Abstract

At the critical juncture of innovation-driven transformation, the inherent characteristics of “high specialization, high innovation, and light assets” among Specialized, Refined, Distinctive, and Innovative (SRDI) enterprises render their green technological innovation subject to a structural dilemma, namely, excessive internal capital consumption coupled with constrained access to external financing channels. The promulgation of the Intellectual Property Pledge Financing (IPPF) pilot policy has introduced a novel pathway to address this challenge. Drawing upon a sample of SRDI enterprises from 2010 to 2024, leveraging the IPPF pilot policy implemented in 2016 as a quasi-natural experiment, this study constructs a high-dimensional two-way fixed-effects model in conjunction with a difference-in-differences (DID) framework to examine the policy’s impact on green technological innovation. The empirical results reveal that the IPPF pilot policy significantly enhances the green technological innovation capacity in SRDI enterprises; Mechanism analyses reveal that the IPPF pilot policy empowers green technological innovation primarily by alleviating financing constraints. Moreover, fintech not only moderates the relationship between the IPPF pilot policy and financing constraints, but also positively moderates the mediating effect of financing constraints in the linkage between the IPPF pilot policy and green technological innovation. Heterogeneity analyses show that the promotive effect of the IPPF pilot policy on green technological innovation is more pronounced among enterprises located in China’s eastern regions, in environmentally less sensitive industries, and in regions characterized by a higher intensity of intellectual property protection.

Keywords

Introduction

With the promulgation of the 2030 Agenda for Sustainable Development (UN2030) and the convening of the 29th United Nations Climate Change Conference (COP29), addressing climate-related risks and accelerating the global transition toward a green and low-carbon economy have become an unequivocal consensus within the international community. In this context, the green economic growth paradigm has progressively emerged as the central pathway for realizing the Sustainable Development Goals (Xia et al., 2023). In parallel, China’s forthcoming 15th Five-Year Plan further underscores the strategic imperative of advancing a comprehensive green transformation of economic and social development by coordinately promoting carbon reduction, pollution mitigation, ecological expansion, and economic growth (Cui et al., 2024). Consequently, facilitating the transformation of enterprises from a traditional production model predominantly driven by conventional factor inputs toward a development paradigm anchored in green and innovation-oriented factors has become the key to alleviating the paradox of emissions abatement and sustained economic growth. Scholarly inquiry into green technological innovation can be traced back to the socio-ecological movements that emerged in the 1960s, which laid the conceptual foundation for integrating environmental considerations into technological and economic systems. Building upon this intellectual lineage, the European Commission subsequently articulated green technological innovation as an integrated assemblage of pollution-free or low-pollution technologies, processes, and products that, in strict adherence to ecological principles and the fundamental laws of ecological economics, aim to conserve resources and energy, prevent, eliminate, or mitigate environmental pollution and ecological degradation, and ultimately minimize the negative externalities associated with economic activities. By reconciling innovation-driven economic development with ecological transition, green technological innovation embodies a synergistic win-win trajectory and has progressively evolved into an important and rapidly emerging frontier within the new wave of global industrial revolution and technological competition (Khan et al., 2025; Sun et al., 2025).

China’s green technological innovation remains at a stage characterized by an overall relatively low level. In order to overcome constraints arising from deficiencies in key and core technologies, the government has cultivated a group of small and medium-sized “hidden champion” enterprises that possess unique technological capabilities within highly specialized market segments, namely, Specialized, Refined, Distinctive, and Innovative (SRDI) enterprises, which achieve high-quality development through its specialization, refinement, differentiation, and innovation. By concentrating on cutting-edge niche markets and establishing competitive advantages through sustained technological deepening, these enterprises are able to effectively reconcile the balance between ecological environmental protection and high-quality corporate development, and have thus emerged as a principal driving force of green technological innovation (M. Liu et al., 2025). However, owing to the inherent “two-highs-and-one-light” characteristic of SRDI enterprises, namely, high technological investment, high human capital input, and light asset structures, which entail high capital consumption and a scarcity of tangible collateral. These firms face considerable financial pressure during the processes of innovation research and development as well as the transformation of innovation outcomes (Cao et al., 2022). Moreover, in recent years, under the combined influence of financial crises and fluctuations in market demand, investor risk preferences have declined and banks’ credit thresholds have risen, leading to constraints on traditional financing channels and thereby severely restricting SRDI enterprises’ motivation and willingness to engage in green technological innovation.

With the expansion of capital demand accompanying technological innovation, Intellectual Property Pledge Financing (IPPF) has emerged accordingly and has become one of the principal forms of intellectual property–based finance. As early as the beginning of the 20th century, Schumpeter’s Theory of innovation underscored the close and intrinsic linkage between finance and innovation (Cevik, 2025). As a form of private right characterized by clearly defined ownership and exclusivity, intellectual property, in accordance with existing legal provisions, may be transferred, recognized, and pledged, thereby constituting, under current conditions, a novel pathway for stimulating the innovative vitality of SRDI enterprises and for achieving qualitative improvement and quantitative expansion in key green technologies. At the international level, the World Intellectual Property Organization (WIPO) regard intellectual property, particularly green technologies (Dietterich, 2020), as an important instrument for achieving the Sustainable Development Goals. IPPF refers to a financing model in which rights holders pledge the proprietary components of their legally valid intellectual property, including patents, trademarks, and copyrights, which, after valuation, are used as collateral to apply for loans from banks and other financial institutions. As a form of policy reform and financial innovation in practice, the introduction of pilot IPPF policies has provided enterprises with opportunities to “inject vitality” and “empower innovation” (Yu et al., 2022), thereby offering sustained impetus for alleviating the financing pressures faced by SRDI enterprises in pursuing green technological innovation and advancing low-carbon transformation.

This study selects a panel of SRDI enterprises spanning the period from 2010 to 2024, and leverages the implementation of China’s IPPF pilot policy in 2016 as a quasi-natural experiment to empirically assess its enabling effect on green technological innovation. The potential marginal contributions of this study are threefold. First, whereas prior studies predominantly examine the economic consequences of IPPF from the perspective of general technological innovation and its quantity or quality, and often focusing on manufacturing sectors or aggregate firm samples while paying limited attention to green technological innovation, this study situates the analysis within the context of green transition and explicitly targets SRDI enterprises as the focal innovation. By constructing a DID model grounded in green technological innovation, the paper offers a distinctive analytical lens through which to evaluate IPPF pilot policy effectiveness, thereby expanding the applicability boundaries of the existing literature. Second, existing scholarship has rarely integrated IPPF with the development of financial markets and the financing constraints faced by SRDI enterprises to elucidate the underlying transmission mechanisms. By jointly considering these contextual dimensions, this study broadens micro-level enterprises’ understanding of financial market dynamism and green sustainable development, while also providing policy-relevant insights for improving the service chains of financial institutions and exploring more effective financial support pathways tailored to SRDI enterprises. Third, by incorporating firm heterogeneity including regional geographic location, environmental sensitivity, and intellectual property protection the study analyzes the differential effects of IPPF pilot policy implementation. These heterogeneous characteristics provide a multidimensional perspective for tailoring, refining, and safeguarding the design, adjustment, and execution of IPPF pilot policy through the interaction of internal incentives and external environments.

Institutional Background and Theoretical Analysis

Institutional Background

In essence, IPPF represents the transformation of intellectual property into cash flows. As an emerging financing instrument, IPPF has, through long-term promotion across multiple regions, gradually evolved into a variety of region-specific operational models characterized by distinct local features. At the global level, developed economies such as the United States, Japan, and Germany initiated practical explorations into the financial empowerment of intellectual property at an early stage, thereby forming relatively mature and well-differentiated intellectual property financing systems. Within China, regions including Beijing’s Haidian District and Shanghai’s Pudong New Area have actively responded to national intellectual property pilot policies and, by leveraging advantages derived from resource agglomeration, conducted experimental explorations that have given rise to regionally distinctive IPPF models characterized by market dominance, government guidance, bank participation, and institutional guarantees operating in a coordinated manner.

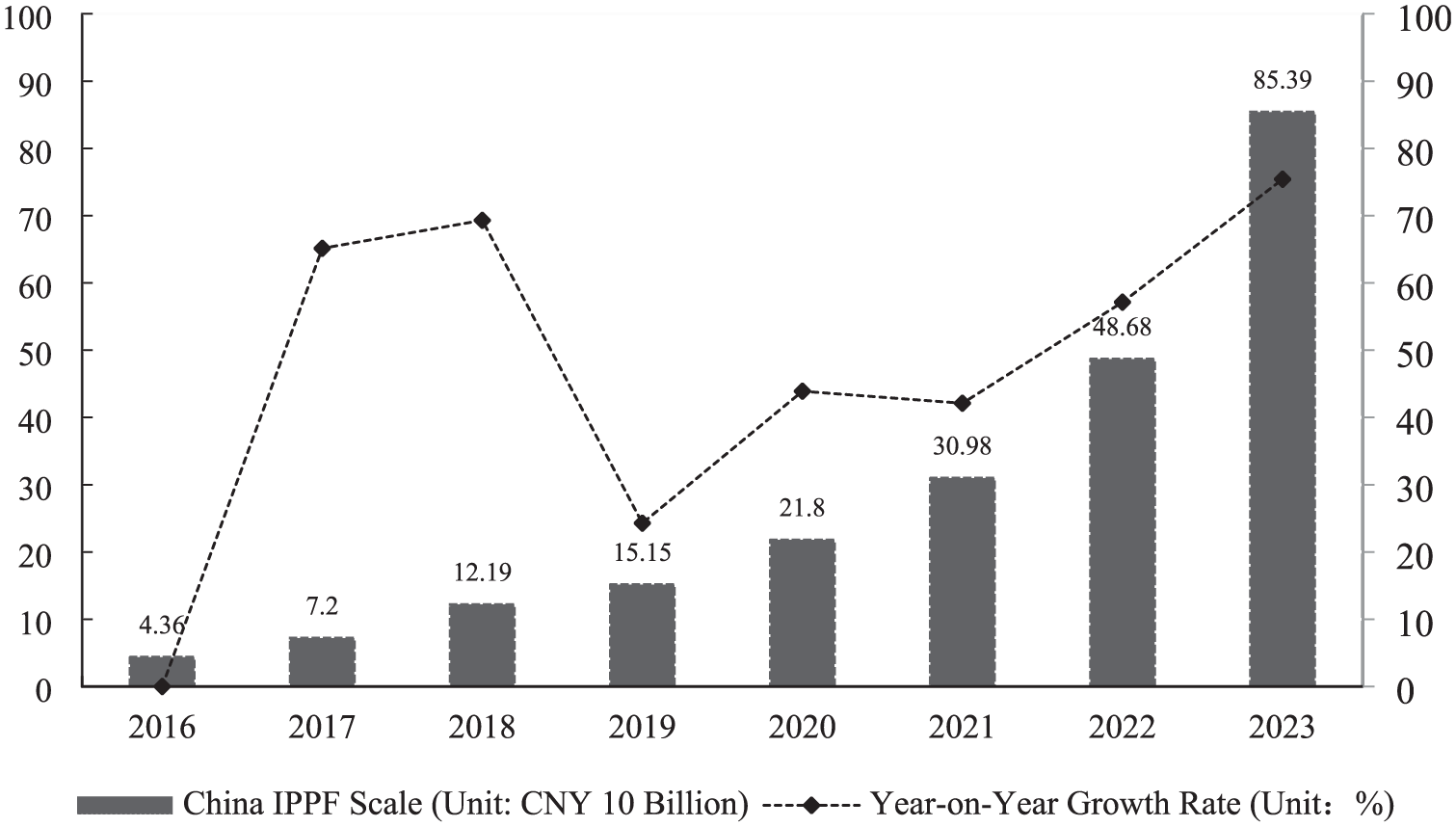

As a sustained policy orientation, China has successively promulgated a series of laws and regulations since 1995, including the Guarantee Law of the People’s Republic of China and the Guiding Opinions on Intellectual Property Pledge Loan Business of Commercial Banks. Beginning in 2008, intellectual property pledge financing pilot programs were gradually launched and implemented in four batches. In 2016, the China National Intellectual Property Administration issued the Notice on Conducting Pilot and Demonstration Programs for Patent Pledge Financing and Patent Insurance in Guangzhou and Other Regions and Institutions, designating 51 pilot and demonstration cities (districts) to carry out a 3-year trial program. With the implementation of the fourth batch of pilots in 2016, the scope of the pilot program has since expanded to more than 70 cities, including Beijing, Shanghai, Guangzhou, Wuhan, Chengdu, and Shenzhen. As intellectual property pledge financing has evolved from a purely market-based transactional activity into a major national strategic initiative, China’s IPPF pilot policy has begun to yield tangible outcomes (Li et al., 2024), with the scale of intellectual property (including patent and trademark pledge) financing experiencing explosive growth over the past decade (as shown in Figure 1). By the end of 2023, the nationwide volume of IPPF reached RMB 853.99 billion, representing a year-on-year increase of 75.4% and benefiting approximately 37,000 enterprises of various types. In parallel, relatively mature intellectual property pledge financing models have taken shape, such as Beijing’s “bank + intellectual property pledge” model and Pudong’s “bank + government fund guarantee + patent counter-guarantee” model.

Scale of intellectual property pledge financing in China.

Theoretical Analysis

IPPF Pilot Policy and Green Technological Innovation of SRDI Enterprises

Institutional Change Theory posits that institutional reforms and governmental policy interventions have the capacity to reshape and enhance regional innovation systems, thereby stimulating firms to pursue high-quality and sustainable innovation activities (Atanassov, 2013). As a derivative financial policy that aligns with the principles of green finance and Environmental, Social, and Governance (ESG) development, Intellectual Property Pledge Financing not only connects with emerging engines of economic growth but also holds the potential to “pay for” green environments and technological breakthroughs, thus catalyzing green technological innovation among SRDI enterprises (Gong et al., 2024).

More specifically, in contrast to tough environmental regulatory measures, the IPPF policy guides capital allocation through relatively flexible mechanisms, thereby generating dual benefits in ecological governance and technological innovation. Through the identification, protection, and utilization of intellectual property, enterprises are able to transform intellectual capital into monetizable assets (Sullivan, 1999), and subsequently internalize the negative externalities arising from corporate pollution emissions via capital allocation, thus steering industrial transformation toward cleaner production and green development objectives (Wang & Wang, 2021). By effectively activating intangible assets and expanding corporate financing channels, the IPPF policy weakens the “crowding-out effect” of productive investment on environmental investment under conditions of constrained financial resources, thereby creating possibilities for the targeted injection of funds into green research and development. When firms allocate such funds toward activities such as hiring highly skilled technical personnel or acquiring green R&D equipment (C. Liu et al., 2019), they are more likely to optimize green production efficiency, develop innovative eco-friendly products and services, and ultimately enhance their green technological innovation capacity (Dutz & Sharma, 2012).

Compared with conventional technological innovation, green innovation exhibits pronounced public and social attributes, in that it simultaneously generates technological spillovers and positive social externalities. This social nature gives rise to a certain degree of investment–return asymmetry, whereby the limited share of public social benefits derived from environmental improvement is insufficient to fully compensate firms for their individual green R&D investments, thereby exacerbating the uncertainty associated with corporate engagement in green research and development (Orsatti, 2024). On the basis of the Institutional Protection Effect, intellectual property, when used as pledged collateral, can, through the processes of intangible asset identification and ownership clarification inherent in pledge arrangements, leverage the exclusivity and monopolistic characteristics of IP rights. Thereby reducing the risk of property rights dilution and infringement faced by firms during the development of green technologies, products, and processes. Mitigates economic losses arising from knowledge spillovers, and enhances, in a private sense, firms’ exclusivity in appropriating market returns from green technological innovation. In this way, the institutional protection effect serves to promote firms’ green technological innovation performance (Heller et al., 2024). Based on the above reasoning, this study proposes the following hypothesis:

The Mediating Role of Financing Constraints

SRDI enterprises play a pivotal role in aggregating technological resources, generating intellectual property, and driving the transformation of the digital economy (Ge et al., 2021), and thus constitute a key category of actors in the development of green technological innovation. Green technological innovation is characterized by substantial upfront capital investment and prolonged return cycles. However, constrained by the “two-highs-and-one-light” attributes of SRDI enterprises, these firms face acute financing demands in the course of pursuing green technological innovation. Conditions of excess demand-excessed and supply-constrained in credit markets, together with credit rationing and credit discrimination, have further restricted small and medium-sized(SMEs) enterprises’ access to financing, thereby exacerbating the impediments to SRDI enterprises’ incentives and willingness to engage in green technological innovation (C. Zhang & Tang, 2022).

Firm’s capacity to obtain and allocate financial resources significantly influences its future green innovation decisions, motivations, and performance outcomes (Shu et al., 2020). Leveraging intellectual property as collateral for financing proves to be no less effective than pledging physical assets in mitigating debt financing constraints and stimulating innovation incentives (Loumioti, 2022). IPPF reshapes the prevailing paradigm of financial development by striking a balance between the adequate protection of investors and the avoidance of excessively stringent and cost-intensive constraints that could otherwise stifle green innovative initiatives. From a direct effect perspective, enterprises may pledge legally owned patents, trademarks, or copyrights in exchange for tangible capital, converting “intellectual assets” into “financial assets,” which directly alleviating financing constraints and creating new momentum and opportunities to engage in green innovation (C. Liu et al., 2019). From an indirect effect standpoint, and based on Signaling Theory, the act of pledging invention patents signals to the market a firm’s solid technological reserves and innovative capabilities. Such signaling not only mitigates credit discrimination typically faced by asset-light firms, but also functions as a form of implicit credit endorsement to attract external investors, assisting market participants make more accurate decisions based on their risk preferences. This process facilitates a more effective matching between investor capital supply and corporate financing demand, thereby expanding financing sources and scales, and promoting firms’ investment in green technological innovation.

Additionally, firms can utilize the valuation outcomes of IPPF transactions to clarify the value of their intellectual property, decrease ambiguity of external R&D information, thereby reduce information opacity and market participants’ perceived risks associated with the firm’s R&D outcomes. This, in turn, channels external capital inward and provides robust financial support for SRDI enterprises to pursue green technological innovation (Hussinger & Pacher, 2019). Based on the above reasoning, this study proposes the following hypothesis:

The Moderating Role of Fintech

Financing Constraint Theory posits that imperfections in capital markets, manifested through information asymmetry and agency costs, generate disparities between internal and external financing costs faced by firms (Levine, 2005; Love, 2003), a divergence that is particularly pronounced among small and medium-sized enterprises (SMEs). The financing difficulties encountered by SMEs constitute the globally persistent and widely recognized “Macmillan Gap,” the essence of which lies in the inherent structural mismatch between the characteristics of SMEs and the traditional financial system.

With the rapid advancement of digital technologies and their progressive penetration into the financial sector, fintech, grounded in information technologies such as big data and artificial intelligence, has been reshaping financial industry application scenarios at remarkable speed, owing to its attributes of convenience and inclusiveness (Gomber et al., 2017). As an organic integration of emerging information technologies and financial services, fintech has broken through the relatively rigid development paradigm of traditional financial services and the highly concentrated allocation of financial credit resources. In doing so, it has, to a certain extent, mitigated the long-standing credit preference for capital-rich firms (Bollaert et al., 2021), compensated for the real-world deficiency embodied in the Macmillan Gap, and incorporated the long-tail groups overlooked by conventional finance, thereby facilitating the downward extension and inclusive provision of financial services in a substantive manner (Arner et al., 2020).

China’s capital market remains at a relatively early stage of development, and the practical implementation of IPPF continues to face multiple challenges. Some scholars have pointed out that, due to excessive reliance on policy incentives and the limited diversity of participating entities, which in turn dampens capital participation incentives, together with the subjective elements inherent in intellectual property valuation, certain enterprises may still be trapped in situations characterized by low financing efficiency and high transaction costs. However, with the empowerment of fintech, the financial ecosystem has increasingly evolved toward a distributed and networked structure. This transformation not only effectively stimulates market vitality and promotes the diversification of market participants (Chuntao et al., 2020), but also alleviates the mismatches across firm attributes, industrial sectors, and development stages that are embedded in traditional financial systems, thereby broadening firms’ financing channels (Tang et al., 2020). In addition, unprecedented improvements in information production and collection efficiency, as well as enhanced ex ante screening and ex post auditing functions, play a critical role in mitigating bilateral information asymmetry and substantially reducing the time and financial costs associated with transactions. These developments undoubtedly facilitate the use of intellectual property as a financing instrument for small and medium-sized firms such as SRDI enterprises (Begenau et al., 2018). Based on the above reasoning, this study proposes the following hypothesis:

The Moderated Mediation Effect

As an important factor influencing firms’ green innovation behavior (Maskus et al., 2019), IPPF represents the outcome of the parallel development of financial capital and property rights markets. According to Innovation Theory, transformations in production technologies and production modes constitute the fundamental driving force of economic development, and the new production modes and organizational forms generated by fintech transformation can effectively activate capital vitality. As a region-specific factor endowment, the deep integration of financial capital and technological innovation is bound to promote the upgrading of the factor endowment structure within the financial industry (Yang & Zhang, 2018). Moreover, the efficient capital allocation and inclusive finance fostered by iterative fintech development are likely to expand exponentially, generating the Multiplier Effect whereby continuous inputs of talent (Domański & Gwosd, 2010), technology, capital, and policy support give rise to economic chain reactions that far exceed the impact of any single financial service itself (Sangwan et al., 2020).

Meanwhile, the Matthew Effect emerging in the process of fintech development tends to concentrate resources and opportunities among individuals or groups that already possess comparative advantages (Wang & Zhao, 2020), thereby reinforcing patterns in which regional economies and technologies exhibit a “strong-get-stronger, weak-get-weaker” dynamic (Frost et al., 2020). Regions characterized by more advanced fintech environments typically possess more standardized and active property rights markets (Zhong & Wang, 2017), enabling them to continuously accumulate resources and, by virtue of first-mover advantages, to accommodate higher-level financing activities such as intellectual property pledge financing. For instance, in regions with well-developed fintech, blockchain and non-fungible token (NFT) technologies (Bao & Roubaud, 2021), owing to their verifiability, transparency, and immutability, can be leveraged to restructure the entire process of rights confirmation and evidence preservation, as well as the pledging and registration of intellectual property pledge financing (Zhao, 2024). This not only ensures the legality of asset sources and ownership for pledgors, but also facilitates the monetization and capitalization of knowledge products, thereby guiding financial and social capital toward technology-oriented SMEs enterprises such as SRDI firms. In doing so, it helps alleviate the structural mismatch between the long development cycles of green technology R&D and short-term debt financing, ultimately providing stable financial support for firms’ sustained investment in green innovation activities. Based on the above reasoning, this study proposes the following hypothesis:

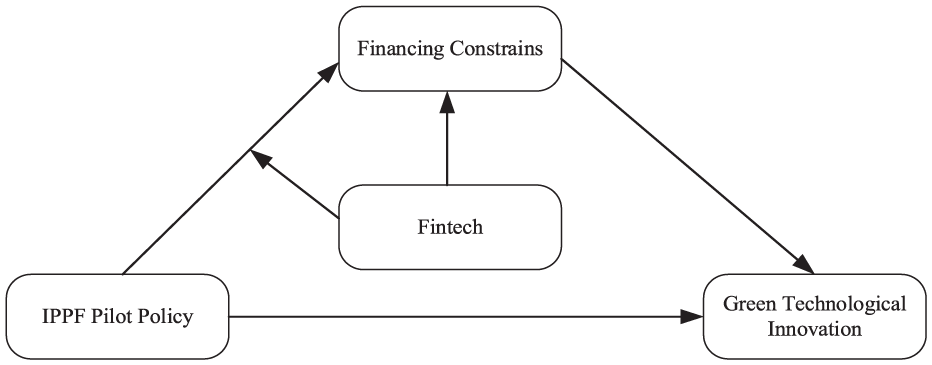

The theoretical model diagram of this study is shown in Figure 2:

Theoretical model diagram.

Research Design

Sample Selection and Data Sources

Given that the pilot programs implemented by the China National Intellectual Property Administration were conducted at different stages of economic and social development, substantial difference exists in their policy content; consequently, pooling multiple pilot programs into a unified empirical analysis may introduce interference and bias into the estimation results. Moreover, the first three batches of IPPF pilots were implemented relatively early and involved a limited number of pilot cities. To more accurately identify the policy effects, this study therefore focuses on the comparatively mature pilot and demonstration program launched in 2016.

The sample is constructed based on the list of four batches of SRDI enterprises by the Ministry of Industry and Information Technology, covering SRDI enterprises over the period from 2010 to 2024. The original data are further screened according to the following criteria: (a) Firms designated as ST or *ST were excluded. (b) Firms that had been listed for less than 1 year, as well as those that had delisted or suspended trading, were eliminated. (c) Firms with missing values in key variables were removed to retain only complete observations. (d) To mitigate the influence of outliers, continuous variables were winsorized at the 1st and 99th percentiles. (e) To address multicollinearity issues in the analysis of moderation mechanisms, all moderating variables were mean-centered.

Firm-level data were obtained from the CSMAR (China Stock Market & Accounting Research) database and the CNRDS (China Research Data Services) platform. Prefecture-level data were sourced from the China Industrial Statistical Yearbook (CISY) and Statistical Yearbook (SY), and the Peking University Digital Financial Inclusion Index.

Variable Definitions

Dependent Variable

The dependent variable in this study is Green Technological Innovation (GTI). In line with the methodology adopted by Wang and Wang (2021), this study measures green technological innovation by the number of green patents filed by listed firms. Specifically, the natural logarithm of the sum of green invention patents and green utility model patents, plus one, is used to construct the variable GTI.

Independent Variable

The independent variable is the Intellectual Property Pledge Financing Pilot Policy (Treatj× Postt). Following the standard DID framework, the implementation of the IPPF pilot policy is captured through an interaction term between a regional policy treatment dummy (Treatj ) and a time dummy for the post-policy period (Postt). The interaction term (Treatj× Postt) equals 1 for firms located in pilot cities during the post-implementation period and 0 otherwise.

Mediating Variable

The mediating variable is Financing Constraints (FC). To quantify firms’ financing constraints, this study adopts the FC index developed by Hadlock and Pierce (2010), a widely used proxy in empirical corporate finance literature.

Moderating Variable

The moderating variable is Fintech (Fintechit). The Peking University Digital Inclusive Finance Index is adopted as a proxy for fintech development, as it systematically measures digital inclusive finance in terms of coverage breadth, usage depth, and the level of inclusive financial digitalization.

Control Variables

To minimize confounding effects and isolate the impact of the IPPF pilot policy on green innovation, several firm-level control variables are included, in accordance with prior literature: firm age (Age), board size (Boards), leverage ratio (Lev), ownership concentration (Top1), separation of ownership and control (Sep). In addition, and following C. Liu et al. (2019), the model also incorporates a regional-level control variable: the tertiary industry’s share of regional GDP (Gdpct3), as a proxy for local industrial development and economic structure. Detailed definitions and constructions of all variables are presented in Table 1.

Variable Definitions.

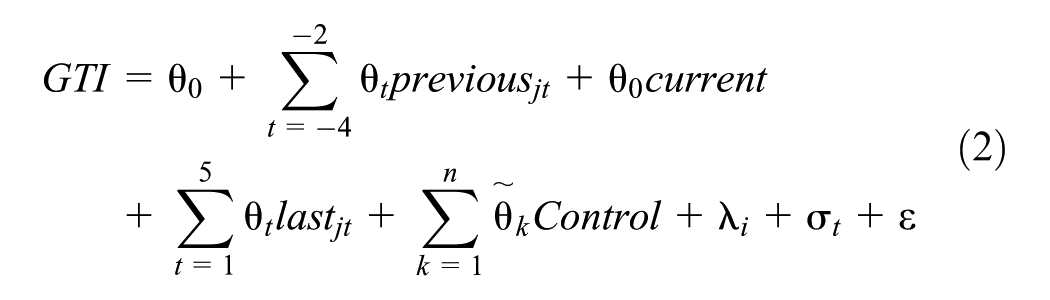

Model Formulation

To empirically test Hypothesis 1, that the IPPF pilot policy exerts a significant influence on the green technological innovation of SRDI enterprises, this study specifies the following econometric model:

Where i denotes the firm, t denotes the year, and Treatj× Postt represents the interaction term between the policy implementation dummy variable and the temporal dummy variable. The term

Empirical Analysis

Descriptive Statistics

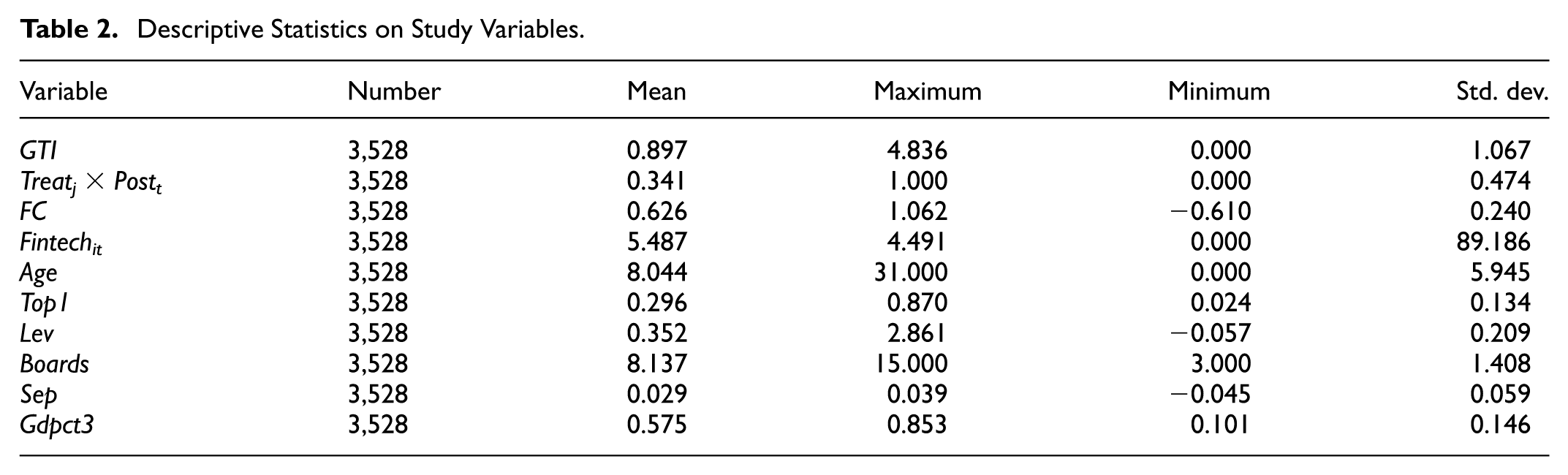

Table 2 presents the descriptive statistics of the key variables employed in this study. Among the 3,528 sample firms categorized as SRDI enterprises, the maximum value of Green Technological Innovation (GTI) reaches 4.836, while the minimum is 0. The binary interaction term Treatj× Postt, designed to capture the treatment effect, has a mean value of 0.341 and a standard deviation of 0.474. The Financing Constraint (FC) index ranges from −0.610 to 1.062, with a standard deviation of 0.240, indicating substantial heterogeneity in financing constraint levels across SRDI enterprises. With respect to control variables, the ownership share held by the largest shareholder (Top1) exhibits considerable variation, ranging from a minimum of 0.024 to a maximum of 0.87, suggesting divergent governance structures among the sampled firms. Furthermore, the level of urban industrialization, measured by the share of tertiary industry in GDP (Gdpct3), ranges from 0.101 to 0.853, with a standard deviation of 0.146, reflecting pronounced regional disparities in the degree of industrial development. The remaining control variables yield results largely consistent with prior literature, and most variables exhibit standard deviations less than one, indicating a relatively high degree of data stability and concentration, thereby enhancing the reliability of subsequent empirical analyses.

Descriptive Statistics on Study Variables.

Dynamic Effects Analysis

One fundamental identifying assumption underlying the Difference-in-Differences (DID) methodology is the parallel trend assumption, which posits that the treatment and control groups should exhibit similar trends in the outcome variable prior to policy implementation. To empirically verify this assumption, this study adopts the event-study approach proposed by Jacobson et al. (1993), constructing the following model for parallel trend testing:

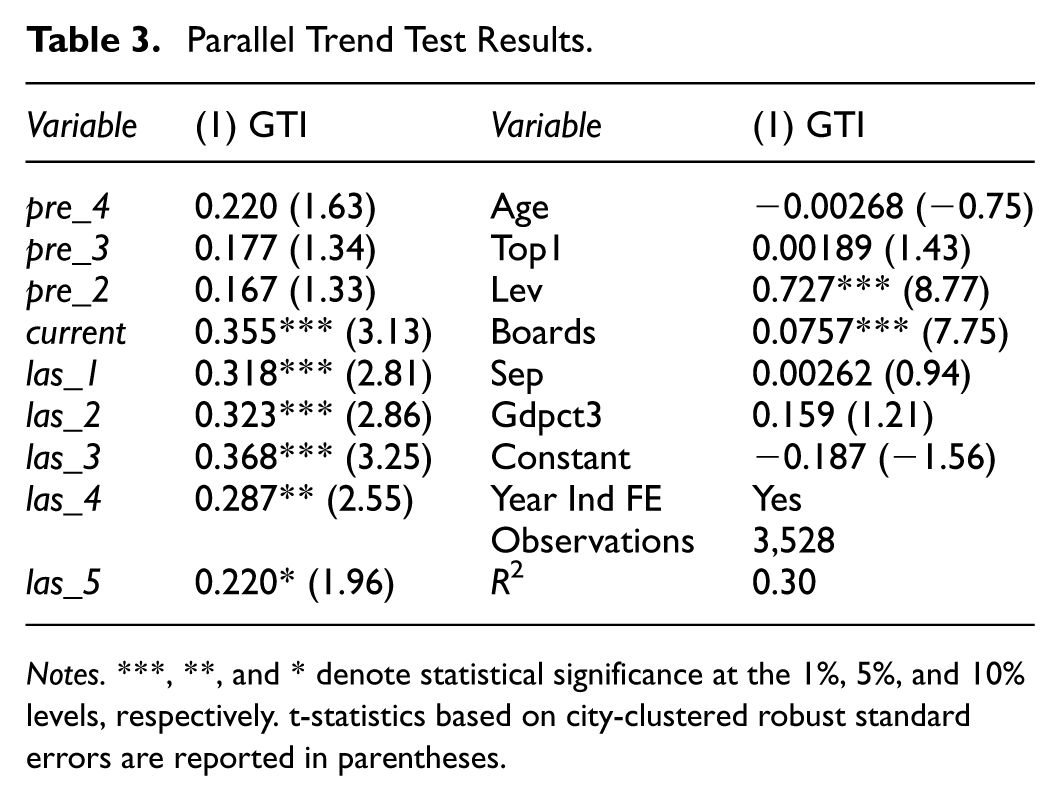

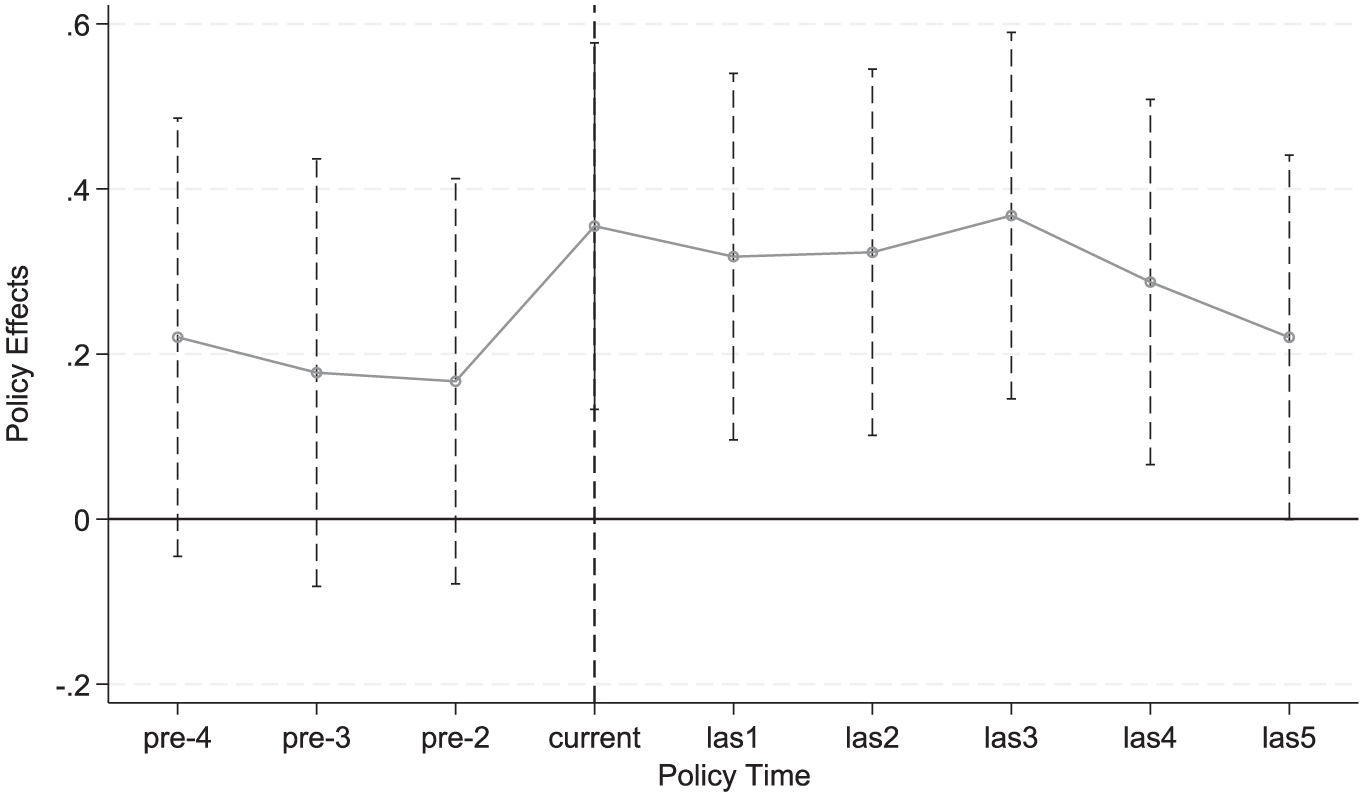

Table 3 shows the parallel trend test results. The estimated coefficients during the prejt period (4 years prior to policy implementation) are statistically insignificant, suggesting that there was no significant difference in the pre-policy trend between the treatment and control groups. By contrast, the coefficients for current and lastjt periods (5 years post to policy implementation) are both significantly positive and display a stable trajectory. We draw a parallel trend test chart to more intuitively reflect policy implementation, as shown in Figure 3, the horizontal axis denoting the timing of the policy and the vertical axis representing the estimated treatment effects, which indicates that the implementation of the IPPF pilot policy has substantially enhanced the level of green technological innovation among SRDI enterprises in the treated regions. Consequently, the parallel trend assumption is satisfied, thereby providing further empirical validation for the core hypothesis of this study.

Parallel Trend Test Results.

Notes. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on city-clustered robust standard errors are reported in parentheses.

Parallel trend chart.

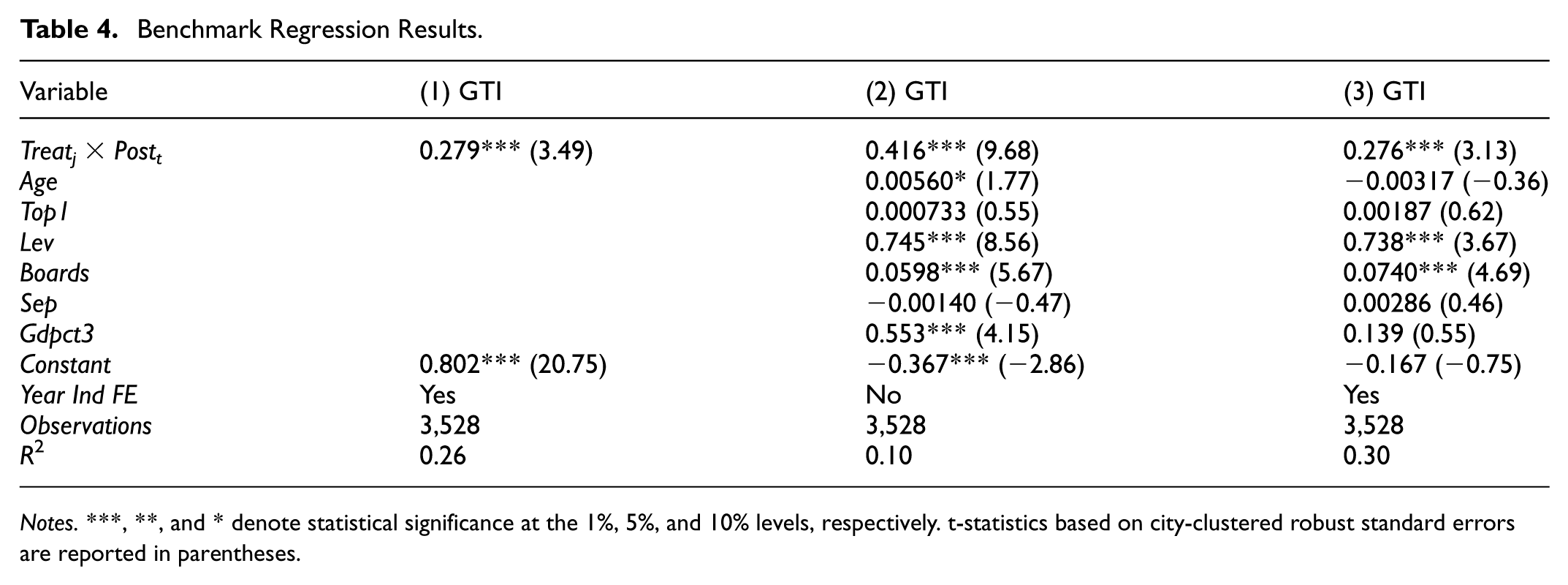

Baseline Regression Analysis

Columns (1) through (3) of Table 4 report the baseline regression results assessing the impact of the IPPF pilot policy on green technological innovation among SRDI enterprises. Column (1) presents the estimates without the inclusion of any control variables, where the coefficient of the interaction term Treatj× Postt is 0.279 and statistically significant at the 1% level, providing preliminary empirical support for Hypothesis 1. In Column (3), after controlling for both firm-level covariates and fixed effects for industry and time, the coefficient of the policy interaction term is 0.276, remaining significant at the 1% level. This robust and positive effect further confirms that the IPPF pilot policy exerts a significant and favorable influence on green technological innovation among SRDI enterprises, thereby validating Hypothesis 1.

Benchmark Regression Results.

Notes. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on city-clustered robust standard errors are reported in parentheses.

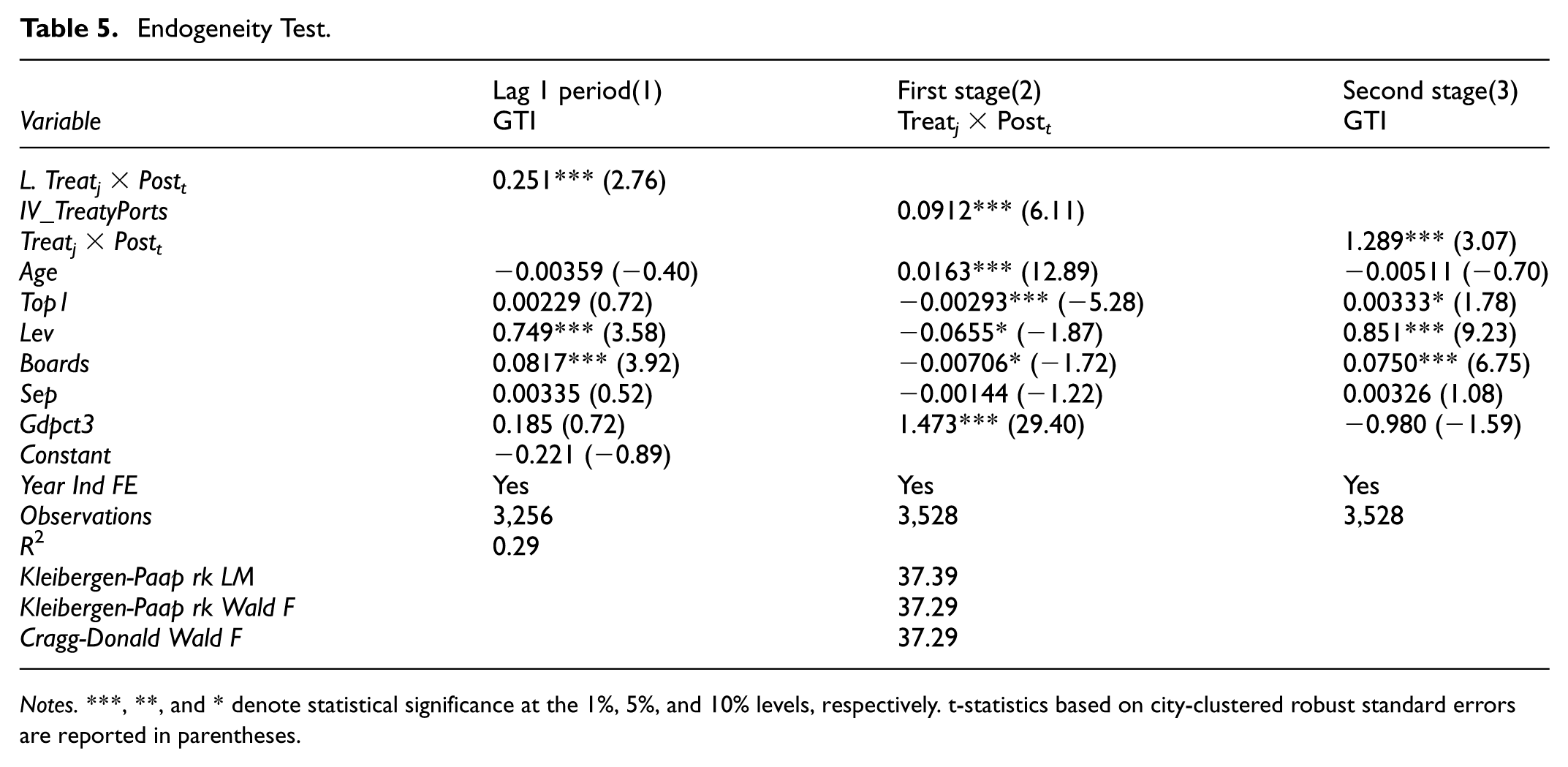

Endogeneity Testing

Lagged Variable

To address potential endogeneity concerns arising from omitted variable bias or sample selection issues, a lagged-variable model is employed wherein the key explanatory variable is lagged by one period. The regression result, presented in Column (1) of Table 5, reveals that the sign and significance level of the estimated coefficient remain largely consistent with those observed in the baseline model. This consistency suggests that the core findings are relatively robust and not unduly influenced by endogeneity stemming from temporal causality.

Endogeneity Test.

Notes. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on city-clustered robust standard errors are reported in parentheses.

2SLS Instrumental Variable

To eliminate potential endogeneity issues arising from reverse causality in the regression model, and following relevant studies (J. H. Zhang & Wang, 2012), this paper employs the Treaty Ports established in the late Qing Dynasty, denoted as IV_TreatyPorts, as an instrumental variable for the explanatory variable in a two-stage least squares (2SLS) regression. As a historical and exogenous institutional shock, the establishment of these Treaty Ports, particularly the five ports and subsequent additional ports following the Treaty of Nanking, represented China’s earliest exposure to modern industry, trade, and finance. Early commercial practices nurtured local business awareness and a spirit of contractual obligation, and this semi-colonial economic environment had a profound impact on regional economic development, thereby establishing a clear historical causal relationship between the Treaty Ports and IPPF, thus satisfying the relevance condition. Moreover, given that these Treaty Ports were products of the Ming and Qing dynasties and that their historical span is extensive, with numerous revolutions and institutional transformations over centuries, they exert no direct influence on green technological innovation, thereby meeting the exclusion restriction.

As shown in Table 5, in the first stage, the Kleibergen-Paap rk LM statistic is 37.39 with a p-value less than .01, indicating strong instrument relevance, and the Kleibergen-Paap rk Wald F and Cragg-Donald Wald F statistics are both 37.29, exceeding the 10% critical value of 16.38, thus rejecting the null hypothesis of weak instruments and insufficient instrument identification. The second-stage regression results reveal that the estimated coefficient of the explanatory variable Treatj× Postt is significantly positive at least at the 1% level, indicating that, after accounting for endogeneity, the IPPF policy still significantly enhances green technological innovation.

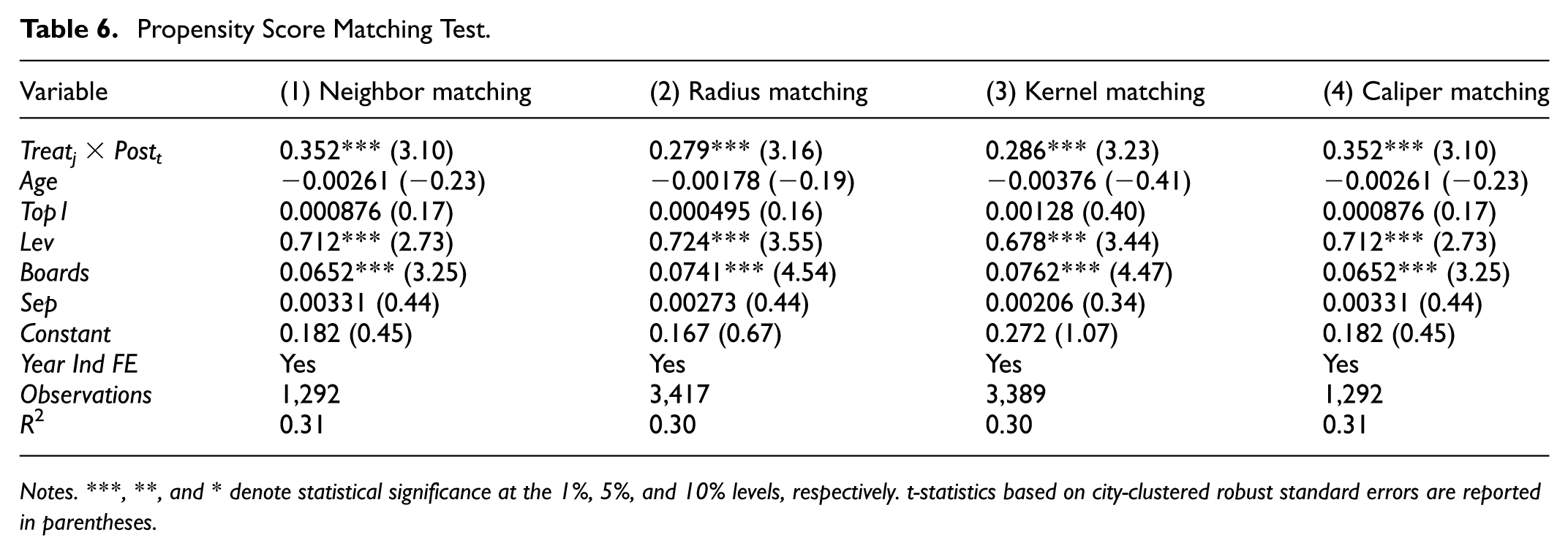

PSM-DID

To further address potential systematic selection bias that may exist between treatment and control groups prior to the policy intervention, such as differences in economic development levels or firm-specific characteristics, this study employs the Propensity Score Matching (PSM) method, following the approach of Rosenbaum and Rubin (1983). This technique enables the construction of a counterfactual control group that is statistically similar to the treatment group in observable characteristics, thus enhancing the robustness of causal inference. Specifically, all firm-level control variables used in the baseline regression are selected as covariates in the Logit model used to estimate the propensity scores. Four matching algorithms are implemented, including 1:1 nearest neighbor matching with replacement, radius matching, kernel matching, and caliper matching with a bandwidth of 0.01. The matched samples exhibit absolute standardized differences below 10%, satisfying the balancing property and indicating high-quality matches. These matched samples are then re-estimated using the baseline DID specification. As reported in Table 6, across all four matching methods, the estimated coefficients for the interaction term Treatj× Postt remain consistently around 0.30 and are statistically significant at the 1% level. These results are closely aligned with those of the baseline model, thereby reaffirming the robustness of the findings. Taken together, after rigorously accounting for sample selection bias and reverse causality, the empirical evidence continues to support Hypothesis 1, that the implementation of the IPPF pilot policy has a significantly positive effect on green technological innovation among SRDI enterprises.

Propensity Score Matching Test.

Notes. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on city-clustered robust standard errors are reported in parentheses.

Robustness Tests

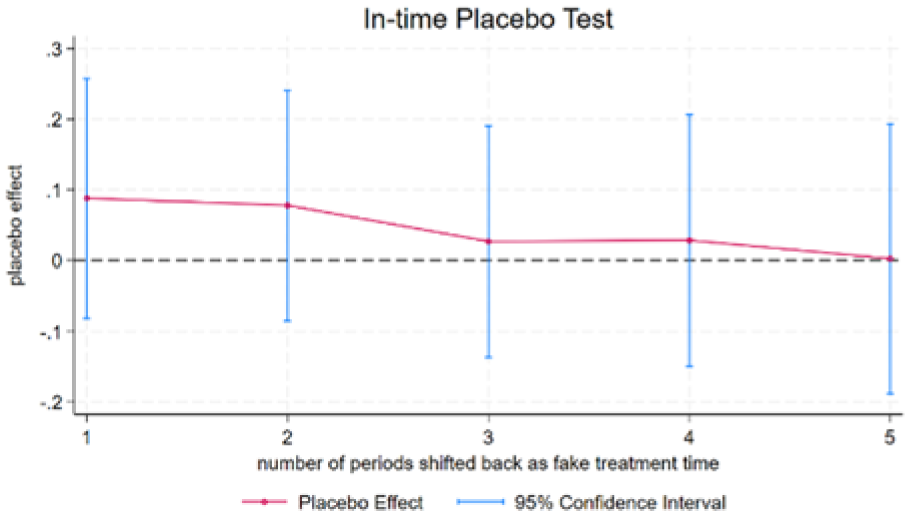

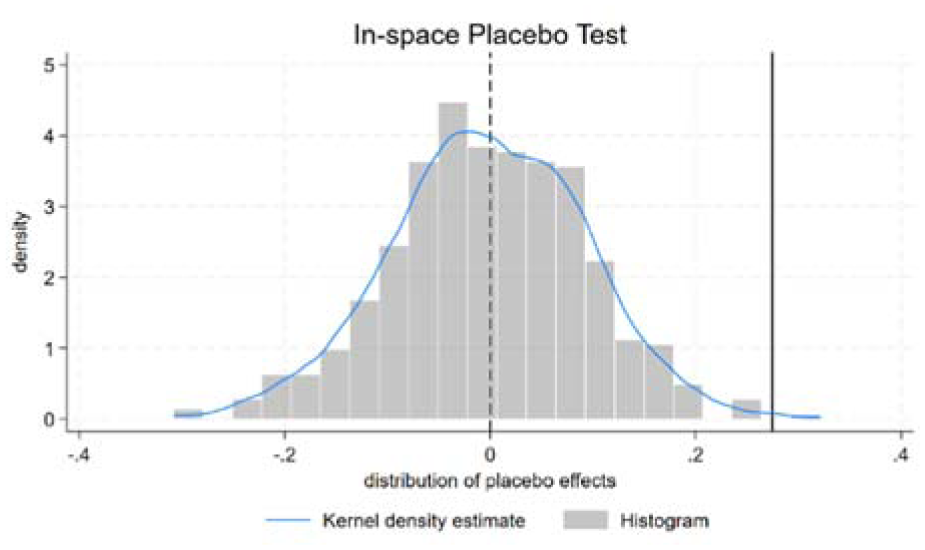

Placebo Test

To further verify the robustness of the empirical results and to rule out the interference of other random or incidental factors, this study follows the methodology adopted in the existing literature (Chen et al., 2025) and employs the didplacebo command to conduct temporal, spatial, and mixed placebo tests, respectively.

In the temporal placebo test, the timing of the policy shock is artificially lagged by 1 to 5 years and treated as a series of “pseudo-treatment periods,” on the basis of which DID estimations are performed. As illustrated in Figure 4, the 95% confidence intervals of the placebo effects all encompass zero, indicating that the estimated placebo effects are statistically insignificant. In the spatial placebo test, the sample is randomly divided, without replacement, into a “pseudo-treatment group,” while the remaining observations constitute a “pseudo-control group.” The kernel density plot in Figure 5 shows that the estimated treatment effect lies in the far right tail of the placebo-effect distribution, representing an extreme value. In the mixed placebo test, “pseudo-treated firms” and “pseudo-treatment timing” are randomly assigned simultaneously for estimation. After repeating the resampling procedure 500 times, the results reported in Table 7 reveal that the two-sided p-value equals .004 (significant at the 1% level), while the right-sided p-value equals .000 (also significant at the 1% level), indicating that the policy effect remains statistically significant even under stringent placebo conditions. Taken together, these findings demonstrate that the empirical results of this study are not driven by chance events and are not contaminated by other random confounding factors, thereby lending strong support to the robustness of the baseline conclusions.

Time placebo test.

Spatial placebo test.

Mixed Placebo Test.

Alternative Regression Specifications

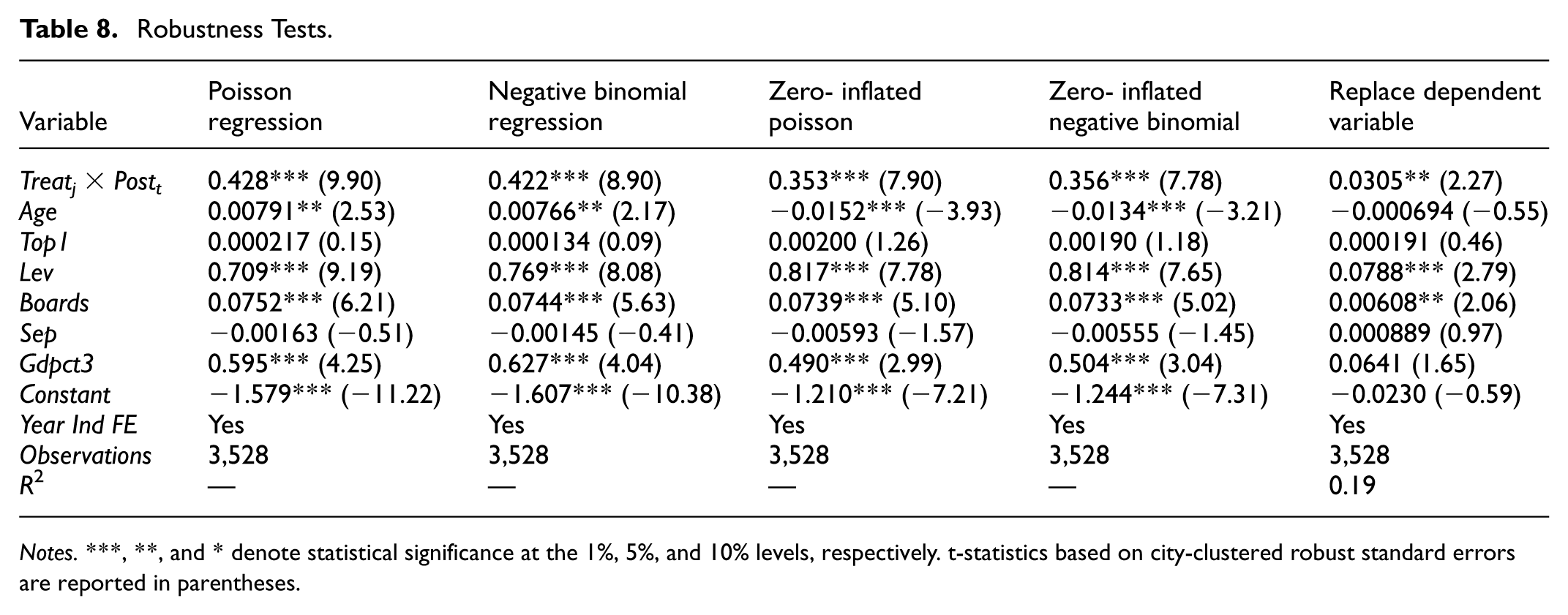

Given that the dependent variable Green Technological Innovation (GTI) is a non-negative discrete count variable, this study further tests the robustness of the baseline findings using count models, specifically the Poisson and Negative Binomial regression frameworks. Considering that a substantial proportion of GTI observations contain a substantial number of zero observations, we implement Zero-Inflated Poisso and Zero-Inflated Negative Binomial models to account for excessive zeros in the dataset, following the approach of Deng et al. (2021). As reported in Table 8, Columns (1) through (4) present the estimation results under the aforementioned alternative model specifications. Across all models, the estimated coefficients for the interaction term Treatj× Postt remain significantly positive at the 1% level, indicating that even after addressing issues related to data distribution and excess zeros, the empirical findings continue to hold. These results collectively affirm the robustness and reliability of the baseline model conclusions.

Robustness Tests.

Notes. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on city-clustered robust standard errors are reported in parentheses.

Replacement of the Dependent Variable

Following related studies, we replace the dependent variable with the ratio of a firm’s green invention patent applications to its total patent applications in the corresponding year, in order to further ensure the robustness of the empirical results. As reported in column (5) of Table 8, after substituting the dependent variable, the estimated effect remains statistically significant at the 1% level, indicating that the baseline findings are robust to alternative measurements of green technological innovation.

Mechanism Analysis

Mediation Mechanism

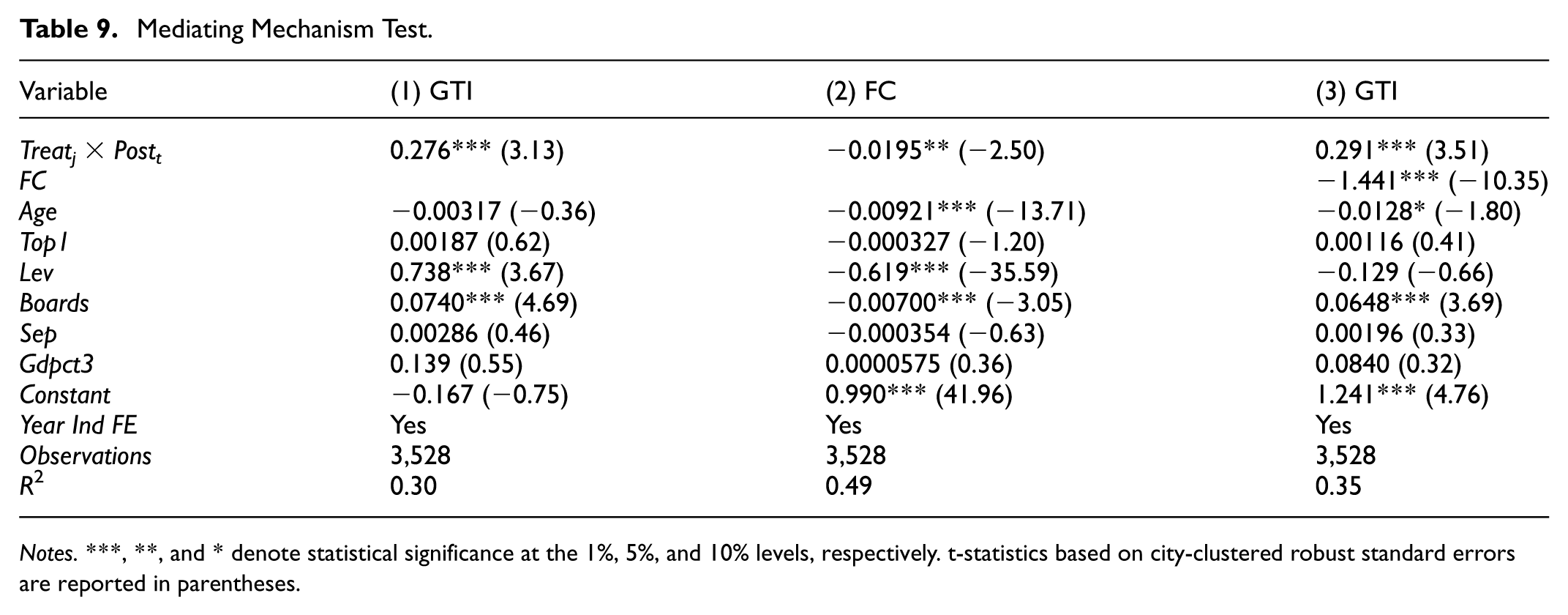

To empirically investigate the mediating role of financing constraints in the relationship between the IPPF pilot policy and the level of green technological innovation among SRDI enterprises, this study draws upon the three-step mediation testing procedure proposed to construct mediation model (3).

In this framework, FC represents the mediating variable, the degree of financing constraints, while all other variables remain consistent with those specified in the baseline regression model. The estimation results are presented in Table 9. Specifically, Column (2) reports the regression of the interaction term (Treatj× Postt ) on financing constraints (FC), yielding a coefficient of −0.0195, which is statistically significant at the 1% level. This result indicates that the IPPF pilot policy effectively alleviates financing constraints faced by enterprises, thereby reducing their cost of capital. In Column (3), the regression results show that the interaction term Treatj× Postt continues to exert a significantly positive influence on green technological innovation (GTI) at the 1% level, while FC is negatively and significantly associated with GTI. These findings collectively suggest that the IPPF pilot policy enhances green innovation capacity among SRDI enterprises by easing their financing constraints, thus providing robust empirical support for Hypothesis 2.

Mediating Mechanism Test.

Notes. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on city-clustered robust standard errors are reported in parentheses.

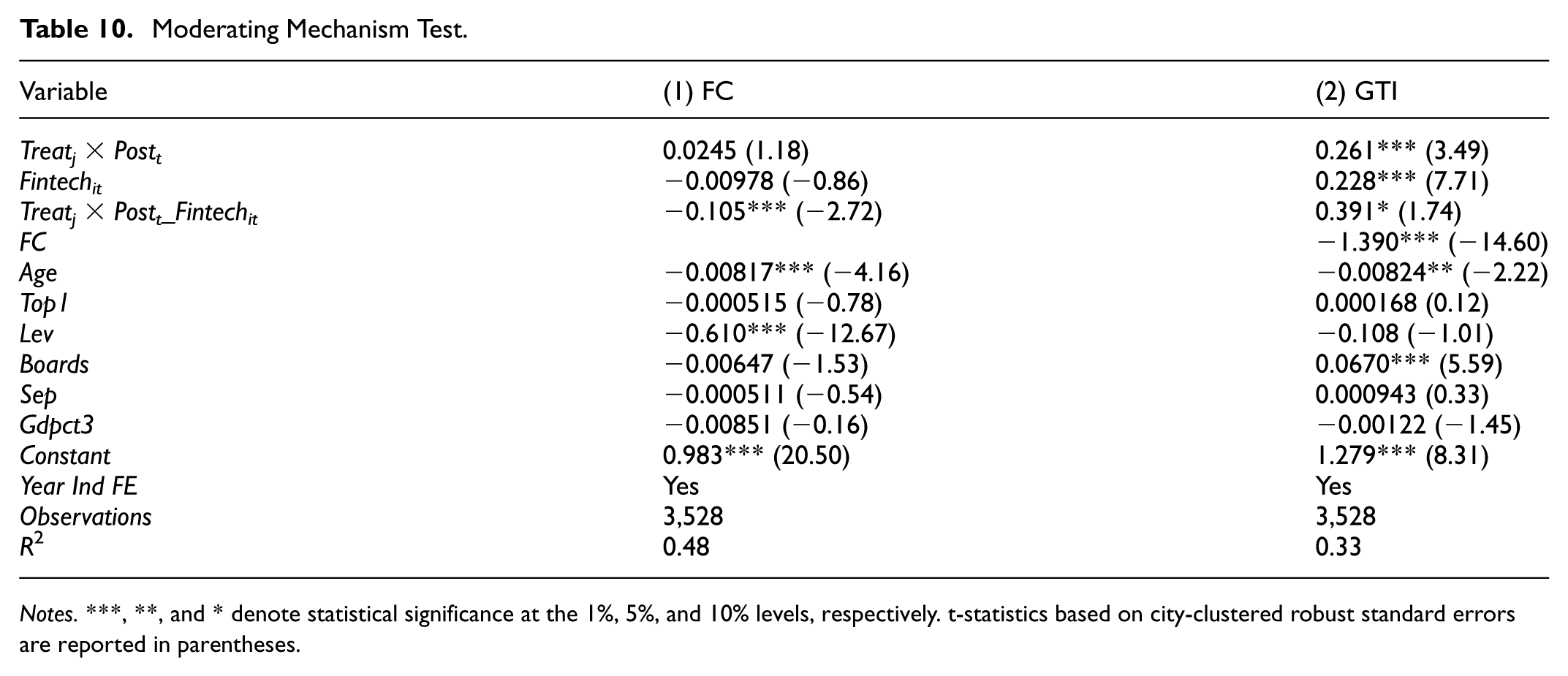

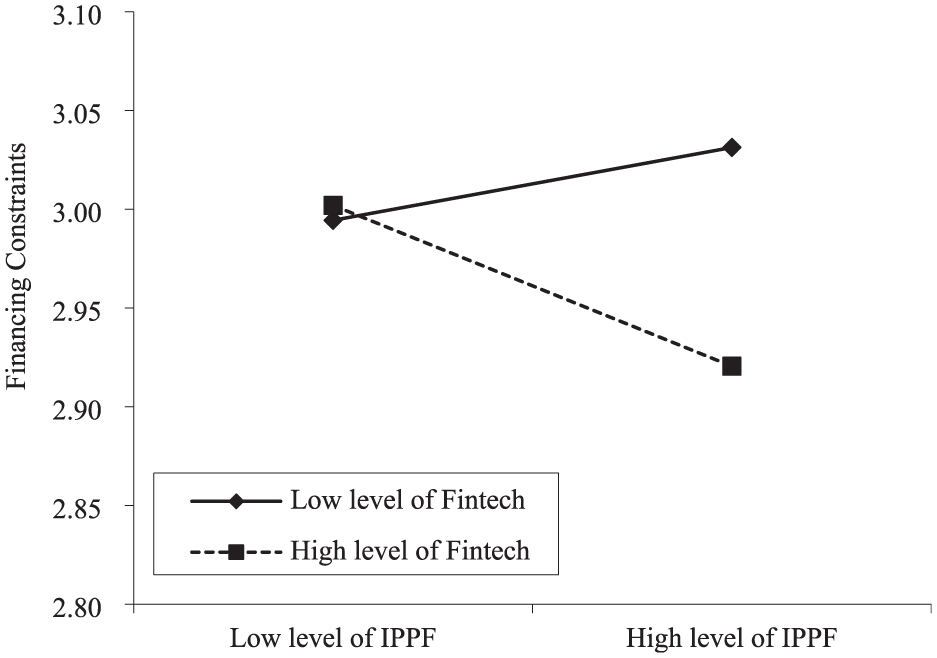

Moderating Mechanism

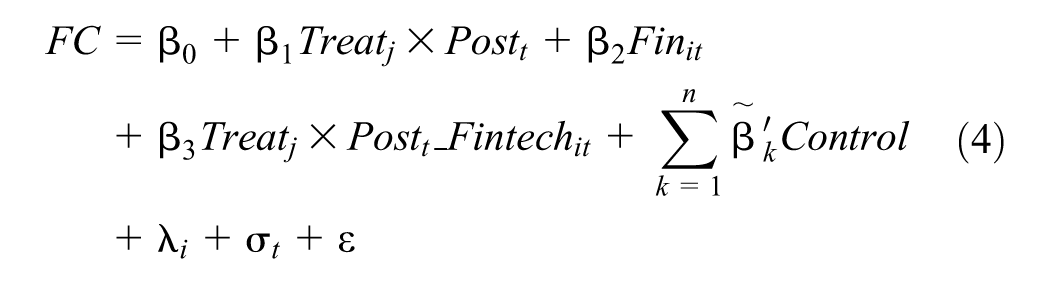

To test whether the level of fintech moderates the relationship between the IPPF pilot policy and financing constraints, this study constructs moderation model (4):

In this model, Fintechit represents the moderating variable, capturing the degree of financial development, and Treatj× Postt_Fintechit denotes the interaction term between the treatment effect and financial development. All other covariates remain consistent with previous regression models. A statistically significant coefficient for this interaction term

Moderating Mechanism Test.

Notes. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on city-clustered robust standard errors are reported in parentheses.

To provide a more intuitive understanding of this moderating effect, a simple slope analysis is conducted. Following standard practice, the sample is stratified into two subgroups based on whether the fintech level is one standard deviation (m ± 1sd) above or below the mean. A marginal effect plot is then generated to illustrate how the IPPF pilot policy’s impact on financing constraints varies across different levels of fintech. As depicted in Figure 6, the negative effect of the IPPF pilot policy on financing constraints intensifies with rising levels of fintech. This visual evidence provides further confirmation of Hypothesis 3 and highlights the critical role of financial market maturity in amplifying the policy’s effectiveness.

The moderating effect of fintech.

Moderated Mediation Mechanism

To further verify the presence of a moderated mediation effect, specifically, whether fintech moderates the mediating role of financing constraints in the relationship between the IPPF pilot policy and green technological innovation. We build upon Model (4) and incorporates analytical frameworks drawn from both domestic and international scholarship to develop an extended moderated mediation model (Model 5).

All variables are defined consistently with the previous models. Following the approach of moderated mediation, if the interaction coefficient

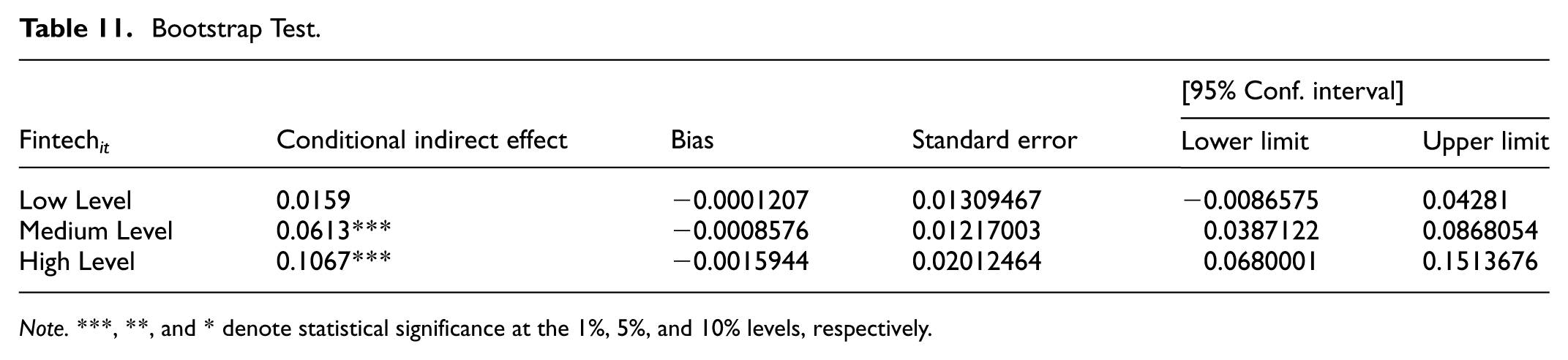

To further substantiate the existence of this moderated mediation effect, a nonparametric Bootstrap approach is employed. Specifically, a bias-corrected (BC) 95% confidence interval is constructed based on 1,000 bootstrap resamples. The conditional indirect effects of the IPPF pilot policy on green technological innovation via financing constraints are estimated at three levels of fintech: low, medium, and high. As presented in Table 11, the conditional indirect effect under a low level of fintech is 0.0159, with a 95% confidence interval of [−0.00866, 0.04281], which includes zero, indicating statistical insignificance. However, under medium and high levels of fintech, the conditional indirect effects are 0.0612 and 0.1067, respectively. Notably, the 95% confidence intervals for these estimates do not contain zero, thereby confirming the statistical significance of the indirect effects at higher levels of fintech. These findings further reinforce the conclusion that financial development exerts a significant positive moderating influence on the mediating effect of financing constraints. That is, as fintech intensifies, the ability of the IPPF pilot policy to alleviate financing constraints is enhanced, which in turn leads to more substantial improvements in green technological innovation among SRDI enterprises. Accordingly, Hypothesis 4 is once again validated.

Bootstrap Test.

Note. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively.

Further Analysis

Additional Mechanism Analysis

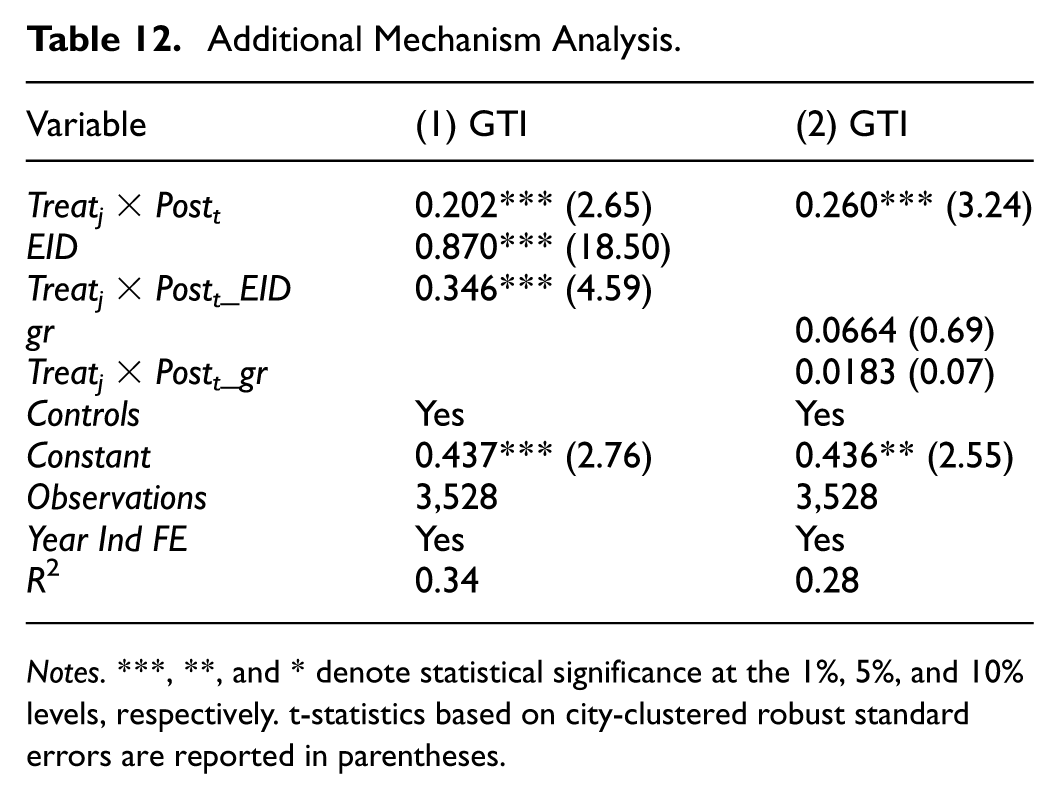

Environmental Information Disclosure

Environmental information disclosure refers to firms’ practices of releasing information related to their environmental performance and environmental governance to external stakeholders. In this study, a binary variable is constructed to indicate whether a firm discloses environmental information (EID). An interaction term between environmental information disclosure and the IPPF policy is then introduced to examine the moderating effect of environmental disclosure on the relationship between the IPPF pilot policy and green technological innovation. As reported in column (1) of Table 12, the coefficient of the interaction term Treatj× Postt_EID is significantly positive at the 1% level, indicating that environmental information disclosure positively moderates the impact of the IPPF pilot policy on green technological innovation.

Additional Mechanism Analysis.

Notes. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on city-clustered robust standard errors are reported in parentheses.

Government Environmental Regulation

With the intensification of governmental environmental governance, firms are increasingly confronted with regulatory pressures in terms of green innovation activities and the legitimacy of their operations. Following related studies, this paper employs data from government work reports and measures the intensity of environmental regulation (gr) as the proportion of the total number of words contained in sentences related to environmental protection relative to the overall word count of each city’s government work report. This indicator is used to analyze the moderating effect of government environmental regulation on the relationship between the IPPF pilot policy and green technological innovation. As shown in column (2) of Table 12, the coefficient of the interaction term Treatj× Postt_gr is 0.0183 but statistically insignificant, suggesting that government environmental regulation does not exert a significant positive moderating effect on the relationship between the IPPF pilot policy and green technological innovation.

Heterogeneity Analysis

Regional Heterogeneity

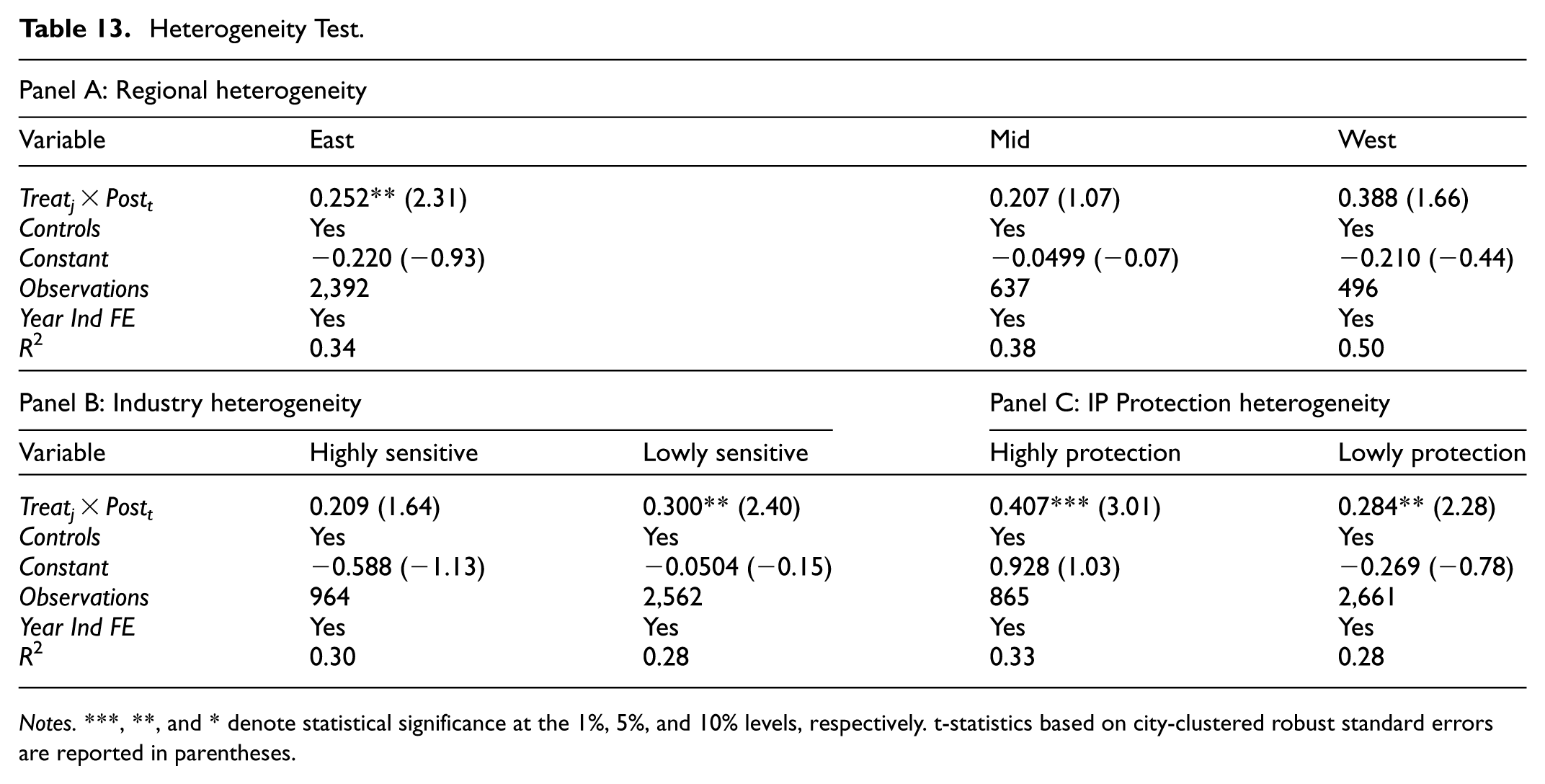

Given China’s vast territorial expanse, pronounced regional disparities persist across areas in terms of economic development levels, resource endowments, and the intensity of policy responsiveness. To examine the regional heterogeneity of the IPPF policy effects on green technological innovation among SRDI enterprises, this study follows the provincial classification of economic zones issued by the National Bureau of Statistics and partitions the sample into three subsamples: eastern, central, and western regions, according to firms’ geographic locations, upon which region-specific regressions are conducted.

The regression results, as reported in Panel A of Table 13, indicate that, compared with the western and central regions, where the estimated coefficients fail to pass conventional significance tests, the eastern region exhibits a more pronounced enhancement effect of the IPPF pilot policy on green technological innovation among SRDI enterprises (p significant at the 1% level).

Heterogeneity Test.

Notes. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on city-clustered robust standard errors are reported in parentheses.

A plausible explanation lies in the fact that the eastern region enjoys marked advantages in both initial endowment conditions and the subsequent development of financial and intellectual property markets, which facilitates effective policy implementation and the amplification of its leverage effects. Following policy support, these regions are better positioned to accelerate the integration of complementary resources and to attract and concentrate diverse innovation inputs. Furthermore, owing to objective differences in local government governance capacity, pilot cities in the eastern region are more capable of developing distinctive intellectual property pledge financing models under policy support, thereby guiding local firms toward green technological innovation. In addition, economic development is inevitably accompanied by regulatory intensification; in particular, under the constraints of high-quality development objectives and the “dual-carbon” targets, eastern regions are subject to stronger environmental regulatory pressure and public scrutiny, prompting local governments to place greater emphasis on advancing green technological innovation. By contrast, although infrastructure conditions in the western region have continued to improve, relatively lagged policy responsiveness and weaker alignment with complementary measures have resulted in a diminished policy transmission effect.

Industry Heterogeneity

Given that a firm’s environmental sensitivity may significantly influence its green technological innovation output, it is worthwhile to investigate whether the incremental effect of IPPF pilot policy on green innovation remains statistically significant within environmentally sensitive industries, such as energy and chemical sectors, which are typically characterized by high pollution intensity. Following the classification framework set forth in the Guidelines for Environmental Information Disclosure of Listed Companies, this study categorizes firms based on the degree to which their production and operational processes impact the environment. Accordingly, industries are divided into two groups: environmentally high-sensitivity industries and environmentally low-sensitivity industries. Subsample regressions are conducted for each group to assess the differential impacts of IPPF pilot policy across industry types. The regression results are reported in Table 13. The findings indicate that the positive effect of IPPF pilot policy implementation on green technological innovation is more pronounced and statistically significant in environmentally low-sensitivity industries (p significant at the 1% level), whereas the effect in high-sensitivity industries is weaker and does not pass standard significance thresholds. A plausible explanation for this divergence lies in the differential cost structures associated with environmental compliance. Firms operating in low-sensitivity industries, such as electronics or telecommunications, are not subject to substantial environmental regulatory costs, which allows them to allocate a greater portion of the liquidity unlocked through IP pledge financing directly toward green R&D initiatives. In contrast, firms in high-pollution industries must dedicate substantial financial resources to pollution control and environmental compliance measures, thereby crowding out potential investment in green technological innovation. As a result, the marginal impact of IPPF on green innovation is diminished in such contexts.

Intellectual Property Protection Heterogeneity

Considering that the intensity of intellectual property protection varies across regions, an important question arises as to whether such differences generate heterogeneous effects in the impact of intellectual property pledge financing on green technological innovation. To address this issue, this study classifies sample firms into two subsamples based on whether the number of intellectual property–related judicial cases concluded in their respective regions is above or below the sample mean, and conducts subsample regressions accordingly.

The regression results, reported in Table 13, reveal that the IPPF pilot policy significantly promotes green technological innovation in both high- and low-intensity intellectual property protection regions. Nevertheless, a comparison of the estimated coefficients shows that the effect size in regions with stronger intellectual property protection (coefficient = 0.407) exceeds that in regions with weaker protection (coefficient = 0.284). This disparity indicates that the IPPF pilot policy exerts a more pronounced positive effect on green technological innovation output in regions characterized by higher levels of intellectual property protection.

Conclusions and Implications

Research Conclusions

Traditional financing mechanisms have proven inadequate in meeting the unique capital needs of SRDI enterprises. In contrast, the emergence of IPPF introduces a transformative pathway for injecting capital vitality into intellectual property assets, thereby facilitating the conversion of intangible assets into practical applications and unlocking their latent economic potential. The effective implementation of IPPF pilot policy not only offers a novel solution to the persistent challenge of financing bottlenecks, but also fosters the strategic integration of intellectual capital, financial resources, and green innovation, empowering enterprises to exchange “intellectual property” for “financial capital” and consequently strengthening their innovation capabilities. Drawing on firm-level data from SRDI enterprises and city-level indicators spanning the period from 2010 to 2024, this study conducts a rigorous empirical analysis to examine the influence of IPPF pilot policy on green technological innovation in SRDI enterprises. The main findings are as follows: (a) The implementation of IPPF pilot policy exerts a statistically significant and positive effect on the green technological innovation performance of SRDI enterprises. This conclusion remains robust across a variety of sensitivity checks and robustness tests. (b) IPPF pilot policy alleviates firms’ financing constraints through both direct capital infusion and indirect financial signaling effects, thereby promoting green innovation activities within SRDI enterprises. (c) Fintech significantly moderates the relationship between the IPPF pilot policy and financing constraints. (d) Fintech positively moderates the mediating effect of financing constraints in the relationship between the IPPF pilot policy and green technological innovation. (e) The positive impact of the IPPF policy on green technological innovation among SRDI enterprises is more pronounced in samples from China’s eastern region, environmentally less sensitive industries, and regions with a high intensity of intellectual property protection.

Policy Recommendations

China’s intellectual property pledge financing system remains at a developmental stage. To further advance the effective implementation of intellectual property pledge financing policies, promote the maturation of financial markets, and enhance the efficiency of green technological innovation among SRDI enterprises, the following policy recommendations are proposed.

Promote the upgrading of intellectual property legislation and judicial protection. It is essential to clarify the financial asset attributes of intellectual property, particularly green patents, as well as their legal status and enforceability as pledgeable assets, to expand the coverage of national intellectual property pledge financing pilot programs, and to accelerate the establishment of a comprehensive, full-chain, and differentiated intellectual property governance system. In parallel, capacity building and governance empowerment in central and western regions should be strengthened so as to enhance the overall effectiveness and equity of intellectual property policies. Taking intellectual property governance as a central lever, policy efforts should prioritize the cultivation of new technologies and new growth drivers to improve the commercialization rate of intellectual property outcomes, while selectively fostering leading green technology enterprises to demonstration and spillover effects.

Optimize the policy environment and cultivate a sound pledge financing ecosystem characterized by government guidance and market dominance. Administrative barriers in intellectual property protection should be dismantled, while the government’s role in “clearing obstacles, building platforms, and channeling financial resources” should be fully leveraged alongside the decisive role of the market in resource allocation. A coordinated allocation mechanism for labor, technology, capital, and data factors should be established to remove barriers to factor mobility and to guide resources away from speculative activities toward the real economy.

Promote the construction of an authoritative intellectual property pledge valuation system to fundamentally address valuation difficulties. This entails establishing specialized institutions for intellectual property valuation, standardizing valuation practices, and embedding professionalism and transparency throughout the entire pledge process, thereby reducing valuation frictions and disputes arising from subjectivity.

Build a multi-tiered risk-sharing market system and improve risk-sharing and compensation mechanisms. Through coordinated collaboration among governments, banks, guarantee institutions, and market participants, risks associated with intellectual property pledge financing can be effectively dispersed and compensated. Government credit endorsement may be used to enhance lending confidence toward enterprises engaging in intellectual property pledge financing, thereby increasing financial institutions’ willingness to participate in such lending activities. In addition, targeted policy preferences may be granted to high-tech enterprises, including income deductions and tax credits, to alleviate financing constraints and to unleash intrinsic incentives for original innovation and breakthroughs in core technologies.

Limitations and Future Research Directions

This study is subject to several limitations that warrant attention. First, due to the inherent time-sensitivity of policy interventions, the analysis primarily focuses on the fourth pilot policy initiative implemented in 2016, while giving relatively limited consideration to the preceding three rounds of pilot programs introduced in earlier years. However, in reality, the implementation of these earlier policies may have exerted varying degrees of influence on the subsequent positive effects of the IPPF pilot policy on green technological innovation among SRDI enterprises. This oversight represents a methodological limitation that future research should aim to address more rigorously. Moreover, corporate behavior in pursuing green technological innovation is shaped by a wide array of external and internal factors, and it would be overly simplistic to attribute such innovation solely to the influence of a single policy instrument, namely, the IPPF policy. There may exist contemporaneous policy interferences or overlapping policy incentives that complicate the causal attribution. Accordingly, future studies should consider employing more refined identification strategies to isolate the net effect of IPPF while controlling for the potential confounding effects of parallel policy regimes. Alternatively, scholars may explore the dynamic interaction between the IPPF pilot policy and other coexisting policies, with a view to understanding whether such interactions exert a synergistic effect that amplifies green innovation outcomes, or conversely, whether they generate unintended counteractive consequences that diminish policy efficacy.

Footnotes

Acknowledgements

We thank the anonymous reviewers’ and editors’ suggestions on revision, which were very important for the improvement of the paper.

Ethical Considerations

This study did not involve human participants or animals. Ethical approval was therefore not required.

Author Contributions

Conceptualization, L.Z. and S.L.; methodology, L.Z. and S.L.; software, S.L.; data curation, S.L. and Q.W.; writing—original draft preparation, L.Z., S.L., and Q.W; writing—review and editing, S.L., K.L.; Resources, K.L.; funding acquisition, L.Z. All authors have read and agreed to the published version of the manuscript.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by The National Natural Science Foundation of China (Grant No.72372106), China Postdoctoral Science Foundation (Certificate No. 2024M752437), Jiangsu Major Project for Philosophy and Social Sciences Research in Universities (Grant No. 2024SJZD059), Jiangsu Major Project for Basic Research in Natural Sciences in Higher Education Institutions (Grant No. 23KJB630005).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Restrictions apply to the availability of these data. Data were obtained from CSMAR, CNRDS, CISY and SY, all of them are available from the authors with the permission of CSMAR, CNRDS, CISY and SY.