Abstract

Bangladesh has seen significant strides in technological developments that have positively affected its GDP. Different modes of financial transactions, such as mobile banking, and credit and debit cards, have proven beneficial for the economy. bKash, Nagad, and other online transaction platforms are widely used by the population of Bangladesh. People, starting from Dhaka to many other rural areas of Bangladesh, are gradually becoming habituated to the digital mode of payment. The case thoroughly analyzed and highlighted the concept of a cashless society and showed how technological advancements in financial services can contribute to broader sustainability goals, including carbon-reduction. Moreover, the case presented three different scenarios on Bangladesh’s devotion towards going cashless. Additionally, the case utilized the diffusion of innovation (DOI) theory, to identify the different categories of innovation adopters, and elucidated their traits in the context of adopting a cashless economy.

Keywords

Introduction

The rise in global temperatures has caused significant challenges for people all across the world and Bangladesh is no exception. The country faces a serious and growing threat from climate change. Four heat alerts have been issued throughout the nation 3 weeks in a row, seriously endangering public health and disturbing lives all over the nation (The Daily Star, 2024a). Furthermore, according to certain figures, climate change will cause Bangladesh’s crop and wheat production to drop by 30 % and 32% in 2100, respectively, posing severe economic damage (Biswas, 2013). It is therefore imperative that Bangladesh take swift and effective actions to lessen the effects of climate change.

Notably, climate change directly affects Bangladesh’s financial environment in addition to posing a serious threat to human health. Bangladesh’s financial institutions need to assess their financial risks more carefully, considering that the country is ranked seventh among those most vulnerable to climate change. Financial institutions are impacted by climate change through both transitional and physical hazards. Bangladesh is especially vulnerable to climate-related calamities throughout a wide portion of the country. As a result, banks and other financial organizations’ assets are at danger when they own property in these weak spots. Global climate initiatives including the Paris Agreement will gradually phase out high-emitting industries and technology. About five hundred of the countries that signed the Paris Agreement have turned in their Nationally Determined Contributions (NDCs), which set goals for cutting greenhouse gas emissions. Thus, companies that rely heavily on fossil fuels should soon be replaced by green and clean industries. The assets of the banks may be impacted if financial institutions fail to take into account the consequences of these climate regulations, market dynamics, and green technological advancements at the portfolio level. As a result, Bangladesh Bank has sent rules for financial disclosure related to sustainability and climate change to all banks and non-bank financial institutions (NBFI) in Bangladesh. Specifically, financial institutions that use the cashless ecosystem for transactions can reduce risks and encourage more environmentally friendly money circulation (Tuhin, 2024).

According to research conducted by the European Financial Authority, using euro banknotes annually has an environmental impact equal to driving 8 km in a car, or 0.01% of a person’s entire carbon consumption. The energy usage of automated teller machines (ATMs) and shipping are the primary sources of the environmental impact of using euro banknotes as a form of payment. These are followed by NCB processing, paper production, and banknote authentication at retail establishments. Hence, the adoption of the cashless or digital financial ecosystem can aid in alleviating climate change and creating a convenient platform for transactions. Interestingly, the inception and rapid growth of mobile financial services (MFS), Bangla QR code, digital banking, and online banking in Bangladesh, exemplifies the country’s devotion to going completely cashless. The purpose of this case study is to highlight some noteworthy initiatives from multiple organizations that are not only strengthening the nation’s economy but also assisting it in becoming a cashless society.

Methodology

This paper is primarily based on secondary information. Three cases of going cashless are collected from The Daily Star—a national newspaper of the country. Secondary data analysis is a process in which data from one study are utilized to address new research questions or apply new statistical methods (Coyer and Gallo, 2005). Secondary data, such as journal publications, conference papers, and newspaper reports, were utilized in this research.

Cashless economy paving the path for a greener future

A cashless society is a term used to describe a scenario in which physical cash transactions, such as paper money and coins, are entirely replaced by digital and electronic forms of payment (Duignan, n.d). In a cashless society, people depend on various electronic methods to conduct cash transactions, including credit cards, debit cards, mobile payment apps, digital wallets, online banking, and other forms of digital currency. Characteristics of a cashless society are described below: • • • • • • •

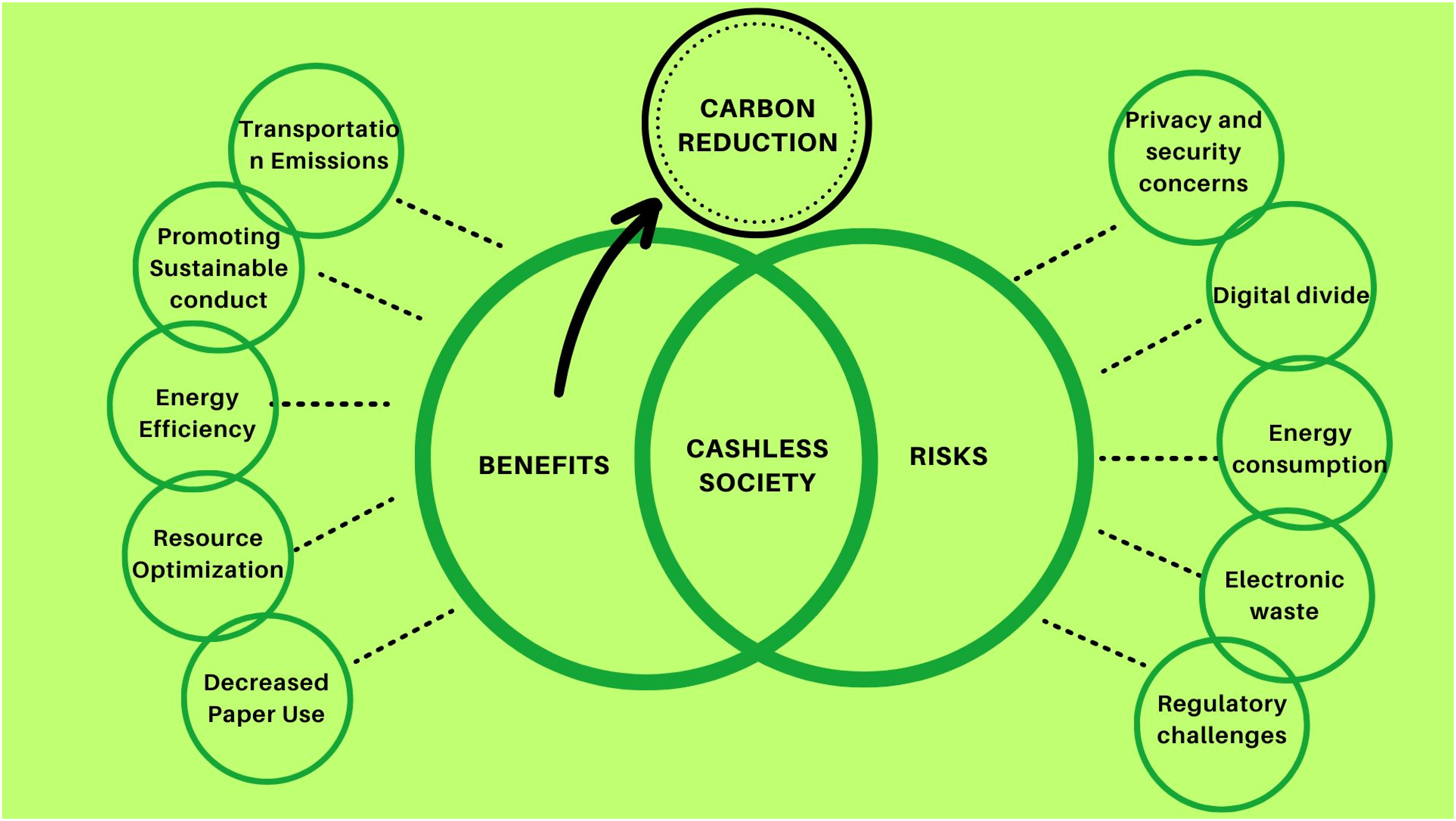

Adopting a cashless society might help cut down on carbon emissions by decreasing the amount of paper used, enhancing energy efficiency, lowering emissions from transportation, allocating resources as efficiently as possible, and promoting sustainable behavior. The benefits of adopting a cashless society are explained below: • • • • •

Even though a cashless ecosystem provides enormous benefits to a large population and the economy as a whole, it is prone to some financial and regulatory challenges and environmental risks. The risks related to the adoption of a cashless society are discussed in the later part of this section: • • • • •

It’s crucial to remember that several variables, such as the energy sources utilized for digital infrastructure and the effectiveness of payment systems, affect how cashless systems affect the environment. Thus, it’s essential to make sure that cashless systems are developed and put into use with sustainability in mind to maximize their potential benefits of carbon-reduction Figures 1 and 2. Benefits and risks of cashless society. Source: Compiled by Authors. Percentage of the different categories of adopters according to DOI. Source: (LaMorte, 2022).

The figure below depicts the benefits and risks of adopting a cashless society

Selected cases of cashless adoption in Bangladesh

The COVID-19 epidemic has somehow triggered a shift in payment methods from contact to contactless (Zahari et al., 2021). People started using cashless payment methods to prevent the virus from spreading, which turned out to be a practical and effective method of payment in the end. A few examples of Bangladesh in adopting cashless payment systems are discussed in the later part of this section.

Mobile financial services and online banking

The adoption of Internet Banking by numerous commercial banks, the development of quick response or QR code-based universal payment systems by Bangladesh Bank, the facilitation of secure e-commerce transactions by Payment Gateway companies, and other factors have all contributed to the rapid growth of cashless transactions in Bangladesh in recent years. The nation has demonstrated its commitment to adopting digital financial services by making significant progress toward becoming a cashless economy. The nation saw a paradigm shift in which people began to favor digital transactions over frequent cash transactions. Bangladesh has been moving closer to being a cashless society thanks in large part to bKash. By providing safe, user-friendly MFS, bKash has made finance more accessible to millions of Bangladeshis, enabling them to take part in the digital economy. Establishing and fostering an inclusive ecology is essential to its continued progress. By introducing cutting-edge solutions like the ability to make payments from Visa cards through the bKash app and the ability for merchants to receive voice notifications in addition to payments, bKash is attempting to revolutionize the experience of both making and receiving payments for both customers and merchants. In addition, Dhaka Bank PLC invented a digital account opening platform that enables users to establish accounts promptly from the comfort of their homes via the ezyBank mobile app or the Account from Home website during the early difficulties caused by the COVID-19 epidemic. Bank employees sent the required supplements—such as checkbooks, PINs, and debit cards—to clients’ addresses while maintaining the most stringent standards of security. Additionally, MTB aggressively promoted the introduction of cashless transactions and has long favored them—even before the outbreak. Through its collaborations with more than 30 fintech companies, MTB is able to provide lending facilities and fast bank account openings via a variety of applications. Notably, in December 2019, MTB was the first to introduce the Bangla QR code, a move that has empowered more than 80,000 micro-merchants. Furthermore, we have enabled the implementation of two thousand Personal Retail Account (PRA) programs, which are a Bangladesh Bank effort targeted at small and medium-sized enterprises (SMEs) and enable users to open accounts using just their National Identity (NID) cards. In order to make significant progress toward a cashless economy, integrated cooperation, ecosystem development, legislative backing, and digital literacy are all necessary strategic initiatives. In addition to providing incentives for cashless transactions, it is necessary to cultivate an atmosphere that supports technical innovation. Government, banking, and fintech companies such as bKash must work together to develop comprehensive plans that remove obstacles to their widespread acceptance and financial inclusion. (The Daily Star, 2024b).

Going cashless in fine dine

As the world moves toward cashless transactions, hotels, and restaurants are collaborating with banks to create elaborate menus that will wow their patrons due to the increased confidence in digital payments. The most popular offerings for sehri and iftar in recent years have been alluring promotions like Buy One Get One (B1G1), cashback, and discounts for using credit and debit cards simultaneously. Currently, certain credit cardholders and premium debit cardholders are eligible for B1G1 offers and discounts. Prestigious hotels and restaurants have access to a list of these bank partners. This year, for example, Eastern Bank Limited (EBL) worked exclusively with Le Meridien and Amari Dhaka to provide a B1G2 deal, further improving their customers’ dining experience by utilizing EBL’s Visa Platinum, Signature, and Infinite credit cards. Furthermore, about 47 well-known hotels have teamed up with EBL to provide B1G1 deals. Cashless transactions—particularly those made possible by credit or debit cards—allow customers to take advantage of these deals and maybe save money or earn points from their purchases. Food delivery services are offering amazing discounts and deals throughout Ramadan in collaboration with banks and non-bank financial organizations. For instance, customers can use Rocket or the DBBL Nexus Debit & Credit Card to pay for any Pathao service, including meals, as often as they can to enter a drawing to win a DHK-COX-DHK Couple Air ticket that includes a complimentary one-night stay (Afrin, 2024a).

Digital donation

In Islam, zakat is very important since it is a tool for increasing wealth as well as a method of purifying it. However, implementing a new cashless transaction method for Zakat can result in a major reduction in time and energy costs. To further optimize the impact of gifts, a multitude of committed Islamic and other social humanitarian groups might guarantee that Zakat money is disbursed to the eligible part of the needy people. With Nagad’s Islamic MFS Account, customers may donate to Islamic charities that work to better mankind for philanthropic reasons, such as Zakat. With a specialized Zakat calculator, users may easily compute their Zakat. Users may determine the precise amount by giving details such as annual income, investments, gold, debts, and assets.

Users of bKash may also help 28 prestigious organizations that have been around for a long time and are known for their substantial charitable initiatives. This helps to build trust. Donors have the freedom to reveal their identities or keep their identities private as they see fit. Contributors may easily and comfortably make donations with the bKash app's easy-to-access donation feature. Currently, 28 charitable organizations like Bangladesh Thalassemia Foundation, JAAGO Foundation, Shakti Foundation, icddr,b, Dhaka Ahsania Mission, BRAC, etc., can easily receive Zakat and Fitra, as well as assistance for food, education, and medical treatment for orphans, destitute, day laborers, and extremely poor, from bKash customers throughout the year. Although many people are still getting used to offering cashless Zakat, usage is increasing gradually, suggesting bright future possibilities (Paul, 2024).

Diffusion of innovation (DOI) Theory

Diffusion of Innovation (DOI) Theory, developed by E.M. Rogers in 1962, is one of the oldest social science theories. The theory elucidates how a particular concept or product diffuses (Spreads) over time, and creates a broader impact on a specific population or target group. People embrace novel concepts that spread to a broad population after the advantages are apparent since they are a part of the social structure. Adoption of a new concept, way of behaving, or item (i.e., “innovation”), however, occurs in a social system in stages, with certain individuals being more likely than others to accept the innovation. It has been discovered by researchers that early adopters of innovations exhibit distinct traits from later adopters. Diverse tactics are employed to appeal to different adopter types while promoting an invention. (LaMorte, 2022).

The figure below depicts the percentage of different categories of adopters according to DOI

The five categories of adopters of innovation are explained below:

Innovators—Individuals who actively seek to obtain an invention or service are known as innovators. They take risks, are price-insensitive, and are capable of managing a great deal of uncertainty. Sweden, for instance, was the first country to implement a cashless economy. The tech-savvy populace of Sweden embraced the unique features of this innovative concept (Arvidsson, 2019)

Early Adopters—Compared to innovators, early adopters are less willing to take risks and usually hold off on purchasing until the product or service has garnered some evaluation. For instance, in Bangladesh, young individuals who were interested in technology were more likely to derive benefits from cashless transactions.

Early Majority—The early majority barely take chances and usually hold off on purchasing until a reliable peer has utilized or tested the good or service. These prudent individuals only want to buy items that have been shown to function. Middle-class customers, for instance, are categorized as belonging to this category when it comes to implementing a cashless economy since they put a product’s or concept’s practicality and dependability before embracing it.

Late Majority—The final large consumer group to join the market is known as the late majority. They are considered conservative and frequently have discomfort with technology, are extremely cost-conscious, doubtful, and careful while making purchases. When it came to embracing cashless transactions or other digital financial services, the elderly or those with little digital literacy were the segments that were the last to adopt. More digital literacy programs and attractive offers on cashless payment options might be made to draw in this demographic.

Laggards—They are the last to adopt any innovation and keep using conventional goods and services until they are no longer offered. This group is often resistant to change and are comfortable with the traditional methods. In the context of transitioning to a cashless system, those who exclusively rely on physical currency and traditional financial services could be seen as trailing behind. For instance, many retailers in Bangladesh remain unfamiliar with mobile financial services (MFS) technology and continue to prioritize cash transactions over electronic payments (Saolin, 2024).

Potential challenges of adopting cashless ecosystem

It is incredible to consider the possibilities of conducting all financial transactions digitally, but before delving further into the subject, it’s important to define cashless transactions. Going cashless entails replacing actual paper money with electronic money obtained through electronic payment systems. Bangladesh’s central bank takes the lead in implementing “Bangla QR,” a Quick Response (QR) Code-based technology, to eliminate cash by the year 2023. With the popularity of Mobile Financing Systems (MFS) like Rocket, Nagad, and bKash, it seemed like a good idea to establish a more centralized system for conducting digital transactions. Integrating all banks and MFS under one gateway, Bangla QR seeks to provide a simple payment option for all kinds of sellers. Bangladesh Bank’s approach is intriguing since it emphasizes street sellers and makes use of a fee-free program. This would allow it to be used by small-scale vendors like rickshaw pullers and hawkers without causing them to lose any money. Bangladesh Bank wants to go cashless by 2027, which sounds like a quick turnaround given that the majority of the nation still uses cash for most transactions. However, given the poor economic situation, the practicality of the goal is questionable.

The problems with adopting a cashless system are by no means restricted. First off, back in 2016, a significant cyberattack targeted the “Bangla QR” implementers themselves, resulting in the theft of $81 million in money from their digital vaults. Moreover, the case of “Forever 21” in the USA is one example of this. The well-known apparel company experienced a security system breach in December 2017 as a result of some cunning hacking and personnel mistakes. As a result, several of their locations were unable to accept online payments for 7 months. If large companies experience negative effects from cyber-attacks for almost 6 months, the poor condition of the small vendors in Bangladesh can be estimated. Hence, the government must also take effective measures against any financial theft or cyber-attacks (Rhid, 2023).

The study “The Phenomenon of Trade-Based Money Laundering in Bangladesh: A Critical Review” indicates that using reputable companies as a front for money laundering is common in this nation’s shadow economy. These companies make their illicit funds appear legitimate by invoicing too much or too little as a means of money laundering into and out of the nation. Therefore, a company’s refusal to accept digital payments or its strong discouragement of them should be viewed as suspicious in and of themselves. (Morshed and Rahman, 2021). Though immensely attractive, the concept of an economy in which all transactions are documented and fraud is rarely heard of is extremely unrealistic. However, limiting the terrible activities of criminals through digital platforms can be a positive approach.

Moreover, Bangladesh lags behind its peers in internet usage which poses a significant hindrance to the adoption of the digital financial ecosystem. According to the report of the World Bank, the average internet usage among lower middle-income countries and South Asian countries is 56% and 42% respectively. However, the percentage of internet usage in Bangladesh stands at 39%, which is significantly lower than the countries with similar economies (Afrin, 2024b). Additionally, due to outdated connection mechanisms and subpar internet connections, businesses in certain low- and middle-income nations that have access to computers and the internet are limited in their ability to pursue a more comprehensive digital transformation. Users employing dial-up internet, which has been discontinued in the majority of countries, have to connect their phone line to a computer. Furthermore, it is estimated that internet access in Bangladesh drops seven times a month on average. It is challenging to maintain business resilience and compete with other firms in the global digital economy while there are regular interruptions like this (World Bank, 2024). As a result, to completely adopt a cashless ecosystem, Bangladesh must prioritize facilitating the population’s use of smartphones and the internet, enhance their digital literacy, and educate them on the significance of safeguarding digital privacy, that is, keeping PINs and passwords confidential.

Future of cashless economy

The future of a cashless society is a promising one but not an effective one yet. Although technological advancements are changing the dominant design of how people perceive cash, there is a positive correlation between opportunities and threats. The concept of mobile payments, apps such as Google Pay or Apple Pay acting as digital wallets, negating the need for physical cash. Moreover, Biometric, and Contactless Payments, where it is possible to process transactions with the help of fingerprint scanning or facial recognition, enhances the overall digital financial ecosystem. Astha by BracBank has already implemented this on their mobile banking app. However, as previously discussed, digital financial services are prone to cyber-attacks. As a result, proper actions and measures must be ensured by the government for the seamless operation of the digital economy (Dhaka Tribune, 2023). Moreover, the government data of Bangladesh estimates that still 50 to 60 million rural people in the country do not have bank accounts—a must for a cashless society (Pieal, 2023). As a result, the biggest challenge for the Bangladesh government before moving towards the cashless society ambitions will be to bring cent percent people of the country under banking services. Although the MFS industry of Bangladesh is making significant strides in bringing the unbanked population under formal banking services, several calculated actions are yet to be taken for the transformation of the country into going completely cashless. This entails creating safe payment methods and increasing internet connectivity. The transition to a cashless economy can also be sped up by educating the public about the advantages of cashless transactions and offering incentives to companies that embrace digital payments.

Conclusions

The shift towards a cashless society seems to be an economic necessity, and it is the function of policy and technological direction. The trend towards going cashless is global, but what works in one country might not apply to others due to cultural and infrastructure gaps. Moreover, specific segments of society might be excluded, such as the older generation that is not so tech-savvy and people in rural areas with poor internet connections. One should be aware of the possible drawbacks that might lead to increased cybercrime, electronic fraud, and digital hacking. However, with time, encryption and strong authentication can help reduce and bring these issues under control and, eventually, establish a prosperous cashless society

Questions

1. How have technological advancements in the financial sector contributed to broader sustainability goals in Bangladesh? 2. What are some of the initiatives taken by different organizations in Bangladesh to encourage the adoption of a cashless society? 3. What are the challenges Bangladesh might face in bringing a cashless society?

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.