Abstract

This case discusses how database management systems (DBMSs) have evolved and become more sophisticated, distributed, and specialized, focusing on SAP’s transition from a traditional pipeline to a platform company. When DBMS was first introduced to the market, firms expected DBMS to store a large set of data in an organized way and extract the stored data consistently and efficiently. With the advent of technologies in the software, hardware, and networking domains, the DBMS industry has seen dramatic changes in the notions of product, customer, market, competitor, value chain partners, business model, and the industry itself. While SAP has dominated the enterprise resource planning (ERP) solution market since 1972, Oracle is closing the gap from 2018 onwards. The loss of SAP’s leadership position in some of the recent customer perception surveys may eventually lead to the loss of its market leadership position. How can SAP retain its market leadership while simultaneously regaining its leadership position in customer perception surveys form the core of this case? The case ends with questions about strategic choices that can help SAP keep up its leadership position and chart out future growth trajectory.

Keywords

Introduction

Database management systems (DBMSs) are programming applications that permit organizations to explore, gather, store, retrieve, analyze, and append enormous amounts of data across business functions and partners. Relational DBMSs are the most widely adopted among the several hierarchical, relational, network, and object-oriented types. Following the transition of the stand-alone software to the cloud, there is a growing movement toward relocating the DBMS application to the cloud. Most businesses intend to utilize the public cloud for their database administration since public cloud platforms offer various advantages, such as scalability, lower cost, and fewer support requirements. Some organizations offering well-known DBMS solutions include SAP, Oracle, MySQL, and Microsoft SQL Server. Although SAP has been the market leader in the enterprise resource planning (ERP) solution segment since 1972, Oracle’s aggressive attempt to reduce the leader-challenger gap poses a significant threat to SAP’s future leadership position. According to recent consumer-based surveys, Oracle has surpassed SAP in customer perception in certain segments (O'Shaughnessy, 2022). Oracle’s winning of these perceptual wars signals a threat to the market leadership position of SAP. This case is written against the backdrop of SAP’s current predicament of an imminent threat from Oracle, in which many industry leaders who have dominated their segments for decades may find themselves. While documenting the evolution of the DBMS industry with a focus on SAP, this case aims to encourage and challenge the participants to think through several strategic choices and alternatives that SAP may pursue to maintain its leadership position.

The database industry: Evolution

The earliest DBMS mainly served the following purposes, viz., develop and perform complex applications efficiently, easy storage, sharing, simultaneous access across departments and users, standard interfaces for communicating with and processing data, and portability across enterprise systems (IEEE Xplore, 2022). NASA was the first organization that formally used a database in a commercial project (IEEE Xplore, 2022). In 1967, IBM designed and built a system called ICS/DL/I—an automated system to track parts and materials—to aid NASA in sending a human-crewed mission to the Moon. After the Apollo 11 Moon mission was successful, IBM started releasing IBM mainframes commercially as IBM System/360 (SAP investor relations, 2022). During this time, the computer division of GE was also struggling to commercialize the IDS (Integrated Data Store). IDS was the first package to adopt the “network data model,” enabling relationships between records flexibly. IDS came with a set of powerful, functional commands and could effectively manipulate data, a feature that later evolved to become the Data Manipulation Language (Quickbase, 2022). Data Manipulation Language maintained a parallel and separate data dictionary and tracked information on the various types of records. By 1964, GE launched IDS as a bundled product for its customers (IEEE Xplore, 2022; Quickbase, 2022). As the software sold by computer manufacturers during the 1960s was platform-specific and IBM held a much larger market share than GE, IBM’s IMS became the most used package despite IDS being thought to be more flexible. Since then, the database industry has undergone fundamental changes in demand and supply (quality and quantity) (Database Schema, 2022; Foote, 2022; IEEE Xplore, 2022; Quickbase, 2022). In response, DBMS solutions have evolved and become more sophisticated, distributed, interoperable, and capable of handling and analyzing specialized voluminous data. The following section provides a brief overview of the significant milestones and developments associated with the evolution and growth of the DBMS industry.

The 1960s–1970s

The traditional method of data storage, such as punch cards, was coming to an end as companies realized that devices such as laser discs and magnetic tapes were expensive. Data processing and extraction were time-consuming, leading to a need among companies for databases to maintain bills of materials in an organized way. This growing need fueled the conceptualization of hierarchical and relational database structures. IBM, GE, Burroughs Corp, and Honeywell Inc. were some of the initial database developers. The initial buyers of the databases included NASA (bought IMS database from IBM for the Apollo Program), Weyerhaeuser Lumber (bought IDS database from GE for data-keeping), and British Telecom. The capability of the early databases was further accentuated by the hardware manufactured by the developer company. The consortium “CODASYL” was established, which developed the language COBOL, leading to the foundation of the modern database system. One of the essential attributes of these databases was platform-agnostic, which increased their user base since non-agnostic databases often failed to attract a high volume of customers as they were not suited to be used in different types of hardware.

The 1970s–1980s

During this phase, the database users wanted ease of doing business features, for example, fast search and data extraction capabilities, to be added on top of mere data storage. This growing need among customers spawned the concept of tables to store particular types of entries. Handling a large amount of data in a format that can be retrieved or manipulated faster based on specific criteria slowly started gaining importance. New entrants into the market included research institutes such as the universities of California, Berkeley, and Michigan. Westinghouse Electric Corporation and Raytheon Company also entered the market. Due to the large volume of data they needed to handle, database usage started gaining prominence among government institutes and departments, for example, the US Department of Labor and the US Environment Protection Agency. Following this widespread acceptance, research on the development of database technology received attention from strategic institutes such as the Airforce Office of Scientific Research and Navy Electronics Command (Fry and Sibley, 1976).

The 1980s–1990s

The SQL database became a commercial success during this period. The SQL database not only allowed its users to update and recall records but also to write and execute customized queries that could simultaneously access, extract, and manipulate data across tables. IBM remained a technology leader in the database industry with many patents. IBM also released one of its major flagship products—the DB2 database—during this period. The introduction and popularity of the IBM PC further encouraged the growth of new database companies and products. Bell Labs developed the “Dali” high-performance database engine during this phase, which DataBlitz commercialized. “Dali” allowed real-time data entry and thus could support high-performance applications. As open standards and RDMS technology gained popularity, several new competitors with comparable offerings emerged (Grad and Bergin, 2009).

The 1990s–2000s

The advent of MySQL revolutionized the database market during this period. MySQL was the first open-source software product to target the online market. It directly contrasted the existing products on which the parent companies had high control over changing and maintaining the source code. The positive network effect was exploited with the open-source license given to web developers with the freedom to enhance and modify the source code to improve the database functionalities. MySQL quickly became popular with online platforms such as YouTube, Google, Facebook, and eBay. The traditional reseller model of business evolved with parent companies forming partner long-term close relationships to increase their penetration and distribution. Dell, HP, and Novell became the first resellers distributing MySQL Enterprise (Grad and Begin, 2009).

MySQL AB, together with Linux (a free and open-source operating system), Apache (a free and open-source cross-platform web server software), and PHP (an open-source scripting language), formed the building blocks of LAMP Technology, an archetype model of a web service stack for delivering high-performance web applications. As a result, a two-sided platform with a positive network effect was enjoyed by MySQL, as 5 million installations and 10 million product downloads were recorded in the early 2000s. Sybase (later a subsidiary of SAP) was the first company to complement its RDMS databases with the provision to establish client–server communication. Microsoft entered the market by combining its DBMS with the relational database engine and graphical user interface with multiple software development tools. The development of open-source and online managed databases targeting the vastly growing e-commerce and social media markets were the other significant changes of this era.

The 2000s–2010s

The usage of databases by most sectors matured during this period. Almost all major FMCG, finance, trading, IT, and service firms started using databases. Whereas SQL databases were table-based and relied on a relational model, the next-generation post-relational databases became known as NoSQL databases involving documents and graphs. A new form of SQL aimed at online transactions also started to emerge. Microsoft, IBM, and Oracle emerged as leaders in this highly competitive database market. The IT recession during this time led to a decline in the database industry, leading to restructuring and reconfiguration in the industry. Sun Microsystems acquired MySQL AB (Grad and Bergin, 2009).

2010–Present

The competitive intensity in the DBMS market continued growing. By 2017, the incumbents had already expanded their customer base, and the switching cost was high in the database industry. Incumbents started acquiring niche and new firms to increase their product portfolio or achieve technology synergy. Oracle acquired Sun Microsystems during this period, thereby obtaining the license for MySQL. Firms' offerings shifted from a single product to a platform of complementary products such as Online Transaction Processing (OLTP) and specialized applications such as Client Application Tool, Personal Application Development environment, Real-Time data entry and processing capability, Online/Internet database connectors with OLTP capabilities, and Analytics and faster processing features (Oracle Corporation, 2022).

Cost, interoperability, and performance became the three primary DBMS evaluation parameters. Robust after-market technical offerings, license renewals, training, and superior support proved to be an emerging need for customers. Committed partners, resellers, distributors, and consultants helped intensify the network effect. Most organizations preferred to continue with their legacy DBMSs and did not switch to newer DBMSs to avoid significant capital expenditures and productivity losses during the transition. This is why interoperability and performance in terms of processing speed and application-specific capabilities become crucial (Quickbase, 2022).

Traditional ERP platforms moved into the DBMS space for the scope of synergy. SAP is a widely used ERP among all organizations. Having a high-performance SAP ERP-specific database enhances the capabilities of the ERP. This customer value proposition innovation (Kim and Mauborgne, 2005), to serve databases as complementary to the traditional product, was new to the DBMS market. The bundling of service with a product and an interface with other related applications helped users in computing/reporting or visualizing the data. Interconnectivity between other platforms enabled users to have “one source of truth,” thus helping them make better decisions. A new “cloud” or “hybrid” business model emerged that provided the option of paying per your usage by positioning offerings as a Software as a service (SAAS) or Platform as a service (PAAS) (Zott and Amit, 2010). These pay per use models, by backloading the huge upfront procurement cost, allowed the DBMS firms to target smaller firms. The new business model also generated the network effect among all stakeholders, which enhanced the capabilities of the ERP, provided high-performance in-memory processing speed for the ERP, and thus enhanced performance (SAP investor relations, 2022). Interoperability permitting data consolidation from multiple sources (different DBMSs) is also gaining prominence, as MNCs often use different databases in different regions. Data from all the DBMSs need to be pulled together to make an informed decision. SAP’s Central Finance model is developing methods to accomplish this (Vertica User Group Community, 2022). Over time, the DBMS companies that thrived provide not a single isolated database but a platform of services that are easy to use by even non-experienced users. The visionary firms have realized this paradigm shift from databases as products to databases as a platform through their R&D, technical, and marketing competencies.

SAP: Evolution in its offerings and business model

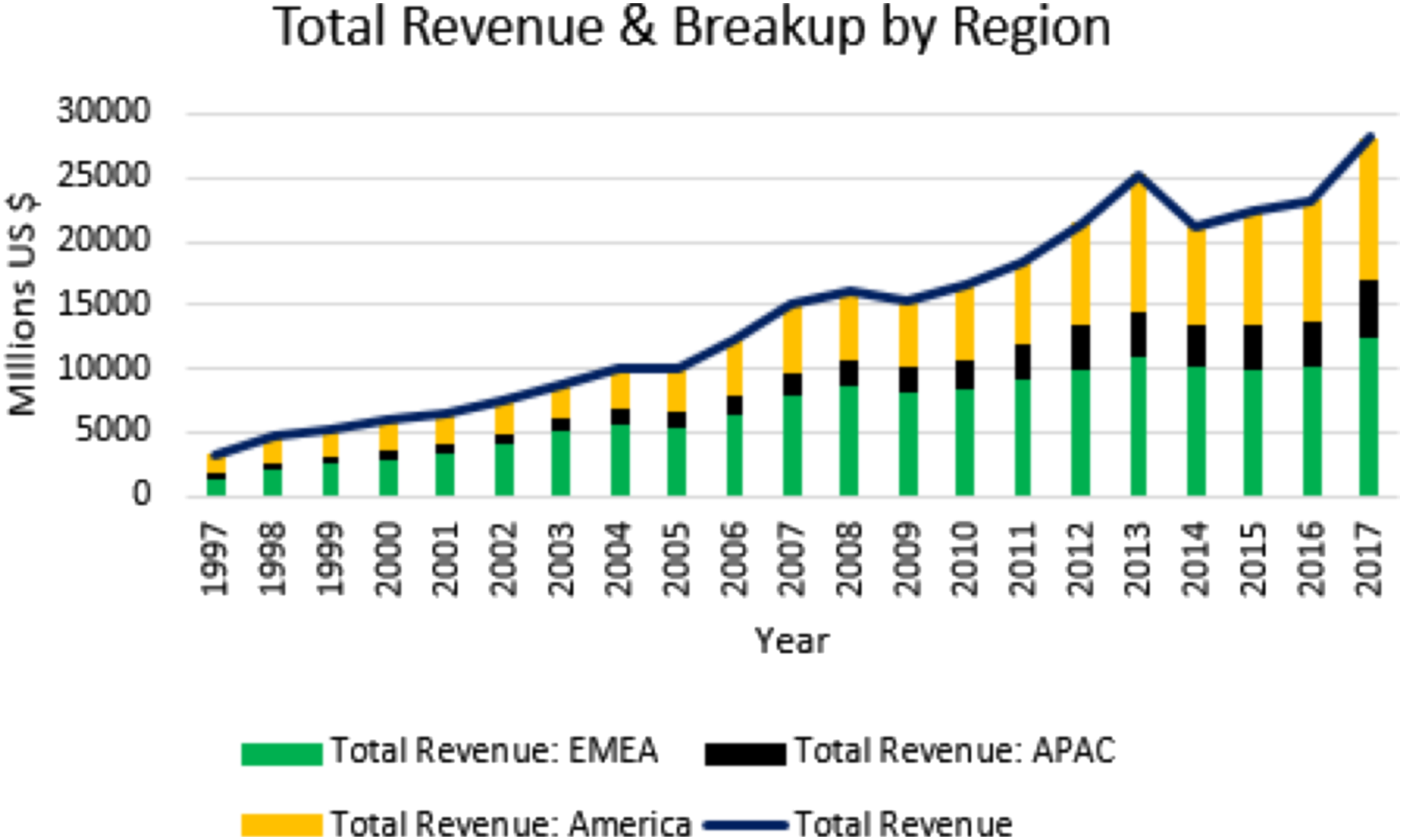

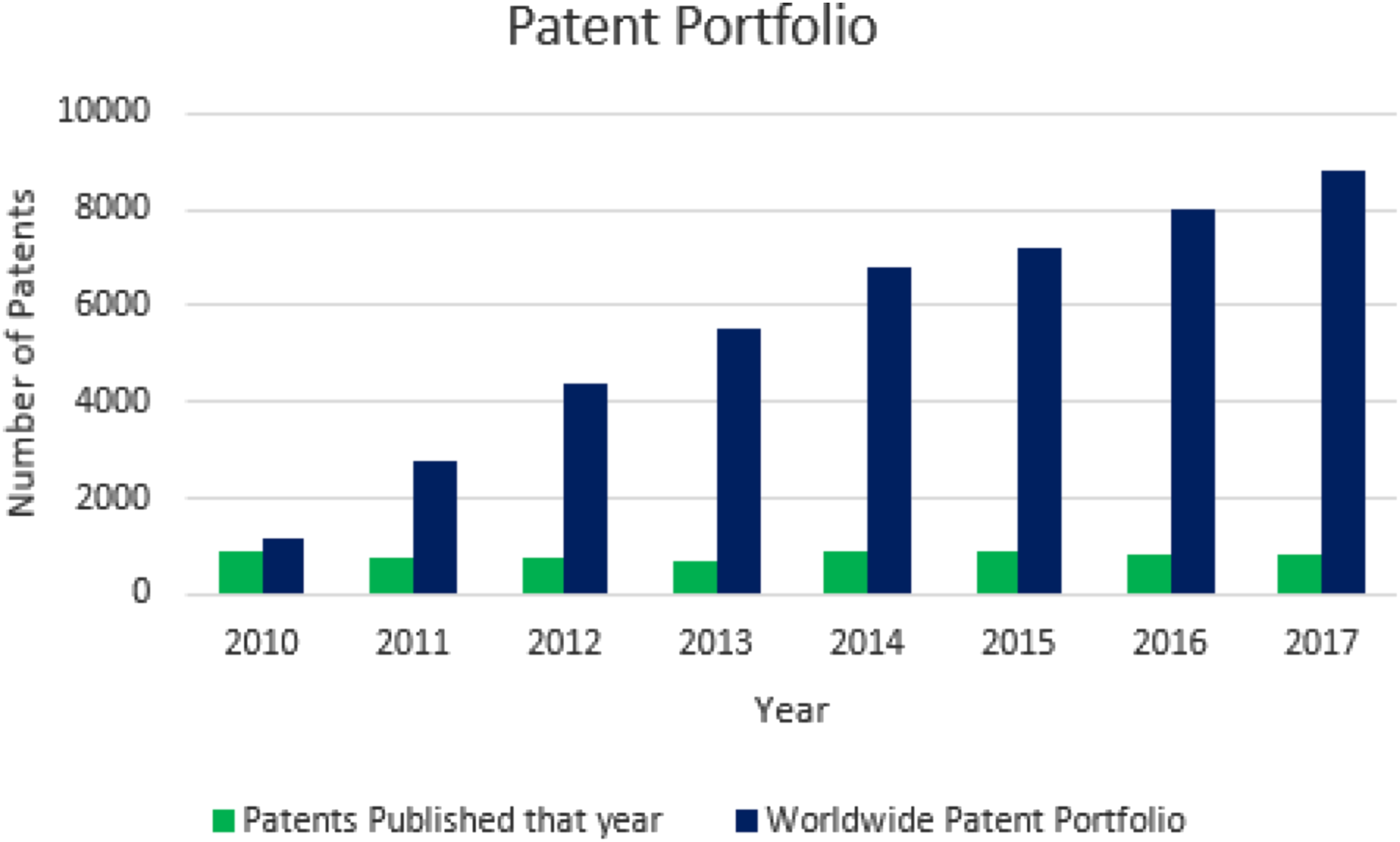

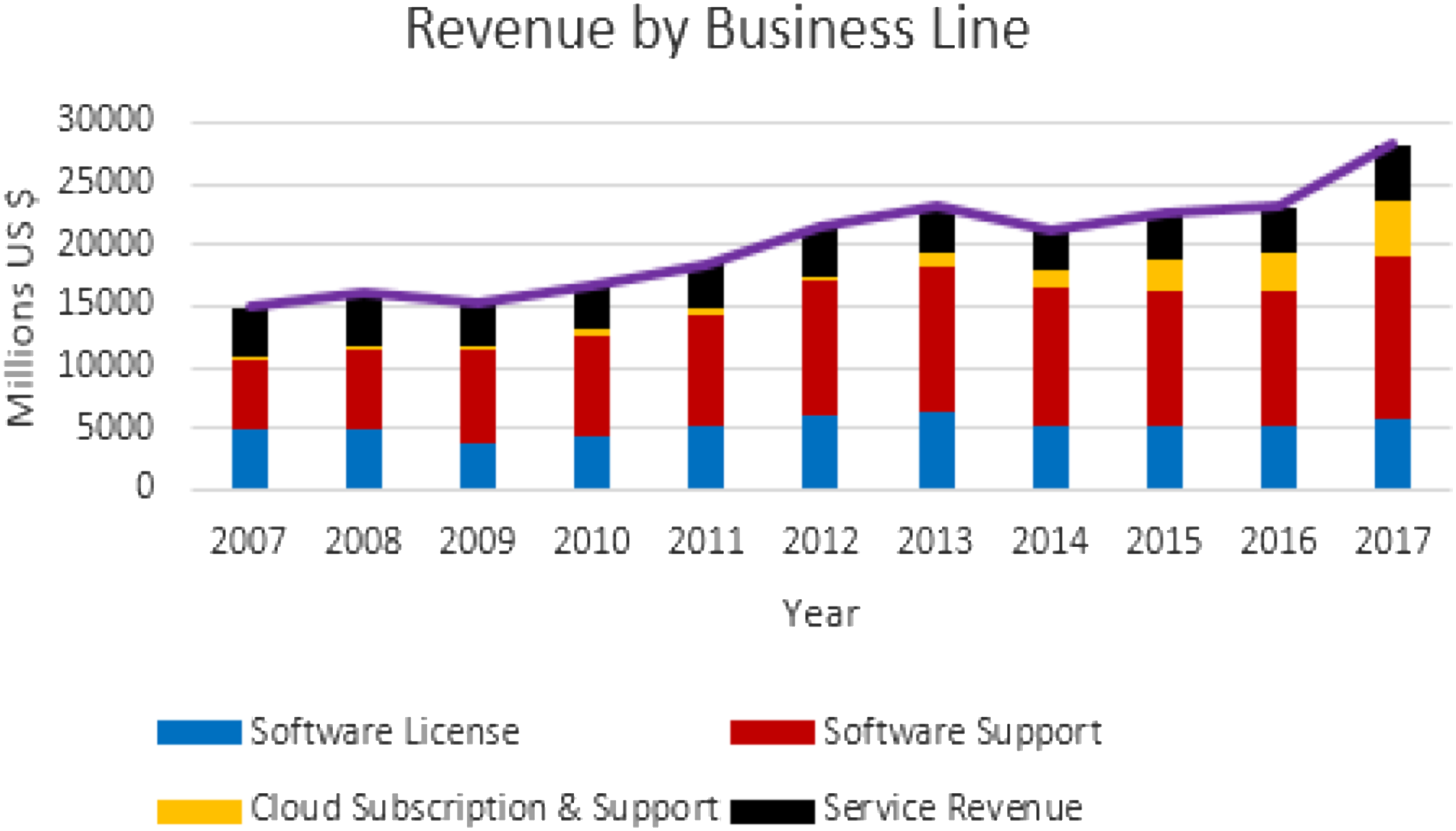

“Systems, Applications and Products in Data Processing” (SAP), a German-based software MNC, was established in 1972 by Dietmar Hopp, Hans-Werner Hector, Hasso Plattner, Klaus Tschira, and Claus Wellenreuther. SAP designs enterprise software to manage businesses, especially their operations and customer relations. The SAP customer base has increased consistently over time (see Figure 1), and it has a presence in more than 180 countries (see Figure 2). It is included as a part of the Euro Stoxx 50 stock market index (SAP investor relations, 2022). SAP SE’s first commercial product was SAP R/98, which focused on central data storage and improving the maintenance/handling of data. SAP pioneered real-time computing over software that traditionally updates data overnight in batches. The first customers of SAP were chemical and tobacco industries using SAP ERP for accounting systems or payroll. Within 3–4 years of commercializing the first product, SAP developed and released additional purchasing, inventory, management, and invoice verification modules. SAP product innovativeness is an outcome of its R&D intensiveness. Its patent portfolio is summarized in Figure 3, and its expanding product portfolio is summarized in Figure 4. Customer Growth of SAP. Total Revenue of SAP regions. Patent portfolio held by SAP. Total Revenue of SAP products.

1999–2009

SAP launched R/2 and R/3 systems during the period. The R/3 system was introduced for a client-server distributed architecture. The R/2 and R/3 systems formed the “integrated enterprise-wide business solutions” for the mainframe data processing. The main product lines for SAP during the late 1990s were industry-specific solutions, custom components and tech infrastructure, and consulting and support services. With the advent of e-commerce and a high volume of transactions online, SAP introduced products that included independent business applications for better support of supply chain management (SCM), customer relationship management (CRM), business intelligence, and electronic commerce. In 1999, SAP developed mySAP.com, the company’s internet portal including the features mentioned below: mySAP Marketplace: a business hub on the internet to provide an open infrastructure for collaborative business; mySAP Workplace: a platform to integrate the employees, customers, suppliers, and partners of a company.

Since its beginning, SAP has focused on a customer-centric approach and has quickly understood customer needs and delivered appropriate solutions. Therefore, every year, SAP offers multiple product enhancements. In 2006, SAP announced its software upgrade release strategy, including optional enhancements until 2010. This strategic move by SAP aimed to send a message to the users that SAP offers a stable and durable platform. The objective was to incentivize the customers to migrate to the latest technology releases by giving them the roadmap of upcoming releases. In 2002, mySAP.com was renamed mySAP Business Suite and several features that enable companies to manage their business value chain across their network were added, repositioning it as an integration platform (Quickbase, 2022). Within a year, SAP Business Design feature pack 1.2 was released to optimize quality, performance, and system stability (SAP investor relations, 2022). After 2003, product consolidation began by condensing the firm-wide resource planning solution in mySAP ERP, the successor of R/3.

2010 Onwards

By early 2010, a combination of SAP and Sybase solutions was released to offer clients a comprehensive and streamlined elite business analytics framework. Organizations could relocate to wireless communication in which critical data could be accessed at any time. The SAP HANA platform was created, involving the SAP HANA database and different parts that empower consistent real-time analytics on enormous amounts of detailed information. Gradually, the cloud solution of every module, including Cloud Suite, was transformed to SAP Business Suite powered by SAP HANA in the cloud. The Open HANA cloud platform was developed. SAP Simple Finance was also launched to address flexibility needs in the most complex finance processes. SAP Simple Finance was later developed into a very successful SAP offering called SAP S/4 HANA. By 2015, significant developments occurred in SAP offerings as they moved from the realm of a product to a platform company offering products with multiple functionalities for diverse stakeholders. The following paragraphs briefly discuss the most prominent SAP platform offerings that revolutionized SAP’s core ERP business.

SAP Ariba

SAP acquired Ariba in 2012 to bring innovative solutions, analytics, and process skills to a distributed cloud-computing portfolio. Ariba was expected to bring all the trading partners to a similar platform from any web empowered PC or mobile phone to buy, sell, and manage their money gainfully and effectively. Through this, SAP hoped to deliver complete, end-to-end cloud procurement management.

SAP HANA (SAP High-Performance Analytic Appliance)

SAP HANA is a flexible, data-agnostic, in-memory product that adds SAP software components to the hardware provided by SAP partners. With SAP HANA, companies can, in a flash, break down their business activities, utilizing gigantic volumes of data from practically any information source. SAP offerings empower clients to organize information and business forms for overall operating scenarios. SAP HANA also provided a foundation for software programmers to develop new and innovative applications (SAP HANA, 2022). The world-leading innovation businesses, including Dell, Cisco, EMC, Fujitsu, HP, Hitachi, Huawei, IBM, and NEC, have ensured that their solutions are aligned with SAP HANA. By 2013–14, HANA became the leading anchor of SAP’s futuristic strategy for customers: “simplify everything so that they can do anything” (SAP investor relations, 2022).

SAP HANA Cloud

SAP S/4HANA Cloud was created in a heterogenous database frameworks landscape with native integration extending beyond existing SAP applications to open interfaces for additional integration and expansions utilizing the SAP Cloud Platform and fast computing speed of in-memory processing (SAP investor relations, 2022). SAP S/4HANA works with an open architecture that can work with the SAP product portfolio and other 3rd-party applications. The new SAP S/4HANA Cloud software development kit (SDK) permits on-premise clients, cloud clients, and partners to rapidly foster innovative solutions on the SAP Cloud Platform while using the solutions of their digital core and in-memory processing (SAP investor relations, 2022).

At SAP S/4HANA Cloud core is a platform-as-a-service model planned to support clients, independent software vendors (ISVs), and partner providers to rapidly, efficiently, and effectively use case-based programming applications to expand businesses' versatility and increase cooperation across business services (Hana definitions, 2022). In 2016, SAP S/4 HANA brought a strong revenue channel to the SAP digital business service domain. The top innovations in SAP digital business service to help customers undertake a digital transformation are SAP Value Assurance covering every possible project stage and scenario to assist users in migrating from SAP ERP landscape to SAP S/4 HANA. HANA has the newest generation of SAP Solution Manager & SAP Model Company, next-gen technological support, and SAP Digital extending the possibilities of SAP Store and messaging services (Berg et al., 2012).

The nemesis: Oracle

Oracle entered the database market back in 1977. After its launch, Oracle became one of the most preferred ERP solutions for businesses from various domains. The company released the first-ever commercial SQL relational database management system. The company released almost eight versions of the software by 1999. Throughout the 1980s, Oracle introduced newer technologies, such as databases rewritten in C, for better portability and improved read consistency. Oracle was also the first to release its services as a client–server model. Oracle released Oracle applications 2, a suite of ERP applications, in 1998. They also announced that they would integrate a Java virtual machine with an Oracle database. They were the first ERP service provider to announce an internet strategy and released Oracle 8i in September 1998, where “I” stood for the internet. Over time, its product portfolio included software technology, cloud solutions, ERP, CRM, and SCM platforms. Revenue-wise, it is consistently among the top three database industry leaders globally. It has a wide range of patents that the R&D team has developed over the years, which helped them deliver the right products to the customers at the right time. Its primary customers are Walmart, Costco, Amazon, Google, etc. (Kolonko, 2018).

Oracle has a single solution for all organizations, SMEs or MNCs. Oracle is less customized for clients, as its functionality is more or less good enough for any organization, making the software less flexible to use. Oracle also used cloud functionalities with Oracle cloud ERP, which is based on Oracle Fusion Applications as a suite of applications. The product is an end-to-end SaaS suite to manage enterprise operations with private and public cloud implementations and hybrid deployment options. The company provides a minimum of two updates to the software annually. The accounting, financials, procurement, risk management, project management, Enterprise Performance Management (EPM), AI ERP, SCM, and NetSuite modules are part of the Oracle cloud ERP solution. The company’s financial modules are considered top-of-the-line and the best solutions for ERP. Reports suggest that Oracle is cheaper, as on average, companies spend 1.7–2% of revenue on the software, and its implementation takes approximately 22 months compared to SAP, which is on the pricier side, with 4% of annual revenue going towards the software vendor and only 4 months for implementation. Since 2017, Oracle has deliberately attempted to unseat SAP as the ERP industry leader and reduce the market share gap with SAP. Furthermore, it has outperformed SAP in several customer satisfaction surveys (O'Shaughnessy, 2022). Only time will tell whether winning customer perception surveys allow Oracle to unseat SAP from the leadership position or whether SAP acts to protect its leadership position.

Concluding remarks

The case documents how the DBMS industry has evolved over the last five decades. During this period, the industry’s critical success factors (Leidecker and Bruno, 1984) changed, driven by the underlying structural forces in the industry. The case also chronicles the evolution of SAP—market leader in the ERP segment—customer value proposition and business model. The case also describes how Oracle challenges SAP’s leadership in integration and R&D capabilities, implementation costs, etc. What should SAP do to maintain its leadership position and reclaim the top position in customer perception surveys?

Assignment/Case Discussion Questions

Q1) How has the structural attractiveness of the DBMS industry changed over time? Q2a) Based on the changing industry structural forces, how have the critical success factors evolved in the DBMS industry. Q2b) What changes can be noted in SAP’s and Oracle’s competencies over time? Q3) As SAP moved from a pipeline to a platform company, how did its customer value proposition and business model (canvas) change? Q4) Critically evaluate SAP and Oracle’s business model changes using the NICE framework? Q5) What should SAP do?

Supplemental Material

Supplemental Material - Platform Revolution in the Database Management System Industry: Evolution of SAP’s Business Model

Supplemental Material for Platform Revolution in the Database Management System Industry: Evolution of SAP’s Business Model by Krishna Chandra Balodi, Rajesh Jain, T B Kiran Kumar and Debarati Banerjee in Journal of Information Technology Teaching Cases

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Disclaimer

Like other cases written solely based on secondary sources, this one also has standard disclaimers such as, the case cannot be used as a source of information on the company. The information/facts/statements/mentioned in the case has been taken from secondary sources and is not endorsed by the company, its founders, partners, and other stakeholders. The case is not intended to serve as an endorsement of (in)effective handling of situation(s). Authors acknowledge that the brand names and trademarks used/mentioned in the cases are owned by respective title holders. All errors are the responsibility of the authors. Upon being notified, the authors will undertake all reasonable efforts to rectify the errors.

Supplemental Material

Supplemental material for this article is available online.

Note

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.