Abstract

Startups dream of becoming unicorns, but only a few make it to the top in the e-commerce space. Where should they look for value creation? This study develops a value creation matrix of e-commerce startups based on the Teece model and Value configurations and validates the same on 96 Indian e-commerce startups. E-commerce startups can locate themselves on this matrix and take appropriate steps to create value. The article validates the prescriptions of the Teece model and Value configuration as applied by Afuah and Tucci (2003) in the e-commerce context. The matrix developed in this study will be a helpful aid for the practitioners. Firms could use it to analyze their current offerings and build a suitable investor pitch. Investors can use the matrix to analyze a firm’s strategies and positioning in the e-commerce space.

Introduction

Value creation—the process of generating value for an organization or its stakeholders (Vargo & Lusch, 2004; Vargo & Morgan, 2005)—is quite elusive in the ecommerce space. Startups in e-commerce usually act as intermediaries between two or more groups of users using digital technology (Muylle & Basu, 2004; Zott et al., 2011). Only a small percentage of startups achieve success—dynamics that may eventually give rise to a winner-take-all outcome (Boudreau et al., 2015; Cusumano et al., 2019; Zhu & Iansiti, 2012). Pride (2018) estimates that almost 92% of startups fail within a year, and others struggle to sustain the competition (Wan et al., 2017). In India, which has the third largest ecosystem behind US and China and has around 77,000 recognized startups, only 107 have turned unicorns. Although impressive, this is a tiny percentage of startups (even considering that one-third of registered startups are e-commerce startups). Theoretically, e-commerce startups are easier to launch as they do not require investment in assets. However, the lack of requirement for physical assets also reduces barriers to entry, making the startup space extremely competitive, so much so that it becomes challenging to carry it through the growth ladder. Moreover, the environment in which these startups operate is highly volatile because of the fast technological progress and the rapid changes in market conditions (Nambisan & Baron, 2013). As soon as a startup becomes somewhat successful, competitors emerge to capture the value it has created. As a result, even very accomplished e-commerce firms struggle to post profits, have to depend substantially on angel investors and venture capitalists, invest continuously in growth, and remain fearful of a hostile takeover.

Several scholars have examined e-commerce startups and have given prescriptive insights into the strategies they must pursue to become successful. For example, Afuah and Tucci (2003), drawing on Teece (1986)’s, profiting from the innovation (PFI) model, prescribed ‘Run,’ ‘Team-up,’ and ‘Block’ strategies for startups depending on the imitability of their business models and availability of complementary assets (assets required to distribute a firms’ innovation to the market). They also argue that different startups may apply one or more strategies depending on their growth stage. Applying Thompson (1996)’s value configuration to the e-commerce context, they prescribed different strategies for different value configurations. Thus, although there is abundant research on value creation in e-commerce platforms, we still find failure among startups a very prominent phenomenon. A reasonable conjecture would be that the startups might be misapplying the value-creation logic, or the value-creation logic itself might be flawed (assuming other factors are favourable). By examining the value-creation logic of successful and failed firms and examining them in the light of theory, we can derive generalized prescriptions and prohibitions regarding where e-commerce startups can look to create value.

Therefore, this study addresses the question: Where should e-commerce startups look to create value? We examine 96 Indian e-commerce companies using the Teece Model and Thomson’s value configurations perspective and identify strategies e-commerce startups can adopt to create value. The choice of Indian context is pertinent as it has grown considerably to be the third largest ecosystem in the world after USA and China. We propose a 3×3 value creation matrix that startups can use to examine their current position and identify strategies they can undertake toward success. Startups may also use this framework for creating a suitable investor pitch for equity financing. Investors can use the framework to analyze their investment strategies in e-commerce startups.

Literature Review and Theoretical Underpinnings

Research on e-commerce has evolved with the evolution of e-commerce itself. Pre-2000 period (before the dot-com burst), practitioners felt there was no need for strategy and that strategy itself was useless in the case of e-commerce businesses (Porter, 2001). Porter (2001), however, argued a greater need for strategy in the e-commerce business. During the first decade after 2000, several scholars applied frameworks from strategy to understand e-commerce businesses. Afuah and Tucci (2003), for example, applied several frameworks, including Teece’s PFI model and Thomsons’ value configurations, to understand e-commerce businesses. Later scholars examined e-commerce businesses as platforms and found that e-commerce platforms differ from traditional businesses because they engage multiple sides of the market, generate network effects, and solve the chicken-or-egg problem (Cusumano et al., 2019). Digital multi-sided platforms enable different groups of participants to exchange information, goods, and social content and create new services, business models and markets (Eisenmann et al., 2006; Parker & Van Alstyne, 2012). Several scholars examined e-commerce platforms from value creation and value capture perspectives. Table 1 presents a snapshot of recent work on e-commerce platforms and how they create value.

Literature on Value Creation in e-Commerce Platforms.

Cusumano et al. (2019) examined several platforms and identified five ways e-commerce platforms create value: matchmaking, reducing friction in transactions, complementary services, complementary technology sales, and advertising. In terms of matchmaking platforms, try to increase the pool size and the likelihood of a better match. Platforms try to reduce friction in transactions by various means, such as enabling the secure exchange of goods and money, authentication, and verification. They also create value by providing complementary services (such as by charging to obtain a better rank in the search engine). In complementary technology sales, they sell technology or other goods and services. Finally, they also create value by allowing advertisers to advertise on their platform once they have gained a substantial user base. Most other scholars examined the phenomena of matchmaking and generating network effects for creating better value. For example, Van Alstyne and Schrage (2016) identified how successful platforms improve matchmaking by improving their users’ capability (such as by educating them, giving them better markets, targets, and so on). Thus, the common theme among platform researchers is to create better value for customers and lock it through strong network effects.

While the need for value-creation is very well-known to e-commerce startups, what is not clear is how to identify a better value-creation logic. How to examine the value creation logic a startup already has? Therefore, considering the need for practice, we find a few prominent gaps in these studies. Most of these studies are strategic in nature and do not inform about specific steps that platforms take in practice to apply them. Second, they address the topic of value creation very broadly. Third, they are primarily conducted in the Western context, which may differ substantially from Oriental contexts. Fourth, most of these studies are biased toward successful cases (De Reuver et al., 2018). We address these gaps in our study by examining successful and failed Indian e-commerce startups in their attempt to create value. With their examples, we wish to learn from their success and mistakes. To categorize specific steps, we again turn to two prescriptive frameworks—the Teece model and value configurations—applied to the e-commerce context.

Teece Model

Teece’s model (Teece, 1986) is an objective framework that helps understand can a firm capture value from its innovation. The motivation for this model came from the puzzling observation of how EMI Central Research Laboratories—the original inventor of the commercial CAT Scan—could not profit from its innovation, whereas companies like General Electric and Siemens, who commercialized it, made huge fortunes. Teece proposed that two factors are essential to make money from an invention: invention capability and complementary capability. Invention capability refers to new ways of doing things that are distinguishable from the activities of other firms. It includes all resources required for building an invention, namely tangible (asset on the balance sheet: plants, machinery, cash, etc.), intangible (brand name, patents, copyrights, trade secrets, etc.), and organizational (know-how, tacit knowledge, routines, processes), as well as activities (such as R&D, manufacturing, marketing, and so on) and relational capabilities/social capital (relationship with competitors, network effects, and access to finance). Apart from inventing capability, a firm needs complementary capability to capture value from innovation. Complementary capabilities (or complementary assets) primarily refer to the ability to distribute the invention to the masses. For example, a movie producer needs to distribute the movie throughout the country, which is available to those having distribution rights. Afuah and Tucci (2003) applied this framework to the e-commerce context to examine what makes an e-commerce firm make or lose money. He also identified three strategies (Run, Teamup, or Block) that e-commerce firms should use as they grow.

According to this framework, if the imitability is high and complementary assets are freely available (Quad I), it is difficult to make money. Hence, a firm must adopt the run strategy in this phase by continuously innovating its offerings. Continuous innovation is typical of what we see in companies in the beginning years of the startup phase. If the imitability is high and complementary assets are tightly held (Quad II), the holder of complementary assets makes money. In most e-commerce firms, neither the firm itself nor incumbents hold complementary assets, and the firm itself has to build them. For example, Flipkart itself created the logistics infrastructure in the country to complement its onlineretailing model. If, however, the complementary assets are available with incumbents, then startups can pursue team-up options (such as joint venture, strategic alliance, and acquisition). We also observe this phenomenon in the startup space, where firms seek acquisitions/alliances to expand their product and customer base. If the imitability is low and the complementary assets are tightly held (Quad III), the party with the technology and assets or bargaining power makes money. In this stage, a firm can pursue a block or team-up strategy, typical of e-commerce firms that have surpassed the growth stage and are positioned as formidable competitors to others. Amazon, for example, pursued block strategies by launching Amazon Prime and through ecosystem development (offering products and services that cover the entire related e-commerce space). If the imitability is low and complementary assets are freely available (Quad IV), a firm should pursue a block strategy so that no competitor enters its space. A few successful brick-and-mortar firms successfully blocked others’ entry into the e-commerce space as they already had a stronghold in the market. An example of this strategy is grainger.com, which entered the e-commerce space with an already existing stronghold in the industrial supplies market. The entry of startups into emerging markets is an important source of innovation (Phillips & Zhdanov, 2013). Startups usually begin in quadrant I and grow to quadrant II and sometimes III. We leverage Afuah and Tucci (2003) to conceptualize the three stages of e-commerce startups and examine whether the strategies of startups match the stage they are in.

Value Configuration Logics

Another important framework useful to examine value creation among existing startups is Thompson’s value configuration. Thompson (1996) proposed three configurations in which organizations create value: value chain, value network, and value shop. Afuah and Tucci (2003) examined these value configurations in the context of e-commerce. In a Value chain, interdependencies are sequential, and tasks are accomplished serially. Long-linked technologies are a continuous output of standardized products, repetitive tasks, the conversion of raw materials into finished goods, clear-cut criteria for selecting capital and labour, and continuous improvement in production. Value chains should look for in-process efficiency (rather than product differentiation) and low cost to succeed. A Value network provides the service of a connection between two or more customers who wish to be interdependent, such as borrowers and lenders (depositors) or buyers and sellers. Thus, mediating technologies facilitate the role of the aptly named intermediary service. An example of this would be online travel agents such as Travelocity and Expedia. To succeed, value networks should increase and widen the network by focusing on network promotion and contract management. Value shop is an intensive business oriented toward solving highly specific problems. There is likely to be an intensive interaction between the service provider and the service receiver. Most service provisions, such as doctor’s service in a clinic, and restaurants providing customized service, are examples of value shops. To succeed, value shops should look to get the basic information back to customers without the intervention of customer service agents in a timely and cost-efficient fashion and increasingly provide value on the basic services, such as flight status, aeroplane layouts, and seat locations. We leverage the value configuration to examine the configuration of e-commerce startups regarding their match with Afuah and Tucci (2003)’s prescription.

Value Creation Matrix for e-Commerce Startups

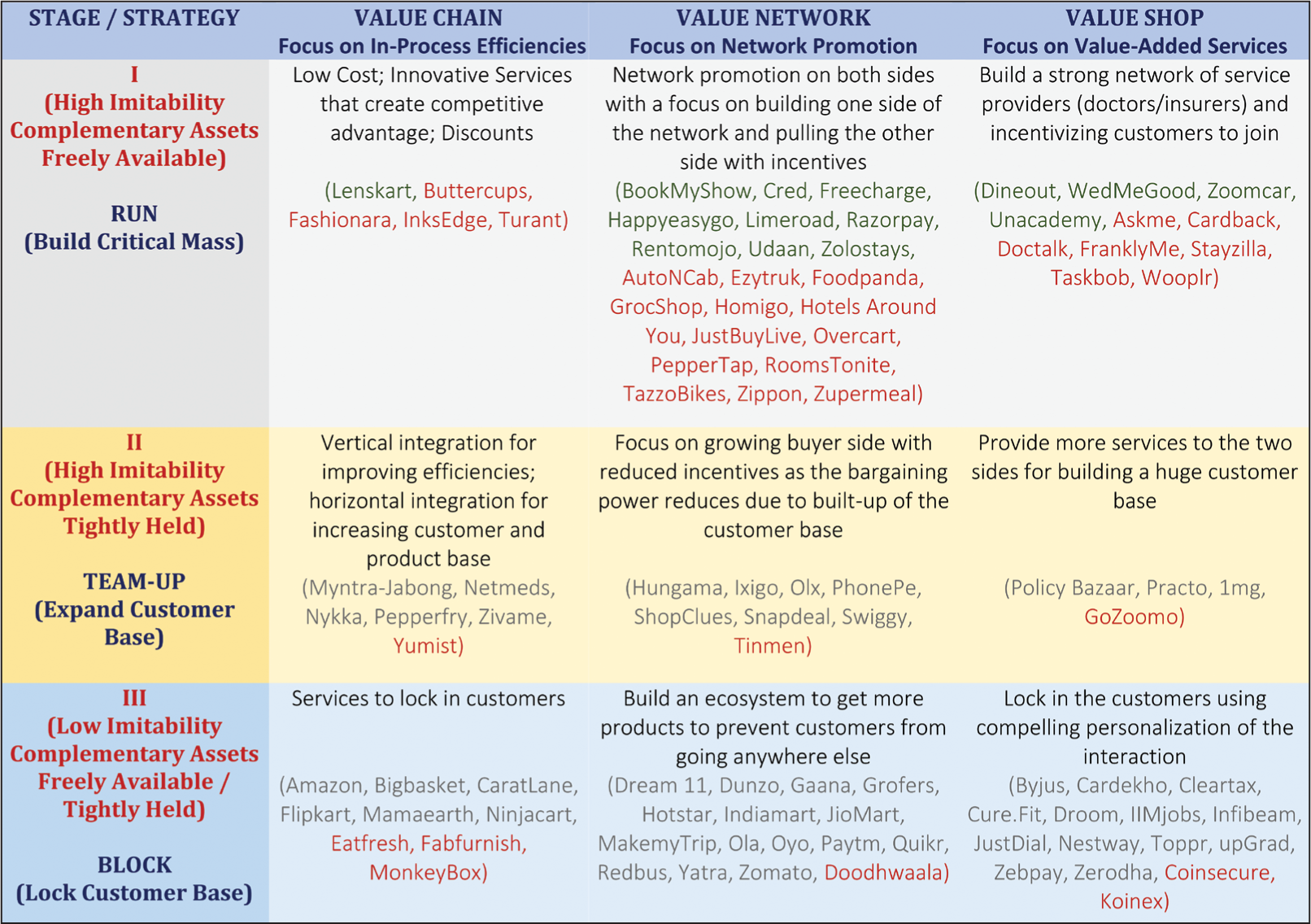

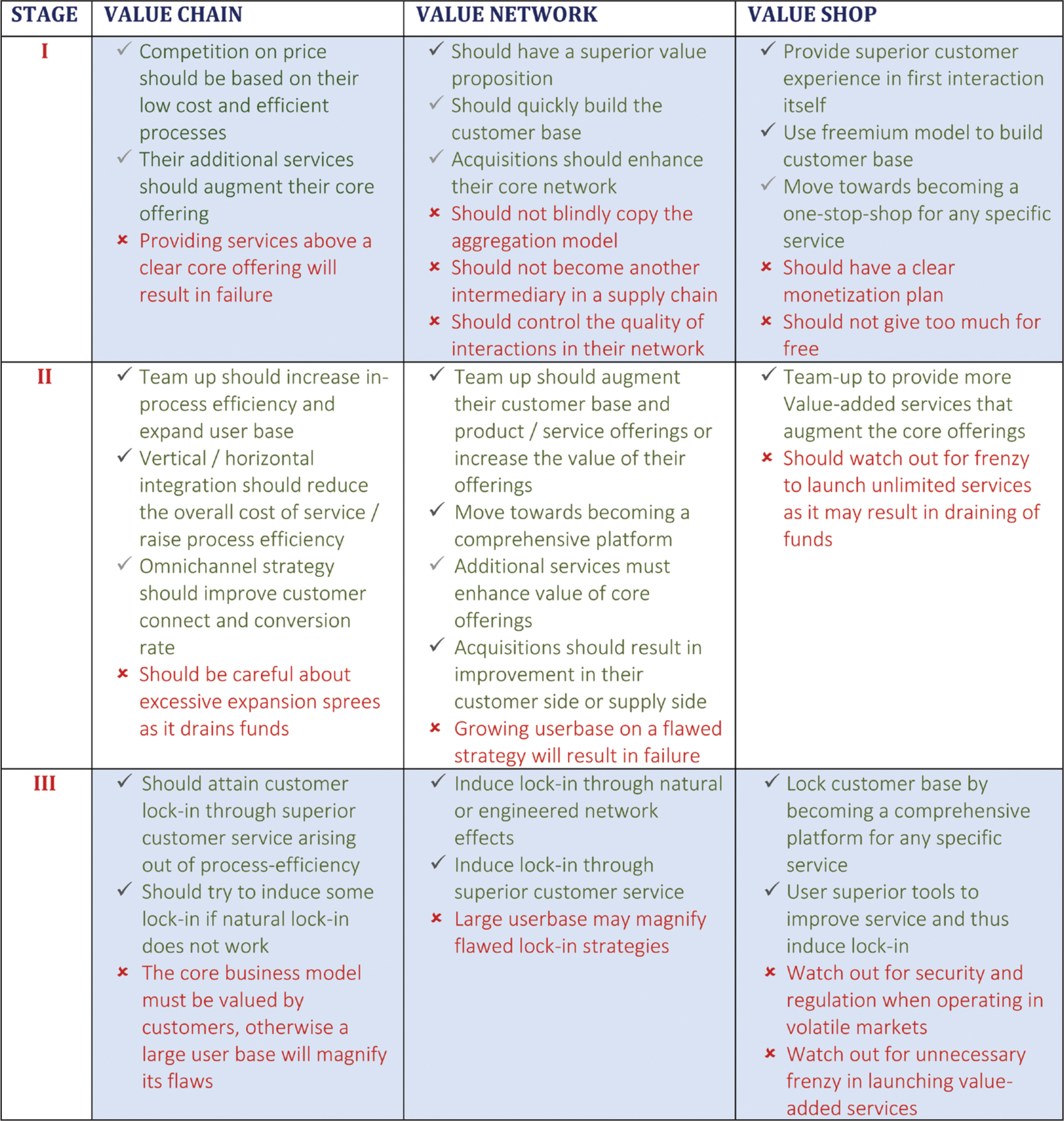

The Teece model and Value configuration models are quite prominent in the e-commerce literature. Several authors, including (Baden-Fuller & Haefliger, 2013; Casper & Glimstedt, 2001; Fjeldstad & Snow, 2018), have prominently used them. By combining these two based on Afuah and Tucci (2003)’s conceptualization, we derive interesting prescriptions and insights into the business models of e-commerce firms. Baden-Fuller and Haefliger (2013) and Fjeldstad and Snow (2018) have examined these typologies together by using the value configuration model for taxonomy and the recommendation of the Teece model for highlighting the imitability. We propose a 3×3 value creation matrix by combining the Teece model and value configuration (Figure 1) to study the strategies adopted by the firm in each cell. The three value configurations are the columns of this matrix, and the three prominent strategies from Teece Model, namely Run, Team-up, and Block, are the rows of the matrix.

Prescriptions of the Value Creation Matrix

A value chain should look for in-process efficiencies at different stages of a firm’s development. In stage I, a startup should pursue a run strategy to increase its in-process efficiency. By reducing prices, a startup gets engulfed in price wars with competitors. The in-process efficiency could result from faster delivery or easier and better acquisition of supplies. In stage II, startups should team up to improve their in-process efficiency. In stage III, value chains should pursue key ecosystem moves that increase efficiency and lock in the customers.

A value network should look for network promotion as it moves through various stages. In stage I, it should pursue a run strategy to incentivize building a vital side of its platform. Most two-sided platforms almost invariably incentivize one side to pull the other through network effects. In stage II, firms achieve network promotion through acquisition/team-up. In stage III, firms achieve network promotion through ecosystem strategies that lock in customers to the platform.

A value shop develops through service provisioning. The key is accuracy and value-added customer service. In stage I, the unique value-added services are the means to attract customers. In stage II, value shops should team up with firms that enhance their service offerings. In stage III, a value shop should ensure that the customers always feel that it is a place where they will ever get the best. Value shops block the customers by providing the best, most reliable, and accurate service and becoming a comprehensive platform.

Now, we examine the prescription of the value creation matrix.

Method and Results

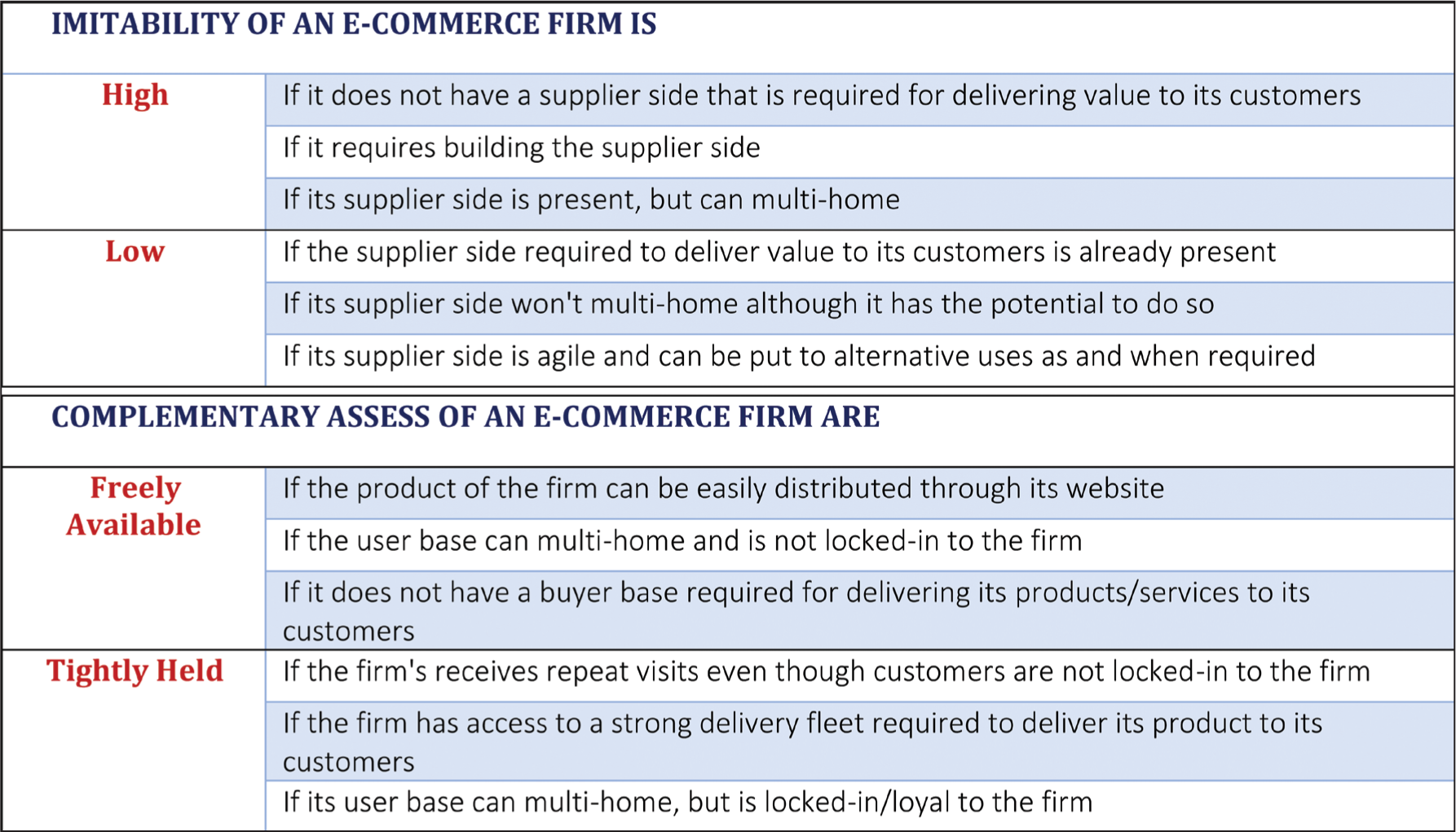

To examine the prescription of the value creation matrix, we studied 96 e-commerce firms operating in India. Out of these, 33 were unsuccessful for various reasons. To select the sample, we curated a long list of e-commerce Indian startups showing the potential to succeed and selected those about which information was readily available. We purposefully use the term potential to grow to designate the robust status of the startup at any given point in time. To validate our work, we also searched for failed startups and chose 33, about which the data was readily available. The number of unsuccessful firms was lower as data for many of these firms was not readily available. We obtained secondary data available on these firms through online search. We could gauge a firm’s business from its website and its strategies from news portals, magazine articles, etc. These sources were quite helpful for us in building a profile of sampled firms, which we then converted into a comprehensive database. We analyzed their business model, value proposition, and strategies and mapped them into the matrix based on their value configuration and the stage of development. A challenging question to answer was identifying their appropriate position in the Teece model. We developed a set of guidelines to determine the appropriate positioning on the Teece model (Figure 2). While Afuah and Tucci (2003) provide general guidelines to determine the position of a firm on the Teece model, we faced several confusions when trying to do so. Therefore, based on our examination, we developed a general set of guidelines to standardize the placement in the matrix (Figure 2).

Generally, any business consists of two sides, namely, the supplier side and the buyer side. The inimitability comes from how well firms organize their supplier side, and the complementary assets stem from their ability to have exclusive access to the buyer side. In e-commerce, these sides are generally well-defined, and in most cases, the model becomes inimitable when the supplier side is very strongly built and protected. For example, a firm may establish exclusive connections with sellers/suppliers that other firms cannot easily copy. When such suppliers are few, then the firm’s business becomes inimitable. However, many e-commerce firms with the same business model can co-exist with many suppliers. Moreover, such suppliers may multi-home (e.g., drivers on Ola and Uber, hotels listed on makemytrip.com, or booking.com), in which case the imitability of a business model remains high.

On the customer side, an e-commerce firm needs complementary assets to sell its products/services to buyers. In e-commerce companies where the product/service is digital, complementary assets are freely available, and customers can directly go to the firm’s website to purchase the product/service. However, in many e-commerce firms, complementary assets are either unavailable or need to be built from scratch. An e-commerce firm may gain tight control over its customer base by providing several services that lock them in and increase its switching cost. In such cases, we consider the complementary assets as tightly held. Complementary assets are also tightly held in cases where customers can multi-home but stick to the platform because of experiencing better service. A tightly held customer base is always better than a freely available one. Firms can then cross-sell other products/services to them or reconfigure resources to compete with new entrants. Complementary assets are freely available when the market is vast and can serve several firms and where e-commerce firms do not have tight control over them. Many delivery companies rely on delivery boys to provide their service. In such cases, these delivery boys act as complementary assets for the firm. Although they can multi-home, we can consider complementary assets as tightly held if they remain wedded to the firm.

We examined each of the 96 firms using this general criterion and placed them in the value creation matrix (Figure 1). Figure 3 summarizes the core principles that we discuss now in detail.

Stage I (Highly Imitable/Complementary Assets Freely Available)

Since the imitability is low and complementary assets are freely available, an e-commerce firm should quickly build its user base before incumbents overtake it. Therefore, it should pursue a run strategy by offering services that give at least a temporary competitive advantage. The run strategy differs for different value configurations.

Value chains should focus on building in-process efficiencies that they can pass to customers through low prices, cashback, or discounts. Lenskart—an online retailer for eyeglasses—entered the unorganized and competitive eyeglasses market where price discovery is difficult, and customers prefer interaction with the shopkeeper. By virtue of owning a high-quality manufacturing facility and supplying directly, it could pass on process efficiencies to value-conscious customers in the form of low prices. However, value chains should guard against the tendency to give discounts by burning investors’ money without having a clear path to profitability. Fashionara started as an inventory-led online fashion retail business and retailed premium and trending merchandise at deep discounts. However, when investors stopped funding, it caved into its rivals—Snapdeal, Flipkart, Myntra, Koovs, and Jabong.

In applying a run strategy, the additional services offered by value chains should augment their core offering. Lenskart, for example, offers a virtual try-on 3D feature that uses face recognition and enables customers to look for frames that best fit their face cut and thus reduce the need for physical interaction. It also uses robotics to maintain the quality of glasses to three decimal places. Providing add-on services without a clear core offering may fail. Buttercups—one of India’s leading online lingerie retailers—introduced the concept of fitting rooms with lingerie experts. It failed miserably as it tried to sell premium brands to largely value-conscious customers with little awareness of brand differentiation in Bras. Similarly, Inksedge also started with an innovative idea of do-it-yourself e-Greeting Cards. It failed, as most customers look for greeting ideas from the market rather than doing it themselves.

Value networks are quite common in e-commerce as they demand minimal investment in assets. However, because of this same reason, they are also quite vulnerable as entry barriers are also low. They need to quickly build critical mass by incentivizing at least one side of the platform. Such incentives could be in the form of free services, cash backs, referrals, and incentives. The first success criterion is having a superior value proposition that can keep incumbents gauging until they gain critical mass. Happyeasygo—an online flight and hotel bookings firm—entered the market dominated by makemytrip.com and yatra.com but could make its niche by offering lower prices than the competition and innovative booking options (advance booking facility for flight and hotel tickets, easy cancellation and rescheduling options). Razorpay, similarly, excelled in the crowded digital payments space by entering a lesser crowded B2B segment with fully digital and hassle-free onboarding of merchants. Zolostays excelled in online rental accommodation space by providing students and professionals with fully furnished coliving spaces. RentoMojo excelled by identifying the need for furniture on rent among transient professionals. It gained success in this space with a contained rollout, prudent use of capital on market expansion, and not burning cash to provide services to make ends meet. Udaan entered as an Amazon for B2B space. It allowed SMEs/Kirana (local grocery) stores to source their requirements at a lower price and permitted buyers and sellers to negotiate the terms of their transactions. It was able to onboard 3+ million retailers in this non-competitive space.

Second, value networks must be agile in building the customer base. BookMyShow—an online ticket booking portal—quickly developed its user base by establishing tie-ups with various events and attracting their participants. It now operates in five countries with over 30+ million customers in 650+ towns and cities where it covers 5,000+ screens. Similarly, Freecharge gained customers by providing discount coupons through partnerships with McDonald’s, Domino’s, CCD, Puma, Crossword, and a few e-commerce websites. Thus, it acquired a considerable customer base that remained useful when it launched wallet and digital payment services. Cred—a newbie in the digital payment space—gave its users rewards in the form of coins or gems for paying credit card bills on time. Now, it has access to a user base with high credit ratings, which it can use for offering loans and other financial services.

Blindly copying the aggregation model may prove expensive. AutoNCab was a ride-hailing application similar to Ola for Autos. However, as Ola had deeper pockets and an established user base, it simply launched its auto-aggregation service and drove AutoNCab out of the market. Ezytruk tried an on-demand aggregation for trucks but failed as the truck industry works on long-term contracts. Tazzo bikes attempted to apply the car rental model to bikes but underestimated its capital-intensive nature. The fuel and monthly instalment costs were so high that investors stopped further funding leading to its closure. Inspired by the success of Oyo, several firms launched variations of the rental business but failed to gain traction. HotelsAroundYou and RoomsTonite were into last-minute hotel room booking. However, hotels did not see a clear value proposition in this space as they had to provide rooms at half the price and readily update the room availability status. Zupermeal started with the idea of providing homemade food to its customers from domestic or home chefs. It failed as these housewives had little motivation to remain professional and maintain timings and standards for ₹10,000 per month.

Value networks also fail when they attempt to become another intermediary in the supply chain. Peppertap started with the idea of delivering groceries to customers from the local grocery store. However, as customers perceive online to be cheaper than offline, it had to provide deep disproportionate sales discounts to keep that perception. GrocShop started with the idea of delivering groceries within 90 minutes and was good with busy modern consumers. It failed as its acquisition cost and logistics were too high for it to break even in a short period of time. Overcart started as a heavily discounted marketplace for over-stock, unboxed, refurbished, and pre-owned products. Such products were traditionally sold in street markets without any guarantee of the product. Overcart could not fulfil customer expectations for better after-sales service and handling.

Quite commonly, value networks get into an acquisition spree. Even established players usually remain unprofitable to fund their growth. However, when companies only burn cash without a clear path to profitability, it is a red signal. AutoNCab acquired BigZop very early in its venture and could not compete with Ola as its funds dried up. JustBuyLive started as a Brand to Retail business model in the B2B space bypassing distributors/wholesalers. However, it could not operate for more than 2 years due to intense competition. It spent heavily on the advertisement and provided credit-based purchases under the Udhaar scheme to its retailers leading to heavy bleeding of money.

Finally, value networks are highly prone to quality issues. Foodpanda grew fast in the food delivery space in India, but barely 4 years into the business, it encountered fake listings and customers, and its image got tarnished. Similarly, Limeroad—an online fashion retailer offering clothing and fashion accessories—differentiated itself by providing all the information about the product, including the manufacturing details, place of origin, material, and fabric details. To prevent counterfeit products, it built exclusive contracts with 600 vendors. Its website provides an interactive and immersive experience. However, it faced high returns as suppliers frequently deliver products that are different from what is ordered, in effect, raising their supply chain costs.

Value shops build the user base by providing superior customer value in their interactions. In the beginning, when they are quite vulnerable to competition, they have to invest in building a customer base by providing free services or by giving referral benefits to their customers. The freemium model helps build a substantial user base even if customers do not convert. The key to converting customers is their experience during their first trial of the product/service. Grammarly, for example, offers basic grammar checking for free. Customers convert to full service when they see value in the software. Zoomcar gained popularity due to its hassle-free customer experience in the self-drive car rental space. After their first booking, customers could forego the security deposit and drop the car at a nearby Zoomcar location rather than return to the city of origin. Some value shops also gain customers by becoming a one-stop shop for any specific need. WedMeGood became popular by becoming a one-stop solution for all one’s marriage services needs, including Photographers, Makeup Artists, Decor, Bridal Wear, Grooms Wear, Cinematographers, Invitations, Mehendi Artists, Wedding Planners, Jewellery, Trousseau Packers, Venue Bookings, Catering, Wedding Cakes, DJs, Choreographers and Accessories. Similarly, Dineout became a platform of choice for table booking in restaurants as it allowed cashless payment and cashback and discounts up to 50% on the bill. Its Dineout passport offers a minimum of 25% discounts on restaurants across 20 cities in India and 5-star hotel restaurants. In the EdTech space, Unacademy built a learning platform for several students that provides material and examination preparation content for major competitive examinations and provides lectures from good teachers in the form of videos on different subjects.

Value shops fail when they do not have a clear monetization plan. Cardback—a payment recommendation platform—recommended the best mode of payment to credit, debit, prepaid cardholders, and mobile wallet users. However, it failed as not many users used multiple credit cards in India. Askme started as a one-stop platform for information related to any business, mainly restaurants, flights, travel, and gadgets. However, after gaining a user base, it began experimenting with furniture and grocery retail and failed miserably. Value shops should also be careful not to give too much for free. DocTalk—an online consulting platform for patients to consult with doctors and have follow-up consultations—incorporated an Electronic Medical Records facility so that doctors could write digital prescriptions. However, this solution resulted in a high cost of operations, and doctors preferred writing manual prescriptions to save time. Similarly, Taskbob started with the idea of providing home services at the tap of a button and removing the major pain point of poor-quality service. It did not succeed because customer acquisition costs remained high, scalability was difficult, and fund flow was irregular, making profits elusive.

Stage II (Highly Imitable/Complementary Assets Tightly Held)

The key in this stage is to expand the customer base through tie-ups/mergers & acquisitions/joint alliances. Even if a firm’s business model is highly imitable, it can compete in the market as it has access to complementary assets. If a firm starts from this stage and does not have access to complementary assets, it should either build them or tie them up with those who own them. The team-up strategy differs for different value configurations.

Value chains should team up to expand their customer base through horizontal integration or improve efficiencies through vertical integration. Horizontal integration typically involves acquiring other firms. For example, Myntra & Jabong retailed Fashion wear and merchandise of popular brands. Flipkart acquired Myntra in 2014, and Flipkart-owned Myntra acquired Jabong in 2016 to build a combined user base of 15 million monthly active users. Firms may also expand their product base through horizontal integration. Nykka built exclusive tie-ups with premium brands and retailed authentic products in the niche beauty retail segment. It also established tie-ups with several sellers, brands, and independent vendors across the country to expand into innerwear. Pepperfry tied up with Zefo—an online marketplace for pre-owned furniture—to provide customers with an opportunity to sell their old furniture to Zefo in exchange for Pepperfry gift cards through the ‘Exchange Your Furniture’ service.

Value chains also integrate vertically to reduce intermediaries, augment the supply chain, and improve customer service and conversion rates. For example, Netmeds acquired Delyver to strengthen its logistics network. Pepperfry—an online furniture retailer—partnered with furniture merchants and connected them with customers by listing their products on its website. Instead of outsourcing logistics, it built a hub and spoke distribution model to transport goods. It claims to have the capability to deliver more than 100,000 large items per month. Value chains typically practice an omnichannel strategy by being present offline and online to improve customer connection and conversion rates. Pepperfry has established 40+ experience centres all over the country with an average size of 3,000 sq. ft., which allows consumers to interact with the products physically. Similarly, Zivame—an online lingerie retailer—has a presence in 800+ Multi Brand Outlets stores across India and focuses on helping women buy a wide range of lingerie discretely. It plans to open up to 100 offline retail stores across the country to establish itself in this highly competitive space. Value chains also practice private labelling by organizing lesser-known brands under its label. Zivame, Pepperfry, Myntra, and Nykaa, have all launched their private labels.

Value chains must watch out for excessive expansion sprees. It is easier to scale a value network, but scaling a value chain is expensive, as similar chains have to be established in various terrains. Moreover, their rapid expansion leads to intense cash burning and may even deplete capital and funding sources. Netmeds played this game very well. It is an online pharmacy that allows customers to purchase a wide range of healthcare products like prescription drugs, over-the-counter medicines, diet/fitness supplements, general healthcare products, and ayurvedic and homeopathy medicines. It expanded into the offline pharmacy market by offering franchises and helping other offline pharmacies source medicines at wholesale prices, thus replicating its business model beyond the online platform to reach all parts of the country. This has given it a clear strategic advantage over its online and offline rivals. However, Yumist succumbed to cash burn when it attempted to scale. It started with the idea of providing homemade meals rather than restaurant delivery within 30 minutes in a city. It focused on preparing the food itself rather than sourcing from restaurants. It grew quite well with few offerings. But since consumer tastes are different, it became difficult for them to scale their business for various food items and diverse cities. They eventually ran out of cash for further operations and had to exit the market.

Value networks should focus on growing the two sides with zero or reduced incentives and build complementary assets to improve customer value and profitability. Lowering incentives does not have a detrimental effect on the supply side because of the network effect. The network effect occurs because of the tightly held customer base and the additional services provided to the other side of the network. Value networks should aim to become a comprehensive platform. Generally, value networks team up to augment their customer base. Snapdeal, which started as a daily deals and coupons website and later shifted to an inventory model followed by a marketplace model, grew up with several acquisitions, such as Grabbon, eSportsbuy, ShopO, Exclusively, Freecharge, and Vulcan, to augment its product range as well as logistics. It later divulged many of these acquisitions to prevent a cash crunch but amassed more than 300,000 sellers and build a country-wide delivery. PhonePe grew in the digital payment space. Flipkart acquired it and rebranded it as a PhonePe wallet. As a result, it acquired a vast user base.

However, value networks must ensure their strategy is workable before growing their user base. Tinmen, a food delivery platform, provides students and working professionals with home-cooked meals. It failed to gain traction because of its flawed strategy. It registered 60 home chefs and was clocking 1,500 orders per day. It managed to get down the cost of delivery to a fraction of its competitors by bringing down the average cost of a meal on its platform to under ₹100, and at the same time achieving operational profitability. Home-cooked food is always preferred in India, but every home has a different taste. Tinmen connected students with different home chefs who could not provide variety and home taste. As their strategy was flawed, expanding the user base did not work.

Value networks also team up to augment their offerings (supply-side). Augmenting offerings also has a retention effect on customers who may want to stick to a comprehensive platform. Olx India, for example, started as a marketplace for buying and selling services and goods, such as electronics, cars, furniture, and bikes. Surprisingly, it did not have major head-on competition from any firm in India. Quikr came close but had a different offering. It made strategic acquisitions to grow its classified offering, particularly in the real estate division. It expanded its customer base primarily through aggressive advertising and is among the few online marketplace platforms that turned profitable. Many times firms augment their offerings to cross-sell to their existing user base. A good example is Swiggy—one of India’s largest online food ordering and delivery platforms. It has built a strong network of 75,000 restaurant partners and a 135,000 delivery fleet across 120 cities in India. After establishing solid tie-ups, it expanded into general product deliveries (Swiggy Stores), instant pick-up and drop service (Swiggy Go), Daily meal delivery service (Swiggy Daily), and dedicated inexpensive meals for one called Swiggy Pop.

Value networks can quite often cross-sell additional services to their existing customer base. These additional services must enhance the value of their core services. PhonePe, for example, is planning to release its CRM solution—PhonePe for Business—which will allow offline merchants to get a digital view of their earnings. It may add additional services like credit and insurance for offline retail stores. Trying to lock in customers without building a substantial customer base may not always be a good strategy. Shopclues specializes in domestic appliances, fashion, and daily utility items. It has managed to stay afloat and established a customer base by primarily targeting customers in Tier 2 and 3 cities and listing goods from Chinese vendors. However, it is venturing into the enterprise business early on and selling its in-house solution and SmartOps to other e-commerce vendors. It seems to be a losing proposition.

Value networks also team up with/acquire firms that increase the value of their offerings, such as analytics and technology services firms. Ixigo is an AI-based online travel comparison engine. The online travel services industry is highly competitive due to low entry barriers, and companies burn huge cash with lucrative offers to acquire and retain customers. Its comparison service has garnered a solid user base of 170 million. The service provides real-time price comparisons of flights, and hotel reservations, attractive customer cashback offers, and an easy-to-use interface.

As a value network becomes comprehensive, it also becomes invincible. Hungama, for example, has become a comprehensive platform for Asian and Bollywood entertainment in India. It provides free and unlimited access to music in India’s Hindi, English, and other regional languages to its vast customer base of 1.5 Billion South Asian worldwide. It also provides access to exclusive content. Users stick to the site because it is a comprehensive platform that offers quality content at a lower price. Exclusivity and comprehensiveness increase network effects which keep the customer returning to the site.

To build a comprehensive customer base, value shops should provide more value-added services (by acquiring/teaming up). Such services should augment their core offering. Services that do not enhance a firm’s core offering would unnecessarily drain its resources. Practo, for example, has marked a strong presence as an online platform for medical appointments with a doctor. Its successful core offering provides a platform where patients can take consultations from doctors online. The company keeps a timeline of patients’ medical records and helps them get the right fit of doctors and medical practitioners. To augment its core offering, it acquired Qikwell, which allows appointment bookings and contactless payments and thus reduces waiting time. In the same space, 1 mg started as an online platform for information about all varieties of medicines and later included further related services, such as medicine delivery, information, lab test, and doctor consultations. To augment its information base, it acquired Homeobuy, which deals in homoeopathic and ayurvedic medicines. Because of an outstanding database of information about medicines, authentic pharmacies, and excellent customer support, 1 mg has made an indelible space online. PolicyBazaar has become India’s largest aggregator and marketplace for all insurance products in the online insurance space. It helps customers research and compare various insurance policies and thus make an informed decision. It also assists in the renewal or cancellation of the insurance policy. It has many exciting features that augment its core offerings, such as a hospital locator, garage locator, insurance premium calculator, and claim assistance. It also launched DocPrime, an online medical service platform that provides real-time consultation with doctors over chat and call.

However, value shops should watch out for the frenzy to launch several services as it may unnecessarily drain their funds. GoZoomo—a mobile-based peer-to-peer platform for purchasing pre-inspected cars directly from owners—solved the trust problem behind the used car market. There is no structured way to inspect cars in India, and people find it hard to trust used cars. GoZoomo inspected the car itself. However, it could never recover the inspection cost if the car turns out of poor quality. Moreover, their price engine—a self-developed software could not capture the market price.

Stage III (Low Imitability/Complementary Assets Freely Available/Tightly Held)

The key in this stage is to lock the customer base. E-Commerce firms may reach this stage by growing organically or directly starting if their business model is inimitable and complementary assets are freely available or tightly held. The lock-in could arise due to network effects or superior customer service. How much lock-in manifests depends on the value configuration of the firm.

Value chains lock in customers primarily through superior customer service that stems from their process efficiency. Bigbasket became indomitable in online grocery retailing by virtue of its inimitable supply chain competencies and garnered a strong base of 10 million customers. Customers remain wedded to Bigbasket due to its superior services. Ninjacart—India’s largest fresh produce supply chain platform in the B2B space—became successful by leveraging technology to solve supply chain problems. It could enlist 7,000+ farmers and 8,500+ retailers and move 500 tonnes of fruits and vegetables to hundreds and thousands of retail stores across India within just 2.5 hours with an accuracy of 99.88%. Due to superior technology and expertise in the supply chain, it provided excellent service and locked-in retailers. Similarly, Caratlane—an online jewellery retailer—locked in customers owing to its superior customer service because of its expertise in diamond cutting at its manufacturing facility. It became a retailer of choice for those who wish to have custom-built diamond jewellery. Mamaearth—an online lifestyle and beauty business—became a retailer of choice for those who wanted chemical-free products. It was Made Safe certified in the entire Asian beauty and lifestyle market. Its chemical-free products were digitally marketed by 500+ moms involved from conceptualization to formulation of products, thus creating a sort of lock-in for its customers. Value chains should look to induce some kind of lock-in, particularly in the face of competition. Amazon Prime comes with free access to entertainment content and locks-in customers. Similarly, Flipkart has launched an innovative lock-in strategy—Flipkart plus—which is entirely free but requires customers to gather a certain number of points to access this service. It thus creates greater engagement for customers on the platform and locks them in.

Successful value chains sometimes face inherent flaws in their business model, which become serious with a more extensive user base. FabFurnish—an online store for custom-fabricated furniture—failed because it could not respond to requests for the furniture replacement. Replacement of furniture is inherently tricky. Although FabFurnish processed close to 0.1 million requests per month with an average exchange size of ₹14,000, it could not survive. Similarly, Eatfresh—an online restaurant and food delivery service—could not continue with its idea of custom chef delicacy after it gained several customers. While the concept was lucrative to start with, it failed later as the idea of a daily changing menu did not go well with customers.

Value networks induce lock-in primarily through network effects, either natural or engineered. Dunzo—a delivery platform—experienced substantial cross-side network effects because an average user used Dunzo more than five times a month for delivering items. It garnered a considerable merchant and customer base and received around 35,000+ orders daily. Similarly, Zomato—a food delivery platform—became the world’s largest restaurant aggregator. By virtue of network effects, it gathered a huge customer base and locked them in through induced network effects. It provided a host of related services, such as restaurant information, menus, and user reviews of restaurants. It provided restaurants with access to the customer database and analytical tools for targeting them. Restaurants could connect to their customers directly using Zomato Whitelabel. Customers could book a table in a restaurant using Zomato book and get complimentary food and drinks using Zomato Gold. IndiaMart—a trading marketplace for B2B buyers and sellers, garnered 93 million buyers, 5.9 million suppliers, and 60+ million products and services by providing hosting services on its platform.

Similarly, Quikr became indomitable in the C2C buy and sell space due to network effects generated by more than 10 million unique visitors. It developed several verticals, such as real estate, used cars and bikes, goods, Quikrjobs, and QuikrEasy, and provided regional language support so that buyers/sellers could chat in their preferred language. Ola became a prominent player in the taxi aggregation space due to its excellent service and strong cross-side network effects. Ola locked drivers by providing them with financing options and thus also locked customers. Similar is the case with OYO—an online platform for hotel booking—which became the largest chain of hotels in the world with an international presence in several Asian countries. Because of strong network effects, it could develop its network in 500+ cities and offer a hassle-free experience at a reasonable price. To further create lock-in, it practised a multi-brand strategy. It launched several products, such as OYO rooms, SilverKey (Corporate Apartments), OYO Living (millennial housing), Pallete (Resorts), OYO Homes (Vacation rentals), and OYO townhouse. Yatra—an online travel booking company—locked in customers by providing a full range of travel services, including domestic and international air ticketing, hotel booking, holiday packages, rail ticketing, bus ticketing, and cruise ticketing. It differentiated itself from the rest by providing a comprehensive Self-Booking Platform that seamlessly integrates with customers’ ERPs/HRIS systems and can ensure tight policy compliances and manage complex approval processes.

Some value networks induce lock-in by providing customers with superior value. Gaana, a music streaming app, streams Indian and International music. By providing access to exclusive regional music and a highly personalized listening experience, it garnered a strong base of 150 million. It struck exclusive contracts with music providers for music streaming on its website. Its AI engine provides personalized recommendations, which gives users a very satisfying experience on the platform, thus creating a virtual lock-in for its customers. Grofers—a hyperlocal delivery platform—locked in customers with superior service and value. It identified the customers’ needs very well and made sub-verticals to satisfy their needs. It onboarded 5,000+ retailers and wholesalers and can deliver 25 million+ products monthly. Similarly, RedBus—an Indian online bus ticketing platform—grew indomitable. It provides many bus booking options and unmatched benefits to its 18 million customers. It offered SeatSeller, a global distribution system used by RedBus for the bus ticketing applications of different travel companies and third-party travel agencies.

Value networks also induce network effects. JioMart started as a platform for same-day delivery of household essentials and groceries. It is an online-to-offline marketplace that sources grocery items from nearby merchants. To induce network effects, it enticed its existing Jio user base with early grocery purchases and delivery discounts, thus building a vast user base. It collaborated with the local grocers with POS terminals and provided low interest working capital, GST compliance, and inventory management skills to make the system work. Similarly, Dream11—a gaming platform for fantasy sports—garnered more than 100 million customers. It offered fans numerous opportunities to connect closely with the sports they enjoy, including fantasy sports, content, exchange, interactions, and activities. Dream11’s fans remain sticky through induced network effects—the more users, the greater the prize money. MakeMyTrip—an online travel agent that allows booking tickets for airlines, hotels, trains, buses, cabs, etc.—became a leading online travel company by continuously focusing on new product offerings and services. At the same time, it continually kept evolving its technology to meet the ever-changing demands of the rapidly developing global travel market.

An extensive user base may become dangerous because of flawed lock-in strategies. Doodhwala—a hyperlocal milk delivery application—allowed users to order milk and household products straight to home. Its business model was robust, and its last-mile workforce consisted of existing milkmen and part-time workers. It grew to have 30,000 deliveries per day, became the largest milk e-tailer with 13 lakh litres monthly, and had the highest delivery fulfilment rate at 99.8%. Even though the space was not so competitive, it failed due to its joining bonus strategy. The first month’s subscription was free, but customers took advantage of free subscriptions by logging in from different accounts each month. Doodhwala could not recover its expenses and, as a result, collapsed.

Value shops lock the customer base by becoming a comprehensive platform for any specific service. Byjus—a successful EdTech platform—provides highly personalized learning and preparation for competitive exams for school children and undergraduates. Students consider it their first choice because of rich, engaging, quality content and prevalent network effects. Unacademy—another EdTech player that focuses on providing material and examination preparation content for major competitive examinations and lectures from good teachers. It built a community of 3+ million and benefitted over 0.3 million students from over 2,400 online lessons and specialized courses. Similarly, upGrad, which targets the higher education segment, has partnered with reputed institutions. It has a more than 85% course completion rate and more than 50,000 paying students. It has a vast learner base of around 0.3+ million. It has created a robust community designed to improve the experience further, including one-on-one mentoring, peer-to-peer learning, business networking, and, most importantly, expert career guidance with reputed institutes. IIMjobs—an online job search platform—became indomitable by focusing on the premium end of the recruitment space. The quality of jobseekers registered on iimjobs.com is not available on other channels. Because of its excellent quality services, it could acquire a base of 30,000+ recruiters and 500,000+ job seekers.

Value shops use superior tools to improve their service and thus induce lock-in. ZebPay was quite successful in the cryptocurrency space because of providing secure exchange services for different cryptocurrencies. It rebooted in India after a big break post-RBI’s ban on cryptocurrency. It does not charge anything for withdrawal and depositing in the crypto wallet, and its API integration helps them capture new markets easily. Similarly, CarDekho—a comprehensive car information portal—locked in its customer base. It provided rich automotive content, such as expert reviews, detailed specs, price comparisons, videos, and pictures of various car brands and models available in India. It launched many innovative features to ensure users get an immersive experience of the car model before visiting a dealer showroom. It used a rich array of tech-enabled tools, such as apps for dealer sales executives to manage leads, cloud services for tracking sales performance, call tracker solutions, digital marketing support, and a virtual online showroom. It also outsourced lead management operational processes for taking consumers from inquiry to sale. Thus, it created stickiness for its customers by providing value-added tools. Droom is another platform for purchasing and selling used and new vehicles, including two-wheelers, four-wheelers, bicycles, and air vehicles in B2C, C2C, C2B, and B2B segments. It uses AI and data science to drive online transactions on its platform. It offers private buyers and sellers, distributors, and large companies purchasing and selling and managing the entire life cycle and all ancillary vehicle services. Thus, it can lock in its customer base by providing comprehensive services related to the vehicle. ClearTax started as a platform to facilitate individuals, accountants, and traders to file income tax. It created a host of services to ensure its user base remains sticky to the platform. These include trademark registration, company registration, mutual funds, Tax consultancy, and education on GST.

Similarly, Cure.fit grew substantially in the online fitness space by launching different fitness verticals, namely cult.fit, eat.fit, mind.fit, and care.fit, cover the entire gamut of care a person needs. JustDial became India’s leading local search engine that provided local search-related services to make several day-to-day tasks conveniently actionable and accessible to users through one App. It recently launched an all-in-one application with multiple features, including map-aided search, live TV, videos, news, and real-time chat messenger. Justdial also launched a business management solution for SMEs—JD Omni—through which it offered them POS Billing, Inventory management, e-commerce, and website management. Nestway built an indelible mark in the home accommodation and rental market by acting as an intermediary between the house owners and the tenants. It took care of the entire rental life cycle, from the start to the closing of the rental agreement, ran background checks on the tenants, and did all the paperwork, onboarding, and collecting rent from the tenants. It also provides NestAway maintained spaces where it furnishes the entire house and rents it on a sharing or individual basis. Zerodha is a thriving online stock trading platform having members of various markets: NSE, BSE, MCX, and MCX-SX. It offers several services, including retail and institutional broking, mutual funds, currencies, commodities, trading, and bonds. With its highly disruptive pricing model and in-house technology, it has become the most prominent stockbroker in terms of maximum active retail clients. It also educates its customers on stocks and empowers and helps retail and small traders and investors. It does not have relationship managers who push their clients for turnover, and thus customers remain loyal to it.

Value shops must watch out for security and regulation when operating in volatile markets. CoinSecure—a real-time Indian bitcoin trading platform—failed miserably due to a theft of 438 bitcoins amounting to $3.3 billion of customers’ money. It did grow by building a slew of services, including a bitcoin wallet, merchant gateway, robust APIs, a test net service, and a blockchain solution. But it went loose on security and was stung by theft by its employee, who got hold of the private keys to the exchange’s wallet. Similarly, Koinex—another multiple cryptocurrency exchange platform and a trading platform that fuels Blockchain-powered internet—closed down because of RBI’s notice to exchange platforms to avoid trading in Bitcoin.

Discussion and Implications

The study developed the value creation matrix based on Teece Model and Thomson’s value configuration to gain further insights into the value creation by e-commerce startups. The same was validated on a sample of 96 Indian e-commerce startups. The study is in line with the propositions of the Teece Model and Thomson’s Value configuration, as applied to the e-commerce context by Afuah and Tucci (2003). Using that, we found that those e-commerce firms that followed Afuah and Tucci’s (2003) strategic prescriptions remained successful, and those that did not experience failure.

Implications for Research

In terms of implications for research, this research develops the value-creation matrix for examining the strategies of specific startups. Since this matrix is validated over 66 successful and 33 failed startups, the findings are fairly generalizable. This study thus adds to the Rietveld and Schilling (2021) call to holistically examine the valuecreation phenomenon in e-commerce platforms. Scholars can use this matrix to examine specific strategies of startups. The article extends the seminal work by Teece (1986) on profiting from innovation and Thomson’s value configurations as institutionalized by Afuah in the case of ecommerce businesses. The use of a value configuration lens ensures a holistic view of platforms covering, which could start on the tenets of pipelines (value chain), marketplace (value network), and service (value shop). As evident from the review of the prior work, the current state of the literature on value-creation strategies in platforms is scarce in covering insights from the Indian context. The present study adds insights from the Indian context, which is booming with e-commerce startup initiatives. Also, prior work has focused on successful cases. Hence, the inclusion of unsuccessful e-commerce startup firms for the analysis, along with successful cases, adds to the robustness of the current framework.

Implications for Practice

The research shows that firms adopt different strategies in different value configurations and growth stages. The proposed framework can aid the practitioners—managers, entrepreneurs and investors in locating the e-commerce firm’s offering and suggest the strategies to be adopted by them. The value creation strategies of e-commerce startups are presented as a prescriptive matrix (Figure 3). The matrix developed in this study will be helpful for firms to analyze their current offerings and build a suitable investor pitch. Investors can use the matrix to analyze a firm’s strategies and positioning in the e-commerce space. Startups can look for inspiration from this matrix for specific prescriptions for their firms. Investors can locate their firm’s offering in the value creation matrix and identify strategies to help them scale further in the e-commerce space.

Limitations and Future Research

The results of this study should be examined in light of its limitations. The biggest limitation of this study is that the data has been drawn from secondary sources. Since the dataset is huge, it was almost impossible to gain access to these firms, so we had to resort to secondary sources. Future studies may examine the framework using the primary data. Future studies may also examine the value creation matrix in other geographical contexts.

Conclusion

The study reveals that firms adopt different strategies in different value configurations and growth stages. Few strategies are common across all the value configurations, such as cash-burning to quickly build the customer base, teaming up or acquisition to expand the customer base and locking in to block and defend the customer base. All firms try to protect their customer base by building an ecosystem of their offerings and locking-in customers to their ecosystem. Still, some strategies starkly differ across different value configurations. Value chains make the customer base by offering products from existing sellers and adopting strategies to increase profit margins. They pursue the private label strategy for providing cheaper products and an omnichannel strategy to improve customer conversion rates. Value networks incentivize one side of the platform to create a customer base. They stop incentivizing after reaching a critical mass of the customer base, as the network is valuable. Value shops use technology to make more value from managing the transactions for both parties. Their intensity of service increases with the development of the customer base.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.