Abstract

The present study investigates the relationship between working capital management and SME profitability. It also analyzes the impact of macroeconomic impulses on firm profitability through efficient management of working capital in the case of Indian small and medium scale enterprises over the time period spanning from 2010 to 2017 using Feasible Generalized Least Square (FGLS) regression models. The study concludes the negative relationship of account receivables together with a positive relationship of inventories and account payables with SME profitability. It implies the firm managers can maximize SME’s profitability by converting the credit sales to cash as early as possible, by increasing the days of accounts payable and following a conservative inventory management strategy. Changes in economic growth and commercial bank advances to small scale industries are the key macroeconomic determinants that are impacting SME profitability. The results from this paper may guide the firm managers to shape their working capital management strategies to maximize profitability. Policymakers may find the study interesting to identify the macroeconomic parameters that significantly influence Indian SMEs.

Introduction

Smith (1980), emphasizes the role of working capital on firm profitability, risk and consequently on its value. The working capital management has gradually gained importance due to its contribution to shareholder’s value that maintains a tradeoff between profitability and risk (see Banos et al., 2010; Kieschnick et al., 2013; Lazaridis & Tryfonidis, 2006; Nazir & Afza, 2009; Ukaegbu, 2014). According to Aktas et al. (2015) and Yunos et al. (2015), efficient working capital management (WCM) helps in reallocating underutilized resources to generate higher-value that can lead to the enhancement of firm’s performance and can help in increasing profitability without resulting in liquidity problems. These studies have the privilege of analyzing large firms with all the necessary physical resources as well as managerial and intellectual ability to manage their working capital requirements. However, the growth of small and medium scale enterprise (SMEs) is hindered by issues such as poor infrastructure, inadequate market linkages, lack of access to institutional finance, poor management and lack of advanced technology (See Abor & Quartey, 2010; Pansiri & Temtime, 2008; Saleh & Ndubisi, 2006). At the same time some selective studies specific to SMEs like Varaporn and Kiattichai (2018), find a positive impact within industry diversification on the performance of SMEs in emerging markets. Yuan and et al. (2016) find the firm-level features like revenues, profitability, competitive position and future prospects of SMEs play a dominant role in determining the nature of the strategic decisions of SMEs. And according to Alexander et al. (2017), operational and governance improvements are the common value creation measures in all buy-outs of SMEs.

These are some experiences about issues and challenges of small and medium scale enterprise across the globe. The present study will bridge the research gap in WCM literature by providing empirical evidence on the relation between WCM and SME profitability in the case of Indian SMEs and also analyze the impact of macroeconomic inputs on their profitability. So far no such evidence is available in prior literature despite the fact that SMEs are the backbone of not only the Indian economy but also for developing as well as developed countries (Kumar & Rao, 2015).

The present study has two main focuses. Firstly, it aims to investigate the relationship between working capital management and SME profitability. Secondly, it attempts to analyze the impact of macroeconomic impulses on firm profitability through efficient management of working capital. The study contributes to the literature in several ways. Firstly, the study is undertaken on the constituents of the Bombay Stock Exchange (BSE) SME IPO index that are listed as SMEs in the Indian stock market. Secondly, the study tries to capture the impact of all the components of working capital management and macroeconomic impacts on SME profitability. Thirdly, the study uses a feasible generalized least square estimator to handle within sample unobservable heterogeneity.

The paper is structured in the following manner. Section 2 presents the theoretical background of the study. Section 3 presents a methodological approach and research methods, section 4 presents data analysis, section 5 presents findings of the study, section 6 concludes.

Theoretical Background and Review of Earlier Studies

Theoretical Background Between Working Capital Management and Firm Profitability

Looking at the relevance of WCM on firm profitability, all the components of working capital management need to be analyzed independently and the study intends to do that.

Accounts Receivables (AR) and Profitability

The relevance of AR on profitability is analyzed by several studies (Banos–Caballero et al., 2014; Peel et al., 2000) and its nature of relationship depends on aggressive or conservative policy adopted by the firms (Garcia-Teruel & Martinez-Solano, 2007; Nazir & Afza, 2009; Tauringana & Afrifa, 2013). An aggressive policy followed by a lower accounts receivable period may increase profitability via increasing cash flow that ultimately increases the current asset and liquidity level of the firm. It increases their creditworthiness and protects the firms from liquidity crunch and financial distress (Arena & Julio, 2010). Timely payment of current liability also increases stakeholders’ and suppliers’ confidence which translates to larger commercial benefits in the long run. According to the transactional cost theory on the trade credit of Ferris (1981), firms can increase their operational efficiency by reducing transaction costs by decreasing the account receivable period. Hence the reduction of AR will lead to profitability (Bhattacharya, 2008; Nelson, 2002). On the basis of the above discussion, the present study has identified the following hypothesis to test.

Hypothesis (H1): Whether there exists a negative relationship between account receivables and profitability.

Accounts Payable and Profitability

Accounts payable stands to be the second most relevant determinant of WCM. It has both positive and negative effects on firm performance (Banos-Caballero et al., 2014). According to Ferris (1981), transactional cost theory accounts payables increase the operational efficiency of firms through the reduction of transaction costs caused by delaying payments (i.e. increasing of days of accounts payable period). In line with transactional cost theory, Nelson (2002), Bhattacharya (2008), and Sharma and Kumar (2011) find a positive relationship between accounts payables and profitability. It implies that firms are able to increase their profitability through reducing transactional costs of bills payment by delaying payments or by increasing payable days. Whereas, Laziridis and Tryfonidis (2006), Garcia-Jeruel and Martinez-Solano (2007), and Samiloglu and Demrigunes (2008) find a negative relationship between accounts payable and firm profitability. On the basis of the above discussion, the present study sets its hypothesis on the basis of transactional cost theory.

Hypothesis (H2): Whether there exists a positive relationship between account payables and profitability.

Inventory Management and Profitability

Inefficient inventory management could lead to a reduction in firms’ productivity, efficiency and hence profitability (Ching et al., 2011; Eroglu & Hofer, 2011; Gill et al., 2010; Mathuva, 2013). Firm managers can follow either an aggressive or a conservative strategy of inventory management to maximize profit. Holding a lower amount of inventory is considered an aggressive inventory management strategy whereas holding a higher level of inventory is considered to be a conservative strategy. Holding lower inventory through aggressive strategy may increase profitability due to the reduction of holding cost (Garcia-Teruel & Martinez-Solano, 2007; Laziridis & Tryfonidis, 2006; Nazir & Afza, 2009; Tauringana & Afrifa, 2013). It is further justified by the “Just-In-Time” (JIT) theory of inventory management. Accordingly, Banos-Caballero et al. (2010) and Chen et al. (2005) found a significantly negative relationship between inventory and profitability. Contrary to this, the precautionary, speculative and transactional motive theory of holding inventory stands in favor of conservative inventory management strategy and suggests that companies keep inventory as a precaution against the situation of stock out (Bhattacharya, 2008). In a similar line, Blinder and Maccini (1991) and Corsten and Gruen (2004) have favored holding of larger inventory and stated its positive impact on profitability. Nevertheless, it also increases holding and financing costs (Kieschnick et al., 2013), which may lead to high-interest expenses and higher credit risk (Aktas et al., 2015). The above findings of inventory management strategies and their impact on firm profitability will be more appropriate for large firms. But in the case of SMEs, it will be quite preliminary to set the hypothesis for the firms who are suffering from poor infrastructure, inadequate market linkages and lack of access to institutional finance. Therefore, the present study would like to test the following hypothesis by drawing an implication for SMEs and set the hypotheses as follows;

Hypothesis (H3a): Whether an aggressive Inventory management strategy with a minimum stock of inventory will support SME profitability.

Hypothesis (H3b): Whether a conservative Inventory management strategy with more stock of inventory will support SME profitability.

Working Capital Management and Firm Profitability

Earlier studies have analyzed the relationship between overall working capital management (WCM) and profitability under different aspects of the economic environment and also in different industry aspects (Koumanakos, 2008, Panda and Nanda, 2018). Some of the studies such as Karaduman et al. (2011) and Alipour (2011) have found a negative relationship between working capital management and profitability; whereas Lazaridis and Tryfonidis (2006) and Stephen and Elvis (2011) has found positive relationships. These studies leave the firm managers indecisive by providing mixed results and most of the findings are for large firms. Therefore, the present study has attempted to analyze the relevance of WCM on firm profitability for Indian SMEs and set the hypothesis as follows.

Hypothesis (H4a): Whether there is a positive relationship between working capital management and SME profitability.

Hypothesis (H4b): Whether there is a negative relationship between working capital management and SME profitability.

Research Methodology

To establish the relationship between working capital management (WCM), macroeconomic shocks, and firm profitability for Indian SMEs, the present study has estimated a set of models. The basic model in equation–1 explains the above-mentioned three key components, which include various components of working capital management, macroeconomic effects, and firms’ specific control factors for capturing their effects on profitability.

Working Capital Management and Firm Profitability

The effects of working capital management on SME’s profitability are captured by the following models. The models are primarily developed on the conceptual basis of working capital and are subsequently expanded on the empirical grounds of the existing literature. Each component of working capital management is estimated separately. Following the studies of Aktas et al. (2015), Pais and Gama (2015), Enqvist et al. (2014), Tauringana and Afrifa (2013), Net Working Capital Cycle (NWCC) has been used as the single entity to represent working capital management for capturing its overall impact on profitability.

Firm size, growth, debt, and liquidity are used as control variables to increase the predictive ability of the model.

Effect of Macroeconomic Impulses on Working Capital Efficiency

The present study has attempted to capture the effects of macroeconomic policy on the profitability of Indian SMEs. We have considered the growth rate of the economy to incorporate the impact of the business cycle. Since the Government of India has taken up many initiatives and special policies to prioritize the sector’s development, the public sector has planned the outlay in the annual budget for industries, which has been considered to capture the impacts of the designed policy on the performance of SME. Similarly, the commercial bank makes advances to small scale industries, and the changes in interest rates capture money market impacts; and the changes in exchange rate addresses the open economy shocks to SME’s profitability. Equations 6 to 9 are designed to capture the impacts of macroeconomic shocks on working capital management of SMEs. All the macroeconomic variables are lagged by a single period to handle the possible issue of simultaneity in econometric modeling. Moreover, policy variables function with a time lag, and the existence of control variables helps in improving the overall level of significance as well as the goodness-of-fit for all the models. The models are explained below.

The above models are being estimated by using Feasible Generalized Least Squares (FGLS) Estimators. The FGLS estimator is simply the OLS estimator applied to a transformed regression that purges the heteroscedasticity and/or autocorrelation. However, if the model of heteroscedasticity and/or autocorrelation then FGLS is asymptotically unbiased, efficient, and consistent.

Data Analysis

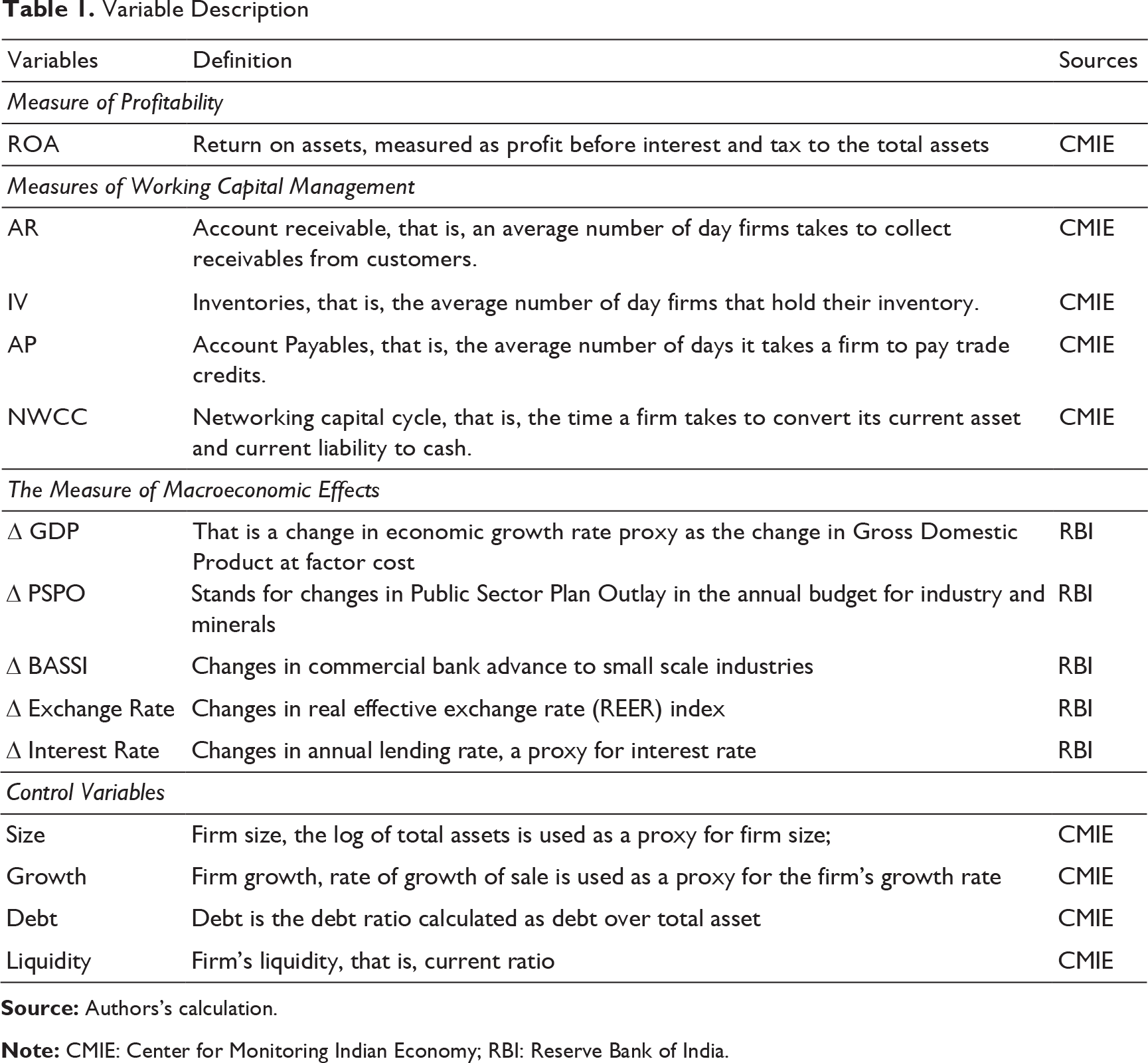

Variable Description

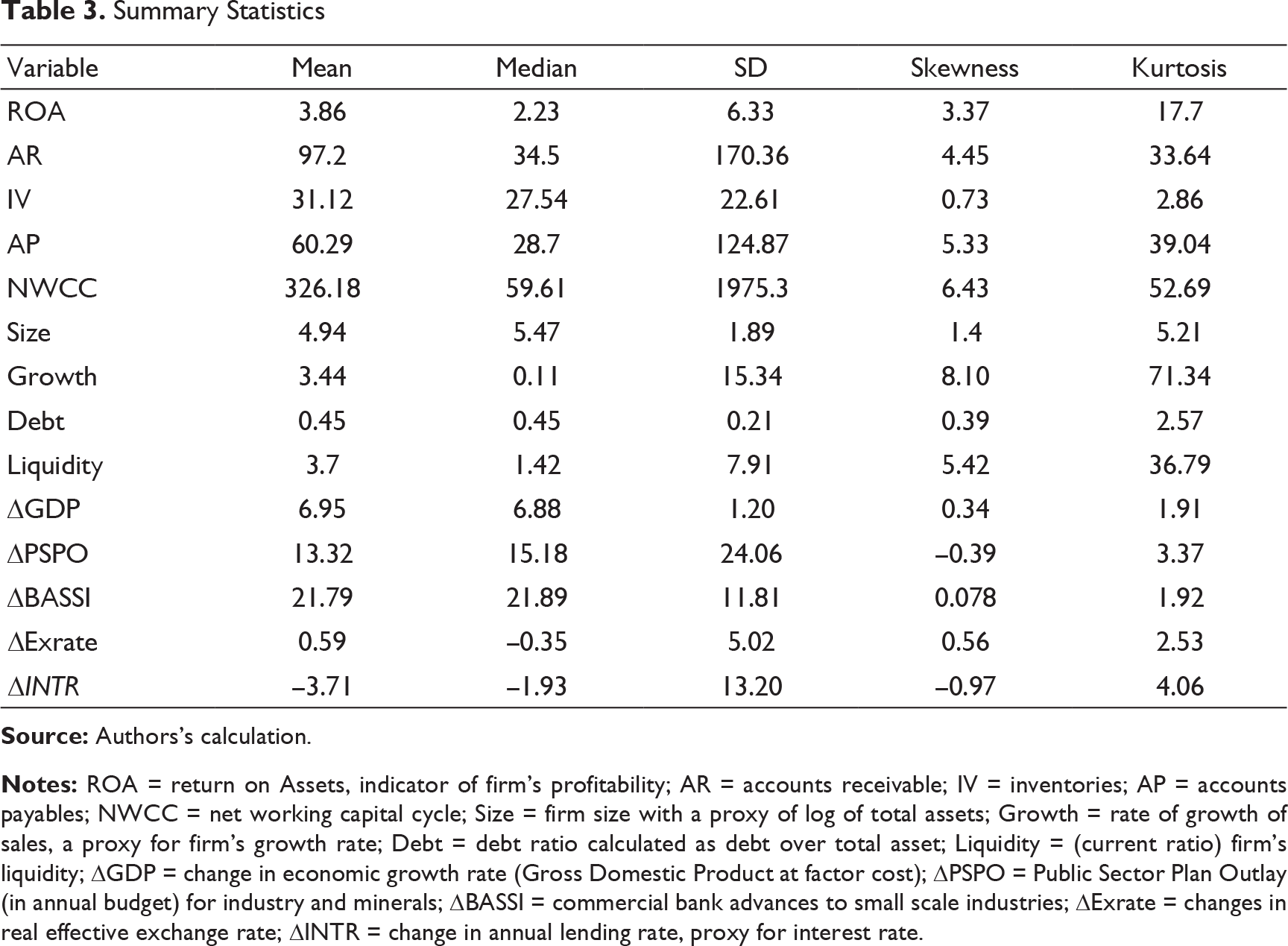

Summary Statistics

Table 2 reports the pair-wise correlation coefficients with their respective level of significance. Among the firm-specific factors, profit is negatively and significantly correlated with account receivable, NWCC, size, and growth. Among the macroeconomic indicators, profit is positively and significantly correlated with economic growth. The parameters of working capital management are experiencing an insignificant correlation with the changes in macroeconomic impulses, whereas the firm-specific control variables like size, growing debt, and liquidity have shown some significant correlation. The size of SMEs shows a significant negative correlation with the changes in the advances made by a commercial bank to small scale industries and their positive correlation with the changes in the exchange rate. The growth of Indian SMEs is significantly and positively correlated with the changes in public sector plan outlay in the annual budget for industry and by the changes in the exchange rate. Similarly, debt and liquidity positions are positively correlated with the changes in the advances made by the bank to small-scale industries. The study finds evidence about the significant impacts of macroeconomic policy variables on the key performance parameters of Indian SMEs, particularly those that are expected to influence profitability and working capital management cycles of the firms.

. Correlation Coefficients of Firm-specific Variables Used in the Study

Summary Statistics

Findings of the Study

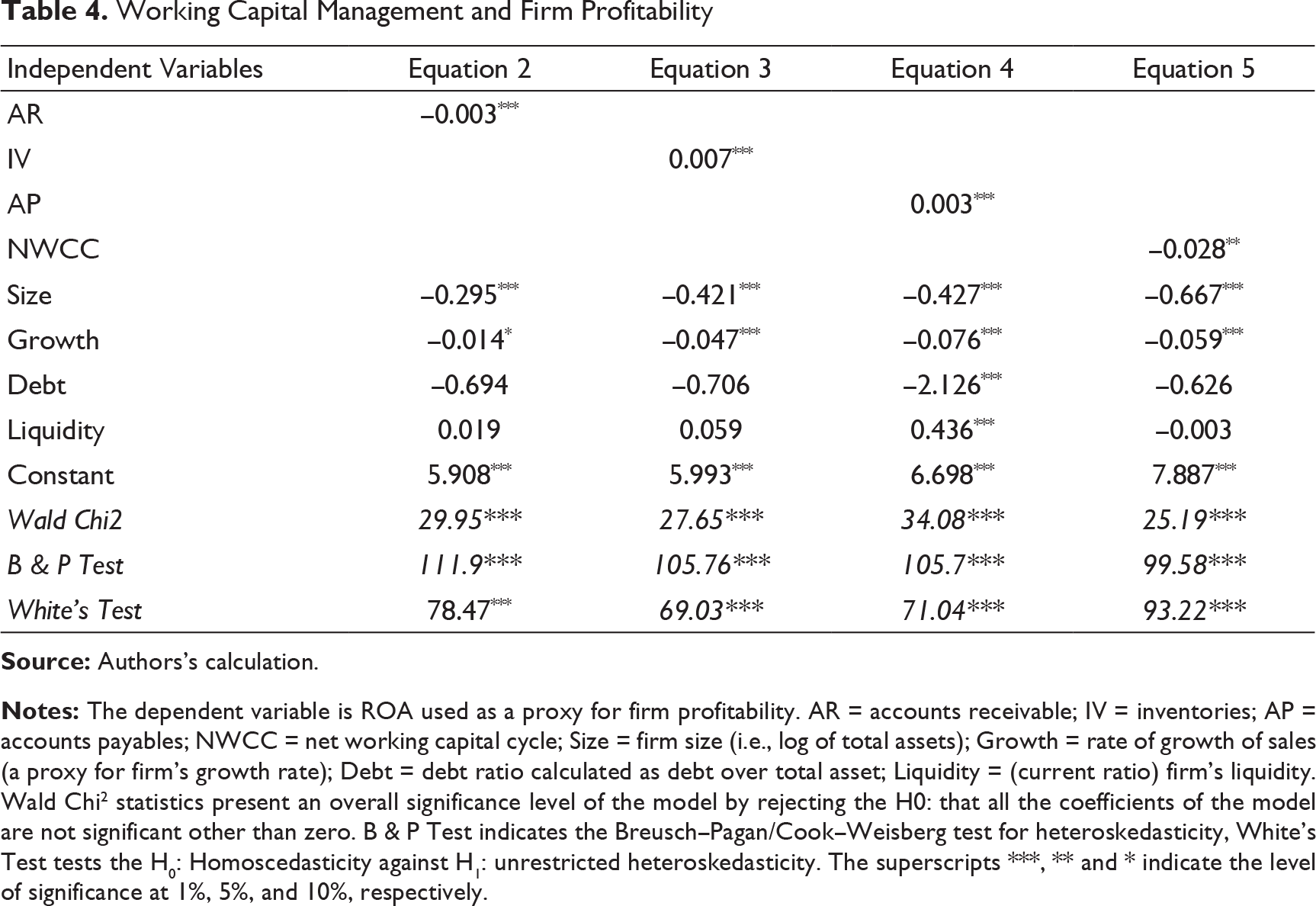

Working Capital Management and SME Profitability

Working Capital Management and Firm Profitability

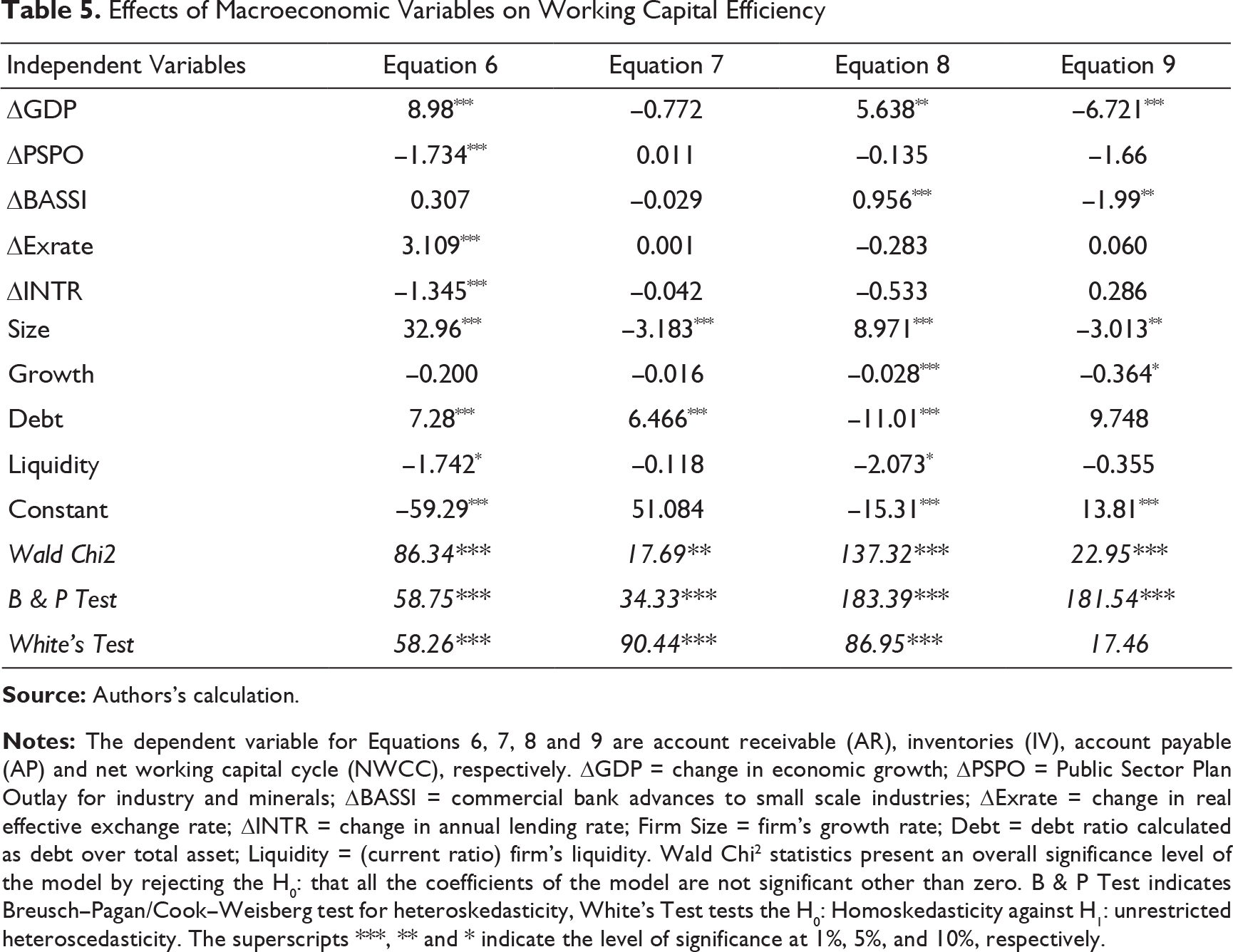

Effects of Macroeconomic Variables on Working Capital Efficiency

Effects of Macroeconomic Variables on Profitability via Working Capital Efficiency

In this part of the study we are trying to analyze the effects of macroeconomic policies on SMEs profitability through the channels of WCM by estimating equations 6, 7, 8 and 9 and the estimated results are presented in Table 5. In this section, the study aims to explore the relationship of macroeconomic parameters with the components of WCM and then using the finding of our 1st objective discussed in section 5.1, we will analyze the implied relationships of macroeconomic parameters with SME profitability and will validate the hypotheses. The relation between macroeconomics variable is WCM are analyzed through the channels of account receivable, stock of inventory accounts payable and networking capital cycle. Economic growth is expected to have a positive impact on SME profitability. An increase in GDP is significantly increasing AR which intern decreases profitability and hence we fail to accept the hypothesis. Change in GDP is positively impacting AP and hence can boost SME profitability. Similarly, NWCC is negatively related to GDP and hence justifies the positive impact of GDP on profitability. Altogether, we accept the hypothesis that economic growth supports SME profitability through account payable and NWCC. Similarly, Government planned allocation (PSPO) is expected to increase SME profitability and found significant only with AR. An increase in PSPO decreases accounts receivable and hence increases profitability. Coming to commercial bank advances to small scale industries (BASSI), it is significantly impacting accounts payable (AP) and NWCC. An increase in BASSI increases AP and hence increases SME profitability, whereas an increase in BASSI decreases NWCC and increases profitability. Similarly, AR is the only component of WCM that is significantly explained by the exchange rate and interest rate. Overall, changes in economic growth (GDP) and commercial bank advances to small scale industries (BASSI) are the macroeconomic parameter that is explaining SME profitability significantly better than others.

Conclusion

The present study analyzes the relationship between working capital management, macroeconomic impulses, and profitability of Indian SMEs from 2010 to 2017. The study finds a negative relationship between AR (like Enqvist, 2014; Garcia & Solano, 2007; Gill et al., 2010; Lazaridis & Tryfonidis, 2006; Yunos et al., 2015) and positive coefficient of AP with ROA. It implies the firm managers may maximize SME’s profitability by converting the credit sales to cash as early as possible and by increasing the days of AP. In spite of the risk of increasing financing cost and increasing the sensitivity of high credit risk (see Aktas et al., 2015; Kieschnick et al., 2013), the study finds evidence that high inventories may support the profitability of Indian SMEs. With the drawback of poor management capability of the SME owners or managers (Pansiri & Temtime, 2008), it is certainly not easy for SMEs to predict the accurate inventory level. Holding larger inventory may increase carrying cost, but for Indian SMEs, it is relatively favored. For ordering inputs and selling outputs, SMEs are largely dependent on local markets and there is always a risk of inventory dry out. The operational supply chain may any time be disturbed. Hence, holding higher inventory seems to be increasing SME’s profitability for Indian SMEs. While SMEs are struggling to obtain finance for their operation and investment (Allen et al., 2012; Thampy, 2010), it is highly essential for Indian SMEs to convert their credit sales and inventories to cash. Finally, for the overall impact of working capital management on SME profitability, the paper concludes that minimizing NWCC can maximize the profitability of Indian SMEs.

The study further finds the strong impact of macroeconomic policies on SMEs performance and conclude that changes in economic growth (GDP) and commercial bank advances to small scale industries (BASSI) are the most influential macroeconomic parameter to explain SME profitability significantly better than others. The study further undertakes a sensitivity analysis of SME profitability and finds the impact of economic growth is clear and dominant.

The major limitation of the study is the unavailability of secondary financial data for Indian SMEs, which makes it difficult to undertake research based on financial aspects. Therefore, the study has used the financial information of the constituents of the SME IPO index of the Bombay Stock Exchange (BSE). Furthermore, the findings of the study might have limited implications, as there are hundreds of small scale enterprises that are not listed in the BSE SME IPO index. This study makes a potential contribution to the existing literature on corporate finance of SMEs and is unique in its kind because it explores the nexus between working capital efficiency, macroeconomics impulses, and profitability of the Indian SME. The findings of the study will definitely guide the firm managers to shape their working capital management strategies. Policymakers may find the study interesting to identify the macroeconomic parameters that significantly influence Indian SMEs.

The present research has lots of scope for future studies. The working capital management practices of Indian SMEs can be integrated with their financing practices. The study can be extended to relate the existing practices of working capital management with capital structure and working capital financing practices. Integrating the best practices of working capital management with its financing structure can help in maximizing firm value is the issue to be explored.

Footnotes

Declaration of Conflicting Interests

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.