Abstract

Food inflation in India for the past few years has been at a historic high. However, the evidence suggests that higher food prices, while adversely affecting those who spend most of their income on food, have not necessarily been helpful to smallholder farmers. The volatility of food prices at the wholesale and retail levels has also remained high, creating uncertainties for consumers and producers. This article reviews recent trends in food prices in India, examines the sources of food price increases and volatility, separates the relative roles of demand–supply imbalances, cost-push factors and speculation and draws out some of the implications of those factors.

Introduction

Food crises, epitomized by periodic spikes in the global prices of food, have moved to centre stage globally. In 2012, the world experienced its third food crisis in five years. While demand has indeed grown as population expands and countries move up the income ladder, the fundamental factors explaining these periodic crises seem to lie elsewhere. One is a long-term crisis affecting agriculture in many countries, as a result of inadequate investment in essential infrastructure, such as irrigation and drainage and poor extension of the benefits of technical knowledge to the farming community. This not only directly affects the level and elasticity of supply, but also limits productivity increase. Combined with cost increases that are not easily passed on, these inadequacies are challenging the viability of crop production in many contexts. Thus, when bad weather, for example, adversely affects food production at some source, the demand–supply imbalance provides cause for strain.

Second, with geopolitical and other factors keeping oil prices high and near their oil crisis levels in real US dollars, the world is turning to bio-fuels as a source of energy. The result is the diversion of food output to non-food uses and the shift of land away from the production of food to the production of ‘feedstock’ for fuel. FAO Director General José Graziano da Silva, writing in the Financial Times (9 August 2012), called on the United States to substantially reduce the diversion of maize to ethanol production. He argued:

[w]ith world prices of cereals rising, the competition between the food, feed and fuel sectors for crops such as maize, sugar and oilseeds is likely to intensify. One way to alleviate some of the tension would be to lower or temporarily suspend the mandates on biofuels. At the moment, the renewable energy production in the US is reported to have reached 15.2 billion gallons in 2012, for which it used the equivalent of some 121.9 million tonnes or about 40 per cent of US maize production. An immediate, temporary suspension of that mandate would give some respite to the market and allow more of the crop to be channelled towards food and feed uses.

The result is that food prices tend to move with fuel prices and remain high so long as the latter are buoyant. This, unfortunately, has been the case for more than a decade now, with few and very short signs of reprieve.

Third, the tendency to food price inflation that these developments generate is being strengthened by the discovery of commodities, including food products, as an ‘alternative investment class’. The resulting financialization of commodity markets and the rapid growth in commodity futures trading is, according to analysts, influencing spot prices, largely in the upward direction.

The continuous play of these factors means that any temporary shortfall in supply paves the way for sharp price increases, resulting in consecutive spikes of crisis dimensions. The result is an increase in the number of the world’s citizens that is deprived of adequate access to food and experiencing an intensification of chronic hunger. The previous two crises, in 2007–08 and 2011, had also led to high food prices, resulting in increased hunger, localized famines and widespread increase in deprivation. These twenty-first century crises confirm that the world still remains prone to food price inflation (and volatility), with unacceptably adverse implications for nutrition, health and survival. Such inflation is even more unacceptable in developing countries, such as India, with a higher proportion of their populations living at the margins of subsistence.

Food, which provides nutrition, has the first claim on the budgets of human beings. Not surprisingly, food accounts for bulk of the expenditure of lower income groups of population in poor countries, with diversification away from food being significant only above some critical level of income where the minimum requirement for this basic necessity is met. When food prices rise, those with incomes above this critical level tend to reduce their consumption of non-essentials and protect their economic access to essential food items. This option is not available to those below that critical level. Thus, food price inflation intensifies hunger among the poorer sections of the population and deprives them of the minimum nutrition needed for a healthy life.

It is, therefore, of concern that food inflation in India for the past few years has been at a historic high. However, the evidence suggests that higher food prices, while adversely affecting those who spend most of their income on food, have not necessarily been helpful to smallholder farmers. The volatility of food prices at the wholesale and retail levels has also remained high, creating uncertainties for consumers and producers. This article reviews recent trends in food prices in India, examines the sources of food price increases and volatility and draws out some of the implications of those changes.

Food Price Trends: India

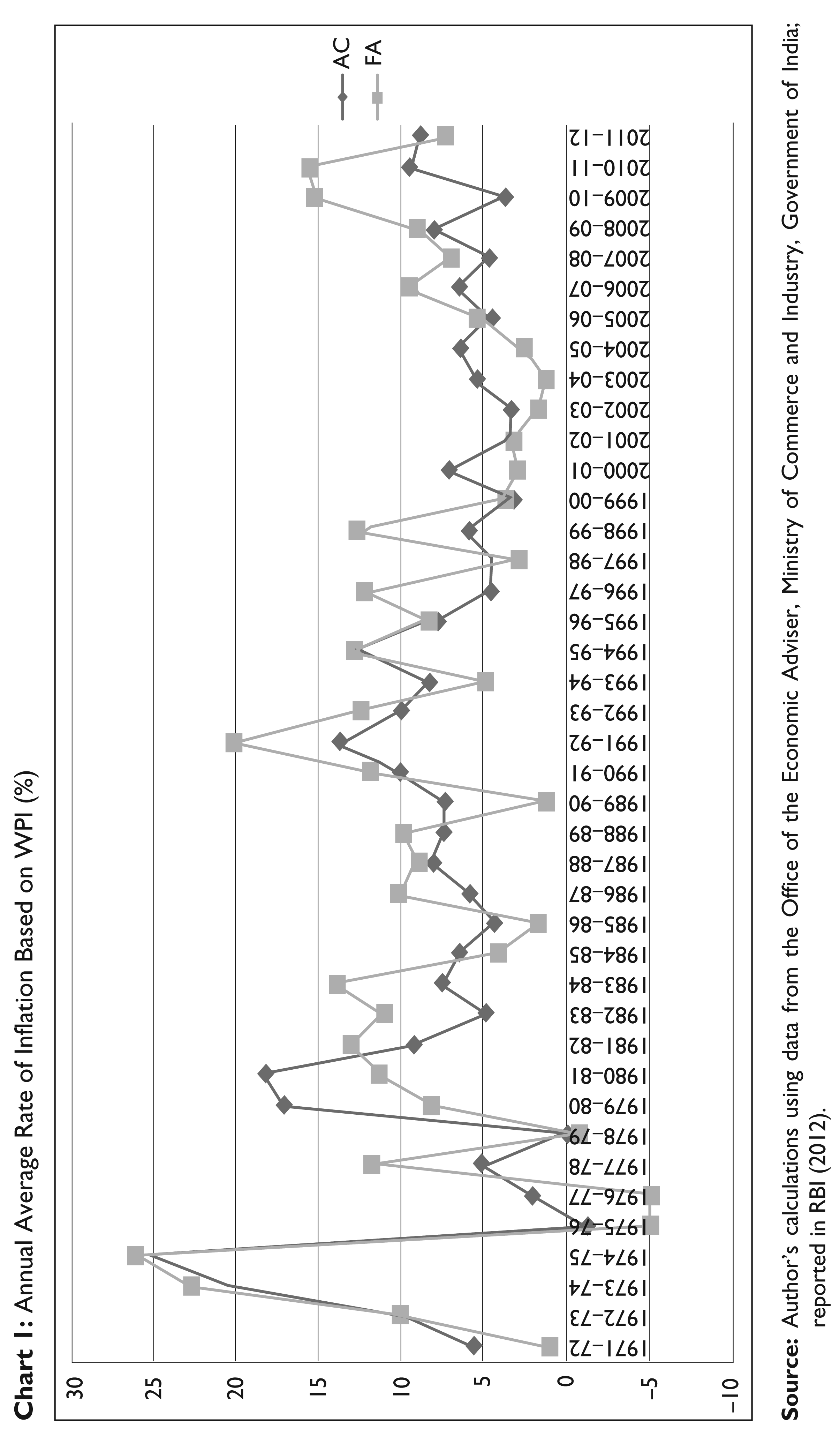

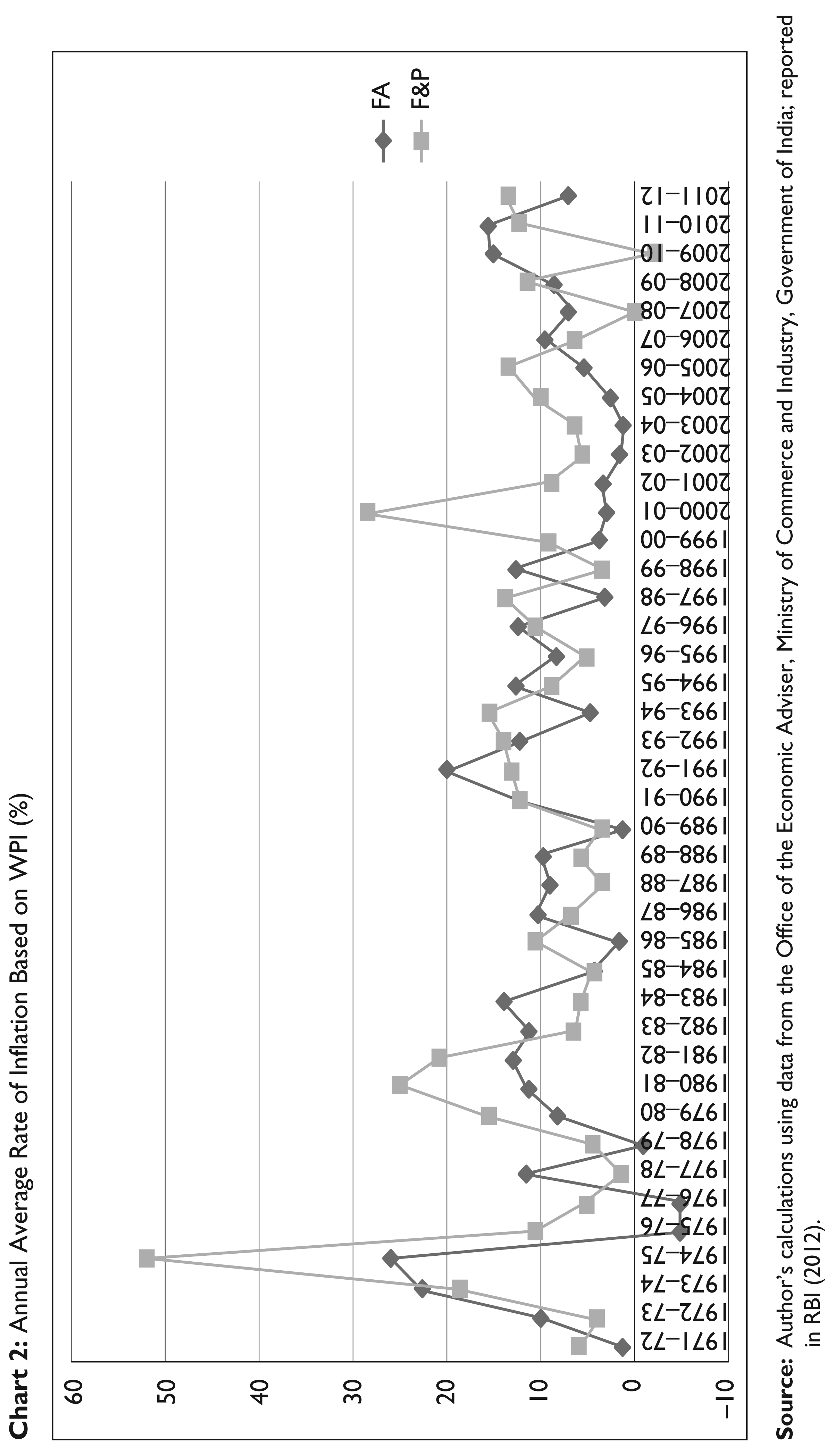

Over much of the 1970s, after the food crises of the 1960s and before India moved on to a higher GDP growth trajectory, the movements in the Wholesale Price Index (WPI) for Food Articles (FA) more or less corresponded to those of the index capturing the prices of all commodities (AC). However, from the 1980s onwards, movements in the two indices deviated from each other, with the volatility in the index of food prices being much greater than that in the index for all commodities (Chart 1). This deviation occurred despite the fact that, barring 1979–82 and 2000–01, when fuel prices peaked, movements in the price indices for food articles (FA) and fuel and power (F&P) showed a substantial degree of correspondence (Chart 2).

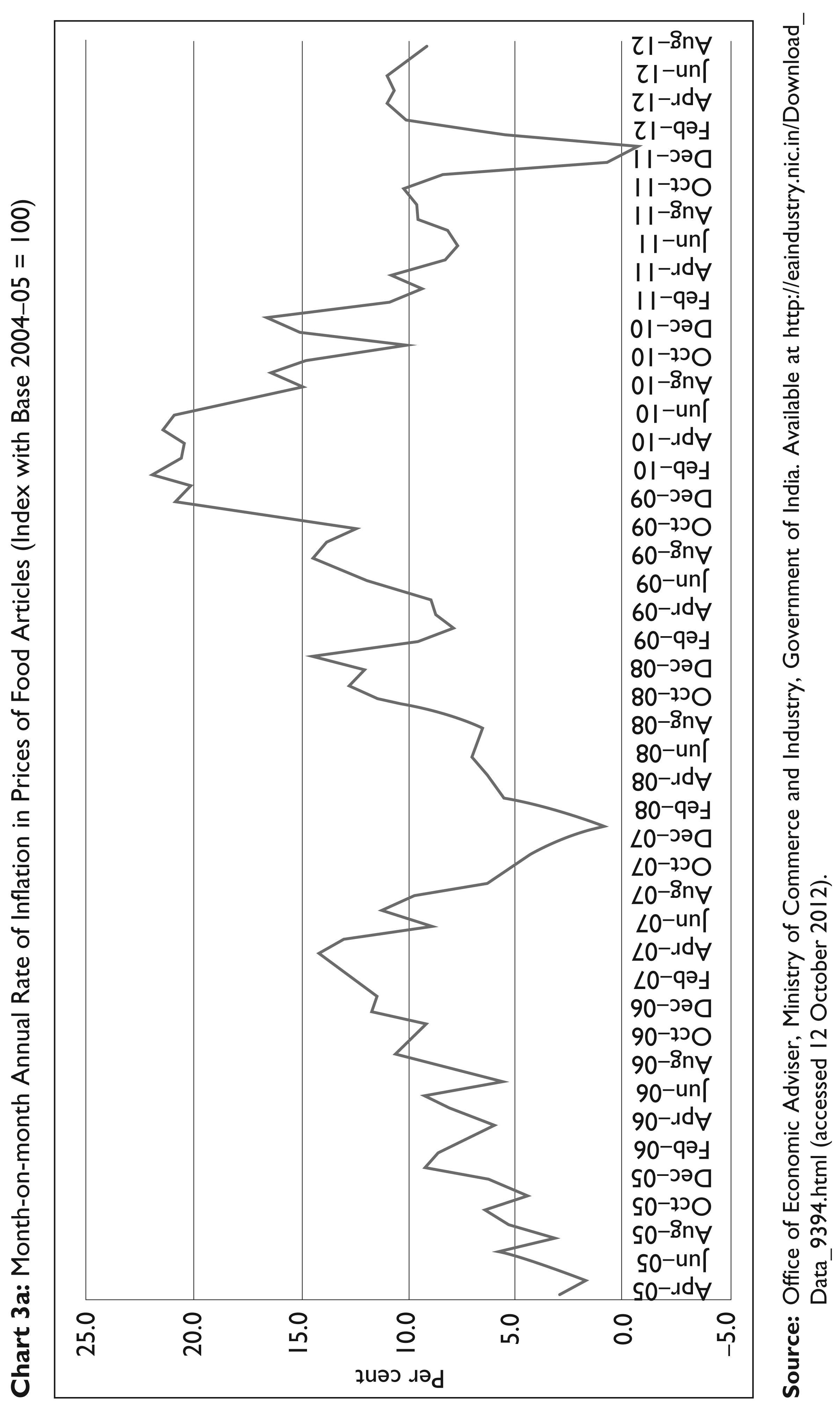

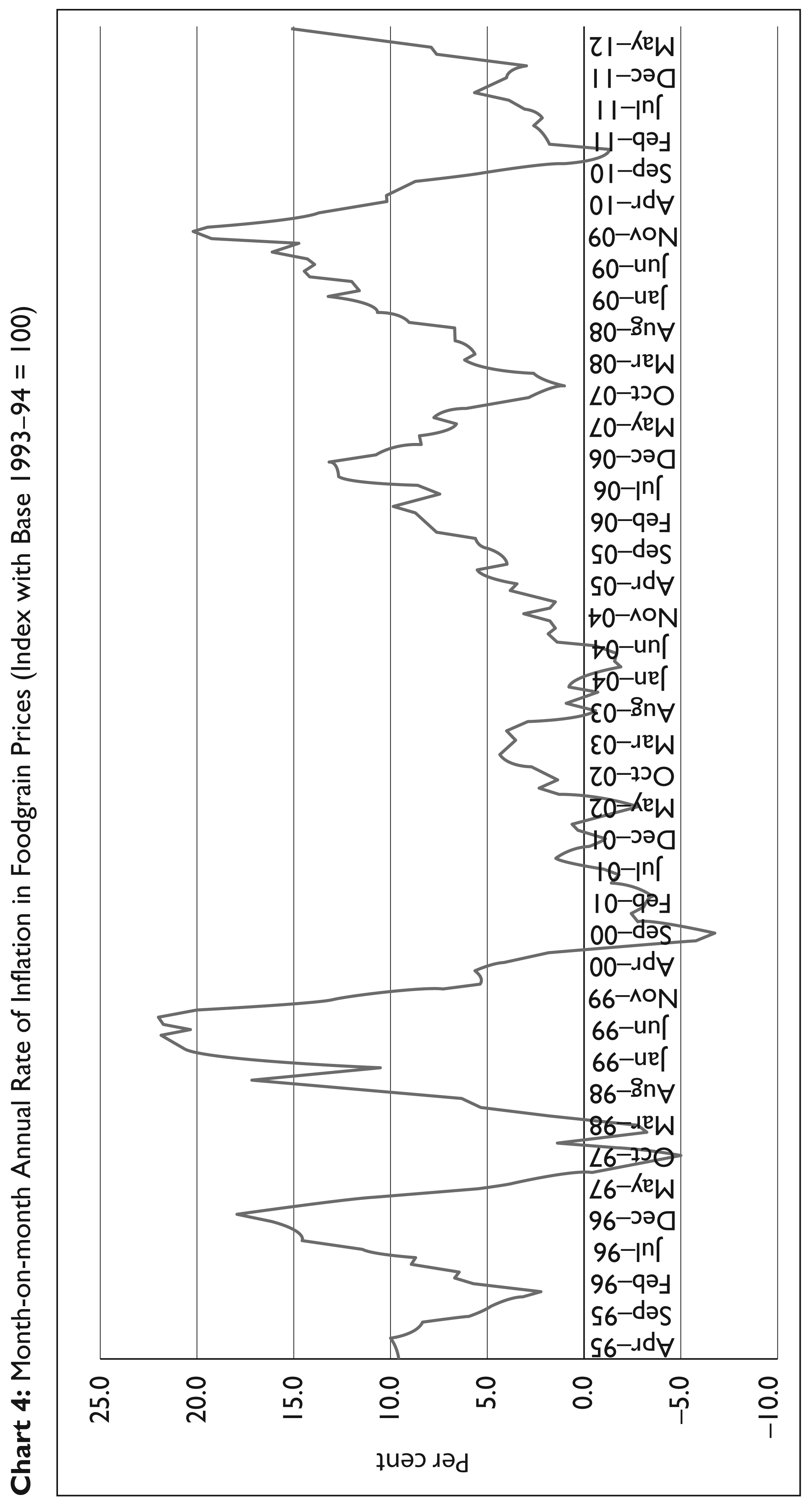

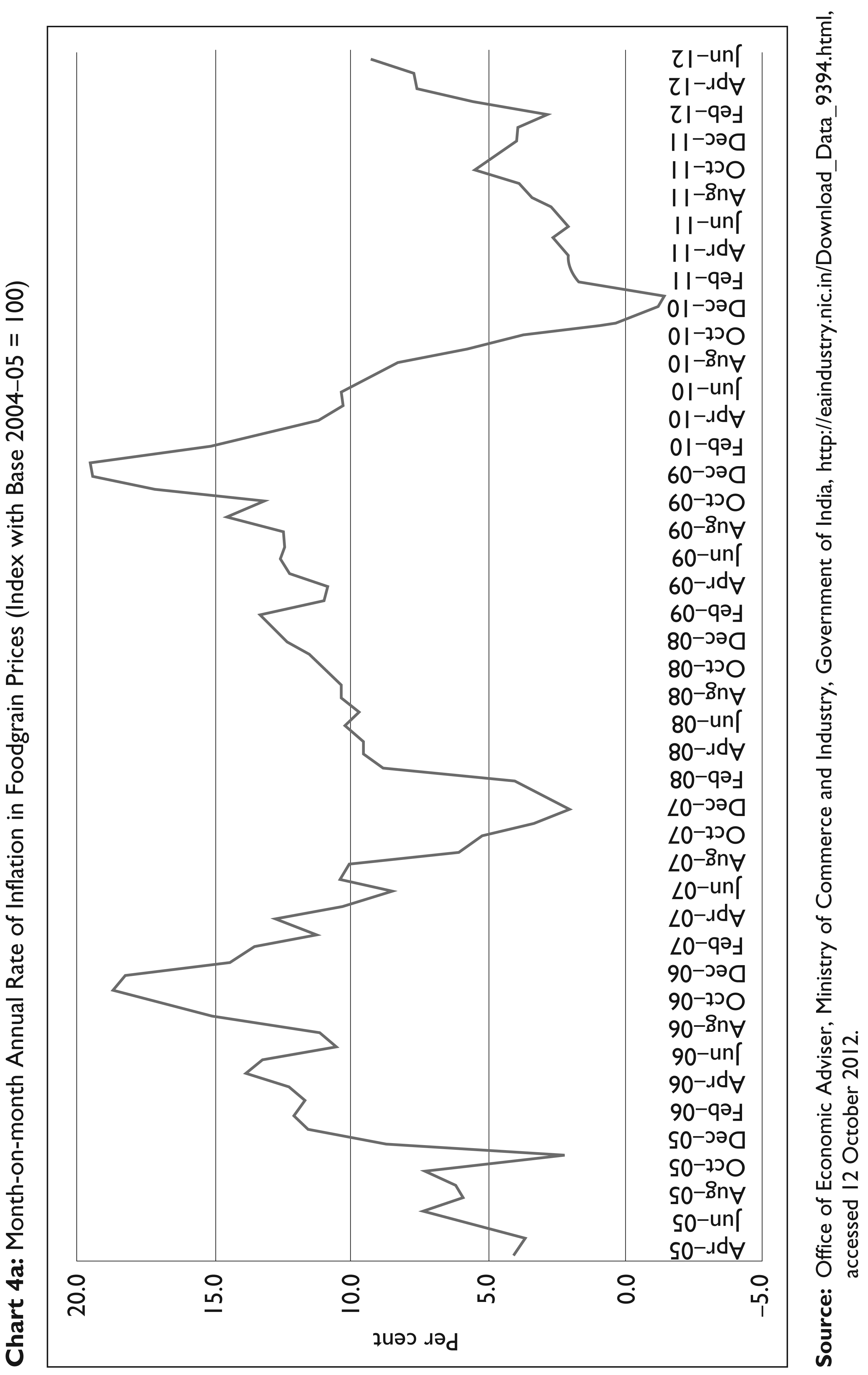

A second notable feature has been the tendency to periodic and near-persistent inflation in recent times. Over a period of two years beginning December 2007, the annualized point-to-point inflation in the prices of food articles in India, as measured by the WPI, rose from a temporal low to a peak in December 2009 (Chart 3). Through much of this period, food grain prices, too, were rising (Chart 4), as were the prices of other food articles, such as fruits and vegetables, eggs, meat, fish and milk. Furthermore, for almost a year following December 2009, the inflation rate, though declining, remained in the two-digit range. Though the inflation rate came down sharply over the next year in the case of food grains and the next two years in the case of food articles (Charts 3a and 4a), it once again recorded an increase during 2012, especially in the case of food grains.

Given the fact that India is a country in which a substantial proportion of the population consists of individuals with insecure employment, earning incomes that are not indexed to inflation and with no access to social security, the government was under pressure to rein in inflation and mitigate its adverse effects on sections at the margins of subsistence. However, despite some effort on its part and periodic assurances that inflation would abate, the problem has persisted (despite fluctuations). This persistence took the government by surprise, partly because over the first few years of the 2000s, food grain prices were relatively flat, with inflation not exceeding five per cent, until the middle of 2005. It was only subsequently that the inflation rate rose above five per cent on an annualized month-on-month basis and touched double-digit levels for a brief period between September 2006 and January 2007. In the months that followed, the rate of inflation fell from its December peak of 13.1 per cent to less than 5 per cent in September 2007. But this declining trend reversed itself in March 2008 and food price inflation rose to 10.8 per cent in December 2008 and remained at high double-digit levels until June 2010. India seemed to have returned to the situation that prevailed in the second half of the 1990s, which was characterized by high inflation and substantial volatility in food prices (Charts 3 and 4).

Month-on-month Annual Rate of Inflation in Prices of Food Articles (Index with Base 1993–94 = 100)

Month-on-month Annual Rate of Inflation in Foodgrain Prices (Index with Base 1993–94 = 100)

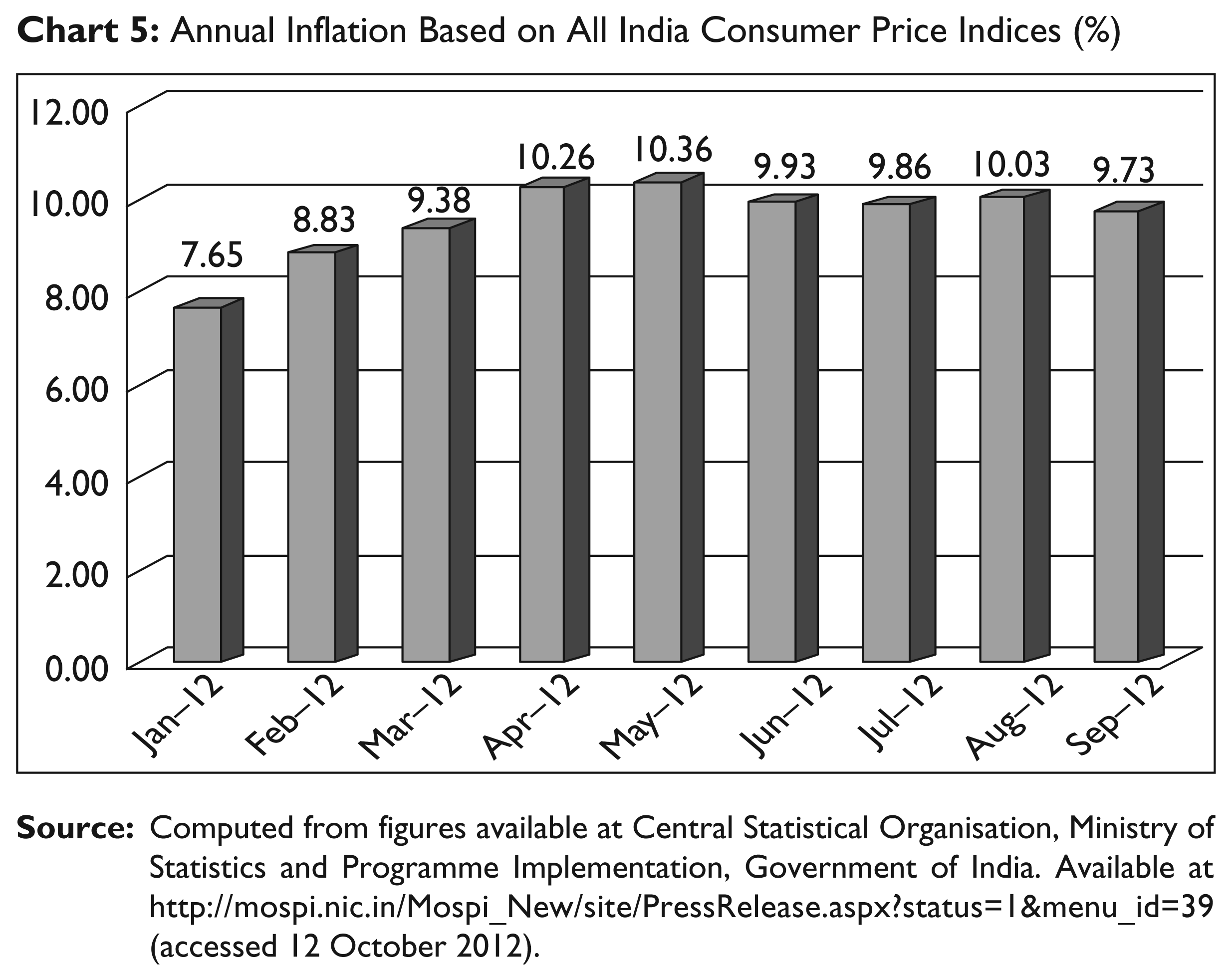

For the consumer, inflation was more damaging than indicated by trends in the WPI, which most often understate the actual inflation experienced at the retail level. Since January 2011, the Central Statistical Organization has been releasing a new monthly series of All India Consumer Price Indices (with 2010 as base), which permits an estimation of retail price inflation from January 2012. According to the recently released Consumer Price Index (CPI), the annual month-on-month rate of inflation had risen to 10.36 in May, from 7.65 per cent in January and stayed close to the 10 per cent level until September (see Chart 5).

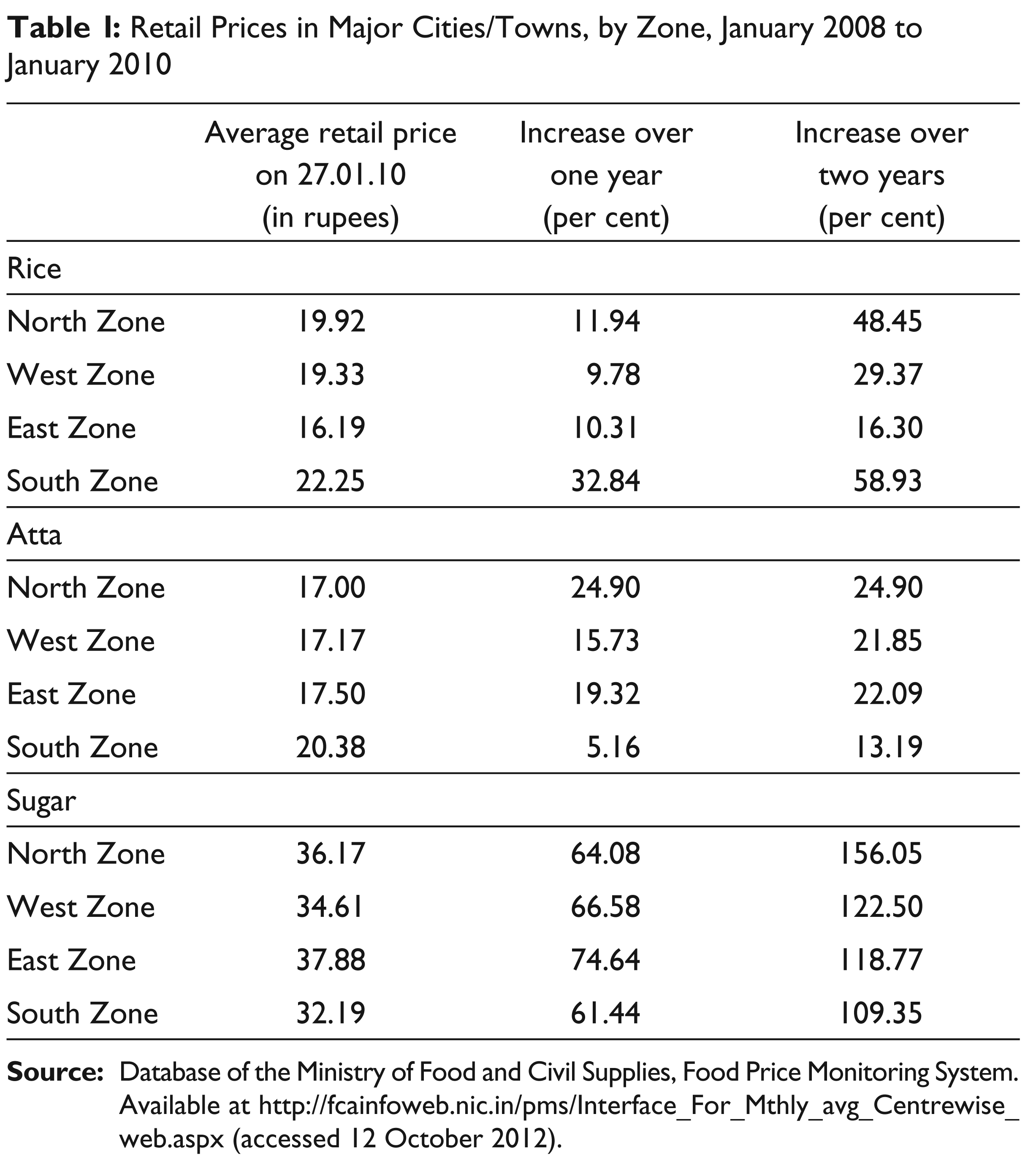

Similarly, figures collated by the Price Monitoring Cell of the Department of Consumer Affairs establish that in the case of a few commodities there is a significant difference between inflation as measured by retail prices (collected from and averaged across 18 reporting centres nationwide) and the WPI. Table 1 reports the retail price increase in the major regions, for rice, atta (wheat flour) and sugar at the end of January 2010, which was just after inflation had peaked, as measured by the WPI. It is evident that the price increase had been alarming especially over the previous two years, with rice prices increasing by nearly half in Northern cities and more than half in Southern cities. Atta prices had on average increased by around one-fifth from their level of two years ago. The sharpest increase was in sugar prices, which had more than doubled across the country. Other food items, ranging from pulses and dal to milk and vegetables, had also shown dramatic increases especially in the previous year. In sum, during the period of enhanced price volatility, the consumer has been affected even more adversely than suggested by the wholesale price figures.

Retail Prices in Major Cities/Towns, by Zone, January 2008 to January 2010

Explaining Price Trends: The Domestic Dimension

There are many reasons why food prices in India could be more upwardly flexible and more volatile than the prices of other commodities. With greater presence and effectiveness of ‘degrees of oligopoly’ in the non-agricultural sector, especially manufacturing and supplies being elastic and easily increased in the short run, because of excess capacities, agents in non-agriculture are seen as ‘price makers’, setting prices at levels that include some mark-up over costs. On the other hand, unlike in the manufacturing sector, supply from the agricultural sector, which directly or indirectly contributes much of the food consumed, tends to be less responsive in the short run to increases in demand (at any price level). Furthermore, agricultural production in most developing countries is dependent on variable natural conditions such as rainfall. A bad monsoon can limit supply and result in demand–supply imbalances that fuel inflation. The combination of inelastic supply and volatile production also makes the market for agricultural commodities, including food, prone to speculation that worsens any inflationary tendency. Thus, food prices are in substantial measure ‘demand determined’ (given short-run supplies), as compared to non-food prices that are ‘cost determined’.

This distinction is of greater relevance in countries (like most developing countries) which are characterized by a chronic ‘disproportionality’ in the rates of growth of the agricultural and non-agricultural sectors, with the former registering lower growth rates than the latter (Chakravarty 1993). Periodically, such disproportionality results in the demand for food from the non-agricultural sector being in excess of marketed supplies, triggering inflation.

As Table 2 shows, the rates of growth of non-agricultural GDP have been way ahead of that of agricultural production, especially food grains, through much of the post-Independence period in India. What is particularly remarkable is that the acceleration of non-agricultural growth during the late 1990s and early 2000s was accompanied by a decline in the rate of agricultural growth. Even during the period 2004–05 to 2009–10, though agricultural GDP had revived to 2.7 per cent, the trend rate of growth of non-agricultural GDP accelerated much more and exceeded 8 per cent. Such disproportionality is visible even when the comparison is restricted to industrial and agricultural growth. This makes for a long-term tendency for upward buoyancy in agricultural prices, including food prices.

Annual Trend Rates of Growth

However, sectoral growth rates alone do not reveal in full the exact nature and intensity of the imbalances that influence trends in food prices. This is because manufacturing, or the non-agriculture sector as a whole, is not homogenous, but is characterized by significant inequalities in the distribution of income. If growth in aggregate GDP is accompanied by a concentration of income gains in the upper income groups in these areas, whose demand for food, especially staples, would be more or less satiated, the demand for these commodities may not rise pari passu with the growth in non-agricultural GDP.

Further, given the importance of government in modern-day economies, the responsiveness of the demand for food would also be influenced by the fiscal policy stance of the state. This is because the adverse fallout of any restriction in state expenditure or measures of austerity aimed at reducing public debt tends to affect disproportionately the poorer sections of the population. They often involve contraction of programmes that generate mass employment. This reins in incomes that would be largely allocated to food. They require imposing user charges and raising tariffs in services like health and education, utilities like power and transport and commodities such as fuel. Since there are limits to which consumption of such services or goods can be reduced, the increases in their prices would result in an enforced squeeze on food consumption. Combined with the concentration of income increases in the hands of those whose demand for food is satiated, these effects of a deflationary fiscal stance can significantly reduce the incremental demand for food associated with increases in income. Thus, any level of imbalance generated by higher rates of growth of the non-food relative to the food sectors would be associated with a lower imbalance in the demand and supply of food and a lower level of food price inflation.

Finally, efforts to curb the budget deficit of the government reduce the direct demand of the government for the goods and services it consumes or in which it invests. If in addition, as part of reform, the government cuts effective direct tax rates and reduces the indirect tax burden to incentivize private investment, the tax-to-GDP ratio could decline. A smaller dose of borrowing when tax revenues are being reined in would substantially reduce the stimulus to growth offered by government expenditure. A slow down in non-agricultural growth would be the result, which would directly reduce the imbalance between agricultural and non-agricultural growth rates and therefore the rate of food price inflation.

A feature of neoliberal reform is the adoption of a deflationary fiscal stance. This could have partly contributed to the 2001–07 moderation in food price inflation. It could be asked why this did not apply in the 1990s to the same degree, since reforms began early in that decade. The reason is that the policy of curtailing expenditures and the deficit was implemented with a lag and despite its stated objective, the government in India could not rein in the deficit during much of the 1990s. There were only four years in the period after 1990–91, starting in 2004–05, in which the fiscal deficit at the Centre was below four per cent of GDP (GoI 2012: 42, Table 4.3). Thus, it was only later that this objective of reform began to be implemented successfully with attendant consequences.

This ‘deflationary’ fiscal stance of the government is, however, only one factor explaining muted disproportionality post-liberalization, though an important one. Another set of factors explaining this tendency was the change in the pattern of growth itself. The pattern of growth under an open economic regime is such that the responsiveness of employment growth to the growth in output tends to decline. This is because (Patnaik 2006): (a) tastes and preferences of the elite in developing countries are influenced by the ‘demonstration effect’ of lifestyles in the developed countries, so that new products and processes introduced in the latter very quickly find their way to the developing countries when their economies are open to cater to their demand; and (b) technological progress in the form of new products and processes in the developed countries is inevitably associated with an increase in labour productivity. Hence, after trade liberalization, labour productivity growth in developing countries is exogenously given and tends to be higher than prior to trade liberalization, leading to a growing divergence between output and employment growth.

Needless to say, this argument is not a complete explanation of this divergence in the case of India, because of the dominance of services in total growth. However, the lack of correspondence between output and employment growth is true here as well. Tertiary sector employment in 2004–05 amounted to only 25 per cent of the workforce, despite the fact that close to 50 per cent of GDP came from this sector. Moreover, between 1999–2000 and 2004–05, employment in the tertiary sector increased by only 22 per cent, whereas GDP at constant prices contributed by the service sector expanded by 44 per cent. 1

When these features of the pattern of growth are recognized and their consequences added to the effects of a ‘deflationary’ fiscal stance, it is possible to understand why the tendency towards disproportionality tends to get muted. But that raises the second aspect of the puzzle noted earlier: why have we witnessed a reversal after the middle of 2000s, leading to the return of disproportionality and therefore a surge in food price inflation for a prolonged period.

It must be noted here that it was after 2003–04 that India moved from an annual six per cent GDP growth trajectory, to a growth rate in the eight to nine per cent range, marking its membership among the successful emerging market countries. This substantial step up in growth rates for a considerable period of time must have had implications for the direct and indirect demand for food, providing the basis for a reassertion of the demand–supply imbalance. That this may have been the case is suggested by the fact that the period of relatively high food inflation came at the end of the period of high GDP growth, with much of that growth being attributable to sectors other than agriculture, especially services. The surge in growth rates was partly driven by a boom in credit-financed private investment in housing and an expansion of credit-financed private purchases of automobiles and durables. This substitution of credit-financed private expenditure for credit-financed public expenditure allowed growth to accelerate despite fiscal conservatism, resulting in the emergence of demand–supply imbalances and resurgence of inflation.

Further, this was a period when agricultural performance was indifferent or poor. As some economists have noted, in the period of reforms, when the Indian economy had ostensibly turned dynamic, as suggested by the GDP growth figures, agriculture continued to be neglected, resulting in a silent agricultural crisis. That neglect had many components. Public investment in agriculture has been in long-term decline. The extension system aimed at reaching new agricultural technologies and information on better farming practices to India’s agriculturists has either been dismantled or allowed to degenerate. Agricultural research, which served India well during the Green Revolution years, has been given inadequate attention and resources. And, a ‘reform’-induced combination of trade liberalization and domestic deregulation has raised costs while inadequately compensating farmers with remunerative prices, damaging the viability of crop production and increasing farmer exposure to income volatility.

Not surprisingly, the country is experiencing a deep-seated food crisis that is concealed by claims of self-sufficiency. The per capita availability of food in a country where much of the population is below the level of nutritional adequacy has been low and declining (Patnaik 2004). This has not proved to be much of a problem, because low incomes and purchasing power among a significant section of the population kept demand in check as well. But the indirect demand for grain on the part of the well-to-do has increased. The net result is a tendency for the re-emergence of supply–demand imbalances. Hence, with low levels of per capita availability persisting, food prices finally turned buoyant.

The Support Price Wedge

The influence of these fundamentals on food prices in India has, however, been moderated by policy, which is that of setting Minimum Support Prices (MSP) for selected agricultural commodities. The adoption of this measure of price intervention was part of the strategy to raise food production through the Green Revolution. An essential component of the Green Revolution strategy was the decision to incentivize production by setting a ‘remunerative’ cost-plus floor to certain agricultural prices. The MSP with respect to the major 24 crops, including food grains, is set by the Commission for Agricultural Costs and Prices (CACP) to ensure a remunerative, cost-plus price for the producer, while the government guarantees purchases at these prices of surpluses delivered to it during the procurement season. The farmers, on the other hand, can either sell their produce to government agencies at the MSP, or in the open market, depending on which is more advantageous to them. This does mean that (a) the MSP sets a floor to the open market price; and (b) that the flow of grain to the government’s warehouses would vary with changes in the levels of production and supply, which influences the level of open market prices relative to the MSP floor. (Thus the demand–supply imbalance does, in some ultimate sense, have an effect on food price trends).

The operation of these factors results often in the accumulation of stocks with the government in excess of buffer stocking norms, especially in normal or good monsoon years. To boot, uneven agricultural growth, engendered by historically given inter-regional variations, on the one hand, and the nature of the Green Revolution strategy, on the other, results in yield increases and food surpluses being concentrated in a few states in the country. The challenge this set to the government was that of moving food from surplus to deficit (and often poor) regions and ensuring the effective demand required to absorb these surpluses. This necessitated the sale of a part of that stock at lower and affordable prices through the PDS to sustain demand. As a result, the government had to provide a subsidy to cover the difference between, on the one hand, the cost of acquiring these food grains, carrying them and transporting them to urban areas and deficit states and, on the other, the lower price at which it offered this food through the PDS to ensure off-take. Thus, though the food subsidy is presented as being largely an effort to reach affordable food to the consumer, it was actually also the outcome of the strategy of enhancing agricultural production by offering farmers a ‘package’ of hybrid seeds, inputs, credit and prices. The food subsidy outlay on the government’s budget reflected the nature of the agricultural growth strategy and the cost of it involves.

However, inasmuch as the MSP set an ‘administered’ cost-plus floor to agricultural prices, it reduced or nullified the asymmetry in which manufactured goods prices were cost-determined and agricultural prices were demand-determined. In the context of our discussion, it muted the influence of demand–supply balances on trends in the prices of various food items. However, since as mentioned earlier the success of procurement itself depended on the level of supplies in the market, demand–supply imbalances continued to matter. Moreover, as the government opted for raising the issue prices of food provided through the public distribution system in order to reduce the subsidy bill as part of fiscal reform, off-take from the PDS tended to decline. The result was that output procured by the government at the MSP remained in government warehouses (especially in good monsoon years), often rotted for lack of adequate space and was even exported at low prices to dispose of embarrassingly large stocks. This pre-emption and withdrawal of supplies from the domestic market, increased the relative role of demand in influencing prices.

Explaining Price Trends: The International Dimension

However, it is to be expected that as liberalization dilutes the boundaries separating the domestic and the international market, the role of domestic demand-supply imbalances in influencing prices would decline, with domestic prices and price relatives approaching international levels. But in this case, too, there were factors driving a wedge and sustaining a difference between domestic and international price levels and trends. While liberalization enhances the cross-border transmission of those trends, other elements of the policy environment influence the intensity of transmission of price signals leading to substantial variations across commodities. In particular, given the role of the MSP policy in the case of food products like wheat and rice and the tendency for the government to use trade policy to stabilize domestic prices of ‘sensitive’ products like food (for example, by resorting to imports and/or imposing export bans when market prices rule high), it is likely that the correlation of domestic and international prices would be lower in the case of food articles than in the case of commercial crops.

But net effects are ambiguous and, even in the case of specific commodities or groups of commodities like food grains, different analysts arrive at diverging results on the issue of the relationship between international and domestic price levels and trends. Not insignificant among the reasons for this divergence is a statistical factor: the international and domestic reference prices chosen to make the comparison. For example, a recent study (Tripathi 2010) that attempted to assess India’s trade competitiveness in a range of agricultural commodities found that in the case of wheat over the period 1981–2005, barring a few years, the f.o.b.(Free on board) price of domestic produce based on the MSP was higher than the f.o.b. price of US wheat of similar quality. That is, while transport costs and trade taxes restore the competitiveness of Indian wheat, India was not competitive in export markets involving similar transport costs for American and Indian producers. Government intervention was managing to sustain this wedge between the two prices, insulating the domestic price from international movements.

However, a study by the Finance Ministry (Dasgupta et al. 2011: 9) found that international price movements did influence domestic price trends, though the impact was relatively weak. Moreover, the effect of physical export bans on domestic prices was also contrary to expectations. The study found that the direction of causality was such that, while export bans are ‘applied and persistent when domestic wheat prices are high’, they do not appear to have any ‘independent effect in lowering domestic wheat prices relative to international prices’.

Finally, an earlier study by the Reserve Bank of India (Rajmal and Misra 2009: 7) pointed to a significant association between trends in international and domestic prices of agricultural products, though the pass-through was only partial and varied across commodities. To quote:

[t]he international food price indices increased by around 15 per cent during 2007 and further by 23 per cent in 2008. It is observed that food prices in India have generally been moving in tandem with the international prices, but at a significantly lower pace when compared with international food prices, thus, reflecting a less than complete pass-through. In India, food prices increased, on an annual average basis, by about 6–7 percent during the period 2006–2008 (11–23 percent at the world level). Interestingly, while world food price index has shown a sharp fall in 2009, domestic food articles price index has risen, albeit, slowly as compared to the previous years reflecting the role of domestic factors in influencing prices.

Overall, while the cross-border transmission of the influence of trends in international food prices has played a role, country-specific factors seem to be more responsible for food price inflation in India. As noted previously, obvious reasons for this are the adoption of the MSP (which set a domestic cost-plus floor to domestic prices) and of trade policy measures, such as quantitative restrictions on imports and exports and trade tariffs that insulate domestic prices from international trends. However, international factors can still influence domestic food prices from the cost side. If for example, domestic prices of petrol, oil and lubricants (POL) are calibrated to reflect international fuel costs, any increase in the international prices of oil will drive up domestic oil prices and affect in myriad ways (input costs, wage costs, transportation costs, etc.) the cost of production of food in India. Furthermore, to the extent that there is a relationship between international food prices and international fuel costs, this would lead to some relationship between international and domestic food prices as well. Since liberalization in different sectors tends to close the distance between domestic and international prices (before accounting for transport costs), the influence from the cost side of international price trends on domestic prices, even in the case of food, are likely to rise in the post-liberalization era. This tendency will intensify if the process of setting the MSP is itself influenced by trends in international prices.

The Role of Reform

The continuous shift in the commodities on which recent inflation has been focused suggests that multiple factors—imported inflation, flagging supplies, administered price increases, cost push and speculation—have combined to keep high inflation going. If there is an element common to them, it is that they are partly the outcomes of economic reform. Consider the many links between neoliberal reform and inflation. India’s vulnerability to the effects of changes in international prices has increased with trade liberalization. The disproportionality between agriculture and non-agriculture has increased because of aspects of the post-reform strategy of growth leading to increased demand–supply imbalances. Even if this has been partly moderated by the MSP policy, the MSP itself has been influenced by cost increases resulting from reform-induced increases in administered prices and cuts in input subsidies. The effort to reduce subsidies has resulted in a continuous increase in the prices of commodities such as petroleum and fertilizer whose prices are administered. Imbalances between demand and supply of primary products are accentuated by the government’s reluctance to release additional food through the public distribution system in order to curb subsidies. The list is long and almost endless. What the recent inflation experience suggests is that while the earlier regime of intervention and regulation is criticized for generating a high-cost (and, therefore, a high price) economy, the processes of liberalization and deregulation are the ones that lead to a high inflation economy.

Further, while speculation has always played a role in the food market, because of the uncertainty that demand–supply imbalances create, that role has increased significantly after liberalization. In the past, large farmers and/or traders used to acquire and retain stocks in the expectation that prices would rise. This often ensured that such expectations were realized. However, in recent times the transition from older forms of speculation and from forward to futures trading has transformed the nature and enhanced the role of speculation.

Forward trading has a long history in the country, but it has never been a matter of much public concern. Until recently, that is. When searching for explanations for the increase in the prices of food some time ago, some observers turned their attention to the massive increase in forward and futures trading in commodities. What emerged was revealing.

Volumes on the National Commodity Exchange, which started trading futures contracts in 2003, reached US$378 billion in the year ended 31 March 2012. That was more than the US$139 billion worth of shares traded on the Mumbai stock exchange in the same period. Forward and futures trading had been promoted on the ground that it helped traders deal with market uncertainty, by hedging their transactions and stabilized prices for the final producers. However, the surge in futures trading could not be explained by pure hedging requirements and obviously reflects an increase in speculative activity.

In 2006, political leaders saw in this speculation an explanation for the spike in food prices. Their view was endorsed by Congress President Sonia Gandhi, who reportedly told a meeting of Congress Parliamentary Party members in early August 2006,

2

that in a meeting she and the Prime Minister had with chief ministers, they were:

[u]nanimous that forward trading, particularly in wheat, has had an adverse impact and called for a more effective regulatory framework to deal with speculation.

In the event, the rapid increase in futures trades along with signs of inflation in food prices led to the ban on futures trading in tur, urad, rice and wheat, in January and February 2007. A year later, in May 2008, it suspended futures trading in soybean oil, potatoes, rubber and chickpeas. The latter ban was revoked in November 2008 and the ban on wheat futures trading was lifted in 2009, but the ban on rice futures trading continues. 3

Futures Trading and Inflation

Forward contracts have historically been a feature of commodity markets, partly because supplies come into the market at specified points in time, such as the harvest season, while the demands of actual users of many commodities is continuous across the year. Producers of commodities have to make production decisions based on expectations of the price that they would receive when the output arrives and purchasers of commodities as inputs or final goods must make judgements of the availability and cost of the commodity at different points of time during the year. To guard against price volatility and uncertainty in production and availability, sellers and buyers often entered into forward contracts, specifying the quantity, quality and price of the commodity they would deliver for sale or acquire for purchase at a pre-decided date in the future.

It should be clear that forward contracts are means of hedging against the risk of price volatility or uncertainty of supply. But hedgers cannot function without the presence of speculators. If the market is restricted to hedgers, who are actual producers or users of the commodity, the volume of many contracts could be so low that on some days a trade cannot occur, because a buyer cannot find a seller, or vice versa. This is where the speculators step in. They buy or sell in forward trades, not with the intention of actually making or taking delivery, but with the idea of transferring the concerned contract to an actual producer or user at a profit. They can therefore, buy and sell a large number of contracts, enabling the hedger to transfer risk with ease by injecting liquidity into the system. But the moment speculation begins there is the risk that prices could be manipulated to move consistently in one direction for significant periods of time, inflicting losses on some and generating gains for the others.

Forward contracts, however, are cumbersome. It requires intending sellers of specific quantities of specific quality at specified times to find the appropriate number of buyers. This entails costs of search and inspection. Further, since there is no centralized market or exchange where the contract is drawn up, prices tend to vary and there is uncertainty about delivery. It is for this reason that futures contracts were evolved.

Futures contracts differ from forward contracts in important respects. 4 Futures contracts are standardized contracts to buy or sell a standard quantity of a standard quality of a commodity. These are traded in exchanges, through brokers, with no need for the buyer and seller to meet and negotiate. An important feature is that a contract need not be settled by actual delivery. It can be matched by an offsetting contract taken by the buyer or seller and the two can be squared at any point at some gain or loss. The administrators of the commodities exchanges guarantee that contracts would be settled and require traders to pay up margins to cover on-going losses, if any, to secure the viability of the exchange. To avoid paying margins, traders can buy an option to offer or acquire a contract at some specified future date. If the option is not exercised, because price movements are contrary to expectations, the loss is restricted to the premium paid to hold the option and the transaction costs of acquiring it.

The existence of futures contracts allows sellers or buyers to hedge against risk by buying offsetting futures contracts that would protect them against losses if the market moves against them. But hedging is not the sole driver of futures markets. The emergence of futures contracts and derivatives such as options in commodity markets, allows the implicit trade in commodities to be many multiples of the explicit trade. The volume of implicit trade is only restricted by the extent of liquidity in the market, whereas the volume of explicit trade is limited by the actual availability of the commodity from different sources. If liquidity in the market fed by speculation is high, prices in futures markets can move in ways that could influence the spot prices at which the commodity is actually sold.

With the liberalization of futures markets in the 2000s (following the passage of the Commodity Futures Modernization Act in 2000 in the United States), investors encountering increased uncertainty or suffering losses in equity markets, turned to commodity futures an ‘alternative asset class’. This brought into the market a range of ‘Index speculators’, consisting of asset management firms, hedge funds, pension funds and other institutional investors, who invest in index futures or derivatives built on a futures index like the S&P GSCI Index. The index captures returns obtaining in commodity futures markets.

Index speculators enter the market to buy a hedge against potential losses from investments in other markets, but when their entry results in a rise in prices of commodity futures they stay and expand their positions in the hope of speculative returns in this market. Thus, the demand for commodity futures from index speculators keeps rising. The additional catch is that index futures are long-only investments, where investors buy and choose to roll over but never sell. The net result is the volume of such instruments and the commodity futures prices underlying them tend to continuously increase. This is why the futures market is subject to transactions that are many multiples of the value of the commodities concerned or the volume of transactions in spot markets. To the extent that the futures prices serve as some signal for spot prices, there would be a disjunction between actual spot prices and those that would prevail if only physical supply–demand balances determined the spot price. Speculation in futures markets begins to influence prices in spot markets.

Given the logical and physical separation of spot and futures markets and the fact that the latter does not involve any physical delivery of the underlying commodities, it is indeed difficult to establish the kinds and magnitudes of the influence of futures on spot markets. But the suspicion that futures do influence spot prices is partly corroborated by the fact that whenever inflation is high in certain sensitive commodity markets (such as food), regulators who may have themselves liberalized the market opt for controls on futures trading, as happened in India.

In India, the process of liberalization began after the government set up a Committee under the Chairmanship of K.N. Kabra in 1993, to examine the role of futures trading in the context of liberalization and globalization. The Kabra Committee, while cautious, recommended allowing futures trading in 17 selected commodity groups. It also recommended strengthening of the Forward Markets Commission (FMC) and amendments to Forward Contracts (Regulation) Act, 1952.

However, this cautious approach was dropped in 1998, which saw the adoption of a major reform package involving the FMC and the Exchanges, spurred by a World Bank-funded grant. The reform included the introduction of futures trading in edible oils, oilseeds and their cakes, which was a turning point in the development of commodity futures contracts in India. The National Agricultural Policy announced by the government in 1999 declared that the government will enlarge the coverage of the futures market to minimize the wide fluctuations in commodity prices, as also for hedging their risk. In the Budget for 2002–03, the Finance Minister announced the expansion of futures and forward trading to cover all agricultural commodities. These initiatives paved the way for speculative price increases.

The Response to Inflation

Given the set of factors that combine to drive prices upwards, it is not surprising that India has over the last decade entered a phase where food inflation is an almost persistent problem. On the other hand, given the government’s commitment to liberalization and deregulation, it finds the task of combating inflation more difficult to undertake. A central tendency is the growing inability of the government to use its procurement and distribution mechanism as a means of controlling the domestic prices of cereals and pulses. This inability stems from three sources. The first is the failure to ensure that marketed surpluses of these commodities grow at a fast enough pace to match consumption and buffer stocking requirements in years when demand is buoyant. The second is the liberalization of trade in many of these commodities that has seen the entry of private traders, including large transnational buyers, who in years of production shortfalls tend to corner stocks and limit procurement by government agencies like the Food Corporation of India. And the third is the tendency to both permit exports and calibrate domestic procurement prices to track international prices so that in periods when international prices are rising, so are domestic prices.

Furthermore, poor distribution, growing concentration in the market and inadequate public involvement have all been crucial in allowing food prices to rise in this appalling manner. Successive governments at the Centre have been reducing the scope of the public food distribution system and for some time now, even in the face of significant increases in prices, the central government has been delaying the allocation of food grain for the Above Poverty Line population to the states. This has prevented the public distribution system from becoming a viable alternative for consumers and impeding private speculation and hoarding. In addition, allowing corporates (both domestic and foreign companies) to enter the market for grains and other food items has led to some increase in the concentration of distribution. This has not been adequately studied, but it has many adverse implications, including the fact that farmers will benefit less from periods of high prices even as consumers suffer, because the benefit will be garnered by middlemen.

Not surprisingly, the government appears to have given up on the task of curbing inflation and is either hoping that it would just go away or that people would not notice. The common man, it is hoped, would learn to live with the phenomenon and somehow adjust. This is reflected in the changing response to persisting inflation. Initially, government spokespersons declared inflation to be a temporary aberration that would fade away. Then it was attributed to non-addressable international factors, or just plain statistics.

But since these arguments could not be convincingly advanced for too long, the tendency more recently has been to recognize the problem, express concern and then declare that it was the inevitable outcome of high growth that can be tackled only in the medium or long term. The argument seems to run as follows. With incomes rising rapidly, demand for a number of commodities is growing, but supply is either not keeping pace or can, in some cases, only adjust over the medium term. Inflation, it is suggested, is a result of this frictional imbalance. It is a cost that has to be paid for the good life. And only the cussed would point out that neither does everybody bear the cost nor do all benefit from the good life.

The one organization that has, hitherto, chosen to respond to inflation is the Reserve Bank of India (RBI). However, it has relied largely on a single instrument. It expects interest rate increases to moderate investment demand, curb debt-financed housing purchases and consumption and rein in speculation financed with credit. In fact, it has been aggressive on the rate increase front over the last couple of years, hiking it by far more than the market expected. Thus, the repo rate was hiked through a series of steps by more than three percentage points, before being marginally reduced when there were signs that growth was slowing. Clearly, however, the RBI’s heavy reliance on this instrument did not help matters. Prices continued to rise and inflation persisted at high levels for quite some time.

The Gainers and Losers

The inadequate response to inflation is partly a reflection of the unwillingness of the government and the central bank to rethink the policies of neoliberal reform that underlie the rise in both costs and prices. That failure is partly ignored because there are strong interests gaining from the increase in prices. In the past, the understanding was that increases in food prices benefited sections in the agricultural sector by shifting the terms of trade in favour of agriculture and the rural areas. Needless to say, not all sections benefited.

There have been many analyses of the distribution of marketed surpluses across farmers of different size and class characteristics. 5 An early study by Dharm Narain (1961) had found that the bulk of the marketable surplus was concentrated in the hands of large landholders, though he argued that the distribution of marketed surplus as a ratio of output across holdings of different size classes was ‘U-shaped’ because of forms of distress sales of crops by small farmers. This was contested with evidence for 1960–61 by Utsa Patnaik who found a direct relationship between the marketed surplus ratio and the class of farmers. Later, others like M.V. Nadkarni (1980) found that, in the region studied, farms with landholdings of 10 acres or more accounted for 60 per cent of the marketed surplus of wheat and as much as 80 per cent of the marketed surplus of wheat, jowar and bajra combined. At the other end of the spectrum, small farmers, too, were exposed to the market by selling and buying significant quantities of food. Two factors are responsible for this kind of market engagement. One is that some small farmers sell superior varieties of food grains and buy inferior varieties to sustain consumption. The other is that marginal farmers are often required to sell their output at relatively low prices immediately after the harvest to cover cash expenses and commitments and buy food at higher prices in the lean season.

Given this distribution of the marketed surplus and the tendency towards net purchases of food among smaller farmers, it is to be expected that the benefits derived from a rise in food prices would be unevenly distributed across those engaged in agriculture. While large farmers (who most often are also grain traders) would benefit because they produce to sell and market a larger share of their produce, smaller farmers would lose because they are net purchasers of food and tend to sell when prices are low and buy when prices are high. Agricultural workers, like wage workers and fixed income earners in urban areas, would, of course, lose. It is only those sections in urban areas whose incomes are indexed to prices, or are able to adjust the prices and revenues they receive to cover for the increase in the prices of the food they consume, who would be untouched.

Trading Margins

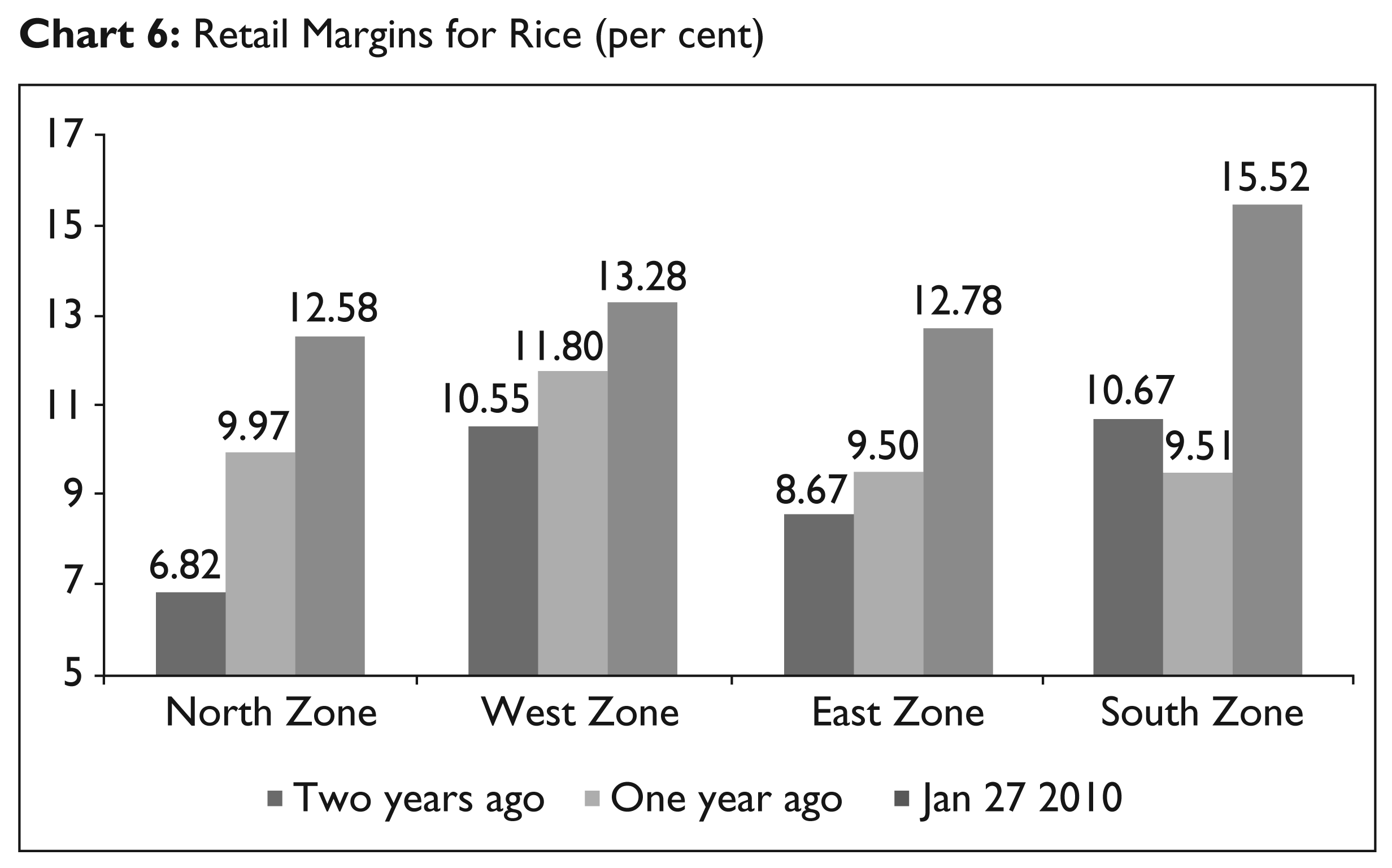

Over time, even the distinction between agriculture and non-agriculture and rural and urban areas, has been found inadequate when assessing the gainers and losers from food price increases. This is because of the growing separation of the trade from production and the rising share of trading margins in the retail price of food. This tendency is reflected in the first instance in a widening of the gap between farm gate and wholesale prices, noticed in individual studies (Agarwal 1986; Kurien 1981). Unfortunately, adequately collated secondary data is not available to assess these trends. But a similar story is evident from the gap between wholesale and retail prices. In rice, for example, by early 2010, the gap between average wholesale and retail prices had widened considerably—even doubled—when analyzed over the previous two years across the four major zones of the country, as shown in Chart 6. In wheat (Chart 7), the pattern is more uneven but the retail margins are very large indeed, as expressed by the difference between the wholesale price of wheat and the retail price of atta (which is the most basic first stage of processing).

Retail Margins for Rice (per cent)

Thus, there appear to be forces allowing for marketing margins—at both wholesale and retail levels—to increase. A corollary is that the direct producers, the farmers, do not get the benefit of the rising prices which consumers in both rural and urban areas are forced to pay. The factors behind these increasing retail margins need to be studied in much more detail. While the role of supply shortfalls in particular years cannot be ruled out, the tendency has been marked even when production shortfalls are not the source.

In addition to this, there is also initial evidence that there has been a process of concentration of crop distribution, as more and more corporate entities get involved in this activity. Such companies are both national and multinational. On the basis of international experience, their involvement in food distribution initially tends to bring down marketing margins and then leads to their increase as concentration grows. This may have been the case in certain Indian markets and is an area that clearly merits further examination.

Many people have argued, convincingly, that increased and more stable food production is the key to food security in the country. This is certainly true and it calls for concerted public action directed at agriculture, on the basis of the many recommendations that have already been made by the Farmers’ Commission and other advisory bodies. But another very important element cannot be ignored: food distribution. Here, too, the recent trends make it evident that an efficiently functioning and widespread public system for distributing essential food items is important to prevent retail margins from rising. It is clear that emergency measures are required to strengthen public food distribution, in addition to medium term policies to improve domestic food supply. A properly funded, efficiently functioning and accountable system of public delivery of food items through a network of fair price shops and co-operatives is the best and most cost-effective way of limiting increases in food prices and ensuring that every citizen has access to enough food.

Impact on the Consumer

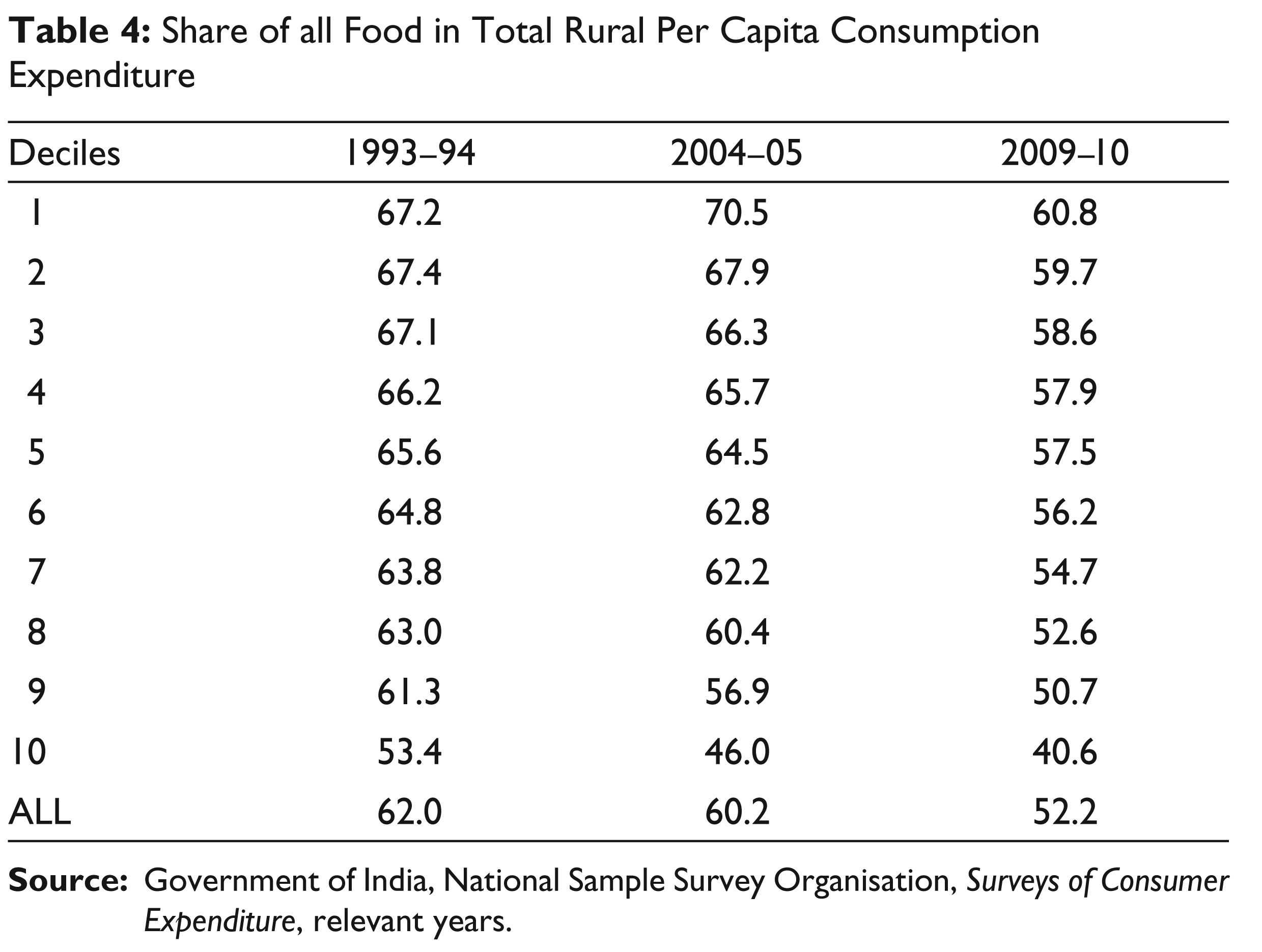

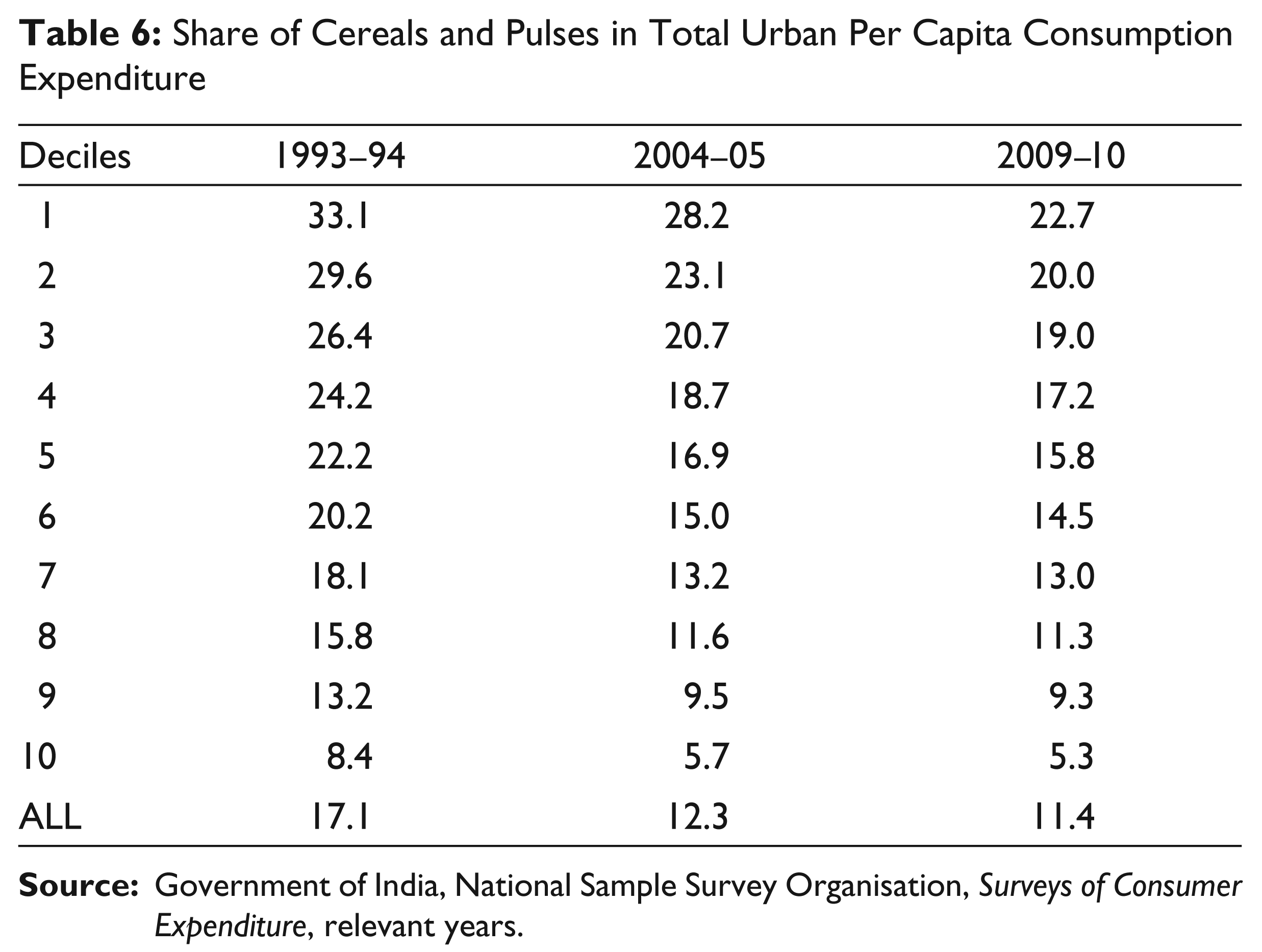

It is a truism that a consumer qua consumer would be adversely affected by any increase in food prices. However, different consumers (rich and poor) would be affected differentially. As Tables 3 and 4 show, across the three National Sample Surveys on consumer expenditure patterns relating to 1993–94, 2004–05 and 2009–10 (based on the mixed reference period), the share of total monthly per capita expenditures devoted to cereals and pulses falls quite sharply as we move from the lowest to the high per capita expenditure deciles. The decline in the case of all food articles is (as expected) less sharp, though the decline here, too, is significant. This points to the well-known fact that food expenditures (especially that on staples) constitutes a much larger proportion of total expenditure in the case of the poor. Thus food price inflation, as noted earlier, would substantially erode their real expenditures and therefore their access to nutrition.

Share of Cereals and Pulses in Total Rural Per Capita Consumption Expenditure

Share of all Food in Total Rural Per Capita Consumption Expenditure

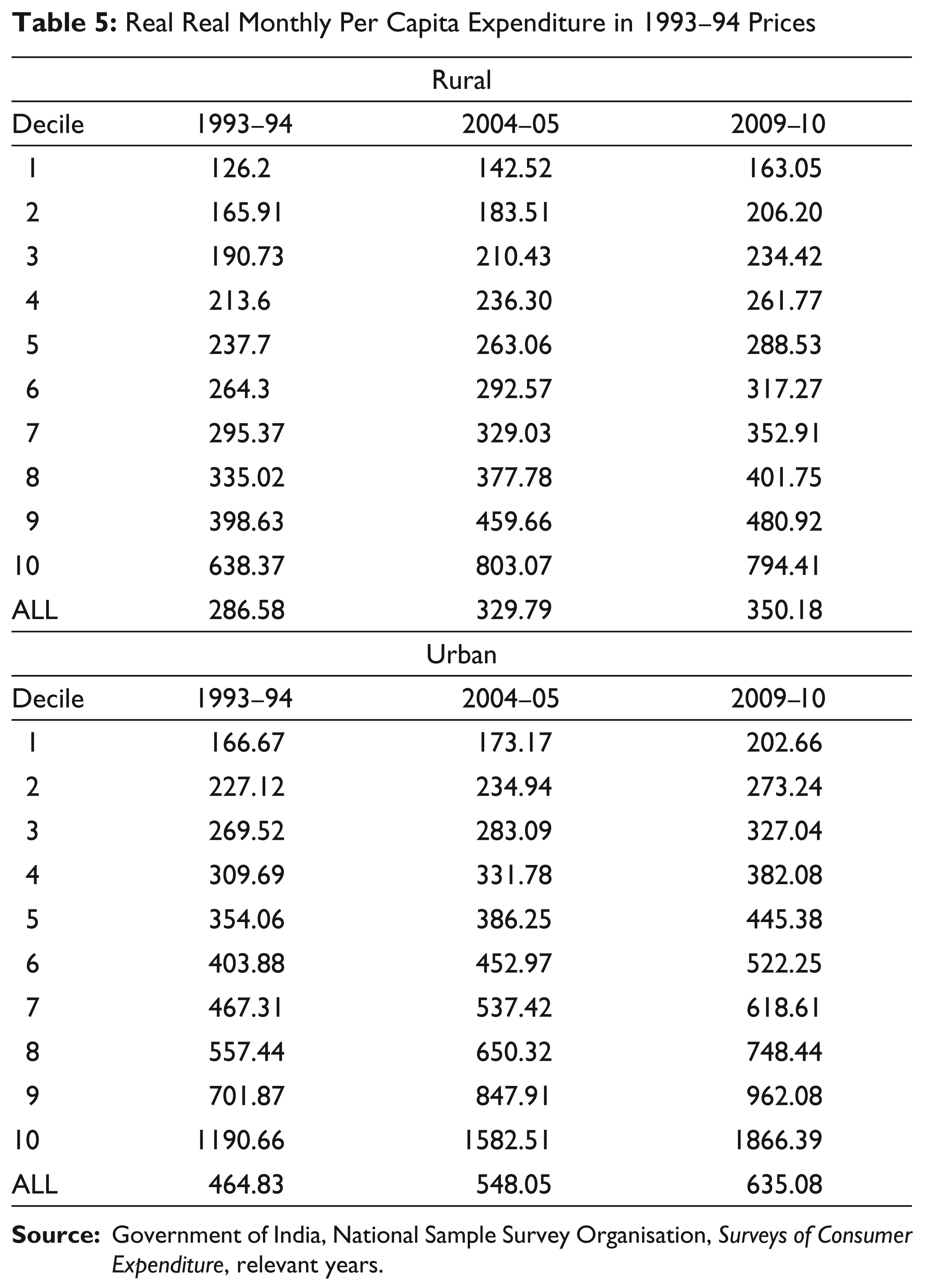

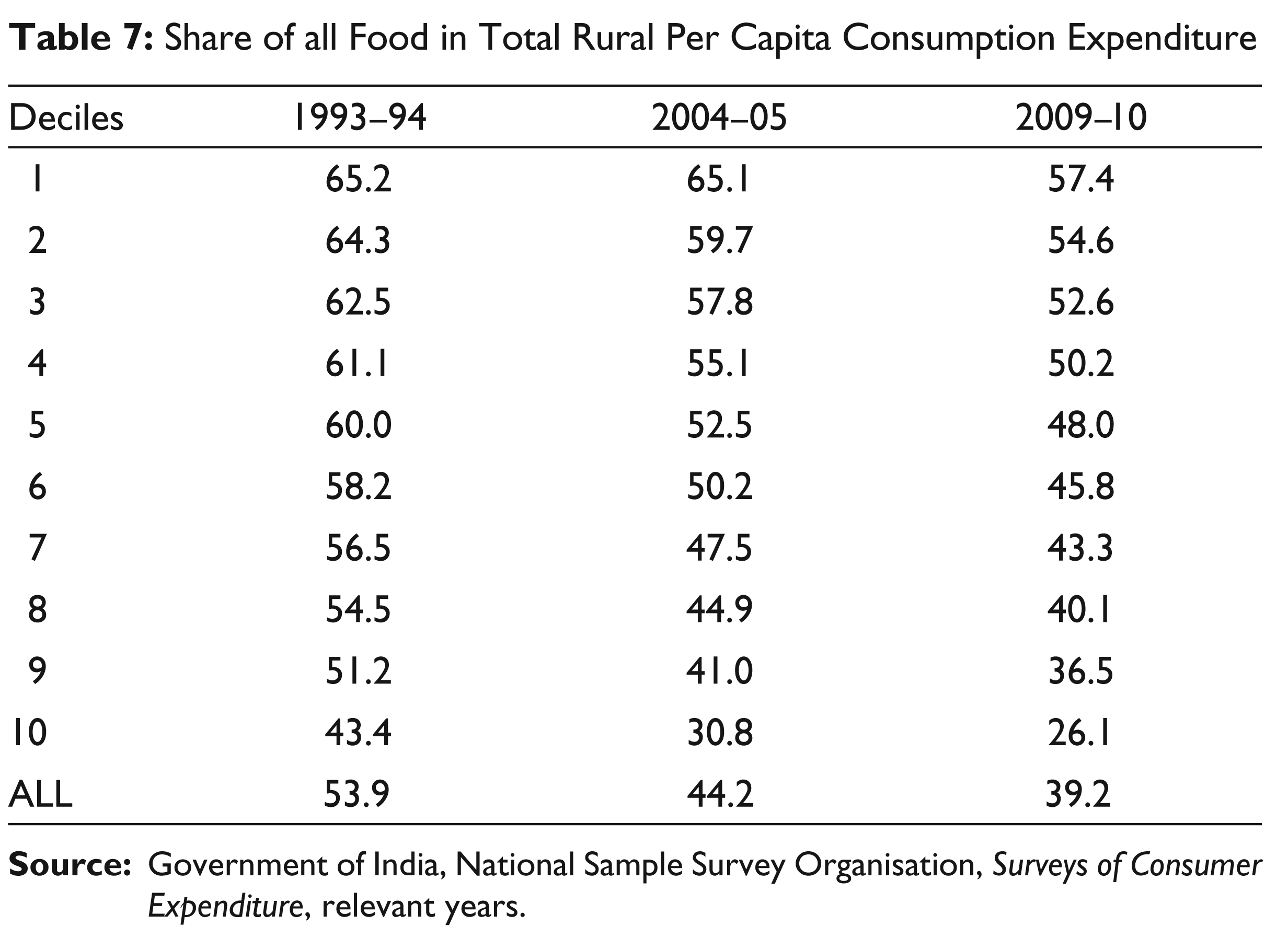

However, there is a larger issue involved here. As Table 5 shows, both in rural and urban areas real monthly per capita expenditure (computed by deflating nominal values by the consumer price indices for agricultural labourers and industrial workers, respectively) has risen across these three years in all expenditure deciles. Yet, as Tables 6 and 7 show, the consumption of cereals and pulses and of all food articles has declined in real value, or stagnated across time periods in some of the poorer expenditure groups. This is partly reflective of the tendencies noted earlier of a loss of access to common property resources, or of a need to rely on privately delivered services (for health and education), which have necessitated the diversion of a larger amount of expenditure to these items, adversely affecting the consumption of food by the poor. In other words, as and when it occurs, the adverse effect of food price inflation would be felt on top of this underlying trend, with damaging impacts on the poor who are already under severe strain.

Real Real Monthly Per Capita Expenditure in 1993–94 Prices

Share of Cereals and Pulses in Total Urban Per Capita Consumption Expenditure

Share of all Food in Total Rural Per Capita Consumption Expenditure

Thus, it is not surprising that questions of food security and the right to food have become such urgent political and social issues in India today. Rapid aggregate income growth over the past two decades has not addressed the basic issue of ensuring the food security of the population. Instead, nutrition indicators have stagnated and per capita calorie consumption has actually declined, suggesting that the problem of hunger may have gotten worse rather than better (Patnaik 2004, 2012). So, despite apparent material progress in the last decade, India is one of the worst countries in the world in terms of hunger among the population and the number of hungry people in India is reported by the United Nations to have increased since the early 1990s.

Some Implications for Policy

Food price inflation has had a major role to play in this process as we have argued earlier. This is disturbing in a country still characterized by substantial poverty and deprivation, since the evidence suggests that food prices have risen to a substantial extent because of major failures of state policy. This calls for a major redesign of policy. Instead of harping on targeting subsidies and shifting to cash transfers, the emphasis in the first instance should be to strengthen distribution by increasing the geographical spread and coverage of the public distribution system, which must be ensured adequate supplies and must be monitored to prevent leakages. The effort to complicate the system and target it through cumbersome definitions of included sections, divided in turn into segments with differential access at differential prices, has been shown to result in substantial errors of exclusion and inclusion. The shift must be in the direction of universal access.

But even ensuring physical access is not enough. To include the really poor who need this system most, the government must through an appropriate pricing and subsidy mechanism render essential items of food affordable. In addition, these poorer sections should be ensured an income through strengthening programmes like the National Rural Employment Guarantee Scheme, so that they can have the power to purchase the physically accessible and affordable grain. No food security system can work unless a minimum of employment is assured for all.

There remain two questions that may still arise. The first is, where is the money to come from? This question has been answered many times over. India’s tax-to-GDP ratio is still low even by developing country standards: there are too many concessions and loopholes that allow otherwise eligible corporations and individuals to avoid paying tax and that reduces the effective rate at which they are taxed; and tax evasion is rampant and arrears due and disputed are huge. Mobilizing revenues to cover the likely subsidy bill should not be a problem, so long as the political will exists and the social sanction won.

The second question is more serious and relates to how the requisite supplies of food can be made available. Domestic food production has been adversely affected by neoliberal economic policies that have opened up trade and exposed farmers to volatile international prices, even as internal support systems have been dismantled and input prices have been rising continuously. Inadequate agricultural research, poor extension services, overuse of ground water and incentives for unsuitable cropping patterns have caused degeneration of soil quality and reduced the productivity of land and other inputs (Government of India 2006). Sections that constitute a large proportion of those tilling the land, have been deprived of many of the rights of cultivators, ranging from land titles to access to institutional credit, knowledge and inputs and this, too, has affected the productivity and viability of cultivation. All this suggests that besides immediate measures to deal with the food crises, attention needs to be paid in the medium term to the larger agricultural crisis affecting the country. But that is something the government of any modern nation should anyway do.

The campaign for a just food order should, in turn, focus on three different sets of issues. The first is the need to dampen food price inflation and reduce the volatility in food prices, through measures aimed at increasing and stabilizing supply so as to correct any demand–supply imbalances, preventing profiteering at the expense of both producers and consumers and reining in speculation. The second is to insulate the poor from the asymmetrically adverse effect that food price increases have on them by ensuring access to affordable food through a strengthened food distribution system. And, finally, work in the long run to assure everyone an income adequate to meet their basic needs and improve the viability of crop production so as to encourage farmers to contribute to self-sufficiency even when the demand for food is substantially stepped up.

Footnotes

Acknowledgements

This article is the result of a study commissioned by Oxfam, India.