Abstract

Accounting education continues to navigate a delicate balance between maintaining foundational technical skills and embracing digital transformation. This study argues that accounting education has evolved beyond its traditional technical focus into a multidimensional domain shaped by digital transformation, AI, sustainability, and ethical awareness. This study combines a systematic literature review, conducted under the guidelines of the PRISMA 2020 protocol, with bibliometric analysis to examine 2,362 peer-reviewed studies published between 1970 and 2024 in the Web of Science database. The findings reveal four main areas of concentration: pedagogical innovation, sustainability and ethics, technological advancement and curriculum reform. Highly cited studies, the themes that stand out are the alignment between qualifications and the labor market, students’ motivations, expectations and academic readiness, the impact of COVID-19 and crisis management in education, creative teaching practices, ethics and human values education. The analysis also shows that the United States, the UK and Australia dominate both publication output and collaboration networks, shaping global discourse but potentially constraining the diversity of pedagogical perspectives. Emerging research frontiers highlight the transformative role of artificial intelligence, data analytics and automation in reshaping accounting curricula, alongside growing attention to sustainability reporting, ESG frameworks and corporate social responsibility. These developments signal a shift toward interdisciplinary, competency-based education that balances technical proficiency with critical thinking, ethical reasoning and adaptability. Overall, the future of accounting education will depend on the integration of interdisciplinary approaches, industry-linked learning models and the embedding of ethical and digital competencies advancing toward a more inclusive and sustainable global framework.

Plain Language Summary

This study looks at how research on accounting education has changed over the past fifty years, from 1970 to 2024. We examined 2,362 academic articles from an international database to see what topics have been studied, who has worked together, and how the field has developed over time. Our findings show that accounting education is no longer focused only on technical skills, such as learning how to record and report financial transactions. Today, it also covers professional abilities like communication and teamwork, ethical awareness, and the ability to think critically and solve problems. We found five main areas that researchers focus on: innovative teaching methods, sustainability and ethics, the use of technology in teaching and learning, the skills needed for the profession, and the design of accounting curricula. Studies that have been widely read and cited show that there is still a gap between what employers expect from accounting graduates and what graduates can actually do. These studies also highlight the growing importance of sustainability and ethical responsibility, as well as the increasing role of digital technologies in the classroom and workplace. Our analysis shows that the United States, Australia, and the United Kingdom are leading in publishing research and building international collaborations in accounting education. Based on these findings, we recommend that universities design courses that bring together different subjects, work more closely with industry partners, and integrate sustainability and digital skills into their programs. This approach can help prepare future accountants not only to meet the needs of the business world but also to contribute to ethical and sustainable practices in society.

Keywords

Introduction

The evolving business environment is experiencing a profound transformation, driven by rapid digitalization, the extensive integration of digital information into organizational processes and the exponential growth of data volumes (Guşe & Mangiuc, 2022; Handoyo, 2024). This transformation is redefining the roles and responsibilities of accountants and calls for a comprehensive professional adaptation. Accountants are now expected not only to possess strong technical expertise but also to embrace a sustainability-oriented mindset and adjust to new working conditions and environments (Tsiligiris & Bowyer, 2021; Winterton & Turner, 2019). Furthermore, accounting has emerged as a central component of corporate governance, assuming significant responsibilities within governance structures (Efferin & Soeherman, 2024; Hopper, 2019) and playing a strategic role in value creation across various business operations (IAESB, 2019). Accountants can assume diverse roles in advancing the Sustainable Development Goals (Bebbington & Unerman, 2018). Meanwhile, the growing integration of artificial intelligence (AI) is reshaping the accounting profession. Organizations now expect graduates to demonstrate advanced AI competencies alongside traditional accounting skills (Abdo-Salloum & Al-Mousawi, 2025; Damerji & Salimi, 2021). While accounting education plays a critical role in equipping professionals with necessary knowledge and competencies (Asonitou & Hassall, 2019; Baharom & Abdullah, 2024; Tharapos, 2021), it has been criticized for being slow and outdated in adapting to market changes (Amernic & Craig, 2004; De Silva & Nilipour, 2024; Humphrey, 2005; Mangion, 2006). Nevertheless, accounting education has undergone significant changes in line with stakeholder expectations (Baharom & Abdullah, 2024; Rebele & St. Pierre, 2019), yet the continuous evolution of production patterns and professional roles has made dynamic curriculum reforms inevitable (Apostolou et al., 2017; Apostolou et al., 2021; Nanjundaswamy et al., 2025). Universities are attempting to adapt by incorporating information technologies, data analytics and sustainable development goals into their curricula (Birt et al., 2023; De Silva & Nilipour, 2024; Jackson & Allen, 2023), updating specialized courses to meet global market needs (Al-Hazaima et al., 2024; Ebaid, 2022; Handoyo & Anas, 2019; Nanjundaswamy et al., 2025).

Despite these efforts, significant theoretical gaps remain in understanding the intellectual and structural evolution of accounting education (Handoyo, 2024). Numerous bibliometric and systematic studies have attempted to trace this evolution from various perspectives (Amin et al., 2025; Apostolou et al., 2022; Baharom & Abdullah, 2024; Handoyo, 2024; Linnenluecke et al., 2020; Merigó & Yang, 2017; Pattnaik et al., 2021; Poje & Groff, 2022). However, most have focused on limited dimensions either technology integration into accounting curricula (Amin et al., 2025; Amjad, 2022; Handoyo, 2024; Romero-Carazas et al., 2023) or the inclusion of sustainability and social responsibility topics (De Silva & Nilipour, 2024; Frizon & Eugénio, 2022). Others have analyzed developments in accounting and business education research during specific periods (Hallinger & Wang, 2020; Linnenluecke et al., 2020; Merigó & Yang, 2017; Najaf et al., 2022). Yet, few comprehensive studies have systematically mapped the dominant themes and intellectual structures of accounting education over extended time spans.

Recent studies carried out in academia demonstrate the need to perform more encompassing research in this area. According to Amin et al. (2025), future research should concentrate on novel competencies required in the labor market, specifically in the area of artificial intelligence, blockchain technology and data analytics. Moreover, Gil (2025) underlines the importance of the analysis of structural aspects and related socio-political factors in the context of accounting education. Abdo-Salloum and Al-Mousawi (2025) state that AI-based accounting subjects should become a part of the traditional curriculum to equip students qualitatively in order to meet the requirements of the profession. Similarly, Al-Hattami (2025) highlights the role of digital accounting tools, technological self-efficacy and digital literacy in driving innovation, encouraging future research that uses longitudinal approaches across diverse cultural settings and develops teaching strategies to enhance problem-solving and creativity.

In pursuit of accounting education research gaps and mapping the theoretical and practical gaps in accounting education studies, the current analysis incorporates a holistic approach based on the usage of both bibliometric mapping and the qualitative assessment of highly cited documents. Utilizing the total of 2,362 documents identified in the Web of Science between 1970 and 2024, the current analysis holistically investigates general trends and structures and the development of themes related to the topic of accounting education. As a preferable procedure in SLR studies due to both its consistency and reliability of the final results (Anomah et al., 2025; ElKelish, 2023), the SLR strategy has been considered as the solid foundation for the above-mentioned analysis. This integrated approach offers an up-to-date and comprehensive overview of Accounting Education Research (AER), systematically examining key themes and notable contributions that have influenced the field’s development. In this context, the study acts as a valuable guide by identifying key directions for future research and curriculum design. Accordingly, the following research questions have been developed:

The remainder of this paper is structured as follows. The paper first provides an overview of the theoretical framework and presents a detailed review of the current literature, highlighting key trends and gaps in AER. It then explains the methodology, including the bibliometric and qualitative content analysis techniques used to investigate the field. The findings of the study are subsequently presented, encompassing publication trends, thematic clusters, and collaboration networks. The results are then discussed in depth, offering critical insights and implications for accounting education practice and policy. The paper concludes with a summary of the main contributions and proposes directions for future research. Finally, the policy and practical implications derived from the study are presented.

Theoretical Perspectives

This study adopts a multidimensional approach by jointly considering Human Capital Theory and Institutional Theory to explore the evolution of accounting education. Initially, Human Capital Theory is examined to highlight how accounting education contributes to the enhancement of individual skills, employability and the development of competencies. In contrast, Institutional Theory is employed to explain how external factors such as business demands and institutional pressures influence accounting education and how educational systems establish legitimacy by aligning with these expectations.

Based on these theoretical perspectives, current issues in accounting education, educational approaches and development dynamics have been comprehensively addressed in conjunction with the literature. The literature review presented below, based on the theoretical framework, systematically addresses the important findings of academic studies related to accounting education and attempts to reveal the multidimensional nature of the field.

Human Capital Theory

Human Capital Theory is acknowledged as a fundamental paradigm for enhancing organizational performance. In institutions and organizations, value generation essentially relies on faith in the knowledge, skills and competencies of individuals (Wuttaphan, 2017). As McConnell et al. (2009, p. 78) assert that “a more educated, better trained person is capable of supplying a larger amount of useful productive effort than one with less education and training.”

According to Becker (1964), human capital is a form of physical production and organizations invest in it through education, training and healthcare. Accumulation of human capital can occur via education, training, migration and health-related measures, through which individuals gain competencies. These investments are made with the expectation of long-term positive returns.

Subsequent developments in the literature have underscored the shifting perspective on human resources within organizations. Ulrich (1998) suggested that human resources were traditionally viewed as a cost to be minimized. However, this understanding has shifted today, human resources are increasingly seen as sources of value (Wuttaphan, 2017). Phillips (2005) classified human capital as a subcomponent of intellectual capital, noting that in knowledge-based organizations, intangible assets tend to outweigh tangible ones. Vejchayanon (2005) added that institutional capital is part of total capital, categorized as both intellectual and financial, with intellectual capital further consisting of relational, organizational and human capital.

Nevertheless, several critical academics contend that Human Capital Theory provides a constrained perspective on the connection between education and employment by overlooking the social stratification and institutional environments that influence educational results (Marginson, 2019). Also, in reaction to the constraints of the excessively individualistic perspective, several scholars have adopted a more holistic interpretation of Human Capital Theory. Ployhart et al. (2014) introduced the notion of “human capital resources” to characterize human capital functioning at the collective or organizational level, such as within teams or firms regarding skills and knowledge. Nyberg et al. (2014) also assert that the rhetoric on human capital has become excessively centered on individualism, overlooking the wider organizational environment (Wuttaphan, 2017). Consequently, contemporary thought regards individual human capital as a component of a broader system of human capital resources inside an organization (Ployhart et al., 2014).

Establishing a learning-oriented organization requires prioritizing investment in human resources. To achieve this goal, it is essential that training programs are carefully designed and that employees are encouraged to actively participate in both general training and field-specific specialized training (McConnell et al., 2009). In this context, Bui and Porter (2010) argue that accounting education should not be confined to the transmission of technical knowledge rather, it should be redesigned to equip graduates with communication skills and professional competencies. Similarly, Howieson (2003) emphasizes the importance of integrating skills such as analytical thinking, critical analysis and technological literacy into accounting education, rather than focusing solely on traditional technical training. Sangster et al. (2020) state that the COVID-19 pandemic has accelerated the transition from face-to-face education to digital platforms and that this change has brought with it various challenges as well as new opportunities. Researchers state that this transformation has significant implications for areas such as student interaction, data security and interactive learning, and that it could lead to long-term changes in the way education is delivered.

From a different perspective, McPhail (2001) argues that teaching in accounting education should not be limited to the transfer of technical knowledge. McPhail argues that developing ethical awareness and social sensitivity is as important as acquiring professional knowledge. The author warns that viewing students solely as numerical data can lead to ethical insensitivity. McPhail further maintains that restructuring the education system is essential for the full integration of ethical awareness and emotional understanding. In this context, McPhail argues that an exclusive focus on professional regulations is insufficient students must also cultivate a strong sense of moral responsibility toward others.

Similarly, Bebbington and Unerman (2018) emphasize that sustainability, particularly its ethical and social dimensions, is becoming increasingly important in accounting education. The researchers argue that accounting should be viewed not only as a financial reporting tool but also as an interdisciplinary field that supports the achievement of the Sustainable Development Goals (SDGs). This is because it is important to educate accountants not only with technical knowledge but also as socially responsible, critical thinkers and individuals capable of multidisciplinary collaboration.

Al-Hattami (2025) found that digital accounting tools and technological self-efficacy significantly enhance innovation, with digital literacy playing a direct role. Amin et al. (2025) identify artificial intelligence, blockchain and data analytics as core trends reshaping accounting curricula. Müller (2025) emphasizes the integration of ethical values with digital competence as a defining feature of modern accounting education. Feltham et al. (2025) found that employers place considerable emphasis on fundamental accounting knowledge, ethical judgment and critical thinking, alongside the ability to use AI tools in a supportive capacity.

Collectively, these recent studies suggest that accounting education is becoming an increasingly multifaceted field that integrates technical expertise with ethical awareness, sustainability and innovation. Developing human capital in this context requires curricula that balance digital competencies with critical thinking, ethical reasoning and social responsibility.

Institutional Theory

Institutional Theory is a widely accepted perspective in organizational and social research, one that gives primacy to considerations of legitimacy and social norms alongside efficiency (Scott, 2008). It suggests that organizations are influenced not just by rational pursuit of productivity, but also by the need for legitimacy in the eyes of stakeholders. Proponents of this view contend that a fundamental outcome of institutional pressures is the alignment of organizational behavior with prevailing ethical and societal norms. In practice, organizations tend to consider how peer institutions are optimizing their structures and processes, rather than focusing solely on internal, rational decision-making (Marquis & Tilcsik, 2016).

DiMaggio and Powell (1991) introduce the concept of “New Institutionalism,” as a theoretical perspective that serves as the counterpoint to the rational actor models used in classical economic thought. Rather than focusing solely on the actions and motivations of individuals as the cause of organizational and societal-level phenomena, the focus shifted toward the cognitive and cultural aspects at more general, supra-individual levels. According to the theory of institutional, the structures and procedures used in the organization are shaped not only by the principles of efficiency but also the drive for conformance to outside expectations and the pursuit of gaining legitimacy. DiMaggio and Powell (1983) describe the process of conformance as “isomorphism.” This takes on three forms: coercive, mimetic and normative. While coercive is based on laws and regulations, mimetic is based on the organization as a copy of the more successful form under uncertain circumstances. Normative isomorphism stems from shared professional values and educational norms (DiMaggio & Powell, 1983).

Three types of isomorphic pressure are clearly observed in the context of accounting education. Coercive isomorphism stems from the influence of government regulations and powerful professional organizations such as AACSB and AICPA on universities (Fogarty, 1997). Fogarty (1997) notes that accounting programs in the United States are increasingly aligning with the expectations of these institutions. This situation leads to the emergence of structurally similar curricula among universities and is considered a clear indicator of coercive institutional pressures (Fogarty, 1997). Mimetic isomorphism arises when institutions facing uncertainty model themselves after highly regarded or successful organizations. According to Fogarty (1997), this results in imitation of the academic practices and program structures of elite institutions, even when such emulation lacks independent justification. Sikka and Willmott (2002) argue that accounting education is largely determined by professional orthodoxy, which limits the space for critical or alternative pedagogies.

Sikka and Willmott (2002) argue that dominant themes such as employability, ethics and technology integration, which arise under the influence of these pressures, stem not only from pedagogical requirements but also from the accounting field’s pursuit of institutional legitimacy. Also emphasizes that, with the rise of performance measurement and accountability cultures in educational institutions, academic activities have become increasingly shaped by external audit and evaluation mechanisms. Although these systems are effective in establishing institutional legitimacy, they do not improve the quality of education (Power, 2003). In this context, with the growing interest in the United Nations Sustainable Development Goals (SDGs), many universities have added sustainability-focused courses to their curricula and started publishing regular institutional sustainability reports. These initiatives, developed in collaboration with governments and communities, reflect the systematic integration of sustainability into higher education strategies (Nikolaou et al., 2023).

Institutional Theory and Human Capital Theory together help explain how accounting education evolves under both internal dynamics and external pressures. In today’s context, legitimacy requires meeting regulatory expectations while fostering innovation, ethical awareness and sustainability (Bebbington & Unerman, 2018; Guşe & Mangiuc, 2022; IAESB, 2019). These dual pressures institutional and market-driven require curricula that respond to technological transformation while addressing wider social and professional responsibilities.

Methodology

In this study, a comprehensive systematic literature review (SLR) covering the past 50 years was conducted to identify the general trends, structural characteristics and thematic developments within the accounting education literature. The review was undertaken to create a comprehensive dataset for subsequent bibliometric and content analyses and no statistical meta-analysis was performed. The primary objective was to systematically examine the general trends, structural characteristics and emerging themes in the field. The SLR process was carried out in accordance with the PRISMA 2020 guidelines to ensure an accurate, transparent and reproducible analysis of the literature (Anomah et al., 2025; Page et al., 2021). This approach enhanced methodological consistency at every stage of the research process, thereby strengthening the reliability of the findings (ElKelish, 2023; Massaro et al., 2016). The resulting dataset was then analyzed in the second stage of the study using bibliometric methods.

Bibliometric analysis is a quantitative method frequently employed in the social sciences to identify patterns within the literature and to evaluate networks of scholarly contributions (Abdullah et al., 2023; Byington et al., 2019; Pattnaik et al., 2021; Zupic & Čater, 2015). Rather than focusing on individual research findings, this approach analyses bibliographic data to assess the overall structure of the accounting education literature (Amin et al., 2025; Hallinger & Wang, 2020). By quantitatively mapping prevailing research trends and patterns of scholarly collaboration, bibliometric analysis provides a deeper understanding of the structural characteristics of the literature (Amin et al., 2025; Anomah et al., 2025; Baharom & Abdullah, 2024; ElKelish, 2023; Handoyo, 2024; Linnenluecke et al., 2020; Merigó & Yang, 2017; Najaf et al., 2022; Pattnaik et al., 2021; Poje & Grof, 2022). On the other hand, the growing volume of publications in the field underscores the necessity of employing qualitative content analysis to achieve a deeper understanding of the literature (Najaf et al., 2022; Stemler, 2015). Content analysis offers a systematic approach to examining the literature and identifying core themes, thereby making a significant contribution to the advancement of the field (Cavanagh, 1997; Grosse, 2024; Krippendorff, 2018; Neuendorf, 2017). In this context, similar approaches that integrate bibliometric mapping with qualitative content analysis have been widely adopted across various disciplines (Goksu et al., 2022; Klarin, 2024; Spiegel-Rösing, 1977).

To gain a comprehensive understanding of conceptual trends in Accounting Education Research (AER), a qualitative content analysis was conducted on highly cited studies. From a total of 2,362 articles, those receiving at least 100 citations were classified as “high-impact studies” and included in the analysis. In line with this approach, previous research by Merigó and Yang (2017), Linnenluecke et al. (2020), and Hallinger and Wang (2020) has also relied on highly cited publications to identify thematic structures. Focusing on citation impact rather than publication counts is consistent with established bibliometric practices, as prior studies have shown that while the volume of publications is a necessary condition for receiving citations, it is not sufficient only a limited proportion of studies generate lasting influence within their field (Garfield, 1998; Podsakoff et al., 2008). Garfield (1998) reported that among approximately 33 million articles indexed in the Science Citation Index between 1945 and 1988, only 0.4% had received more than 100 citations (Podsakoff et al., 2008). This underscores that studies surpassing this threshold represent exceptional research that exerts a sustained and substantial impact on the field. Accordingly, the present study focuses on such high-impact works to identify the most influential contributions in AER and to uncover their underlying conceptual trends. Specifically, six studies met this threshold and were included in the qualitative content analysis: Jackling and De Lange (2009; 258 citations), Bui and Porter (2010; 172 citations), Sangster et al. (2020; 139 citations), Byrne and Flood (2005; 118 citations), Chiou (2008; 106 citations), and McPhail (2001; 102 citations).

These publication sources represent the most influential and lasting effort in the area of accounting education research and were employed in the derivation of thematic insights presented in the findings section. However, we recognize the potential limitation of our approach in only focusing on citations as measures of success, as it might lack the influence of important works published in regional or outside the English general publication domain that tend to generate relatively fewer citations.

Thematic patterns were identified inductively through careful examination of the selected studies. Rather than applying a predetermined framework, themes arose from the data itself, following standard qualitative methods (Elo & Kyngäs, 2008; Elo et al., 2014; Thomas, 2006). This inductive strategy works well for exploratory and interdisciplinary research since it avoids imposing existing categories and can reveal unanticipated connections (Chakma & Li, 2025; Elo et al., 2014).

To enhance transparency and reduce individual bias, we employed a multi-researcher triangulation process. Following Elo et al. (2014) and Chakma and Li (2025), three researchers independently reviewed each of the six most-cited articles, recording potential themes separately before discussing them collectively. Overlapping ideas were then consolidated and differences were resolved through joint re-examination of the source texts. When disagreements persisted, the team revisited the original materials until consensus emerged. This iterative process enhanced the credibility of the analysis. Additionally, a word cloud illustrated the most frequently appearing keywords in these influential studies and a graph was used to visualize key patterns. This comprehensive methodological approach allowed for an in-depth understanding of trends in accounting education from both qualitative and quantitative perspectives, thereby offering valuable insights into the field’s development.

Earlier work, notably Spiegel-Rösing (1977), established the methodological basis for integrating bibliometric and content analysis in studies of academic disciplines. More recently, Goksu et al. (2022) and Klarin (2024) have demonstrated that combining bibliometric mapping with qualitative thematic analysis can effectively trace the conceptual evolution and intellectual structure of research fields.

The three-phase methodological framework described above comprising systematic literature review, bibliometric analysis and qualitative content analysis is synthesized in Figure 1. This integrated research design illustrates the systematic progression from initial data collection through quantitative mapping to in-depth thematic examination, providing a comprehensive approach to understanding the evolution of accounting education literature over the past five decades.

Research design framework.

Data Collection and Analysis

The data for this study were obtained from the Web of Science (WoS) Core Collection database, employing a comprehensive search strategy rather than relying on repeated keyword refinements. We carried out a comprehensive search from 1970 to 2024 for the keyword “accounting education” in all fields, including titles and keywords. This strategy offered 3,584 recordings in total and allowed to explore a wide range of subjects. This made it less likely that the literature review would have selection or exclusion bias.

The dataset included only peer-reviewed journal publications to reduce duplication. For instance, papers from conferences that were later published in journals were only counted once. Within this scope, we identified a total of 2,362 articles published between 1970 and 2024. Different studies employed similar ways to obtain data. (Alcalá-Albert & Parra-González, 2021; Le Thi Thu et al., 2021; Ouyang et al., 2022). Figure 2 demonstrates the PRISMA 2020 flow chart displaying the stages involved in choosing and identifying data during the data screening process (Borges et al., 2022; Bosi et al., 2022; Cumbana & Ventura, 2024).

PRISMA model.

We selected the Web of Science Core Collection as our primary data source because of its rigorous indexing standards and stable coverage across the 50-year study period, which provides reliable and comparable data. However, this choice means we may have missed relevant publications available in other databases such as Scopus or Google Scholar, particularly work published in regional or non-English journals. Readers should bear this limitation in mind when interpreting the results.

The bibliographic data obtained from the WoS database was analyzed through the use of Microsoft Excel and VOS viewer. Excel was used for cleaning and organizing the data obtained for the purpose of creating appropriate classes for the descriptive statistical analysis techniques like frequency and percentage distributions. The creation of the structural visuals encompassing the geographic location of the publications, the word co-occurrence pattern visualizations, as well as the network visualization related to the co-authorship details were facilitated through the use of VOS viewer. The network visualization in the form of the word co-occurrence thematic map allowed the thematic grouping based on the relationship intensity to create distinct thematic clusters (Bosi et al., 2022; Umar et al., 2022).

Findings and Analysis

This section delineates the principal conclusions obtained from the bibliometric and qualitative analyses performed in this study. A bibliometric analysis is conducted to assess the distribution of document types, publishing evolution, author productivity, institutional connections, international collaboration patterns and prominent journals. A qualitative content analysis of the most frequently cited studies is performed to discern common themes and conceptual ideas. The integrated approach offers a thorough examination of the structural landscape and topic themes in AER on research from 1970 to 2024.

Distribution of Publication Types in Accounting Education Research

Table 1 shows the distribution of publication categories in accounting education literature, providing insight into the structural makeup of scholarly production in the area. A detailed study reveals that the great majority of publications are peer-reviewed journal articles (n = 2,362). This dominance suggests that academic journals are the major medium for distributing research in accounting education and the most widely recognized platform for scholarly communication.

Distribution of the Studies According to Document Types.

Source. Authors’ own creation.

Following journal articles, editorial articles (n = 285) and book chapters (n = 283) are the other most common types of publications. This situation shows that academic interest in compilation books and editorial contributions continues in this field. In addition, publication types such as conference papers (n = 257) and book reviews (n = 207) are also noteworthy. These types are important for both sharing early research findings and critically evaluating academic works. Furthermore, other document types such as early access publications (n = 75) and compilation articles (n = 44), although present in more limited numbers, can be effective in synthesizing existing information and shaping current debates. Books (n = 21), letters (n = 17) and a small number of biographical notes, corrections, meeting summaries, and retracted publications demonstrate the diversity of academic production but are represented at a limited level in the field. This distribution shows that scientific studies in the field of accounting education are largely published in peer-reviewed journals based on empirical and theoretical contributions. It also points to a more diverse but limited number of publication formats that support the academic discourse in this field.

Temporal Evolution of Accounting Education Publications (1970–2024)

An examination of Figure 3 shows that the first examples of accounting education literature in the Web of Science (WoS) database date back to 1970. It can be seen that the number of articles published between 1970 and 2001 was quite limited and did not show any significant change over the years. This period can be termed as the commencing phase wherein the development of accounting education has garnered insignificant attention in the scientific community. However, the increase in the publication of significant numbers of articles began from 2003, and since then the increase has been intensified in the 2020s. In fact, the surge in the publication of a remarkable number of articles related to accounting education has been identified in the years 2021, 2022, 2023, and 2024. This increase can be seen as a reflection of new themes such as digitalization, sustainability and professional competencies in the global accounting education literature.

Publication trends in accounting education (1970–2024).

Productivity Analysis of Authors, Institutions and Countries in Accounting Education

The total number of researchers who have published on the topic of “accounting education” in the Web of Science database has been determined to be 200. The top 50 authors with at least 7 publications are listed in Table 2. The list shows only individual productivity. Co-authorships have not been taken into account.

Researchers With the Most Publications.

Source. Web of Science Core Collection (2024).

The findings indicate that the five most prolific researchers in the field of accounting education are Beverley Jackling, Paul De Lange, Fred Phillips, Satoshi Sugahara and Kim Watty. These scholars have made consistent contributions to the accounting education literature and are considered to have significantly influenced the development of the field at the international level.

According to the data in Table 3, the 25 universities with the highest number of publications in the field of accounting education in the Web of Science database are ranked. This ranking is based on the institutional affiliation information of the relevant universities and is organized according to the number of publications.

The Most Productive Universities in Accounting Education Studies.

Source. Web of Science Core Collection (2024).

The findings indicate that academic production in the field of accounting education is largely carried out by universities based in the United States. Among the universities in this country, the University System of Ohio, the State University System of Florida and the University of North Carolina are particularly noteworthy. Additionally, Australian universities (e.g., RMIT, Deakin University, Monash University) also have a significant share in the literature.

This distribution indicates that accounting education is a more intensive area of research in countries where the Anglo-Saxon education system is influential, and that there is a strong link between professional education and academic production in these countries.

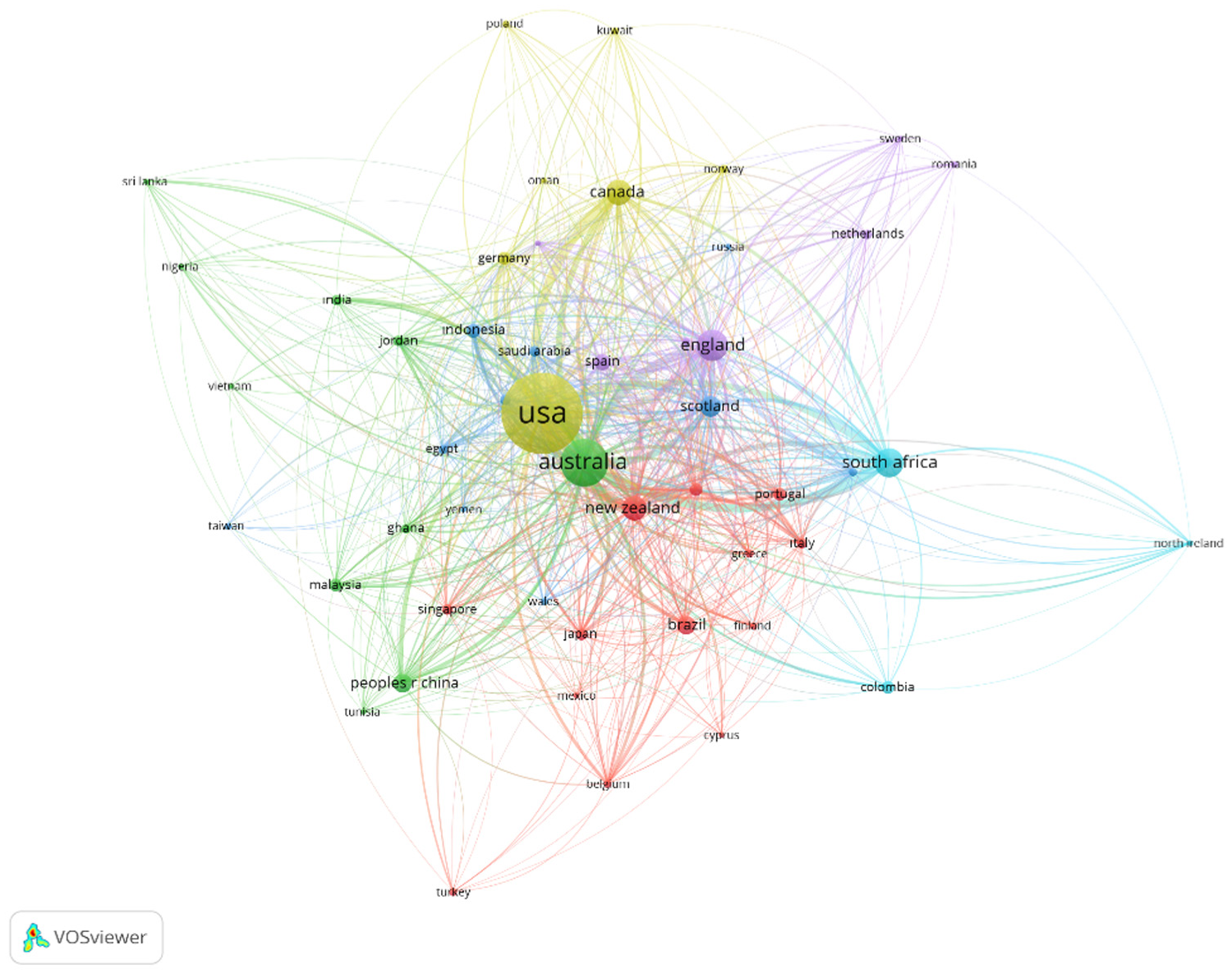

Figure 4 visualizes the country-based scientific collaboration and citation network created by considering publications that have received at least five citations in the field of accounting education. The visual analysis reveals the academic interaction between countries in terms of both scientific impact (number of citations) and collaboration intensity (co-publication links). When citation counts are considered, the United States emerges as the leading country in terms of scientific influence in the field of accounting education, accumulating a total of 8,864 citations across 1,033 publications. Australia follows in second place, with 5,525 citations from 368 publications. The United Kingdom ranks third, achieving 2,449 citations from 164 publications, while New Zealand also demonstrates a noteworthy contribution with 1,918 citations drawn from 98 publications.

Distribution of the most cited studies in accounting education by country.

These figures indicate that Anglo-Saxon countries hold a dominant position in accounting education not only regarding the quantity of publications but also in terms of scientific impact. Analyzing the network structure illustrated in Figure 5, it becomes clear that publications originating from the United States have formed strong collaborative links with numerous countries. Similarly, Australia, the United Kingdom and South Africa emerge as key hubs for collaborative research in this field. In this network, the size of the nodes represents the citation intensity for each country within the accounting education literature, whereas the thickness of the connecting lines reflects the frequency of collaborative relationships. This analysis highlights that international collaboration in AER is strengthening over time and that academic knowledge in the field is increasingly organized on a global scale within distinct regional clusters.

Cooperation map by countries.

Leading Journals in Accounting Education Research Output

From 1970 to 2024, the publication of studies related to the area of accounting education has appeared in 200 academic journals. Table 4 shows the 10 most prolific journals that have published the largest number of studies related to the area. As shown in Table 4, a large percentage of the published studies related to accounting education can be found in the category of specialized studies under the themes of “accounting” and “accounting education.” The three main journals that have pooled the largest number of studies in the field are: Issues in Accounting Education, Accounting Education and Advances in Accounting Education: Teaching and Curriculum Innovations.

The Journals With the Most Publications in the Field of Accounting.

Source. Authors’ own creation.

These journals represent the main outlets for the publication of both theoretical and applied studies in accounting education and have made important contributions in the area of curriculum design, instructional practices, ethics education, digital transformation and competency-based education. This table represents a useful resource for researchers planning to carry out studies in accounting education as a way of identifying the premier outlets and the academic context in which the field continues to develop.

International Collaboration Patterns in Accounting Education Studies

The findings in this area of the study demonstrate international collaboration in accounting education and academic links. In this case, the diameters of the nodes in Figure 5 represent the number of collaborations in each country and the thickness of the lines represents the strength of inter-country linkages. Color clusters represent groups of countries that commonly publish together. The analysis shows that Australia, the United States, the United Kingdom, South Africa, Canada, New Zealand and Scotland have the best global networks for AER. These countries’ research outputs serve as the foundation for AER and are at the center of the worldwide academic network in accounting education.

Most Cited Scholars in Accounting Education Research

In this section, publications that have received 100 or more citations between 1970 and 2024 in the field of accounting education were examined. Publications that received at least 100 citations were identified by searching for the keyword “accounting education” in the Web of Science (WoS) database. Studies that were not directly related to accounting education in terms of content were excluded from the list.

According to the findings obtained within this scope, the authors who have contributed the most to the accounting education literature and received the most citations are Jackling and De Lange (2009), Bui and Porter (2010), Sangster et al. (2020), Byrne and Flood (2005), Chiou (2008), and McPhail (2001). The works of these authors span a wide range of themes, including workforce expectations, learning motivations, remote education experiences during the COVID-19 period, ethics education and conceptual learning methods (Table 5).

The Most Cited Authors in the Field of Accounting Education.

Source. Authors’ own creation.

The key concepts obtained from these publications are visualized in the form of a word cloud in Figure 6 The visualization shows that concepts such as labor market, learning, education, teaching, methods and employers stand out. This indicates that the accounting education literature has been shaped primarily by the expectations of the business world, methodological transformation in education and student-centered learning approaches. This analysis reveals that AER focuses on both pedagogical practices and the development of professional competencies, and is integrated with current social issues (e.g., ethics, COVID-19, digitalization).

Word cloud according to the most cited works in the field of accounting education.

Thematic Insights From the Most Cited Studies in Accounting Education

An evaluation of studies in the field of accounting education that have received 100 or more citations reveals a set of recurring thematic patterns based on their objectives and findings. Below is a summary of the key themes and contributions of these highly cited works:

Jackling and De Lange (2009) investigated whether the skills acquired in undergraduate and graduate accounting programs align with employer expectations. Their findings indicated that accounting programs are often insufficient in equipping graduates with essential soft skills such as leadership, teamwork and verbal communication, which are highly valued by employers.

Bui and Porter (2010) explored the gap between the qualifications employers expect from accounting graduates and what universities actually provide. Despite curriculum reforms, the study found that a disconnect persists between higher education outcomes and labor market demands. The authors proposed various recommendations to better align accounting education with professional expectations.

Sangster et al. (2020) analyzed the perspectives of 66 academics from 45 countries regarding the impact of the COVID-19 pandemic on accounting education. The study emphasized the problems and potential associated with the swift shift to online education, noting that the pandemic expedited the implementation of hybrid learning models and initiated a new research agenda centered on crisis management in education.

Byrne and Flood (2005) investigated the motivations, expectations and academic readiness of first-year university students who opted to pursue accounting in Ireland. The survey indicated that students predominantly selected accounting programs for professional advancement and intellectual enrichment, although expressed apprehensions regarding their academic readiness and anticipated greater autonomy in their studies.

Chiou (2008) assessed the impact of idea mapping methodologies on academic achievement and student engagement in accounting courses in Taiwan. The study determined that concept maps markedly enhanced student learning relative to conventional approaches and were favorably regarded by students as an efficient instrument for comprehending intricate accounting subjects.

McPhail (2001) advocated for a humanistic approach to accounting ethics teaching in a theoretical analysis, highlighting the significance of emotional connection and empathy. The report condemned the dehumanized character of the accounting profession and advocated for the incorporation of ethical considerations rooted in compassion and moral accountability. It moreover provided suggestions for ethical revitalization in accounting by referencing advancements in other professional fields.

When the most cited studies in the literature are considered, the five main themes identified as part of AER can be observed. Figure 7 shows the thematic structure based on the findings of the most cited studies. The theme of alignment between qualifications and the labor market has been identified based on the studies conducted by Jackling and De Lange (2009), as shown below. These studies revealed that accounting programs often fail to adequately prepare graduates for employer expectations, particularly in developing essential soft skills such as leadership, teamwork and verbal communication.

Five dominant themes in accounting education research.

The second theme, students’ motivations, expectations and preparedness, draws on the study by Byrne and Flood (2005), which examined the reasons students choose accounting education and their perceptions of academic readiness. The third theme, impact of COVID-19 and crisis management, is informed by Sangster et al. (2020), who highlighted how the pandemic accelerated the transition to online and hybrid learning models and sparked a new research agenda focused on crisis management in education.

The fourth theme revolves around creative teaching practices. This theme has been established based upon the findings of Chiou (2008), stating that the usage of the methodologies of idea mapping had a positive impact upon the grades and attentiveness of students in accountancy classes. The theme of education in ethics and human values has been based upon the theoretical concepts presented in the study of McPhail (2001), the fifth theme. This study underscores the significance of emotional connection, empathy and moral responsibility in accounting ethics instruction. Collectively, these five themes offer a thorough conceptual framework that encapsulates contemporary trends and prospective research trajectories in the accounting education literature.

This theme synthesis illustrates how the field of accounting education has evolved from the traditional technical field to a more complex area that encompasses professional competencies, ethics awareness and intellectual development. Notably, the five themes correlate to a couple of significant clusters mentioned in our bibliometric analysis (see Figure 8), thereby solidifying their significance in the intellectual landscape of AER. For example, research emphasizing the expectation-performance disparity and the advancement of professional skills pertains to Cluster 4 (Blue), Professional Competencies and Curriculum Development. On the other hand, studies based on ethics education and human values fall under Cluster 2 (Green), Sustainability and Ethics. Moreover, innovation in education falls under Cluster 1 (Red). However, while digital transformation and technological integration are not directly featured among the five dominant themes in the cited literature (Figure 7), they emerge prominently in the bibliometric clusters. Particularly, Cluster 3 (Yellow) highlights a growing area for future research.

Thematic keyword clusters.

Thematic Clusters in Accounting Education Literature

In the period between 1970 and 2024, a total of 5,203 unique keywords were identified based on 2,362 published articles related to accounting education. This reflects the multidimensional nature of the discipline and the diversity of research directions. Using VOSviewer software, a keyword co-occurrence network analysis was conducted, and the resulting map was clustered to highlight major thematic areas in the literature.

Figure 8 illustrates how the colors of the thematic map denote distinct focuses for the research. The largest group in the red category encompasses keywords such as innovation in teaching, student involvement and participation in active learning, general competences and graduates’ job market entry. The other dominant category, green, reflects the increasing importance of sustainability and ethics in accountants’ education. Keywords in this category include sustainability studies, business ethics and CSR. The yellow category encompasses technological and analytics topics such as Blockchain Technology and Artificial Intelligence. The blue cluster includes professional competences and curriculum development areas that use words such as IFRS (International Financial Reporting Standards) and audits.

The following thematic map demonstrates that AER is shifting away from traditional issues and toward sustainability, talent development, ethical awareness and technology-related topics.

Discussion

Today, accounting education is undergoing a profound transformation influenced by digital technologies, artificial intelligence, ethical values and sustainability (Al-Hattami, 2025; Amin et al., 2025; Bujaki et al., 2025; Gil, 2025; Lew et al., 2025; Müller, 2025; Rani et al., 2025). This multidimensional transformation has also significantly affected the volume and direction of research in the field of accounting education. In this context, scholars seeking to understand how the accounting education literature has evolved over time have increasingly turned to bibliometric analysis methods. By examining studies indexed in international databases such as Web of Science and Scopus, these researchers have analyzed the theoretical development, thematic trends and structural patterns of the field, contributing to the advancement of educational policies and offering valuable guidance for future research (Apostolou et al., 2022; Baharom & Abdullah, 2024; Hallinger & Wang, 2020; Handoyo, 2024; Pattnaik et al., 2021).

The findings obtained in this study support the view that bibliometric studies are an effective tool for tracking changes in the accounting education paradigm (Handoyo, 2024). In this context, according to our bibliometric research findings, the majority of valid publications in the accounting education literature are peer-reviewed journal articles. This indicates that the main area of accounting education research is academic journals and that scientific knowledge in this field is concentrated in these outlets. In addition, the fact that a large part of the research is published in specialized journals such as Issues in Accounting Education, Accounting Education and Advances in Accounting Education reveals that these journals play a determining role in shaping theoretical and pedagogical discussions in the field. Likewise, the leading position of US and Australian universities at the institutional level in the research findings also suggests that accounting education has a strong academic tradition institutionalized within the Anglo-Saxon system. On the other hand, the fact that the United States, Australia, the United Kingdom, South Africa and Canada stand out as the countries with the strongest networks in terms of international collaboration provides clues about how accounting education is structured at the global level and points to the geographical centralization of knowledge production.

The temporal analysis of publication trends in the research represents two different periods as shown in Figure 3. During this period, the number of publications remained low between 1970 and 2001 and failed to show any noticeable increase. From the beginning of the 2000s onwards, such stagnation was joined by a strong upward trend. This development overlaps with the global adoption of international accounting standards. In fact, the result of the bibliometric analysis study conducted by Sapra et al. (2025) on the Web of Science (WoS) database over the years 2003 to 2023 determined an increase in studies related to IFRS and that most of these studies were conducted by developed countries.

Mirroring this development, it is also observed that there has been a corresponding rise in interest in reporting frameworks related to sustainability, as reflected in the increased prominence of terms relating to ESG and integrated reporting. Similarly, research on ESG and CSR developed rapidly since 2008. This signals that sustainability and governance elements are increasingly integrated into accounting and finance literature (Rani et al., 2025). By contrast, the impact of regulatory transformation upon long-term accounting education research remains under-investigated. Further research may investigate how such structural changes influence topic prioritization, publishing patterns and pedagogic approaches across diverse regional and institutional settings.

Another important finding is that the USA, Australia and the UK significantly lead the pack in both the volume of publications and citation impact factors as indicated in Table 3 and Figure 4. A total of 36% of the publications in the literature come from the USA and 10% from Australia. These countries also lead the pack when viewed in the context of international collaborations and are identified as the intellectual hubs of the field as shown in Figure 4. This highlights the geography that recognizes the USA and Australia as identified in the findings of Amin et al. (2025), as the most productive and influential countries when viewed in the context of accounting education research. The underrepresentation of countries and context related to accounting education in the field of the literature should raise more critically questioning inquiries about the causes of the observed underrepresentation and should encompass analyses that account for factors like the availability of opportunities for publication, language constraints and distances from intellectual hubs.

These findings suggest that accounting education has become more sensitive to broader professional, ethical and cognitive dimensions rather than being perceived as a field of study focused narrowly on technical training. As shown in Figure 7, the most frequently cited publications in the literature cluster around five main themes reflecting established concerns regarding the purpose and content of accounting education. Figure 8, which represents the bibliometric map based on keyword co-occurrence, presents four clusters representing more recent developments. Although there is a visible degree of overlap between the thematic focus of influential studies and the thematic focus of current research, it can be noticed that technology-related topics, particularly digitalization and data analytics, have gained greater emphasis in recent publications as compared with earlier works. This situation reflects a change in the focus of academics and a further need for research with regard to the integration of technological competencies into the field of accounting education. In this context, while examining the thematic results of this research;

The first cluster (Red) focuses on pedagogical innovation and the development of social competencies. This reflects an increase in academic interest in effective learning strategies, employability and critical thinking. This finding is consistent with both bibliometric analyses and the most cited studies. The studies in question point to the need for student participation and innovative teaching designs. Future research should examine how pedagogical approaches can promote not only technical competence but also ethical awareness, creativity and adaptability (Feltham et al., 2025; Müller, 2025).

In the second cluster (Green), increased sustainability and ethical awareness are shown to be key new ideas in accounting education in response to international attempts at enacting Corporate Social Responsibility (CSR) and Environmental, Social and Governance (ESG) principles into education. Bebbington and Unerman (2018) argue that accounting should contribute to the United Nations Sustainable Development Goals (SDGs) and can do so through tools such as carbon accounting, social impact measurement and integrated reporting. Gil (2025) and McPhail (2001) extend this by suggesting that dominant neoliberal and technocratic understandings need to be questioned in order for accounting education to be human-centered. This cluster strongly brings in normative literature, notably through McPhail’s focus on moral responsibility. Future studies should critically investigate sustainability education not only as an exercise of regulatory compliance but also in relation to systemic inequalities, power relations and epistemological diversity (Gil, 2025).

The third cluster (Yellow) reflects the emergence of technological innovations such as artificial intelligence, blockchain and data analytics. As explained above, even though these themes are outstanding on the bibliometric map (Figure 8), they did not appear in the most cited studies (Figure 7). Therefore, it can be said that there is a recognition that digital transformation should be a key area for future research. Specifically, studies show that both digital literacy and technological self-efficacy support innovation in a complementary way (Al-Hattami, 2025). Building on critical pedagogy and socially engaged approaches (Ballantine et al., 2024; Gil, 2025), future research should explore how technology can be used in inclusive, ethically grounded and pedagogically meaningful ways that support rather than replace human judgment and critical thinking (Feltham et al., 2025).

The last cluster (Blue) discusses professional competencies and the reform of the curriculum of accounting education due to efforts to adapt and respond to the increasing demands of global business. Among the key themes leading to the expectation-performance gaps is that identified by earlier works of the most cited studies in this research. This gap between the competencies acquired in accounting education and employer expectations is irrespective of the economic changes that happen in the world. For instance, the studies conducted by Jackling and De Lange (2009) and Bui and Porter (2010) clearly showed the problems graduates have in terms of attaining professional standards. Amin et al. (2025) pointed out the gap between graduate competencies and employer demand as one of three key themes driving changes within the field. In the study by Feltham et al. (2025), though, it was found that basic accounting knowledge, critical thinking and ethical reasoning are more important than advanced artificial intelligence knowledge. Therefore, future research should establish whether or not critical thinking, ethical reasoning and fundamental professional knowledge, in addition to technological competencies within accounting education, match employer expectations through longitudinal and contextual approaches.

These findings clearly reveal that the field of accounting education has embarked on a multidimensional, transformative journey beyond the traditional structure. From the above bibliometric analysis, the ever-ascending interrelationship between innovation in education and sustainability, ethics, technological development and the requirements of the labor market has been observed. The pattern of publication in the above-mentioned literature clearly indicates that the development of accounting education has moved toward a more critical, inclusive and humanistic structure incorporating more diversity in both theories and methodologies. This development has not been homogeneous across the world. The less developed and developing nations have been inadequately presented. In fact, the development of more inclusive strategies has been necessitated based on the geographic and structural disparities. The future of the development of accounting education can evolve not only based on the development of digital literacy but also based on the development of critical thinking and ethical-social awareness.

Conclusions

This study, through a comprehensive systematic literature review and bibliometric analysis of 2,362 articles published in the Web of Science database between 1970 and 2024, holistically reveals the 50-year evolution of the field by identifying the general trends, structural characteristics, and thematic developments of the accounting education literature.

In this context, the research offers various contributions to the literature. Firstly, there have been two distinct eras observed in the evolution of the literature, namely the stable period covering 1970 to 2001, followed by the phase of intensive growth in 2003 and beyond. This period of growth is also contemporary with the global adoption of the IFRS, digitalization, and the subsequent evolution of sustainability in terms of ESG.

Secondly, the geographic distribution of the production of knowledge has been identified. The United States, Australia and the United Kingdom show dominance in terms of numbers of publications and citation influence, such that there is an Anglo-Saxon pattern in relation to the production of knowledge, while other regions remain underrepresented.

Third, current research has been shown to cluster around four main themes: pedagogical innovation and social competencies, sustainability and ethics, technology and data analytics, and professional competencies with curriculum reform. These clusters reflect the field’s multidimensional transformation.

Fourth, the gap between competencies acquired in accounting education and employer expectations, as identified by Jackling and De Lange (2009) and Bui and Porter (2010), continues to persist.

Fifth, accounting education has been documented as evolving from a narrow technical focus to a broader perspective encompassing professional, ethical, and cognitive dimensions. This transformation demonstrates the field’s shift from traditional structures toward critical and inclusive approaches.

In general, the findings seem to reveal the fact that the domain of accounting education is currently undergoing a paradigm shift at the confluence of technological advancements, ethical considerations and educational transformation. For the sake of future studies, the area should focus on the ethical dimension of technological transitions, the educational implications of curricular changes and the discrepancies of knowledge-creation at the regional level. This would contribute to the broader understanding of the domain of accounting education.

However, there are some limitations acknowledged. Firstly, the analysis has only been conducted on the Web of Science database. This database could have excluded important studies that have been indexed in other sources such as the Scopus database. Secondly, the analysis has been conducted only on the sources that are published in English. This might result in the under-representation of important works published other than English and in regional publications.

Future research should expand the dataset to include multiple databases such as Scopus, EBSCO and Google Scholar to enhance coverage and robustness of findings. Moreover, qualitative synthesis methods such as meta-ethnography or realist synthesis could complement bibliometric analysis by providing insights into pedagogical effectiveness and implementation challenges.

Policy and Practical Implications

The increasing rapidity of technological advancements and the worldwide commitment to sustainability have led to the modification of expectations related to accounting education. As such, national education plans should be developed to improve students’ understanding and awareness related to important sectors like technology, ethics and sustainability.

To accomplish this, a curriculum review, development of teaching staff professional competency and establishment of programs that involve collaboration between industry and academia should be achieved. Accrediting bodies such as, AACSB, EQUIS, should also review their assessment criteria to ensure the incorporation of subjects such as technological competency and sustainable practices in their curriculum. However, in the case of growing and underdeveloped economies, the development of capacity-building programs and faculty development activities should gain importance for improving the implementation of curriculum programs. Regional partnerships and context-sensitive curriculum frameworks are equally necessary to reconcile international standards with local realities, allowing accounting education to advance in a more equitable and sustainable direction.

Recent evidence highlights the importance of digital competencies in the field of accounting education. Students exhibiting technological self-efficacy and digital literacy competency have been shown to exhibit stronger innovation abilities and greater confidence in their usage of the newer technologies (Al-Hattami, 2025). The effective integration of digital technologies and AI systems across the curriculum domain, in accordance with the ethical principles of responsible use, will assist in sustaining the paradigm shift (Müller, 2025). This can be achieved by adopting interdisciplinary methodologies and incorporating accounting education into the more general business and societal environments (Gil, 2025). As the field continues to develop in the wake of globalization and technological advancements, accounting education should strike the appropriate balance between technological literacy and ethical thought as required in the ever-complex world of today (Ballantine et al., 2024; Feltham et al., 2025).

To achieve these multifaceted objectives interdisciplinary courses play a vital role in achieving a comprehensive understanding of sustainability in higher education and the United Nations’ Sustainable Development Goals (SDGs). However, it is not enough for these principles to be included only in the course content. Rather, their implementation at the organizational level in a holistic approach is required. For the fulfillment of the skill deficits identified among the university graduates and for improving the alignment between the education system and the industry demands and societal expectations, the faculty should resort to creative approaches to teaching such as problem-based learning. Transforming accounting education necessitates the integration of technological proficiency, ethical awareness, sustainability orientation and interdisciplinary collaboration. Such transformation requires sustained institutional engagement, progressive accreditation requirements and contextually adapted strategies that reconcile universal standards with regional circumstances.

Footnotes

Author Contributions

All authors contributed to conceptualization of the manuscript. SC extracted, analyzed, and charted the data, and SC validated the result. SC and IY conducted quality appraisal. SC, SC and IY drafted the manuscript. All authors contributed to editing and revision, and approved the manuscript.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting the findings of this study are available from the corresponding author upon reasonable request.*