Abstract

This study has been undertaken in order to estimate the impact on IRDA guidelines on customer satisfaction in the life insurance sector from the time of its inception in 1999 to the IRDA Amendment (The Insurance Laws Act) of 2015. In order to accomplish the research aim and objectives appropriately, a thematic framework has been implemented that aspires to conduct quantitative analysis of the primary data collected in relation to the research topic through questionnaire-based survey. Further, comparative survey of customer confidence on IRDA guidelines pertaining to pre- and post-IRDA regulation 2017 has been made in the study. The study findings confirm that IRDA guidelines, that is, transparent and make clear specifications on aggressive online selling by insurance companies, provide outsourcing guideline for them, direct the customers on timely settlement of claims without delay, and are abided by the mandate of Government of India to link PAN and Aadhaar card of the consumers to their policies show significantly positive impact on consumer confidence. Simply put, there is significant increase in confidence post-2015 Amendment Act.

Introduction

Regulatory Architecture in Insurance Sector: Emphasis on Life Insurance Market

The Insurance Regulatory and Development Authority (IRDA) of India is an autonomous, statutory body that regulates the insurance industry in India. The Government of India established it for regulating, directing, and controlling the insurance sector to ensure its smooth functioning. Constituted by a Parliament of India Act called Insurance Regulatory and Development Authority Act, 1999 following the recommendations of Malhotra Committee (1994) and passed by the Government of India in April 2000, IRDA’s objectives include promoting competition to enhance customer satisfaction with increased consumer choice and lower premiums while ensuring financial security of the insurance market. IRDA also regulates investment of funds by insurance companies, regulating maintenance of margin of solvency, adjudication of disputes between insurers and intermediaries or insurance intermediaries. The IRDA Act, 1999 allows private players to enter the insurance sector besides a maximum of foreign equity of 26 percent in a private insurance company operating in India. In December 2000, the subsidiaries of the General Insurance Corporation of India were restructured as independent companies and it was converted into a national reinsurer. IRDA was amended in 2002. At the end of financial year 2016–2017, there are 62 insurers operating in India out of which 24 are life insurance companies, 23 are general insurers, 6 are health insurers involved in health insurance business exclusively and 9 reinsurers including foreign reinsurers’ branches and Lloyd’s India. As far as the classification of insurers into public and private sector is concerned, 8 are operating in the public sector and the remaining 54 in the private sector (Table 1).

List of Registered Insurers (IRDA, 2019)

Clearly the number of life insurers is more than the number of insurers serving other products or purposes. Life insurance industry earned a premium income of 41,84,768.2 million during 2016–2017 compared to 36,69,432.3 million in the previous financial year 2015–2016 (IRDAI, 2018). This translates to a growth of 14.04 percent and an increase in the growth by 2.2 percent. The growth of the private sector in terms of the premium income of its insurers which was 17.40 percent (as compared to 13.64% in the previous year) was more than the growth of the Life Insurance Corporation of India given by 12.78 percent (as compared to 11.17% in the previous year). Growth in the private sector can be attributed to the rise in the FDI limit in the insurance sector which was raised to 49 percent in June 2016 from its previous level of 26 percent through the automatic route.

As per section 4 of the IRDAI Act 1999, IRDA of India specifies the architecture as:

The authority consists of a 10-member team of which 1 is Chairman, 5 are whole time members, and 4 are part time members. All the members are appointed by the Government. According to the IRDAI Amendment Act, 2015, with respect to life insurance market, an insurer will be eligible to be appointed as an Appointed Actuary provided some conditions are met. Some of these conditions are: first, the person is a resident of India; second, the person has passed specialization subject in life insurance; third, the person has the relevant experience of at least 10 years in life insurance industry of which minimum of 5 years will be post-fellowship experience; and fourth, the person has at least 3 years of post-fellowship experience in annual statutory valuation of a life insurer.

Customer Growth Picture in Life Insurance Market of India

Growth trends in registered life insurers have been significant since the establishment of IRDA. Increase in the private insurer is more than the public sector insurer represented solely by LIC. Based on the total premium income, the market shares of LIC went down from 72.61 percent in 2015–2016 to 71.81 percent in 2016–2017. On the contrary, market share of private insurers increased to 28.19 percent in 2016–2017 from 27.39 percent in 2015–2016 (IRDAI, 2018).

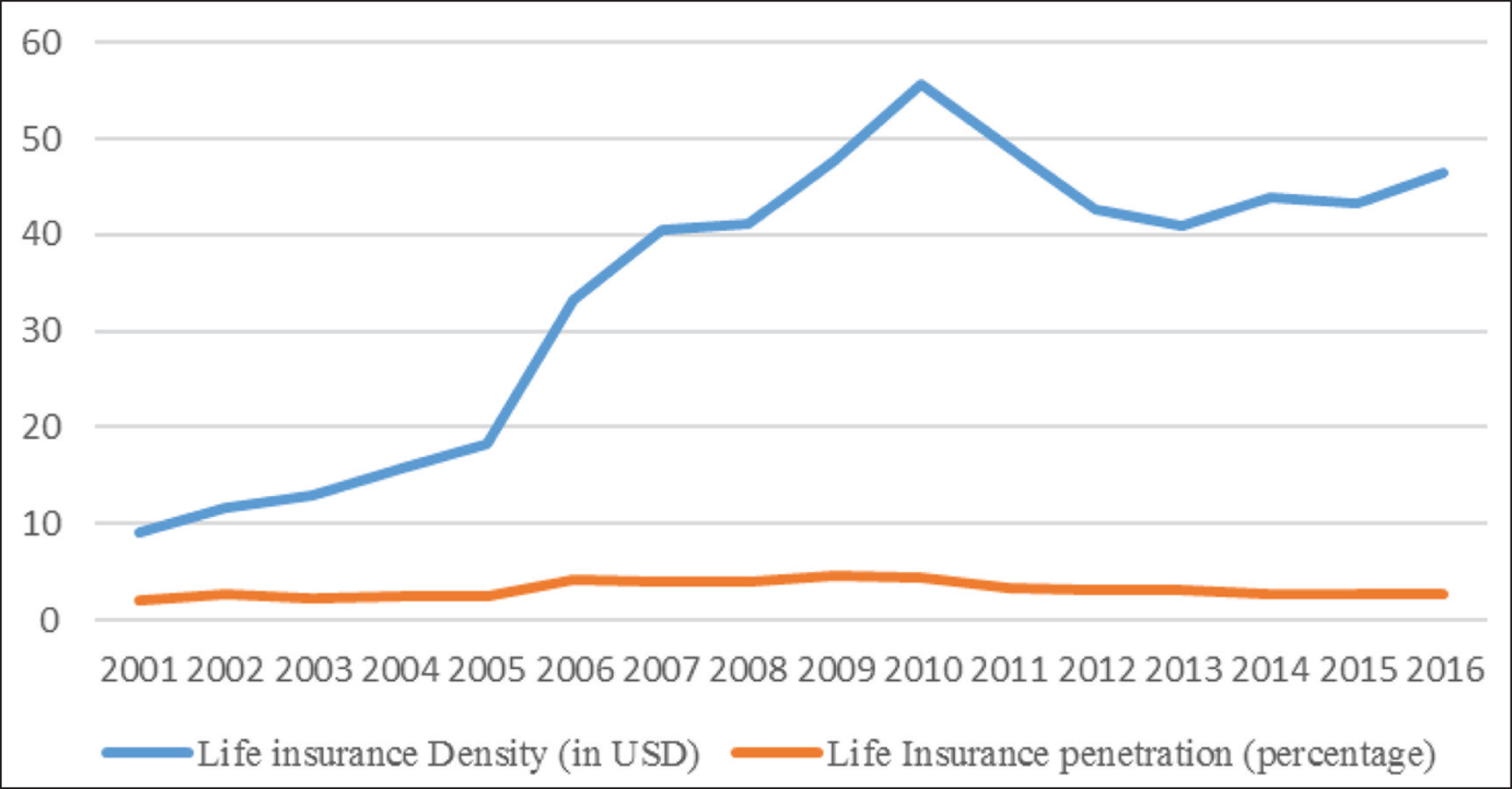

Customer growth picture in the life insurance market is captured by indicators such as insurance penetration and insurance density (Bharadi, 2012). Insurance penetration is defined as the percentage of insurance premium to GDP and insurance density is measured as the ratio of premium to population or per capita premium. The first decade after the insurance sector liberalization witnessed a steady increase in insurance penetration. It reached its peak at 4.6 percent in 2009. The insurance density also experienced a growth reaching its peak at $55.7 in 2010. Figure 1 represents the insurance penetration and insurance density in India for the time period 2001–2016 (IRDAI, 2018).

Also private life insurers issued 6,324 new policies in 2016–2017 and LIC issued 20,132 new policies. The former reflected a growth of 2.13 percent in the number of new policies issued whereas LIC faced a decrease of 2.02 percent. Much of the growth in the private life insurance market happened due to the establishment of IRDA.

Need for Study

The facts and figures presented in Figure 1 indicate that IRDA has been playing a crucial role in the Indian life insurance sector. The growth of the insurance market also indicates that there is increasing demand in the market with respect to insurance product, marketing, competition and customer’s awareness (Rewadikar, 2013). Introduction of large number of new life insurance policies every year proves that consumers are confident about investing in the insurance products. Therefore, there is a definite scope to study the phenomenon of consumer confidence in the life insurance market in India since the inception of IRDA Act in 1999 to 2015 IRDA Amendment Act, which made notable revisions in the facilities, notably protection of interests of insurance policyholders; insurers, distribution channels, and other regulated entities fulfill the promises they made to the policyholders; and standard procedures and best practices in sales and services of insurance policies are maintained (IRDAI, 2017). However, since this study purports to observe the consumers’ behavior against the amendment in the act, capturing the behavioral change of the past 20 years (1999–2018) was practically difficult. Therefore, a period of 10 years (2007–2017) has been considered to conduct the study and establish observations, covering the pre-2015 situation (then) and post-2015 situation (now).

Aim and Central Question

The aim of the study is to investigate the impact of most recent 2015 IRDA amendment act vis-à-vis the IRDA guidelines of 1999 on the behavior of the consumers by doing a comparative analysis of confidence of those consumers who have been purchasing life insurance products for 10 years and more. This study tries to answer the following question:

Is there a change in consumer confidence in the life insurance market from 1999 IRDA guidelines vis-à-vis the recent IRDA Amendment Act of 2015?

Literature Review

IRDA Guidelines in Life Insurance Market: Critical Analysis of the Past 10 years

After being constituted in 1999, IRDA focused on increasing competition in the life insurance market as at that time, there was monopoly enjoyed by the Life Insurance Corporation of India. Along with bringing competition in the market, the other objectives were to increase customer satisfaction by providing them with more choice and to allow them to pay lower premiums. It also aimed that the insurance market becomes more secure financially. The market was opened up for registration applications in August 2000 where foreign companies could have ownership up to 26 percent. As specified in Section 114A of the Insurance Act, 1938, IRDA possesses the power to form guidelines and since 2000, these guidelines included company registrations and the protection of policyholders’ interests. The regulatory changes also included minimum death benefit structure and structure to surrender value payment (Iyer, 2014). IRDA revised its guidelines from time to time in order to increase policyholders’ interests and welfare. In the year 2010, guidelines towards Unit Linked Insurance Policies were revised. Lock in period was increased from 3 to 5 years. Minimum payment term was also increased to 5 years. Mandatory insurance cover was made for all insurance products. IRDA also introduced maximum limit on expenses. The year 2015 also brought significant changes in the IRDA guidelines (Iyer, 2014). Insurers were directed to launch products that complied with these revised guidelines. It also required that the existing life insurance products which were noncompliant could not be brought to the market beyond the stipulated deadline of December 31, 2015. All these guidelines were made to ensure growth of insurance business and increase the life insurance penetration. The FDI limit in the insurance sector was increased from 26 to 49 percent in June 2016 in accordance with the attempt of IRDA in 2015.

Regulation of Investment

In IRDA Act of 1999, prohibition was imposed on investment of funds outside India. Under section 27C of the act, it was specifically mentioned that no insurer will be able to invest the funds of the policy holders directly or indirectly outside India. However, under section 27D certain guidelines were specified on the manner and conditions on investment. It was stated that without prejudice to any term contained in any other sections of the act, the authority may specify the guidelines made by the act regarding the time, manner and conditions of investment of assets totality in the interest of the policy holders. Moreover, such investments can be made in infrastructure and social sector. In addition, it was also stated that such guidelines on investment will be uniformly applicable to all the insurers carrying on the business of life insurance, general insurance, or re-insurance in India on or after the commencement of the Insurance Regulatory and Development Authority of India Act, 1999 (Insurance Regulatory and Development Authority of India, 2007). The Insurance Act previously allowed foreign investment up to 26 percent of paid up equity capital in Indian insurance companies (CUTS, 2016). However, while discussing the Union Budget of 2004–2005, it was mentioned by the-then finance minister of India that the IRDA projects to increase foreign direct investment cap in insurance to 49 percent from 26 percent. Finally, in the Insurance Laws Amendment bill of 2015, it was stated that the cap of foreign direct investment and portfolio investment in the insurance sector would be raised to 49 percent (Pandey, 2017). Guidelines were also made since IRDA Act of 1999 regarding increment of capital from domestic sources. Thus, while in 1999 the insurance companies were only allowed to have capital in their form of shares, by 2015, guidelines were issued by IRDA that allowed the companies to o have capital in form of preference shares and subordinate debt. It has additionally been specified that the insurance companies can raise their capital shares by means of public issue on completion of ten years from the date of commencement of business, or any other period prescribed by the central government (CUTS, 2016).

Expenditure by Insurance Companies

The IRDA Act of 1999 made some guidelines regarding funds and expenditure made by insurance companies. In this, it was specified that a fund shall be maintained by insurance companies by the name The Insurance Regulatory and Development Authority of India Fund where all the governmental grants, fees and charges received by the authority shall be deposited, This fund should be exclusively used for incurring expenses like salaries, allowances and other remuneration of the members, officers and other employees of the Authority along with meeting other expenses that are related to the discharge of its functions and for the purposes of this Act (Insurance Regulatory and Development Authority of India, 2007). While previously IRDA Act capped commissions or remunerations paid to the insurance agents in any form in life insurance business, according to the type of insurance, term, and year of premium, in the Act of 2014 this clause was eliminated. Instead, it was stated that while making guidelines with respect to remuneration of intermediaries, factors such as nature and tenure of the policy and in particular the interest of the agents and other intermediaries concerned shall be taken into consideration. Thus, presently, the commissions have been linked with the premium collected on the relevant insurance products. It has further been stated that in case of single premium products commissions or remunerations meant for the procurement of all individual policies in respect of all distribution channels, excluding the direct marketing shall not exceed 2 percent of the single premium. Guidelines in management expenses have also been brought in the IRDA Act of 2015. In this, it has been stated that certain exemptions in management expenses would be provided based on factors such as the size, age of the insurance company as well as the type of business segment. For instance, private insurance firms incurring high initial setup costs shall be exempted from paying this expense for a five years from the commencement of business operations, from compliance of the mentioned rules (CUTS, 2016).

Retention of Customers

One of the core objectives of IRDA Act of 1999 had been to work towards customer retention. For this, the Authority formulated a plan of action to ensure that customers receive clear, precise, and correct information about the products a services they buy. Additionally, the authority also considered it as a part of this plan to make the customers aware of their subsequent duties and responsibilities related to specific insurance plans. Further, it was included in the action plan to IRDA to work towards speedy settlement of genuine claims, prevent insurance frauds and other malpractices, and set up effective grievance Redressal machinery through which customers can lodge their complains. As guidelines on premium and tariff also determine the rate of customer retention, so IRDA Act of 1999 laid out that the annual premium that every insurer is supposed to make to the Advisory Committee should not exceed 1 percent of the total premiums in respect of facultative insurance accepted by the customer in India. It was also specified that in case of any other insurance business, this premium should not exceed more than 1 percent of the total gross premium written direct by the customer in India (Singh, 2010; Yadav & Mohania, 2014). As part of the customer retention policy, IRDA amendments of 2015 have reconsidered the important aspects such as persistency rate, orphan policy and deferred commissions. While the average persistency rate for each agent for financial year 2011–2012, 2012–2013, and 2013–2014 was 50 percent, in 2014–2015 it became 75 percent. Further guidelines were made from July 1, 2014 onward that stated that life insurers were required to have their own company specific persistency criterion for renewal of individual and corporate agency for removing the requirement of maintaining 50 percent persistency rate. In order to agent credibility for the customers, it was also made a mandate in IRDA Act of 2015 that agents must maintain a record of the policies sold as well as their persistency on a year to year basis and the insurer was required to endorse by the same was at the end of the year (CUTS, 2016).

Impact of IRDA on Consumer Confidence: Systematic Review with Instances from Past 10 Years

One of the key themes identified in correspondence to impact of IRDA guidelines on customer confidence is customer satisfaction. In this context, the research conducted by Siddiqui and Sharma (2010) focused on the factors that determine satisfaction of customers on the service quality of insurance sector. The findings suggest that cardinal features in insurance products in the form of assurance, personalized financial planning, competence, corporate image, tangibles, and technology operate as primary determiners of customer satisfaction. Similar research was conducted by (Kathirvel & Radhamani, 2013) on the factors influencing the satisfaction of customers with the insurance sector. The findings presented additional factors in addition to those specified by Siddiqui and Sharma in the form of comfortable environment in the insurance office, transparency with insurance officials and exposure to new strategies undertaken by the insurance companies to make the services offerings more effective and efficient as factors that determine the satisfaction of insurance policy holders towards their insurance products.

The next theme identified is identification of risks and significance of risk management strategy on the insurance sector. In relevance to this theme identified, Pandey and Rao (2013) conducted research presents that factors like entry of private players, corresponding policy changes and the present day fact of unprofitable books, erosion of capital resulting from unmanageable claim ratios have increased risks in the insurance sector. Hence, implementation of risk management strategy has become integral in the sector because it safeguards the investors as well as investment. Research on the similar topic conducted by Eikenhout (2015) further suggests that identification of risk management strategy helps an insurance company in developing a systematic approach by virtue of which the unprecedented risks and uncertainties could be effectively identified. The scholar further states the accurate identification of these risks and timely implementation of risk management strategies shows positive impact on the performance as well as the value of the insurance company. In context to identification of risks in the insurance sector, the study conducted by Eling and Pankoke (2016) suggest that traditional insurance activity in the life, nonlife, and reinsurance sectors do not contributes to systemic risk. These activities do not increase the insurers’ vulnerability to impairments of the financial system either. Rather, nontraditional insurance activities in the form of credit default swap underwriting usually contribute to systematic risks in the insurance sector and make the financial system of the insurers susceptible to impairment. Such activities even make the life insurers more vulnerable than nonlife insurers due to higher leverage.

Based on the above exploration of literature highlighting the change in IRDA Act since its inception to till date and the resultant impact on customer confidence, this study proposed the following hypothesis for further investigation:

H0: There is no difference in impact of IRDA guidelines on consumer confidence from then (pre-2015) to now (post-2015).

Research Methodology

Research Design

This study aimed to measure the impact of IRDA guidelines on consumer confidence, a comparative analysis of pre- and post-IRDA amendment act of 2015, based on a positivist belief, which lies in understanding the of real world objects existing beyond human knowledge (Kaboub, 2008). Based on the positivist paradigmatic approach this study applied the descriptive as well as explanatory methods. Under descriptive, the demographic distribution of the respondents and their general perception were presented (Bhattacharjee, 2012), while under explanatory, the causality of the IRDA Act and amendments on consumer confidence was measured (Morgan, 2014). Following the application of method, a quantitative approach of data collection was entailed which was essentially carried out using survey strategy.

Survey Participants

In order to determine whether there is any impact of IRDA guidelines on consumer confidence, the survey respondents needed to be familiar with life insurance market for a long period of time. The sampling method in the study was selective sampling where inclusion criteria was that the customers invested in their life insurance products for more than 10 years.

Initially a pool of 500 respondents was targeted for the survey (N = 500). But many of them were not willing to participate in the survey and among those who were willing, many did not turn in their responses within due time or their responses were incomplete. Finally, responses from 300 participants (N = 300) were collected and analyzed. Therefore, a response rate of 60 ([300/500]×100) was obtained for the study. These participants answered the questions asked in the survey was valid enough to proceed with the analysis. The survey was conducted in Delhi NCR with the only inclusion criteria mentioned above.

Measurement Instruments and Measures

The questionnaire—a structured and close-ended in nature—was designed in such a way that customers were able to reveal whether there has been a difference in their confidence level towards increasing their investment cap on life insurance and increasing purchase of new life insurance policies online.

A pre- and post-test design based experimental survey was implemented wherein the respondents were asked whether factors related to IRDA amendment act 2015 were able to cause a rise in their confidence level.

Procedure of Data Collection and Analysis

Data collection was carried using a purposive sampling approach, wherein the respondents were selected with the criterion that they are insurers for at least 10 years. This inclusion criterion was adopted to ensure that the respondents are aware of the changes occurred in IRDA act for a prolonged time and hence will be able to capture the impact on their overall confidence appropriately. Respondents’ information was obtained through personal visit to select insurance offices and explaining the Branch Manager about the study aim. Utmost care on the part of the researcher was taken to maintain ethical consideration in the data collection. All the respondents were informed about the motive of the study and its aim and objectives. They were not forced any way to participate and were allowed to withdraw any time. Furthermore, complete anonymity of the respondents were promised and maintained throughout the study.

Findings

Demographic Profile

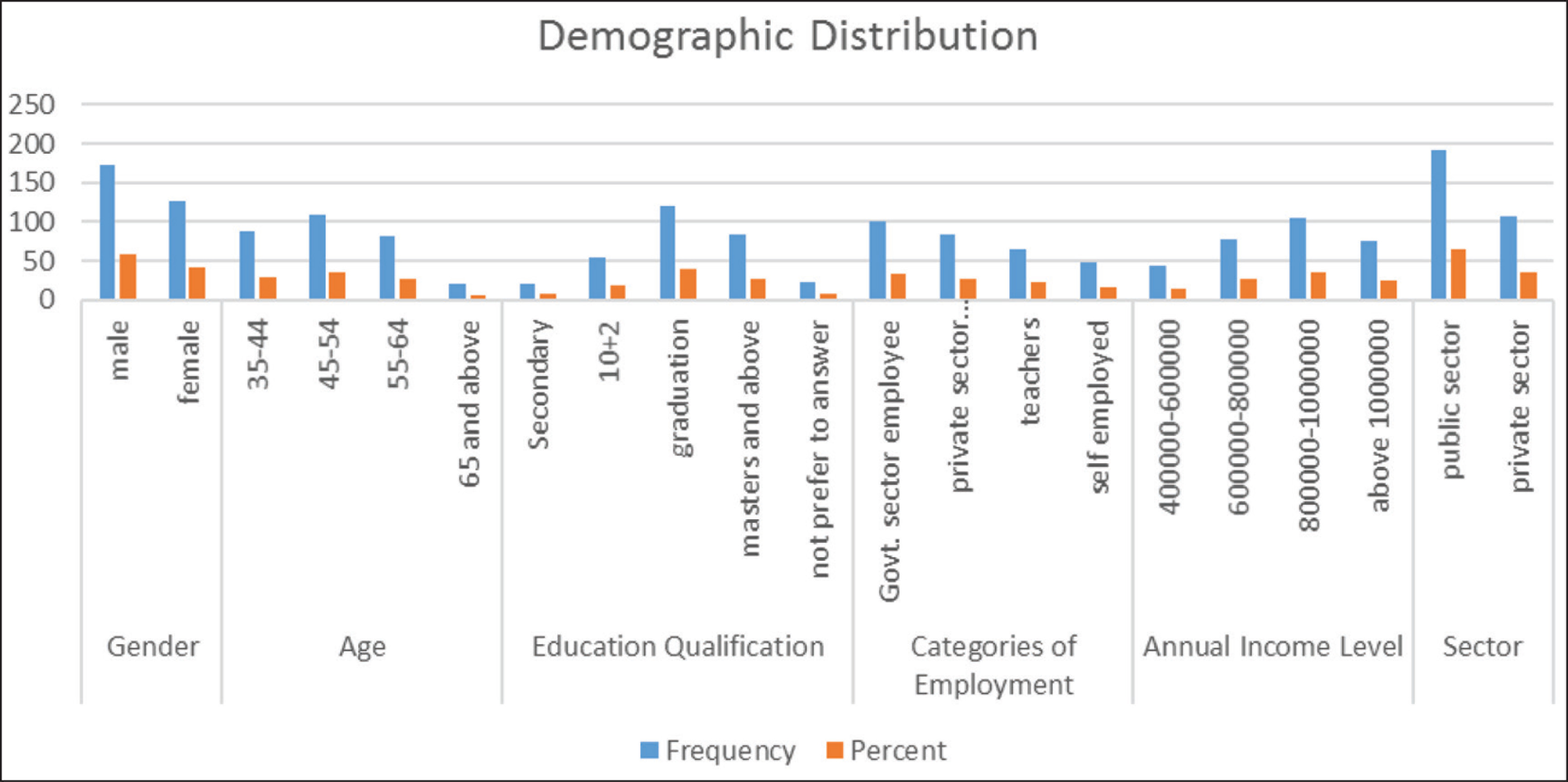

The demographic profile consisted of information collected on gender, age, educational qualification, job category of employment, annual income of the respondents, and the insurers from whom they bought their life insurance.

Frequency distribution of demographic profile of participants in Figure 2 reveals that out of 300 respondents, percentage of male was higher than the percentage of female. Also that most of the participants who purchased life insurance, belonged to the age group 45–54. Contrarily, respondents who are aged 65 years and above were the least to have insurance. Further, it was noticed that most of the insurance holders earn 800,000–1 million per annum whereas people from lower earning category like 400–600 thousand per annum buy the least number of insurance products. The annual income level distribution of the respondents reveals that since all of them had been earning at least ₹400,000 per year, they were in a good position financially to invest in the life insurance market.

General Background

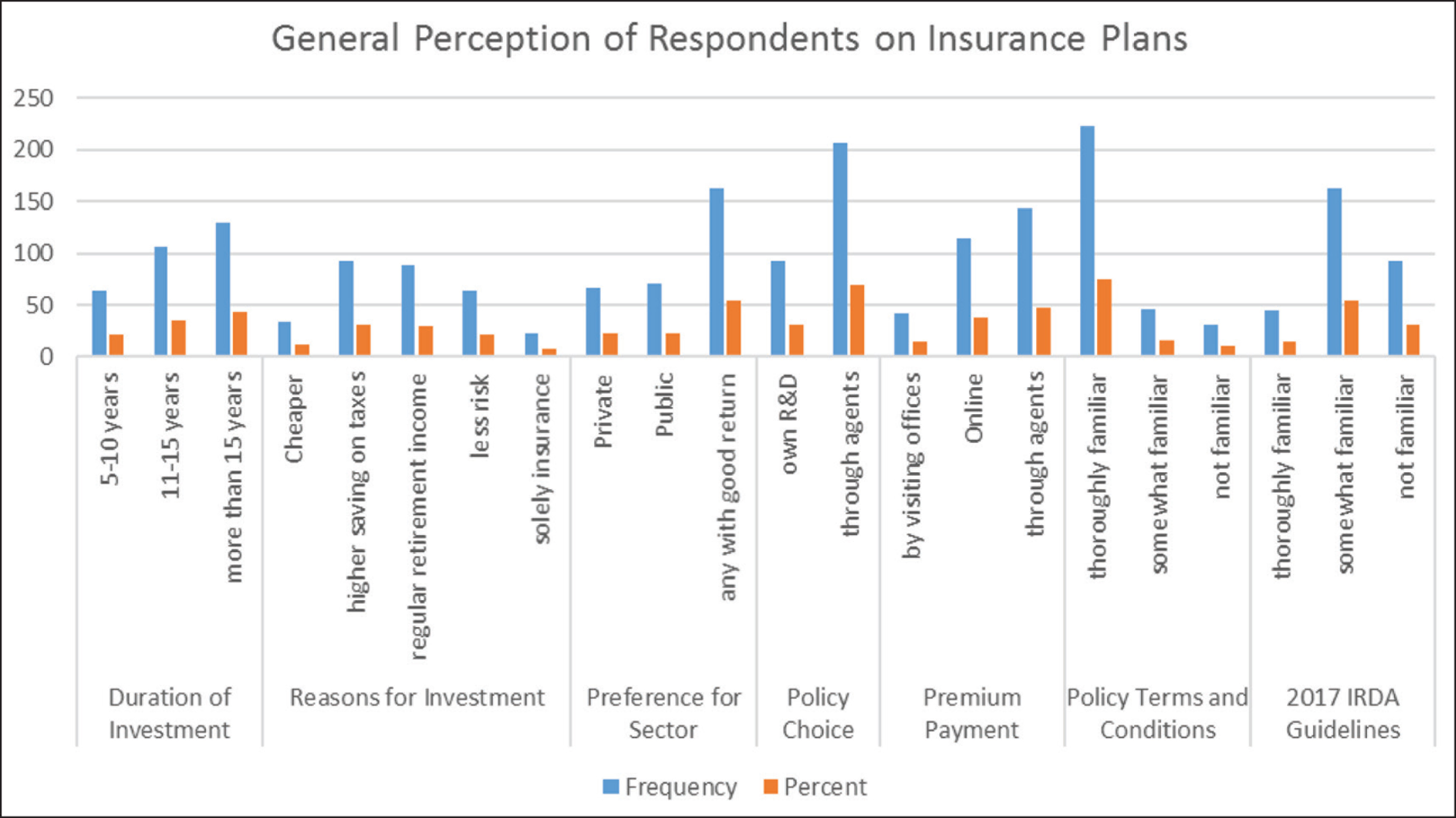

The general background of the survey participants revealed information about their behavioral pattern regarding life insurance market.

While analyzing through the frequency distribution of general background of the respondents in Figure 3, it was found that more than 78 percent of the participants have been investing in insurance for more than 11 years. And most commonly used reasons for keeping an insurance were to save taxes, to incur regular retirement income and futureproofing for risks. However, when they were asked the type of insurance they buy, most of them did not have preferences on any particular sector and instead they were inclined to buy any insurance package with good returns. Moreover, almost 70 percent of the respondents have agreed that they did not personally research about the type and specifications of the insurance, instead relied on the recommendations from agents and buy from them. With the thorough advancement in technology some of the insurance buyers started to pay their insurance premium online, but the majority of them still depends on their agents for paying insurance premiums. It can be inferred that since most of the survey participants started investing in life insurance more than 10 years ago when there was less scope of obtaining information online compared to today, they had to rely on agents and they continued doing so since then. When the respondents were asked whether they were familiar with the terms and conditions of the policies they purchased. It was found that three fourth of the total participants were thoroughly familiar with the T&Cs. Together, almost 90 percent of them were familiar to some degree implying that buyers of life insurance in India are generally aware of the terms and conditions of the policies at the time of investing. Lastly, when the participants were asked whether they were familiar with the IRDA amendment act of 2015. Almost 70 percent of them revealed that they had some degree of familiarity with these guidelines implying that majority of the respondents were well aware of the changes made by the regulatory authority that is IRDA in the insurance sector to safeguard and protect their interests.

Wilcoxon Signed Rank Test Analysis

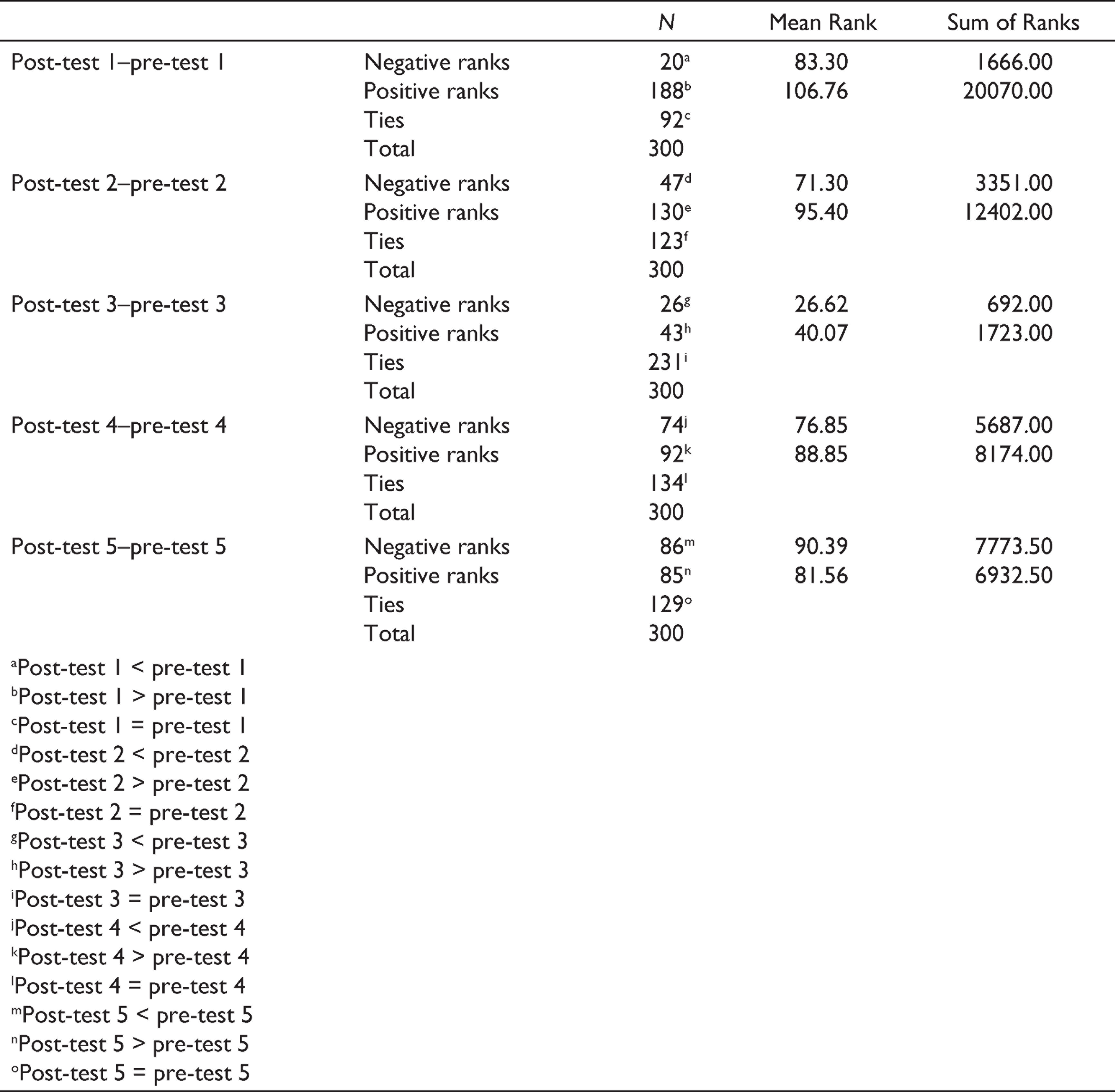

The Wilcoxon signed rank test was performed in two steps. In the first step, it was analyzed whether there was an increase in consumer confidence because of the IRDA Amendment Act (Table 2), 2015 pertaining to five factors which were restrictions on aggressive online selling activities, clear outsourcing guidelines, timely settlement of claims, mandatory Aadhaar linkage, and provision of free look-up period. In the second step, it was analyzed whether there was an increase in consumer confidence reflected by their investment decisions which were increase in investment cap and increase in online purchase of life insurance.

Tables 4 and 5 show the results of the rank test in the first step. Pre-test and post-test represent responses of the participants in the pre-2015 Amendment Act (then) and post-2015 Amendment Act (now). Pre-test 1 and post-test 1 are the responses due to the factor of restrictions on selling activities, pre-test 2 and post-test 2 are those due to the factor of outsourcing, pre-test 3 and post-test 3 are those due to the factor of timely settlement, pre-test 4 and post-test 4 are responses due to the factor of Aadhaar linkage and pre-test and post-test 5 are those due to the factor of free lookup period. Before moving further, it is clear from Table 2 that for four out of five factors, mean positive rank is higher than the mean negative rank indicating that there is a definite increase in consumer confidence due to these recent amendments. Timely settlement in claims have helped the consumer to trust their respective insurers. As timely and effective communication and resolution helps the customers in buying again with confidence (Nebo & Victor O, 2016). In other words, it confirms that the consumers have started to put more faith in insurance companies while purchasing insurances after the changes in the IRDA guidelines. This is further validated by the value of the respective test statistics presented in Table 5.

Wilcoxon Signed Rank Test Results for Factors of IRDA Guidelines, 2015

Wilcoxon Test Statistic Values for the Factors of IRDA Guidelines, 2017

For the first three factors, the null hypothesis has been rejected at 1 percent level of significance (Table 3). The fourth factor rejected the null hypothesis at 5 percent level of significance. Only the fifth factor showed a nonsignificant impact on consumer confidence, for which the null hypothesis was accepted. This shows that the amendments like restricting aggressive online selling activities, clearing outsource guidelines, settling claims on time and mandating Aadhaar linkage have strongly influenced the confidence and purchasing behavior of the customers in a positive way. These changes in the IRDA guidelines have certainly helped the consumers while buying the insurances. Though, fifth factor, the provision of free look-up period did not aid in boosting the confidence of consumers in any way. The reason behind could be the short length of look-up period provided by different insurers which usually lasts for 10 days or more. There are the type of consumers exist in market who only seeks information and takes opportunity for self-gratifying reasons when it comes to free sampling (Carrie et al., 2004). Furthermore, the short time involved in free look-up period is not enough to understand the advantages and disadvantages of insurance products. Overall it shows, now that the IRDA has changed some of the guidelines in favor of consumers, people feel more secured and satisfied while buying insurance products.

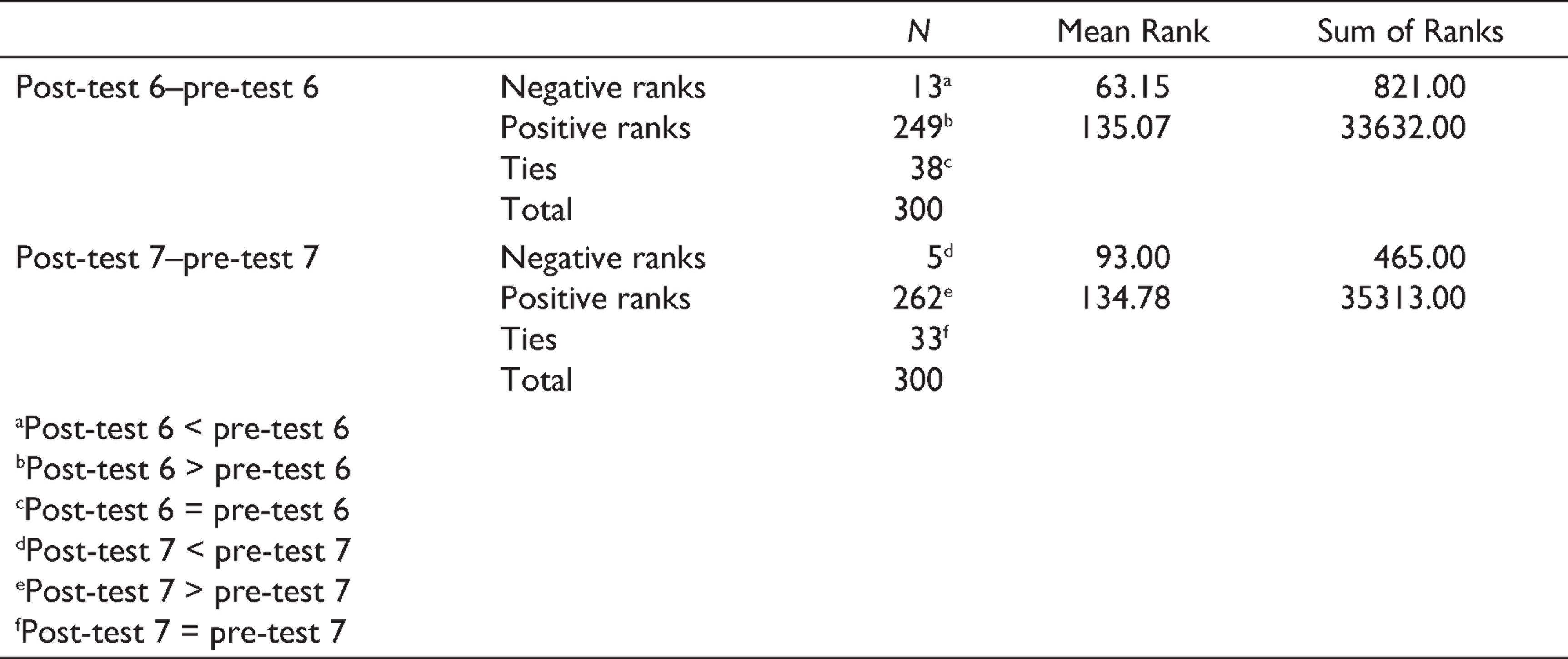

Wilcoxon Signed Rank Test Results for Consumer Confidence

Wilcoxon Test Statistic Values for Consumer Confidence

The implication of the first step of the analysis is that consumer confidence has increased due to four out of five factors that were part of IRDA amendments. Due to this increase, they were expected to reflect this in their investment decisions. This led to the second step of the rank test analysis where the survey participants were asked whether their life insurance investment cap increased and whether they purchased new life insurance policies online rather than buying through insurance agents compared to the pre-2015 amendment situation.

Similar to the first step, pre-test and post-test represent responses for before and after 2015 Amendment Act. Pre-test 6 and post-test 6 represent consumer confidence in terms of increase in investment cap and pre-test 7 and post-test 7 represent consumer confidence reflected by an increase in online purchase.

Both the increases measured by the positive ranks as the difference between post-test responses and the pre-test responses are found to be statistically significant at 1 percent level. In these cases, the null hypothesis is rejected. It implies that consumer confidence in the life insurance market has significantly increased post-IRDA guidelines indicating an increase in investment cap and online purchases. The search of information is an important factor that helps the customers to find the suitable products or services according to their needs (Mittal, 2013). Put otherwise, these guidelines have had a positive and significant impact on consumer confidence as it lets them take their own time to research and compare insurance policies online to make a responsible decision, whereas the increase in cap has helped assuring the consumers to take a more confident decision.

Conclusion

Recommendations

In this section, perspective of three different entities are involved which are IRDAI, insurance companies and consumers. Based on these results, it is recommended that IRDAI should come up with such guidelines in the future that not only help consumers to keep their faith in the market, but also increase the growth rate of the insurance industry as a whole. For the insurance companies, either they should increase the time involves in free look-up period or should rather focus on some more evident factors mentioned above that wins consumer confidence to see a significant rise in their consumer base and retaining them. Further, they should be more transparent to the consumers by providing complete and comprehensible details of the insurance products to their consumers beforehand. Consumers can simply start doing their own research understand the insurance T&Cs before investing in insurance instead of relying on their agents.

Limitations and Future Scope

Despite the fact this study has established some proven realities, it still suffered some of the limitations like availability of sufficient data, and relatively new topic to find the supporting studies. The volume of total researches on the impact of changes in IRDA guidelines on consumer behavior is very limited and researchers had to rely upon the documentation and information available from other countries to develop the conceptual foundation for this study. Along with that, this study was conducted taking the survey sample data from one part of India which restrained the study to understand the behavior and confidence level of consumers buying insurance from different part of India. It would have been possible if more time was granted to collect and analyze the data in depth.

Findings of this study can be taken forward in future by collecting data from more sources and areas which help in a better understanding of consumer behavior in different places or all over India. An adequate size of sample data can be collected in order to derive more close to reality judgements.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Questionnaire

This questionnaire aims to help the researcher to determine if there has been any boost in the confidence of customers of selected life insurance companies of India over the period 2008–2017. Your participation in the survey will be highly appreciated. In doing so, the researcher ensures the anonymity of the participant and complete confidentiality of data collected.