Abstract

There is a widespread view that inflation or inflationary expectations are the only way to overcome the zero lower bound on interest rate. This article shows that this is not true. It is shown that a tax-subsidy scheme can be used to overcome the zero lower bound on interest rate—without any inflation or inflationary expectations. A simple ‘old’ Keynesian model is used though the treatment is novel and in-depth. The article ends with a discussion that suggests that the ‘non-inflation solution’ is superior to the ‘inflation solution’ under some conditions.

The difficulty lies, not in the new ideas, but in escaping from the old ones … . (John Maynard Keynes, 1936)

Keywords

Introduction

In Economics literature, the problem of zero lower bound (ZLB) on interest rate can be overcome by inflation or inflationary expectations only. 1 This article asks the question: Is it possible to overcome the ZLB on interest rate without any inflation at all? The answer is yes. This answer has, as we will see, some significance.

This article will show that fiscal policy can be used instead of monetary policy to take care of the ZLB problem. Correia et al. (2012) too has explored the same theme. However, that paper uses fiscal policy instead of monetary policy to engineer (consumer price) inflation which, in turn, takes care of the ZLB problem. However, this article does not use inflation at all whether through monetary policy or through fiscal policy (more shall be discussed later).

Currency yields zero nominal return. So the nominal interest rate on a debt instrument cannot be negative in equilibrium otherwise there is an arbitrage opportunity. So, there is a ZLB on nominal interest rate. This can come in the way of ensuring macroeconomic stability. A remedy for the above problem is inflation (see, for example, Summers, 1991, and a recent paper like Yehoue, 2012). Inflation creates a gap between the nominal interest rate and the real interest rate. It is possible then to have a non-negative nominal interest rate and a negative real interest rate that can clear market for funds without endangering macroeconomic stability. A weaker version of the argument relies on credible inflationary expectations if the prevailing inflation rate is zero or low (Krugman, 1998). This too can bring about a gap between nominal and real interest rate. In what follows, we will, for simplicity, consider actual inflation and not inflationary expectations.

This article will show that there is a tax-subsidy scheme that is implicit in inflation. There is an implicit tax on savings

2

and an implicit subsidy on investment. This tax-subsidy scheme is at work to ensure macroeconomic stability. This raises an interesting question. Why does the tax-subsidy scheme have to be implicit and through the central bank rather than explicit and through the treasury? To examine this question, this article will consider two explicit tax-subsidy schemes. In all, this article considers three schemes, which are labelled as follows:

Implicit tax-subsidy scheme, Explicit and mimicked tax-subsidy scheme, and Explicit and non-mimicked tax-subsidy scheme.

The first scheme is implicit in inflation. There is no inflation in the other two schemes. Only the first scheme is implemented by the central bank. The other two schemes are in the domain of the treasury. It is well known that the first scheme can ensure full employment (though the argument is not presented in the form in which it is done here). This article shows that the second scheme cannot ensure full employment but the third scheme can. The implicit tax rate on savings is equal to the implicit subsidy rate on investment in the first scheme. This common rate is the same as the inflation rate. The explicit tax rate on savings is equal to the explicit subsidy rate on investment in the second scheme. It is in this sense that this explicit tax-subsidy scheme mimics the implicit tax-subsidy scheme. Finally, the explicit tax rate on savings is not equal to the explicit subsidy rate on investment in the third scheme (in fact, the tax rate on savings is zero). It is in this sense that the third scheme does not mimic the first scheme. Inflation is basically a corrective measure rather than a distortionary measure in the first scheme. Similarly, the tax on savings and subsidy on investment are basically corrective measures in the third scheme.

The explicit and non-mimicked tax-subsidy scheme seemingly has one difficulty. The subsidy on return from investment needs to be financed. However, this is, as we will explain, easy to handle. The treasury can impose a small tax on investment in all years other than the (occasional) year(s) in which the problem of ZLB is faced. 3 There can also be, as we will discuss, scope for international sharing of the ‘ZLB risks’ across countries.

Towards the end, we will explain the significance of the results in the article and discuss why there is merit in using the explicit and non-mimicked tax-subsidy scheme (fiscal policy) in lieu of the implicit tax-subsidy scheme (monetary policy). This is, in a sense, not surprising considering that tax-subsidy schemes are more naturally in the domain of fiscal policy than in the domain of monetary policy. The discussion will use a bit of history, empirical evidence about related issues and behavioural economics.

To begin with, this article will consider the literature review in the second section. Thereafter, the formal analysis of the ZLB problem and the three tax-subsidy schemes will be presented in the third section. The explicit and non-mimicked tax-subsidy scheme leads to a fiscal deficit in the ‘ZLB year’. In the fourth section, we will discuss how this deficit can be met. This will be followed by an informal comparison of ‘inflation solution’ and ‘non-inflation solution’ in the fifth section. We will then conclude in the sixth section.

Literature Review and This Article

The theme in this article has been missing in the literature. There is, in a sense, one exception, which is a recent paper—Correia et al. (2012). 4 Much of this section will review Correia et al. (2012) in relation to this article. Thereafter, we will consider some other related papers including Farhi et al. (2011).

A part of the theme in this article and in Correia et al. (2012) is very similar, which is that unconventional fiscal policy (instead of monetary policy) can be used to overcome the ZLB problem. However, there is an important difference. While Correia et al. (2012) use fiscal policy to engineer (consumer price) inflation instead of using monetary policy, this article avoids inflation altogether. Instead, a tax-subsidy scheme is used in lieu of the tax and subsidy like features implicit in the ‘inflation solution’ to the ZLB problem. Though fiscal policy is used in both articles, the form of the fiscal policy and the models used in the two articles differ considerably. Correia et al. (2012) uses the New Keynesian Model. This article, on the other hand, uses, what may be called, the Old Keynesian Model. Though the basic structure of the model is old, there are novel features in the model in this article. Correia et al. (2012) has an elaborate model. This article, on the other hand, has the virtue of being simple.

To appreciate the difference between this article and Correia et al. (2012), let us quickly review this article (possibly at the cost of some repetition). It begins with the observation that in the context of the ZLB problem, inflation is tantamount to a tax on savers and a subsidy on investing entities. Tax on savings discourages the latter. On the other hand, subsidy on investment encourages the latter. Such a tax-subsidy scheme has a bite when the real rate of interest is negative. It is this tax-subsidy scheme that is implicit in inflation and that is at work in the ‘inflation solution’ to the ZLB problem. Based on this insight, this article uses an explicit tax-subsidy scheme in the ‘non-inflation solution’ to the ZLB problem. So this article uses fiscal policy to overcome the ZLB problem without any inflation.

Correia et al. (2012) distinguish between producer price inflation and consumer price inflation. Setting of prices is staggered by producers in their model. There can be distortion due to inflation for producers. So the idea ‘is to induce inflation in consumer prices, while keeping producer price inflation at zero’ (Correia et al., 2012, p. 3). Their model ‘… involves engineering over time an increasing path for consumption taxes, a decreasing path for labour taxes, coupled with a temporary investment tax credit or a temporary cut in capital income taxes’ (p. 2). As is clear from this description of Correia et al. (2012), the latter take an approach that is very different from the one used in this article.

This article explores the possibility of international risk sharing in the context of the ZLB problem. To see this, note that it is possible that the ZLB problem does not occur simultaneously in many countries. Each country can accumulate a corpus of funds in each of the many non-ZLB years. This corpus may be pooled together as an international fund. This fund may be used by whichever country is faced with a ZLB problem. International sharing of risks due to the ZLB problem is not there at all in Correia et al. (2012). However, the latter includes issues of time consistency, which this article does not consider formally (though there is some discussion on this in the fifth section).

Correia et al. (2012) begin by considering sticky prices. Thereafter, they consider sticky wages. In contrast, this article assumes that the price level and the money wage are flexible; the only ‘rigidity’ in this article is that there is a lower bound on interest rate. Wage-price flexibility is sometimes viewed as a ‘classical assumption’ (or non-Keynesian assumption). This is not entirely correct.

5

See the quote below:

… in ‘Book V: Money-Wages and Prices’, Keynes drops the assumption of a constant money-wage rate. (Patinkin, 2008, p. 697)

It may be said that this article is more in line with the thinking in Keynes (1936) than is the case with ‘Keynesian’ models with nominal rigidity. The latter group includes Correia et al. (2012).

Though there are many differences between this article and Correia et al. (2012), there is some similarity as well. One similarity between this article and Correia et al. (2012) is the inter-temporal balancing of the government’s budget in both cases. Correia et al. (2012) show that changes brought about by fiscal policy can be reversed after the natural interest rate is back to positive territory. In fact, the unconventional fiscal policy can be applied in reverse as a preventive policy. There is a similar policy suggestion in this article, which is that the treasury can impose a small tax on investment in each of the many non-ZLB years. This prepares a corpus of funds that can be used to subsidize investment in ZLB years.

Next consider Farhi et al. (2011). Though this paper is not on the same theme as this article, it has some resemblance to this article and Correia et al. (2012). Farhi et al. (2011) considers an economy in which there is a need for devaluation but the same is not possible. The authors show how fiscal policy can be used instead to get the desired effect.

This article is a part of the larger research on ‘narrow monetary policy and extended fiscal policy’ by this author. See Chapter 11 in Singh (2012). The latter argues that some functions that are usually associated with monetary policy can instead be looked after by fiscal policy. This article now carries the argument in Singh (2012) further. Fiscal policy can take care of the ZLB problem. So far a solution to this problem has been associated primarily with the monetary policy. So there can be, as this article shows, a narrow monetary policy and an extended fiscal policy even in the context of the ZLB problem. This was not considered in Singh (2012).

This article has a ‘sister article’—Singh (2013). The current article shows that fiscal policy can be used to overcome the ZLB problem. The other article shows that fiscal policy can be used to overcome other problems, which may be faced in ensuring macro-financial stability. Both articles study the role of extended fiscal policy given that the inflation rate is zero.

Much of the literature emphasizes the role of inflation or inflationary expectations in overcoming the ZLB problem. However, some authors have also advocated depreciation of the currency in this context (McCallum, 2000). Klose (2011) suggests a modified Taylor rule to accommodate the issue of ZLB on nominal interest rate. These suggestions are all in the domain of monetary policy. This article, on the other hand, considers the role of fiscal policy in overcoming the ZLB problem. It uses, in principle, tax on savings and subsidy on investment. This fiscal policy is very different from the standard Keynesian fiscal policy, which is focused on varying government demand for goods and services over the business cycle. This is, in turn, supposed to stabilize aggregate demand and thereby stabilize output and employment.

There can be strategic considerations in policy implementation and in allocation of responsibility between the treasury and the central bank in the context of the familiar solutions to the ZLB problem. For a recent article on these aspects, see Dhami and al-Nowaihi (2011). This article will abstract from these issues. If the ZLB problem can be taken care of by fiscal policy alone, then this obviates the need for coordination between monetary policy and fiscal policy in the context of the ZLB problem.

At the heart of the ZLB problem is the difficulty in realizing a negative interest rate. In this context, Goodfriend (2000) suggests a fiscal policy in the form of carry tax on money (a stock) so that the effective interest rate on money is negative. 6 This article will consider, as mentioned earlier, a tax-subsidy scheme involving savings and investment (flows) with the aim to realize interest rates that are effectively negative.

Model

This article will use the standard macroeconomic model which may now be termed Old Keynesian Model. However, the interest rate rigidity will be incorporated and this will be done in novel ways. 7

This section is divided into four subsections. First, the ZLB problem will be explained in the absence of any policy intervention. Second, it will be shown formally that the implicit tax-subsidy scheme by the central bank can overcome the ZLB problem. Third, it will be shown that the explicit and mimicked tax-subsidy scheme cannot help overcome the ZLB problem. Finally, it will be shown that the explicit and non-mimicked tax-subsidy scheme can overcome the ZLB problem.

The Zero Lower Bound (ZLB) Problem

In this subsection, it is assumed that the inflation rate is zero. Accordingly, the nominal rate of interest is the same as the real rate of interest in this subsection. So there is one interest rate in the economy. This is denoted by r. Accordingly, the non-negativity constraint on interest rate in the economy is:

Here the focus is on implications of the floor on interest rate and on policy solutions to the problem. To retain this focus, it is assumed that wages and prices are flexible.

8

The rest of the model is as follows:

and

where S, Y, I, P, N, w denote savings, output, investment, price level, employment and nominal wage respectively. Further

Description of the model is as follows. This is a standard closed economy macroeconomic model. Equation (2) is the condition that savings are equal to investment in equilibrium. Equation (3) is the equilibrium condition that the supply of money is equal to the demand for the same. Equation (4) is simply the production function that relates output to employment. Equation (5) says that in equilibrium real wage is equal to the marginal product of labour. Finally, Equation (6) is the equilibrium condition that workers are on their supply curve (supply of labour depends on real wage).

Following features are implicit in the above model. Savings depend on income and interest rate. Investment consists of two parts— exogenous investment and endogenous investment. The latter depends on the interest rate. Demand for money increases proportionately with the price level. There is no money illusion.

These are fairly standard in the literature. Observe that both

Each case will be considered separately. The latter case is the problematic case of low aggregate demand which can lead to less than full employment level of output, as we will see.

There are five equations (2)–(6) in five variables Y, r, P, N and w. The following assumption is made.

The last part of Assumption 1 in particular will play an important role in the model.

Observe that three equations (4)–(6) have three variables Y, N and

Indeed,

If investment is large in the economy i.e.,

Given that the savings and investment functions are well-behaved except for the fact that the market clearing rate of interest is negative when

The interest rate is flexible so long as

The gap between the left hand side and the right hand side is the (involuntary) unemployment given that the real wage is

Considering both cases

The crucial part of the model is that it is not possible to realize

It may be said that the above analysis is consistent with what Keynes himself believed to be the essence. As Keynes (1937) observed a year after the publication of his General Theory,

The novelty in my treatment of saving and investment consists, not in my maintaining their necessary aggregate equality, but in the proposition that it is, not the rate of interest, but the level of incomes which (in conjunction with certain other factors) ensures this equality. (p. 249)

Summing up, less than full employment is possible if investment demand is low, there is a ZLB on interest rate and there is no policy intervention. 9 In this subsection, it was assumed that there is no implicit or explicit tax-subsidy scheme in place to ensure that investment is equal to savings at the full employment level of output. In the next subsection, an implicit tax-subsidy scheme (through inflation) will be considered. Thereafter, an explicit tax-subsidy scheme will be considered.

An Implicit Tax-subsidy Scheme by the Central Bank

In the previous subsection, there is no policy intervention to ensure full employment. In this one, central bank intervention will be considered. This takes the stylized form that the central bank engineers inflation to take care of the ZLB problem. The analysis in the previous subsection suggests that policy intervention is required in periods when exogenous investment is low i.e.,

The model explained here is a multi-period model (unlike the one-period model in the previous subsection). So, subscript t date has been attached to the variables to signify date as we will see in the equations later. The basic model structure in this subsection is, however, the same as that in the previous subsection. In some periods, it is the case that

In standard macroeconomics, it is usual to consider a policy maker’s trade-off between inflation and output. However, a departure will be made from this. This is for analytical simplicity. It is assumed that the preferences of policy makers are lexicographic. The first preference is for large output (Y) and the next preference is for low inflation (this is equivalent to large real money balances (

The role of monetary policy here is to maintain inflation to create a wedge between the nominal rate of interest (

In the previous stanzas, there was only one interest rate and this had to be non-negative. Here, there are two interest rates—the nominal rate of interest and the real interest rate. The non-negativity constraint applies to only the nominal interest rate. The real interest rate can be negative. So the ZLB constraint takes the following form:

Given that both savers and investors are rational, it follows that savings and investment depend on the real rate of interest rather than on the nominal rate of interest (we will comment on the assumption of rationality later). Accordingly, the equilibrium condition that savings are equal to investment takes the following form:

where t is, as mentioned already, the subscript for time period. The demand for real money balances depend on the nominal interest rate as this is the opportunity cost of holding real money balances. Hence, we have:

The rest of the model resembles the model in the previous subsection except that subscript t has been attached to variables.

10

Let

Given the structure of the model, it follows that,

Let

and

and Equations (4), (5) and (6) in the previous subsection. The last three equations have three variables Y, N and

Taking

See Assumption 1. Further note that there are two values of

Given lexicographic social preferences of the public authorities, there is a need to target the least value for

Now this gives

This does not violate the ZLB condition (9) regardless of the value of

whether

Let us compare the model described here with that explained previously. If

Two (nominal) variables P and w need to be determined now. P can be determined from Equation (16). This has three variables Y, P and

where

Let us now take a close look at the exact way in which inflation is useful in this model. The gap between the nominal and the real interest rates (

Here, it has been seen that an ‘inflation solution’ can be used to get around the ZLB problem and to ensure full employment. 11 Further, we will explore if there are ‘non-inflation solutions’ to take care of the ZLB problem.

An Explicit and Mimicked Tax-subsidy Scheme by the Treasury

In this subsection, it is assumed that the inflation rate is zero. So there is no implicit tax-subsidy scheme by the central bank. Instead, an explicit tax-subsidy policy by the treasury will be considered, which will attempt to mimic the implicit tax-subsidy scheme by the central bank, and do so without any inflation. We will see that this is not possible, and accordingly this scheme cannot ensure full employment.

In the earlier section, the implicit tax rate on savings is equal to the implicit subsidy rate on investment. Accordingly, to mimic this scheme, the explicit tax rate on savings will be taken to be equal to the explicit subsidy rate on investment. Let this common rate be

where

There is an important difference between the implicit and the explicit tax-subsidy schemes. In the former case, the public authorities need to maintain inflation in all periods. As argued already, it is not possible to engineer inflation for only one period and revert back to price stability thereafter. In contrast, it is assumed that the explicit tax-subsidy scheme can be implemented quickly in the periods in which investment is low. So this scheme is temporary. Assume that the policy makers can observe the realization of

The explicit subsidy burden is exactly matched by the explicit tax collected, given that the tax rate is equal to the subsidy rate and that savings are equal to investment in equilibrium. The government has no other expenditure or taxes.

The explicit tax-subsidy scheme is a case of fiscal policy. However, observe that this is very different from the standard Keynesian fiscal policy. 12

The net interest rate for investors is the gross interest rate minus the subsidy. The net interest rate can be negative as there is no rationale for evading a subsidy. So there is no non-negativity constraint on interest rate for investors. Next, consider the savers. The net interest rate on savings is irrelevant for savers if savings are inelastic (

Assume that agents are rational (more on this assumption later). Accordingly, savings and investment are functions of the after-tax interest rate and the after-subsidy interest rate respectively. Accordingly, the savings–investment equality takes the form

Next consider the demand and supply of money. Demand for real money balances depends on the opportunity cost of holding money. Since there is no tax or subsidy on holding money, the opportunity cost of holding money is the gross interest rate

The rest of the model consists of Equations (4), (5) and (6) (as in the previous two subsections).

Is it possible to attain full employment under the explicit and mimicked tax-subsidy scheme? The next proposition answers this question.

Model 1: Equations (4), (5), (6), (15) and (16), and the ZLB constraint (9).

Model 2: Equations (4), (5), (6), (21) and (22), and the ZLB constraint (20).

We know that

Consider the five equations in each of the two models. Equations (4), (5) and (6) are common to the two models. Further observe that the set of Equations (15) and (16) are mathematically the same as the set of Equations (21) and (22) except that

and

where the inequality follows from Equation (17) (which gives the solution to interest rate in Model 1, given that

(b) If

The thrust of Proposition 1 is that the explicit and mimicked tax-subsidy scheme by the treasury can ensure full employment when investment is low, only if savings are interest inelastic. If savings are interest elastic, then the explicit and mimicked tax-subsidy scheme fails to ensure full employment if investment demand is low. So, there is, indeed, a good reason why the implicit tax-subsidy scheme should be used instead of the explicit and mimicked tax-subsidy scheme. This is, indeed, what is observed in practice.

Further, we will check if an explicit and non-mimicked tax-subsidy scheme by the treasury can help achieve full employment when investment is low and

An Explicit and Non-mimicked Tax-subsidy Scheme by the Treasury

Here, we will consider the general case i.e., the subsidy rate and the tax rate can be different from each other. Let

In the previous subsection, the special case

Policy makers have two policy instruments:

As discussed previously and for reasons considered previously, there is no policy intervention if investment demand is large i.e., if

The net interest rate on investment (

The rest of the model is as follows. Since savings are a function of the net interest rate for savers i.e.,

There is no tax or subsidy on money holdings. So neither

Is full employment possible now if

As will become clear later, B is the net interest rate for investors, which ensures full employment given that the net interest rate for savers is zero.

We can now state our next result as follows.

(a) The model includes Equations (4), (5), (6), (22) and (24), the inequality (23) and Definition 1. From the first three equations, we know that

If

Next, it follows from

We have shown that if policy makers choose

(b) Given

The thrust of Proposition 2 is that the explicit and non-mimicked tax-subsidy scheme by the treasury can ensure full employment if investment demand is low, and it can do so without any inflation or inflationary expectations.

So far, each scheme has been considered somewhat in isolation. It is worthwhile carrying out a comparison. In this section, it was seen that if investment demand is low, full employment can be attained under two schemes: the implicit tax-subsidy scheme and the explicit and non-mimicked tax-subsidy scheme as discussed. Previously, it has been seen that it is optimal policy that the implicit subsidy rate on return from investment is

We need to show that

Given that

where the first equality follows from Definition 1, the weak inequality follows from

Intuition for Proposition 3 is straightforward. Under the implicit tax-subsidy scheme,

Let us sum up this section and recapitulate two well known results in the context of the ZLB problem in the literature alongside three new results in this article.

Unemployment is possible in the absence of policy intervention (Keynes, 1936).

The implicit tax-subsidy scheme can ensure full employment (Summers, 1991).

The explicit and mimicked tax-subsidy scheme cannot ensure full employment.

The explicit and non-mimicked tax-subsidy scheme can ensure full employment.

The optimal subsidy rate under the explicit and non-mimicked tax-subsidy scheme is greater than the optimal subsidy rate under the implicit tax-subsidy scheme.

The last three statements are the gist of Proposition 1, Proposition 2 and Proposition 3 respectively.

Though the explicit and non-mimicked tax-subsidy scheme proposed here ensures full employment, there is some minimum deficit for the government in the ‘ZLB year’. The next section will show how this deficit can be financed.

Government’s Budget, and International Pooling of the ‘ZLB Risks’

It was seen earlier that the treasury needs to run a deficit in its budget to ensure full employment under the explicit and non-mimicked tax-subsidy scheme. This deficit needs to be financed. This financing can be quite simple. The treasury can impose a tax on investment in normal years. Since the ZLB problem arises occasionally (once in about 70 years if we go by the US experience), this implies that there can be a small tax over a large number of years. Furthermore, these taxes can be earmarked (possibly by legislation) for use in a ZLB year. This ensures credibility of the financing arrangement. In this way, there can be an inter-temporal balance in the government’s budget (a deficit in the ZLB year and a surplus in non-ZLB years).

If there is certainty about the frequency and the timing of the ZLB problem, the above financing arrangement can work smoothly. However, there can be uncertainty. In this case, there can be a need for a cushion in, what we may call ‘the stabilization budget’ in the form of an ex-ante reserve of funds or an ex-post support from ‘the usual budget’ of the government.

An arrangement to finance the subsidy in the ZLB years was discussed above in the context of a single economy. However, several economies can be considered so that the risks due to the ZLB problem can be shared at the international level. Though there is often a correlation between the economic downturns at the international level, it is interesting that the ZLB risk is not highly correlated internationally given the past experience. Consider some examples. In the aftermath of the crash in much of the asset market in 1989–1990 in Japan, there was a problem of ZLB (or near-ZLB) on interest rate in Japan. This was at a time when hardly any other country faced such a problem. Consider another example. In the more recent financial crisis, though much of the developed world in North America and Europe has faced the ZLB problem or near-ZLB problem somewhat simultaneously, the rest of the world (emerging economies, developing economies and oil producing countries) does not face this problem. This suggests that there is scope for international risk sharing in the context of the ZLB problem.

International risk sharing in the context of the ZLB problem may happen as follows. At the international level, the involvement of an international public body such as the IMF (or the BIS) may be considered. Such a body may function not only as a financial institution but also as an insurance institution (though this may require a change in the mandate). Consider a case in which many countries adopt the proposed scheme to take care of the ZLB problem. Suppose that each country buys insurance from the IMF. Each country pays an insurance premium to the IMF every year and finances this premium by a small tax on investment in normal years. The funds thus collected by the IMF may be used to help the countries that face the ZLB problem. In the unlikely event that too many countries face the ZLB problem somewhat simultaneously, the IMF may need to pay more than was initially anticipated. In such a case, the IMF may need to use up its own resources.

The insurance solution can work best if the risks of hitting the ZLB on nominal interest rate across countries are not perfectly correlated. The less is the correlation, the greater is the scope for the proposed scheme at the international level.

Two Solutions to the ZLB Problem: A Further Comparison

Three schemes have been considered in this article. These are (a) implicit tax-subsidy scheme, (b) explicit and mimicked tax-subsidy scheme, and (c) explicit and non-mimicked tax-subsidy scheme. It was seen that only the first and the third schemes can help overcome the ZLB problem. In what follows, these two schemes will be considered with a focus on the third scheme which is unfamiliar.

It may be argued that there is hardly any compelling need to devise an explicit tax-subsidy scheme to deal with the ZLB problem if it occurs very rarely (more on this later). We would like to make three observations. First, while it is true that in the past the ZLB problem has occurred occasionally, this may not be the case in future. Second, even if it is as rare ‘on an average’ in the long run as it has been in the past, the problem may occur in quick succession at times. In such situations, the cost to the economy due to the ZLB problem can be very high. So it is important to have a solution in place. Third, in any case, it is not our argument that the ZLB problem is small or large, rare or frequent. Our argument is simply that given the potential ZLB problem that is considered serious in the literature, there are two solutions. One is the well known ‘inflation solution’ in the literature. This article has provided an alternative ‘non-inflation’ solution.

To see the significance of the alternative solution, let us take, what may seem, a digression and consider an analogy. It was at first believed that the earth is ‘flat’ and consequently there is only one direction in which to travel to a given place on earth (consider, for simplicity, two places on the same latitude on globe). Subsequently, it was discovered that the earth is ‘round’ and that consequently one may, in principle, travel in any one of two directions to reach a given place. This was a most remarkable and historic discovery. It provided an alternative. More important, it paved the way for thinking afresh on many issues. Let us return to the economic problem at hand. So far, it was believed that there is only one way to take care of ZLB problem. This article and Correia et al. (2012) have opened up a new way to approach the given problem. It may possibly pave the way for fresh thinking on other issues. This is not to say that the analogy with the discovery that ‘earth is round’ is appropriate in so far as scale of the significance of the alternative solution to the ZLB problem is concerned. However, qualitatively, there is an interesting parallel between the two cases. In Science, it is an important step forward to find a new way. Though the scientific value counts in itself, we conjecture that this is useful in practice too. To see this, consider a broad perspective.

Measurement plays an important role in daily life. This is true in case of weight, height, temperature and so on. There is a similar problem in Economics too. There is a need for a numeraire that is stable, if not fixed. Such a numeraire has somewhat eluded the public. Economists have not been able to help the general public in this matter as they have had to worry about dealing with problems such as the ZLB problem, which, it has been argued, requires positive inflation. This immediately implies that the value of the numeraire (Rupee or Dollar) is not fixed. This makes the public uncomfortable. In this context, this article has made an attempt to satisfy both the public and the economists. The former would be happy with zero inflation. The economists too would be happy with zero inflation as the ZLB problem can be taken care of in the light of this article (and Correia et al., 2012).

It is true that there are a few more problems other than the ZLB problem that inflation helps solve. It is only when alternative solutions to all these problems can be found that inflation rate of zero can be viewed as the optimal rate. However, this larger exercise is outside the scope of this article which is lengthy in itself. What this article has done is to take the first step in the direction of showing that zero inflation can be a realistic target. It is, as is often said, the first step which is the difficult one. This has been done. It is hoped that a ‘non-inflation solution’ will emerge in case of the other problems as well, for which inflation is currently considered the only solution.

Although the alternative solution to the ZLB problem suggested here avoids inflation, it involves taxes and subsidies. These can be distortionary in which case there is a need to consider the economic costs of the tax-subsidy scheme. Two observations may be made here. First, a tax-subsidy scheme is not unique to the ‘non-inflation solution’. It is present in the ‘inflation solution’ as well. It is just that the tax-subsidy scheme is implicit in the ‘inflation solution’ whereas it is explicit in the other case. Second, if there is a first best situation to begin with and then taxes or subsidies are used, there is indeed a distortion. However, this is not the case where a tax-subsidy scheme is used as a corrective measure in a situation which is not the first best.

Consider an analogy from Public Economics. It is well known that taxes or subsidies used to take care of externalities are welfare enhancing rather than welfare reducing. Now let us return to the problem at hand in Macroeconomics. Suppose there is a shock and it takes the form of loss of confidence. Investment falls considerably and the market clearing real interest rate is negative for ensuring full employment. Given this situation, the tax-subsidy scheme is welfare enhancing rather than welfare reducing. The treatment of a transitory shock in macroeconomics through a tax-subsidy scheme can be similar to the treatment of an externality in Public Economics. For more on this, see Jeanne and Korinek (2010a), Jeanne and Korinek (2010b) and Singh (2013).

This article has used a simple model to understand and convey the essence of the new idea that a ‘non-inflation solution’ to the ZLB is possible. In the context of this simple treatment, distortions are not in the picture in case of both the ‘inflation solution’ and the ‘non-inflation solution’. However, in a more elaborate model that incorporates other complexities, there can be scope for distortions. But this is outside the scope of this article.

In what follows, we will make a (further) comparison between the implicit tax-subsidy scheme and the explicit and non-mimicked tax-subsidy scheme.

First, in the formal model in this article, aggregate savings and aggregate investment were considered. Let us now consider a disaggregated model with a focus on subsidy on investment.

In the case of an implicit subsidy scheme, the gap between the nominal interest rate and the real interest rate is effectively the rate of subsidy on all investment. Recall that the investment function was:

where I is investment,

where

Consider two sectors in an economy—sector A and sector B (say). Assume that investment in sector A is more desirable than investment in sector B of the economy. More desirable investment can be subsidized at a higher rate than less desirable investment. Let us use superscripts A and B for investment in sector A and in sector B respectively. Let

Clearly, different subsidy rates are possible under the explicit and non-mimicked tax-subsidy scheme. However, a set of differentiated subsidy rates in the occasional ZLB years across different sectors of the economy is not possible under the implicit tax-subsidy scheme given the common inflation rate for all sectors. So the explicit and non-mimicked tax-subsidy scheme can be superior to the implicit tax-subsidy scheme.

Second, there are side-effects of policies. The formal model in this article considered only one asset viz., money. Let us now informally consider an economy that includes more assets. When monetary policy is used to engineer negative real rates of interest in the context of the ZLB problem a la Summers (1991), such rates of interest apply not only to the real and the monetary sector of the economy but they apply more generally to the economy as a whole including the asset markets. In contrast, the changes in interest rates under the explicit and non-mimicked tax-subsidy scheme need not apply to the asset markets. Interest cost can be subsidized only in the context of new real investment in projects and not in case of financial investment. So the possible side-effects under the implicit tax-subsidy scheme can be minimized, if not eliminated completely, under an alternative explicit tax-subsidy scheme. The side-effects can be quite damaging for the real economy (Feldstein, 2002). These may lead to asset price bubbles which can, in turn, have adverse effects on the real sector. A good example of this is the boom or bubble in the housing market in the post-2000 period up to about 2007, which has been attributed by several economists to the low interest rates in general. A scheme like the explicit and non-mimicked tax-subsidy scheme can avoid or reduce such effects. For a recent discussion on side-effects of the (general) low interest policy since 2007–2008, see Bank for International Settlements (2012).

Third, the formal model in this article has abstracted from distribution effects. However, when the central bank imposes an implicit tax on savers and provides an implicit subsidy on return from investment, a redistribution from savers to investors is involved (Goodfriend, 2000). In contrast, the explicit and non-mimicked tax-subsidy scheme in this article does not involve any such redistribution from savers to investors. Accordingly, the explicit and non-mimicked tax-subsidy scheme can be less controversial than the implicit tax-subsidy scheme.

Fourth, though the formal model in the article abstracted from issues related to transparency and accountability, these can be important. First consider the issue of transparency. The use of the explicit and non-mimicked tax-subsidy scheme is transparent. The public will know that all or some investors are being subsidized in the ZLB year(s), and that investors are being taxed in normal years. The use of implicit tax-subsidy scheme is not transparent. The subsidy for investors and the tax on savers are implicit and hence not transparent. To the extent that transparency is valued, 13 the explicit tax-subsidy scheme is preferable to the implicit tax-subsidy scheme.

Next consider the issue of accountability. As mentioned already, when the central bank imposes an implicit tax on savers and provides an implicit subsidy on investment, redistribution from savers to investors is involved. Ideally any redistribution should receive the approval of an appropriate body such as the Parliament. However, this does not happen in practice in the case of the implicit tax-subsidy scheme. So there is little accountability in the implicit tax-subsidy scheme. In contrast under the explicit and non-mimicked tax-subsidy scheme, it is proposed that there is a Parliamentary approval and so the treasury is accountable. Furthermore, the Parliamentary approval may be obtained in advance as a general constitutional mandate to be used in the event that a ZLB problem is faced. This can avoid possible delays if an approval is required in each case separately after the problem has occurred.

Fifth, it may be argued that the ZLB problem is being currently faced by many developed countries and that if such countries were to adopt the explicit and non-mimicked tax-subsidy scheme proposed here, they would need to incur the expenditure on subsidy on return from investment now and collect taxes in future (given they had not built any reserve for this purpose in the past). So they would need to borrow (in addition to their current borrowings) at present. This can further aggravate the public debt problem faced by these countries. Hence the proposed new fiscal policy to take care of the ZLB problem is, it may be argued, not pragmatic. This is particularly true given that there exists an alternative implicit tax-subsidy scheme to overcome the ZLB problem without creating any budgetary imbalance. While there is merit in this argument, it is important to make a few observations.

It is not clear that the fiscal burden due to the proposed new fiscal policy can be large in a ZLB year. Consider a ‘back of the envelope’ calculation on the possible fiscal burden. Assume that the prevailing interest rate is zero. Investment as percentage of GDP is low and needs to be increased by another, say, 8 per cent of GDP. Suppose that the treasury needs to provide a subsidy such that the effective or net or after-subsidy interest rate for investing firms is –5 per cent (one figure mentioned in Buiter, 2009). This implies that the explicit subsidy required for raising investment is 0.4 per cent (= 0.05 # 8) of GDP. This is not a large figure relative to the size of fiscal stimulus in many countries in the aftermath of the financial crisis and the recession beginning in 2007–2008.

Consider the financing of this subsidy by a tax on investment in non-ZLB years. Assume that the ZLB problem occurs after 50 years (though in the US it has, as mentioned already, occurred after about 75 years). Ignoring economic growth and discounting for time, there is a need for a tax of 0.008 per cent (= 0.4/50) of GDP in each of the non-ZLB years. This is a small figure.

The subsidy in the occasional ZLB periods is used to increase investment which is productive. This can be better than the fiscal stimulus seen in practice in the years around 2008–2009 which was not entirely for productive purposes (or redistributive purposes).

Taxes on investment in future in normal years can be earmarked (possibly by legislation) for the purpose of paying subsidies in the occasional ZLB years. Therefore, there can be credible repayment of the public debt used for this purpose.

The proposed scheme is not only to tackle the ZLB problem at present but also in future. Since it is not the case that even the advanced countries will forever continue to have serious debt problems, there is a need to consider the proposed scheme.

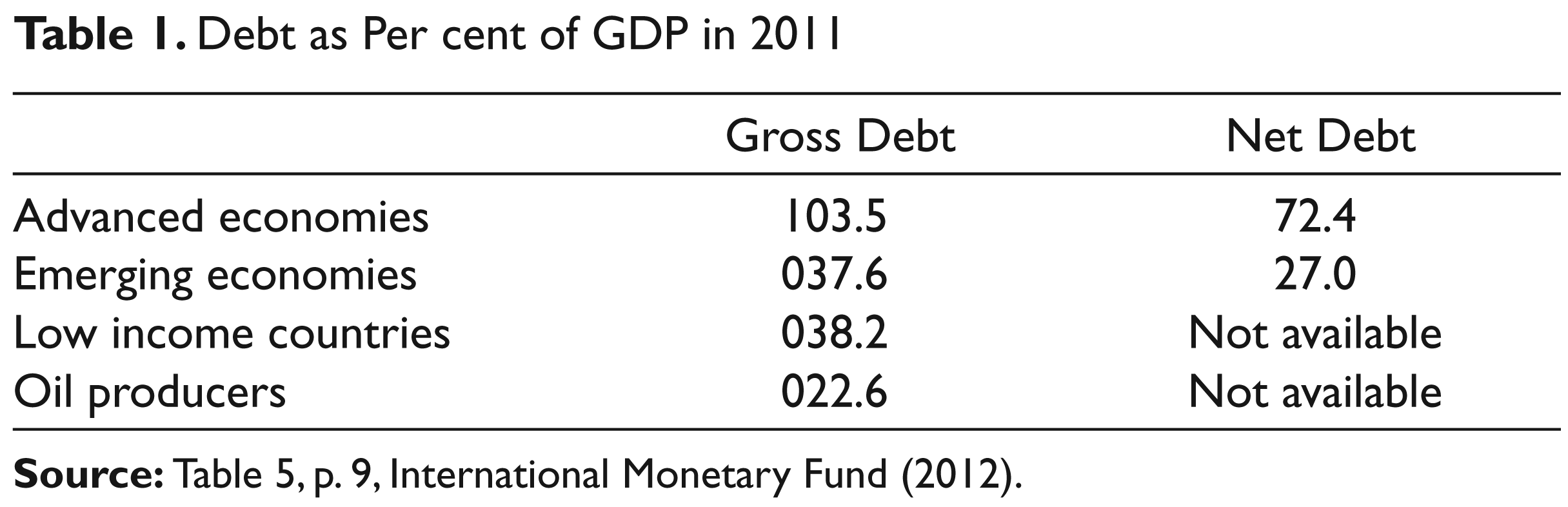

The proposed scheme here is not only for advanced countries that are highly indebted but also for other countries that are not highly indebted. Such countries need not have any worries if the proposed scheme is adopted. It may help to consider some data on the public debt at the international level as shown in Table 1. The gross debt as per cent of GDP in 2011 was high for advanced countries only. For the others, the debt problem on an average does not seem to be serious.

Debt as Per cent of GDP in 2011

All this suggests that the explicit tax-subsidy scheme can be pragmatic for many countries.

Sixth, the model in this article makes the assumption of rationality. The implicit tax-subsidy scheme implemented through monetary policy involves inflation. It was assumed that the expected inflation is equal to the actual inflation in our model. So there was an abstraction from any adverse effects for the economy due to any gap between the actual inflation and the expected inflation. However, it is hard to achieve this equality in practice. It was assumed that agents are rational and that they clearly distinguish between the nominal and the real interest rate. However, as behavioural economics has shown, this assumption is not always realistic. So there can be adverse effects of the implicit tax-subsidy scheme. Such effects are absent in the case of the explicit tax-subsidy scheme proposed here since there is no inflation involved and the distinction between gross and net interest rates can be much clearer than the distinction between nominal and real interest rate for the general public (people are anyway familiar with usual taxes and subsidies). So on this count the explicit and non-mimicked tax-subsidy scheme can be superior to the implicit tax-subsidy scheme.

Consider an example of a divergence between expected and actual inflation. In the early 1980s, the FED and the Bank of England embarked on an anti-inflationary policy. This policy was indeed successful in bringing about a significant and apparently lasting reduction in the inflation rate. However, there were other effects such as high interest rates for quite some time. One reason for such high nominal interest rates was the belief that high inflation was likely to return. Though this belief turned out to be incorrect and the nominal interest rates did fall over time, there were adverse effects in these economies. This was also due to the fact that agents did not always realize exactly the distinction between nominal and real interest rates (see Shiller (2008) for the US case).

The boom in the stock market before the year 2000 is sometimes attributed to the fact that interest rates had fallen considerably over time. Though this is indeed true of nominal interest rates, it is not equally true of real interest rates. However, many investors do not make the ‘subtle’ distinction between nominal and real interest rates. This leads to errors or ‘irrational exuberance’. This can be avoided or reduced if there is zero inflation. It is true that the ZLB problem cannot be taken care of through monetary policy in this case. However, as this article (along with Correia et al., 2012) has shown, the ZLB can be overcome through fiscal policy.

Summing up, there is a prima facie case that the explicit and non-mimicked tax-subsidy scheme is superior to the implicit tax-subsidy scheme. However, there is need for formal research.

Conclusion

The standard policy to deal with the problem of zero lower bound (ZLB) on nominal interest rate is to have inflation or credible inflationary expectations. It has been shown that the standard solution through inflation involves an implicit tax on savers and an implicit subsidy for investors. We called it the ‘implicit tax-subsidy scheme by the central bank’.

This article asks why the tax-subsidy scheme has to be implicit and not explicit. Related to this question, it was asked why the tax-subsidy scheme has to be by the central bank and not by the treasury. To answer this question, ‘explicit and mimicked tax-subsidy scheme’ by the treasury was considered. This scheme mimics the implicit tax-subsidy scheme with one important difference. There is no inflation associated with this new scheme. We find that such a scheme cannot, in general, ensure full employment (it can help only in the special case that savings are interest inelastic).

This article subsequently asked if there exists any other scheme by the treasury that can help overcome this ZLB problem without inflation or inflationary expectations. We find that the answer is yes. We called it the ‘explicit and non-mimicked tax-subsidy scheme by the treasury’. In this scheme, there is no inflation, the tax on return on savings is zero, and the subsidy on return from investment makes the interest rate for investment effectively negative.

Under the explicit and non-mimicked tax-subsidy scheme, the treasury needs to incur a deficit in the ZLB years. This article explained that this deficit can be financed by a small tax on investors in non-ZLB years. So there need not be any inter-temporal deficit for the government in the context of the ZLB problem. There can also be sharing of the ZLB risks at the international level.

As mentioned earlier, two schemes can work to take care of the ZLB problem—the implicit tax-subsidy scheme by the central bank (with inflation), and the explicit and non-mimicked tax-subsidy scheme by the treasury (without inflation). Each solution involves a tax-subsidy scheme, which works as a corrective measure to deal with a macro-economic shock. 14 So, the two schemes are somewhat similar. However, the discussion towards the end of the article suggests that there are other grounds on which the explicit tax-subsidy scheme can be superior to the implicit tax-subsidy scheme. A formal comparison on these grounds is outside the scope of this article, which has focused on formally showing that there does exist a non-inflation solution to the ZLB problem.

Footnotes

Acknowledgements

I appreciate the role of my family and that of Indian Statistical Institute (ISI), Delhi Centre in making this work possible. This article is a revised, much expanded and formalized version of one section of an earlier paper ‘Inflation Targeting and Extended Fiscal Policy’ (2010). I appreciate the comments made by Sunil Ashra, Monisankar Bishnu, Sanjit Dhami, Chetan Ghate, Gita Gopinath, Robert Hall, Thomas Laubach, B.L. Pandit, Arti Singh and Lawrence Summers on different versions of the article. This article has been presented at Management Development Institute (MDI), Gurgaon, at the 8th Annual Conference on Economic Growth and Development at the ISI, Delhi Centre, December 17–19, 2012, and at the National Institute of Public Finance and Policy (NIPFP). I thank the organizers and the seminar participants for their comments, questions and suggestions. Last but not the least I thank an anonymous referee for suggestions to improve the article. Any errors are my responsibility.