Abstract

This paper challenges the conventional wisdom that systemic risk is primarily a feature of market downturns. We test the hypothesis that financial fragility intensifies symmetrically at both extremes of market sentiment, uncovering a “smile curve” in risk transmission across China’s financial markets. Using daily data from 2009 to 2025, our multi-stage framework combines bubble detection (GSADF) with dynamic connectedness modeling (TVP-VAR). Our central finding is that total connectedness is significantly elevated not only during extreme bear markets (“fear”) but also, symmetrically, during exuberant bull markets (“greed”). Our robustness analysis suggests distinct mechanisms drive this symmetry: “fear” contagion is significantly amplified by the retail-dominated stock market, whereas “greed” co-movement is a more fundamental feature that persists even within the institutional core of the financial system. These findings imply that macroprudential oversight must be vigilant during periods of market ebullience, not just during crises.

Plain Language Summary

It is widely believed that the greatest danger to a financial system occurs during market crashes, when “fear” causes panic and losses to spread. This study asked a different question: Can periods of market euphoria, or “greed,” create a similar level of system-wide risk? We investigated this in the context of China’s large and influential financial system. We analyzed daily data from 2009 to 2025 for six key Chinese financial markets: stocks, bonds, funds, commodities, gold, and foreign exchange. Using advanced statistical techniques, we measured the level of risk contagion—how shocks in one market spread to others—under different conditions. Specifically, we compared the intensity of this risk-spreading during periods of extreme market fear (crashes), extreme market greed (bubbles), and normal market calm. Our central finding is a “smile curve” pattern. We found that the overall risk of contagion was significantly elevated during both extreme downturns and extreme upturns. This means that the collective “greed” driving a market bubble can make the financial system just as fragile as the “fear” driving a crash. We also identified the stock market as the most consistent net spreader of risk. Finally, we found that this system-wide risk is driven by a mix of global factors (like U.S. interest rates) and domestic economic conditions, and that the influence of these drivers changed after the U.S.-China trade war began. This research shows that financial stability is threatened at both extremes of market sentiment. The key implication for regulators and policymakers is that they must be just as vigilant during market booms as they are during busts. Proactively cooling down an overheating, “greedy” market may be crucial to preventing a future crisis.

Introduction

Financial contagion, the rapid transmission of shocks across interconnected markets, is a defining feature of the modern global economy. An extensive literature documents how crises propagate, showing that during periods of market distress, correlations spike and diversification benefits evaporate as “fear” spreads across assets and borders (Diebold & Yilmaz, 2012; Forbes & Rigobon, 2002). While spillover dynamics in bear markets are well-studied, the literature has less clarity on whether the “irrational exuberance” of asset price bubbles, driven by “greed” and herding behavior, creates comparable systemic vulnerabilities. A central finding in connectedness studies is the asymmetry of spillovers: risk transmission intensifies during downturns, as “bad” volatility shocks have a greater impact than “good” ones (Y. F. Chen et al., 2019; Shahzad et al., 2021; Xie et al., 2023). This focus on a binary crash-versus-calm regime, while insightful, leaves a critical gap. Modern econometric tests robustly identify asset price bubbles (Phillips et al., 2015), but it remains unclear if the associated “greed” generates fragility comparable to that driven by “fear.” The hypothesis that systemic risk intensifies at both extremes of market sentiment remains largely untested.

Against this backdrop, China presents a compelling case study (Younis et al., 2025). As the world’s second-largest economy, the stability of its financial system has profound global implications. Its markets possess a distinct institutional structure—including significant state influence, evolving capital controls, and a prominent retail investor base—that can amplify sentiment-driven movements and herding (Guan et al., 2021; Lu et al., 2018). Although numerous studies examine risk spillovers within China (Afsar et al., 2025; Zhao et al., 2023), the literature has not systematically investigated whether these spillovers are symmetric across the full continuum of market regimes. Understanding whether system-wide risk intensifies in both bull and bear markets is critical for designing effective, pre-emptive financial regulation.

This paper addresses this gap by investigating the anatomy of extreme risk transmission across China’s six principal financial markets: stock, bond, fund, goods, gold, and foreign exchange. We use the term “anatomy” to signify a deep analysis of the structure, dynamics, and underlying drivers of the risk transmission network. We seek to answer four primary research questions. First, how does extreme downside risk, measured by Expected Shortfall (ES), propagate across these markets? Second, how does this risk connectedness network evolve, particularly in response to major domestic and global economic events? Third, and central to our narrative, does the intensity of risk spillover depend on the overall market state? Specifically, we test the hypothesis that the relationship is non-linear and forms a “smile curve,” where systemic risk is elevated symmetrically during both extreme bear markets (fear) and extreme bull markets (greed). Finally, what macroeconomic and policy factors drive the aggregate level of this systemic risk?

To answer these questions, we employ a multi-stage econometric framework. First, we use the Generalized Sup-ADF (GSADF) methodology of Phillips et al. (2015) to identify periods of asset price exuberance. Second, we measure time-varying extreme risk using a non-parametric rolling-window Expected Shortfall. Third, the core of our analysis utilizes a TVP-VAR model to map the dynamic connectedness network. To test for state-dependent asymmetry, we apply the connectedness framework to data sorted by market sentiment quantiles. Finally, we use an Adaptive Lasso and Post-Lasso OLS regression to identify the primary macroeconomic drivers of the aggregate risk spillover index.

This paper makes three principal contributions. First, we provide a comprehensive dynamic map of extreme risk spillovers within the Chinese financial system, identifying the time-varying roles of markets as net risk transmitters or receivers. Second, we present novel evidence of a “smile curve” in risk transmission. We find that total connectedness is significantly higher in both the extreme left tail (fear) and the extreme right tail (greed) of market states, challenging the conventional focus on downside contagion. This finding suggests that regulators should monitor for systemic risk not only during crises but also during periods of market euphoria. Third, using a robust variable selection procedure, we identify the key domestic and global drivers of this systemic risk. Our results show that while global factors such as the VIX and U.S. monetary policy are significant, domestic fundamentals like industrial growth and macroeconomic sentiment are also powerful predictors. Furthermore, by analyzing a sub-sample corresponding to the U.S.-China trade war, we document a significant structural shift in these drivers, with external trade variables gaining prominence.

The remainder of this paper is organized as follows. Section “Literature Review” reviews the relevant literature. Section “Institutional Background and Stylized Facts” outlines the institutional background of China’s financial markets. Section “Data and Methodology” details the data and our multi-stage methodology. Section “Empirical Results” presents the empirical results. Section “Discussion” discusses the findings. Finally, Section “Conclusion” concludes.

Literature Review

This study is situated at the intersection of three research streams: the measurement of dynamic financial connectedness, the analysis of spillover asymmetry, and the econometric detection of asset price bubbles. By synthesizing these areas, we motivate our central hypothesis: systemic risk exhibits a symmetric “smile curve,” intensifying during periods of both extreme market distress (fear) and speculative exuberance (greed).

Measuring Dynamic Financial Connectedness

The literature on financial contagion has evolved from static correlation analysis toward dynamic connectedness frameworks based on vector autoregressions (VAR) (Diebold & Yilmaz, 2009). The state-of-the-art approach frequently employs time-varying parameter (TVP-VAR) models, which capture the evolving nature of market linkages with greater granularity than traditional rolling-window methods and avoid arbitrary window-length choices (Antonakakis et al., 2020; Feng et al., 2023). This methodology produces intuitive, time-varying measures of systemic risk, such as the Total Connectedness Index (TCI), and is now a cornerstone for analyzing risk transmission across diverse assets and markets (Assaf et al., 2025).

Spillover Asymmetry: From Downturns to a “Smile Curve”

A dominant theme in this literature is asymmetry. A large body of work finds that risk spillovers are more pronounced during market turmoil, a phenomenon often modeled by decomposing volatility into “good” (upside) and “bad” (downside) components. These studies consistently find that bad volatility spillovers are significantly larger than good volatility spillovers (Y. F. Chen et al., 2019; Shahzad et al., 2021; Xie et al., 2023). This asymmetry is attributed to investor panic and flight-to-quality behavior during crises (Jin, 2018).

However, this conventional focus on a binary crash-versus-calm regime leaves a critical research gap. It overlooks the possibility of heightened systemic risk during periods of extreme market optimism. Recent evidence has begun to challenge this dichotomy. For example, Assaf et al. (2025) find that return connectedness intensifies during extreme events in both the lower and upper tails. More directly, Li et al. (2024) document an “asymmetric U-shaped pattern of risk spillovers within China’s financial market,” showing that spillovers are larger in the right tail than in the median state. These nascent findings suggest that the “greed” associated with asset bubbles may generate systemic vulnerabilities comparable to the “fear” seen in crashes. While the literature has robustly documented an asymmetry between downturns and normal periods, the hypothesis of a symmetric, U-shaped “smile curve” in risk spillovers—high during both extreme fear and extreme greed—remains largely underexplored. This is the central gap our paper seeks to fill by providing a robust, state-dependent test of this hypothesis.

Econometric Detection of Market Exuberance

To formally test the “greed” side of our hypothesis, we require a rigorous method for identifying periods of speculative exuberance. The state-of-the-art approach is the Generalized Sup-ADF (GSADF) test developed by Phillips et al. (2015). This methodology reconceptualizes the problem as detecting periodically collapsing explosive behavior in a time series and has become the standard for identifying multiple asset price bubbles in real time (Ariza & Ferrer, 2025). By integrating this methodology, we can explicitly link the high-spillover states in the right tail of the market distribution to econometrically identified bubble periods.

The Chinese Context and Our Contribution

China provides a compelling setting to test the “smile curve” hypothesis. Its markets are characterized by high retail investor participation, which can amplify sentiment and herding behavior during both bubbles and crashes (Bu et al., 2019; Lu et al., 2018). While many studies examine risk spillovers in China (Aloui et al., 2022; Zhao et al., 2023), they often focus on specific crises, such as the 2015 stock market crash or the COVID-19 pandemic (Ahmed & Huo, 2019; Ali et al., 2022), rather than systematically testing for asymmetry across the full spectrum of market states. Our paper contributes by integrating these distinct literature streams. We use the TVP-VAR framework to map dynamic connectedness, employ the GSADF test to identify periods of “greed,” and explicitly test for a symmetric “smile curve” in risk transmission, thereby providing a more complete picture of the anatomy of systemic risk.

Institutional Background and Stylized Facts

Understanding risk spillovers in China requires an analysis of its unique institutional landscape. The country’s financial system combines market-based features with significant and persistent state influence. This structure, along with rapid economic development and specific policy events during our sample period, creates a distinctive environment for the generation and propagation of financial risk. This setting provides a compelling case for examining systemic risk dynamics driven by both “fear” and “greed.”

Key Characteristics of China’s Financial Markets

Several features of China’s financial system are particularly relevant to our study of risk transmission. Each feature can amplify the dynamics of both “fear” and “greed.”

First, the Chinese stock market is characterized by dominant retail investor participation. Unlike in developed markets where institutional investors are prevalent, retail investors in China have historically accounted for the majority of trading volume. This composition has profound implications for market dynamics, as retail investors are often more susceptible to sentiment, media narratives, and herding behavior (Guan et al., 2021; Lu et al., 2018). Such behavior provides a direct microfoundation for our central hypothesis, as correlated herding can amplify market volatility during both the rapid inflation of bubbles (“greed”) and panic selling during downturns (“fear”).

Second, the state plays a pervasive role, creating potential moral hazard. The significant presence of state-owned enterprises (SOEs) among listed firms and the dominance of state-owned banks in the financial system can foster an “implicit guarantee” from the government. This perception can distort risk pricing, leading market participants to underprice risk and take on excessive leverage, thereby fueling the “greed” phase of asset price bubbles. During boom periods, strong economic fundamentals combined with these implicit guarantees can foster correlated, fundamentals-based risk-taking among institutional and state-linked actors, providing a distinct mechanism for the “greed” phase of the cycle. The potential for this guarantee to be withdrawn or prove insufficient during a crisis can, in turn, trigger a sharp and systemic repricing of risk, characteristic of the “fear” phase.

Third, China operates with a managed capital account and a controlled exchange rate regime. Throughout our sample period, the capital account was not fully liberalized, a feature documented in studies of Qualified Foreign Institutional Investor (QFII) schemes and Stock Connect programs (Huo & Ahmed, 2018; Yang et al., 2020). This policy insulates the domestic economy from certain external shocks but can also trap domestic liquidity and policy shocks within the system, causing them to reverberate more intensely across domestic markets. This “closed-loop” effect can amplify both booms and busts, rendering the exchange rate itself a potential channel for spillover and a signal of policy intent.

Major Economic and Policy Events

Our sample period covers several critical episodes that have shaped China’s financial risk profile. We view these events not as isolated crises but as real-world manifestations of the fear-and-greed dynamics we investigate. They also serve as natural experiments to test the stability of the underlying risk transmission mechanism.

Illustrative Episodes of the Fear-and-Greed Cycle

Post-2008 Global Financial Crisis Stimulus: In response to the global crisis, China launched a massive credit and fiscal stimulus package. While successful in maintaining growth, this policy led to a rapid expansion of leverage and the growth of a less-regulated “shadow banking” sector, creating the preconditions for a classic “greed”-driven asset boom.

The 2015–2016 Stock Market Turbulence: This period provides a quintessential example of the full fear-and-greed cycle. From mid-2014 to mid-2015, China’s stock market experienced a dramatic, leverage-fueled bubble, driven in part by margin trading (Gao et al., 2018). This bubble was followed by a precipitous collapse, with the market losing over 40% of its value in weeks—a clear display of systemic “fear.” These events serve as key interpretive benchmarks for the dynamic connectedness index we develop.

Exogenous Shocks and a Test for Structural Break

While the 2015 crash was largely endogenous, our sample also includes two major exogenous shocks that imposed different pressures on the system.

The COVID-19 Pandemic (2020): The initial outbreak in China and the subsequent global pandemic represented a massive, synchronized shock to both the real economy and financial markets (Yousfi et al., 2021), leading to a sharp, global risk-off event.

The US-China Trade War (2018 Onward): The imposition of tariffs by the United States marked the beginning of a prolonged period of heightened economic and policy uncertainty (Bissoondoyal-Bheenick et al., 2022).

Both events provide an opportunity to test for a structural break in the drivers of systemic risk. The literature has widely used these shocks as natural experiments to study financial market dynamics. For instance, Ali et al. (2022) examine how the pandemic altered spillovers between oil and stock markets, while Bissoondoyal-Bheenick et al. (2022) focus specifically on how the trade war impacted market connectedness. Following this literature, we leverage these events to assess the stability of the risk spillover network and its drivers.

For our sub-sample regression analysis, we choose the onset of the US-China trade war as the breakpoint. This choice is motivated by the nature of the shock: unlike the sudden, acute shock of the pandemic, the trade war initiated a sustained, multi-year regime of heightened geopolitical and trade-related uncertainty. This makes it a more suitable natural experiment for identifying a potential structural shift in how external factors, particularly trade flows and US policy, influence China’s domestic risk network.

Data and Methodology

This section describes the data, variable construction, and the multi-stage econometric framework we use to analyze risk spillovers within China’s financial system.

Data and Variables

Our analysis uses daily and monthly data from April 2009 to July 2025. The dataset comprises price indices for six core Chinese financial markets and monthly data on a set of domestic and international macroeconomic and policy variables that may drive systemic risk.

Daily Market Data: We proxy six primary markets using the following indices, sourced primarily from the RiceQuant data platform: ○ Stock Market: Shanghai Stock Exchange (SSE) Composite Index (000001.XSHG) ○ Fund Market: CSI Fund Index (H11020.XSHG) ○ Bond Market: ChinaBond Composite Index (H11001.XSHG) ○ Goods Market: CSI Commodity Futures Index (H30009.XSHG) ○ Gold Market: SWS Gold Index (850531.INDX) ○ Foreign Exchange Market: US Dollar to Chinese Yuan exchange rate, sourced from the Federal Reserve Economic Data (FRED) database (Ticker: DEXCHUS).

For the spillover analysis, we compute daily log-returns for each series as

2. Monthly Factors Data: To analyze the determinants of risk spillovers, we use 13 monthly variables that reflect domestic economic conditions, policy stances, and global risk factors. These include industrial value-added growth (industry_2_growth), CPI, M2 growth, consumer confidence (consumer_mood), import/export growth, macroeconomic sentiment, the 10-year/1-year government bond yield spread (interest_gap), the 7-day SHIBOR, China and US economic policy uncertainty indices (Baker et al., 2016), the effective Federal Funds Rate, US M2, and the CBOE Volatility Index (VIX).

Methodological Framework

Our empirical strategy proceeds in five stages: we first identify market fragility and quantify risk, then model its transmission, and finally, explain its underlying drivers.

Stage 1: Identifying Asset Price Bubbles (GSADF)

To detect periods of speculative exuberance, we employ the Generalized Sup-ADF (GSADF) test of Phillips et al. (2015). This method improves upon standard right-tailed ADF tests by using a flexible windowing approach to identify episodes of explosive price behavior. We select this state-of-the-art methodology because its flexible windowing approach is superior to standard right-tailed ADF tests for robustly identifying multiple, non-contemporaneous bubble episodes, which is essential for testing the “greed” component of our hypothesis. The underlying regression model is:

The GSADF statistic is the supremum of the ADF statistics computed across all feasible rolling windows in the sample, providing a robust indicator of asset price bubbles. We derive critical values via Monte Carlo simulation for statistical inference. Having identified periods of market exuberance, we now turn to quantifying the high-frequency risk that propagates through the system.

Stage 2: Measuring Extreme Risk (VaR and ES)

We quantify time-varying market risk using Value-at-Risk (VaR) and Expected Shortfall (ES). VaR at the

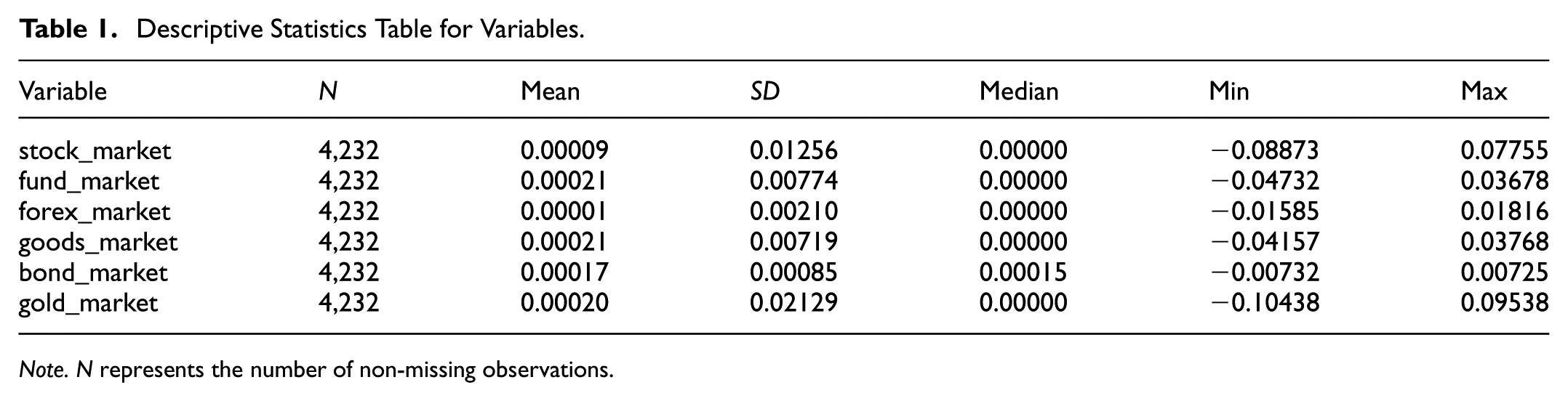

We compute these metrics using a non-parametric historical simulation with a 250-day rolling window, which avoids the potential model misspecification of parametric GARCH models. We use the ES series for our spillover analysis due to its theoretical coherence as a risk measure (Acerbi & Tasche, 2002) and the empirical properties of our data. As the descriptive statistics in Table 1 show, the return series exhibit significant fat tails and negative skewness, making ES more suitable than VaR for quantifying tail risk.

Descriptive Statistics Table for Variables.

Note. N represents the number of non-missing observations.

Stage 3: Modeling Dynamic Risk Spillovers (TVP-VAR Connectedness)

To measure the magnitude and direction of risk spillovers, we employ the dynamic connectedness framework of Antonakakis et al. (2020), which extends the approach of Diebold and Yilmaz (2012, 2014) to a time-varying parameter VAR (TVP-VAR) setting. This approach is chosen over the standard rolling-window VAR to avoid arbitrary window-length selections and to capture the evolving nature of market linkages with greater granularity and responsiveness. The TVP-VAR(p) model is specified as:

where

We then compute H-step-ahead generalized forecast error variance decompositions (GFEVD) to construct the connectedness table. The key measure is the Total Connectedness Index (TCI), which represents the average proportion of the forecast error variance of each market explained by shocks from all other markets. We also compute Net Spillovers for each market, defined as the difference between the gross spillovers transmitted to all other markets and the gross spillovers received from all other markets. A positive net spillover indicates the market is a net transmitter of risk. This dynamic analysis reveals when systemic risk is high. To understand how risk transmission depends on market conditions, we now move to a state-domain analysis.

Stage 4: Analyzing State-Dependent Spillovers (Quantile Rolling Window)

To test our central hypothesis of a “smile curve” in risk transmission, we move from a time-domain to a state-domain analysis. We first construct a proxy for daily market sentiment using the cross-sectional average of returns across all six markets. We then sort the full sample of daily observations according to this sentiment proxy. Finally, we apply the static VAR connectedness methodology of Diebold and Yilmaz (2012) over a rolling window of 500 observations across this sorted data. This procedure allows us to map the TCI to different quantiles of the market state, from extreme bear markets (left tail) to extreme bull markets (right tail), in order to test the smile-curve hypothesis.

Stage 5: Identifying Drivers of Systemic Risk (Adaptive Lasso and Post-Lasso OLS)

In the final stage, we investigate the macroeconomic and policy determinants of the TCI. The TVP-VAR model produces a daily time series for the TCI. To examine its relationship with macroeconomic variables, which are measured at a monthly frequency, we must align the data series. We therefore aggregate the daily TCI to a monthly frequency by taking the average value within each month. This is a standard and necessary procedure in the literature for linking high-frequency financial dynamics with lower-frequency macroeconomic fundamentals (Feng et al., 2023). Given the number of potential regressors (

Empirical Results

This section presents our empirical findings, structured to follow the methodological stages and develop our argument.

Descriptive Statistics and Bubble Diagnostics

Table 1 presents summary statistics for the daily log-returns of the six financial markets under study. The data confirm several stylized facts of financial returns. Mean daily returns for all series are economically and statistically negligible, clustering near zero. However, volatility, measured by the standard deviation, exhibits significant heterogeneity. The gold market (SD = 0.021) and stock market (SD = 0.013) are the most volatile, whereas the bond market (SD = 0.00085) is the most stable.

The statistics also reveal strong evidence of non-normality. The wide ranges between minimum and maximum returns, particularly the large negative returns observed in the stock (Min = −8.87%) and gold (Min = −10.44%) markets, indicate significant negative skewness. The presence of these extreme events indicates that the return distributions are leptokurtic, with fat left tails. These features underscore the inadequacy of risk measures that assume normality and justify our focus on Expected Shortfall, which is designed to capture such tail risk.

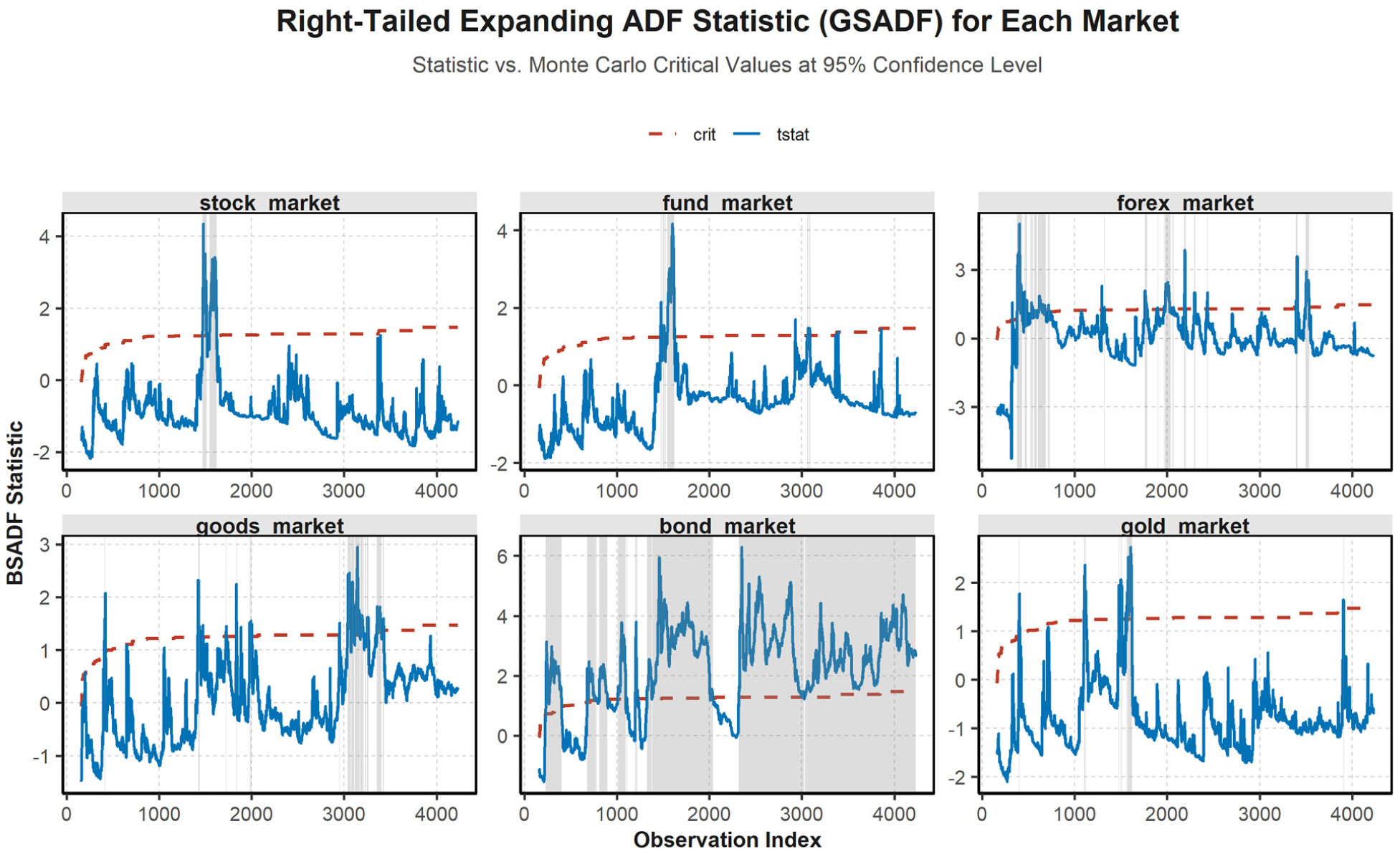

Figure 1 displays the results of the GSADF bubble detection procedure. We identify several statistically significant episodes of explosive price behavior across the markets. The bond, goods, and, to a lesser extent, stock markets exhibit the most pronounced and prolonged periods where the BSADF statistic exceeds its 95% Monte Carlo critical value. These findings provide initial evidence of market exuberance, substantiating the “greed” component of our framework and motivating our investigation into spillovers during both positive and negative market phases.

GSADF test statistics.

Dynamic Risk Connectedness

Figure 2 plots the Total Connectedness Index (TCI), derived from the TVP-VAR model of the Expected Shortfall series. The TCI exhibits significant time variation, fluctuating between approximately 20% during tranquil periods and surging above 80% during major crises. We observe distinct spikes corresponding to significant economic events, including the 2015–2016 Chinese stock market turbulence, the onset of the US-China trade conflict in 2018, and the global financial shock induced by the COVID-19 pandemic in early 2020. This result demonstrates that systemic risk evolves dynamically in response to domestic and global shocks.

Total connectedness index (TCI).

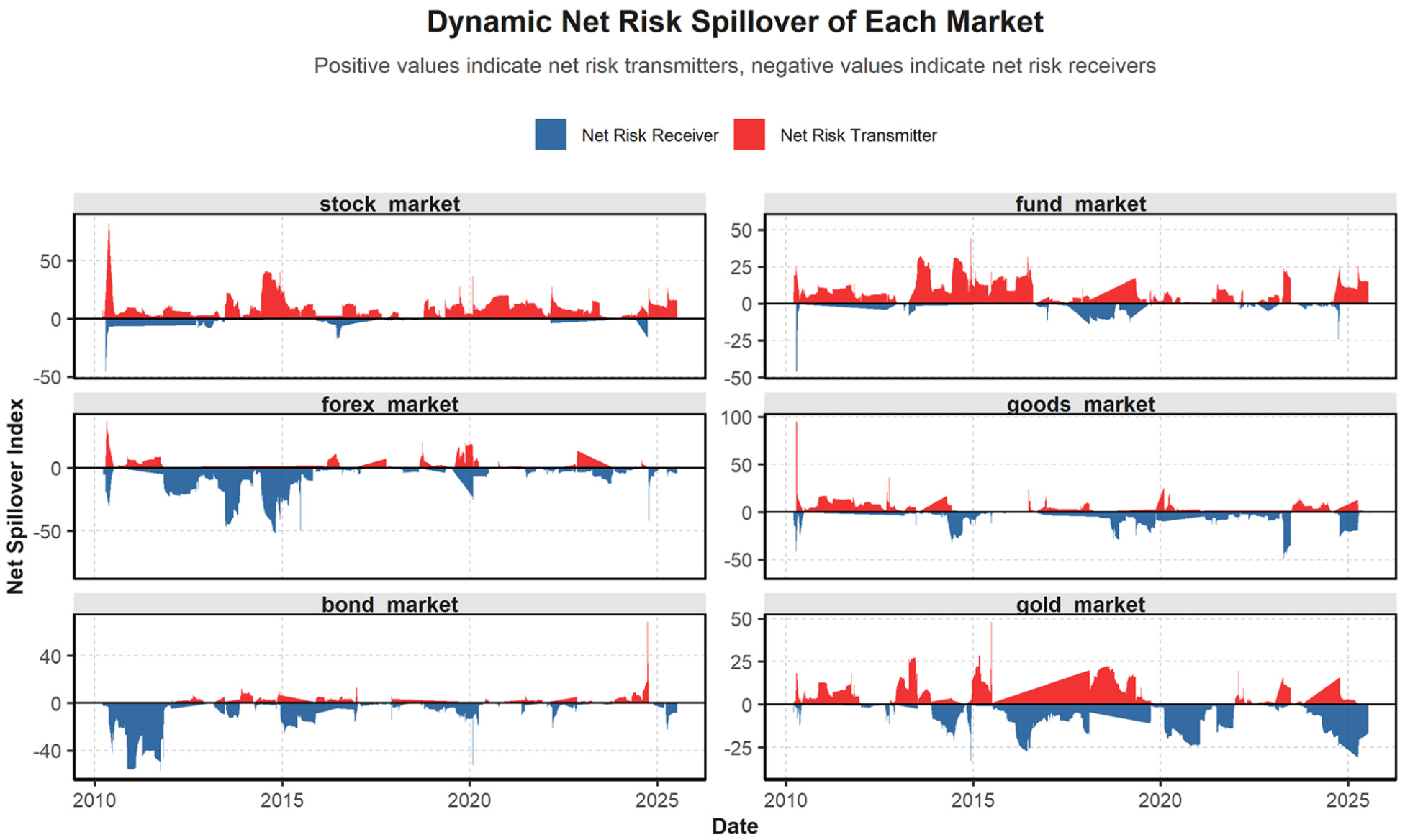

Figure 3 presents the net risk spillovers for each of the six markets. The results reveal distinct network roles for each market. The stock market consistently acts as a net transmitter of risk, particularly during periods of high volatility. Its role as a persistent net transmitter, given its high retail participation, positions it as the likely primary conduit for the behavioral contagion that underpins the “fear” side of our smile curve hypothesis—a conjecture we test explicitly in our robustness analysis. Conversely, the bond and fund markets are predominantly net receivers of risk. The roles of the foreign exchange and goods markets are more time-dependent, as they alternate between being net transmitters and receivers. This detailed decomposition highlights the complex, heterogeneous nature of risk transmission channels.

Dynamic net spillovers for each market.

The role of the gold market is notably volatile. At times, it acts as a net receiver of risk, consistent with its traditional safe-haven status during “fear”-driven shocks like the initial COVID-19 outbreak. At other times, it acts as a net transmitter, likely reflecting speculative activity during commodity price booms—an example of the “greed” dynamic. This dual role underscores the state-dependent nature of asset correlations in China’s financial system.

The “Smile Curve” of Risk Spillovers

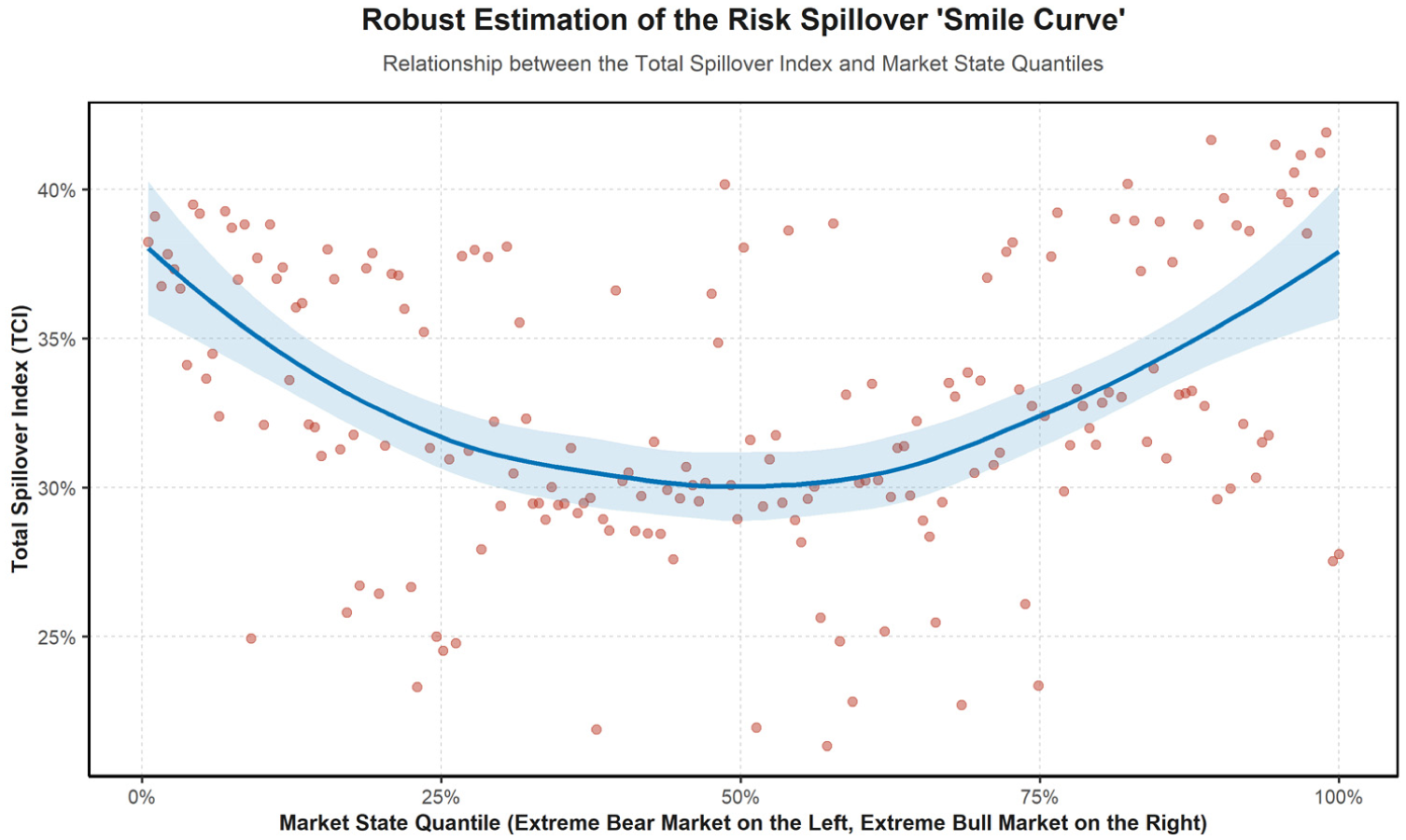

Our central finding emerges from the state-dependent analysis presented in Figure 4. The figure plots the Total Connectedness Index against quantiles of the market state. We uncover a distinct, non-linear, and symmetric U-shaped relationship, which we term the “risk spillover smile curve.”

The smile curve of risk spillovers.

Total connectedness is at its minimum (around 30%) during normal market conditions (the middle quantiles). However, it rises sharply in both tails of the distribution. In the left tail, representing extreme bear markets or “fear,” the TCI approaches 40%. Symmetrically, in the right tail, representing extreme bull markets or “greed,” the TCI also rises to similar levels. This finding contradicts the conventional view that high systemic risk is a feature solely of market crashes. Instead, our results suggest that periods of intense, correlated market euphoria can generate system-wide fragility comparable to that observed during panics.

Robustness Checks

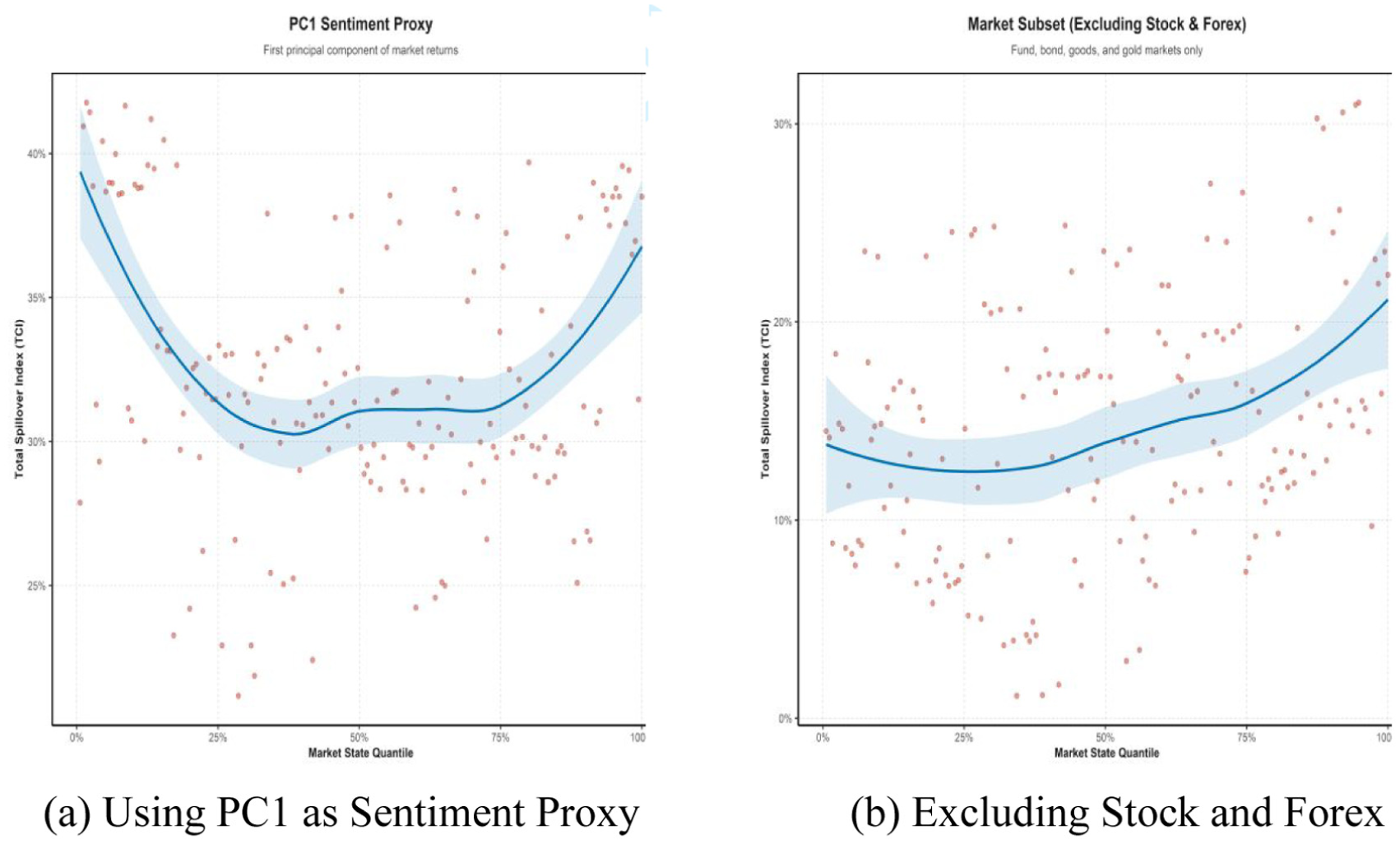

To ensure the validity of our central “smile curve” finding, we conduct two robustness checks designed to test the sensitivity of our results to the sentiment proxy and market composition. The results are presented in Figure 5.

Robustness checks for the smile curve: (a) Using PC1 as Sentiment Proxy; (b) Excluding Stock and Forex Markets.

First, we replace our cross-sectional average return proxy with the first principal component (PC1) of the six market return series. Panel (a) of Figure 5 shows that the symmetric U-shaped relationship is clearly preserved, confirming the result is not an artifact of a specific sentiment proxy.

Second, we conduct a more revealing stress test by excluding the stock and foreign exchange markets and re-estimating the smile curve for the remaining four-market “institutional core” (fund, bond, goods, gold). The rationale is that the stock market, with its dominant retail investor base, is the primary channel for behavioral contagion, while the heavily managed foreign exchange market may not reflect pure market-based risk transmission. The result, shown in Panel (b) of Figure 5, provides a crucial insight into the mechanisms driving the smile curve. The curve becomes asymmetric: the left “fear” tail flattens considerably, while the right “greed” tail remains pronounced.

This is an economically significant finding. The flattening of the left tail after removing the stock market strongly suggests that extreme downside connectedness—that is, fear-driven contagion—is disproportionately amplified by the panic and herding behavior of retail investors. Conversely, the persistence of the right tail suggests that exuberant connectedness— that is, greed-driven co-movement—is a more fundamental feature of the system, driven by correlated institutional responses to strong macroeconomic fundamentals that affect commodity prices, bond yields, and fund flows.

Therefore, this robustness check does more than validate our initial finding; it helps to anatomize it. We find evidence that “fear” contagion is amplified by the retail-dominated periphery of the market, while “greed” co-movement is a more robust feature of its institutional core. This deepens the contribution of the paper by suggesting distinct channels for each side of the smile curve.

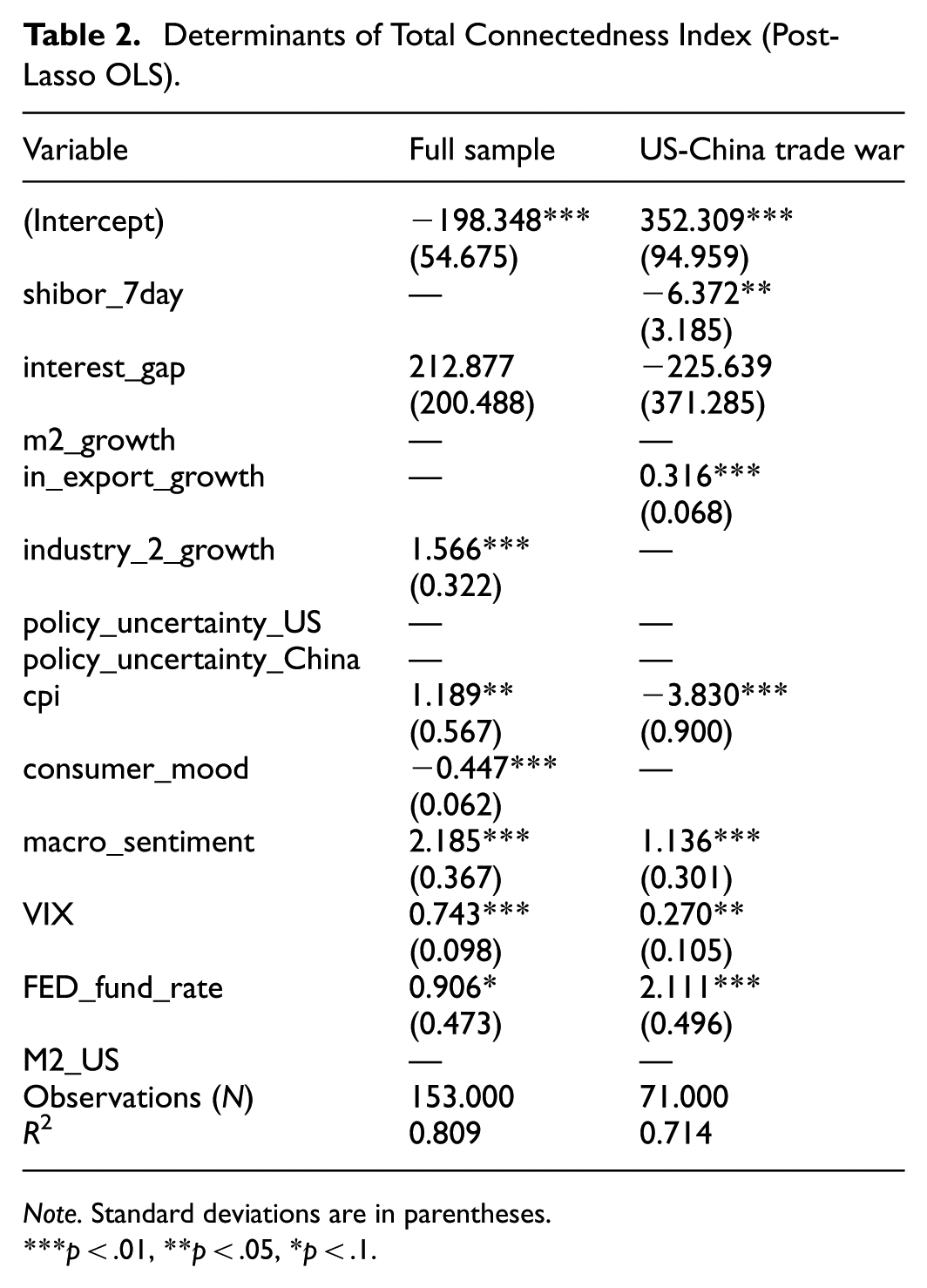

Determinants of Total Risk Spillover

Table 2 presents the results of the Post-Lasso OLS regression explaining the determinants of the monthly TCI for the full sample and for a sub-sample beginning with the US-China trade war.

Determinants of Total Connectedness Index (Post-Lasso OLS).

Note. Standard deviations are in parentheses.

p < .01, **p < .05, *p < .1.

For the full sample, we find that both global and domestic factors are significant determinants of systemic risk. Among global factors, the VIX (coef. 0.743, p < .01) and the FED fund rate (coef. 0.906, p < .10) have a positive and significant impact, confirming that global risk aversion and US monetary policy affect China’s domestic risk network. Domestically, macroeconomic sentiment (coef. 2.185, p < .01) and industrial growth (coef. 1.566, p < .01) are powerful predictors: stronger economic performance is associated with higher connectedness. The positive coefficient on industrial growth may seem counterintuitive; however, it provides strong evidence for the “greed” channel of our hypothesis. Periods of rapid economic expansion can foster investor overconfidence and lead to correlated risk-taking in pursuit of higher returns, thereby tightening the interconnectedness of the financial system. Furthermore, higher inflation (CPI) and lower consumer mood are also associated with heightened risk spillovers.

The analysis for the post-2018 period reveals a structural shift. The influence of global factors intensifies. The FED fund rate becomes more significant (coef. 2.111, p < .01), and import/export growth becomes a highly significant driver (coef. 0.316, p < .01), a factor not selected by the full-sample model. This suggests that during the trade conflict, the financial system became more sensitive to external trade shocks and US policy. Conversely, the significance of some domestic variables, such as industrial growth and consumer mood, disappears, indicating a regime shift in the determinants of systemic risk.

Discussion

Our findings provide a more complete anatomy of risk transmission in China, advancing the literature by moving beyond a simple crash-versus-calm dichotomy. We find that the Total Connectedness Index (TCI) is highly dynamic, a result consistent with the broad TVP-VAR literature showing that market interconnectedness evolves over time and intensifies during crises (Assaf et al., 2025; Feng et al., 2023). However, our central contribution is to show that this intensification is symmetric across both extremes of market sentiment.

The discovery of a “risk spillover smile curve” challenges and refines the extensive literature on asymmetric spillovers. We find, in line with numerous studies (Y. F. Chen et al., 2019; Shahzad et al., 2021), that connectedness rises sharply in the left tail of the market state distribution, confirming that “fear” is a powerful driver of systemic risk. Our novel contribution is the symmetric finding for the right tail. While prior work often contrasts downturns with periods of “calm,” our results suggest this masks a non-linear relationship. We show that systemic risk during periods of extreme market ebullience is just as high as during crashes. This finding provides robust, state-dependent validation for nascent evidence from studies like Assaf et al. (2025) and Li et al. (2024), which also hint at a U-shaped pattern in connectedness. By integrating the GSADF methodology of Phillips et al. (2015), we explicitly link this right-tail fragility to econometrically identified periods of speculative “greed.”

Furthermore, our robustness analysis provides a deeper understanding of the distinct mechanisms driving each side of the smile curve. When we exclude the retail-dominated stock market, the “fear” tail of the curve flattens. This strongly suggests that the classic fear-driven contagion is significantly amplified by the panic and herding behavior of retail investors, a key feature of China’s market (Lu et al., 2018). In contrast, the “greed” tail remains pronounced even within this more institutional market subset. This indicates that exuberant co-movement is a more fundamental phenomenon, driven by correlated institutional risk-taking and responses to strong macroeconomic signals during boom periods.

Our analysis of the macroeconomic drivers provides further evidence for this dual-channel view of systemic risk. The significance of the VIX aligns with existing work confirming the impact of global risk aversion on domestic markets (B. X. Chen & Sun, 2022). More importantly, the positive and significant coefficient on industrial growth, as discussed in our results, provides empirical support for the “greed” channel. It suggests that strong economic fundamentals can fuel correlated optimism and risk appetite, thereby increasing market connectedness. Finally, the structural shift we identify after the 2018 onset of the US-China trade war, where external trade variables become highly significant, reinforces the findings of Bissoondoyal-Bheenick et al. (2022). This result demonstrates that the channels of risk transmission are adaptive and can be fundamentally reshaped by shifts in the geopolitical and economic regime.

Conclusion

This paper investigates the anatomy of extreme risk transmission in China’s financial system, challenging the conventional focus on downside contagion. Our central contribution is the empirical identification of a “smile curve” in risk transmission: we find that systemic risk, measured by total connectedness, is symmetrically elevated during periods of both extreme market distress (“fear”) and speculative exuberance (“greed”). This result suggests that the systemic fragility arising from the correlated euphoria of asset bubbles is comparable to that from panic-driven sell-offs. Our multi-stage econometric analysis confirms the dynamic and heterogeneous nature of China’s risk network, with the stock market acting as a persistent net transmitter. We find that the drivers of systemic risk include both global factors and domestic fundamentals, and we document a structural shift in these drivers following the onset of the US-China trade war. Taken together, our findings provide a more complete understanding of financial contagion by demonstrating that extreme market sentiment itself—whether positive or negative—is a primary source of systemic fragility. We show that fear and greed are symmetric in their capacity to amplify systemic risk, though their underlying channels appear to differ: our evidence suggests that fear-driven contagion is amplified by retail investor panic, while greed-driven co-movement is a more fundamental feature of the institutional core.

Policy and Practical Implications

Our findings have significant and actionable implications for policymakers, regulators, and investors.

For Policymakers and Regulators: The “smile curve” of risk spillovers provides a crucial insight for macroprudential oversight. This finding implies that systemic risk monitoring should not be confined to crisis periods; regulators must also be vigilant during periods of market euphoria. Our results suggest that macroprudential authorities should consider incorporating real-time bubble surveillance metrics, such as the GSADF statistics employed here, into their financial stability dashboards. A sustained period of elevated GSADF statistics could trigger targeted policy responses, such as stricter loan-to-value ratios for mortgages or increased margin requirements for stock trading, to cool exuberant markets before they generate systemic fragility. Furthermore, the identified structural break in risk drivers suggests that regulatory models must be dynamic and adaptive, capable of recalibrating as the economic and geopolitical environment changes.

For Investors and Risk Managers: Our results show that diversification benefits are most likely to evaporate when needed most: at the extremes of the market cycle. The sharp increase in connectedness during both crashes (“fear”) and bubbles (“greed”) indicates that traditional portfolio allocation strategies based on normal-period correlations will likely fail to provide adequate protection. Risk managers should incorporate state-dependent correlation and spillover models into their frameworks. The finding that the stock market is a primary net transmitter of risk suggests that hedging strategies should pay particular attention to spillovers originating from the equity market.

Limitations and Avenues for Future Research

We acknowledge several limitations that suggest avenues for future research. First, our analysis is conducted at the aggregate market-index level. Although this provides a clear macroeconomic perspective, it abstracts from the heterogeneity at the firm or institutional level. Future research could apply the “smile curve” framework to micro-data to investigate whether systemically important financial institutions (SIFIs), as identified by methodologies such as those in Fan and Zhao (2022), contribute differently to spillovers during fear versus greed cycles.

Second, our core analysis relies on a single risk measure, Expected Shortfall, derived from financial returns. While theoretically coherent and empirically justified, this measure does not capture all facets of risk, such as credit or liquidity risk, which may propagate through different channels. Integrating alternative risk measures, perhaps from the credit default swap market or interbank lending networks, could provide a more holistic view of the spillover landscape.

Finally, although our paper documents the “smile curve” and connects it to narratives of fear and greed, a deeper exploration of the underlying transmission mechanisms is warranted. Future studies could employ more granular data, such as order book information or investor-level account data, or utilize theoretical frameworks like agent-based models to more explicitly model the behavioral dynamics of herding and panic that likely underpin our findings. Such research would further illuminate the anatomy of fear and greed in driving systemic risk.

Footnotes

Acknowledgements

We would like to express our deepest gratitude to professor Wang YongMao and Wang Jia for their invaluable help and support throughout this research.

Ethical Considerations

No human or animal studies were carried out by the author for this article.

Consent to Participate

This study did not involve human subjects or personal data collection.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by Zhejiang Province Public Welfare Technology Application Research Project (Grant No. LGF22G010002), and the Humanities and Social Science Fund of Ministry of Education of China (Grant No. 18YJC790131).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Declaration of Generative AI and AI-Assisted Technologies in the Writing Process

During the preparation of this work the authors used Gemini 2.5 pro in order to translate and polish text. After using this tool, the authors reviewed and edited the content as needed and take full responsibility for the content of the publication.