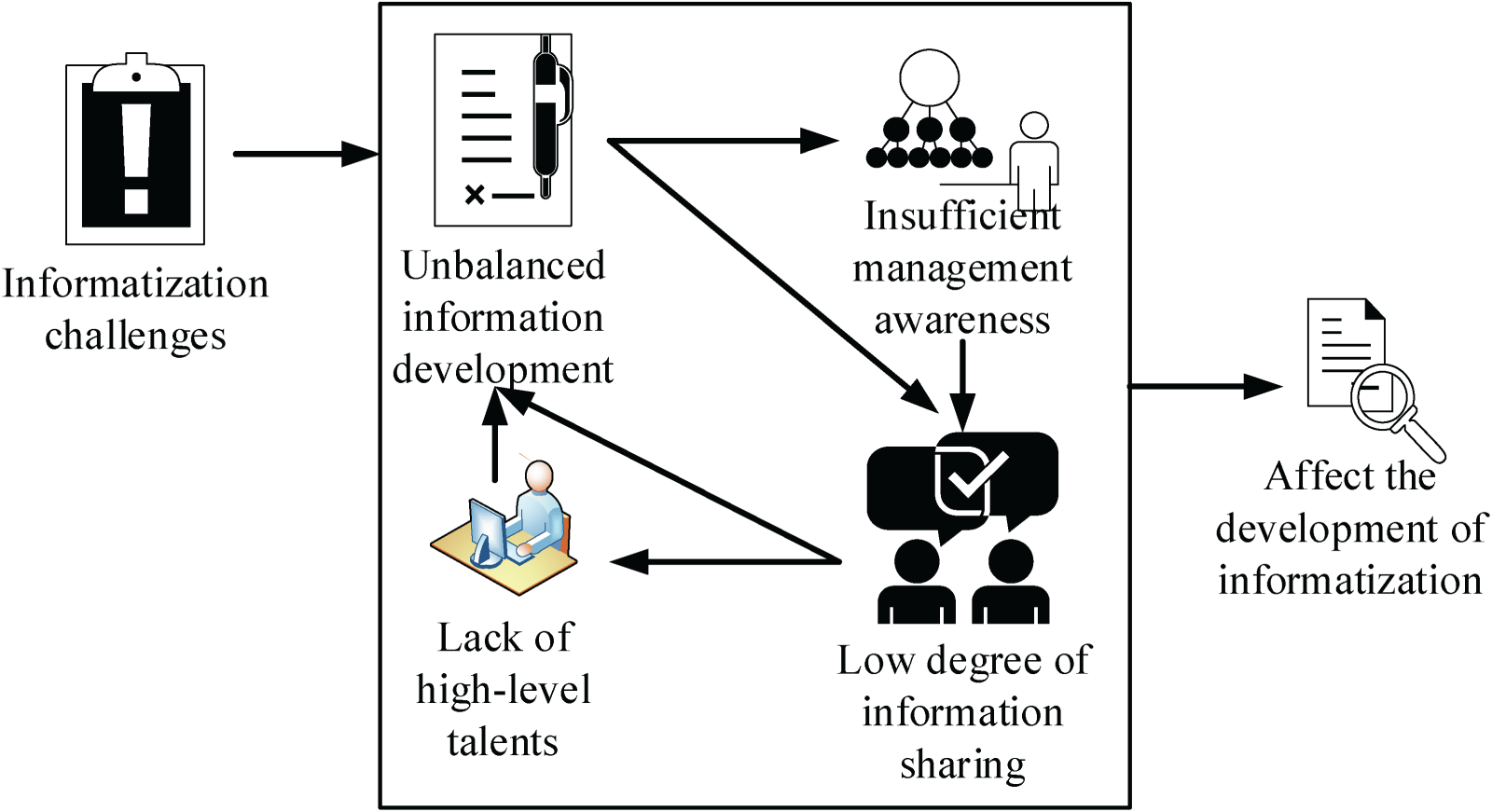

The financial management of power enterprises also needs to be improved and deepened. A large amount of data must be processed promptly. The workload of financial personnel is increasing. The relevance of financial information is increasingly obvious and does not meet the requirements of financial management. The specific challenges include several aspects, as shown in Figure 2. The first is the unbalanced development of financial information. The development of network resources lags behind the development of financial information. With the increase in business and network traffic demand, the existing network bandwidth can no longer meet the actual demand. The second is the lack of high-level talents. Financial informatization can help accountants and standard-setters improve financial accounting in the public sector. 13 In other words, information engineering still depends on these high-quality professionals to a large extent. Due to the lack of high-tech experts in power management and information technology, high-tech experts must be trained to speed up the informatization construction of power enterprises.

Challenges faced by electric power financial informatization.

The third is the lack of energy financial information management knowledge. The central role of financial information in the company's management system is not fully understood, and there are many unreasonable phenomena. Some electric power enterprises do not realize the need for modern management and information resources. Financial information is an important guarantee of management modernization. Many people expressed doubts about this. The fourth is the low degree of information sharing. Due to the lack of comprehensive data analysis and use, the scale of data collection and processing is different, and the portability of the subsystem is low. There is a lack of unified application and information coding standards as well as information exchange. Information cannot be exchanged and transmitted within the group. The utilization and integration of information and the timely exchange of specific business information between different companies are insufficient. Therefore, the lack of necessary information concentration and control is reflected in the vertical and horizontal separation of various business information (including financial information). It is difficult to exchange information.

The future financial information about electricity would lead to changes in management mode, application scope, business, and timeliness, as shown in Figure 3. Financial informatization would introduce a highly centralized management mode from the decentralized single accounting unit management mode to the centralized group management mode. Therefore, to ensure effective resource allocation and unified planning, under this influence, the financial management of power enterprises must also support centralized management. To control and manage the application, the application must be extended to the initial activity point of the enterprise. The starting point of the enterprise's operation should be strictly by the unified business process, and should not be arbitrarily changed according to their respective business conditions. There is a significant negative correlation between management's obstinacy and accrual earnings management. 14 Financial information refers to the whole process of business activities of electric power enterprises with financial capital as the center, including all transactions related to the company's financial situation, and the development of management activities of the financial department itself.

Future trend of power financial informatization.

Financial management is the most basic form of enterprise management and the core element of enterprise management. The information structure of enterprise financial management must include all business processes related to the financial situation of the enterprise. The requirements for the speed of information collection are very low, and there may be some delays. The implementation cost is low, and the storage and processing can be decentralized. Data can be synchronized and centralized regularly, or can be directly requested through the WAN. On the other hand, resource allocation and condition control requirements are very high, which requires overall real-time performance and can not be delayed. When establishing a financial information system, information should be obtained or completed promptly according to resource allocation and control. This requires the implementation of data storage models and business processes in the financial information system. That is, when allocating and controlling resources in real-time, centralized data storage and integrated operation processing are carried out.

Evaluation of the reasons why enterprises use ERP

The main reason why enterprises use ERP is that they can meet the different needs of users, the needs of enterprise management, and the requirements of development. ERP emphasizes not only the reliability of information but also the relevance and timeliness of information. It reflects not only quantitative information but also non-monetary information. In terms of structure and process, information users can access multiple views, including a large amount of non-financial data. With the expansion of the data area generated by the accounting system, it provides a lot of information. The standardization of business processes and the strict integration of management systems and operation links have solved many problems in the traditional financial management model. The company's resources are reasonably allocated and managed, and the capital management is improved to meet the basic requirements of the company's management. Once ERP is fully put into operation, enterprises must develop a dynamic monitoring and reporting system according to their own management needs. The information resources provided by ERP are used to provide timely feedback and solve management problems. Market-oriented development is the basic direction and premise for protecting enterprise resources and improving enterprise value. Enterprises should use information technology to manage enterprise resources and obtain enterprise financial data, to support the sustainable and healthy development of enterprises.

Difference evaluation between ERP and other financial systems

First of all, the financial system is an important part of ERP. ERP integration module includes purchase management, sales management, inventory management, production management, etc. In the enterprise ERP system, the financial management module can be used alone or integrated with other modules. With the increasing attention of enterprises and institutions to financial information, the financial system is becoming more and more mature. ERP software manufacturers have reformed the financial management module by the financial laws and regulations of relevant countries to achieve its practicality. Therefore, many enterprises choose a financial management module or procurement module to reduce the financial cost and workload of future information construction through sales and inventory. Secondly, the financial software only calculates and manages the company's financial affairs. The financial personnel first prepare the supporting documents, and visit the financial software, to conduct financial analysis and summary. They spend a lot of time on the tedious initial work. The ERP system automatically generates accounting records, which can update various detailed ledgers and accounting books, thus greatly reducing the accounting workload and improving the productivity and accuracy of accounting information.

Application direction of ERP in power financial informatization

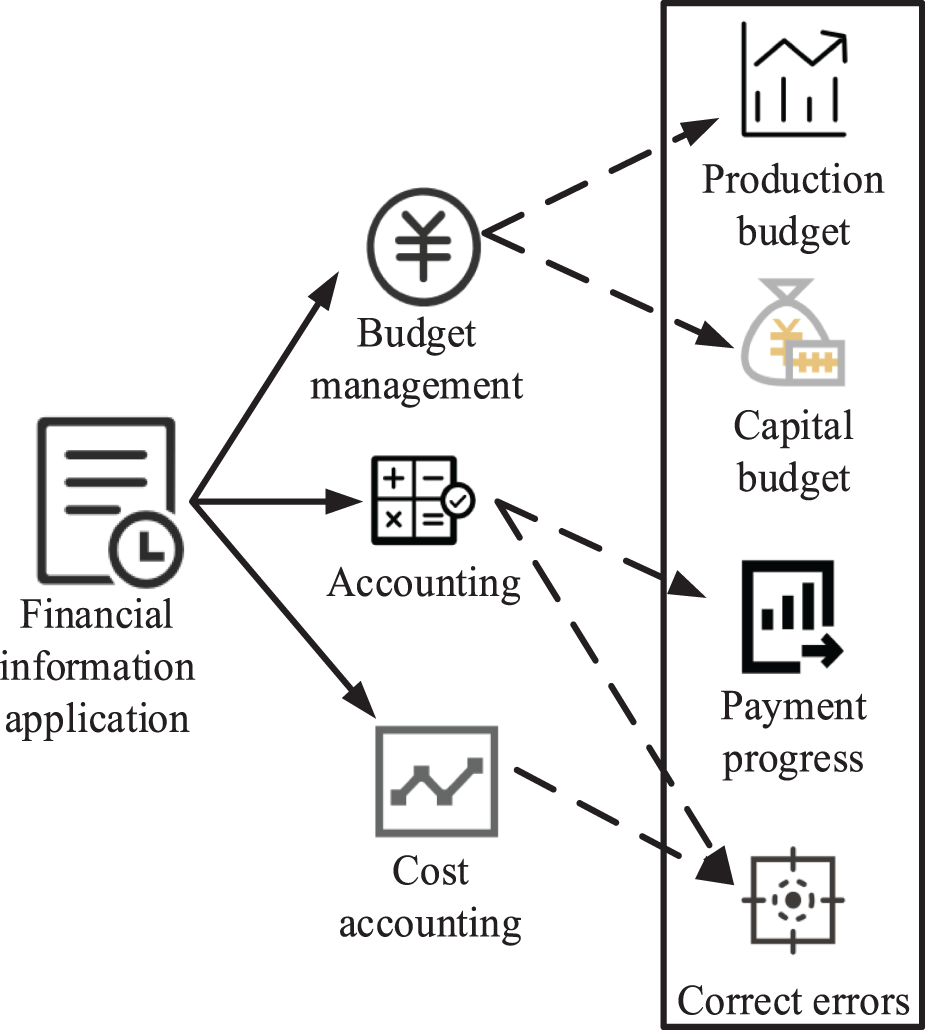

The application of ERP in power financial informatization can be summarized in the following three directions, as shown in Figure 4. The first is the application in budget management. Budget management is an important module of the company's ERP financial management system, including sales budget, production budget, procurement budget, capital budget, cost budget, etc. This provides a simulated operating environment for actual business development and realizes and effectively integrates enterprise resources. The second is the application of accounting. ERP can significantly manage the workload of financial personnel and improve the usefulness of accounting information. Through accounts receivable and accounts receivable, business managers can control performance accounts and understand the progress of payment and settlement. Financial management plays a leading role in controlling capital flow and managing the decision-making process of enterprise development. 15 The third is the application of cost accounting. By integrating human resources, materials, finished products, and semi-finished products into the real-time ERP cost calculation system in the actual production process of products, the product cost is calculated and the cost difference is corrected in time. The cost and income of the whole process are controlled to reduce the product cost and support the operation of power enterprises.

Application of ERP in power financial informatization.

To promote the development of financial information, this paper analyzed the equilibrium measurement factors and characteristic quantities of electric power financial information under ERP through an adaptive calculation model. According to the confidence level of financial informatization, the risk control function of financial informatization under ERP was obtained, and finally, the adaptive index calculation model of financial informatization was obtained. First of all, the calculation model of the equilibrium measurement factor of power finance is constructed as follows:

Increased implementation of ERP

The inherent business philosophy of enterprise leaders should be fundamentally changed. Their awareness of the importance of ERP should be enhanced, and appropriate ERP solutions should be selected according to the characteristics of the enterprise. Through the ERP management system, the development prospect of the enterprise is scientifically planned, and the implementation of the ERP application is improved. The training of relevant employees is improved, and the awareness of rights and obligations is cultivated, which lays a solid foundation for the implementation of ERP in energy enterprises. In addition, it can also establish a financial management model for the power industry, and accurately record the financial information related to power generation and transmission, to effectively implement the standardized management model of modern power enterprises.

Improvement of ERP financial management system

First, the heads of relevant enterprises and departments should discuss financial management issues in depth. They should develop corresponding business systems, and prepare documents for distribution to all departments. The rights and responsibilities of each department should be clearly defined in the system. The second is to strengthen the implementation of the financial management system and supervise the overall signing and approval process of various bills, to manage the enterprise budget scientifically and reasonably, and try to avoid any risks in future production activities. Enterprises must have a sound evaluation and incentive system; on the one hand, the production and operation of enterprises are evaluated; on the other hand, the working conditions of budget and accounting personnel are evaluated. Only through rewards and punishment can employees’ enthusiasm be fully mobilized and work efficiency be improved.

Assurance of the accuracy of ERP data

The ERP system must be based on accurate data. Without accurate data, the ERP system cannot operate normally. The operation and implementation of ERP is a long-term task, which requires employees to provide true and effective financial data to support the normal operation of ERP. It is necessary to establish a strong monitoring and auditing mechanism and formulate monitoring rules and regulations, to clearly specify the time and frequency of testing and auditing to reduce inaccurate data.

Optimization of financial informatization process

With the increasingly fierce market competition, the living conditions of electric power enterprises are no longer comfortable. Electric power enterprises should not only pay attention to production safety but also pay attention to production efficiency. Compared with other companies, electric power enterprises have unique characteristics and cannot store products, including grid transportation, power generation, and transmission. Only through power distribution and other connections can the technology and management level of power enterprises be tested. The implementation of an ERP system can optimize and rethink the business process of enterprises, to make it adapt to the market and rely on production planning and budget control. The Internet platform would help enterprises successfully manage their budgets, and ensure the company's cost-effectiveness, to improve the budget management system according to ERP recommendations.

Implementation of relevant training and publicity work

In the financial information management of power companies, professional information technology personnel are an important factor in ensuring the ERP system. The improvement of information technology personnel can gradually deepen the ERP work of power companies. ERP operation is complex, and the system is not perfect. Once the management personnel handle it poorly or lack knowledge of the ERP system, errors often occur. This requires more in-depth training for practitioners. Through effective training, employees’ awareness of ERP management is improved. From managers to basic operators, the importance of the ERP system is emphasized. The training enables each employee to understand their challenges and shortcomings and improve the competitiveness of the company.

Experimental evaluation of adaptive indicators of power financial informatization under ERP

To study the specific application effect of the adaptive index calculation model of electric power financial informatization under ERP, this paper analyzed the data accuracy and information reliability of the adaptive calculation model of financial informatization to study the confidence level of the calculation model and the output value of the adaptive index. Compared with the informatization level and financial risk level of traditional financial informatization, the specific impact of ERP on power financial informatization was studied. For this reason, this paper investigated the recognition degree of three electric power enterprises for the application of ERP in electric power financial informatization. The recognition degree was divided into three levels. Each electric power enterprise investigated 50 people, and the specific investigation is shown in Table 1.

Recognition degree of three electric power enterprises for the application of ERP in electric power financial informatization.

Recognition degree of three electric power enterprises for the application of ERP in electric power financial informatization.

According to the data described in Table 1, the employees of the three electric power enterprises had a high overall recognition of the application of electric power financial informatization. Thirty seven employees were recognized in Power Enterprise 1, accounting for 74% of the total number of employees surveyed by the power enterprise; there were 6 neutral employees, accounting for 12% of the total survey of the power enterprise; there were 7 employees who are not recognized, accounting for 14% of the total survey of the power enterprise. There were 40 employees recognized in Power Enterprise 2, accounting for 80% of the total number of employees surveyed in the Power Enterprise; there were 5 neutral employees, accounting for 10% of the total survey of the power enterprise; there were 5 employees who were not recognized, accounting for 10% of the total number of employees surveyed by the power enterprise. Forty three employees were recognized in the power enterprise 3, accounting for 86% of the total number of employees surveyed by the power enterprise; there were 4 neutral employees, accounting for 8% of the total survey of the power enterprise; there were 3 employees who are not recognized, accounting for 6% of the total survey of the power enterprise.

On the whole, among the employees of the three electric power enterprises, about 80% of the total number of employees surveyed approved the application of electric power financial information. Neutral employees accounted for about 10% of the total number of respondents, and employees who did not recognize accounted for about 10% of the total number of respondents. The recognized employees all believed that ERP could standardize the storage and management of financial data of power enterprises, and could also help leaders make correct financial data management decisions. The employees who did not approve of the ERP system thought that the mode of the ERP system was different from the development direction of the enterprise, and the enterprise also needed a large number of high-tech talents for data operation. The data accuracy and information reliability of electric power financial informatization under ERP were analyzed and compared with the original electric power financial model. A total of three enterprises were surveyed, and the statistical time was one week. The specific changes are shown in Figure 5.

Comparison of data accuracy and information reliability under new and old financial models.

Figure 5(a) shows the traditional financial model, and Figure 5(b) shows the new financial model. The data accuracy and information reliability of the new financial model were higher than those of the traditional financial model. According to Figure 5(a), under the traditional financial model, the data accuracy of power enterprise 1 was 60%, and the information reliability was 57%; the data accuracy of power enterprise 2 was 63%, and the information reliability was 55%; the data accuracy of power enterprise 3 was 57%, and the information reliability was 52%. According to Figure 5(b), under the new financial model, the data accuracy of power enterprise 1 was 73%, and the information reliability was 68%; the data accuracy of power enterprise 2 was 78%, and the information reliability was 75%; the data accuracy of power enterprise 3 was 72%, and the information reliability was 69%. The average accuracy of data in the traditional mode was 60%, and the average reliability of information was 54.7%; the average accuracy of data under the new model was 74.3%, and the average reliability of information was 70.7%. Through comparison, the data accuracy of the new model was 14.3% higher than that of the traditional model, and the information reliability was 16% higher than that of the traditional model. It could be seen that the accuracy of financial data accounting and the reliability of financial information were greatly improved after ERP was applied to the finance of power enterprises. This showed that ERP could simplify the financial accounting process of enterprises, and help managers to carry out relevant statistical analysis of data, to reduce the error rate. The adaptive calculation model in this paper was used to analyze the confidence level and the output value of adaptive indicators after ERP was applied to financial informatization, and this was compared with the original financial model. The specific comparison is shown in Figure 6.

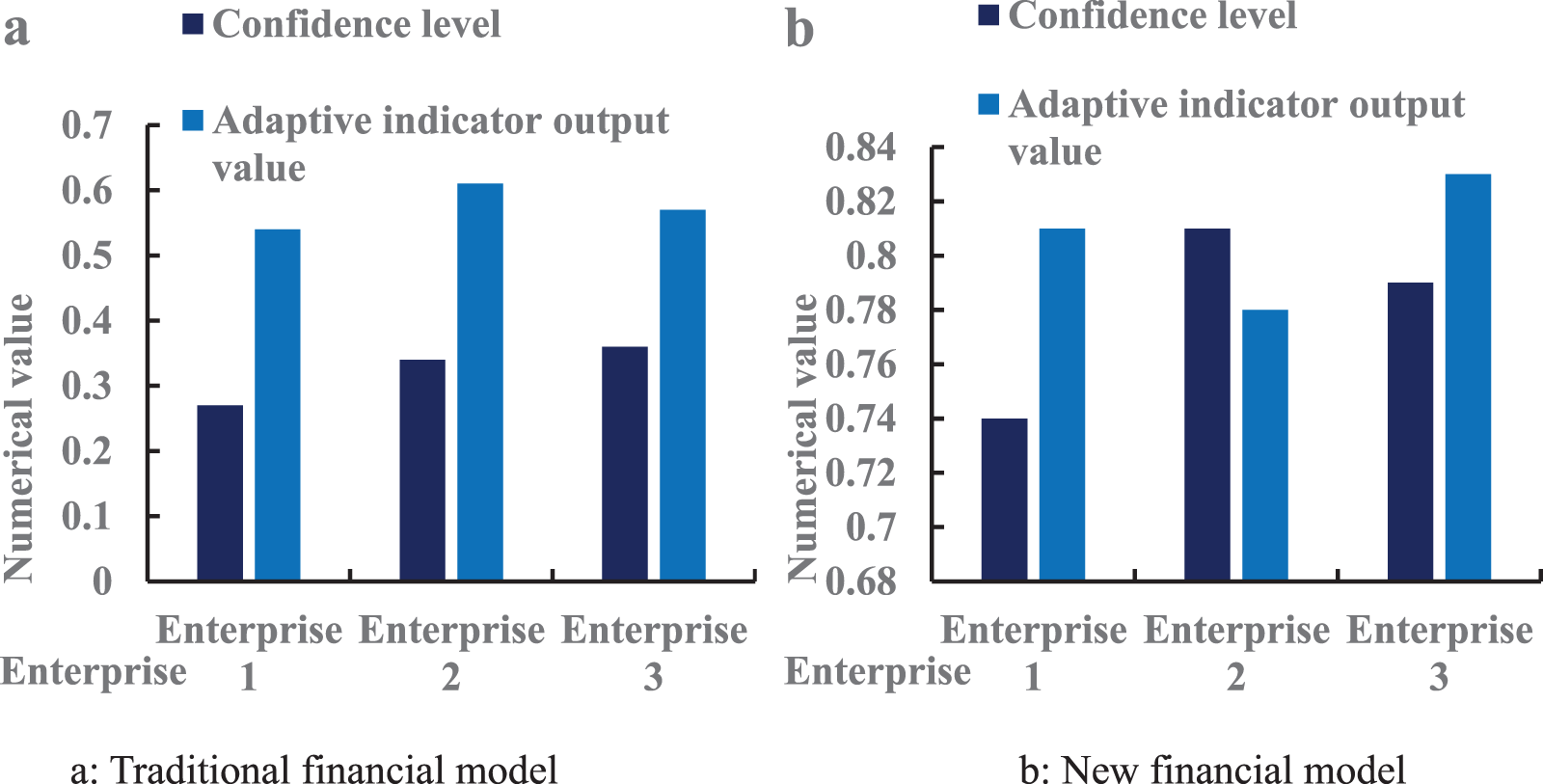

Comparison of confidence level and adaptive indicator output value in financial informatization.

Figure 6(a) shows the traditional financial model, and Figure 6(b) shows the new financial model. The confidence level and adaptive index output value of the new financial model were higher than those of the traditional financial model. According to Figure 6(a), the confidence level of power enterprise 1 under the traditional financial model was 0.27, and the output value of the adaptive index was 0.54; the confidence level of power enterprise 2 was 0.34, and the output value of the adaptive index was 0.61; the confidence level of power enterprise 3 was 0.36, and the output value of the adaptive index was 0.57. According to Figure 6(b), the confidence level of power enterprise 1 under the new financial model was 0.74, and the output value of the adaptive index was 0.81; the confidence level of power enterprise 2 was 0.81, and the output value of the adaptive index was 0.78; the confidence level of power enterprise 3 was 0.79, and the output value of the adaptive index was 0.83. The average confidence level in the traditional mode was 0.32, and the average output value of the adaptive index was 0.57; in the new mode, the average confidence level was 0.78, and the average output value of adaptive indicators was 0.81. The comparison showed that the confidence level of the new model was 0.46 higher than that of the traditional model, and the output value of the adaptive index was 0.24 higher than that of the traditional model. It could be seen that the confidence level of financial informatization and the rise of adaptive indicators both indicated that ERP could improve the efficiency of financial data collection of power enterprises. The reliability of its data would also continue to improve with the expansion of financial data samples, and the accuracy of its adaptive indicators would also be better than manual data accounting. Finally, the informatization level and financial risk level calculated by the indicators of financial informatization under ERP were analyzed and compared with the original financial data model, as shown in Figure 7.

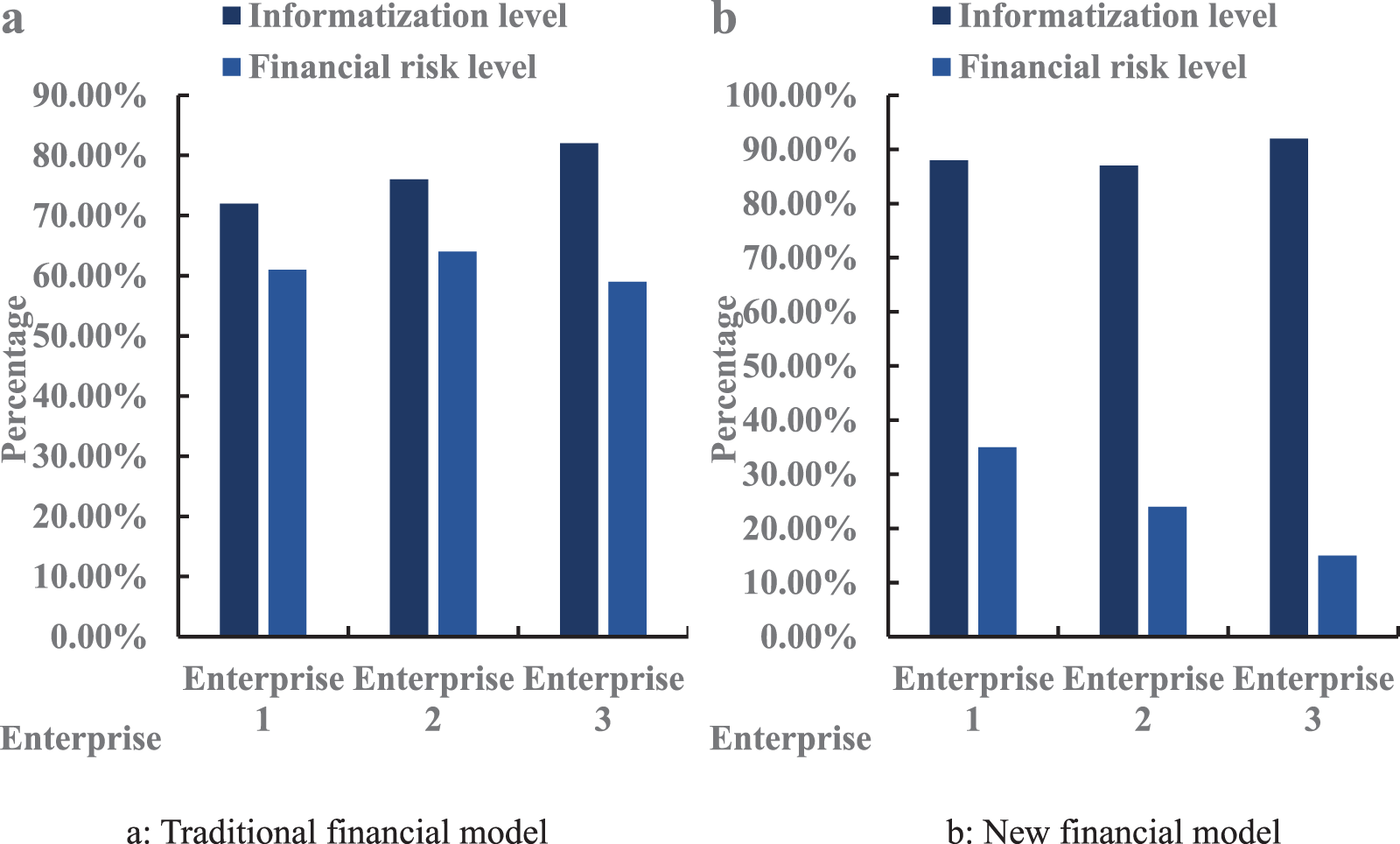

Comparison of informatization level and financial risk level calculated by financial informatization indicators.

Figure 7(a) shows the traditional financial model, and Figure 7(b) shows the new financial model. The informatization level of the new financial model was higher than that of the traditional financial model, while the financial risk level was lower than that of the traditional financial model. According to Figure 7(a), the informatization level of the three enterprises under the traditional financial model was 72%, 76%, and 82% respectively. The financial risk level was 61%, 64%, and 59% respectively; according to Figure 7(b), the informatization level of the three enterprises under the new financial model was 88%, 87%, and 92% respectively. The financial risk level was 35%, 24%, and 15% respectively. The average informatization level of enterprises in the traditional mode was 76.7%, and the average financial risk level was 61.3%; the average informatization level of enterprises under the new model was 89%, and the average financial risk level was 24.7%. Through comparison, it could be seen that the level of enterprise informatization under the new financial model was 12.3% higher than the traditional model, and the level of financial risk was 36.6% lower than the traditional model.

Through the experiment in this paper, it was found that after applying ERP to the financial informatization of power enterprises, the data accuracy and information reliability of enterprises would be improved, and the informatization level would also increase. This was because ERP could scientifically and reasonably plan the enterprise's management system and improve the staff's cognitive level of financial data. With the optimization of the adaptive calculation model, the accuracy of the financial data accounting of power enterprises gradually increased, and the confidence level also increased significantly.

In the focus of financial informatization, the ERP system combines information technology with advanced management concepts, which truly reflects the rationalization of the company's resource allocation and meets the needs of business development to the greatest extent. The establishment of a reliable ERP financial management system is crucial for the long-term sustainable development of enterprises. Proper use of power financial information can further improve the power financial system and promote the sustainable development of power companies. Leaders in the power industry pay more attention to the application of ERP and use scientific and reasonable management methods to implement innovative internal financial control, to improve financial management level, and put enterprises in an invincible position in the market economy. This paper proved that ERP could effectively improve the accuracy of financial adaptive calculation through experimental analysis. However, due to the effectiveness of the research sample in this paper, although the same research results as other literature were obtained, there were still some defects. The research results of this paper could also be applied to the subsequent financial information construction, which provided an adaptive computing model for financial intelligent information.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.