Abstract

Migrant remittances constitute a vital financial resource that supports the well-being of recipient households and communities, financing sustainable development in the Global South. Yet, remittance flows are limited by fragmentation in financial systems infrastructure and regulatory frameworks across sending and receiving countries, evidenced by the high transaction costs of remitting to sub-Saharan Africa. Consequently, these limitations drive the persistent uptake of often cheaper but less secure informal remittance forms. The rapid expansion of financial technologies, such as mobile money and Web-based platforms that shape the digitalisation of remittance-sending and -receiving processes, has the potential to address some of these challenges. The transformations within remittance ecosystems introduced by new digital financial technologies warrant a detailed assessment of individual migration corridors. This paper presents a case study of the Ghana–Canada migration and remittance corridor, analysing the adoption of digital remittances and identifying existing barriers. This understudied corridor reflects increased migration flows, expanding immigrant communities with strong transnational linkages, and high remittance participation, despite socio-economic integration barriers faced by racialised immigrants in Canada. The rapid growth of Ghana’s mobile money system further illustrates this digitalisation process.

Introduction

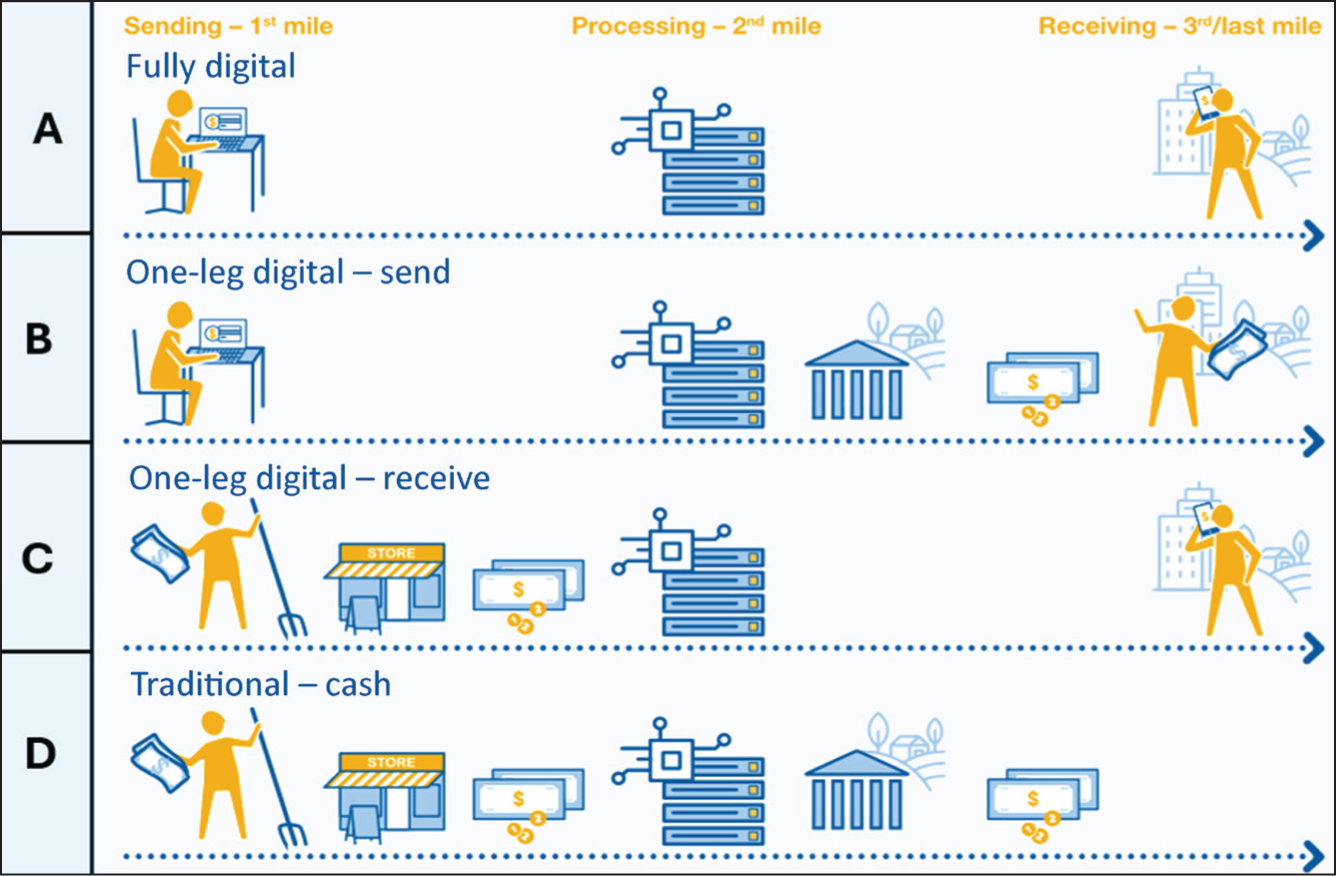

While various types of remittances exist, including financial, in-kind and social remittances, the most common and tangible are money transfers (IFAD, 2017, 2024). These financial remittance transactions can be categorised as formal or informal based on several factors, such as whether they involve cash or non-cash payments, the method of sending or processing, the type of technology used, service regulations and recipient platforms (Pieke et al., 2007). Informal transfers predate formal remittances, are primarily cash-intensive and are made personally by migrants or delivered through relatives, friends or unregistered remittance couriers (Freund & Spatafora, 2005). Informal remittances are prevalent in contexts where formal financial infrastructure is limited and remittance costs are high. However, these undocumented processes may be vulnerable to theft and other financial crimes (Crush et al., 2015; Kosse & Vermeulen, 2014). In contrast, formal remittances are channelled through the regulated multilateral networks of financial institutions, including banks and non-bank financial services, money transfer operators and remittance service providers (RSPs), offering protection against fraud (Metzger et al., 2019). Formal remittance transactions may be wholly traditional or cash-based, from end to end, involving regulated financial institutions (see Figure 1(D); IFAD, 2024).

While banks and cash-to-cash services dominated the formal global remittance landscape, significant shifts towards money transfer operators and RSPs have occurred over the last decade because they are less costly than banks and offer both cash-based and digital transfers (IFAD, 2017). Banks and money transfer operators have established invisible partnerships, working together to facilitate remittance sending and payouts (Metzger et al., 2019). Three RSPs—Western Union, MoneyGram and Ria—account for 35% of the global remittance market share and more than 50% in sub-Saharan African (SSA) countries (IFAD, 2017; Metzger et al., 2019; Rodima-Taylor & Grimes, 2019). However, this market share may be declining as digital-only RSPs emerge, offering application-based remittance services that can be received as cash payments via banks or mobile wallets (IFAD, 2024). Digital-only RSPs enable the transfer of foreign currencies through online platforms, which can be received in local currencies via mobile money platforms (Metzger et al., 2019).

In recent years, advances in financial technology (fintech), digital innovations, electronic payment systems, and online and mobile payment instruments have transformed formal remittance transfers towards digitalisation and facilitated an emerging trend away from informal remitting (Global Partnership for Financial Inclusion (GPFI), 2023). These notable changes have also been influenced by the expansion of regulate financial services, mobile phones, telecommunications networks and internet availability (IFAD, 2024; Sohst, 2024). Formal remittances that are sent through online platforms, processed and received into accounts at banks, non-bank deposit-taking institutions and mobile or electronic money accounts are referred to as digital remittances (see Figure 1(A); World Bank, 2020). However, remittance transactions may be partially digital, sent through self-assisted digital platforms, received in cash, or vice versa, whereby transactions sent using cash are received digitally via mobile financial accounts (see Figures 1(B) and 1(C); IFAD, 2024). Digital remittances, facilitated by fintech technologies such as mobile money and Web-based platforms, are rapidly transforming and accelerating the remittance process. Digital platforms also enable the regular tracking of remittance transfers sent through formal channels (Guermond, 2022).

The uptake of digital remittances fosters relationships with formal financial institutions, thereby enhancing access to financial services, including savings and loans, and facilitating financial inclusion (GPFI, 2023). Financial inclusion has emerged as a key global development priority, recognised as a significant outcome of digitalisation-driven poverty reduction strategies, bolstered by the expansion of affordable financial products and digital remittance services for underserved populations (Ozili & Mhlanga, 2024). The United Nations recognised this important development by designating ‘digital remittances towards financial inclusion and cost reduction’ as the theme for the International Day of Family Remittances in 2023 (GPFI, 2023; International Fund for Agricultural Development, 2024). The use of digital remittances for sending and receiving funds surged during the COVID-19 pandemic due to travel bans and containment measures that restricted in-person visits to money transfer shops and informal transfers (Rodima-Taylor, 2023).

Problem Statement

The United Nations’ 2030 Agenda and its Sustainable Development Goals (SDGs) recognise remittances’ development role and call for reduced transfer costs and greater financial inclusion (Ramachandran & Crush, 2024). Examining how digital remittances can be further harnessed for sustainable development in Global South migrant-sending countries is critical. Significant research has examined the nexus among migration, remittances and sustainable development in major migration corridors, such as the Mexico–United States corridor (De Haas & Vezzoli, 2010; IOM, 2022, 2024; Zamora & Gaspar Olvera, 2020). Other corridors, including the Zimbabwe–South Africa corridor, are also receiving increased attention (Crush et al., 2015; Sithole et al., 2023). Corridor-specific research on remittance practices can provide new insights into remittance-sending and recipient-country linkages, as well as optimised remittance transfers, especially through digital channels. However, several important corridors remain underexplored, despite increasing migration and remittance flows between SSA and North America, exemplified by the Ghana–Canada migration corridor.

Canada ranked seventh among the top destinations for migrants in 2024, with a rising number of migrants from sub-Saharan countries, including Ghana (OECD, 2022; UN DESA, 2025). Yet, African immigrant groups are under-researched in Canada and are often grouped under the broad racialised category of ‘Blacks’, which homogenises, oversimplifies and overlooks the specific experiences of different national groups (Owusu, 2003). The remittances landscape in the Canada–Ghana migration corridor has become increasingly more digitalised, presenting new opportunities and challenges for the uptake of digital remittances. As a leading remittance recipient country in SSA, Ghana’s national policies have significant implications for the uptake of digital remittances and their broader socio-economic outcomes.

Drawing on a case study of the Ghana–Canada migration corridor, this article examines how digitalisation is transforming remittance practices and analyses the emerging opportunities and constraints arising from these latest shifts. It addresses the following research questions: (a) How are Ghanaian migrants using digital remittance platforms within this corridor? (b) What structural, technological and regulatory factors facilitate or hinder the adoption of digital remittances among Ghanaian migrants? (c) What is the significance of these shifts for development outcomes and financial inclusion in Ghana? The article adopts a corridor-specific analytical approach, conducting a thematic review of existing literature and policy documents to assess remittance flow patterns, the role of fintech innovations and the uneven accessibility of digital financial services across socio-economic groups in Ghana and sending migrant communities in Canada. This analysis of an under-researched corridor provides nuanced insights into the scope of digital remittances and their development potential for migrant-sending households in Ghana.

The article is organised into four sections. The first section introduces the article and outlines the research questions and the problem statement. The second presents the methodology, which provides a contextual foundation for the analysis. The third integrates the results and discussion, detailing findings from the thematic review on the digitalisation of remittances, barriers, and regulatory and policy underpinnings for the corridor. The final section concludes with actionable policy recommendations.

Methodology

A thematic literature review was conducted, involving database searches, screening over 50 papers and thematically analysing the selected studies and reports in light of the research questions (Creswell & Creswell, 2018). A structured search was conducted across major academic databases, including Scopus, Web of Science and Google Scholar, along with repositories of relevant international and national organisations, such as the World Bank, International Fund for Agricultural Development, International Organisation for Migration, Organisation for Economic Cooperation and Payments Canada, using a combination of keywords. The chosen keywords were ‘remittances’, ‘digital remittances’, ‘mobile money’, ‘fintech’, ‘migration corridor’, ‘Ghana’ and ‘Canada’. The review examined peer-reviewed journal articles, book chapters, working papers and policy reports published between 2005 and 2025 to analyse earlier and latest developments in digital technologies, remittance practices and policies, and migration dynamics across the Ghana–Canada corridor. Thematic analysis was conducted using selected sources to identify common patterns across key analytical categories, such as remittance channels, regulatory frameworks and development outcomes. These themes shaped the outline of the article’s analysis and allowed a synthesis of linkages across them for the Ghana–Canada migration corridor. Rather than providing an exhaustive review, the article prioritises depth and conceptual integration of relevant literature in answering the research questions. Despite concerns about subjectivity and potential bias in identifying and synthesising themes, thematic literature reviews can offer structured insights and a broader understanding, especially for complex and under-researched topics.

Ghana–Canada Migration: Context and Migrant Socio-demographics

Canada ranks among the top five Organisation for Economic Co-operation and Development (OECD) destination countries for Ghanaian citizens (OECD, 2022). Historical ties between the two countries date back to 1906, when Québécois missionaries established a church in the Northern Region (Government of Canada, 2024). Bilateral relations have been significantly strengthened through their shared involvement in the Commonwealth and the United Nations (Government of Canada, 2024). However, migration to Canada began much later, particularly during the 1980s, driven by political and economic instability in Ghana (Mensah et al., 2018; Owusu, 2003).

The 2021 Canadian Census recorded 25,755 members of the Ghanaian diaspora, with over half residing in Ontario, particularly in Toronto (Statistics Canada, 2021). Among Ghanaians in Canada, 52.6% are first-generation migrants (Mensah et al., 2018), typically aged 25–64, with youth (15–34 years) constituting 31% of the population (Mensah et al., 2018; OECD, 2022). Nearly half (49%) consists of females. Increasingly, Ghanaians have migrated through economic channels, with highly educated and skilled workers, such as health professionals, emigrating for better-paying jobs in English-speaking countries, including Canada (Government of Ghana, 2016; OECD, 2022). Ghanaian youth have also migrated to Canada for professional and higher education training, with Ghanaian student numbers increasing by 87% between 2013 and 2019 (OECD, 2022).

Despite educational qualifications comparable to those of Canadians, Ghanaian migrants face significant challenges, including lower median incomes and systemic barriers common to racialised communities (Firang, 2019; Mensah et al., 2018; Nkrumah, 2022). Ghanaian migrants are over-represented in processing, manufacturing and construction, particularly in Toronto (33.3%), and under-represented in managerial or professional roles. About 11% of Ghanaian migrants were employed in the health sector in 2015/2016 (Firang, 2019, 2022; Mensah et al., 2018). In 2015, the average annual income for full-time employed Ghanaian immigrants (CA$48,010) lagged behind that of Canadian-born workers (CA$53,431; Mensah et al., 2018). Among Ghanaian entrepreneurs, hurdles include racial profiling and excessive business scrutiny as reported in the Prairie provinces (Nkrumah, 2022).

Amid these challenges, Ghanaian diaspora networks are critical in helping new migrants settle, thereby enhancing their remitting potential. Social ties formed through friends, churches and hometown associations can ease settlement by providing information on jobs, labour market entry points and employment resources for new migrants (Alliance of Ghanaian–Canadian Associations, 2024; Kyeremeh et al., 2024). Well-established migrants are better positioned to send financial remittances to their left-behind relatives.

Results and Discussion

Ghana and Africa’s Remittance Ecosystem

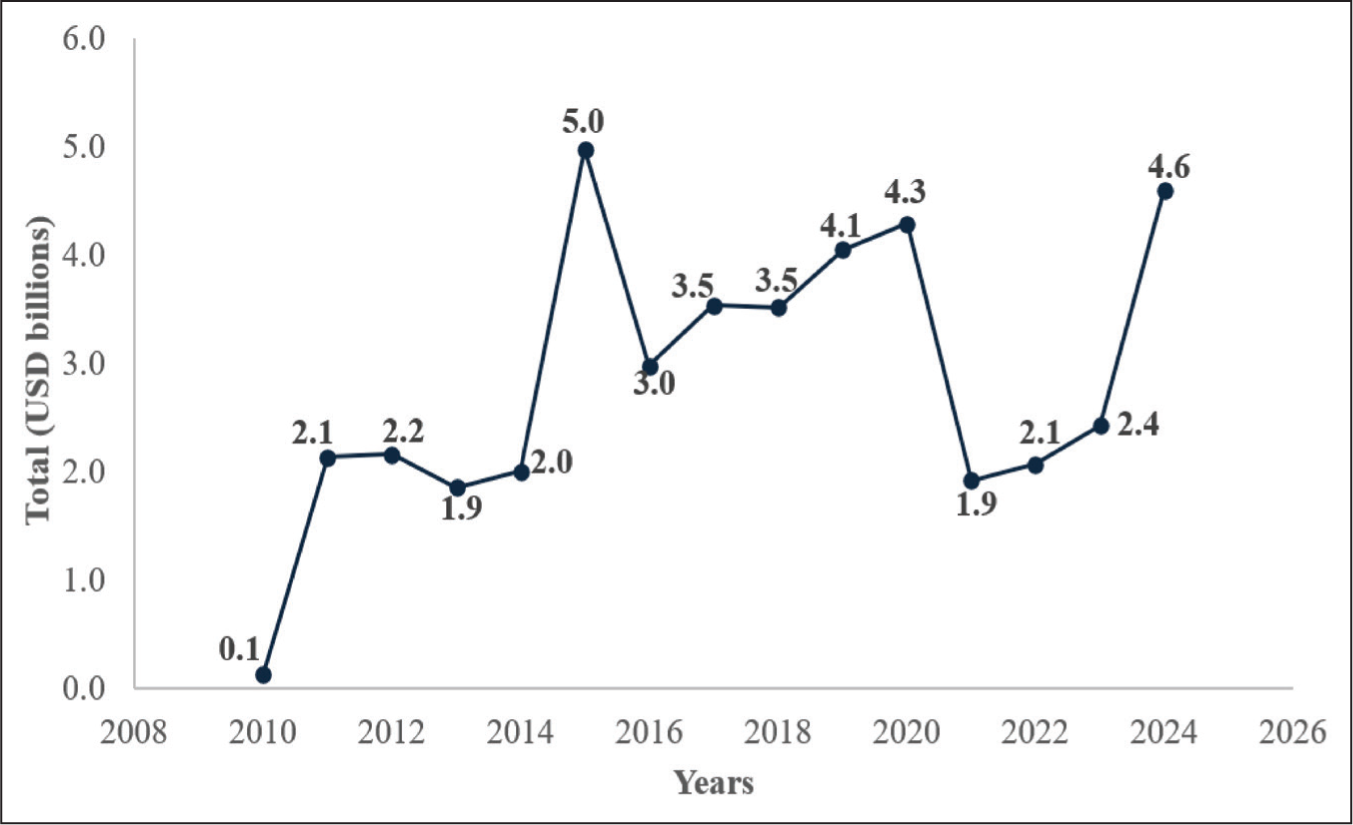

According to the Remittance Index, a composite metric that measures the significance of remittance inflows relative to the recipient country’s size and diaspora numbers, Ghana scored 62, ranking 14th among African countries in 2023 (IFAD, 2025a). However, within SSA, Ghana is the second-highest recipient of remittances, receiving $4.6b in 2024 (IFAD, 2025b). Despite fluctuations over time (see Figure 2), remittances support Ghana’s gross domestic product (GDP) growth, accounting for 6.2% of GDP in 2024 (IFAD, 2025a). It is estimated that 20% of Ghana’s population receives international remittances (IFAD, 2023a). In 2021, Ghana’s remittance inflows from Canada amounted to $127m, representing approximately 1.55% of Canada’s total international remittance outflows of $8.2b that year (IFAD, 2025a; MPI, 2025). Canada is one of the top eight remittance-sending countries globally and ranks fifth among countries in the Global North for Ghana (IFAD, 2025a).

Ghana’s Inwards Remittance Dynamics and Impacts

Remittances generate beneficial outcomes in Ghana, including reductions in current account deficits, stimulation of the domestic economy through increased investment in housing and financing of local community development projects (Teye et al., 2017). Formal remittances strengthen macroeconomic development both directly and indirectly by strengthening financial institutions, enhancing GDP and increasing foreign exchange reserves (Abdulai, 2023). Remittances also increase Ghana’s GDP per capita, indirectly strengthening the local economy through household spending and investment (Dridi et al., 2019). Estimates suggest that a 1% increase in remittances results in nearly a 4% growth in Ghana’s GDP per capita (Agyei, 2021).

Remittances sent to Ghana support access to food, cash income, healthcare, education and housing, alleviating socio-economic risks and poverty among recipient households (Armah-Attoh, 2022). Non-cash remittances, such as canned food, are also vital for recipients (Coffie, 2022). An International Organization for Migration (IOM) baseline remittance assessment in Ghana’s Ashanti and Brong-Ahafo regions found that 80% of remittance recipients used funds for basic needs, such as education (21.9%), medical treatment (16.4%) and child support (6%), with 40% of households receiving remittances via informal platforms (Statistical Service Ghana & IOM Development Fund, 2017). Notably, remittance gains mostly benefit recipient households, usually middle-income, migrant-sending households (Agyei, 2021).

Overall, informal remittance inflows have been declining with Ghana’s rapid digital expansion. Digital remittance recipients in Ghana, particularly mobile money users, are more likely to invest in education, microbusinesses and real estate, promoting financial resilience, especially for rural female-headed households (Abdul-Mumuni et al., 2019; Apiors & Suzuki, 2018; Sakyi-Nyarko et al., 2022). While digital remittances, particularly mobile money services, facilitate financial inclusion, they may expose remittance receivers to exploitative loan packages and debt-settlement services (Guermond, 2022). Additionally, informal remitting limits the development potential of remittances.

Within the Ghana–Canada corridor, Ghanaians in Canada maintain strong transnational social, economic and cultural ties with their country of origin, marked by regular remittance-sending, return visits and investments (Firang, 2020, 2022). Recent research on Ghanaian immigrants in Toronto found that 93% of participants regularly remitted to family and friends (Kyeremeh, 2020). Previous research has shown that over 90% of participants consistently remitted amounts ranging from CA$50 to CA$5,000 (Owusu, 2003). Ghanaians in Toronto with strong ties to Ghana typically prioritise investing in housing in their country of origin rather than in Canada (Firang, 2020; Kuuire et al., 2016). However, remittance pathways, whether digital or non-digital, were not specified.

Digitalisation of Remittances and the Canada–Ghana Corridor

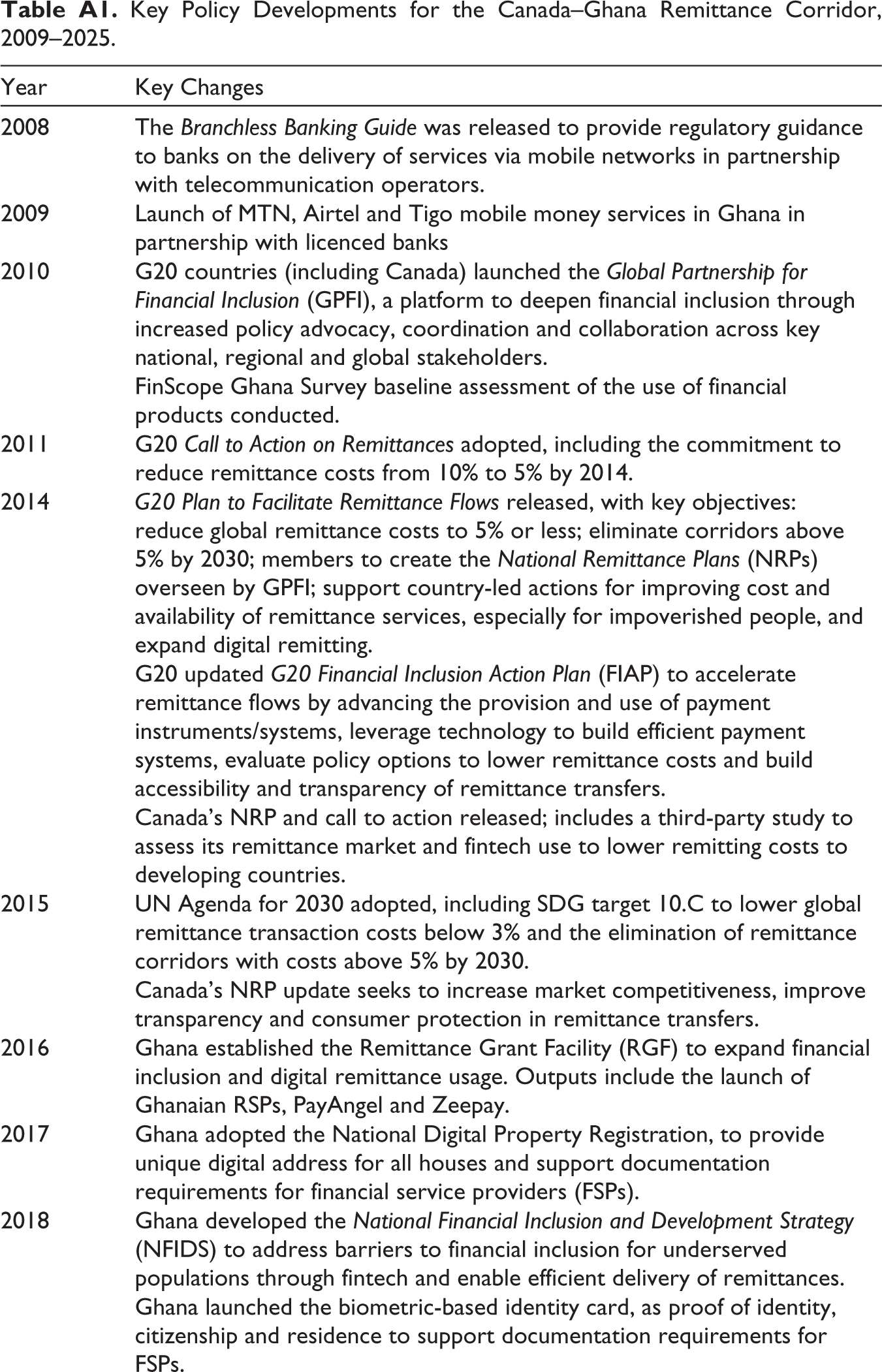

There is limited information on diverse remitting practices across the Canada–Ghana corridor. However, broad trends in Canada suggest that remittance transfers to Ghana are increasingly digitalised. End-to-end digital remittances allow both senders and receivers to utilise online applications to debit and credit their accounts (IFAD, 2024). The widespread use of mobile phones and the introduction of mobile money services by MTN, Airtel and Tigo telecommunication companies between 2009 and 2012 marked an important chapter in the development of digital payments and remittance systems in Ghana (see Table A1; Bank of Ghana, 2022). The fintech industry began to infiltrate Ghana’s mobile money system in 2017, facilitating digital financial services, including payments, remittances and investments, provided by banks and other specialised deposit-taking institutions (Bank of Ghana, 2022).

Furthermore, the launch of Ghana’s Interbank Payment and Settlement Systems Platform in 2018 laid the groundwork for effective interoperability among all financial service providers, including banks, mobile money operators and fintech companies (IFAD, 2023b). Enhanced collaboration and interoperability between financial service providers enable inbound international remittances to be received via multiple channels, such as cash and bank accounts, along with electronic and mobile money wallets supported by telecommunication companies such as MTN and Vodafone (IFAD, 2023b). Fintech companies such as Terrapay and Etranzact further act as aggregators, connecting international RSPs with local partners, optimising time-consuming processes and facilitating faster remittance payouts (IFAD, 2023b).

Ghana has one of the most advanced and fastest-growing digital financial systems in SSA, with mobile money serving as a central and thriving component (IFAD, 2024). Between 2010 and 2021, the proportion of formal bank accounts in Ghana shrank from 34% to 30%. Conversely, the usage of mobile money services surged from 7% to 65%. These positive shifts signal substantial progress towards the Government of Ghana’s digital financial inclusion target of 85% by 2023 (Ghana Ministry of Finance, 2021). Ghana surpassed this target by achieving a 95% financial inclusion rate by 2021, attributed to high mobile money access, combined with expanded telecommunications services and increased mobile phone usage (Ghana Ministry of Finance, 2021). Mobile money agents play an increasingly important role in customer financial transactions. In 2021, there were over 442,375 active agent centres for mobile money, compared to approximately 3,000 bank branches, fewer ATMs and other formal remittance access points (IFAD, 2023b).

At the remittance-sending end in Canada, 33% of digital remittance outflows in 2020 were sent via financial institutions, such as banks, while 18% were sent via traditional RSPs, including Western Union and digital-only RSPs like Wise (GPFI, 2021). A Payments Canada study found that one in five Canadians (20%) sent international remittances using their bank accounts in 2023 (Yun et al., 2024). According to Payments Canada, the operator of Canada’s payment-clearing and settlement systems, new migrants tended to remit larger amounts, primarily directed towards Asia and Africa (including Ghana; GPFI, 2021).

The use of Fourth Industrial Revolution Technologies (4IR), such as artificial intelligence (AI) and blockchain technologies by fintech companies that provide digital remittance services, is increasing. These 4IR technologies enable faster, more cost-effective and transparent remittance transactions by eliminating certain central intermediaries and their associated costs (Ratha et al., 2018). Notably, digital-only mobile remittance applications, such as Remitly and Wise operating across the Canada–Ghana corridor, combine AI, Big Data and machine learning platforms to detect fraudulent transactions and enhance customer security (Remitly, 2024; Wise, 2024). Almost 50% of Canadian businesses, including RSPs, prefer 4IR platforms, such as generative AI, to personalize customer service experiences, prevent fraud and improve time and cost efficiency (Yun et al., 2024). Nevertheless, the new digital remittance platforms can expose users to new cybersecurity risks, which have increased since 2019 (Sohst, 2024).

Barriers and Challenges

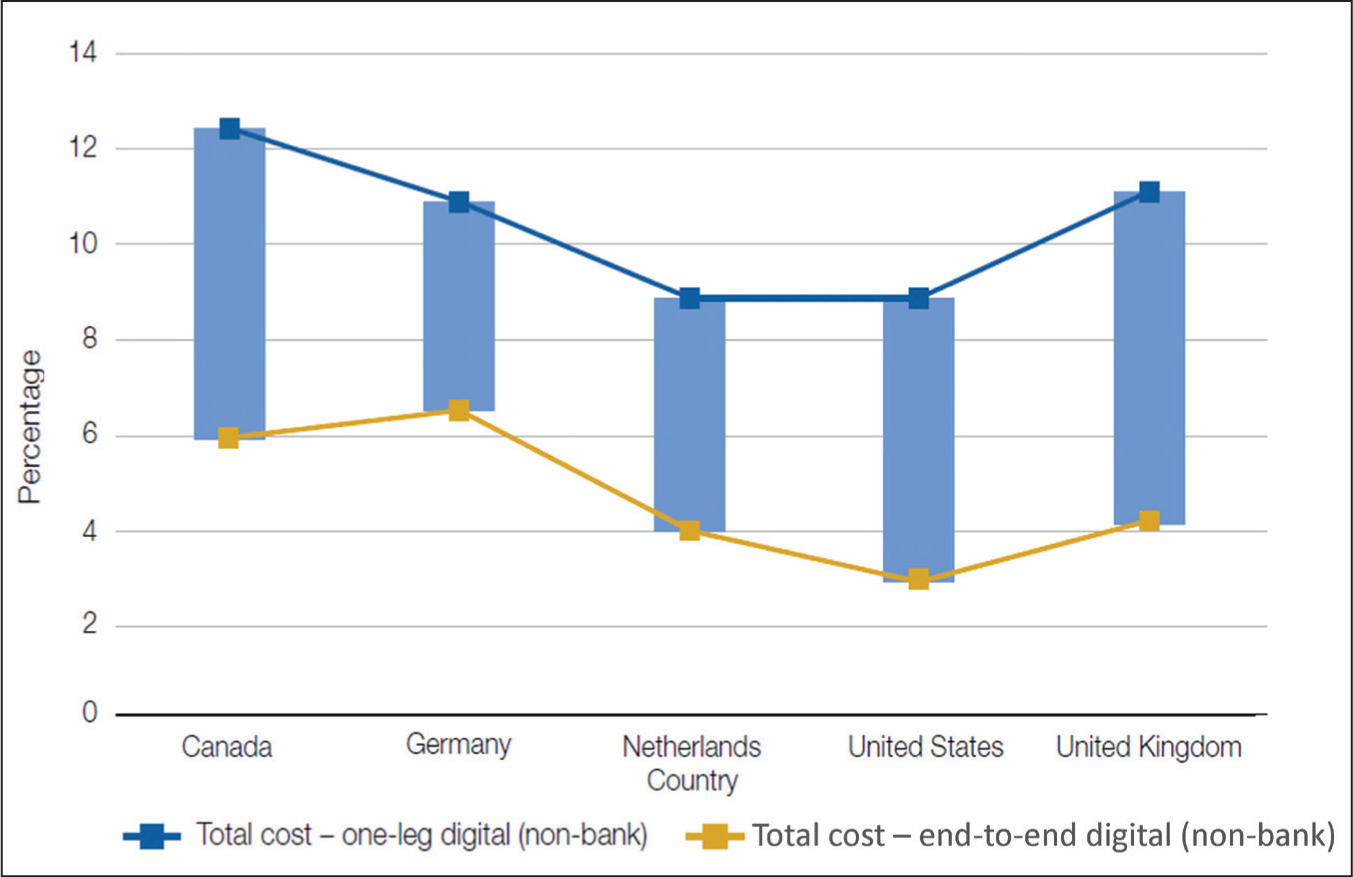

Despite these positive developments in the digital remitting landscape between Canada and Ghana, challenges related to usage, costs and access persist. The cost of outbound remittances from Canada decreased from 9.7% to 7.7% between 2014 and 2019, but it is high now. The Government of Canada committed to lowering remittance costs to 5% by 2022 (GPFI, 2019), although this target has not been met. Canada is the second-most expensive remittance-sending country among the G20. The cost of remitting $200 to Ghana was 6.23% in 2022, while fees in the United States were significantly lower at 3.5% (Figure 3; IFAD, 2023b). End-to-end digital remittance transactions within the Canada–Ghana corridor, especially via digital RSPs, are lower-cost than partially digital remittances (Figure 3; IFAD, 2023b). Overall, migrants and their families prefer cheaper remittance transactions to maximise the amounts received by recipients, which encourages the sustained use of informal channels (Higazi, 2005). Ghanaian migrant remitters and recipients also continue to favour informal channels for convenience and remain hesitant to adopt mobile remittances due to trust issues and fears of fraud (IFAD, 2023a).

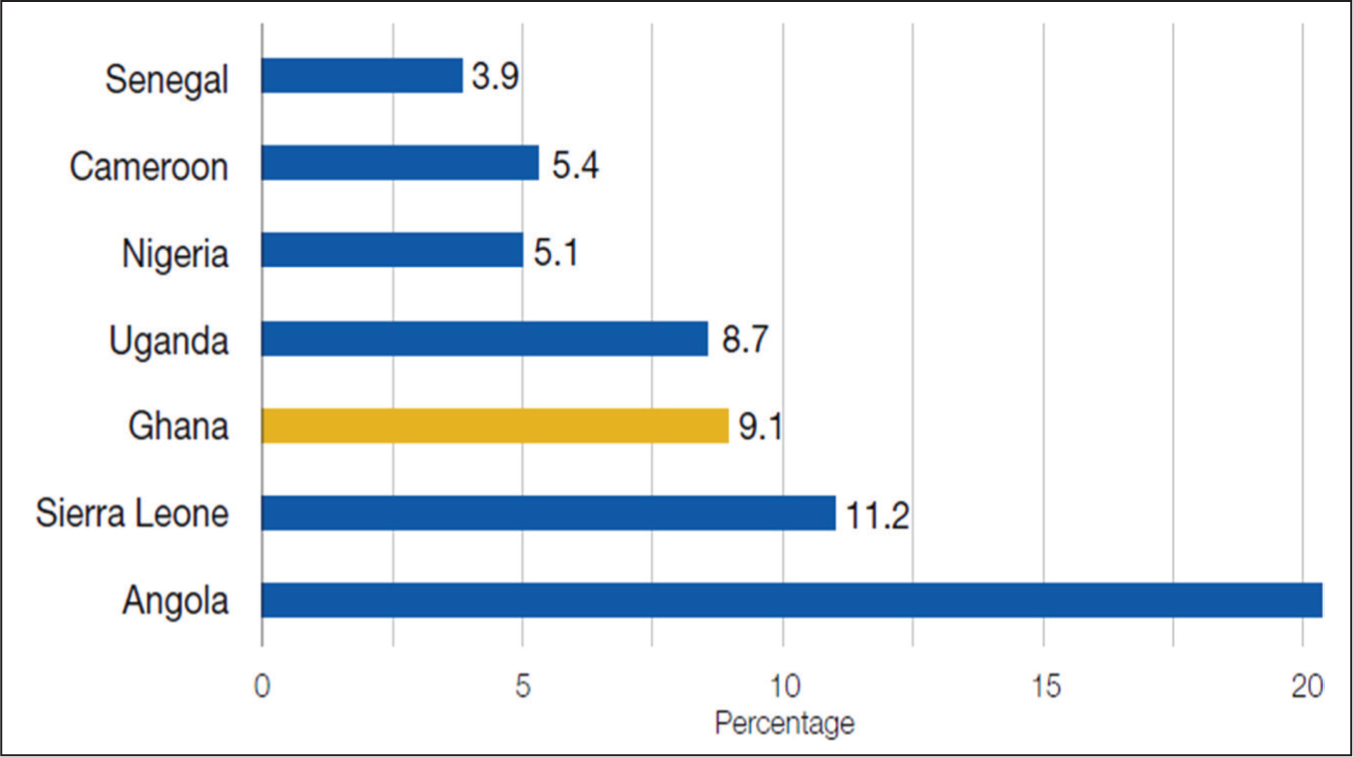

Sending remittances to SSA countries, including Ghana, remains expensive (see Figure 4). Ghanaian mobile service users are among the most heavily taxed in SSA, with taxes accounting for over 30% of mobile expenses (GSMA, 2023). Since 2020, a 5% communications services tax has applied to all mobile phone services in Ghana. An additional 1.5% electronic transfers (e-levy) tax was introduced in May 2022, affecting all mobile money, remittances and bank transfers exceeding GH₵100 (approximately CA$9.21; GSMA, 2023). Remittance prices to Ghana rose by almost 3% in 2022, reaching 9.1% and surpassing the SSA average of 8.6% (IFAD, 2023b). In 2024, the remittance cost for $200 exceeded 8% of the total transaction. By comparison, the cost to Southeast Asia was less than 6% on average, while the global average was 6.65% (World Bank, 2024a). Factors shaping high remittance transaction costs in Ghana include high foreign exchange margins, inflation, trade restrictions, volatile financial markets and high digital financial taxes (e-levy) on electronic transfers (Coffie, 2022; Higazi, 2005; IFAD, 2023b).

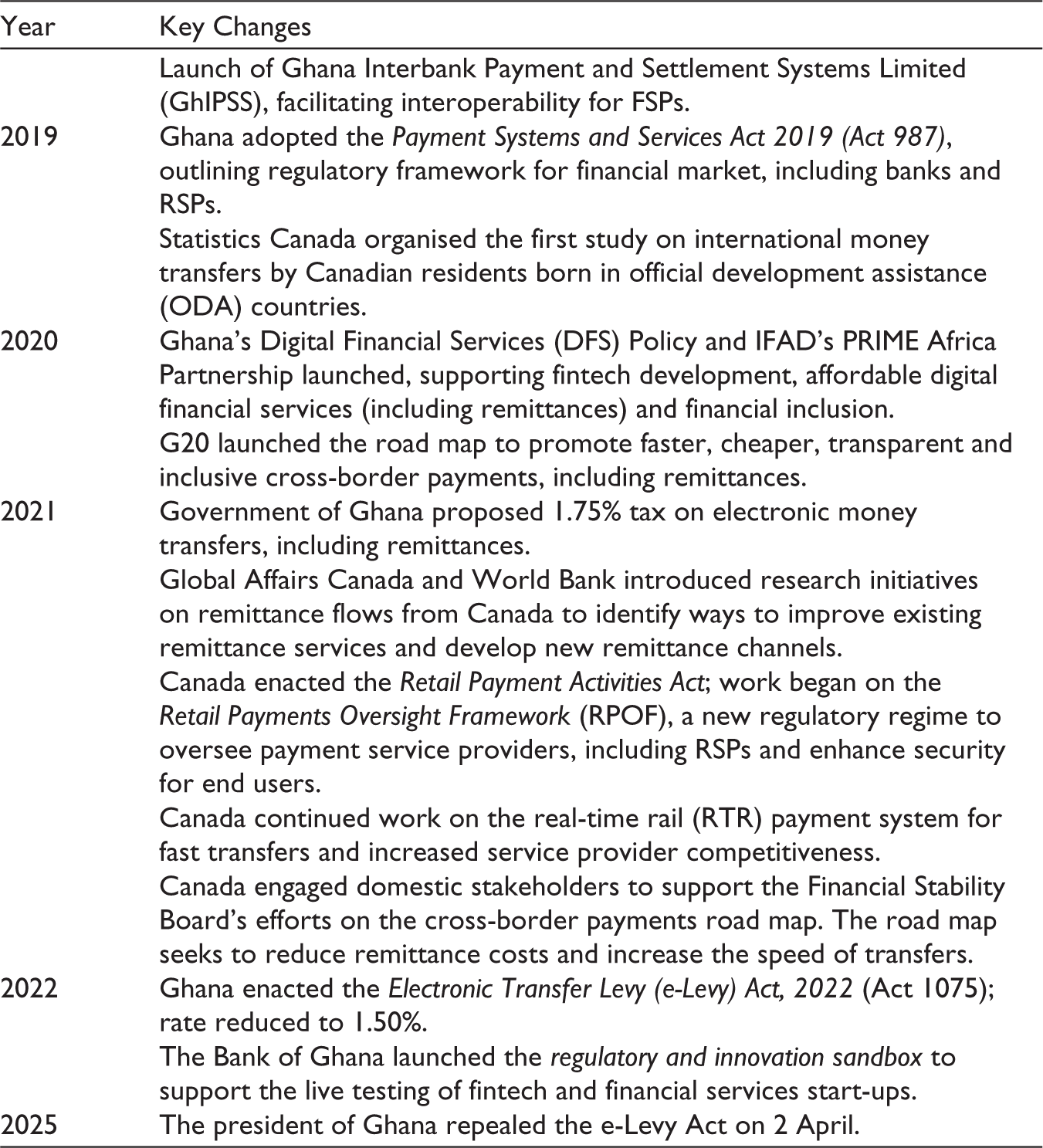

Amid compounded economic pressures post-COVID, the additional e-levy tax was unpopular and discouraged digital financial transactions, including remittances. While pre-e-levy total person-to-person mobile transactions grew from 40 to 50 million (May 2021–March 2022), after the e-levy announcement, they fell to 38 million in May 2022 and remained below pre-e-levy levels by January 2023 (GSMA, 2023). Overall, the levy resulted in a 14% decrease in person-to-person digital financial transactions and a 48% drop in transactions above GH₵200 (GSMA, 2023). Ghana is still working to reduce remittance costs following a government change and the March 2025 repeal of the e-levy. As a result, circulating mobile money transactions in person-to-person and agent-to-agent channels increased by approximately 13% year-on-year by the end of the first quarter of 2025 (Bank of Ghana, 2025).

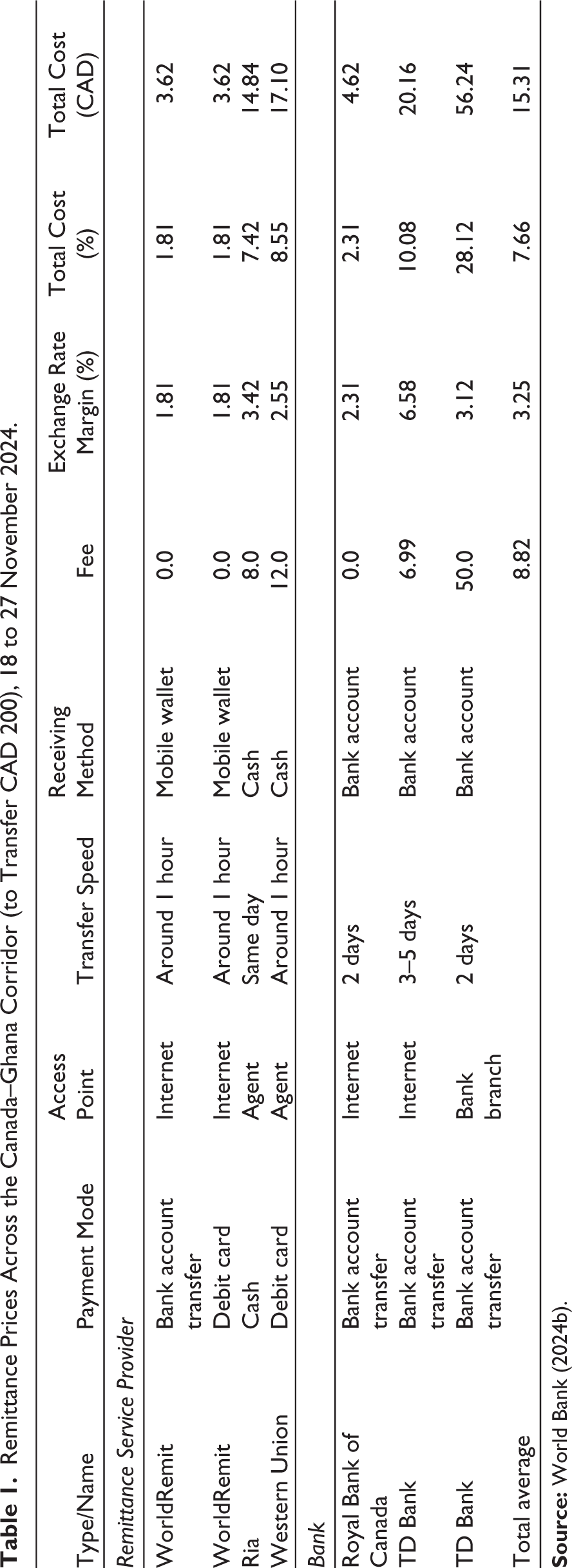

Digitalisation is lowering remittance transaction costs across the Canada–Ghana corridor, though costs vary widely between partially digital and fully digital transactions (GPFI, 2023). While remittance fees vary, the World Bank’s remittance price tracker shows that traditional channels, such as banks, charge the highest fees and require the longest transfer periods, especially when funds are sent to a bank account at the receiving end (see Table 1). To address the significant challenge of high costs, digital-only RSPs, such as WorldRemit, offer services with zero or less than 1% upfront fees while charging for their services by adding small percentages to the mid-market exchange rate. Remittances sent through online platforms and received by mobile wallets had the lowest costs and reached the earliest (Table 1). Notably, according to a Payments Canada study, migrants cited hidden charges, unknown foreign exchange rates, high transaction costs and limits on sending amounts as the main challenges to international remitting from Canada (Yun et al., 2024).

Remittance Prices Across the Canada–Ghana Corridor (to Transfer CAD 200), 18 to 27 November 2024.

The other significant hurdle concerns accessibility. Digital remittance platforms are largely inaccessible to irregular migrants and remittance recipients without valid identification documents (GPFI, 2017; United Nations, 2018). Digital remittance barriers related to accessibility within the Canada–Ghana corridor have received limited research attention. However, there are cross-cutting access challenges that affect all migrant remitters in Canada. A 2017 Statistics Canada study of international money transfers found that convenience for both senders and recipients was the most critical factor in remitting practices (Dimbuene & Turcotte, 2019). Although migrants had access to digital remittance channels in 2017, 56% used in-person money transfer stores (account-to-account), while 10% relied on hand-carrying (Dimbuene & Turcotte, 2019; GPFI, 2019). This finding suggests that access at the recipients’ end is also a prime consideration in remitting practices.

In 2024, Ghana scored 86 on RemitSCOPE’s Digital Remittances Readiness Index for its elevated digital remittance accessibility and preparedness in Africa, ranking second after Kenya (IFAD, 2025b). Nevertheless, disparities persist in its digital landscape tied to gender, socio-economic standing and geographical location. Ghana has a mobile penetration of 135%, but women owned 10% fewer mobile phones and were 6% less likely to use mobile money services in 2021 (Dabalen & Mensah, 2023). Between 2010 and 2021, urban internet uptake rates increased from 13% to over 80%, compared to a 2%–54% increase in rural areas (Dabalen & Mensah, 2023). Rural areas are relatively less connected, and historically disadvantaged regions, such as northern Ghana, are less likely to use the internet and fintech due to lower incomes and other disparities.

Regulatory, Policy and Institutional Aspects

Regulatory, policy and institutional changes have been central to the adoption, costs and accessibility of digital remittances along the Ghana–Canada corridor. Next, we briefly discuss key global, national and other developments that have shaped end-to-end digital remittance flows in this corridor and uptake among senders and recipients. We also highlight the regulatory environment in both countries, which facilitates and hinders digital remittances (for additional details, see Table A1).

Both Canada and Ghana have committed to meeting remittance-related SDGs: specifically, SDG 10.c.1, which aims to reduce transaction costs to less than 3% and eliminate remittance corridors with costs above 5%, and SDG 17.3.2, which seeks to increase remittances as a share of recipient countries’ GDP (UN SDGs, 2016). Canada has a well-regulated financial system that supports greater international RSP competitiveness, improved financial regulatory and payment system infrastructure and enhanced consumer protection (GPFI, 2019, 2021). A key regulation that enhances consumer protection is Canada’s Retail Payment Activities Act, enacted in 2021. It extends the Bank of Canada’s financial regulatory scope to include RSPs and requires them to meet registration, operational risk and fund-safeguarding requirements (GPFI, 2024). In 2024, Canada granted payment service providers access to core payments clearing and settlement systems operated by Payments Canada, thereby boosting competitiveness in the digital financial services sector (GPFI, 2024). Payments Canada is further upgrading the national rapid payment system infrastructure, Real-Time Rail (RTR), to facilitate near-instantaneous transactions, clearing and settlement of data-rich payments, including remittances (GPFI, 2024).

Canada is also engaged with the GPFI, a G20 initiative, and its Financial Inclusion Action Plan to expand access to affordable formal financial services for financially excluded groups (GPFI, 2017). Transfer costs remain a key barrier to the uptake of digital remittances. Canada participates in the G20 Plan to Facilitate Remittance Flows, initiated in 2014, by ‘working to reduce the average global costs of transferring remittances to 5%, and subsequently to below 3% as mandated by SDG 2030 goals’ (GPFI, 2023, p. 10). Under this programme, G20 countries are expected to release national remittance plans every 2 years, outlining their actions to support remittance flows and lower transfer costs. The Government of Canada released two national remittance plans in 2019 and 2021, but did not issue one in 2023, unlike other countries such as the United States, United Kingdom, France, Germany and Italy (GPFI, n.d.; GPFI, 2023).

On the receiving end, Ghana has prioritised regulatory reforms to expand financial inclusion through digital financial services, including digital remittances. Key reforms included empowering non-bank institutions, particularly telecommunications companies, to operate mobile money services in 2009, building on the 2008 Branchless Banking Guidelines (Bank of Ghana, 2022). The establishment of the Ghana Interbank Payment and Settlement System (GhIPSS) in 2018 ensured interoperability among financial service providers, while the Payment Systems and Services Act, 2019 (Act 987), created a favourable environment for the active participation of fintechs with varying capacities (Bank of Ghana, 2022; Dabalen & Mensah, 2023). In 2020, Ghana introduced a digital financial services policy to guide fintech innovation and interoperability (Ghana Ministry of Finance, 2020).

Under IFAD’s PRIME Africa Partnership for fintech development, Ghana received $2.2m for the Remittance Grant Facility (RGF) between 2016 and 2021 to catalyse innovations in remittance services and products that support economic growth (IFAD, 2024). These investments led to the emergence of two Ghanaian-owned digital-only RSPs, PayAngel and Zeepay, serving international remittance corridors, including the Canada–Ghana corridor. By 31 December 2021, 40 entities, comprising payment and financial technology service providers, were approved to operate in Ghana’s digital payment space (Bank of Ghana, 2022). Other transformative interventions include the National Digital Property Registration, 2017, and the Ghana Primary National ID, 2018, to support the valid identification requirements of financial service providers and increase access to remittances (IFAD, 2023b).

Despite these policy-driven advances, there remains room to streamline the remittance landscape across both countries, particularly in transfer costs. Remittance-focused in-depth research can contribute to this process, especially on the Canadian end with Ghanaian migrant and diaspora groups. Although Canada is a major immigration country, there is a paucity of detailed data and research on remittance inflows and outflows. Statistics Canada organised the first national study on remittance transfers from Canada as late as 2017 (Dimbuene & Turcotte, 2019). In 2021, Global Affairs Canada initiated another research project on remittance-sending in Canada, in collaboration with the World Bank, which was scheduled for completion by 2024 (GPFI, 2021). Additional details of this project have not yet been released. In Ghana, the Ministry of Finance, the Bank of Ghana and other financial institutions, in partnership with the World Bank and IFAD, are involved in research on local and international remittance transactions. However, the Bank of Ghana collects limited information on remittance indicators and does not publicly release it. Collaborative efforts involving regulatory authorities, research institutions, remittance senders and recipients are critical for developing evidence-based research to streamline and optimise transfers across the Ghana–Canada corridor.

Conclusion and Recommendations

In this article, we examined key remittance practices and challenges associated with the Ghana–Canada migration corridor. We also reviewed how digitalisation is affecting remittance-sending and -receiving across this less-studied corridor. The digitalisation of remittance-related processes has significantly reduced average transfer times, slightly lowered remitting costs and expanded the pool of funds that recipients in Ghana can redeem and use. The World Bank remittance price tracker indicates that money sent from Canada via digital platforms is less expensive and can be received within 1 hour in the recipient’s mobile wallet in Ghana (World Bank, 2024b). Conversely, traditional institutions such as banks typically take 2–3 days to deliver these funds and incur higher total costs. The additional funds released through lower remittance prices have broader implications for Ghana’s economic development. Emerging initiatives in Canada, such as the new RTR payment system and the Cross-border Payments Roadmap, have the potential to further streamline remittances. The increased speed of transfers can be especially beneficial when remittances need to be sent urgently during crises or disasters, such as floods, droughts, cyclones, fires and other emergencies.

Our analysis highlights several evidence-based findings on the digitalisation of remitting in the Ghana–Canada corridor, including the expansion of mobile money, high transaction costs and persistent disparities tied to socio-economic and geographical factors. However, because it is based on a thematic review, the study has several limitations. It relies on a qualitative review of secondary literature and publicly available data sets, with very limited empirical research on migrants’ remittance practices. Weak, detailed corridor-specific data on migrant remittance practices limit the assessment of adoption patterns for digital remittances and constrain evidence-based policymaking aimed at improving access and reducing costs. Nevertheless, in under-researched contexts such as the Ghana–Canada migration corridor, a guided literature review, as conducted in this study, offers valuable insights that contribute to knowledge development and inform the policies. Building on these results, the following recommendations are proposed to address existing gaps and leverage the developmental potential of digital remittances.

To strengthen the Government of Ghana’s enabling regulations, fiscal policies and institutional capacities to leverage international remittances, greater engagement of migrants is required. Ghana offers migrant-friendly financial packages, such as direct migrant investment schemes, foreign account ownership, and health and funeral insurance for relatives; however, uptake remains low (IFAD, 2023). Beyond personal packages, the GH₵50m Golden Jubilee Savings Bond, issued in 2007 to fund development projects, raised only about GH₵20m, with only 6% purchased by the Ghanaian diaspora, primarily migrants in Canada, the United States and the United Kingdom, compared with over 90% purchased locally (Coffie, 2022; Faal, 2019). This reflects weak diasporan participation in state-backed migrant investment initiatives. Additionally, financial and digital literacy gaps among migrants and remittance recipients limit the uptake of digital remittances, while urban–rural, socio-economic and gender disparities in access to digital remittances persist in Ghana.

Strengthening the uptake of digital remittances along the Ghana–Canada migration corridor requires further cost reductions. Policies should prioritise accurate, timely data on remittance types, trends and channels to inform cost reductions and maximise the impact of remittances. West African countries, including Ghana, can benefit from additional research that documents both formal and informal remittance dynamics, the integration of 4IR technologies, cybersecurity risks, and gender and urban–rural disparities. This is crucial because remittance flows to lower-middle income countries in SSA currently surpass official development assistance and foreign direct investments and may increase further (IOM, 2024; World Bank, 2020). Globally, reducing the cost of formal remittances by 5% of the principal amount can yield $16b in additional savings annually, making more money available to senders and recipients (World Bank, 2023). Thus, research that engages diverse stakeholders to address remittance costs and access challenges will support increased formal digital remittance transactions within the Canada–Ghana corridor.

To leverage digital remittances for broader SDG implementation, clear strategies and targeted education for migrants and remittance recipients are needed to promote the effective use of digital remittance platforms and channel remittances towards investments beyond recipient households. The Ghanaian–Canadian diaspora must be engaged in the design of relevant policies and processes to streamline financial, technological and migration policies and optimise digital remittance uptake for sustainable development. Ghana could further partner with RSPs and provide tax waivers to invest proceeds in social, infrastructure and development projects, alongside actively expanding migrants’ participation.

Footnotes

Acknowledgements

The authors would like to thank the editors of the special issue, Jenna Hennebry, Kim Rygiel and Jonathan Crush, as well as Nelson Graham and Marika Jeziorek, for their feedback and comments on a previous draft of this article. An early version was presented at the ‘Migration and Technology: Governance Innovation, Challenges and Future Directions’ workshop at the Balsillie School of International Affairs in Waterloo, Ontario, on 8 October 2024.

Data Availability Statement

Data sharing does not apply to this article, as no data sets were generated during the current study.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: The research for this article was supported by the projects ‘Remitting for Resilience (R2): Enhancing Food Security and Climate Adaptation Through Gender-inclusive Migrant Remittances’, funded by the Canadian new frontiers in research fund (NFRF Grant No. NFRFI-2023-00324) and ‘Migration and Food Security in the Global South (MiFOOD): Interactions, Impacts and Remedies’ funded by a partnership grant from the social sciences and humanities research council of Canada (SSHRC Grant No. 895-2021-1004).

Annexure

Key Policy Developments for the Canada–Ghana Remittance Corridor, 2009–2025.

| Year | Key Changes |

| 2008 | The Branchless Banking Guide was released to provide regulatory guidance to banks on the delivery of services via mobile networks in partnership with telecommunication operators. |

| 2009 | Launch of MTN, Airtel and Tigo mobile money services in Ghana in partnership with licenced banks |

| 2010 | G20 countries (including Canada) launched the Global Partnership for Financial Inclusion (GPFI), a platform to deepen financial inclusion through increased policy advocacy, coordination and collaboration across key national, regional and global stakeholders. |

| FinScope Ghana Survey baseline assessment of the use of financial products conducted. | |

| 2011 | G20 Call to Action on Remittances adopted, including the commitment to reduce remittance costs from 10% to 5% by 2014. |

| 2014 | G20 Plan to Facilitate Remittance Flows released, with key objectives: reduce global remittance costs to 5% or less; eliminate corridors above 5% by 2030; members to create the National Remittance Plans (NRPs) overseen by GPFI; support country-led actions for improving cost and availability of remittance services, especially for impoverished people, and expand digital remitting. |

| G20 updated G20 Financial Inclusion Action Plan (FIAP) to accelerate remittance flows by advancing the provision and use of payment instruments/systems, leverage technology to build efficient payment systems, evaluate policy options to lower remittance costs and build accessibility and transparency of remittance transfers. | |

| Canada’s NRP and call to action released; includes a third-party study to assess its remittance market and fintech use to lower remitting costs to developing countries. | |

| 2015 | UN Agenda for 2030 adopted, including SDG target 10.C to lower global remittance transaction costs below 3% and the elimination of remittance corridors with costs above 5% by 2030. |

| Canada’s NRP update seeks to increase market competitiveness, improve transparency and consumer protection in remittance transfers. | |

| 2016 | Ghana established the Remittance Grant Facility (RGF) to expand financial inclusion and digital remittance usage. Outputs include the launch of Ghanaian RSPs, PayAngel and Zeepay. |

| 2017 | Ghana adopted the National Digital Property Registration, to provide unique digital address for all houses and support documentation requirements for financial service providers (FSPs). |

| 2018 | Ghana developed the National Financial Inclusion and Development Strategy (NFIDS) to address barriers to financial inclusion for underserved populations through fintech and enable efficient delivery of remittances. |

| Ghana launched the biometric-based identity card, as proof of identity, citizenship and residence to support documentation requirements for FSPs. | |

| Launch of Ghana Interbank Payment and Settlement Systems Limited (GhIPSS), facilitating interoperability for FSPs. | |

| 2019 | Ghana adopted the Payment Systems and Services Act 2019 (Act 987), outlining regulatory framework for financial market, including banks and RSPs. |

| Statistics Canada organised the first study on international money transfers by Canadian residents born in official development assistance (ODA) countries. | |

| 2020 | Ghana’s Digital Financial Services (DFS) Policy and IFAD’s PRIME Africa Partnership launched, supporting fintech development, affordable digital financial services (including remittances) and financial inclusion. |

| G20 launched the road map to promote faster, cheaper, transparent and inclusive cross-border payments, including remittances. | |

| 2021 | Government of Ghana proposed 1.75% tax on electronic money transfers, including remittances. |

| Global Affairs Canada and World Bank introduced research initiatives on remittance flows from Canada to identify ways to improve existing remittance services and develop new remittance channels. | |

| Canada enacted the Retail Payment Activities Act; work began on the Retail Payments Oversight Framework (RPOF), a new regulatory regime to oversee payment service providers, including RSPs and enhance security for end users. | |

| Canada continued work on the real-time rail (RTR) payment system for fast transfers and increased service provider competitiveness. | |

| Canada engaged domestic stakeholders to support the Financial Stability Board’s efforts on the cross-border payments road map. The road map seeks to reduce remittance costs and increase the speed of transfers. | |

| 2022 | Ghana enacted the Electronic Transfer Levy (e-Levy) Act, 2022 (Act 1075); rate reduced to 1.50%. |

| The Bank of Ghana launched the regulatory and innovation sandbox to support the live testing of fintech and financial services start-ups. | |

| 2025 | The president of Ghana repealed the e-Levy Act on 2 April. |