Abstract

To explore how emerging adults grapple with the increasing demands of fiscal responsibility, the present study tests a model of identity formation in the domain of finance. We draw on Erikson’s theory of identity formation as operationalized by Marcia’s identity status model, which details four identity statuses: achieved, foreclosed, moratorium, and diffused. A sample of college students (N = 1,511) were surveyed at two time points: in their first (ages 18–21, T1) and fourth (ages 21–24, T2) years of college. Primarily, we find evidence for financial identity stability, although we found some evidence for financial identity regression from moratorium to foreclosed status. After controlling for T1 financial identity, T1 variables were most predictive of changes in T2 foreclosure: Increases in foreclosure were predicted by measures of perceived parental socioeconomic status, parental communication, financial education, and subjective norms at T1.

In industrialized cultures such as the United States, emerging adults are expected to make increasingly complex financial decisions often without having acquired even basic financial knowledge and skills such as budgeting and saving (Consumer Federal Protection Bureau, 2013). Given current economic trends and the significance of identity formation during emerging adulthood, the present study explores identity development in the domain of finance. Identity provides meaning and direction through commitments, values, and goals (Kroger & Marcia, 2011). We contend that a well-formed financial identity may facilitate the transition from adolescent financial dependency to financial self-sufficiency in adulthood.

In the present study, we draw upon Erikson’s (1950, 1968) theory of identity formation and Marcia’s (1966) identity status model, which details four identity statuses: achieved, foreclosed, moratorium, and diffused. To examine financial identity development, we use data from a sample of college students in their first and fourth year of college. In addition to psychological factors indicative of beliefs (i.e., attitude, subjective norms, and perceived behavioral control), we test a number of contextually related variables associated with financial socialization (i.e., parental financial communication, formal financial education, work experiences, and perceived parental socioeconomic status [SES]). We assume that a better understanding of the factors associated with financial identity formation will facilitate the design and implementation of intervention programs aimed at promoting financial literacy and fiscal responsibility among emerging adults.

Theoretical Framework

Identity Formation

Erikson (1950, 1968) has suggested that a fully formed identity is an essential aspect of human development. Indeed, a rich literature suggests that a highly developed sense of identity serves to guide and stabilize individuals, as they navigate the ever-increasing demands of modern living (for reviews, see Berzonsky, 2011; Kroger & Marcia, 2011). Throughout the lifespan, individuals will fluctuate on the continuum between identity diffusion and identity achievement (Erikson, 1950, 1968).

In an effort to operationalize Erikson’s theory for empirical research, Marcia (1966) developed the identity status model and posited exploration and commitment as two fundamental dimensions of identity formation. Exploration represents an active search for information regarding lifestyle, belief, and value options. Commitment reflects selecting the options that best fit the individual’s worldview as well as the application of those self-selected options in different contexts. By intersecting these two dimensions, Marcia derived four patterns of identity formation or statuses (i.e., achieved, foreclosed, moratorium, and diffused) that vary according to the strength of the identity-related exploration and commitment.

Over the years, researchers have extended the domains of identity formation beyond those originally proposed by Erikson (for a review, see Schwartz, 2001). However, the development of an identity related to financial values, the requisite psychological shift toward assuming greater personal responsibility for financial security, and the central role of financial independence in adult life remains unexplored (Arnett, 2000; Furstenberg, Rumbaut, & Settersten, 2005; Littrell, Brooks, Ivery, & Ohmer, 2010). Given the current economic landscape and the societal demand for self-sufficiency in adulthood, a critical examination of the processes whereby young adults form their financial identity seems prudent. Therefore, we conceived this study to test Erickson’s (1950, 1968) concepts of exploration and commitment as operationalized by Marcia (1966) in the domain of finance.

Contextual Factors That Promote or Impede Identity Development

Although much is known about personality correlates, less is known about the socializing factors that predict identity formation. Accordingly, current conceptualizations of identity development have endeavored to incorporate Erikson’s (1968) views on the role of social contexts in shaping development (e.g., Adams & Marshall, 1996; Baumeister & Muraven, 1996; Côté & Levine, 2002; Schachter & Ventura, 2008; Yoder, 2000). Yoder (2000) introduced the concept of barriers to provide “a means by which to describe some of the external influences associated with adolescent and young adult ego identity exploration and also the commitment processes that affect and possibly limit individual developmental options” (p. 95). Other scholars have also suggested that the functional utility of identity commitments, with or without exploration, may depend on how well such commitments fit the demands individuals face in their particular cultural setting (Berzonsky, 2011; Côté & Levine, 2002).

Because previous research has found evidence for both continuity and change in personal identity formation (Kroger, Martinussen, & Marcia, 2010; Meeus, 2011; Yoder, 2000), we examined several potential contextual predictors of financial identity: socialization agents (i.e., parents, school, work), personal beliefs (i.e., financial attitude, perceived control over finances, social norms), and perceived parental SES.

Socialization and Financial Identity Development

Parental financial communication

Previous studies have examined the links between family dynamics and identity formation. One study found that family relationships characterized by flexibility, the free expression of differences, and autonomy are associated with higher levels of exploration (i.e., achieved and moratorium statuses; Grotevant & Cooper, 1985; Perosa, Perosa, & Tam, 1996). Another found that familial warmth, cohesion, and relatedness are associated with higher levels of identity foreclosure (Adams, Berzonsky, & Keating, 2006; Perosa et al., 1996). Yet a third study found that low family expressiveness and limited parental involvement and control are associated with higher levels of identity diffusion (Perosa et al., 1996). Finally, positive communication between parents and their college-aged children concerning financial topics has been shown to promote responsible financial behavior and greater well-being (Jorgensen & Savla, 2010). Hence, we expect parent–emerging adult communication to predict higher financial identity commitments (i.e., higher achieved and foreclosed statuses).

Formal financial education

A number of studies have come to differing conclusions about the benefits associated with formal financial instruction. Some studies find evidence to suggest that exploring financial practices can encourage individuals to reflect upon their personal financial experiences and, so in doing, gain a better understanding of his or her financial attitudes and behaviors (Huston, 2010; McCormick, 2009). From Erikson’s theoretical perspective, access to financial information within an educational setting should promote financial identity formation through exploration and commitment making (i.e., higher achieved and foreclosed statuses). However, the rationale for making such identity commitments may differ. Namely, those with an achieved identity status will make personally meaningful commitments because the information makes sense on a personal level, whereas those with a foreclosed identity status may elect to commit because the information represents a tacit agreement with a prescription offered by an authority figure (e.g., expert, teacher).

Work experiences

It is estimated that 80–90% of adolescents become formally employed at some point during high school (Hirschman & Voloshin, 2007). These early paid-work experiences may provide opportunities to gain a sense of personal responsibility, to test and develop new skills, and to develop a personal understanding of those aspects of work that are beneficial and aversive (Staff, Messersmith, & Schulenberg, 2009). Given the emphasis that Erikson (1968) placed on exploration, more paid work experiences should facilitate financial identity formation (i.e., higher achieved status).

Self-Beliefs and Financial Identity

Because identity scholars generally agree that beliefs and values form the core of an individual’s identity, we tested associations between three financial self-beliefs, which are associated with responsible financial behavior and financial identity (Croy, Gerrans, & Speelman, 2010; Jorgensen & Savla, 2010; Perry & Morris, 2005; Shim, Barber, Card, Xiao, & Serido, 2010; Shim, Serido, & Tang, 2011a): Financial attitude refers to the degree to which a person evaluates or appraises a financial behavior favorably (e.g., saving money is a good idea); financial subjective norm refers to the individual’s perception of the social pressure that influences a decision to perform (or not perform) a financial behavior (e.g., my parents expect me to save money); and perceived behavioral control refers to the individual’s perception of the difficulties associated with the performing of a particular financial behavior (e.g., it is easy for me to save money). Given the available empirical support, we expected these three financial self-beliefs to predict financial identity. Specifically, we expect positive financial attitudes to predict financial identity commitments (i.e., higher achieved and foreclosed statuses). Likewise, we expect higher subjective norms (parents’ expectations) to predict higher foreclosed status (Berzonsky, 2004; Dunkel, Papini, & Berzonsky, 2008). Finally, because identity achievement has been associated with self-determined regulatory efforts, self-esteem, internal locus of control, and ego strength (Schwartz Côté, & Arnett, 2005; Soenens, Berzonsky, Vansteenkiste, Beyers, & Goossens, 2005), we expect higher levels of perceived behavioral control to predict higher achieved status.

Perceived Parental SES

Given the extant literature, we expected SES to predict identity formation during emerging adulthood. However, the extant findings are mixed. On the one hand, studies demonstrate an association between lower SES and higher rates of physical, emotional, and behavioral problems (Berkman & Kawachi, 2000; Oakes & Rossi, 2003) as well as lower rates of educational achievement and attainment (Schoone, Parsons, & Sacker, 2004). On the other hand, researchers find that individuals who experience economic hardship during adolescence often perceive themselves as older than their peers and tend to self-identify as an adult when surveyed during emerging adulthood (Foster, Hagan, & Brooks-Gunn, 2008; Johnson & Mollborn, 2009). Yoder (2000) has also theorized that lower SES environments may create more barriers to exploration. Hence, we expect higher SES environments to predict higher foreclosed status and lower moratorium status, given the absence of financial challenges (e.g., lower exploration given no need to budget or prioritize spending).

In conclusion, we test the following hypotheses:

Method

Participants and Procedure

The students in this study (N = 1,511) responded to both the Wave 1 survey (T1), which was conducted during their first year in college (18–21) at a major, 4-year, public university in the United States, and the Wave 2 survey (T2), which was conducted during their fourth year of attendance (21–24). The respondents included male (37%) and female (63%) students in the following race/ethnic groups: 67.4% White, 14.9% Hispanic/Latino, 9% Asian/Asian American/Pacific Island, 3.4% African American/Black, 1.8% Native American, and 3.5% Other/missing. The ethnic distribution of the respondents was similar to that of all fourth-year students at the university (College Board, 2011); however, females were more heavily represented than males. Parental SES of the sample included 42% lower SES (∼ annual income < US$50,000), 30% middle SES (∼ annual income between US$50 and US$150,000), and 28% higher SES (∼ annual income over US$150,000).

Measures

Financial identity

We used a Financial Identity Scale (Barber, Card, Serido, & Shim, 2011b) based on the revised extended objective measure of ego identity status (Bennion & Adams, 1986) and modified to reflect the personal financial domain. The scale consisted of 12 items designed to measure the degree to which participants saw themselves reflected in each of the four identity statuses: achieved (3 items; e.g., “based on past experiences, I’ve chosen the type of money management style I want for now.”), foreclosed (3 items; e.g., “my parents know what’s best for me in terms of how I should take care of my finances.”), moratorium (3 items; e.g., “there are so many different ways to manage money. I haven’t decided which to follow but I’m trying to figure it out.”), and diffused (3 items; e.g., “I don’t think about money much. I just kind of take it as it comes.”). At T1 and T2, participants rated each item on a 5-point Likert-type scale (1 = strongly disagree to 5 = strongly agree). Cronbach’s α coefficients for the T1-achieved, T1-foreclosed, T1-moratorium, and T1-diffused subscales were .74, .75, .67, and .67, respectively. Cronbach’s α coefficients for the T2-achieved, T2-foreclosed, T2-moratorium, and T2-diffused subscales were .76, .75, .71, and .71, respectively. We used continuous data to maximize the power to detect effects (Aiken & West, 1991).

Parental financial communication

At T1, participants indicated the extent to which their parents discussed six financial matters with them before coming to college (Shim et al., 2010). Items were measured on a 5-point Likert-type scale (1 = strongly disagree to 5 = strongly agree; e.g., “my parents often talk to me about the importance of financial security for my later life,” α = .85). To form the latent construct for this variable, the 6 items were parceled into three manifest variables using an item-to-construct balance approach (Little, Cunningham, Shahar, & Widaman, 2002).

Financial education

At T1, participants were asked two questions to indicate how much financial education they received in high school: number of financial education classes and number of financial workshops/seminars (Lyons, 2003). The possible responses to both questions ranged from 0 (none) to 3 (three or more). Using Cohen’s (1988) benchmarks, the magnitude of the correlation between these 2 items was moderate (r = .33, p < .001). The 2 items were averaged.

Paid work experience

At T1, participants were asked whether or not they were employed outside the home during high school. Responses were coded as follows: 1 (no work experience during high school), 2 (worked but only during the summer), and 3 (worked all year round).

Financial attitudes

At T1, participants were asked to indicate their attitudes toward six typical financial behaviors (e.g., tracking monthly expenses) on a 5-point scale (1 = very unfavorable to 5 = very favorable; α = .85; Shim et al., 2010). The 6 items were parceled into three manifest variables as previously described (Little et al., 2002).

Parental subjective norms

Two scales were used to assess parental subjective norms (Shim et al., 2010). At T1, participants were first asked to indicate on a 5-point scale (1 = strongly disagree to 5 = strongly agree) how strongly they felt their parents believed (parental expectation) they should engage in each of six financial behaviors (e.g., spend within budget). Participants were also asked to indicate on a scale ranging from 1 (not influenced at all) to 5 (significantly influenced) the extent to which their own financial behaviors were influenced by their parents’ expectations (parental influence). We constructed parental subjective norms by multiplying the participant’s parental expectation score by the participant’s parental influence (Ajzen, 1991; (α = .83)). The multiplied scores for these 6 items were parceled into three manifest variables using the method described previously (Little et al., 2002).

Perceived behavioral control

Perceived behavioral control was measured at T1 by means of a single item, asking participants to indicate on a 7-point scale (from 1 = difficult to 7 = easy) how hard it was to stick to their plans when managing their money (Shim et al., 2010).

Perceived parental SES

Perceived parental SES (T1) was measured as the sum of three index variables reported by participants: education level of mother and father (from 1 = less than high school to 5 = graduate school or professional degree) and parental income (from 1 = less than US$50,000 to 4 = more than US$200,000; range of SES = 3–14; Coleman, 1983).

Results

To maximize power and to minimize the number of participants excluded (because of missing data), we performed a single imputation of missing values using a Markov Chain Monte Carlo algorithm in SAS Version 9.4 (Graham, Cumsille, & Elek-Fisk, 2003). We also verified the assumption of normality for all variables. All scales were within the range of acceptable skewness (less than 1.66) and kurtosis (less than 3.52; Kline, 2011). All models were fit using the maximum likelihood method of estimation (in LISREL Version 8.8). To determine model fit, we relied on the root mean square error of approximation (RMSEA) and the comparative fit index (CFI) statistics. Nested models were compared by measuring the change in χ2 relative to the change in degrees of freedom (Kline, 2011).

Measurement Equivalence

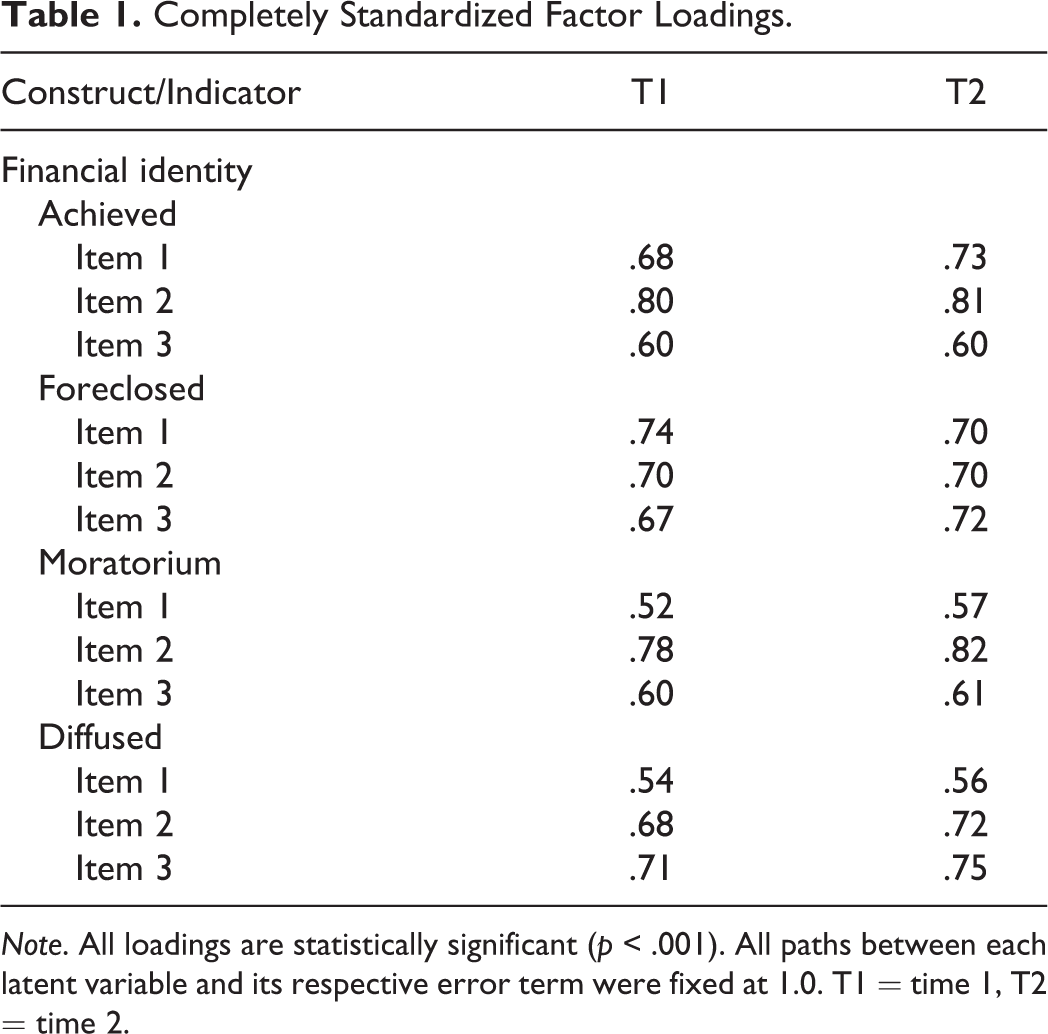

To ensure meaningful comparisons between the financial identity constructs at T1 and T2, we fit a series of three confirmatory factor analysis models to successively evaluate configural, weak, and strong invariance (Little, Preacher, Selig, & Card, 2007). All three tests indicated measurement equivalence. The completely standardized factor loadings are summarized in Table 1.

Completely Standardized Factor Loadings.

Note. All loadings are statistically significant (p < .001). All paths between each latent variable and its respective error term were fixed at 1.0. T1 = time 1, T2 = time 2.

Confirmatory Factor Analysis

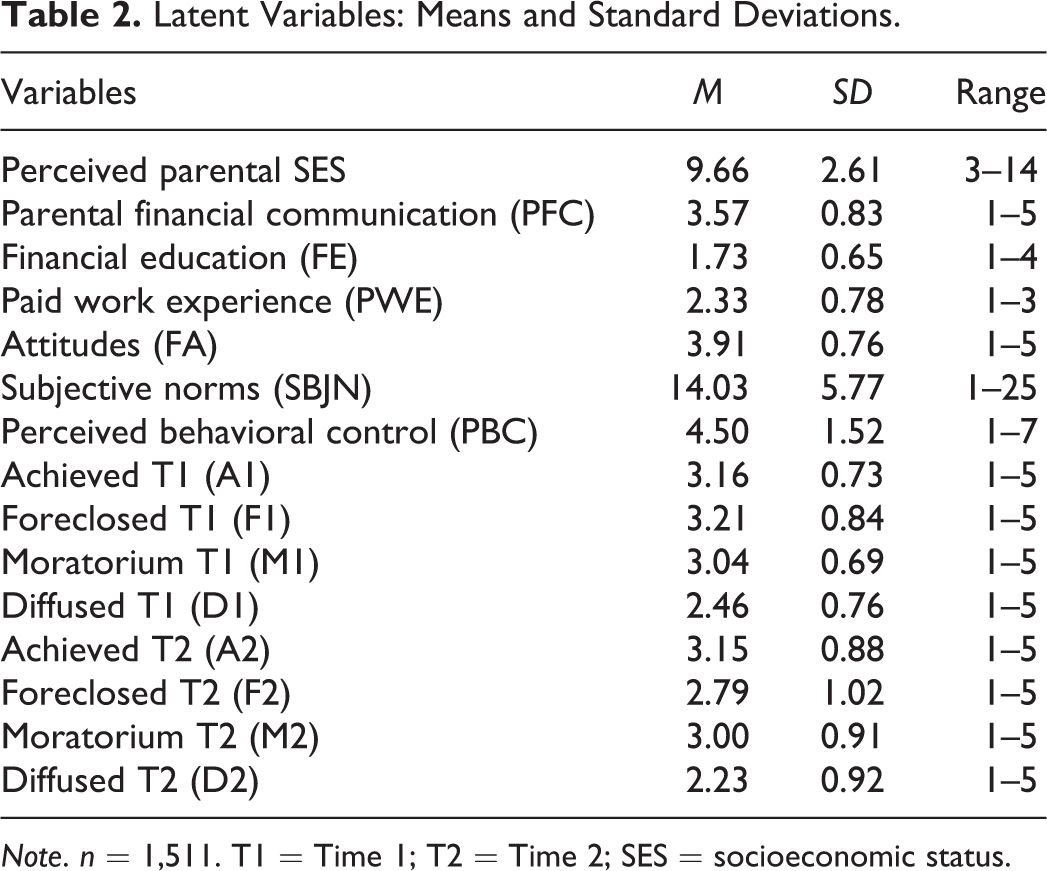

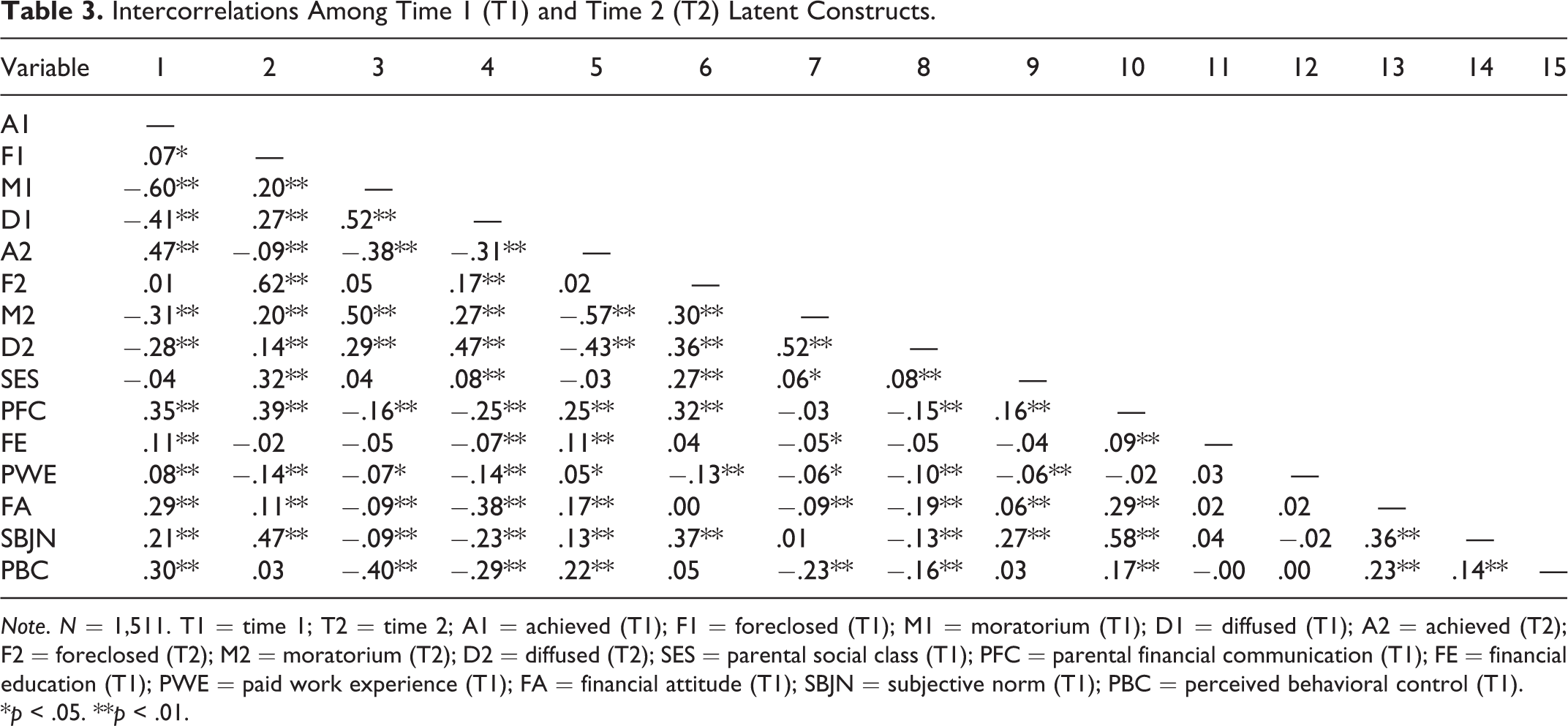

We evaluated the hypothesized measurement structure of the longitudinal model, including the T1 contextual measures (socialization, beliefs, and perceived parental SES), the T1 financial identity, and the T2 measures of financial identity. For scale-setting purposes, the latent variances were fixed at 1.0. All latent constructs in the model were allowed to correlate. The model closely fits the data: χ2(524, n = 2,098) = 2,226.47, RMSEA = .04, 90% confidence interval (CI) [.038, .041], CFI = .97. All hypothesized factor loadings were substantial and significant. The means and standard deviations for the latent variables are shown in Table 2. The bivariate correlations among the constructs are shown in Table 3.

Latent Variables: Means and Standard Deviations.

Note. n = 1,511. T1 = Time 1; T2 = Time 2; SES = socioeconomic status.

Intercorrelations Among Time 1 (T1) and Time 2 (T2) Latent Constructs.

Note. N = 1,511. T1 = time 1; T2 = time 2; A1 = achieved (T1); F1 = foreclosed (T1); M1 = moratorium (T1); D1 = diffused (T1); A2 = achieved (T2); F2 = foreclosed (T2); M2 = moratorium (T2); D2 = diffused (T2); SES = parental social class (T1); PFC = parental financial communication (T1); FE = financial education (T1); PWE = paid work experience (T1); FA = financial attitude (T1); SBJN = subjective norm (T1); PBC = perceived behavioral control (T1).

*p < .05. **p < .01.

Structural Equation Model (SEM) for Testing Hypotheses

To fit the proposed SEM of the predictive relations among the constructs, we allowed all seven T1 independent variables and all four T1 financial identity variables to predict all four T2 financial identity variables. For scale-setting purposes, the latent variances were fixed at 1.0. The seven T1 independent variables and the four T1 identity variables were allowed to correlate with one another, as were the four T2 identity variables. The model fits the data closely: χ2(524, n = 2,098) = 2,226.47, RMSEA = .04, 90% CI [.038, .041], CFI = .97. Results are shown in Figure 1; only significant paths are reported.

Prediction of Time 2 financial identity with Time 1 financial identity and contextual factors.

We next determined whether identity formation in the financial domain would reflect more stability than developmental change over time (Hypothesis 1; see Meeus, 2011). To assess developmental change, we estimated the mean-level comparisons of the T1 to T2 statuses and found a significant decrease in both foreclosed status, t(1,504) = 16.447, p < .000, and diffused status, t(1,504) = 7.767, p < .000. By examining the coefficient pathways in the tested model, we were able to confirm a high level of stability in foreclosed status (.66), while the remaining statuses were moderately stable: moratorium (.46), diffused (.41), and achieved (.39). We found more evidence for stability than for developmental change in identity within the financial domain.

We found full support for our hypothesis that T1 parental financial communication was predictive of higher T2 achieved and T2 foreclosed statuses (Hypothesis 2a). We found that T1 financial education predicted higher T2 foreclosed status, but the association with T2 achieved status was not significant (partial support of Hypothesis 2b). We found no support for our assumption that T1 paid work experience would predict T2 achieved status (Hypothesis 2c).

We found limited support for our assumptions related to financial beliefs. Only T1 parental subjective norms significantly and positively predicted higher T2 foreclosed status (providing support for Hypothesis 3b.). T1 financial attitude did not predict T2 achieved or foreclosed statuses (Hypothesis 3a). T1 perceived behavioral control did not predict T2 achieved status (Hypothesis 3c). Unexpectedly, we found that higher T1 parental subjective norms were significantly and negatively associated with lower T2 diffused status, although the effect size was trivial.

Finally, we found support for our assertion that higher T1 perceived parental SES would positively predict higher T2 foreclosed status (Hypothesis 4a); however, we found no support for the hypothesized inverse relation between T1 perceived parental SES and T2 moratorium status (Hypothesis 4b).

Discussion

Identity development within the financial domain is an important research topic because many emerging adults believe that self-sufficiency, including financial independence, is an essential aspect of subjective adulthood (Arnett, 2000). We proposed a model of financial identity development and tested for evidence of several potential predictors (e.g., parental financial communication, financial education, work experience, and perceived parental SES) in a sample of college students at two different time points (first and fourth year of college). Although we found some evidence of developmental change, primarily, we found evidence for financial identity stability. A more detailed discussion of our findings and implications follows.

Financial Identity Stability and Development

Previous studies find evidence to suggest both stability and developmental change during identity formation (Kroger et al., 2010; Meeus, 2011). In the financial domain, our findings suggest stability (rather than developmental change), as T1 financial identity was the most robust predictor of T2 financial identity.

Regarding developmental change, after controlling for T1 financial identity, T1 variables were most predictive of changes in T2 foreclosure. That is, increases in foreclosure at T2 were predicted by T1 contextual variables (i.e., perceived parental SES, parental communication, formal education, and subjective norms) and T1 moratorium status. These results suggest that during college, students scoring high on financial identity foreclosure strengthen commitments to the financial prescriptions of authority figures, namely, parents and teachers.

Identity foreclosure may increase over time for a variety of reasons. For instance, although Erikson (1968) described severe, prolonged, and aggravated forms of identity crisis (exploration), he also asserted that “the vast majority of young people … can go along with their parents in a kind of fraternal identification” (p. 33). Thus, Erikson believed that even in modern societies, most young people work through their identity crises in muted and barely discernible ways. With so many emerging adults in the United States currently relying on parents for continued emotional and financial support (Fingerman, Miller, Birditt, & Zarit, 2009; Settersten, 2012), a foreclosed financial identity status may reflect the ongoing need to rely on parents for social as well as financial support during the transition to adulthood. As such, challenging parental prescriptions during the fourth year of college would likely prove hazardous to educational and financial success. If so, those students who scored high on financial identity foreclosure might begin to explore financial identity options after graduation, once some financial independence has been attained.

Erikson (1968) also stressed the importance of identity commitments, contending that these commitments represent the “cornerstone of identity” (p. 125). This conjecture has been demonstrated empirically. The presence of identity commitments, with or without identity exploration, appears to offer protection against a variety of health-compromising behaviors (e.g., Schwartz et al., 2011). More recently, scholars have suggested that the functional utility of identity commitments, regardless of prior exploration, may depend on how well such commitments fit with the societal demands placed on the individual (Berzonsky, 2011, Côté & Levine, 2002). Thus, in relatively stable, tradition-oriented contexts, identity foreclosure may prove sufficient, whereas contexts characterized by rapid change and transition may favor identity achievement. These results may also suggest the absence of experiences (barriers) that could cast doubt on the appropriateness of such commitments (Yoder, 2000).

It is worth noting that the 2008 financial crisis occurred between the T1 survey and the T2 survey. Hence, it is possible some participants were engaged in reconsidering their alternatives in light of recent macroeconomic events. If so, it might explain the weak but positive association we found between T1 moratorium and T2 foreclosure, which suggests regression or stalled exploratory efforts toward personally meaningful financial commitments (Kroger, 1996). Additional waves of data could test this hypothesis.

Contextual Factors and Change in Financial Identity Development

After controlling for T1 financial identity, only T1 parental financial communication predicted T2 achieved status. This finding adds to the extant literature on the ways that various parental socialization techniques may promote or inhibit identity formation (e.g., Adams, Ryan, & Keating, 2000; Grotevant & Cooper, 1985; Perosa et al., 1996). Although the association is weak, future research might explore this association further. For instance, our data set provides only the valence of the communication (i.e., positive, conflictual) but not the tone or the content of the conversations, which could play a significant role. If so, open and supportive (rather than admonitory) discussions may encourage self-expression and critical thinking regarding financial choices, thereby promoting identity achievement (Grotevant & Cooper, 1985; Perosa et al., 1996).

We found some support for other contextual factors. First, we found a positive association between higher T1 perceived parental SES and higher T2 foreclosed status. This finding may reflect a continued reliance on parents for financial support, a reliance that may constrain an individual’s exploration around financial issues. Second, relatedly, the positive association we found between T1 parental subjective norm (i.e., the extent to which students are motivated to comply with parental expectations) and T2 foreclosed status may indicate that these emerging adults may strengthen their commitment to the financial prescriptions of their parents while attending college. Adopting a foreclosed identity status may help an emerging adult achieve developmentally appropriate milestones when the advice of a trusted parent suits the current societal demands (Berzonsky, 2011; Côté & Levine, 2002), in this case, financial self-sufficiency. Also, the correlation between parental communication and parental subjective norms suggests that the students we surveyed were aware of their parents’ expectations regarding their fiscal behavior. Third, although prior studies reported mixed findings on the impact of financial education, we found evidence that T1 formal financial education received in high school predicts T2 foreclosed status (e.g., Huston, 2010; McCormick 2009). Perhaps our participants’ early financial education improved their factual knowledge to such a degree that they deemed further exploration unnecessary. Finally, consistent with other scholars (e.g., Monahan, Lee, & Steinberg, 2011), we did not find the expected association between T1 work experience and T2 identity formation. We surmise that the unskilled manual labor and service occupations that adolescents typically engage in may limit their chances to develop ideas about their occupational futures and to test their capacity to perform adult work roles (Arnett, 2000; Skorikov & Vondracek, 2011).

Limitations and Future Research

Our findings suggest that identity in the domain of finances may be a timely and relevant topic for future research. However, our findings should be interpreted in light of server limitations. To begin, the sample consisted of traditionally aged undergraduate students attending a university in the United States. Future studies should seek to expand and diversify the sample to include emerging adults who do not attend college.

As the associations among the variables we selected were small, future studies might explore other influential variables such as additional parenting style, access to financial services (e.g., savings accounts, credit cards), quality of life, social relations, and identity development in other identity domains. These variables may uncover associations that shed further light on the mechanisms that underpin fiscal responsibility in adulthood.

Our study also relied on retrospective, self-report questionnaires. Future studies might consider bringing students and their parents into a laboratory setting, where conversations about financial matters could be observed and coded for a range of communication indicators. Such methods could provide insight into the qualitative and quantitative factors most strongly associated with financial identity achievement.

The restricted range of some of our measures limited the number of statistical associations that could exist among the variables. In particular, the measures we used to explore perceived parental SES, formal financial education, and work-related experiences were truncated. Future researchers might address this limitation quantitatively by expanding both the range and the number of questions asked.

Finally, our study was not designed to measure the extent to which participants pursued self-understanding, even though self-reflection is a major undertaking during the college years. In particular, early spending and saving habits may contribute to financial identity formation. In the future, researchers might consider focusing on early and middle adolescence to better understand the role that financial identity formation plays in shaping consumer behaviors and financial self-sufficiency in emerging adulthood.

Implications for Practice

In light of our findings and our interpretations, parents may want to promote financial self-sufficiency at home by discussing the financial management practices embedded in facets of everyday family life. Furthermore, given the importance of parents and family communication patterns (Allen, 2008; Koerner & Fitzpatrick, 2006), interventions designed to support financial identity development should include a component that not only helps parents grasp the importance of their role but also provides practical strategies aimed at enhancing their offspring’s involvement in financial decision making. Practitioners might, for example, stress the importance of creating a climate of open communication, wherein many topics and points of view can be freely expressed and discussed (Koerner & Fitzpatrick, 2006).

Concluding Remarks

The current economic realities such as global economic instability and the societal shift toward individuals assuming greater responsibility for personal financial security may delay or even threaten self-sufficiency in adulthood (Littrell et al., 2010). Developing a committed financial identity status could facilitate movement toward adult roles and fiscal responsibility. Thus, applying identity formation concepts to the domain of finance might illuminate the process, whereby the next generation of young adults progresses toward financial independence.

Footnotes

Authors' Contribution

Leslie A. Bosch contributed to conception, design, and acquisition; drafted and critically revised the manuscript; gave final approval; and agreed to be accountable for all aspects of the work ensuring integrity and accuracy. Joyce Serido contributed to conception, acquisition, analysis, and interpretation; critically revised the manuscript; gave final approval; and agreed to be accountable for all aspects of the work ensuring integrity and accuracy. Noel A. Card contributed to design, analysis, and interpretation; critically revised the manuscript; gave final approval; and agreed to be accountable for all aspects of the work ensuring integrity and accuracy. Soyeon Shim contributed to acquisition and interpretation, critically revised the manuscript, gave final approval, and agreed to be accountable for all aspects of the work ensuring integrity and accuracy. Bonnie Barber contributed to conception and design, critically revised the manuscript, gave final approval, and agreed to be accountable for all aspects of the work ensuring integrity and accuracy.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.