Abstract

This study examines the asymmetric effect of ESG uncertainty (ESGUI) on U.S. tourism equity returns over the period 2005:07–2025:04. To provide a richer statistical account of this relationship, the study applies an asymmetric wavelet quantile regression framework that jointly captures distributional heterogeneity, frequency-specific dynamics, and sign asymmetry. The results show that aggregate ESGUI is insignificant in the short term across all quantiles, but becomes positive in the medium term at the extreme lower tails (0.01–0.05) and middle-to-upper quantiles (0.40–0.80), while in the long term it remains positive at the lower quantiles (0.01–0.40) and turns negative at the upper quantiles (0.80–0.90). Positive ESGUI shocks exert a short-run negative effect only at the 0.30 quantile, but become supportive in the medium term at (0.01) and across (0.30–0.90), while in the long term they are negative at the lower tail (0.01–0.30) and positive from (0.40–0.99). Negative ESGUI shocks are positive in the short term at the extreme tails (0.01 and 0.99), remain positive in the medium term at (0.01–0.10), and in the long-term support lower-tail market states (0.01–0.20) but reduces returns from the middle to upper quantiles (0.40–0.99). The study proposes policy implications based on these results.

Introduction

Tourism is widely recognised as one of the most important drivers of global economic activity, with travel and tourism accounting for around 10.5% of global GDP and a similar share of global employment. 1 Because this macroeconomic weight is intermediated through listed firms such as airlines, hotel chains, cruise operators, tour operators, wellness providers and online travel platforms, tourism-related equities (TOR) have attracted growing attention from academics, investors and policymakers who seek to understand which forces drive their returns and risk. Early work on tourism finance (see., refs.1,2,3) focused mainly on macroeconomic fundamentals and broad uncertainty indicators and showed that economic policy uncertainty and global uncertainty exert significant negative effects on tourism stock indices and listed tourism companies.

At the same time, tourism is both carbon intensive and environmentally sensitive, with tourism activities estimated to account for about 8% of global CO2 emissions including transport, accommodation and leisure services, 4 while empirical evidence suggests that tourism revenues and activity are highly vulnerable to climate-related shocks and climate vulnerability more generally.5,6 This combination of a sizeable emissions footprint and high exposure to climate risks has made environmental, social and governance considerations central to the way tourism firms are evaluated in capital markets. Recent studies show that stronger ESG performance and better ESG disclosure are associated with higher market value, improved financial performance and reduced risk for listed travel and tourism companies (see., refs.7–10) and that in wellness and tourism industries higher ESG, management and governance scores tend to raise stock returns while lowering return volatility. 11 This evidence suggests that the ESG profile of tourism firms has become a core determinant of how TOR are priced.

Building on this ESG–performance nexus, a growing strand of the finance literature highlights ESG uncertainty, which is driven by rating divergence, evolving disclosure standards and policy ambiguity, as a distinct risk channel. 12 show that ESG rating uncertainty raises the equity risk premium and lowers investor demand for risky assets, 13 documents a close interaction between ESG uncertainty, investor attention and stock price crash risk, and recent surveys indicate that ESG rating disagreement and uncertainty can distort asset pricing and increase firms’ financing costs. In parallel, 14 propose the ESG-based Sustainability Uncertainty Index, ESGUI, a news-based indicator that captures country-level uncertainty around ESG and sustainability issues and that co-moves strongly with broader uncertainty benchmarks such as the World Uncertainty Index and economic policy uncertainty, which makes ESGUI a natural tool for sectoral and asset-pricing applications. While climate policy uncertainty indices have been used to study tourism development and tourism demand, empirical evidence directly linking ESG-based uncertainty measures such as ESGUI or ESG rating dispersion to tourism-related equities remains scarce.

Against this background, focusing on ESGUI and tourism-related equities addresses an important gap by treating ESG-related uncertainty as a sector-relevant risk factor that can affect tourism stocks through expected cash flows, discount rates, and perceived transition and reputational risks. It also allows us to test whether ESG-related uncertainty matters for tourism equity returns beyond conventional macroeconomic and uncertainty controls. This study contributes to the literature by examining the link between ESGUI and U.S. tourism-related equities within an asymmetric wavelet quantile regression framework. The empirical contribution lies in identifying whether ESG-related uncertainty is priced in tourism stocks. The methodological contribution lies in showing how increases and decreases in ESGUI propagate differently across the conditional distribution of returns and across short-, medium-, and long-term horizons.

This framework goes beyond standard linear and symmetric specifications by accommodating features that are common in financial data but remain underexplored in the tourism–finance literature, namely state dependence, sign asymmetry, and time-scale heterogeneity. By revealing whether positive ESGUI shocks generate different pricing effects from negative shocks, and whether these effects are concentrated in downside or upside return tails and at particular horizons, the analysis provides a richer and more policy-relevant understanding of tourism stock risk. The findings therefore offer useful guidance for regulators, investors, and destination managers in designing ESG disclosure rules, portfolio risk-management practices, and sustainability strategies that recognise the asymmetric and horizon-dependent pricing of ESG uncertainty in tourism equity markets.

The remainder of the article is organized as follows. The next section discusses a synopsis of prior studies, section 3 presents the data and methodology, section 4 reports the empirical findings, and section 5 concludes the study with policy remarks.

Literature review

ESG performance in tourism and tourism-related equities

The literature increasingly shows that ESG performance matters for tourism firms and tourism-related equities, although the direction and strength of the effect are not always identical across outcomes. A common view is that stronger ESG performance improves firm reputation, strengthens stakeholder confidence, enhances operational resilience, and can support market valuation. In the tourism and travel sector, 9 show that ESG factors are associated with the market value of travel and tourism firms, with governance appearing especially influential. In the hospitality setting, 15 further indicate that sustainability-related recognition carries valuation effects in equity markets, suggesting that investors respond to ESG-relevant signals in tourism-related firms. More recent tourism-focused evidence also links ESG to operational efficiency and broader firm outcomes. For example, 16 report that ESG performance is tied to operational efficiency in tourism enterprises, while Lei and 17 show that stronger ESG performance can help reduce stock price volatility in tourism companies. At the same time, the literature is not entirely one-directional. 8 find a negative association between ESG scores and profitability in the European tourism industry, implying that the financial implications of ESG may depend on the performance measure used, the maturity of ESG practices, and the institutional setting. Overall, the literature suggests that ESG performance is relevant for tourism and tourism-related equities, but its effects appear conditional rather than mechanically uniform.

ESG uncertainty, tourism and equities

Compared with the literature on ESG performance itself, research on ESG uncertainty in tourism and tourism-related equities remains much thinner. Existing work nonetheless suggests that uncertainty connected to ESG, sustainability disclosure, and broader policy or climate conditions can shape tourism firms through risk, valuation, and market stability channels. 18 shows that ESG disclosures help weaken the adverse impact of political and climate-related uncertainties on tourism firms’ total and systematic risks, implying that ESG-related information can serve as a buffer when uncertainty rises. Relatedly, emerging evidence indicates that ESG-linked forces may stabilize tourism markets under stress rather than merely reflect firm-level sustainability posture. 19 find that the ESG index acts as a systemic stabilizer in the global tourism market, which supports the idea that ESG-linked conditions matter for tourism equity dynamics beyond standard accounting performance. At a broader level, 20 argue that ESG research in hospitality and tourism is still underdeveloped and has not yet fully moved from CSR-based discussions to a more precise ESG framework. This matters because uncertainty in tourism-related equities is likely to operate through several channels at once, including firm disclosures, investor sentiment, climate concerns, and market-wide re-pricing. Thus, while the available literature points to an important role for ESG-related uncertainty in shaping tourism and equity outcomes, the evidence remains fragmented and still lacks an integrated market-based explanation.

Gap in the literature

Three important gaps emerge from the existing literature. First, most tourism studies concentrate on ESG performance itself rather than ESG uncertainty, even though uncertainty may affect tourism-related equities through channels that differ from realized ESG scores or sustainability disclosures. Second, the available evidence remains fragmented across firm value, profitability, volatility, operational efficiency, and risk, with limited effort to integrate these outcomes within a single framework for tourism-related equities. Third, the hospitality and tourism ESG literature still pays insufficient attention to how ESG-related influences vary across market states, time horizons, and the direction of shocks. In particular, little is known about whether ESG uncertainty affects tourism-related equities differently across the lower, middle, and upper parts of the return distribution, whether these effects change over the short, medium, and long term, and whether positive and negative ESG uncertainty shocks generate asymmetric responses. This omission is important because tourism equities are highly sensitive to information shocks, investor sentiment, and changing sustainability narratives, meaning that favorable and adverse ESG-related disturbances may not produce effects of the same magnitude or persistence. Against this background, the present study advances the literature by moving the focus from ESG performance to ESG uncertainty and by examining its symmetric as well as asymmetric effects on tourism-related equities within a distribution-sensitive and horizon-specific framework.

Data and method

Data

The study examines the impact of ESG uncertainty

2

(ESGUI) on tourism-related equities

3

(TOR) using the case of the USA and from 2005:07–2025:04. The study uses ESGUI proposed by.

14

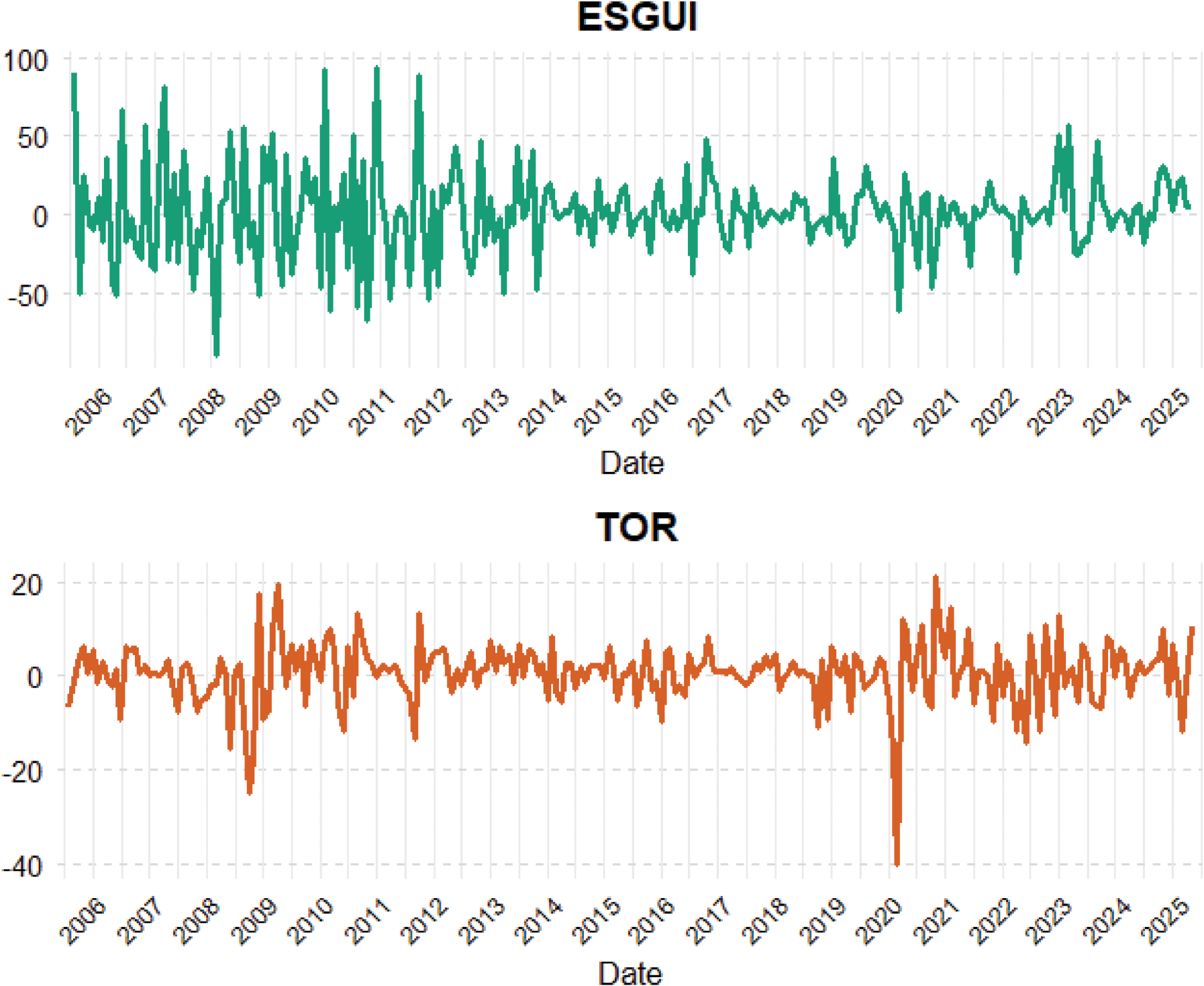

This proxy measures country-level uncertainty surrounding ESG issues using text-based information from Economist Intelligence Unit (EIU). It is built by combining normalized indices of ESG-related term frequency with an uncertainty sub-index based on words such as “uncertain” and “uncertainty,” thereby capturing both the intensity of ESG discourse and the degree of uncertainty around these topics. Furthermore, the study uses tourism-related equities proxied by the Invesco Dynamic Leisure and Entertainment ETF (PEJ), which tracks U.S. firms operating in leisure, travel, hotels, restaurants, entertainment, and related consumer services. PEJ tracks U.S. companies in leisure, travel, hotels, restaurants, entertainment, and related consumer services, thereby providing a broad, market-based measure of tourism-exposed listed firms and capturing aggregate movements in tourism-related equity valuations. The series are transformed into logarithmic returns, defined as

Log returns of ESGUI and TOR.

Traditional quantile regression

For two time series

Quantile regression (QR), introduced by, 21 extends the classical linear regression framework by estimating conditional quantiles of the dependent variable rather than only its conditional mean. Unlike ordinary least squares, which focuses on average effects, quantile regression allows the effect of the explanatory variable to vary across the entire conditional distribution of the outcome variable, thereby providing richer evidence on heterogeneous responses across lower, middle, and upper parts of the distribution. 22

Since relationships between variables may differ across time horizons, traditional quantile regression may overlook important scale-dependent dynamics. To address this issue, Wavelet Quantile Regression suggested by

23

combines the maximal overlap discrete wavelet transform (MODWT) suggested by

24

with quantile regression so that the effect of

Let

The maximum admissible number of decomposition levels in the MODWT (see.,24,25) is bounded by

To account for asymmetry, the explanatory variable is decomposed into positive and negative innovations. Since the variables are expressed in first differences or returns before estimation,

Applying the MODWT separately to

The asymmetric Wavelet Quantile Regression framework is then specified through two separate scale-specific quantile models.

For positive shocks in

For negative shocks in

By comparing

Basic statistical information

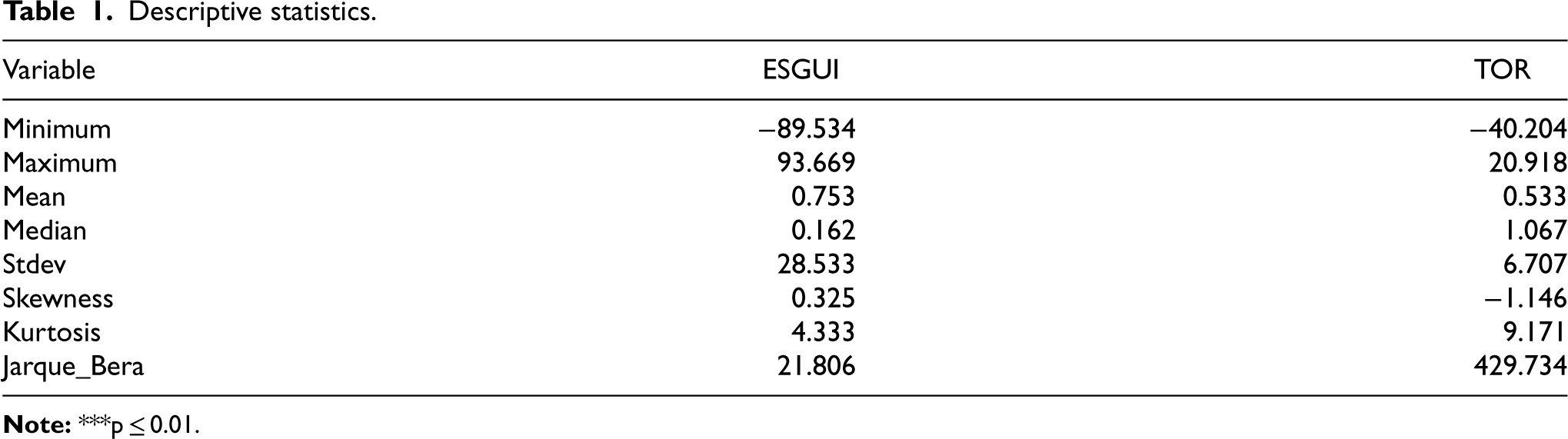

Descriptive statistics.

Descriptive statistics.

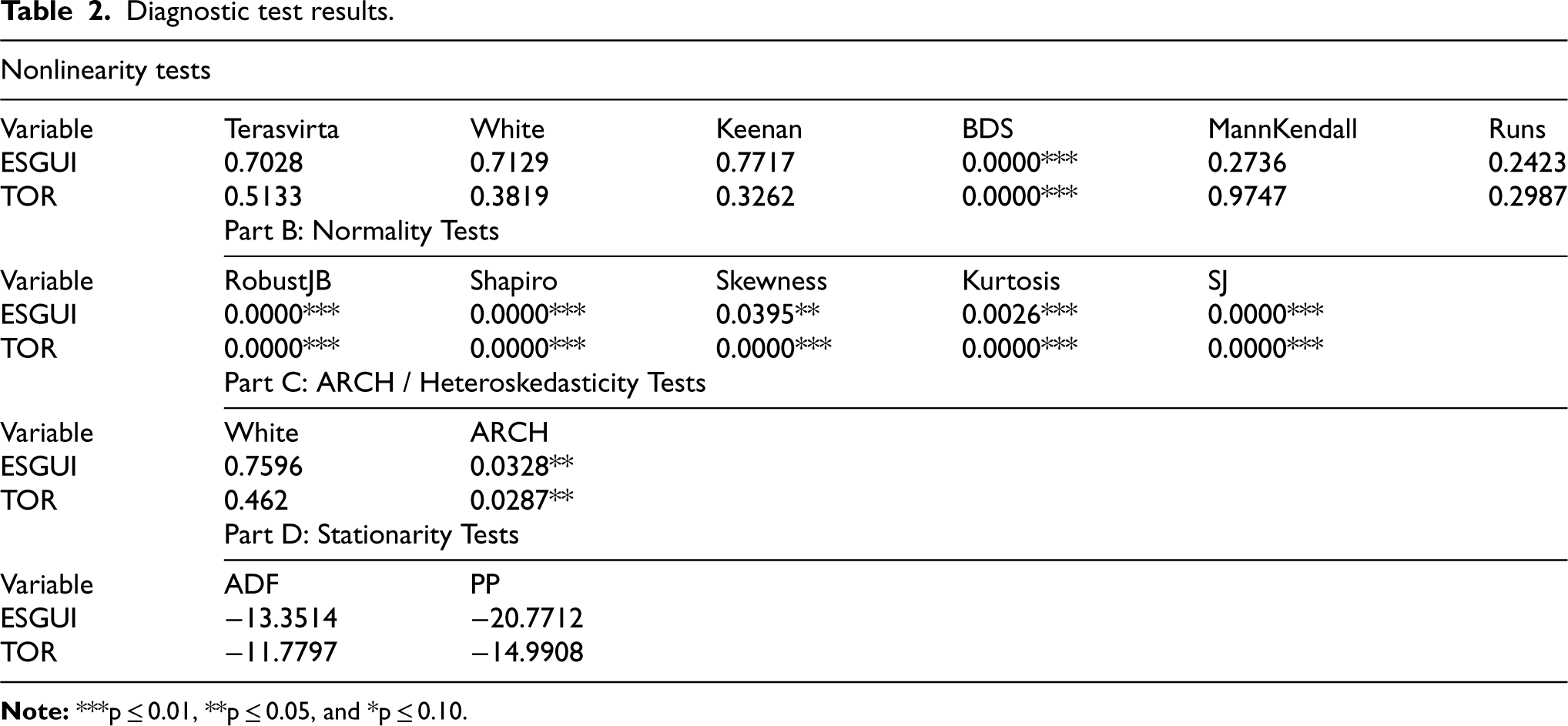

Table 2 reports a comprehensive wavelet-based diagnostic check for ESGUI and TOR and shows clear evidence of nonlinear, non-normal and heteroskedastic behaviour across most scales. In the nonlinearity tests, the Terasvirta, White, Keenan, Mann-Kendall, and Runs statistics are insignificant for both variables, suggesting no strong evidence from those procedures alone. However, the BDS test is highly significant at the 1% level for both ESGUI and TOR, which provides strong evidence of nonlinear dependence and implies that the series are not purely linear or independently distributed. The normality results further show that both variables depart markedly from the normal distribution. For ESGUI, the Robust Jarque–Bera, Shapiro, Kurtosis, and SJ tests are significant at the 1% level, while the Skewness test is significant at the 5% level. For TOR, all normality tests are significant at the 1% level, confirming pronounced non-normality. In the heteroskedasticity tests, the White test is insignificant for both series, but the ARCH test is significant at the 5% level, indicating the presence of conditional heteroskedasticity or volatility clustering. Finally, the ADF and PP statistics are strongly negative for both ESGUI and TOR, showing that both variables are stationary at level.

Diagnostic test results.

Diagnostic test results.

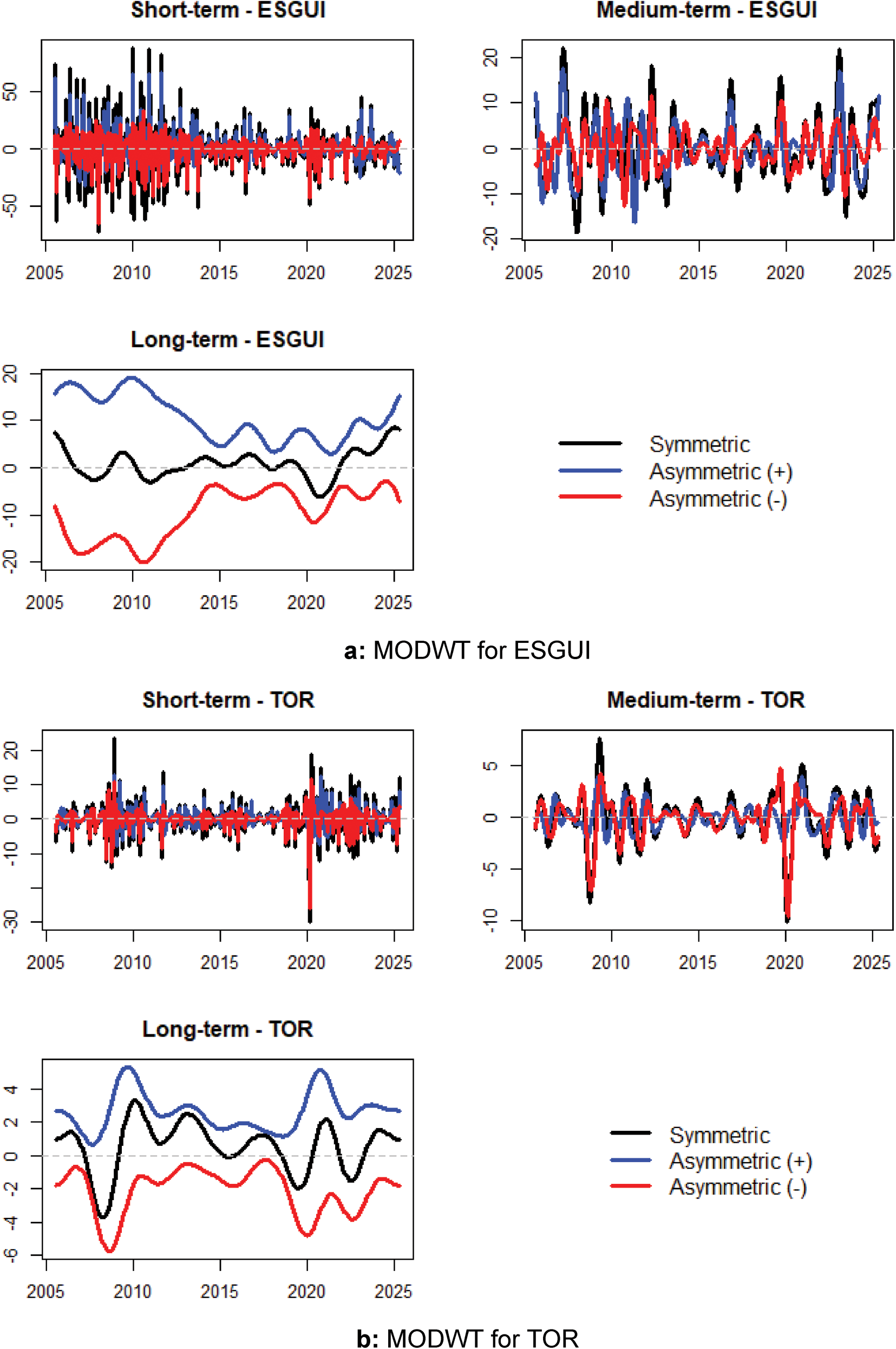

Figure 2 (a, b) present the MODWT decomposition of TOR and ESGUI across short-term, medium-term, and long-term horizons, while also distinguishing the symmetric, asymmetric positive, and asymmetric negative components. In the short term, both variables show sharp and frequent fluctuations around zero, indicating that temporary shocks dominate their movements at higher frequencies. Here, the symmetric component captures the overall variation, while the asymmetric positive and asymmetric negative components reveal that upward and downward changes do not follow the same path or intensity. In the medium term, the movements become more regular and cyclical, with TOR showing smoother oscillations and ESGUI still displaying relatively stronger swings. In the long term, the trends become much smoother and more persistent, making the separation between components clearer. For TOR, the symmetric component follows a moderate and stable wave-like pattern, while the asymmetric positive component remains above it and the asymmetric negative component stays below it, suggesting sustained differences between favorable and adverse movements over time. ESGUI shows an even stronger long-run pattern, with the asymmetric positive component staying persistently high and the asymmetric negative component remaining distinctly low, indicating stronger long-term asymmetry. In summary, both TOR and ESGUI contain significant symmetric and asymmetric behaviour, and that these trends become more visible and persistent as the time horizon lengthens. These results validate the use of asymmetric techniques in exploring the nexus between ESGUI and TOR.

(a) MODWT for ESGUI. (b) MODWT for TOR.

The study employed AWQR to capture the asymmetric effect of ESGUI on TOR. MODWT is implemented with boundary handling (often periodic extension) to limit edge distortions and reduce leakage at the start and end of the sample, while the la8 filter is typically preferred because its near-symmetry and longer support deliver smoother, less phase-distorting decompositions than very short filters like Haar, giving more reliable time–frequency patterns for economic and financial series.

For the monthly data used in this study, the wavelet components are grouped into 3 time horizons. The short-term horizon captures fluctuations of up to 8 months, the medium-term horizon covers movements between 8 and 32 months, while the long-term horizon reflects dynamics beyond 32 months, including the low-frequency scaling component associated with persistent or trend-like behaviour.

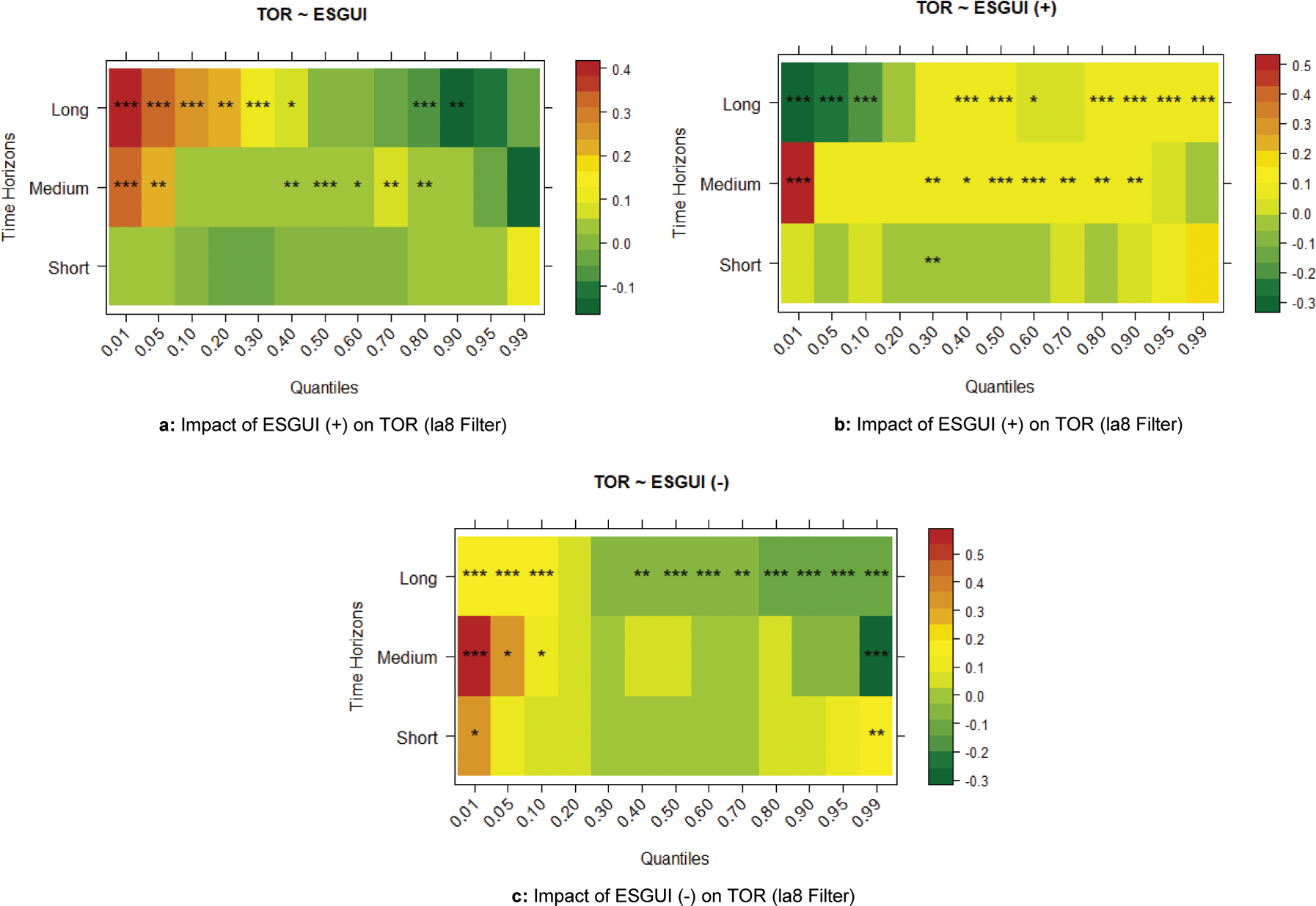

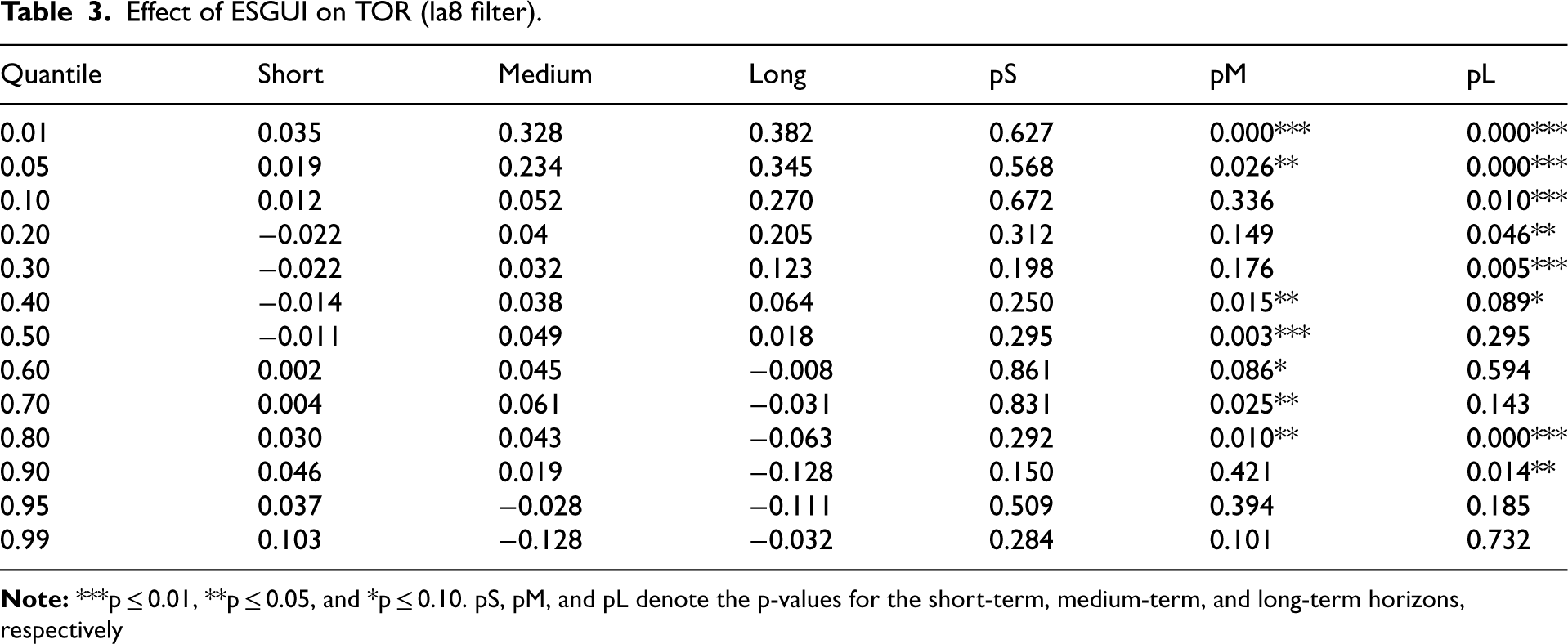

Figure 3(a) (Table 3a) presents the effect of ESGUI on TOR in the United States by considering both the aggregate and the disaggregated dimensions of ESG uncertainty. For the aggregate ESGUI measure, the short-term effect remains insignificant across all quantiles, suggesting that U.S. tourism-related equities do not react immediately to broad ESG uncertainty shocks. This muted short-run response may reflect the fact that tourism firms in the United States often adjust with a lag, since investors initially treat ESG-related uncertainty as background information rather than as an immediate pricing factor. In the medium term, however, ESGUI exerts a positive influence at the extreme lower tails (0.01–0.05) and across the middle-to-upper quantiles (0.40–0.80). This pattern implies that once uncertainty persists, investors may begin to interpret ESG-related pressure as a catalyst for strategic repositioning, stronger disclosure, and improved sustainability alignment within the U.S. tourism sector. In the long term, the effect remains positive and becomes stronger at the lower quantiles (0.01–0.40), but turns negative at the upper quantiles (0.80–0.90). This indicates that under weak market conditions, sustained ESG-related uncertainty may encourage defensive adaptation and resilience-building, whereas under already strong market states, prolonged uncertainty may raise compliance costs, intensify valuation concerns, and weaken optimism toward tourism equities.

(a) Impact of ESGUI (+) on TOR (la8 filter). (b) Impact of ESGUI (+) on TOR (la8 filter). (c) Impact of ESGUI (-) on TOR (la8 filter).

Effect of ESGUI on TOR (la8 filter).

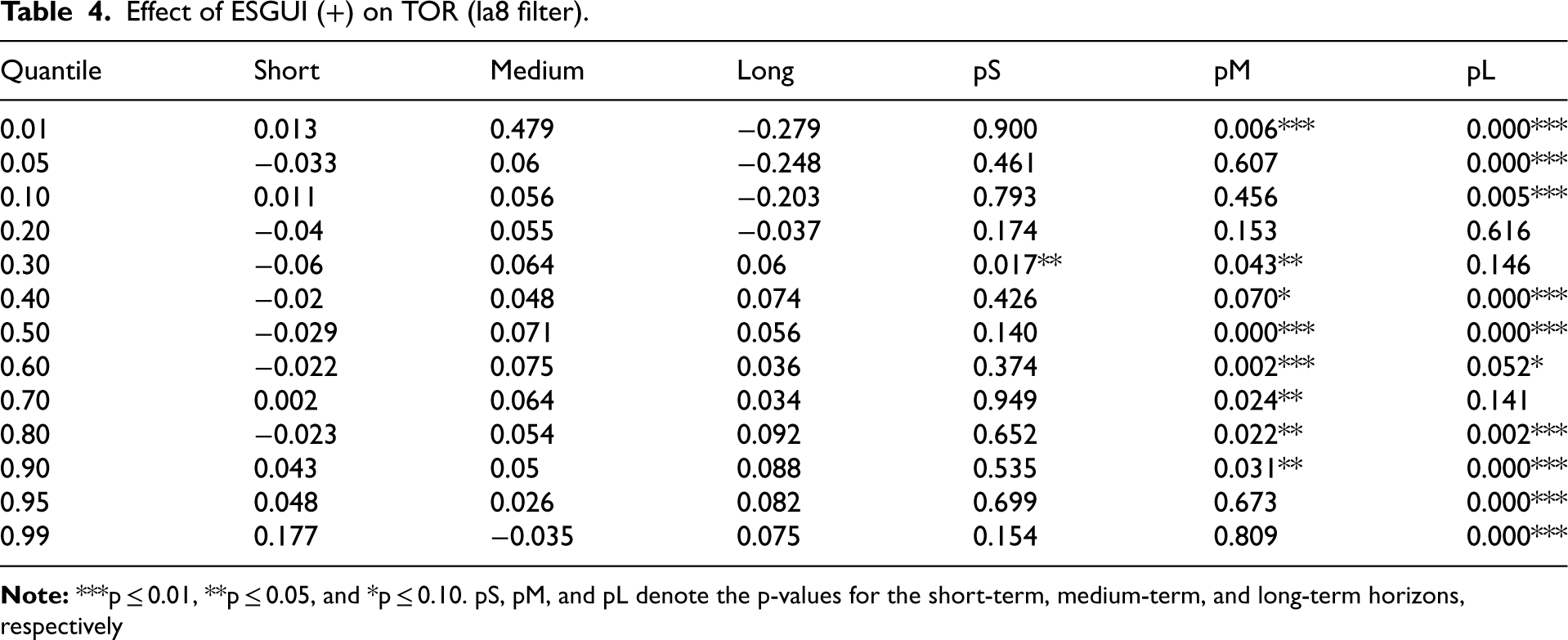

A more refined picture emerges when positive ESG uncertainty shocks (see Figure 3(b) and Table 4), denoted as ESGUI (+), are considered. In the short term, the effect is negative and significant only at the 0.30 quantile, indicating that a rise in favorable or upward ESG-related uncertainty may briefly unsettle moderately performing U.S. tourism equities. One plausible reason is that positive ESG signals can still carry adjustment costs, as firms may be expected to upgrade sustainability standards, improve governance practices, or respond to changing investor preferences before the benefits are fully realized. In the medium term, the effect turns positive at the extreme lower tail (0.01) and across a broad range of quantiles (0.30–0.90), showing that U.S. tourism-related stocks increasingly benefit once the market has time to absorb and price these shifts. Investors may then perceive ESG-oriented uncertainty as a sign of transition, innovation, and long-run competitiveness, especially in a sector where environmental reputation and stakeholder confidence matter greatly. In the long term, ESGUI (+) is negative at the lower quantiles (0.01–0.30) but becomes positive from the middle to the extreme upper quantiles (0.40–0.99). This suggests that firms operating in distressed market states may struggle to convert favorable ESG-related developments into performance gains, while firms in stronger states appear better positioned to transform such uncertainty into enhanced investor confidence and superior equity performance.

Effect of ESGUI (+) on TOR (la8 filter).

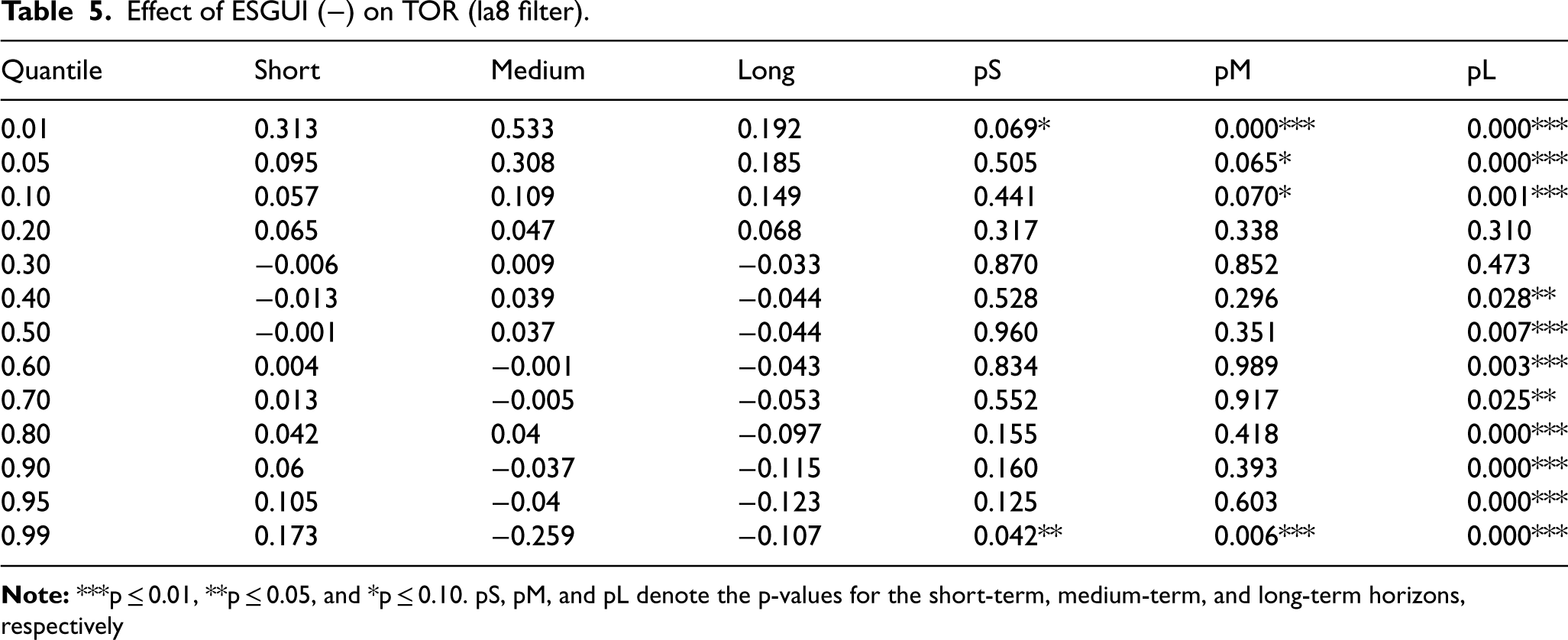

The response to negative ESG uncertainty shocks (see Figure 3(c) and Table 5), captured by ESGUI (-), is even more state dependent in the U.S. case. In the short term, the effect is positive and significant at the extreme tails (0.01 and 0.99), implying that both deeply depressed and highly buoyant tourism equities react sharply to adverse ESG uncertainty shocks. This may reflect speculative repositioning at the lower tail and temporary overreaction or hedging behavior at the upper tail. In the medium term, ESGUI (-) remains positive at the lower quantiles (0.01–0.10), but becomes negative at the extreme upper quantile (0.99). Such a pattern suggests that when market conditions are weak, negative ESG uncertainty may trigger bargain-hunting or expectations of corrective policy and firm-level responses, thereby supporting tourism equities. By contrast, when valuations are already stretched, adverse ESG news is more likely to be interpreted as a threat to profitability, brand image, and future demand. The long-term estimates reinforce this asymmetry, showing a positive effect at the lower quantiles (0.01–0.20) and a negative effect from the middle to the upper quantiles (0.40–0.99). Overall, this reveals that in the United States, ESG uncertainty does not exert a uniform influence on tourism-related equities. Its effect depends on whether the shock is aggregate, positive, or negative, and on whether the tourism equity market is operating in distressed, normal, or exuberant conditions.

Effect of ESGUI (−) on TOR (la8 filter).

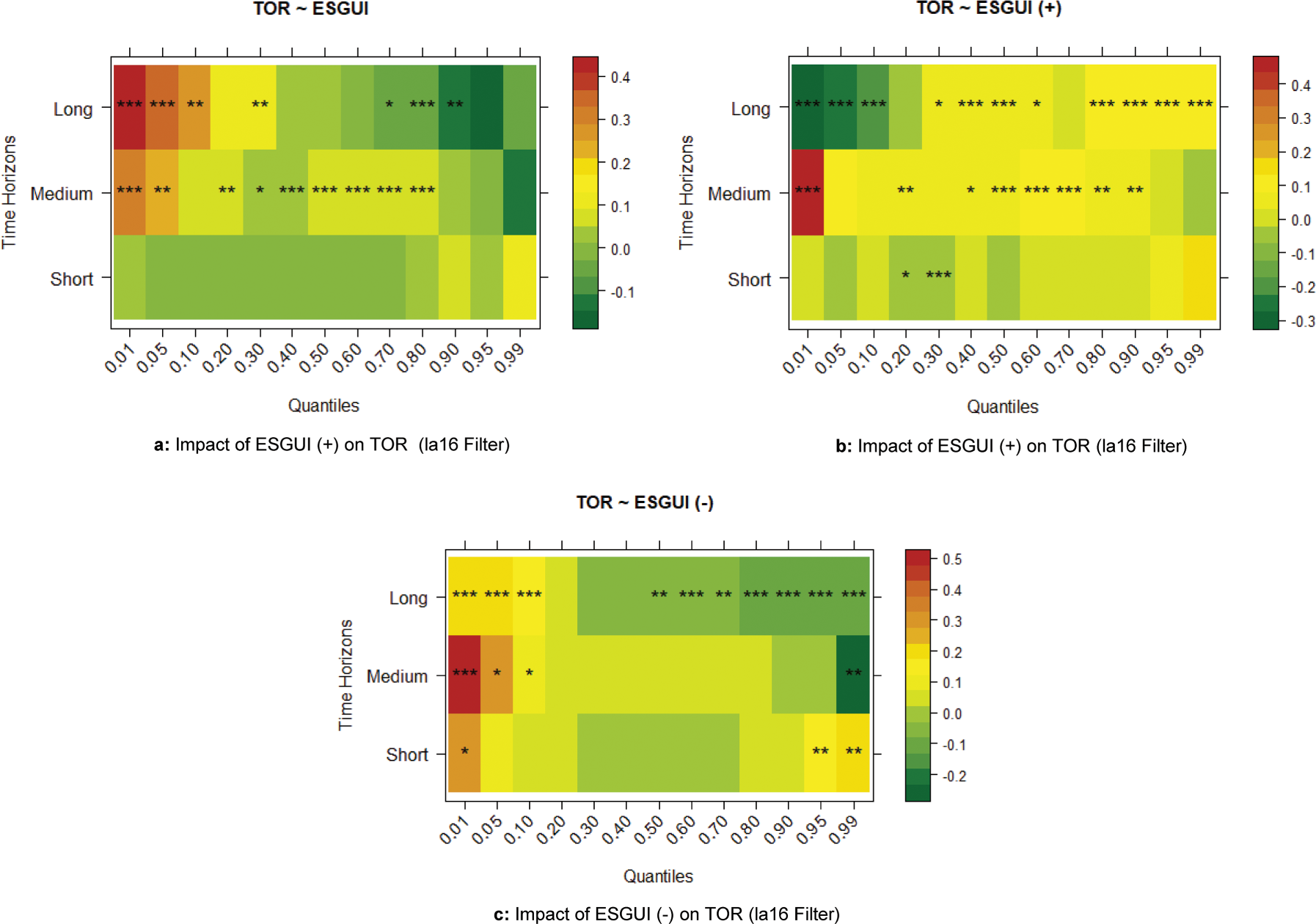

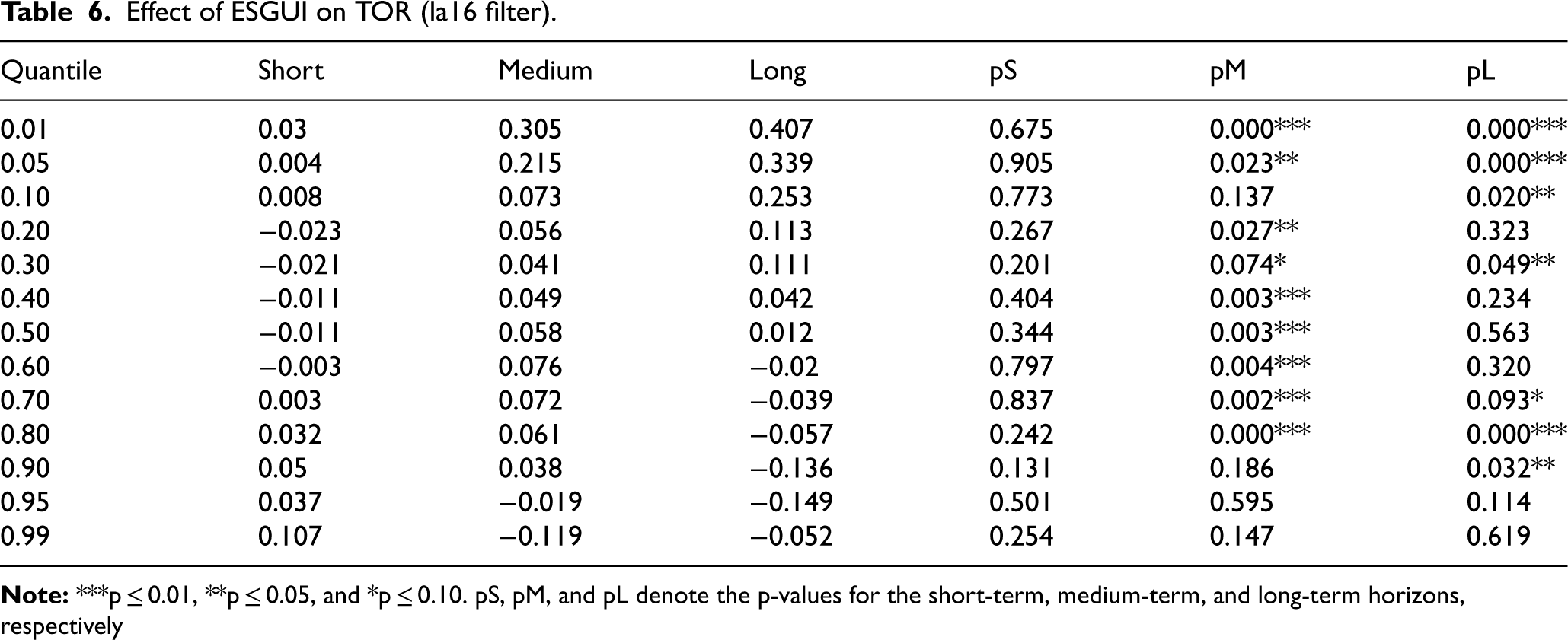

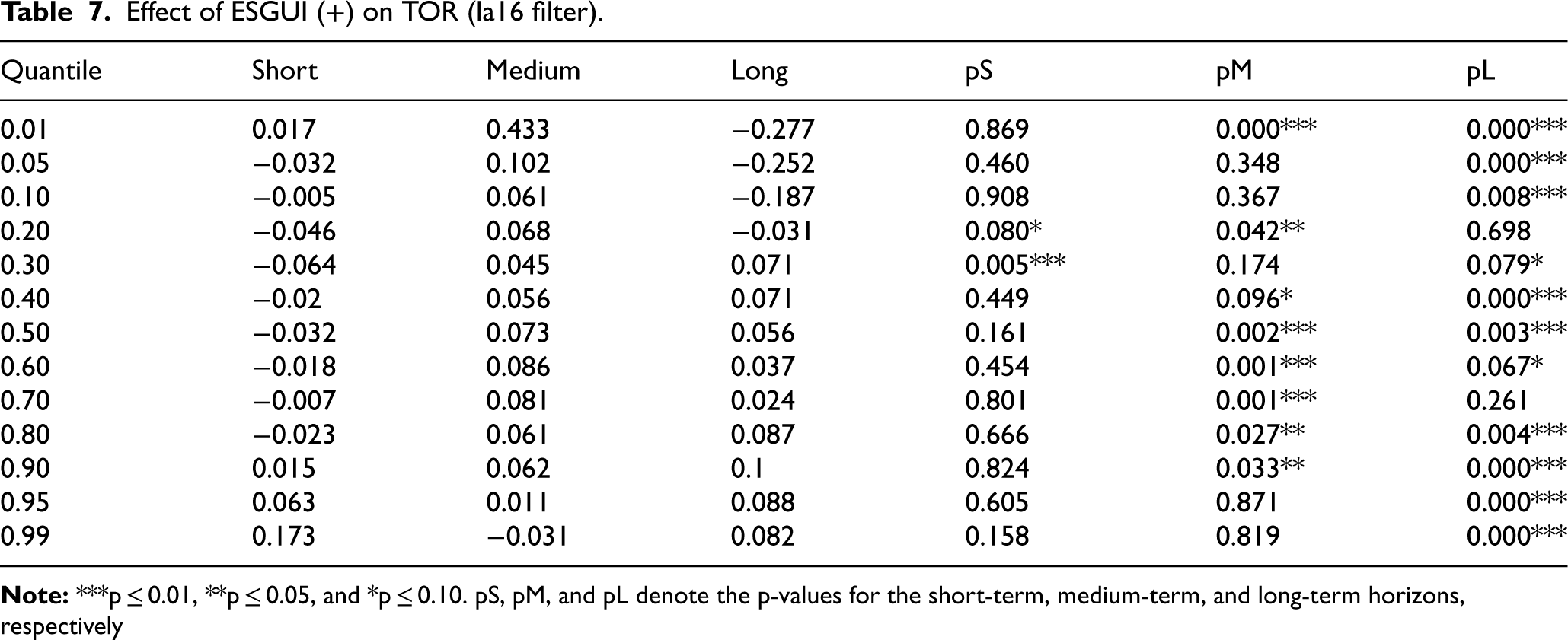

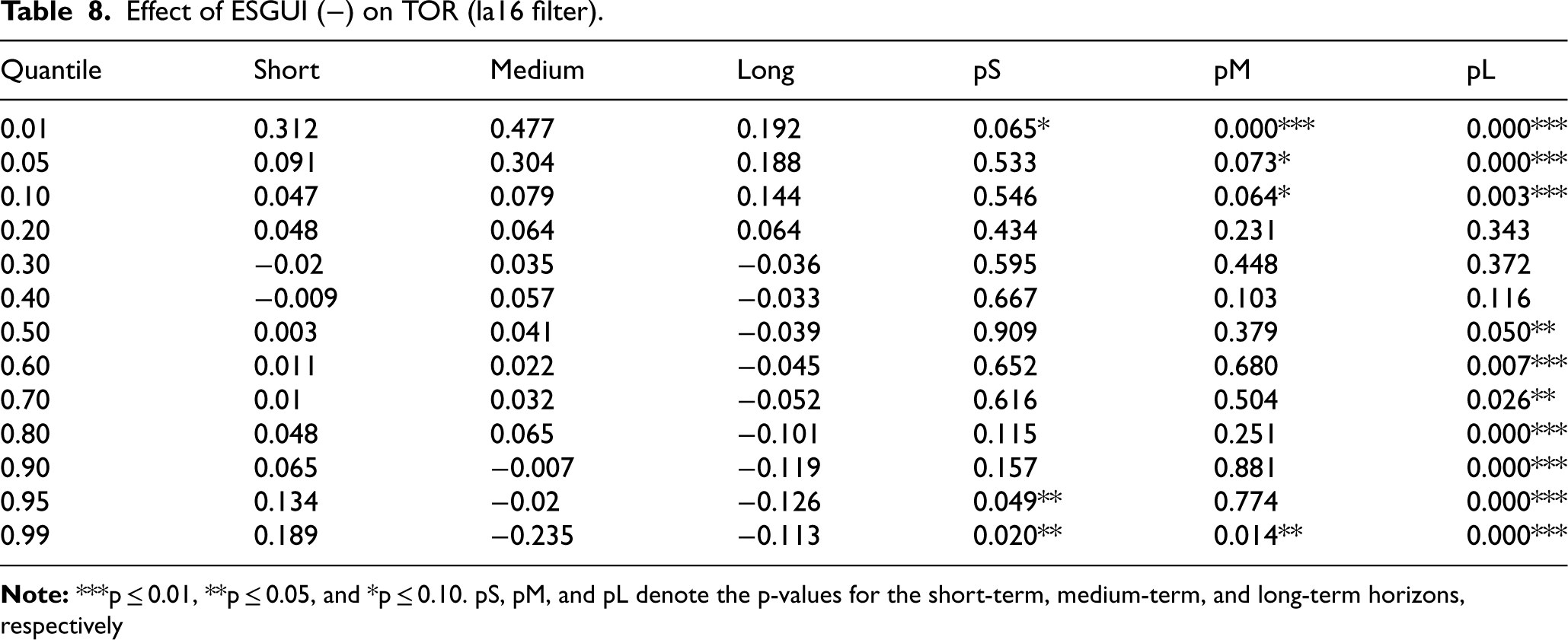

The AWQR model for the impact of ESGUI on TOR was also re-estimated using the least-asymmetric Daubechies LA16 wavelet filter (see Figure 4(a)–(c) and Tables 6–8) as a robustness check to the baseline LA8 specification. The resulting heatmaps display very similar patterns in the sign, magnitude, and statistical significance of the ESGUI coefficients across quantiles and time horizons, indicating that the findings are not sensitive to the choice of wavelet filter. This stability reinforces the robustness of our findings and supports the use of the LA8 filter as the main specification in the analysis.

(a) Impact of ESGUI (+) on TOR (la16 filter). (b) Impact of ESGUI (+) on TOR (la16 filter). (c) Impact of ESGUI (-) on TOR (la16 filter).

Effect of ESGUI on TOR (la16 filter).

Effect of ESGUI (+) on TOR (la16 filter).

Effect of ESGUI (−) on TOR (la16 filter).

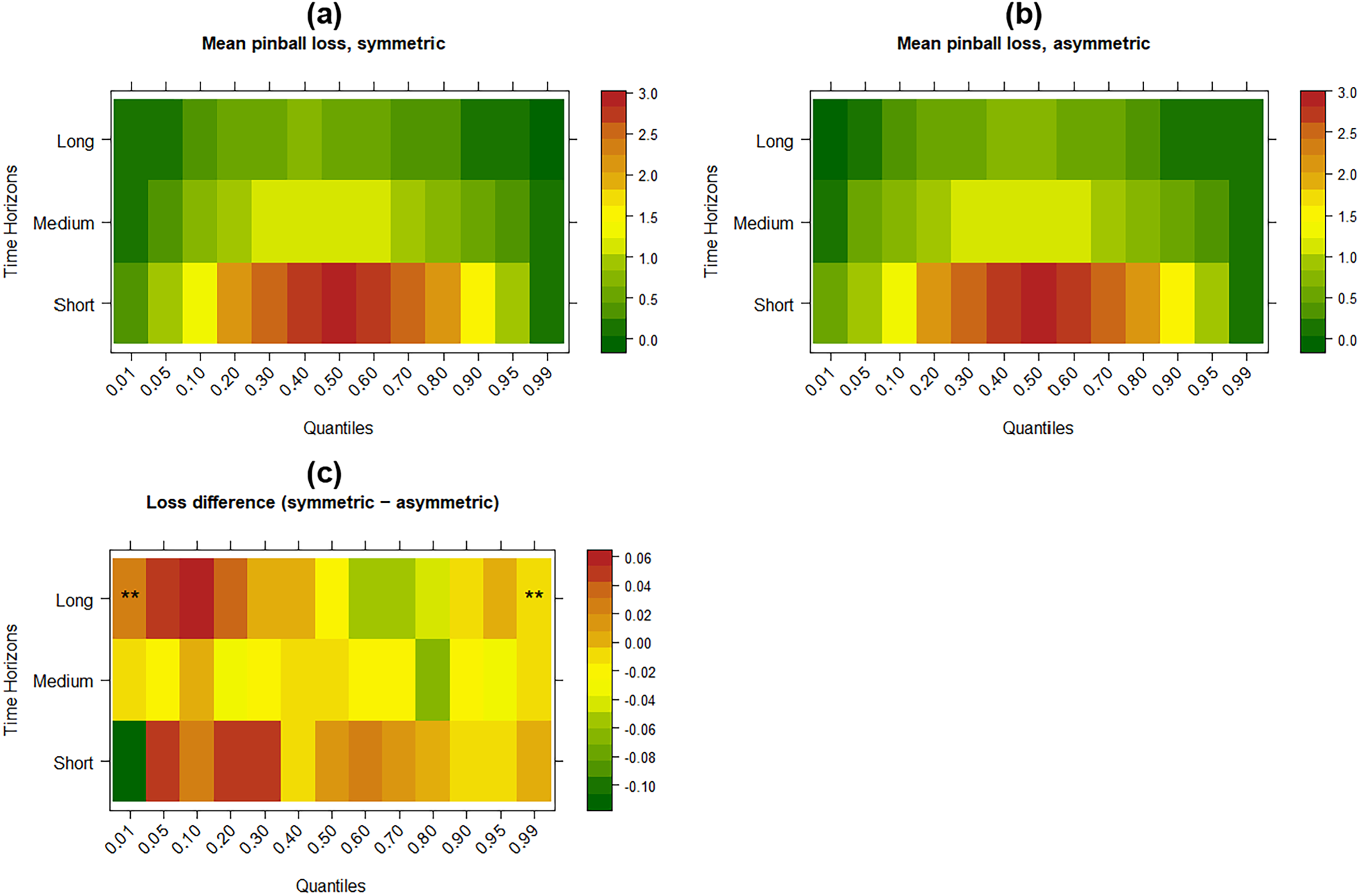

(a) Mean pinball loss, symmetric specification. Fig. 5b: Mean pinball loss, asymmetric specification. Fig. 5c: Loss difference (symmetric – asymmetric).

Figure 5(a) and Figure 5(b) present the out-of-sample mean pinball loss for the symmetric and asymmetric specifications across quantiles and time horizons, where greener shades denote lower loss and better forecast accuracy, while yellow-to-red shades indicate larger forecast errors. In both panels, the largest losses are concentrated in the short horizon, with the most pronounced forecast difficulty appearing around the middle quantiles, especially within the range of (0.20–0.80) and peaking most visibly around (0.40–0.60). This pattern suggests that short-run movements in tourism-related equities are more volatile and harder to anticipate, particularly under normal market conditions rather than at the extreme tails. By contrast, the medium horizon records more moderate losses, mainly concentrated around the central quantiles (0.30–0.70), while the long horizon exhibits the lowest and most stable losses overall, with especially small errors at the extreme quantiles (0.01) and (0.99). Taken together, the figure indicates that TOR becomes more predictable as the forecasting horizon lengthens.

A comparison of Figure 5(a) and Figure 5(b) further shows that the symmetric and asymmetric specifications display very similar broad patterns, but the asymmetric model performs slightly better in several key regions. This is especially visible in the short horizon, where the asymmetric specification appears to reduce the intensity of forecast loss across much of the distribution, notably from the lower-middle to upper-middle quantiles (0.05–0.80). Such a result implies that allowing ESG uncertainty to enter through separate positive and negative components captures nonlinear and state-dependent responses that are masked under the symmetric setup. In practical terms, tourism-related equities in the United States do not respond to favorable and unfavorable ESG uncertainty in exactly the same way, and this asymmetry becomes more relevant when short-run market adjustments are strong and heterogeneous across quantiles.

Figure 5(c) confirms this interpretation by plotting the loss differential given by symmetric minus asymmetric loss. Positive values indicate that the asymmetric specification achieves lower loss and therefore outperforms, whereas negative values imply an advantage for the symmetric model. The short horizon shows the clearest gains from asymmetry across a wide band of quantiles, especially from (0.05–0.80), although the symmetric model performs better at the extreme lower tail (0.01). In the medium horizon, the differences are generally small and clustered around zero, indicating that both models have broadly similar predictive ability, with only mild advantages for the asymmetric setup in selected quantiles. In the long horizon, the pattern becomes more mixed. The asymmetric model performs better at the lower quantiles (0.01–0.40) and again near the extreme upper tail (0.90–0.99), whereas the symmetric model has an edge around the middle-to-upper range (0.50–0.80). The asterisks in panel (c) show that the forecast-performance difference is statistically significant at the long-horizon extremes, specifically at (0.01) and (0.99), indicating that these gains are not merely visual differences but reflect meaningful improvements in predictive accuracy.

Discussion of findings

The findings show that ESG uncertainty affects U.S. tourism-related equities in a delayed and highly state-dependent manner. The insignificant short-run effect of aggregate ESGUI suggests that tourism stocks do not immediately price broad ESG uncertainty, which is consistent with evidence that tourism and leisure assets often react more strongly once uncertainty becomes persistent and begins to affect expectations about demand, profitability, and sectoral risk.28,29 In the medium and long term, the positive response of aggregate ESGUI at the lower and middle quantiles implies that sustained ESG-related uncertainty may be interpreted as a signal for strategic adjustment, stronger sustainability disclosure, and improved market positioning, especially for firms trying to rebuild confidence under weaker market states. This interpretation aligns with studies showing that sustainability engagement and CSR can enhance resilience and reduce equity-holder risk in hospitality-related firms. 30

The disaggregated results further reveal that positive ESG uncertainty shocks tend to support TOR mainly in stronger market conditions, while negative ESG uncertainty shocks are only beneficial in distressed states and become harmful from the middle to upper quantiles, indicating that investors reward adaptive ESG transition signals but penalize adverse ESG news when valuations are already high. Overall, the evidence suggests that ESG uncertainty is neither uniformly harmful nor uniformly beneficial for U.S. tourism equities; rather, its effect depends on the sign of the shock, the forecast horizon, and the prevailing market state.28,29

Conclusion and practical implications

ESG considerations have moved to the core of global financial and corporate decision making, and tourism is no exception. Tourism-related firms such as airlines, hotels, cruise operators and online travel platforms play a key role in economic growth, but are also exposed to sustainability risks and ESG scrutiny. As a result, uncertainty surrounding ESG policies, disclosures and market perceptions can strongly affect how tourism-related equities are priced. This uncertainty can operate through higher perceived regulatory and transition risk, rising compliance and adaptation costs, and shifts in investor sentiment toward carbon-intensive and socially sensitive business models.

This study advances the ESG–tourism literature by examining ESG uncertainty as a direct determinant of tourism-related equity performance in the United States. Using the ESG uncertainty index and tourism-related equity returns over 2005:07–2025:04, the study applies an asymmetric wavelet quantile regression framework that jointly captures distributional heterogeneity, time-horizon heterogeneity, and sign asymmetry. This approach makes it possible to distinguish the effects of aggregate ESG uncertainty as well as positive and negative ESG uncertainty shocks across short-, medium-, and long-term horizons and across different market states.

The findings show that the ESG–TOR relationship in the United States is nonlinear and state dependent. Aggregate ESG uncertainty is insignificant in the short term, turns positive in the medium term at the lower and middle-to-upper quantiles, and remains positive at the lower quantiles but negative at the upper quantiles in the long term. The disaggregated results reveal clear asymmetry. Positive ESG uncertainty shocks are weakly adverse in the short term, supportive in the medium term, and in the long-term, negative at the lower quantiles but positive from the middle to upper quantiles. Negative ESG uncertainty shocks are positive at the short-term tails, supportive at lower quantiles in the medium term, and in the long term positive at the lower quantiles but negative from the middle to upper quantiles.

These findings carry important implications for investors, portfolio managers, tourism firms, and statistical monitoring. ESG uncertainty should be treated as a state-dependent risk factor rather than as a uniform background condition in tourism equity pricing and portfolio allocation. More broadly, the results show the importance of statistical approaches that capture heterogeneity across market states, time horizons, and shock directions when measuring the effect of ESG-related risks. For firms and destination markets, the findings underscore the need for credible ESG disclosure, consistent sustainability strategies, and clear communication with investors, since uncertainty surrounding ESG conditions can either support or depress valuations depending on market conditions and the nature of the shock. The study also points to the value of developing more refined ESG uncertainty indicators and data-informed policy frameworks for monitoring tourism-sector financial performance and sustainability-related risk.

A key limitation is that the evidence is based on the United States and an ETF proxy (PEJ) for tourism-related equities, so the results may not fully generalise to other markets or capture firm-level heterogeneity across tourism subsectors. In addition, the AWQR specification is intentionally parsimonious and does not include control variables (e.g., macro fundamentals or alternative uncertainty measures), meaning the estimated ESGUI effects should be interpreted as bivariate, time–frequency–quantile associations rather than fully “net-of-controls” impacts. Finally, ESG uncertainty is proxied by an aggregate ESGUI index, so the analysis cannot disentangle environmental, social, and governance sub-components or identify which dimension drives the observed asymmetries.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability

All data and code necessary to reproduce the results are available at request from the corresponding author

Use of generative AI

Generative AI tools were not used to generate any manuscript text or to analyse the data. Grammarly was used solely for standard grammar, spelling, and language editing.