Abstract

Debt levels in the Southern African Development Community (SADC) have been rising over the years as countries undertake infrastructure projects and the increased use of bilateral and private credit. Although on aggregate the debt levels are within SADC recommendations on macroeconomic convergence, there are growing fears that a number of countries in the region might default and indeed some are already in default. The frequent occurrence of debt crisis is a cause for concern. This research is an attempt to determine the significant predictors from a small set of variables commonly touted as important in debt crisis prediction. The research considered the output gap, real exchange rate, external debt ratios, commodity shocks and quality of governance as potential predictors. The factor variables being of particular interest Empirical findings on these potential predictors is somehow mixed, which partly is accounted for by the differences in model specifications from author to author. The research employed the event study and fixed effects logistic regression for modelling the probability of default of public debt. Results of the model illustrate that governance indicators and commodity price shocks (global level) were not statistically significant predictors of debt crisis as commonly suggested by theory. However the external debt, output and the real foreign exchange rate were all significant. Real output was shown to be one of the most important predictors of debt crisis. The estimated probability model fared relatively better than a random model.

Keywords

Introduction

According to the Southern African Development Community (SADC) most countries in the region had high external debts around the 1990s. By 2001 external debt to Gross Domestic Product (GDP) in Angola, Democratic Republic of Congo (DRC), Malawi, Tanzania, Zambia and Mozambique was more than the size of the domestic economy 1 . Consequently most member countries benefited from the for debt relief programs since the establishment of the Highly Indebted Poor Countries Initiative (HIPC) by the World Bank (WB) and International Monetary Fund (IMF) in 1995. Indeed this initiative has managed to reduce the indebtedness of most countries in the region. According to SADC most countries in the region by 2012 had lower debt to GDP ratios, on average 40%, with the exception of Seychelles and Zimbabwe which had debts beyond the SADC's Macroeconomic Convergence target of 60% 2 . Whilst SADC recommends a maximum threshold of 60% 3 , IMF recommends debt ratios within the range of 35% to 70% (on present value basis) 4 as laid out in the Debt Sustainability Framework for low income countries. Countries with weak institutional frameworks are expected to have lower debt ratios than those with strong institutional policies.

Although debt levels have decreased considerably compared to the pre 1990s era, there are renewed concerns on rising debt levels in the region and the world at large. In Sub Saharan Africa, most of the debt financing is believed to be coming from private lenders and the growing influence of Chinese funded infrastructure projects in the region 5 . In addition most of the private lenders have shown very little appetite for debt write-offs or restructurings 6 and more over pays little regard for debt sustainability. This is also on the backdrop of rising debt levels in advanced economies as well. According to Bloomberg global debt is at record levels (https://www.bloomberg.com/businessweek), which the IMF, as reported by Guardian, is way above the pre 2008 global financial crisis and could lead to another global meltdown 7 . Given the costs of financial crisis, it is prudent that economies be insulated against such occurrences by maintaining sustainable debt levels-both corporates and sovereigns.

Thus it comes as no surprise that there are renewed fears that the very same economies which some decades ago received debt reliefs may default on their debts. The Economist posits that “Debt stalks Africa once again” 8 . Zambia is an example of a HIPC beneficiary which again today is on the very edge of a debt crisis cliff. Low commodity prices especially copper and weak institutional policies are normally cited as the main drivers of debt pressures. Mozambique's recent revelations of hidden debts amounting to about $2billion 9 further strains the capacity of the country to meet its debt obligations. In fact Mozambique has been in default since 2016 and has expressed incapacity to pay off the huge privately funded debt until after a decade. Again repayment scenarios are premised on revenues from commodities, mostly gas in this instance 10 .

Despite the debt reliefs some decades ago, most SADC countries are experiencing or have fallen back into default. Many point to the rising debt levels which are believed to be unsustainable. Gündüz (2017) argue that external shocks to LICs, such as adverse shocks to commodity prices, could lead to a wave of defaults. Kraay and Nehru (2006) empirical evidence emphasise the importance of institutional policies in the occurrence of debt crisis in low-income countries. In support, Bandiera, Crespo and Vincelette, (2011) argued that the frequent occurrence of debt crisis is in indication of weak underlying institutional policies. The Debt Sustainability Framework was therefore formulated based on the influential paper of Kraay and Nehru (2006) findings. Gündüz (2017) also highlights that multilateral institutions now places greater emphasis on quality of institutions. Since lenders are worried about credit defaults, institutional policies or quality of governance should therefore be a significant determinant of credit events.

High debt ratios have been seen to be positively associated with debt defaults (Herz and Tong 2008). Debt has been rising in the region, and in some countries it's almost at unsustainable levels. Though the risk of defaulting is high, SADC debt ratios are not among the top category of sovereign debts in the world. Japan for instance has carried very high debt ratios for more than a decade. In 2017 it was about 239% and yet has always honored its obligations.

The Financial Times notes that “despite two decades of warnings about fiscal Armageddon, a debt crisis never arrived. It never even came close, despite shocks on the scale of Lehman Brothers and the Tohoku earthquake” 11 .

Some would therefore argue that size does not matter but the sustainability of the debts matters. Accordingly Gündüz (2017) avers that economies with good institutional policies substantially reduce the risk debt crisis even at very high debt levels. However higher debt ratios significantly raises the probability of debt crisis and currency crisis too (Christian, Bernhard and Volker 2007). Similarly Gourinchas and Obstfeld (2012) contends that the probability of debt crisis is increased by high levels of public debt. This is also particularly true when debts have been amassed on the strength of economic growth buoyed by commodity booms. Sudden commodity shocks can therefore potentially spur debt defaults.

Statement of the problem

The high incidence and recurrence of public defaults in the region is worrisome. Davis, et al. (2016) notes the extensive coverage of the impact of debt on the likelihood of debt distress though much of it has extensively examined mostly developed nations at the expense of developing countries. Given that defaults in high income countries are associated with a significant drop in economic growth (Eduardo and Ugo 2011) the high frequency of defaults in developing countries is disturbing. Although very little has been researched on the costs of sovereign defaults of developing countries, it is possible that the economic costs might be even larger and long lasting than expected. Whilst this research is not an investigation on the economic costs of public defaults, it is hoped that in finding the key drivers of public defaults policy makers will take corrective action to avoid defaults in future. In addition debt crisis negatively affects output and the attainment of social development plans (Svetlana, et al., 2018). It is therefore important that a close review of the main factors commonly touted as key drivers of debt defaults be examined. Effectively the research seeks to determine the impact of institutional factors, commodities price volatility, among other factors on the likelihood of public defaults in SADC.

Most of the developing countries are normally believed to have weak governance systems which in turn could have implications on the likelihood of public defaults. In addition commodities also play a significant role in African economies to the extent that a greater portion of their revenues are directly tied to the performance of commodity prices. Shocks in the global economy could have disastrous effects on commodities and in turn on government's ability to repay their debts. It is generally less understood how and why defaults continue to happen in developing economies particularly in African countries. This research therefore seeks to establish the causal link between institutional factors, commodities and other factors with debt defaults.

Literature review

Literature on prediction of debt crisis is abundant especially for developed countries, very little however exists for developing economies. Gündüz (2017) laments the low coverage of the empirical estimation of debt crisis in developing countries, despite the high incidence of debt distress events in developing countries. In spite of that, empirical findings from developed countries have shown that only a very limited set of variables are significant in predicting financial crisis in general.

Definition of debt crisis

Despite the large literature there is no generally accepted empirical definition of sovereign default (Manasse, Roubini and Schimmelpfennig 2003). For instance Herz and Tong (2008) used Paris Club debt rescheduling (treatments) to identify debt crisis. Gerling et al. (2017) on the other hand relies on private creditors to assess public defaults. In his case credit events are defaults or reschedulings greater than 0.2% of GDP with a year on year growth at larger than 10%. For (Cohen and Valadier 2011) a debt crisis occurs when the sum of the arrears exceed 5% of the outstanding debt or when a country receives IMF financial support in excess of 50% of its annual quota. The lack of best practice in dating crisis (Luc and Valencia 2008) partly explains the somewhat mixed results of debt crisis determinants. Researchers generally use various dating approaches and as well as different debt distress indicators. In spite of the differences, most studies focus on some measures of arrears to debt outstanding and IMF support above some threshold ranging from 50% to 100%.

Commonly used variables

Evidence from empirical literature indicates that there are variables which are more likely than others to play a causal role in debt crisis prediction (Gourinchas and Obstfeld 2012). (Svetlana et al., 2018), also concurs that there are generally a very small set of factors that are robust in assessing the probability of crisis occurrence. For instance (Gourinchas and Obstfeld 2012) examined the impact of real GDP, domestic credit, fiscal variable, the current account balance, debt, the real interest rate, the real foreign exchange rate, and reserves as they relate to the occurrence of financial crisis. Kraay and Nehru (2006) on the other considers the real GDP, debt burdens and quality of policies.

With respect to (Gourinchas and Obstfeld 2012) specification this research considers output, real exchange rate, public debt, commodity prices shocks and institutional quality/governance measures as potential predictors of public debt crisis. This research therefore seeks to assess the significance of the variables deemed to be important in early warning systems of public debt crisis. It is not an attempt to investigate on the factors driving public debts crisis in SADC. Specifically the intention is to test the hypothesis that commodity shocks, quality of governance and public debt are significant predictors of debt crisis. Given the recommendation to focus on homogenous groups of countries, Klomp (2010) for example, the focus of this research is on the SADC region. It is assumed countries in the region are more or less affected by the same factors.

The following is a review of the variables under consideration.

Public debt and debt crisis

Although there are various measures used for measuring public defaults most concentrate on external debts and how these may affect the occurrence of crisis. The common understanding is that governments rarely default on domestic debts because of inflation financing. It is therefore no surprise that Herz and Tong (2008) found large debt to GDP ratios to be positively related with a greater likelihood of debt crises. A finding in keeping with Gündüz (2017) results.

In a separate study Reinhart and Rogoff (2011) notes that public debt increases around the period of crisis (both pre and post periods). This happens because most governments would use external funding (or guarantee lending to private banks) to bail out the failing banks and this automatically increases their external loan book coupled with a contraction in GDP makes the government more susceptible to default. Reinhart and Rogoff (2011) asserts that banking crisis escalate the probability of default, presumably via increased sovereign debts and a general weakening of the macro environment.

Although (Cohen and Valadier 2011), and possibly many other authors, finds that indebtedness accounts for 50% of the risk factors giving rise to sovereign debt crises, it does not necessarily follow that high public debts would generally lead to defaults. No doubt other countries are able to carry debts beyond the size of their GDPs for long periods without even defaulting. Other factors also come into play. For instance (Bandiera, Crespo and Vincelette 2011) observed that countries with external debt in excess of 50 percent of GDP reduce the likelihood of default by maintaining a stable macroeconomic environment. They further contend that improving the institutional environment and the quality of economic policies goes a long way in reducing default probability (Bandiera, Crespo and Vincelette 2011). Empirical findings by other researchers also emphasizes the importance of governance indicators in crisis prediction, for instance Cohen and Valadier (2011), and Manasse, Roubini and Schimmelpfennig (2003).

High debt ratios is thus a significant factor in sovereign debt crisis but most importantly is the quality of policies and regulations in place that increases the likelihood of default.

Debt crisis and quality of governance

The role of democracy and institutional policies in economic growth is extensively covered in literature. For instance Moral-Benito (2009) concluded that quality of governance (as measured by the Freedom House Index) is a significant driver of economic growth. Mauro (1995) also observed that corruption (an indication of weak governance policies) negatively affects the economy via the investment channel.

Whilst this view is generally acceptable in economic growth, this has not been extensively tested on how this might affect occurrence of debt crisis. Kraay and Nehru (2006) argued that despite the theoretical prominence of quality of governance in debt crisis prediction, empirical research was however limited especially in LICs. Kraay and Nehru (2006) went on to show that the level of indebtedness and governance were significant drivers of sovereign defaults. In contrast Bandiera, Crespo and Vincelette, (2011) did not find governance to be a significant predictor of sovereign defaults in highly indebted countries.

Empirical literature has employed a variety of measures for governance quality; political variables such as election years dummy, and legislation polarization- a measure of the degree of democracy (Dreher, Herz and Karb 2006); arithmetic mean of the rule of law, the quality of bureaucracy, control of corruption, using the ICRG database (Honda, Tapsoba and Issifou 2018); world bank CPAIA (Kraay and Nehru 2006). Despite the differences most concur that governance is significant in driving the likelihood of debt crisis. The transmission channel is that weak macroeconomic policies as expose economic structures to adverse external shocks, which eventually hinder sustained economic growth and in turn increase the likelihood of debt crisis (Gündüz 2017).

According to Klomp (2010), democracy is an enabler in the process of restoring financial stability. Klomp (2010) further argues that political instability increases the uncertainty of fiscal policies and in turn increasing the uncertainty in financial markets (banking crisis). Banking crisis have been shown to trigger public defaults. For instance, Gourinchas and Obstfeld (2012) notes that banking crisis bailouts may induce sovereign default crisis.

However Klomp (2010) and Eichengreen and Arteta (2000) using a variety of measures of institutional variables, failed to prove the long held hypothesis that political institutional environment and stability of the banking sector (banking crisis). Eichengreen and Arteta (2000) thus concluded that weaker institutional factors, in spite of the clear, intuitive and logical arguments in favor of regulatory quality, were not significant in driving banking crisis risk and by extension to public defaults.

On the other hand Honda, Tapsoba and Issifou (2018) and others showed that enhanced quality of government and political stability reduces the probability of fiscal crisis occurrence. Luc and Valencia (2008), also notes that weak institutional policies worsen the economic impact of crisis. Economies with poor institutional frameworks should therefore “repair the roof when the sun is shining” to avoid the costly debt defaults (Honda, Tapsoba and Issifou 2018).

Commodity prices and sovereign defaults

Economies of most less developed countries are heavily dependent on commodity prices. For instance copper prices in Zambia, crude oil Angola, DRC oil and mineral ores and Zimbabwe agricultural and mineral ores. Falling international commodity prices, ceteris paribus, should directly affect economic prospects through reduced state revenues. Some political instabilities have also been linked to commodity price shocks (Bazzi and Blattman 2014). Obviously this just shows the importance of commodity shocks to state stability.

Gündüz (2017) results confirms that adverse external shocks raise the default probability in LICs. Declines in non-energy commodity prices and increases in energy prices for oil importers, are significantly associated with increased likelihood of debt distress (Gündüz 2017). Gündüz (2017) found real non-energy commodity prices to be the most influential variable of default

In contrast Svetlana et al. (2018) results failed to prove statistically the link between commodity prices and fiscal crisis (a broader definition which also includes public debt defaults). They reasoned that commodity shocks, booms for instance, may have an indirect effect via overheating of the domestic economy. Overheating of the economy is a strong signal of a crisis (Svetlana et al., 2018)

Foreign exchange rates and debt crisis

Generally measures of the real exchange rate among other factors like GDP, reserves and domestic credit have generally been viewed as leading predictors of financial crisis. This is logical given the widespread use of external debt as a key variable to assess the likelihood of debt crisis.

It is expected that interest and principal payments would balloon when exchange rates increase or overheat and this could induce debt defaults, downgrading of sovereign ratings, increase in sovereign risk premium and further increasing the likelihood of default (Bauer, Herz and Karb 2011). Gourinchas and Obstfeld (2012) also shows that real exchange rates, among other factors, are significant predictors of debt crisis.

Output and debt crisis

It is common cause that there are no generally agreeable sustainable debt levels even for economies in the same income bracket. Of course the size of the economy matters, the larger the economy the more debt it can handle, the case of Japan and Zambia. Debt ratios are around 230% in the former and just above 50% in the latter yet Zambia is on the brink of default. Therefore this may seem to indicate that output in isolation may not be that significant but significant when size of the economy and debt ratios are analyzed simultaneously. It is no surprise then that IMF has some kind of sustainability framework (which takes into account various other factors) for countries in different income groups.

Empirical literature is mixed on how output affects debt crisis. For instance Gourinchas and Obstfeld (2012) observed that economies overheat in run up to crisis. However their statistical tests proved that output gap was an insignificant predictor of public debt crisis. In a separate study Gündüz (2017) also found the real GDP growth to be insignificant in debt crisis prediction. Furthermore Svetlana, et al. (2018) did not find meaningful results on how output gap affects the likelihood of fiscal crisis

It is generally accepted that sovereign defaults have a strong negative contemporaneous effect on growth (Eduardo and Ugo 2011). However the effect of output on debt crisis is somehow mixed.

On the other hand Eduardo and Ugo (2011) notes that defaults occur when the economy is in a trough (recession). This could thus be suggestive evidence that lower growth increases the likelihood of public defaults and in the thinking of Eduardo and Ugo (2011) debt crisis occurs at the peak of economic downturns. They reasoned that a slowdown in GDP growth may have negative effects on fiscal revenues and ultimately government's ability to pay public debts (Eduardo and Ugo 2011). This is also a view shared by Bauer, Herz and Karb (2011)

Contribution to literature and relevance

As previously alluded to much of the studies have focused mainly on advanced economies and very little on developing countries. This is particularly worrying given the increased push to regionalism. Regional integration is no doubt beneficial but it also brings along added risk through contagion effects. The risk is further amplified if the risk factors are relatively unknown, hence the focus on the determinants of debt crisis SADC. Consequently this shall further the understanding public defaults in the SADC region, given the high frequency of debt distress in SADC.

Furthermore Caggiano, Calice and Leonida (2014) showed that a regional based early warning system (EWS) outperforms a pooled EWS. Caggiano, Calice and Leonida (2014) argued that analyzing homogenous economies increases the prediction capability of EWS. In this regard this research evaluates economies in the SADC region, and arguably it could be the first to analyse debt prediction in SADC.

Many researchers use subjective judgements in the dating of crisis. For instance some treat years after the first year of crisis to be a tranquil period (Eichengreen and Arteta, 2000) and some completely discards the subsequent periods, Caggiano, Calice and Leonida (2014). Excluding them from the sample however reduces the predictive power of the model especially in a small sample. In dating debt crisis this research borrows from the Frankel and Rose (1996) methodology on currency crisis. In simpler terms debt crisis occurs when the annual growth in arrears exceed the 5% threshold as the second qualifier. Arguably this could be the first attempt in using such a dating system. The main emphasis is the need to adopt quantitative approaches rather than depend on subjective forms of dating.

Whilst Caggiano, Calice and Leonida (2014) leave out Zimbabwe Angola and DRC from their studies because of inflation and currency depreciation, the study makes no distinction or assumption of the cause or source of exchange rate depreciation between countries. And in any case the study makes use of real data to remove the effects of inflation. Namibia and Seychelles are not part of the research because of missing data especially on key variables like external debt balances, private arrears and rescheduling, from which the research relies on calculating debt crisis.

Methodology

Debt crisis dating

As previously mentioned various methods have been employed in the identification and dating of the crisis. In identifying debt crisis, just like Eduardo and Ugo (2011) the research mainly on focusses default on private lenders debt. However we also take into account defaults as measured by the use of IMF General Resources Account (GRA) specifically the Stand-By Arrangements, Extended Fund Facilities and the Extended Credit Facility.

The following are the conditions for identifying debt crisis

As in Kraay and Nehru (2006) the total of interest and principal arrears must exceed 5 percent of the total debt outstanding. This research considers only arrears and rescheduling of interest and principal components on private creditors. In addition the annual increase should be more than 5% for it to be classified as a new debt crisis. An approach borrowed from the Frankel and Rose (1996) currency crisis research. A country must receive substantial balance of payment support from IMF in the form of Stand-By Arrangements or Extended Fund Facilities and Credit Extended Credit Facility. Substantial support occurs when a country draws down more than 50 percent of its quota from the IMF GRA as used in Gündüz (2017), Cohen and Valadier (2011) and Kraay and Nehru (2006). Support above 50% is deemed exceptional and is presumed to indicate actual debt distress avoided through IMF support (Cohen and Valadier 2011).

For the period 1983 to 2016, the unconditional probability of a debt crisis occurring was about 32%. That is from 416 observations, 132 observations were default episodes. The debt crisis observations were largely comparable to the dataset of (Reinhart and Rogoff 2009), at least for common countries; Angola, DRC, Madagascar, Malawi, Mozambique, Tanzania, Zambia and Zimbabwe.

Post crisis bias

The issue of post-crisis bias normally associated with dating of sovereign defaults is a cause for concern in sovereign crisis studies and how one treats years after the crisis introduces bias to the model (Caggiano, Calice and Leonida 2014). In order to avoid counting the same crisis as a new crisis most studies use a variety of techniques to isolate crisis periods. However it is important to note that there is no generally accepted approach in dealing with this crisis bias duration because most methods are to a large extent arbitrary which in part explains the differing results different authors produce (Eichengreen and Arteta 2000).

Empirical literature has treated the post crisis bias differently. The following cases are illustrative; Cohen and Valadier (2011) takes default periods as years following three years of tranquility; Kraay and Nehru (2006) uses periods of at least 3 years followed by 5 years of no distress; Gerling, et al. (2017) on the other hand exclude cases of continued reporting of previously defaulted amounts, which they defined as defaulted nominal amounts that grow by less than 10 percent per year; Eduardo and Ugo (2011) excludes default events within three years of the previous default; Caggiano, Calice and Leonida (2014) uses a multinomial model in order to preserve the potential valuable information. On the other hand Dawooda, Horsewood and Strobel (2017) included all crisis periods as individual crisis episodes in their logit model. They reasoned that dropping crisis periods after the first may lead to loss of valuable information from the sample

It is therefore clear that there are various approaches acceptable in handling the post crisis bias. This research takes into account all debt crisis events as independent events given the requirement that the year on year growth in arrears should be at least 5% higher than the previous year figure.

Potential predictors

The following variables are to be used: public debt to GDP ratio, national output, real foreign exchange rate, energy price, non-energy prices and governance quality. As in Gourinchas and Obstfeld (2012), output and real exchange rates is measured as percentage deviations from trend. Commodity price shocks are measured as first differences of annual prices (Eberhardt and Presbitero 2018). The energy price index is composed of 5% of coal, crude oil (84%) and natural gas (11%). Non-energy prices on the hand includes metals (31.6%), Agricultural commodities (64.9%) and Fertiliser (3.6%). No attempt is made to create country specific commodity prices in the spirit of (Bazzi and Blattman 2014), instead all commodity prices are time-specific variables as used by Gündüz (2017).

For quality of governance the research employs primarily the freedom house index. In addition the CPIA is used as a test of robustness of the freedom house index. The only drawback is that the CPIA) 12 is available from 1996 which could be a short period considering the number of countries in the panel. The research uses the regulatory quality and control of corruption from CPIA, these are deemed important given the low rankings of most developing countries on the ease of doing business index, open budget and other empirical findings. As previously discussed weak policies may negatively impact economic performance and sovereign defaults.

The Freedom house composite index is the main variable for quality of governance due to its long series nature. It takes into account the political rights and civil liberties enjoyed by the citizens. Principally it measures the freedoms enjoyed by the citizens with respect to freedom of expression and belief, associational and organizational rights, rule of law, and personal autonomy and individual rights among other factors. Countries are then rated on a scale of 1 to 7, high scores being the worst 13 .

(Gündüz 2017) argue that reforming economic institutions is difficult because institutions are dependent on the prevailing political framework and political power distribution in society. Thus it seems that economic institutions are perhaps dependent on the quality of civil liberties and political freedoms. High civil liberties and freedoms of association and expression affects how political institutions work. An open political environment is bound to increase government accountability and transparency in fiscal matters. This also tends to reduce corruption; effectiveness of government programs increase and efficient allocation of resources is enhanced because of adherence to rule of law instead of “rule of man”.

To manage the potential endogeneity problem, the research employs 1–2 year lags in all regressors except commodity prices as is standard in empirical literature Jan Babecký a, et al. (2013).

As is common in most empirical work on crisis prediction, Gourinchas and Obstfeld (2012) for instance, the research employs event studies and a logit model for modelling the likelihood of occurrence of debt crisis. Event studies typically illustrate how variables behave at pre-crisis, crisis and post-crisis date.

Event study

Event study are important visual representations of variables evolution around default periods. It is a commonly used technique, Manasse, Roubini and Schimmelpfennig (2003) and Gerling, et al. (2017), for instance. As alluded to by Gerling, et al. (2017) this helps to understand the context in which debt crisis occur without necessarily implying causality.

In line with Gourinchas and Obstfeld (2012) an event study analysis is done as the first visual representation of behavior of variables. An 11 year window period around the default date is normally used, 5 years before and 5 years after. The 5 years takes into account the usually slow adjustment process of variables around default events (Reinhart and Rogoff (2009); Reinhart and Reinhart (2011) as cited in Gourinchas and Obstfeld (2012).

The research closely follow Gourinchas and Obstfeld (2012) and a fixed effects panel regression model for each variable is specified as follows;

For countries that had debt crisis episodes for a long time, the first episode was considered to be the event date. Subsequent crisis episodes were then removed (deleted from the sample). The next crisis event should be at least 5 years away from the first event. Short episodes of debt crisis were also removed for countries with protracted distress periods. In countries where crisis events are not frequent event a single period count as an event date as long as there are no other crisis events in the vicinity (at least 5years).

Logit model

The following panel logistic function with country fixed effects is used to estimate the likelihood of occurrence of public debt crisis and the potential predictors as listed below:

Where

Data presentation and analysis

Data description

Evolution of debt defaults

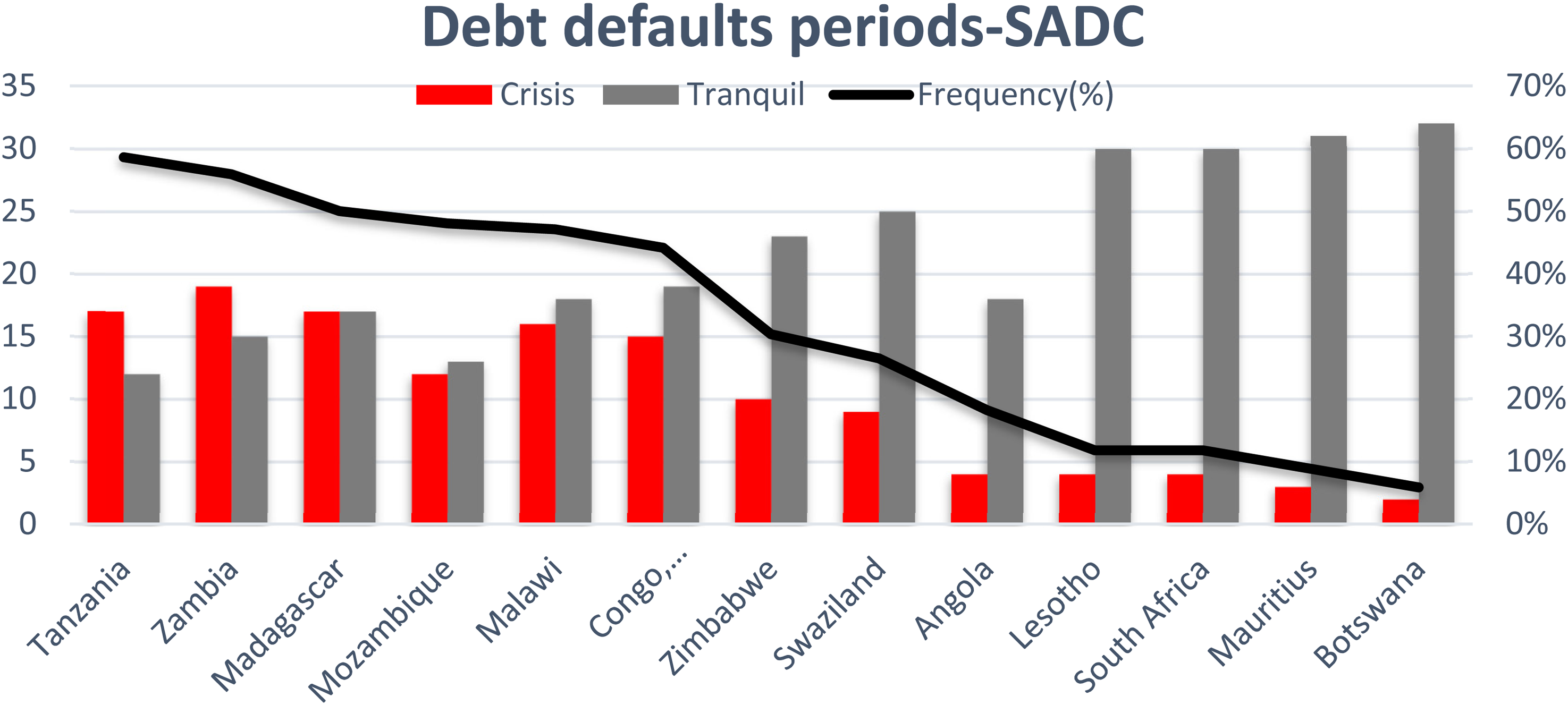

Member countries of the SADC region has experienced many public defaults some of which have spanned over decades. The Figure 1 below illustrates the incidence of public defaults in the region from 1983 to 2016, 34 years in total. It is apparent that Tanzania, Zambia, Madagascar, Malawi, DRC and Zimbabwe had the longest years in default for the period under review.

SADC public defaults in years. Source: Author's calculation.

The unconditional probability of debt crisis for the region is quite high at 32% (crisis periods to total years), with a high of 59% (about 17 years in default) for Tanzania and Botswana being the country with the lowest frequency of debt crisis.

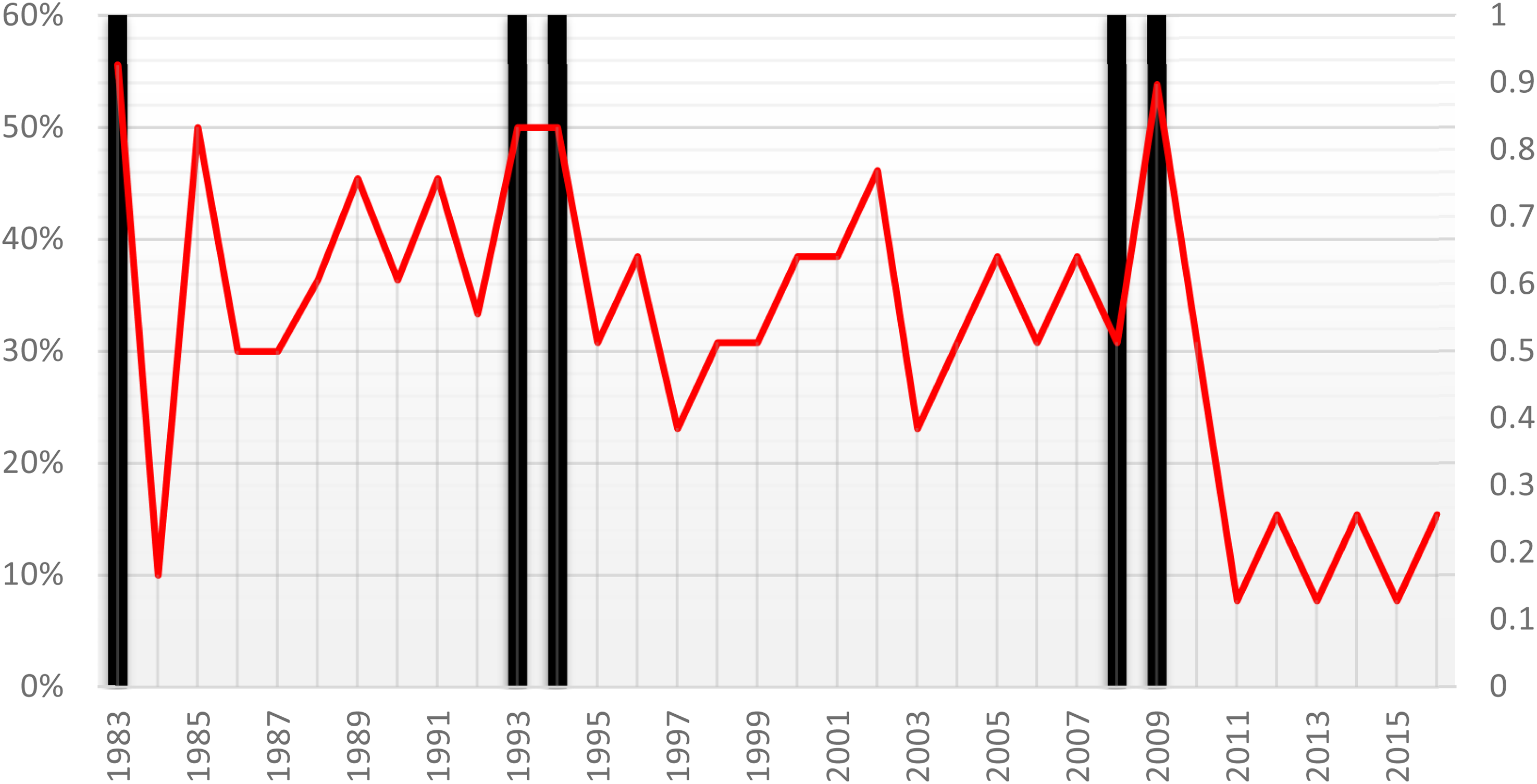

The diagram above shows the proportion of countries experiencing new crisis for the period under consideration. Defaults have been very high hovering above 40% for almost close to three decades. In 1983 about 55% of the member countries under consideration were in default of their public debts. As Gourinchas and Obstfeld (2012) notes the 1980s developing countries crisis were frequent, devastating and widespread. Kraay and Nehru (2006) also notes that most low income countries have been in default for prolonged periods of time.

Periods of widespread distress include the 1983, 1992–1994, and 2009. Despite common belief that developing countries were largely unscathed during the crisis of 2008/2009,

Figure 2 provides suggestive evidence that 2008/2009 were eventful years. Whether it is mere coincidence or an actual causal relationship is something warranting special inquiry.

Debt defaults from 1983 to 2016. Source: Author's calculation.

Debt over time

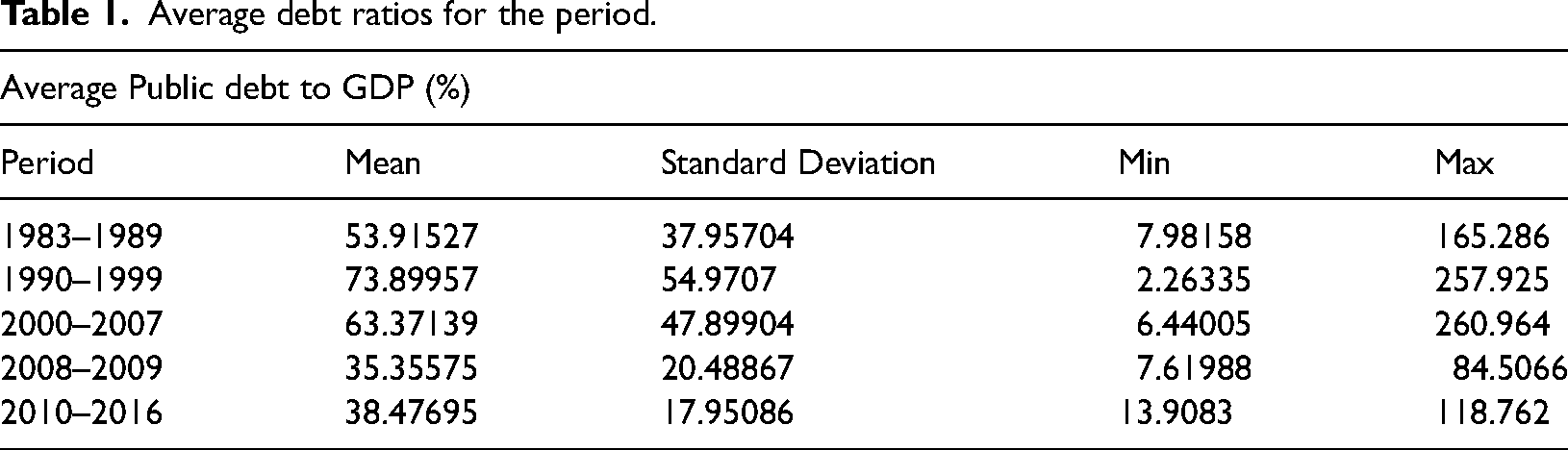

The number of countries experiencing debt distress have been decreasing since 2010. Given the rising debt levels in the region, this downward trend might reverse. Higher debt ratios are normally associated with a higher likelihood of debt crises (Herz and Tong, 2008) (Table 1)

Average debt ratios for the period.

Debt ratios have been relatively high with an overall mean average of 58%. The table above shows that debt ratios have been increasing till the nineties where on average it peaked to 74% from about 54% during the eighties. At the start of the new millennium debt ratios have been decreasing (either because of rising Gross Domestic Product (GDP) or retiring of public debt). In 2008 to 2009, the global financial crisis era, the debt ratios were surprisingly at their lowest, 35% compared to 63% the previous years. Post the global financial crisis, debt ratios have started to rise, and this has been a major concern with international financial institutions.

It is also surprising to note that public defaults (at least according to our measurements) were also at their peak during the global financial crisis despite the low debt ratios.

Debt and GDP growth

A simple linear regression analysis illustrates that debt is negatively associated with output as measured by real GDP. According to the simple model, as illustrated in Table 2, a 1% increase in debt to GDP ratio is associated with a decrease of about 4% in GDP. In other words an increase in debt is significantly associated with output downturns. Although there are various competing theories on effects of debt on economic growth, empirical literature is not conclusive. The channel linking debt to output losses could be the high incidence of debt defaults in the region.

GDP and debt level.

Output gap

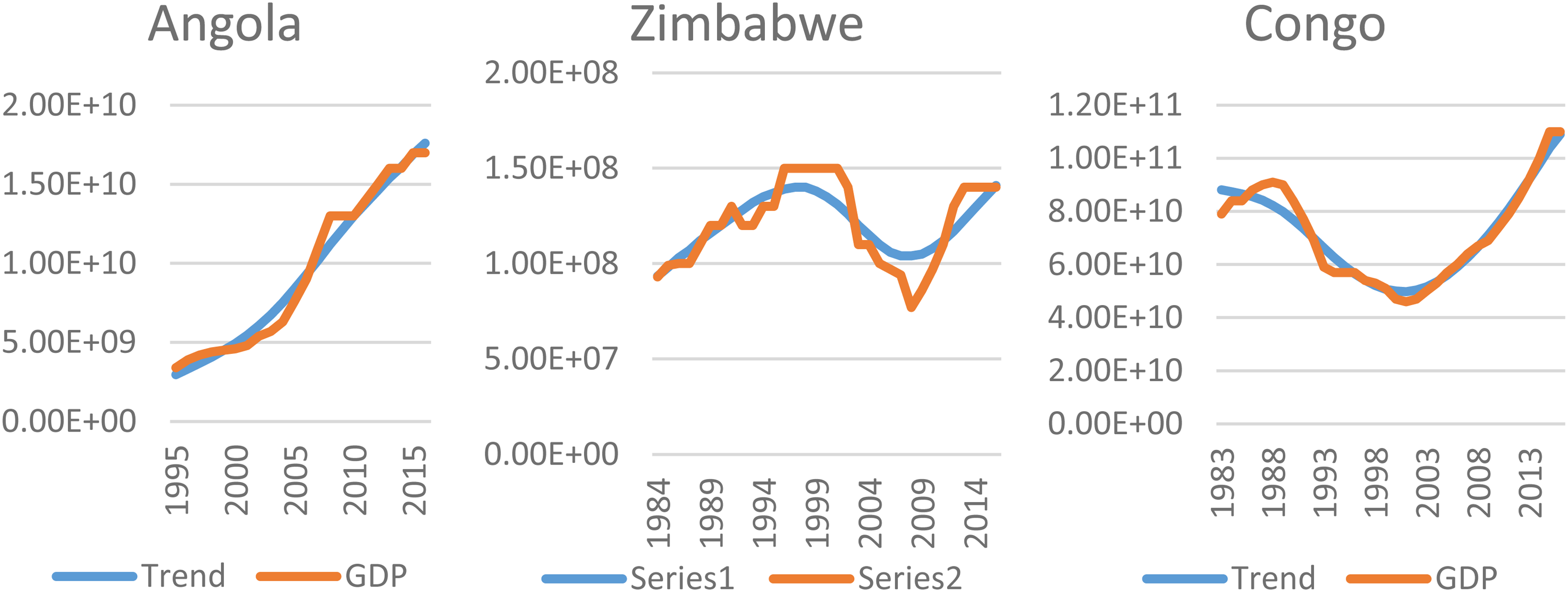

The charts below (Figure 3) serve to illustrate the evolution of output gap ($) for the SADC member states. Some countries like Zimbabwe, DRC, and Angola experienced large output losses for some time, periods which coincide with debt defaults. However other factors can also explain the large negative gaps aside with debt defaults. The following charts are just illustrative.

Output gap ($).

Main commodities per country

Information extracted mainly from the https://atlas.media.mit.edu/en/ details the major export earning commodities for SADC member states . It is clear that commodities still play a very important role in export revenues in SADC. It may therefore be argued that revenues of SADC economies are directly tied to fluctuations in the commodity prices and could therefore have a bearing on debt defaults through fiscal revenues.

The following section presents the main findings of the research. Output from event study analysis is presented first then results from the logit model.

Event study analysis

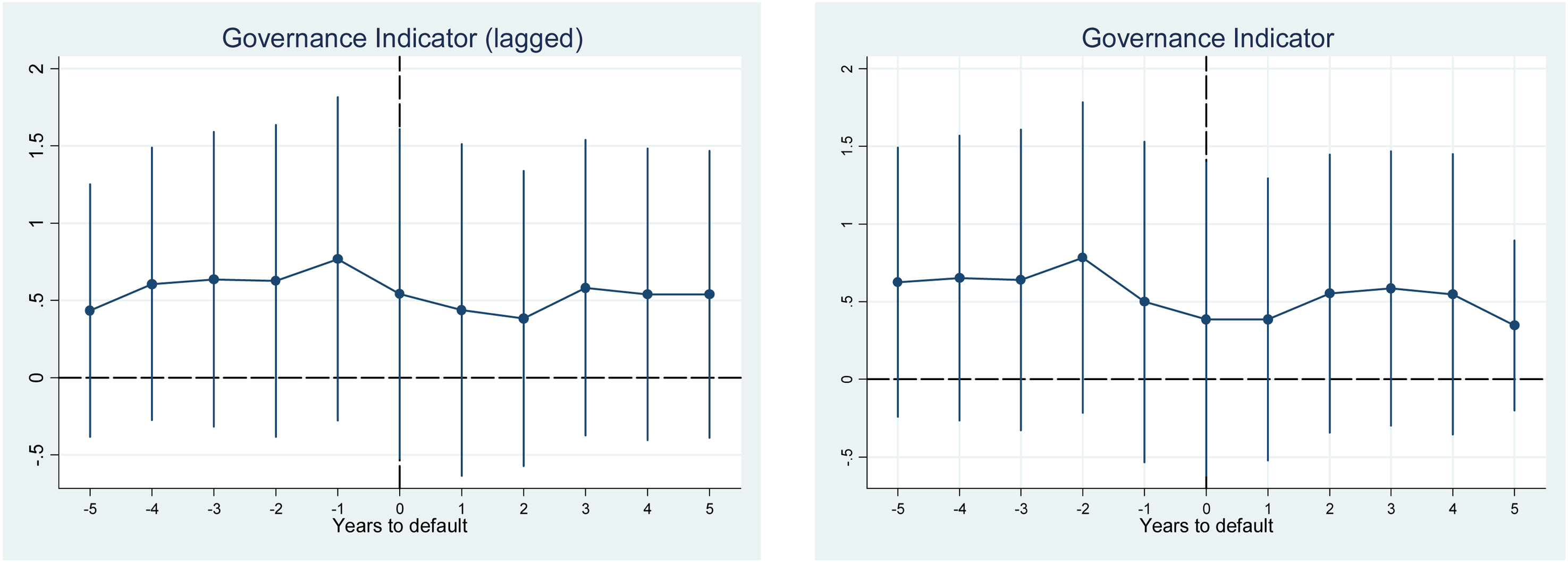

Event studies typically illustrate what happens to the potential predictors in the pre-crisis period, at event date and post-event period. Zero represents the crisis date and both the pre and post crisis periods are within five years of the default debt. The vertical axis plots the coefficients of the dummy variables (years −5 through 0 to year 5) from the univariate fixed effects regression model (Equation 1).the charts also illustrate the 95% confidence interval (the spikes) of the coefficient plots.

Governance quality is one of the variables of key interest in this research. Figure 4 seems to indicate that defaults occur after a sustained increase in governance ratings as measured by freedom house index. In the run up to the crisis, civil liberties and political freedoms decrease marginally compared to the tranquil period. In addition the ratings are somewhat higher in the period before compared to the post- event period. Consequently debt crisis tends to follow after periods of bad governance. It is also surprising to note that debt crisis tend to occur when governance seems to be improving, in fact default occurs when the ratings are marginally better compared to both the pre- crisis and post-crisis period. However the event studies does not seem to suggest strong evidence of governance being a significant harbinger of debt crisis. This is so probably because of the low volatility in the governance index.

Quality of governance.

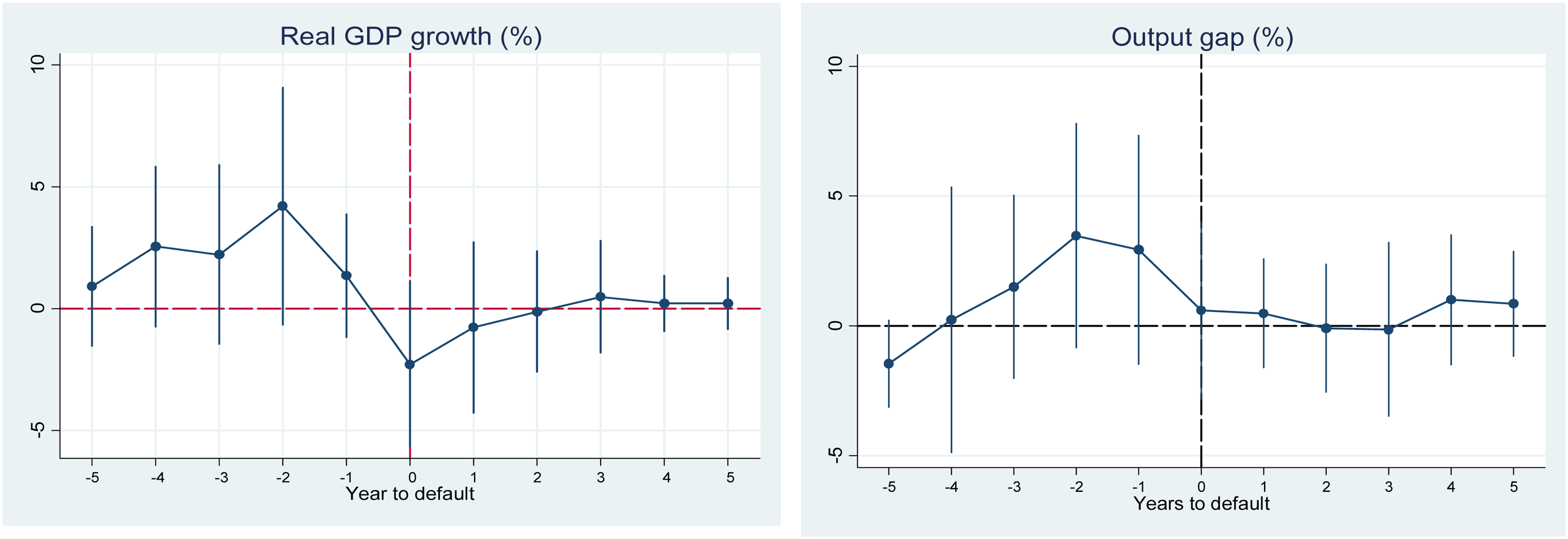

Figure 5 illustrate the evolution of economic growth and output gap around the default date. The economic growth shows the year on year percentages changes in economic growth whilst the output gap measures the deviation of the actual real GDP from long run average growth (the trend). The figures illustrates that economic growth is at its peak before the onset of the crisis. Alternatively the economy normally overheats before the onset of a debt crisis. Gourinchas and Obstfeld (2012), and Gerling, et al. (2017) also observed higher output values in the period before the default date.

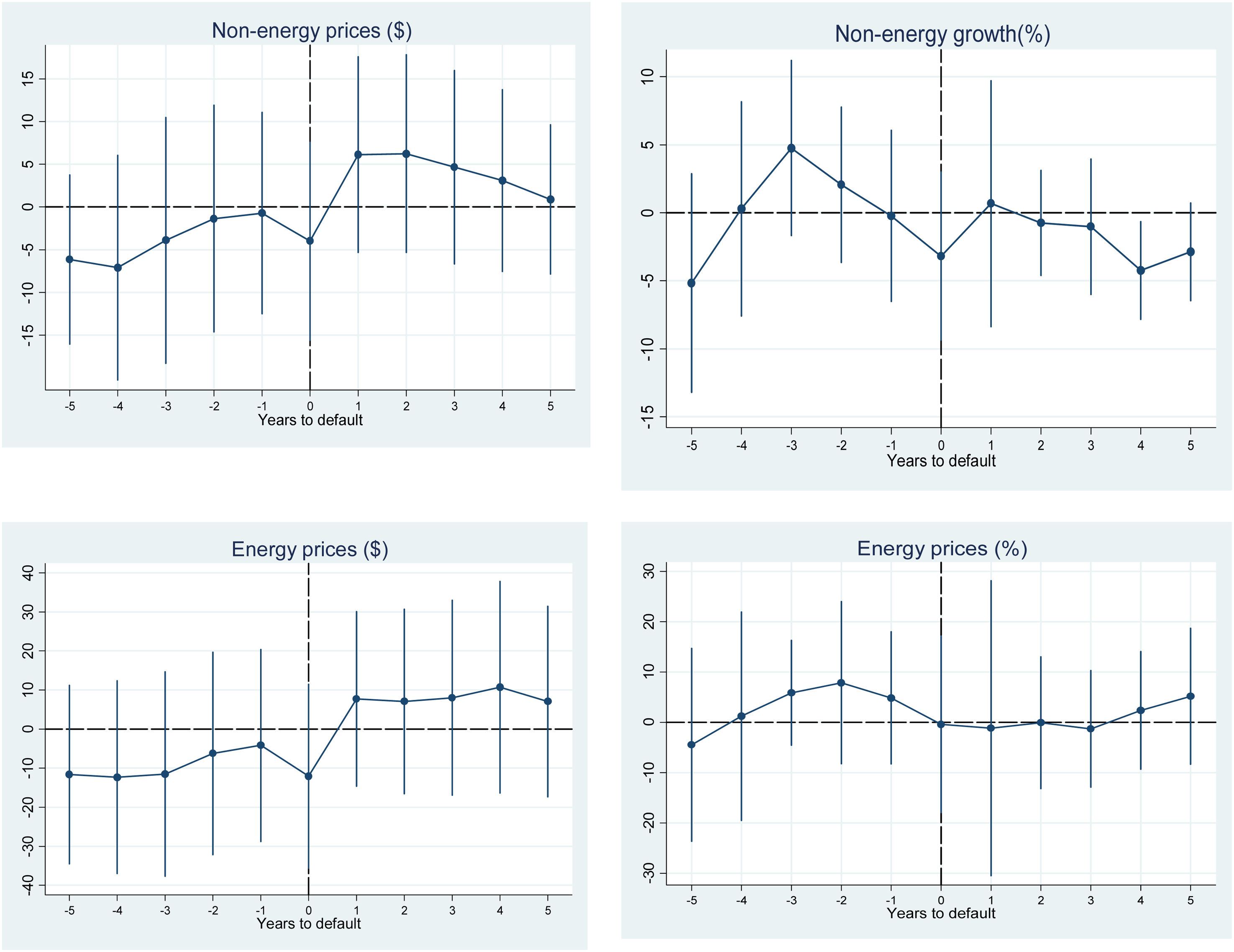

Commodity prices-non-energy & energy.

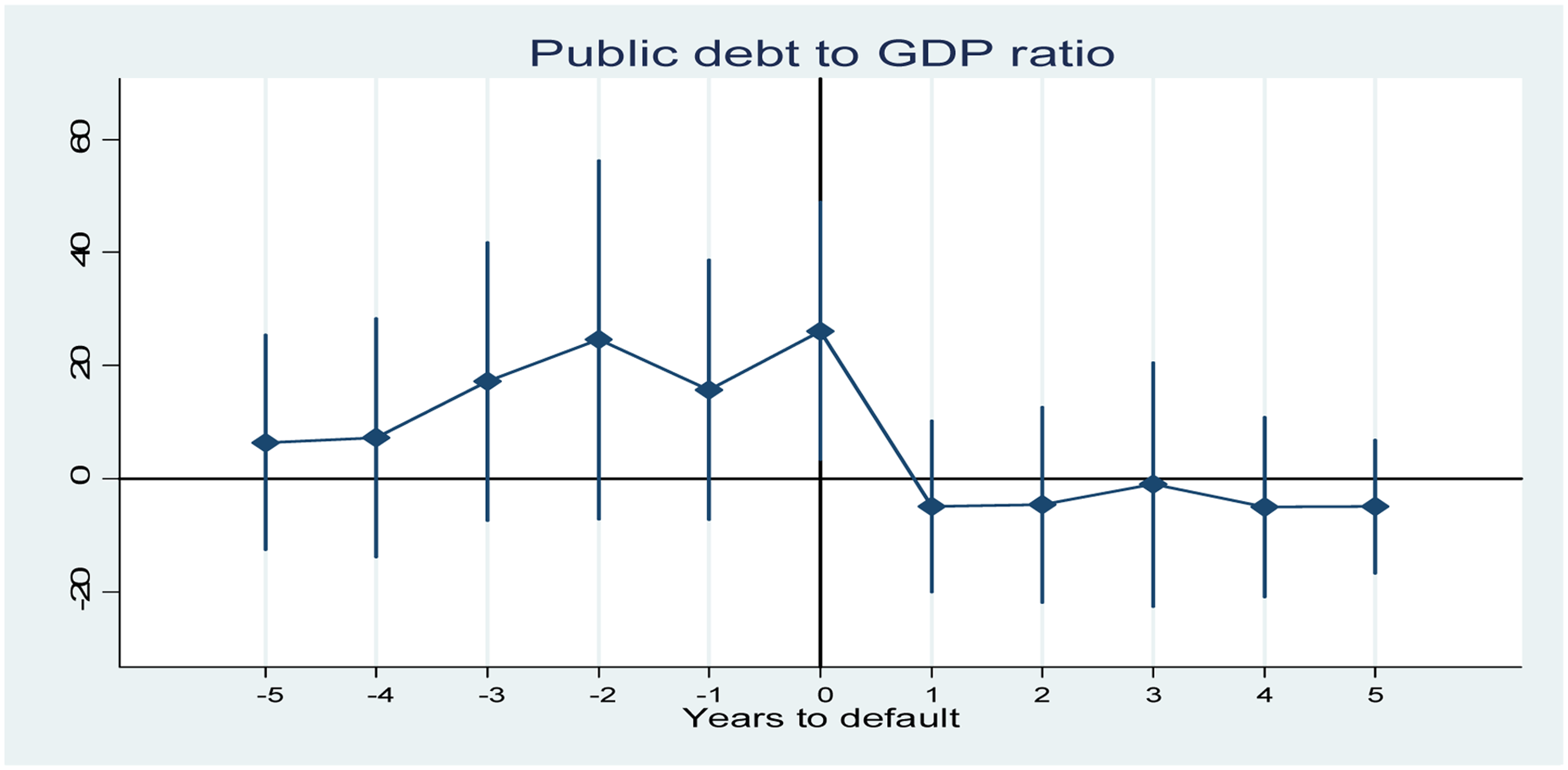

As the economy starts to experience negative economic growths, default on public debts then occurs at the very bottom of that trough. In the period crisis period economic growth recovers but however stays below the pre-crisis peak performance. Even the output gap figure illustrate that in the period after the event date, the economy retains to its long run average growth. Therefore public defaults are preceded by an overheating in the domestic economy. This may be an indication that in the pre-crisis period governments borrow excessively to finance infrastructure development. Figure 6 confirms this- debt levels increase in the years leading to the to the crisis date. Since the economy is growing, servicing of the debts is not problematic. However when the economy starts slowing down the fiscal position is constrained. As a result a prolonged slowing down of the economy is associated with the debt defaults.

Public debt to GDP ratio.

Figure 7 also illustrates the output loss experienced during default periods. The graph for Real Growth rate shows that during public defaults real GDP is negative and remains negative for about 3years. In other words the economy takes time to recover after public defaults. It could also be argued that when economic downturns coincide with debt defaults the economy takes time to recover. Again this saves to explain the output costs associated with public defaults.

Real GDP growth & output gap.

Because most of the countries in the sample are commodity dependent, it seems like economic growth is somehow related to commodity price booms at least in the pre-crisis period. This may also explain why in the run up to debt crisis governments shore up on debt- presumably on the strength of rising commodity prices.

Figure 5 illustrates the performance of commodity prices, non-energy and energy related commodities in terms of actual prices and growth-the shocks. It is clear from the growth charts that in the run up to the crisis, commodity prices have above average returns. Gerling, et al. (2017) notes that fiscal crises usually occur on the backdrop of rising food prices. Food prices are a subset of non-energy prices. Commodity booms are thus a potential precursor to public defaults. In the post crisis period the price process stabilizes and thus grows at a much slower rate than in the pre-crisis period. One could reason that rising commodity prices boost fiscal revenues for commodity dependent countries and hence countries experience minimal pressures to default. When analyzed in conjunction with the debt to GDP ratios and economic growth charts, rising commodity prices may help to explain the overheating of the economy and increasing debt levels. The assumption is that commodity prices have a direct bearing on fiscal revenues through reduced exports value and that countries in the sample are net exporters of commodities.

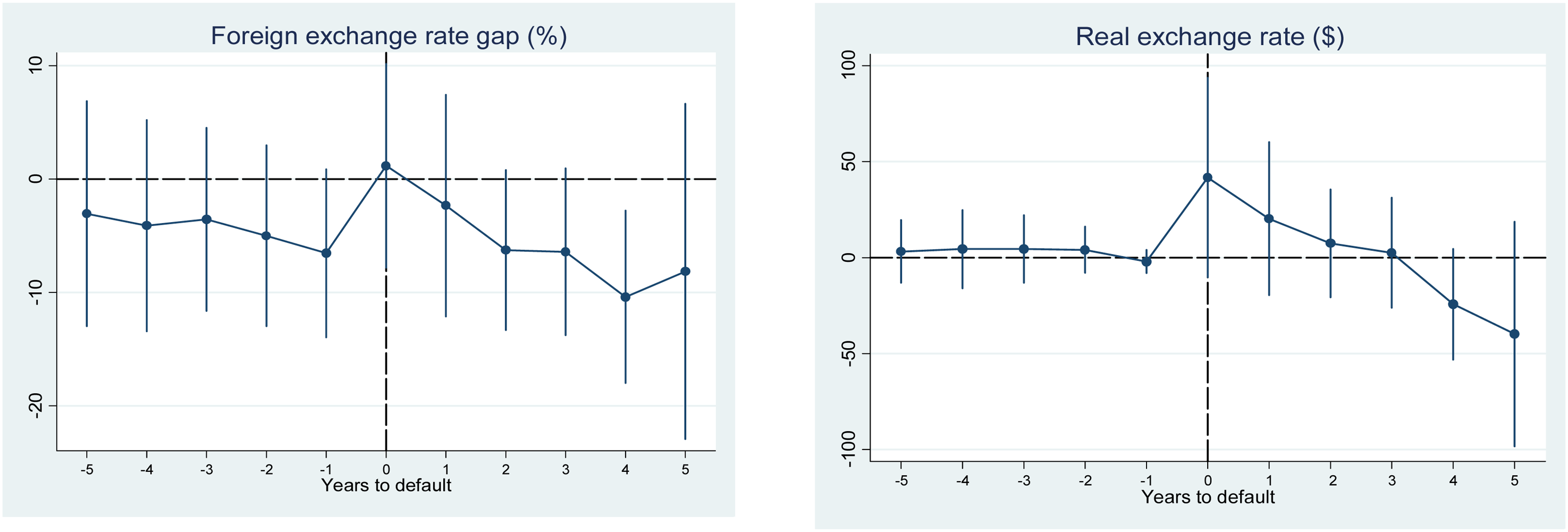

A sharp deviation of real exchange rate from trend is associated with defaults. This is shown in Figure 8. Default occurs when the foreign exchange market is overheating which essentially is a depreciation of the domestic currency. Gourinchas and Obstfeld (2012) also found the foreign exchange rate depreciation to be highly linked with public defaults. A sudden increase in the real exchange rates has obvious implications on the external loan book. Figure 8 illustrates that a 10% upsurge in the real exchange rate has the potential to induce public defaults. This is also particularly important in that the shock is sudden and is a deviation from the declining long run pattern (currency appreciation) exhibited in both periods, pre and post crisis. Therefore a sudden upward shock in the foreign market triggers immediately sovereign default. Interest and principal payments on external debt increase dramatically as the foreign exchange rate depreciate making defaults highly likely.

Real exchange rate.

Figure 6 illustrate the behavior of the public debt position around the crisis date. It is clear that debts are generally higher in the period before the event compared to the post-crisis period. The above zero plots also indicates that in the pre-crisis period debt ratios are higher than debt ratios in the tranquil period. After the default date debt ratios return to an almost tranquil level. Furthermore the event study reveals that debt defaults occur when external debt balances are at their peak. This gives support to the idea that developing countries should adhere to sustainable debt levels. In the sample under consideration this may mean that carrying debt ratios beyond 75% 14 is unsustainable, given that debt crisis occurs when the deviation from non-crisis periods is at its highest It is not clear whether defaults occur because of high external values (from a principal point of view) or foreign exchange related (market values of debt increase when a currency depreciates- Figure 8). Declining economic growth rates might also explain as shown in Figure 7.

Although the event studies are quite informative on the evolution of the variables around the crisis date, they do not provide a significant basis for conclusion, hence the need for logistic regression to model the probability of debt crisis.

Results analysis

The following are the main results of the logistic regression. Results for marginal effects/elasticities (as estimated by the average (semi) elasticities 15 of Pr (y = 1|x,u)). Results for the odds ratios and other summary tables are presented in the appendix.

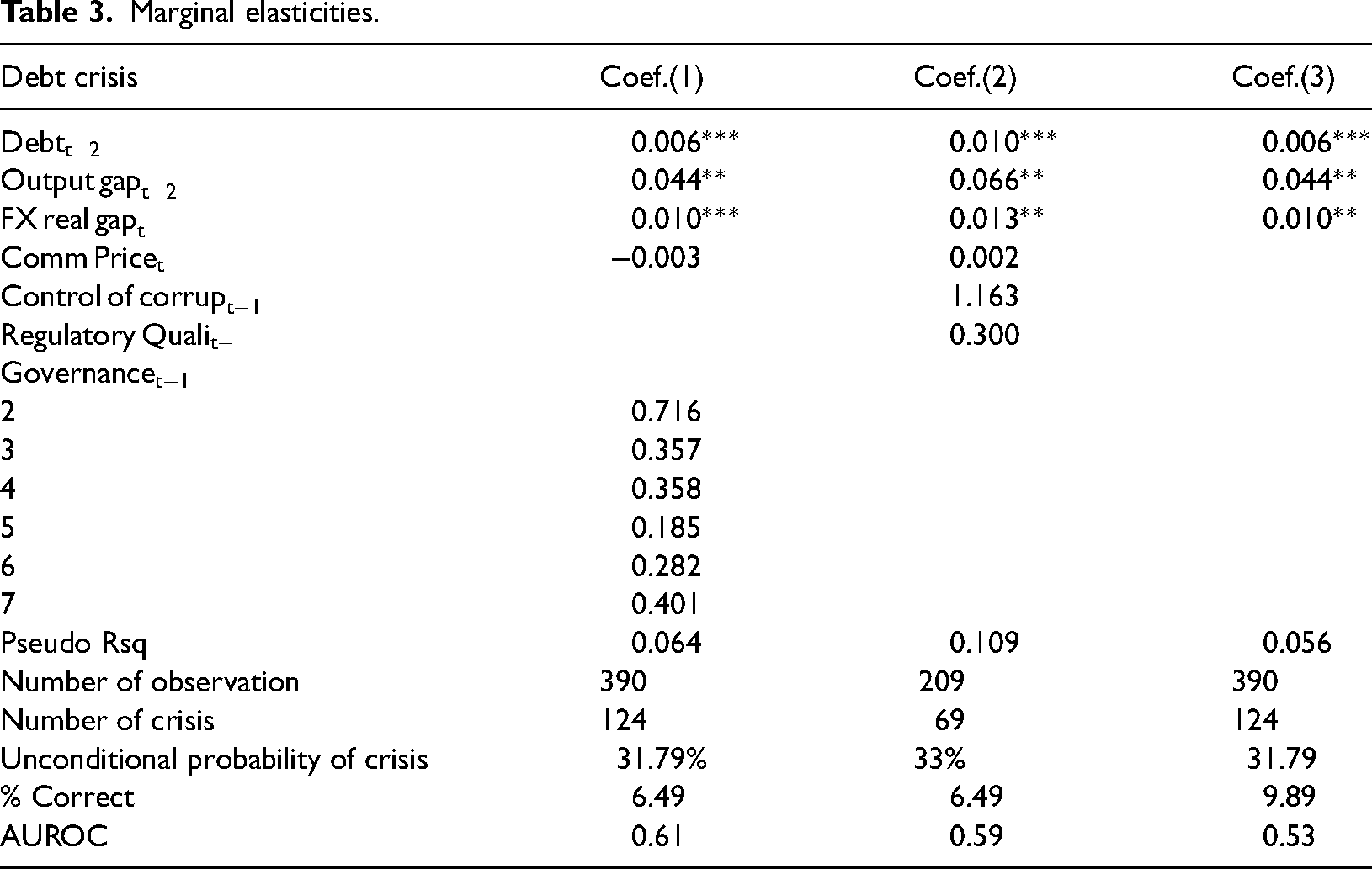

Table 3 illustrates the results from the logistic regression for Model 1 to 3. Model is the baseline model which has all the variables of interest, that is debt to GDP ratio, output, real foreign exchange rate, commodity prices and governance quality. Model 2 replaces the governance quality measures used in Model 1. Thus model 2, instead of political freedoms, uses Country Policy and Institutional Assessment(CPIA) indicators; control of corruption and regulatory quality (data is available from 1996). Lastly model 3 assess the predictive power of the macro variables without governance indicators.

Marginal elasticities.

The Pseudo Rsq of the models are all low as is normal in most logistic regression equations and cannot be interpreted in the same manner with ordinary least squares regressions. Model 2 and 3 used 390 data observations whilst Model 2 used 209 observations because of the constraint of the CPIA indices. The unconditional probability of a crisis occurring is around 33% in in all cases.

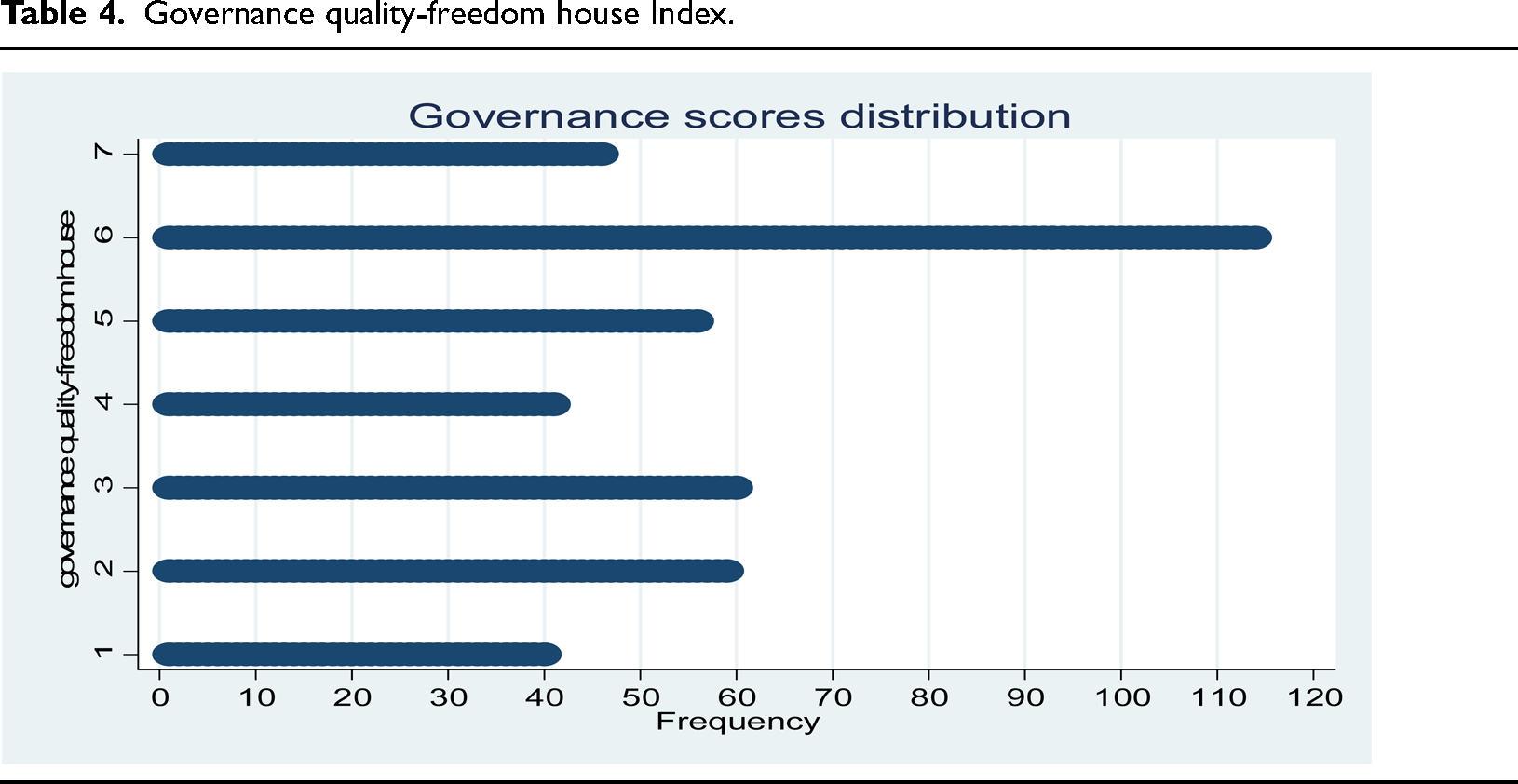

Most importantly Table 3 illustrates the significance of the variables in the logistic regression models. In all cases the macro economic variables were significant; debt to GDP ratio was strongly significant (at 1% level) in all the three models whilst output gap and real foreign exchange rate were significant at 5% level. However the key variables of interest, governance quality and commodity shocks were not significant in neither of the models. The positive coefficients are just suggestive of the direction of influence but in all cases they are not statistically significant as potential predictors of public debt crisis. Political freedoms are measured from a 1 to 7, high scores being the worst ranking. Thus it would seem that an increase in governance scores would tend to increase public debt crisis. Table 4 illustrate the distribution of political rights in the region. Quite a number of countries have very low ratings on governance quality as measured by the political freedoms of the Freedom House Index. The low rankings according to Kraay and Nehru (2006) and others should have indeed had a significant effect on default probabilities.

Governance quality-freedom house Index.

Nevertheless Table 6 (shown in Appendix) shows that variability within country is smaller compared to variability between countries, yet fixed effects uses within country variability. It is also important to highlight that fixed effects logistic regression is almost the standard approach in crisis prediction. Notwithstanding again the challenges of interpreting volatility of categorical variables, the low within variability might therefore help explain the lack of significance of this measure.

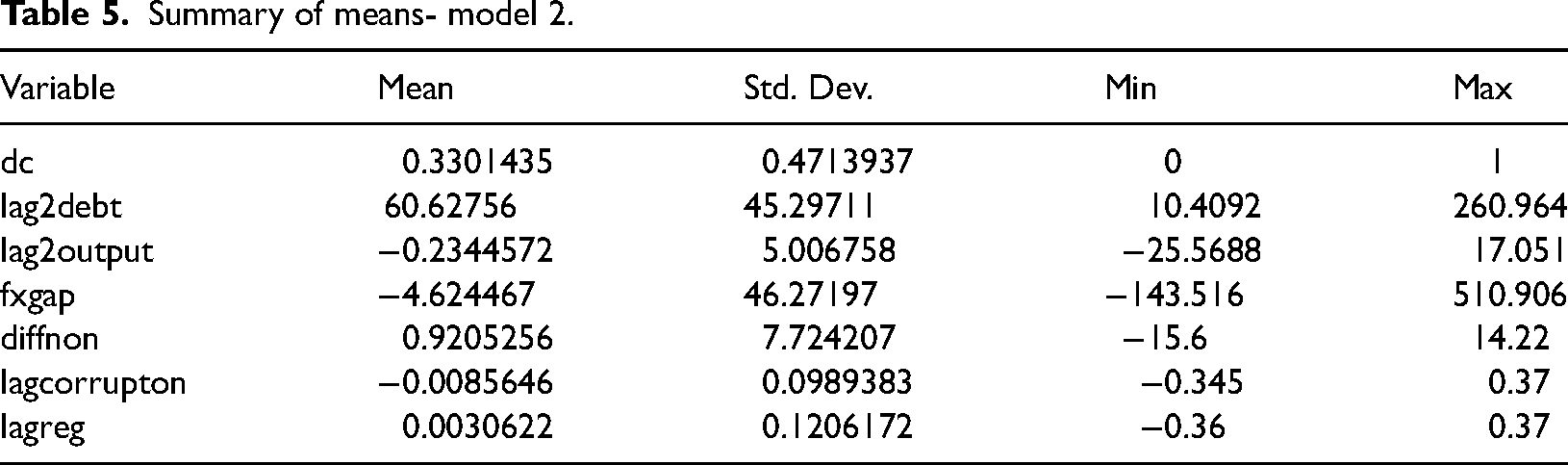

On the other hand the CPIA measures ranges from −2.5 to 2.5, i.e from weak to strong governance performance in that order. The Table 5 below illustrate the summary of measures used in the estimation of the average marginal elasticities in Model 2. On average the level of control corruption and regulatory quality is zero, with the minimum and maximum scores being approximately equal to −0.35 and 0.37 respectively. Again given the low scores it would have been expected that governance quality would be a significant predictor, with negative coefficient, of debt crisis. Surprisingly the CPIA indicators are not statistically significant at normal levels of significance.

Summary of means- model 2.

Empirical evidence has shown to a large extent that governance measure have a bearing on financial crisis prediction. However other empirical findings have shown inconclusive evidence of significance of governance as a significant predictor. For instance Klomp (2010) and Eichengreen and Arteta (2000) showed that governance was not statistically significant in banking crisis prediction. According to Eichengreen and Arteta (2000) this lack of robustness maybe a reflection of the crude nature of the institutional proxies for governance and this makes it an important topic for further investigation.

Although our event studies have shown that commodity prices overheat in the run up to the default, commodity prices turned out to be insignificant. A logical expectation was that commodity shocks would be significant predictors of debt crisis as shown by (Gündüz 2017) among others. However our empirical results seem to be in line with those of (Svetlana, et al., 2018) who could not prove statistical significance of commodity shocks in fiscal crisis prediction. Literature almost always links commodity shocks with default prediction via the fiscal revenues link. However that link seem to be weak, even in developing countries-presumably dependent on commodities, as shown by Svetlana, et al. (2018).

Furthermore our model specified commodity shocks as the first difference of commodity prices at the general level instead of country specific commodity shocks in the spirit of Bazzi and Blattman (2014) and Eberhardt and Presbitero (2018). Indeed countries react differently to commodity price shocks. For countries dependent on energy commodities (gas, crude oil, and coal) for export revenues, Mozambique and Angola for instance, energy prices booms might be more beneficial to their fiscal revenues than to countries like Zimbabwe and Zambia which are net importers of energy products. Although (Gündüz 2017) proved statistical significance with global commodity prices, our model showed could not prove statistical significance.

Notwithstanding their lack of statistical significance, our key variables seem to add some level of prediction to Model 3 which only employs macro-economic variables. The Area Under the Receiver Operator Characteristics curve (AUROC) increases marginally from about 0.53 to about 0.61. A score closer to one is ideal. Thus model 1 is much better than a random model which produces an area of 0.5. However the overall percent of crisis predicted correctly is quite small, about 6.5%. This low rate could be attributed to the lack of statistical significance of the key variables under consideration.

Whilst commodity shocks and governance measures were not significant, debt to GDP ratio, output and foreign exchange rate turned out to be significant. This is in contrast to some empirical literature, Gourinchas and Obstfeld (2012) for example, showed that public debt and output gap were statistically insignificant as debt crisis predictors. Our results however are in keeping with Gündüz (2017) and Herz and Tong (2008) findings.

The average marginal effects for debt to GDP ratio illustrate the marginal changes on average, on the probability of default, from a unit increase in the significant covariates. Therefore a 1% increase in debt is expected to be associated with a 0.6% increase in the probability of default within two years. This finding is also confirmed by our event studies, which shows that debt crisis always occur after “excessive” accumulation of debts.

It is also interesting to note that economic growth as measured by the percentage output gap is positively related to the occurrence of public debt crisis. According to the average marginal effects of the output in Table 3, a 1% increase in the output gap is associated with an upsurge in the likelihood of debt crisis of 4.4% in the next 2 years. That's a very large factor. Assuming all the other variables in our model are held at their “marginal values” a 1% deviation from trend has tremendous implications on the likelihood of defaults. Empirical literature although mixed largely holds output to be statistically insignificant Gourinchas and Obstfeld (2012), Svetlana, et al. (2018) and Gündüz (2017). On the other hand Eduardo and Ugo (2011) and Bauer, Herz and Karb (2011) are of the view that overheating of the domestic economy is significant predictor of debt crisis.

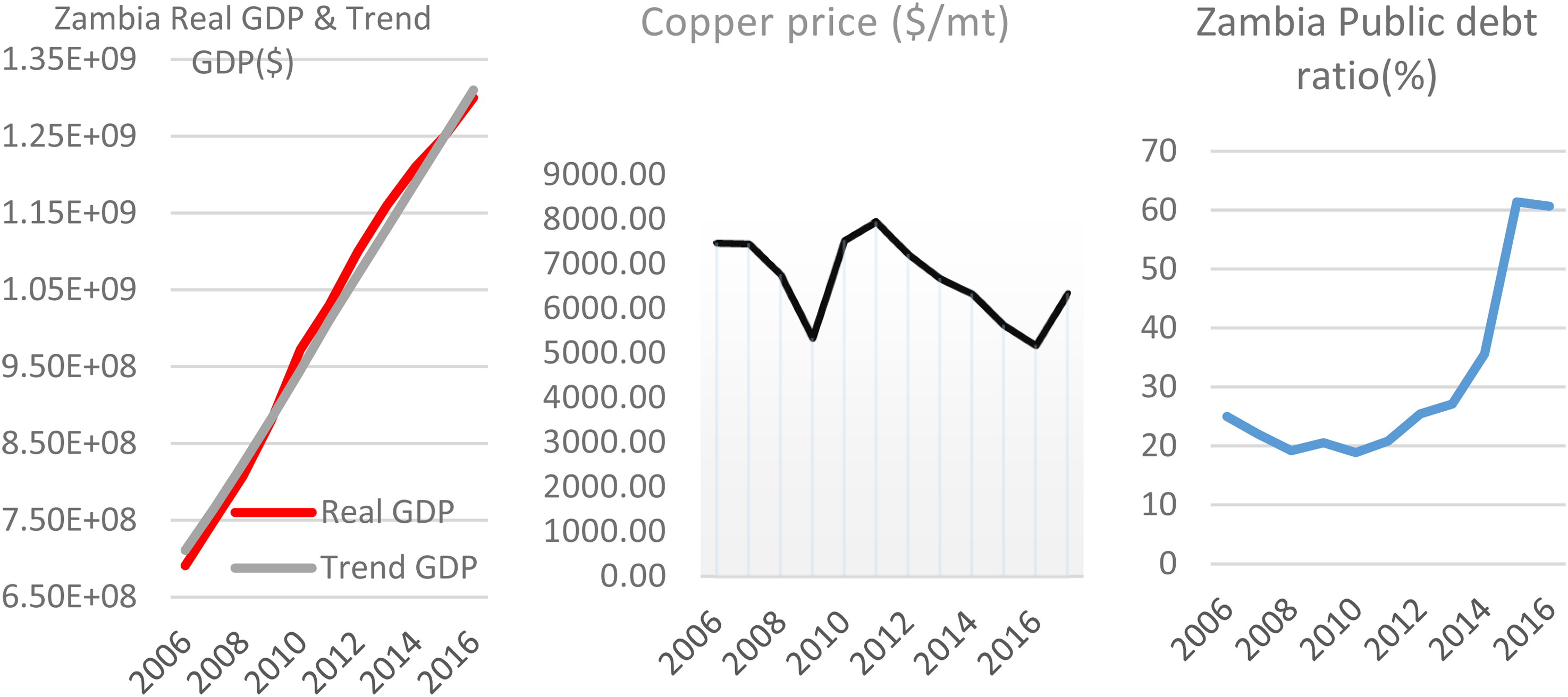

In our sample it may appear as if economic growth is buoyed by rising commodity prices and is financed by huge debts. Event studies have shown the huge increase in debts prior to debt crisis (Figure 6). This could be an indication of leveraged growth. For instance it is public knowledge that Zambia shored up massive debts to finance infrastructural projects at the height of booming copper prices but is now facing challenges in meeting debt obligations 16 . In 2016, the price of fell by 31% to $ 5177 per metric tonne from the 2010 peak of about $7500. The following (Figure 9) is instructive of the contemporaneous effect of overheating of the economy financed by rising debt levels on the strength of commodity booms.

Zambia-Economy overheating, booming commodities & rising debt.

The renewed fears of Zambia falling into debt crisis is as predicted by our model! A sustained output gap is a significant predictor of debt crisis; Commodity price declines (after a boom) are associated with debt crisis (though statistically commodity prices are insignificant) and debt levels peak before debt crisis (Figure 6).

On real foreign exchange rate a marginal increase of 1% is positively related with a 1% increase in the likelihood of default. This is also confirmed by the event studies. This is logically correct since an increase in the foreign exchange rate is simply a real depreciation. This tends to increase the total value of the external debt as measured in local units. A sustained depreciation of exchange rates may thus induce debt defaults as already discussed.

Robustness

The probability of default was also estimated using the random effects model. Results are shown in the Appendices section (Table 12). Regression results of macro-economic variables using two year lagged variables were significant. Output and debt remained strongly significant at 5% and 1% respectively. However the foreign exchange was only significant at the 10% level of significance. The main variables of interest, regulatory quality and commodity shocks, however remained insignificant in the random effects model.

Table 13 (in the Appendices) illustrate the results of the logit estimation using one year lagged variables. The results shows that debt remains significant at the 5% level, whilst foreign exchnage rate is only statistically significant at the 10% level. Output on the other hand becomes statistically insignificant, although it still maintains its positive coefficient. Commodity shocks and regulatory quality lagged by one year remain insignificant predictors of debt crisis.

This shows that debt crisis in the SADC region is significantly associated with debt levels, given the strong significane in all the logit specifications. Foreign exchnage is also a significant predictor as discussed earlier. This is obvious since unexpected shocks in the exchnage rates tends to worsen a countries external position thus raising the odds of probability. However real output gap was insignificant at 10%. In addition commodity shocks and regualtory quality were still not significant predictors of debt crisis.

Conclusions and recommendations

Conclusions

This research has shown that governance quality as measured by the political freedoms of the Freedom House or the Country Policy and Institutional Assessment framework of the World Bank (control of corruption and regulatory quality) is not a significant predictor of debt crisis. Empirical evidence has shown support of our findings though a large part has shown the significance of quality in crisis prediction.

Commodity price shocks have also been shown to be statistically insignificant though the general expectation was that commodity revenue are important in developing countries. Negative downturns in the commodity market should therefore have been significant predictors of financial crisis. Literature in this regard is also mixed.

All the macroeconomic variables in our specification proved to be statistically significant. Output gap has the largest association with public debt crisis within 2 years. We showed that a 1% increase in the output gap increases the chance of default by about 4.4%. Economic growth financed by rising debt and commodity booms have been proffered as suggestive reasons for the large effect output has on the probability of debt crisis.

Recommendations

Although our model has not shown statistically the significance of quality of governance as a predictor of debt crisis, we cannot therefore advocate for the disregard of rule of law, establishment of strong institutional frameworks and other important governance reforms. We contend the quality of governance is important for the overall functioning of the economy and possibly debt crisis occurrence. However our model has statistically shown the absence of such direct linkages with debt crisis prediction.

Because our model has shown that debt levels with a two year lag are significant predictors of default episodes, it is recommended that governments avoid excessive use of external borrowing. Although the research did not look into sustainability of debt ratios in the region, event studies have shown that crisis on average occur after debts peak at above tranquil averages of around 40%. Based on those simple graphical analysis we can safely recommend that debt levels beyond 40% maybe unsustainable given the current economic environment.

The percentage deviation of the real GDP from long run growth potential has been shown to be a significant predictor of the likelihood of debt crisis. It is therefore important that overheating of the economy through excessive infrastructure development (based on media reports most SADC governments have been borrowing to finance infrastructure development) avoided given the size of the marginal effects of output gap on probability of debt crisis. The findings of this research however does not imply that governments should strive to ensure economies operate at below optimum levels but has just shown empirically that debt crisis are heralded by an overheating of the economy. It is possible that economies can safely maintain growth at above average figures even if the financing matrix of growth is heavily financed by debt and reliant on booming commodity prices. The effects of the interaction of output gap and rising debt levels on probability of default has not been examined, but it could have a greater effect than the separate marginal effects suggested by the findings of this research.

There is need to investigate further on the implications of commodities on debt crisis using country specific commodity shocks. This may prove to be significant given that commodities ranging from agricultural, crude oil, metals and minerals are important in the fiscal revenues of the regional economy, as has been shown above. For instance Angola is mainly dependent on crude oil whilst Zambia and DRC rely mainly on copper and cobalt, 78% of Zambia's export receipts are copper related; Malawi depend mainly on agricultural products; Zimbabwe, gold and tobacco are the major exporter earners. The use of one single commodity index might indeed be problematic. This is therefore an interesting area of future research.

A complete review of financial crisis (currency, banking and debt and how they are related) in SADC is also another interesting area of research. Some studies have shown some causal relationship among these types of financial crisis. This research could not delve into that because of limited time. It is clear from the developments on the ground that there is need for extensive research on public defaults in the SADC. The high frequency of defaults are a cause for concern and the search for more significant predictors must continue. However, “Building early warning indicators that help predict future fiscal crises is inherently difficult, including because countries may take mitigating action as they see the growing vulnerabilities!” Svetlana, et al. (2018).

Supplemental Material

sj-docx-1-ias-10.1177_22338659221120074 - Supplemental material for Prediction of debt crisis in Southern African Development Community (SADC)

Supplemental material, sj-docx-1-ias-10.1177_22338659221120074 for Prediction of debt crisis in Southern African Development Community (SADC) by Crispen Chirume in International Area Studies Review

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received financial support from Korea International Cooperation Agency for the research.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.