Abstract

This article attempts to determine the effect of nominal exchange rates on Indian exports between 1996 and 2014. We begin by assuming that the nominal exchange rate can affect export directly as well as indirectly via its pass through on domestic prices. The analysis is conducted with quarterly data after controlling for the effect of exchange rate volatility on exports. The main results that we get are the following: There is no direct evidence that the nominal exchange rate or its volatility influences exports. However, there is a significant relationship between the relative price ratio (domestic to foreign) and export. Further, we find strong evidence of pass through of the nominal exchange rate on prices (about 54%) in the long run. We interpret this result as an evidence of the nominal exchange rate affecting exports indirectly through domestic prices. The results suggest that the debate on the influence of exchange rates on Indian export is still an open one.

Introduction

The value of the Indian rupee has more than halved vis-à-vis the US dollar from the early 1990s to the late 2000s. In the same period, India’s real aggregate exports have more than trebled. Since economic logic suggests that there should be a link between exchange rate depreciation and export, a legitimate question to ask is: Are the two observations causally related? This question, though pertinent in all types of situations, is particularly so during a time when the exchange rate is allowed to float at least reasonably, that is, during a period when the exchange rate is allowed to fluctuate sufficiently in tandem with exports.

The Government of India took its first step towards fully floating currency in the current account on 1 July 1991 when it devalued the rupee. The exchange rate in June 1991 was about ₹21.1 per US dollar. This exchange rate was fully controlled by the government and can be considered as virtually fixed from the free market point of view. The major exchange rate policies undertaken by the government between 1991 and 1994 were as follows: (a) Rupee devalued by 8 per cent on 1 July 1991, (b) Rupee devalued by 11 per cent on 3 July 1991, (c) The rupee made partially convertible in March 1992 in the trade account, with the introduction of the Liberalized (dual) Exchange Rate Management System, (d) The Foreign Exchange Regulation Act 1973 was amended in January 1993, (e) The dual exchange rate system of March 1992 unified. Rupee made fully convertible on the trade account in February 1993, (f) Full convertibility of rupee on the current account. Art VIII status of International Monetary Fund (IMF) attained in August 1994. In August 1994, the value of the rupee was 31.3 per US dollar. Since attaining current account freedom, the rupee almost continuously depreciated up to 2002 when it breached the 50 rupee to the dollar mark. Since then the two major periods when the rupee fell were the 2008–2009 period and the 2010–2011 period. In between, the rupee showed a reverse trend with fluctuations. On the other hand, since the early 1990s, the real value of export increased steadily. The expected relationship between the nominal exchange rate (NOMER) and exports in India thus appears to be obvious from casual observation.

In this article, we argue that the exchange rate affects exports through two channels. First is the direct effect: a depreciation of domestic currency makes domestic goods cheaper abroad and hence increases export (Belke & Polleit, 2009; Case & Fair, 2007). The other is the indirect effect of the exchange rate through the domestic price channel. Logically, the depreciation of domestic currency increases the prices of imported goods and hence domestic goods (Dadkhah, 2009; Daniels & VanHoose, 2005). If the imported goods are non-substitutable intermediate goods used in domestic production, then there is a further indirect effect via the rise in the price of the imported raw materials of domestic goods. Also, the resultant rise in export (due to depreciation of domestic currency) leads to a greater demand on the factors of production in a country raising their prices and hence the cost of production of all goods produced at home. Once domestic prices are affected, exports are in turn affected: a rise in domestic price leading to a lack of competitiveness abroad (Walter, 2014). It is thus necessary to explore the link between the exchange rate and domestic prices to understand to what extent the coefficient of the domestic price term also reflects exchange rate fluctuation.

The main issue of concern here is the problem of multicollinearity between domestic prices and nominal exchange (simple correlation is 0.95). Hence, they cannot be used as separate explanatory variables in the export demand function. To circumvent this problem, we use the ratio of domestic to foreign prices and the NOMER (as well as foreign GDP) in the export demand function. The correlation between NOMER and the price ratio is 0.18. Hence, the problem is solved (without any distortion of the export demand framework) once we integrate the two prices in terms of their ratio. In this article, we therefore interpret the indirect impact of the NOMER as follows: a significant relationship between the domestic to foreign price ratio and exports, and a significant pass-through of the NOMER to domestic prices.

We also argue in this article that we expect a differential effect of exchange rates during the appreciation and depreciation of the domestic currency (Cheung & Sengupta, 2013). For less developed countries such as India, a major part of its export consists of raw materials, intermediate goods and relatively lower quality consumer goods. Since a large number of countries in the world can export such goods, exporters of less developed countries face an acute competition in the international market. If this indeed is true, during the periods of depreciation of domestic currency, its benefits are expected to be passed on. This tendency towards passing on the benefits has aggravated in the recent years with the spread of Internet and other communication devices as the foreign importers become aware of the depreciation almost immediately as the depreciation occurs and demand the adjustment of export prices from the exporters. On the other hand, during the period of appreciation of the domestic currency, the export prices cannot be adjusted for the fear of losing to the competitors in the international markets. Thus, the response of export prices and hence volume of exports are expected to be quite different during the periods of appreciation and depreciation.

While a change in the level variable of exports can thus have asymmetric effect on its volume, export volatility affects the volume of exports through a completely different though more consistent route. Given the nature of export goods in India (primary, no value added, low quality), the risk associated with the volatility of the exchange rate has to be absorbed entirely by the exporters. In the periods of rapidly changing exchange rates, when the risk would appear to be too much for the exporter to shoulder, the obvious route is to hedge. However, hedging, especially in a country like India, can has its own perils, as any advantage that an exporter can have during the periods of depreciation can immediately be nullified through the hedging mechanism. Thus, if the possibility is large that the domestic currency will depreciate to a significant extent in the near future, it is optimum to the exporter not to hedge (Goyal, 2013), which means effectively that the entire risk of volatility once again shifts back to the exporters.

It is thus clear that both exchange and exchange rate volatility are expected to be important determinants of the volume of export for a country and exchange rates may influence exports both directly and indirectly through the channel of domestic prices. The objective of this article is to look at these relationships for the case of India from 1996 to 2014.

Though the aforementioned arguments hold true for any country in the world, we need a substantial degree of exchange rate fluctuation to capture the effects of its variation on exports. In India the exchange rate has fluctuated widely over time and there were periods when volatility was quite high. This makes India an ideal country to observe the effects of the fluctuation in the exchange rate. Second, India is still in a state of transition from a fixed exchange rate regime to a freely floating exchange rate regime; while flexibility in the current account has been achieved, complete flexibility in the capital account is yet to be achieved. Thus a look at the relationship between the exchange rate and export is a good case study as to how exports respond to exchange during the time of transition. Finally, there has always been a debate both among academicians and policymakers about the relative importance of price versus non-price factors (especially foreign income) on export demand. Dependence on the foreign income makes exports vulnerable to global business cycle fluctuations. Given the dip in India’s export during the 2008–2009 crisis, one suspects that foreign income is indeed an important determinant.

The effect of the exchange rate on exports depends on a plethora of issues. Two of the fundamental ones are (a) the extent to which the effects of exchange rate fluctuations are passed on export prices and (b) the nature of the contract that the exporters hold.

In India studies show both the presence and absence of link between exchange rates and exports. Joshi and Little (1994) found that price elasticity of demand for export was 1.1 in the short run and about 3 in the long run. Srinivasan (1998) found that relative prices were a significant export determinant in India. Veeramani (2007) found that due to the appreciation of the real effective exchange rate, the dollar value of India’s merchandise exports fell. However, Ghosh (1990), Sarkar (1994) and Sinha Roy (2011) reported that Indian exports are not necessarily price responsive and India’s export performance was not often led by movements by the exchange rate. These papers did not consider the regime shift due to the implementation of liberalization policy in their analysis. Bhattacharyya and Mukherjee (2014) considered the influence of breaks of trend curve during liberalization policy on India’s export. They found that the real effective exchange rate did not influence Indian exports at the aggregate level. Eichengreen and Gupta (2012) examined (a) whether the determinants of export growth rates and surges differ between merchandise, traditional services and modern services, and (b) whether the experiences of developing countries are different from developed countries, for the period 1980–2000 taking 66 countries. They found that the real exchange rate was an important factor for export growth. Cheung and Sengupta (2013) examined the effect of the real effective exchange rate on the share of exports of Indian non-financial sector firms for the period 2000–2010. They found a significant negative impact of currency appreciation and currency volatility on export shares of Indian firms. There is much concern regarding the pass-through of currency changes into domestic inflation in the developing countries. Dholakia and Saradhi (2000) examined the impact of exchange rate and exchange rate volatility on export–import prices and quantities using quarterly data for the period 1980–1996. Goldfajn and Olivares (2001) observed relatively high degrees of exchange rate pass-through in a number of emerging economies. Ghosh and Rajan (2007) estimated the exchange rate pass-through into consumer price index (CPI) for India from 1980 to 2005. Khundrakpam (2008) examined the behaviour of exchange rate pass-through to domestic prices for the period 1990–2005. Roy and Pyne (2011) estimated the exchange rate pass-through to India’s export prices.

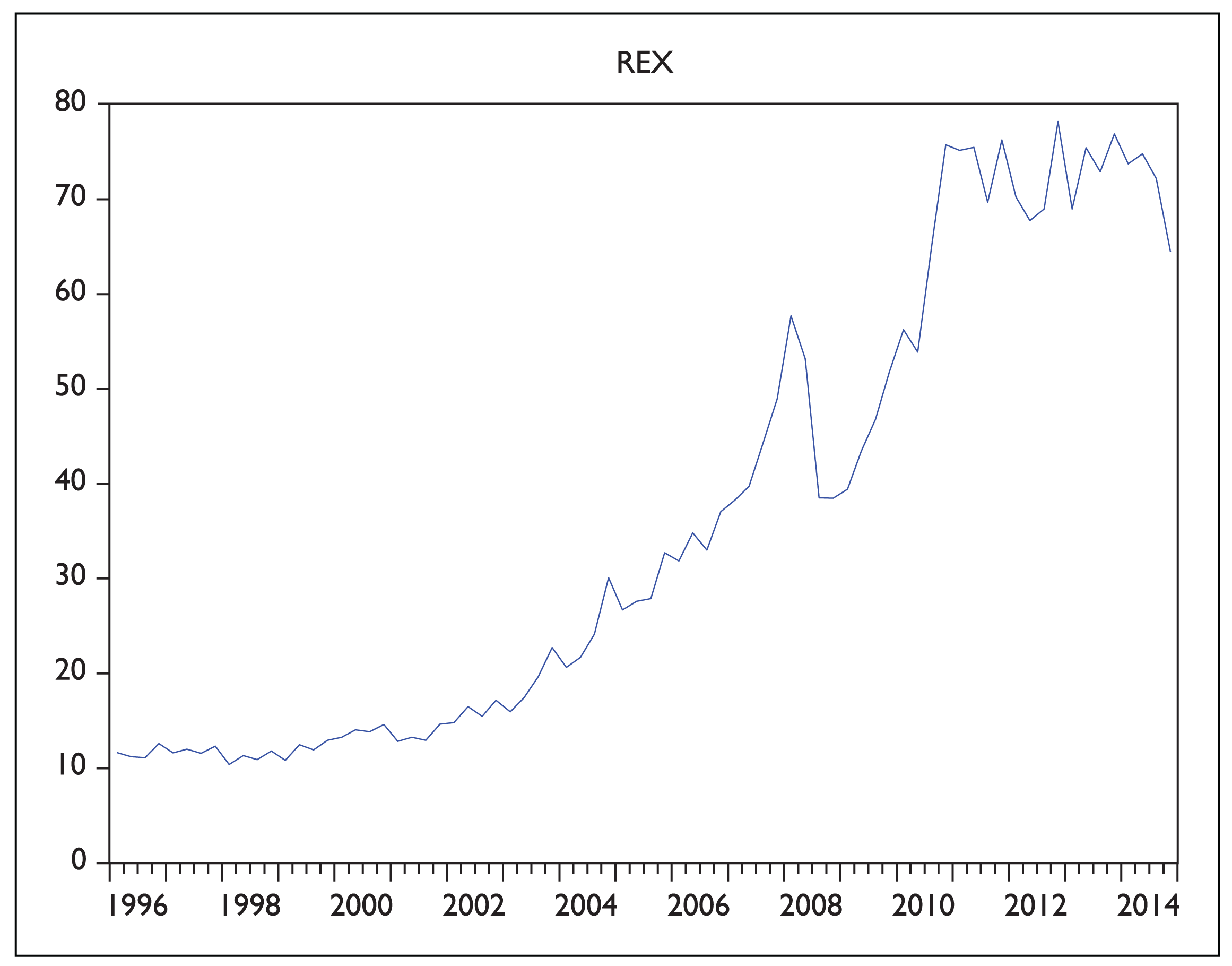

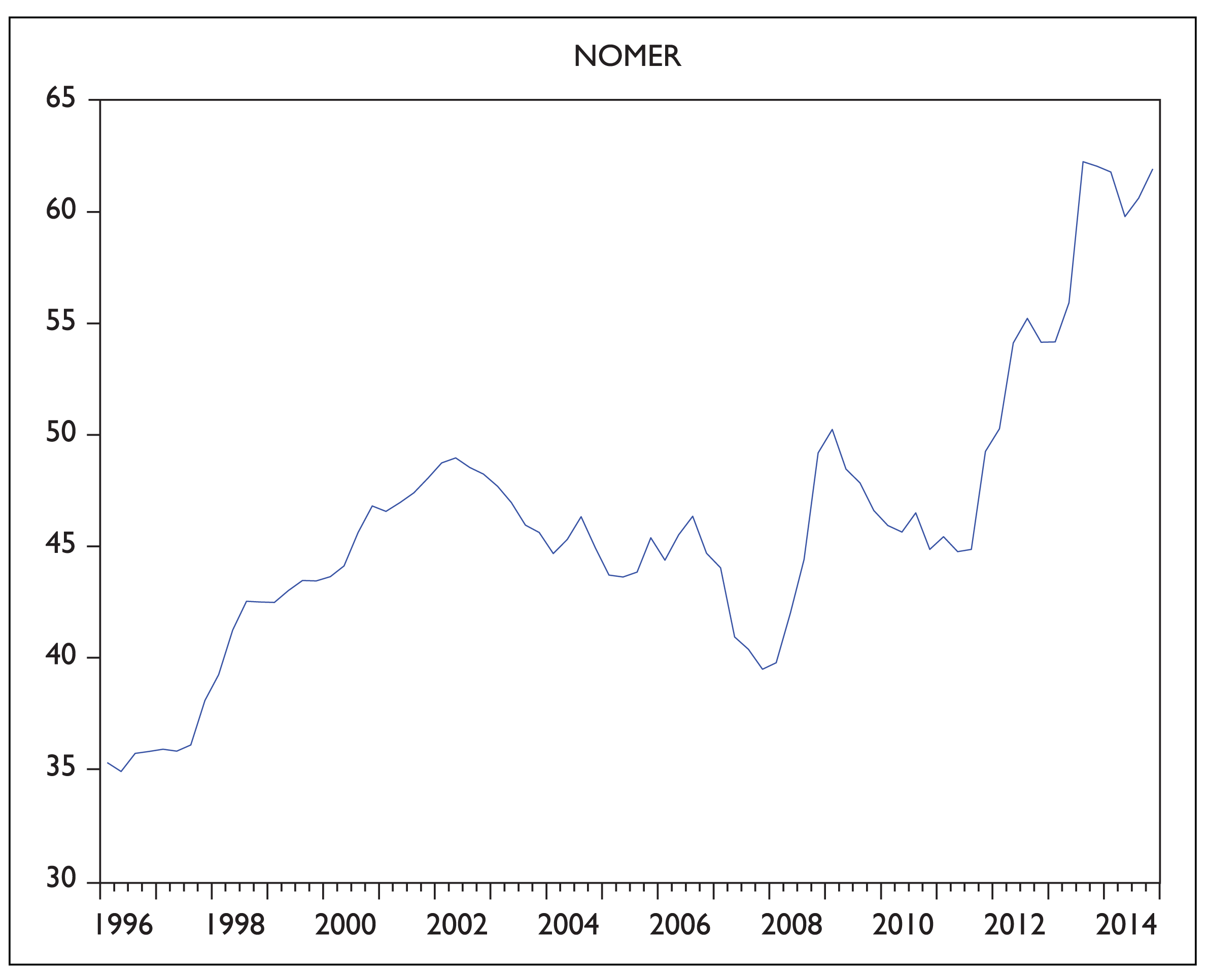

Unlike all the papers mentioned previously, we have used quarterly data to analyse the relationship between exports (Figure 1) and exchange rate (Figure 2) and exchange rate and domestic prices. Quarterly data provide a number of advantages over its annual counterparts: (a) quarterly data allow for important intra-year dynamics, (b) it provides a larger sample size and (c) it minimizes the likelihood of structural breaks. It is clear that all these factors are important in the present case. Exchange rate fluctuations are at a daily or even at hourly basis increasing the frequency of data to a quarterly level which implies that a lot more information can be processed all of which will be averaged out in the annual level. Also, since we do not consider structural breaks in the present analysis, quarterly data are expected to give more robust results than annual data. It should also be noted that since we look at both the direct and the indirect effects of the NOMER through domestic prices on export, we have integrated the findings of those writers who have found a significant relationship between the non-exchange rate price—variables and exports like Srinivasan (1998) and those who have found none or weak relationship between the exchange rate and exports.

The behaviour of the variables used in the regression analysis is shown in Figures 1–3. It is clear that the exchange rate depreciated and exports increased with fluctuations in the period covered here. Thus, some sort of relationship may be expected. Also, in this period, the domestic to foreign price ratio had a mildly negative trend implying that the second channel might have played some role in the story. Thus, the two channels considered here seem to have some a priori casual link from a simple visual examination of the data.

The article is organized as follows. The second section describes the data analysed in this study. The methodology adopted in this study is explained in the third section. The results are described in the fourth section. The conclusions of the study are made in the fifth and final section.

The Data

Data Sources

Nominal export data have been taken from the Reserve Bank of India (RBI). To make the data real (REX), we have divided it by India’s CPI. Three types of world GDP data have been used: un-weighted world GDP (WGDP), total trade weighted world GDP (TRGDP) and export weighted world GDP (EXGDP). In all cases the GDP of India’s 10 major import partners is used. The source for these data is the International Financial Statistics (IFS) and IMF. Total trade and export data are taken from the Organization of Economic Cooperation and Development (OECD) database. Quarterly GDP data for Saudi Arabia and the United Arab Emirates are not available. We have used the cubic interpolation method for conversion from yearly to quarterly data. The domestic CPI data are taken from the RBI database. The unit value index of export has been used as a proxy for foreign price. These data are also taken from RBI. Since these data are also yearly, the same interpolation method was used to transform it to quarterly data. The NOMER data have been taken from IFS, IMF. For the analysis of exchange rate pass-through, the producer’s price index (PPIW) has been taken from the OECD database. The PPIW data were annual for the same countries for which the GDP data were annual and the same method of interpolation was used to transform it to quarterly data.

Determination of Volatility

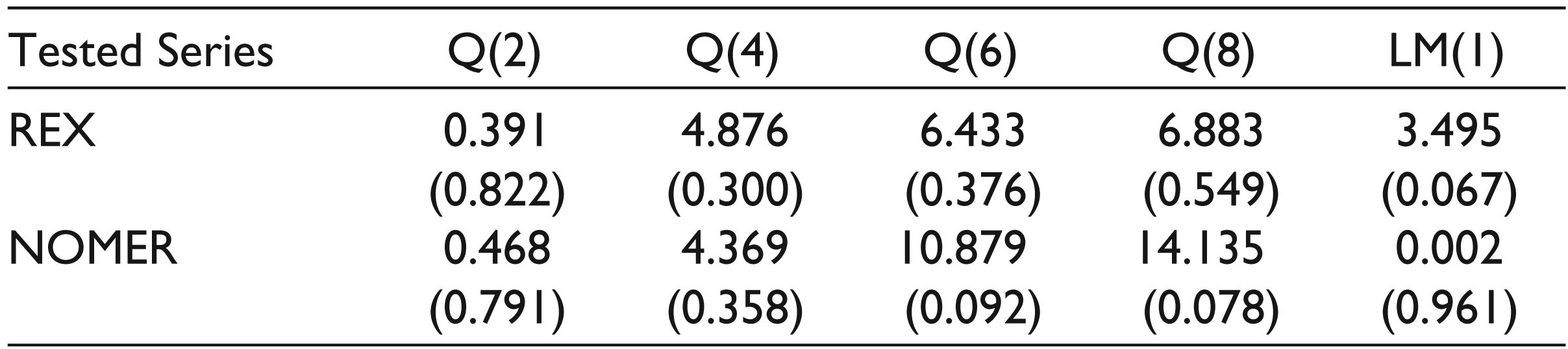

To measure volatility in REX and NOMER series, we conducted the tests for serial correlation and autoregressive conditional heteroscedasticity (ARCH). We have estimated the residuals of the AR(2) process of both series according to the Akaike Information Criteria (AIC) and performed the Ljung–Box test for the serial correlation and Lagrange multiplier (LM) test for ARCH. The Q-statistic at lag k, a test statistic for the null-hypothesis that there is no autocorrelation up to order k, is computed as

where τj is the jth autocorrelation and T is the number of observations. In the ARCH LM test, we assume that the variance of the error term of a regression process follows an ARCH(p) process:

The null-hypothesis is that there is no ARCH effect present:

The LM statistic = (n – p)R2 is computed, and if LM > χ2 for a given level of significance, we reject the null-hypothesis of no ARCH effect.

Table 1 shows the results. The Q-statistics for REX series at lags 2, 4, 6 and 8 are 0.391, 4.876, 6.433 and 6.833, respectively, with p-values 0.822, 0.300, 0.376 and 0.549. Thus, the null hypothesis that there is no autocorrelation is not rejected. The Ljung–Box test for the NOMER series shows that the residuals are not serially correlated. The LM test statistics for the REX and NOMER series on the squares of the residuals are 3.495 and 0.002 with p-values 0.067 and 0.961, respectively. The null-hypothesis that there is no ARCH effect in REX and NOMER is not rejected. The optimum lag length on the basis of the AIC for the ARCH LM test was found to be 1 for both the REX and NOMER series.

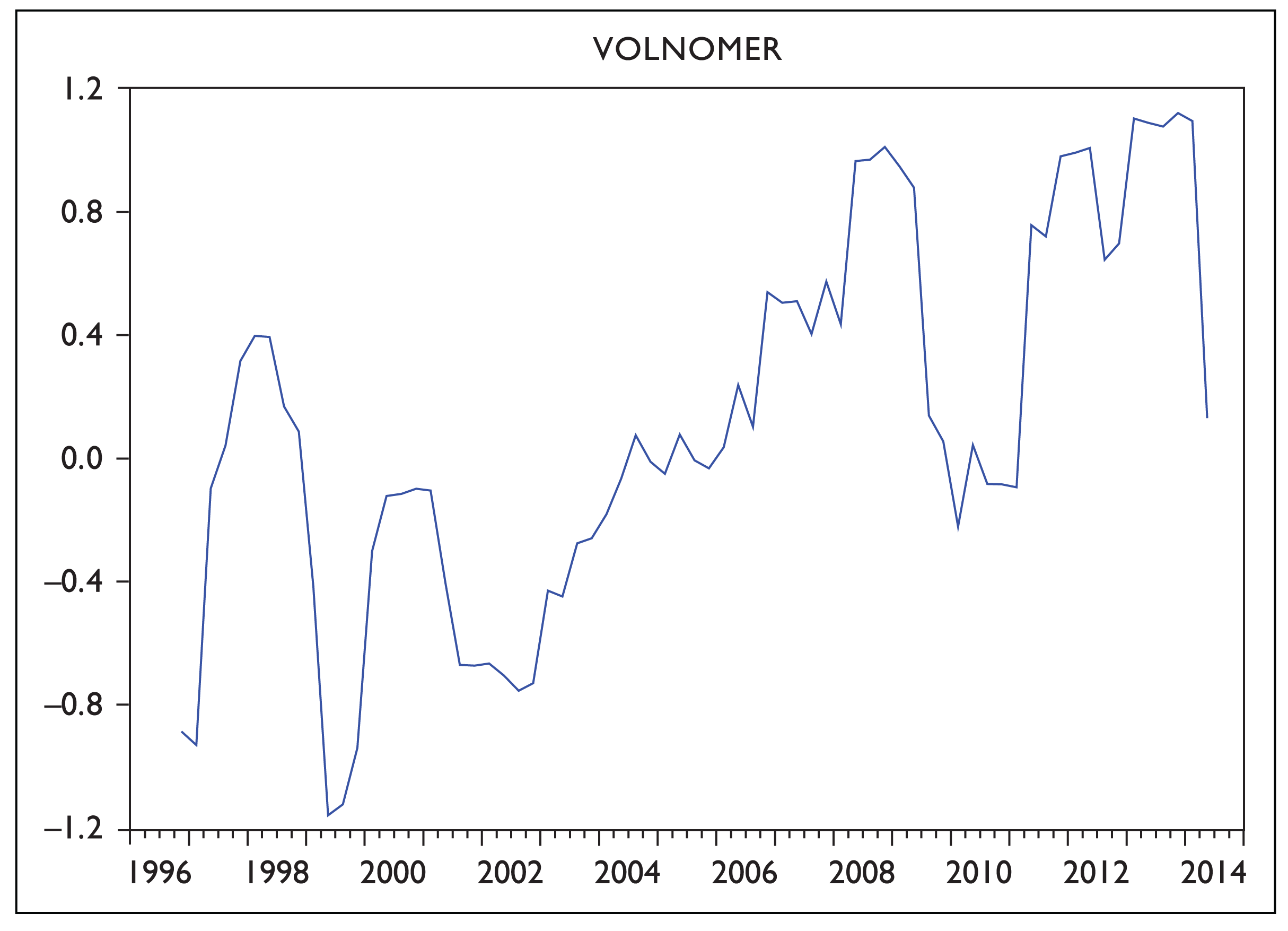

Given that there is no ARCH effect of the quarterly data on export demand and the exchange rate of India for the studied period, we need other operational measures of the volatility of the exchange rate and export demand. Following Arize, Osang, and Slottjje (2000), we use a time-varying measure of exchange rate volatility in the form of moving sample standard deviation, expressed as

where X is the natural logarithm of the seasonally adjusted NOMER and export demand of India, m is the order of moving average, in our study m = 7. The advantages of this method are explained in the study of Baba, Hendry, and Starr (1992). A similar measure has been used to measure the volatility of the exchange rate by Kenen and Rodrik (1986), Koray and Lastrapes (1989) and Chowdhury (1993). The moving standard deviation of the NOMER is denoted as VOLNOMER. The volatility of the NOMER (VOLNOMER) is shown in Figure 4.

Test for Serial Correlation and ARCH

Stationarity

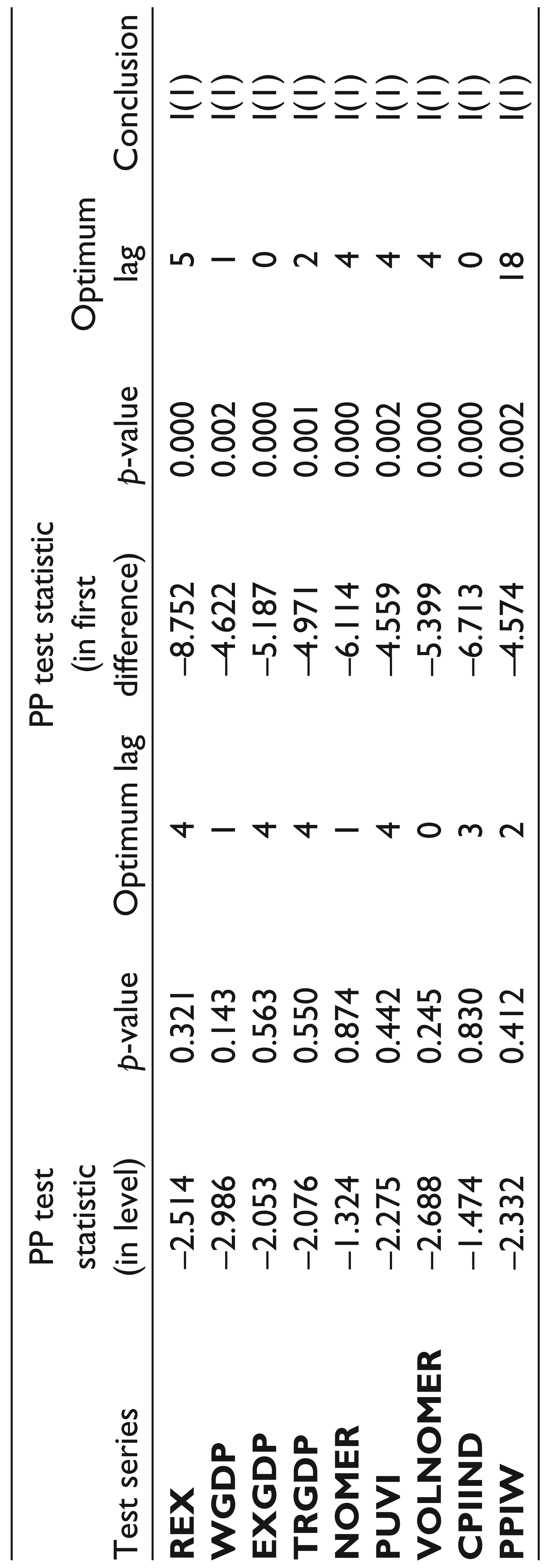

Tables 2 and 3 show the result of the unit root tests. We have used both the augmented Dickey–Fuller (ADF) test (Dickey & Fuller, 1979) and Phillips–Perron (PP) test to determine the stationarity of a variable. The optimum lag length is determined on the basis of the AIC for the ADF test, and for the PP test, the lag is selected on the basis of the recommendation of Newey and West (1994).

From the earlier tables, we can see that all the series are integrated for order 1.

Model Specification and Methodology

The export demand function is specified as follows:

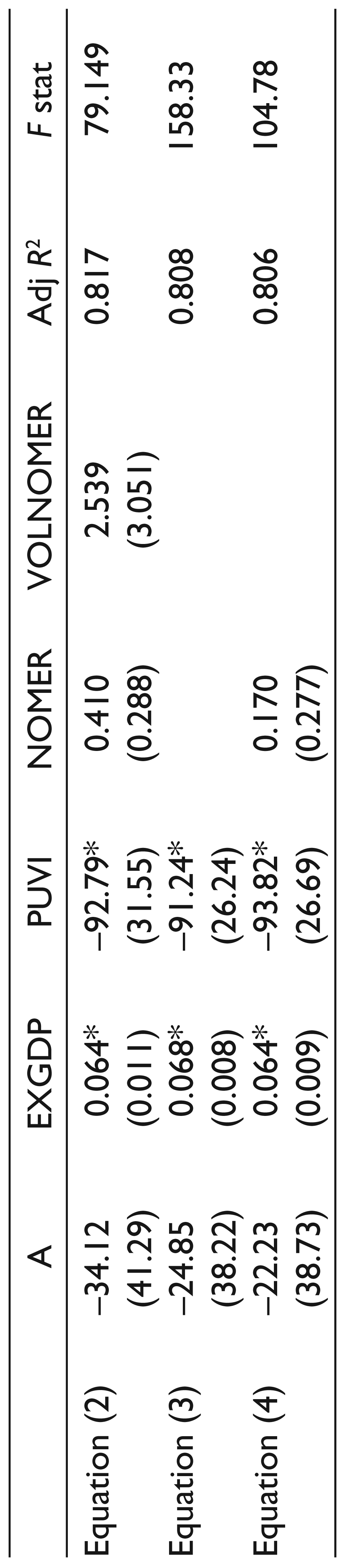

where REX is real export, EXGDP is export-weighted GDP, PUVI is the ratio of domestic price to price of exports, NOMER is the nominal exchange rate of India and VOLNOMER is the volatility of the NOMER. A theoretical foundation for such an equation can easily be given. The normal method for such a foundation is to model the home country’s export demand function as an import demand function of the foreign country (see Senhadji & Montenigro, 1998). The second option for deriving the export demand function for the foreign country is to use the production approach (see Diewert, 1986). An extension to the approach is to derive the export demand function as the first derivative of the profit function of the exporter with respect to price.

We start with the estimation of the export demand function of India for the period of Q1:1996 to Q4:2014. A step-by-step procedure is then followed to test for the robustness of the NOMER variable:

Results of the Unit Root Test (ADF Test)

Results of the Unit Root Test (PP Test)

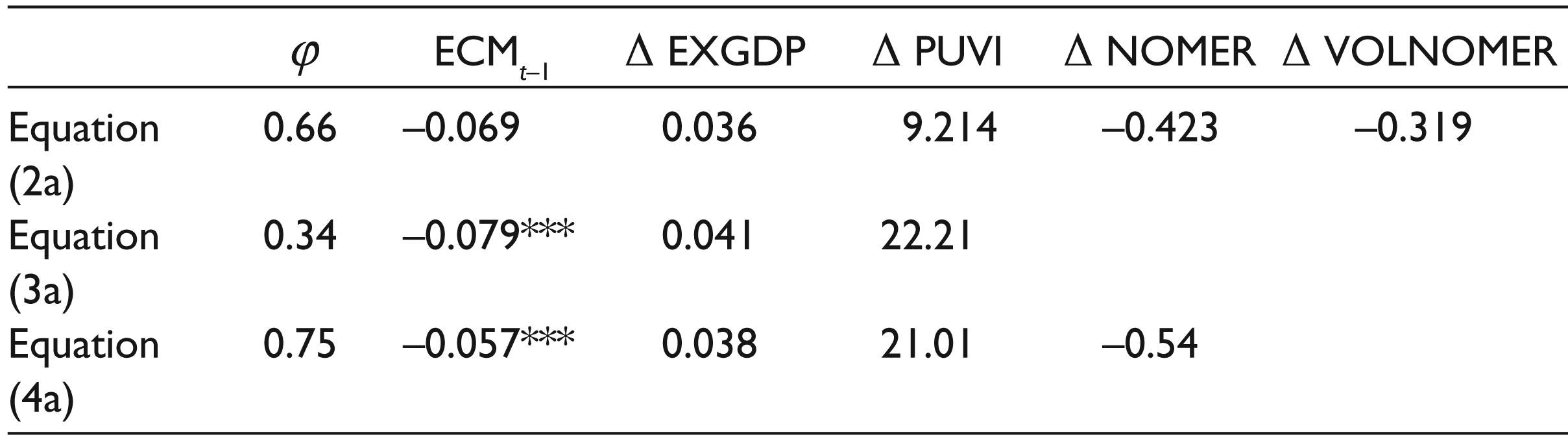

Provided the variables cointegrate, the next step is to determine the error correction mechanisms (ECM) for each equation. These are specified as

To distinguish between the effects during appreciation and depreciation, we have used the following specification of Equation (3):

where D1 is the dummy for an appreciation of NOMER and D2 is the dummy for the depreciation of NOMER.

The extent of exchange rate pass-through into domestic prices is estimated as follows:

where the control variables represent cost conditions of exporting country and demand conditions for importing nation (see Ghosh & Rajan, 2007). Quarterly GDP data have been used for representing the demand condition of importing nation’s market. The exchange rate pass-through elasticity is given by the coefficient β1. If β1 = 1 we have complete exchange rate pass-through and if β1 < 1, we have partial pass-through.

Since the variables of Equation (6) are cointegrated, there exists an ECM for the equation. This is specified as

The coefficient γ1 suggests how fast any deviation from the long-run equilibrium is adjusted in the short run. γ2 shows the short-run exchange rate pass-through.

Results

The estimated results of Equations (2), (3) and (4) are shown in Table 4. First, the residuals in all equations are stationary at the 5 per cent level of significance and hence the variables cointegrate. PUVI and EXGDP are statistically significant, though NOMER and VOLNOMER are insignificant. Clearly, therefore, NOMER has no effect on India’s export demand. The factors affecting export demand are foreign income and relative price.

The ECM results are shown in Table 5. First, note that short-run elasticities are all zero and the model adjusts to equilibrium in the same period (at least at the 5% level of significance).

In order to judge the effect of the appreciation and depreciation of real exchange rate on the amount of export, we have identified the quarters in which the real exchange rates have appreciated or depreciated with respect to the preceding period and used the slope dummies to measure these effects (Table 6). Both these dummies are insignificant. Coupled with observations made earlier, we can thus conclude that (a) NOMER and its volatility does not affect exports in India and (b) this is true both for appreciation and depreciation episodes in the NOMER.

The result of the regression for the exchange rate pass-through to domestic is shown in Table 7. The elasticity of exchange rate pass-through is found to be 54 per cent for the period of 1996:Q1 to 2014:Q4.

The residuals of the earlier equations are stationary. Thus, there is long-run equilibrium relationship among the variables in this equation. We examined the short-run pass-through of exchange rate changes into India’s CPI by using the error correction model (Table 8). The error-correction term suggests that any deviation from the long-run equilibrium is adjusted by about 7.8 per cent in the short run. The short-run exchange rate pass-through to domestic prices is 28 per cent.

Thus, even though there is no direct relationship between the NOMER and exports in India, a depreciation of NOMER by 1 per cent increases domestic prices by 0.54 per cent. Since an increase in domestic prices depresses export, thus, in our model there are two main channels through which price factors affect export: (a) through a direct change in PUVI and (b) and indirect change in PUVI brought about by a change in NOMER. Apart from this, foreign income is an important non-price determinant of exports.

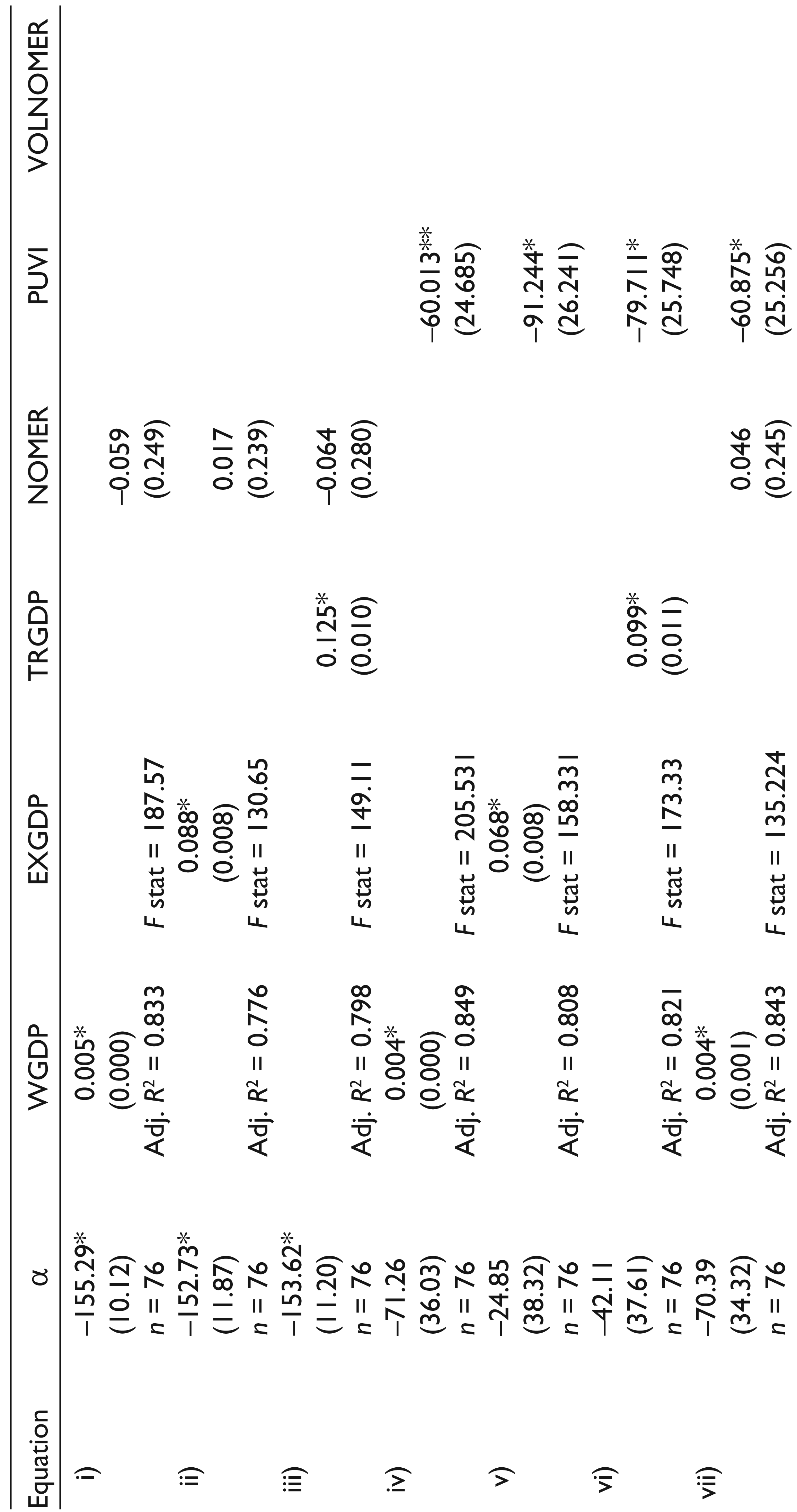

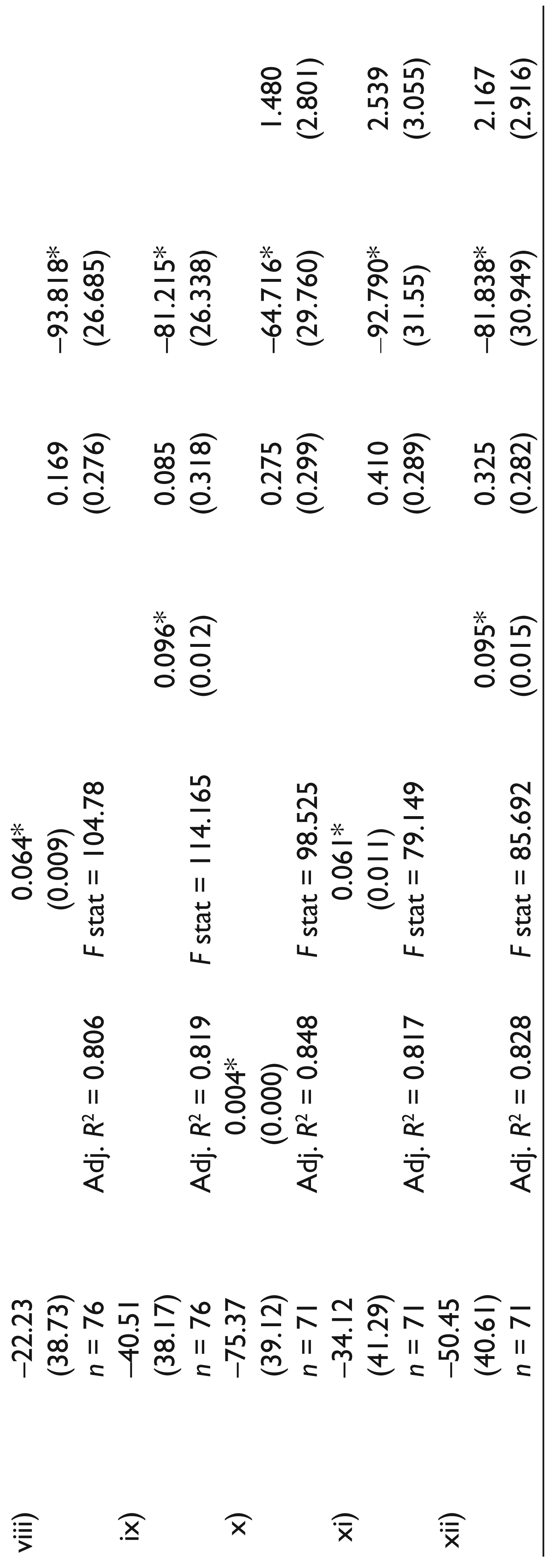

Finally, we conduct some robustness exercises in Table 9. It can be seen that our results are robust to all kinds of model specifications with variables being included and deleted step by step. In all cases, the relative price is statistically significant and the NOMER is statistically insignificant.

The Estimates of Regression Equations (Dependent Variable: Real Export)

Error Correction Mechanism Specification

The Estimates of Regression Equations (Dependent Variable: Real Export)

The Estimation of Regression Equation (Dependent Variable: CPI of India)

Error Correction Specification

The Estimates of the Regression Equation (Dependent Variable: Real Export Demand)

There is mixed international evidence regarding the importance of exchange rate in explaining exports. For instance, significant relations between the NOMER and export were found in China (Zhang & Liu, 2012), South Africa (Poonyth & Zyl, 2000) and Malaysia (Wong & Tang, 2011), while exchange rate was found to have no relationship with export in Singapore (Fang & Miller, 2007), Jordon (Sweidan, 2013) and Ireland (Fountas & Bredin, 1998). As we have noted previously, the evidence for India is also mixed. Note that most of these exercises were addressed towards the relationship between real (rather than NOMER) and export. Since PUVI is statistically significant in this article, there is a possibility for the real exchange rate to be an important determinant in this period as well. However, when exporters and policymakers talk about exchange rate they usually mean nominal rather than the real exchange rate. The point that this article makes is that even though the exchange rate when multiplied by relative prices might be an important determinant of export, it fails to remain so when the price term is separated from it. Thus, the popular notion that the exchange rate affects exports is not validated for the kind of data that we are considering in this article.

Conclusion

Does exchange rate affect exports in India? In this article, we have analysed this question by using quarterly data from 1996 to 2014 in an export demand setting. We have found no direct evidence that the NOMER or its volatility influences exports. However, there is a significant relationship between the domestic price ratio and exports. Taking the cue from there, we have attempted to estimate whether there is any chance that the NOMER influences the domestic price and hence affects exports indirectly. We find strong evidence in this regard in the sense that the pass-through of the NOMER on prices is as much as 54 per cent in the long run (28% in the short run). Thus, there is a distinct possibility that the NOMER affects exports indirectly through the domestic prices.

The policy implications for such a finding are clear: even though there are often demands for the exchange rate targeting to boost exports during times of appreciation, there is no direct evidence that such a policy will yield the necessary outcome. The government should target domestic inflation instead in order to boost exports. Since the indirect effect of the exchange rate occurs through domestic prices, inflation targeting will take care of any such indirect effect of the exchange rate as well. Finally, however, the importance of foreign income looms large over India’s export. The sudden decline of India’s export in 2008–2009 is thus the manifestation of a deeper phenomenon: the vulnerability of India’s exports to the state of the world economy.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.