Abstract

Insurance industry is, and has been for a long time, characterized by a strong presence of customer-owned mutual insurance companies that account roughly one-third of the global annual premiums. As mutuals are owned by the communities they serve, one would expect them to display unique characteristics in how they create not only utilitarian but also hedonic value for their customer-owners. The aim of this study is to examine how managers communicate the hedonic value of ownership to their customer-owners. The data consist of 18 mutual insurance companies’ annual reports from seven different countries: Finland, Ireland, the Netherlands, Sweden, Switzerland, the UK and the USA. The resulting framework, produced by a thematic analysis, illustrates how managers of mutuals communicate the hedonic value of customer ownership. Results as well as the limitations of the study point out several interesting and new research avenues and managerial implications.

Introduction

Insurance industry globally is, and has been for a long time, characterized by a strong presence of customer-owned mutual insurance companies. Today, mutuals account for roughly a third of annual insurance premiums and hold some 9 trillion USD in assets; moreover, mutuals serve 922 million policyholder-owners and employ 1.16 million workers, worldwide (ICMIF, 2019). The purpose and mission of these companies can be considered very different from those of investor-owned insurers (IOIs): while the owner value in IOIs can be defined as to maximize the profit generated for investors, mutuals’ aims coalesce around maximizing benefits and value for the customer-owners as consumers (e.g., Cabrales et al., 2003). This is underpinned by the fact that mutuals do not have any regular customers, since ownership is formed automatically by becoming a customer (e.g., Viswanathan & Cummins, 2003). As mutuals have only customers as owners to satisfy, one would expect mutuals to display unique characteristics in how they create not only utilitarian but also hedonic value for their customer-owners. However, while clearly positing that the operations of mutuals should aim at creating value for the customer-owners as consumers, existing literature falls short in describing how the value is created concretely.

The article begins filling this gap of knowledge by taking a managerial perspective and focus specifically on the hedonic dimensions of value, which have just recently began gaining attention in the insurance industry in general (cf. Maas & Rüfenacht, 2018; Riikkinen et al., 2018; Steiner & Maas, 2018). Further, emotional and identity-related bonds have been suggested to form a defining part of an ideal relationship between mutuals and their customer-owners (c.f. Jussila & Tuominen, 2010; Jussila et al., 2012; Mazzarol et al., 2019; Talonen, 2018). Consequently, the aim of this study is to examine how managers communicate the hedonic value of ownership to their customer-owners. As this is, to authors’ knowledge, the first article in this regard and no existing frameworks have been developed, we followed a qualitative approach. For the purposes of qualitative thematic analyses, the study used an international data of annual reports of 18 mutuals from 7 different countries: Finland, Ireland, the Netherlands, Sweden, Switzerland, the UK and the USA.

In the process, specific attention was paid in the ways how managerial thinking is influenced by customer ownership and mutual nature of the company. This is an important issue to state, since managers of mutuals may not always have a clear understanding of customer ownership (Kalmi, 2007; Talonen et al., 2018). Accordingly, analyses were directed only to those quotes in the annual reports where value creation is argued and described in light of customers being owners of the company. To structure the analysis, managerial views in the annual reports were reflected with a framework of market control and voice-dependent means, conceptualizing the distinct characteristics of value creation in consumer co-operatives (e.g., Diacon & O’Sullivan, 1995; Hansmann, 1996; Spear, 2004; Talonen et al., 2016; Tuominen et al., 2009; Vierheller, 1994). The mechanisms articulated by the annual report and emerging in our analysis fleshed out the intellectual framework that should provide scholars and practitioners with a tool for considering how ownership by the customers is seen by the managers to create hedonic value.

Customer Value and Mutual Insurance Companies

The much-studied concept of customer value can be defined fairly simply: customers judge the balance between what they sacrifice and gain in the relevant transaction (e.g., Smith & Colgate, 2007; Zeithaml, 1988). Hence, value is a ratio of total benefits to total sacrifices, with the customer assessing the component costs and benefits in more or less detail, where the components may lie on any of various dimensions. Some scholars see these in terms of a continuum between utilitarian and hedonic faces of value (e.g., Sánchez-Fernández & Iniesta-Bonillo, 2007). One especially common way of categorizing dimensions of value entails various ranges from economic and functional values to emotional and identity-related symbolic values (e.g., Rintamäki et al., 2007). This article concentrates on creation of hedonic value and, accordingly, places emphasis on emotional and symbolic values. At base, the former refers to positive emotional experiences (primarily pleasure or entertainment) generated during the purchasing process (e.g., Choo et al., 2012; Holbrook, 1999; Rintamäki et al., 2006). In the context of insurance, trust and positive interaction with the staff may also be counted among emotional-value-creating factors (e.g., Steiner & Maas, 2018; Talonen et al., 2016). Symbolic value, in turn, brings a social dimension to the process (e.g., Sheth et al., 1991). Here, purchasing and interacting with the company can be understood partly as a social symbol that is used in building of identity.

In the field of insurance in general, traditional research streams such as actuarial mathematics and risk theory (e.g., Beard et al., 1984; Daykin et al., 1994) have only recently been supplemented by research that is beginning to draw attention to the importance of customer orientation in both theory and practice (Eling & Lehmann, 2018; Gatzert et al., 2012; Maas, 2010). In particular, issues related to hedonic dimensions of value have captured the interest of scholars examining how insurance companies should develop their operations in the future. According to Maas and Rüfenacht (2018), it is crucial for insurance companies to shift from functional product-centred thinking and an emphasis on diversification of offerings towards cultivating emotional connections and strengthening aspects that afford customers’ identification with the insurance company.

Recent work has posited that being an owner of a mutual insurance company brings the customer unique means of affecting the hedonic value he or she perceives. Talonen et al. (2016) present the toolbox for this as comprising market control tools and mechanisms that hinge on having one’s say. Market control involves actions of customer-owners consuming the company’s current offering (e.g., Tuominen et al., 2009), as with the direct impact of the quantity of claims on the company’s claim ratio and, thereby, its efficiency, its performance in the long run, the level of premiums that follows and ultimately, the economic value sensed by customer-owners. As for having a say, a customer-owner who is dissatisfied with the offering of the mutual can resort to voice-dependent mechanisms. Using one’s voice is supposed to contribute to taking the company further in a direction that offers the customer-owner greater value. The customer-owners who speak up paint their vision of the future services and steer the company in the desired direction (Talonen et al., 2016).

Voice-related mechanisms are divided into direct and indirect methods, with the former using immediate feedback (channels for this have proliferated through digital technology) and the latter involving such tools as strategic decision-making upon securing official positions of influence, such as administrative posts with official bodies—the mutual’s board of directors (e.g., Mayers et al., 1997) or general meeting (Chaves et al., 2008), supervisory and advisory boards and various committees (e.g., Diacon & O’Sullivan, 1995; Hansmann, 1996).

In this study, typology of market and voice-dependent mechanisms are used in structuring our analysis. In addition to the latter conceptualizations and various discussions of value, our work was informed by methodological considerations, which are discussed later.

The Research Process

Whether investor-owned, customer-owned, or of some other form, all companies produce annual reports. This material offers two sorts of information as source material for study, in that the report is designed to give stakeholders a valid, trustworthy picture of the company’s performance via both financial figures and explanatory material that addresses the reasons behind those numbers (e.g., Yuthas et al., 2002). That supplementary material may include comments from the company president/CEO or other prose, all of which is well recognized as influencing how financial analysts and investors evaluate the company (e.g., Rogers & Grant, 1997). In the context of mutuals, one may expect the annual reports to provide important and relevant information from the customer-owners perspective.

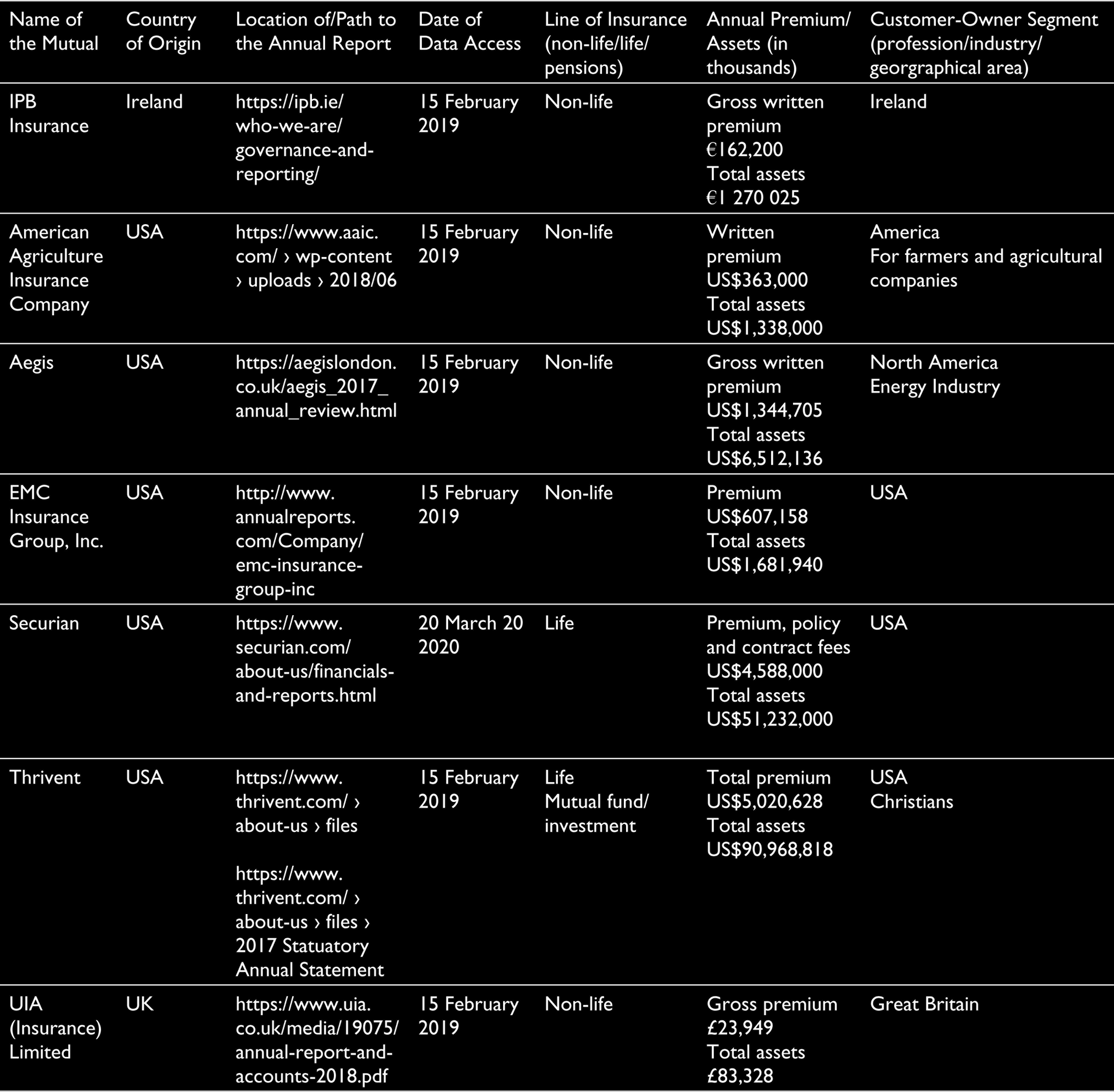

For a good body of annual report data via which to gain better understanding of how managers of mutuals communicate hedonic value for their customer-owners, a sample was sought via the list of members of the International Cooperative and Mutual Insurance Federation (ICMIF). This global body represents approximately 200 mutual insurance companies. As these companies have joined an organization focusing on serving particularly mutuals, one can expect their managers to have at least certain level of understanding of the mutual company form and customer ownership. On perusing their websites, all together 16 of them were identified as having established a practice of publishing the annual report in English. Alongside these, our sample included annual reports from two Finnish mutuals with ICMIF connections; the relevant parts of these materials were translated into the English language for consistent analysis. In this connection, it is good to recognize that mutual insurance companies exist not only in Western countries but in almost every part of the world. Due to language barriers, only Western mutuals were included in the data set of this analysis.

The 18 annual report dataset is characterized in Appendix A. All the annual reports are from the year 2017. For the purposes of a qualitative analysis, considering entities in Finland, Ireland, the Netherlands, Sweden, the UK, and the USA should provide a reasonable picture of insurance companies’ orientation. The size of the data was justified also due to the fact that a qualitative analysis of a larger data would have been inefficient in research wise to conduct.

Since the objective of our research was to examine how managers communicate the value of customer ownership, it was ascertained that qualitative analysis would be the most suitable method, as per the discussion by Denzin and Lincoln (2005). Accordingly, the aim was to identify meanings that managers give to the phenomena in question, namely customer ownership in the field of insurance (cf. Denzin & Lincoln, 2005). What the annual reports articulate can be expected to reflect the emphasis of the mutuals’ managers and provide a useful starting point for addressing the value creation on the ground.

To prepare the data for analysis, all of the supplementary information’s paragraphs and specific sentences explaining the company’s results or operations in light of the co-operative company form was extracted; for example, mentions of data-protection efforts were excluded if data protection initiatives were dealt with only against a regulatory backdrop rather than in terms of, for instance, responsibility linked to ownership by the customers. This produced a body of quotations illustrating the influence of customer ownership and mutual nature of the company on managerial thinking.

Following the example of several authors, a thematic analysis was chosen to analyse annual reports (e.g. Beattie et al., 2004; Conaway & Wardrope, 2010; Tate et al., 2010). The idea of the method is to identify patterns or themes connected with the data. (cf. Braun & Clark, 2006). Applying the technique as used by such scholars as Attride-Stirling (2001), a systematic examination of the corpus was conducted to code the data on two levels: concepts and themes. In the first-order coding, a set of concepts was developed by pinpointing key perspectives of relevance for our work. The framework produced via our 3 rounds of iterative analysis brought out 10 concepts related to market control and 3 connected with voice-related mechanisms. The second phase of analysis was devoted to finding possible second-order relationships: inter-concept connections that reflect higher-level themes. Four market-control themes and two themes related to voice-dependent mechanisms emerged. In the course of the analysis, no voice-dependent processes related to emotional value creation was identified. Lack of managerial communication in this dimension is discussed at the end of the study. Table 1 presents the final framework developed. In both phases of the analysis, the concepts and themes were validated using researcher triangulation (cf. Jonsen & Jehn, 2009). This involved two of the authors working independently at first and then coming together to discuss on the independent-level analysis. This researcher interaction led to the validated concepts and themes in the framework.

The Framework Developed

To aid in finding both concepts and themes, the analysis process utilized existing literature on mutual insurance, other consumer co-operatives and hedonic dimensions of customer value. This design involving systematic reflection on the data against prior literature can be defined as abductive (e.g., Dubois & Gadde, 2002).

Results

Emotional Value via Market Control

The data show that mutuals’ communication about creating emotional value via market control coheres around two distinct themes: meaningful interaction between the staff and the customer-owners and a trusting relationship between the members and the mutual. Related results are summarized in Table 2 which is followed by their detailed elaboration, setting the sample quotes in context.

Market Control-linked 1st-Order Concepts and Illustrative Quotes Connected with Emotional Value

Meaningful Interaction

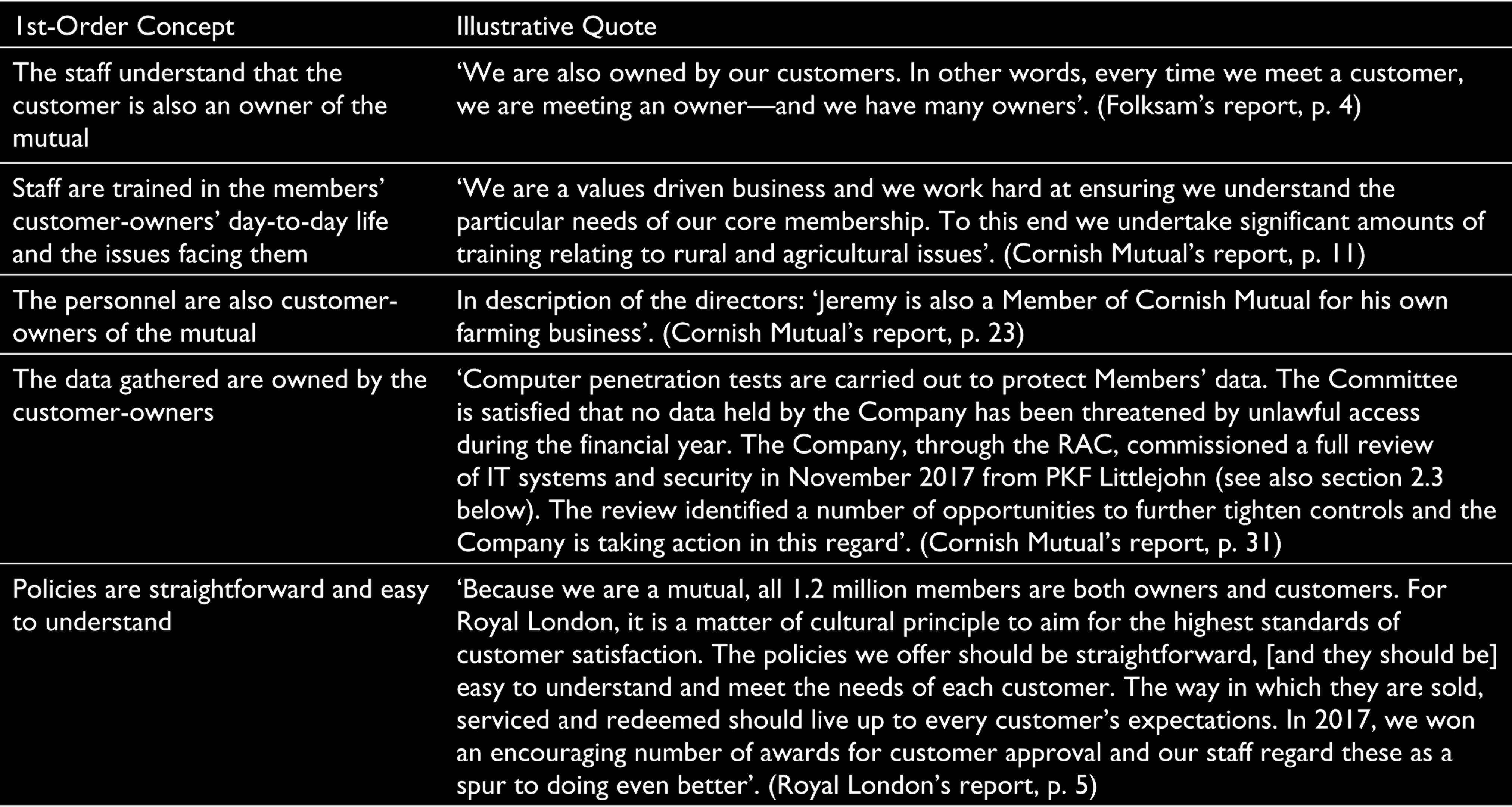

Research into customer ownership indicates that it may manifest itself partly in the meaningful interactions between the staff and other customer-owners. Behind this is a sense that working for one’s own company, by virtue of it being customer-owned, generates a sense of meaning beyond economic benefits for the staff. This, in turn, can nurture a special service atmosphere (Power et al., 2014) and lead customer-owners to perceive the service as ‘friendly, approachable and helpful, demonstrating empathy for members and their circumstances’ (Power et al., 2014, p. 60). Our data point to mutuals being aware that the service encounters hold potential as value-creating processes. Furthermore, the customer-owner has an important part in them, as Swedish mutual Folksam stressed in their annual report (p. 4):

We are also owned by our customers. In other words, every time we meet a customer, we are meeting an owner.

According to our data, the understanding that the customer is an owner of the mutual is strengthened further via special efforts devoted to educating and training the staff. The aim is to make the personnel as familiar as possible with the customer–owners’ life and everyday processes. By doing this, the mutual can be truly anchored in the community and its life. This, in turn, has potential to create a positive atmosphere, in that the customer-owners perceive the mutual as listening and being there to take care of them (cf. Power et al., 2014). The concept is presented in the Cornish Mutual’s annual report (p. 11) thus:

We are a values driven business and we work hard at ensuring we understand the particular needs of our core membership. To this end we undertake significant amounts of training relating to rural and agricultural issues.

Furthermore, agency theory research on mutuals suggests that managers may sometimes act against customer-owners’ interests by, for example, generating unnecessary costs (e.g., Cummins et al., 2004). This can occur because customer-owners may not always have the most extensive opportunities to monitor the managers (e.g., Cummins et al., 1999; Mayers & Smith, 1981). One way to overcome negative expectations in this regard might be to stress on the convergent interests of customer-owners and executives of the mutual. Our data suggest that this can be accomplished via transparent reminders that the executives are also customer-owners of the mutual. This is illustrated in Cornish Mutual’s description of its non-executive directors:

Jeremy is also a Member of Cornish Mutual for his own farming business. (Annual report, p. 23)

A Relationship of Trust

The elimination of conflict of interest between owners and customers can be seen as dovetailing well with foci of the digital age and data economy, such as the emphasis on joint creation of content/value. Only very recently, discussion has been extended to data co-operatives, wherein the data are owned by those generating said data (e.g., Hafen et al., 2014). This sort of arrangement can serve as a mechanism to increase trust that the data will be handled with care and only to the benefit of the consumer. The annual reports attest that mutuals have indeed begun to stress this aspect, as the Cornish Mutual’s report examined (p. 31) illustrates:

Computer penetration tests are carried out to protect Members’ data. The Committee is satisfied that no data held by the Company has been threatened by unlawful access during the financial year. The Company, through the RAC, commissioned a full review of IT systems and security in November 2017 from PKF Littlejohn (see also section 2.3 below). The review identified a number of opportunities to further tighten controls and the Company is taking action in this regard.

The sense of trust can moderate some traditional concerns about insurance simultaneously. Consumers sometimes view insurance companies as seeking loopholes—reasons to deny claims. This sense is grounded in unclear terms of policies, which a company can interpret to its own benefit. Our data show that mutuals seem to recognize this factor and, accordingly, emphasize that they are on the same side as the customer-owners. Highlighting the trust represents potential to facilitate the customer-owners’ emotional value creation by increasing the sense of trust that the company will be there when something happens. Royal London’s annual report (p. 5) provides an example:

Because we are a mutual, all 1.2 million members are both owners and customers. For Royal London, it is a matter of cultural principle to aim for the highest standards of customer satisfaction. The policies we offer should be straightforward, [and they should be] easy to understand and meet the needs of each customer.

Symbolic Value via Market Control

According to our data, communication in the mutuals' annual reports recognizes processes of creating symbolic value via market control. These processes can be grouped under two themes: mutuality-linked values/identity and local focus (Table 3). The content and meaning of these themes merit the elaboration given below.

Market Control-linked 1st-Order Concepts and Illustrative Quotes Connected with Symbolic Value

Alignment with the Values and Identity of Mutuality

The data of annual reports point to mutual-insurance-connected values and identity to create a specific, unique meaning for the customer-owners. Furthermore, this can be achieved in at least three separate ways. First, a mutual insurance company is, by nature, an association of people. It can be defined as a tool whereby customer-owners come together and insure each other (cf. Talonen, 2018). As such, mutuality can imply a contract in which customer-owners express agreement that when something happens to someone, the others participate in compensating for the economic losses (e.g., Aase, 2007). This core principle of mutual insurance is presented thus in the annual report of Achmea (p. 4):

The cooperative legacy is anchored in our business operations and style of management. For over 200 years we have provided products and services based on the idea that insurance means bearing the risk together if someone suffers damage or loss. Our origins have not only largely defined our identity…

Furthermore, mutuals are often established in contexts of certain geographical areas or professions (e.g., Beito, 2000; Guinnane et al., 2012; Pearson & Yoneyama, 2015). The meanings attached to the mutual consequently tie in with the values and characteristics of these communities. Anchored in the values and identity of the community in which they are embedded, mutuals facilitate the creation of a symbolic value, as is stated in one of the annual reports (p. 1):

We also continue to attract members with homes and vehicles from rural and suburban communities around the UK. We seek out and try to attract people who identify with our values and, judging by the number that stay with us at renewal, we seem to be getting that right.

Supporting Local Vitality

Symbolic value of being a customer-owner of a mutual can crystallize in practical initiatives that nurture the local community’s vitality (cf. Jussila et al., 2007). Our data refer to at least two means of doing this. First, mutuals can be used to create job opportunities for members of the community. Thus, the mutual can aid in familiarizing young people with working life and help the unemployed through tough times. Such activities are described in the annual report of Royal London (pp. 7–8):

The work placements allowed members to nominate themselves or a family member for a two-weeks [sic] of shadowing or four-weeks of work experience. This was specifically aimed at those leaving school or university, and anyone considering a career change or wanting to return to work after a long break.

Also, as mutuals are embedded in the life of the community they serve, corporate social responsibility initiatives related to the insurance services are seen as an important aspect of their operations. In other words, schemes that protect the community and reduce the number of claims are deemed important. Customer-owners’ engagement with the company supports these initiatives and strengthens the vitality of the community. As NFU Mutual stated (see p. 50 of the annual report):

Supporting our communities includes developing schemes and initiatives that reflect our member’s [sic] values, working with the police to fight rural crime, reducing death and injury on our farms, teaching young drivers how to stay safe on rural roads and supporting schemes to protect the environment.

Another way to align the operations of mutual with the community’s values is by creating appropriate hiring policies. While hiring criteria can be seen as an important matter for discussion in any organization, mutuals cannot risk leaving the community’s values unaddressed in this connection. It can be inferred from the data that managers see the identity-related aspect of creating hiring policies on the basis of customer-owners’ characteristics. In its annual report, OneFamily stated that its aim

as a customer-owned business, is to reflect the same diversity we see amongst our members, customers and employees. This means ensuring both men and women are equally represented across all departments and levels within our organisation. (p. 24)

Symbolic Value via Voice-Dependent Mechanisms

In our dataset, the mutuals emphasize symbolic value creation via both strategic decision-making and using one’s voice directly. Strategic decision-making can be applied to investment policies, while direct use of voice is described in terms of nominating charity targets and interacting with the executives and staff (Table 4.). These themes are examined in more depth in the following section.

Voice-Related 1st-Order Concepts and Illustrative Quotes Connected with Symbolic Value

Value-based Strategic Decision-making

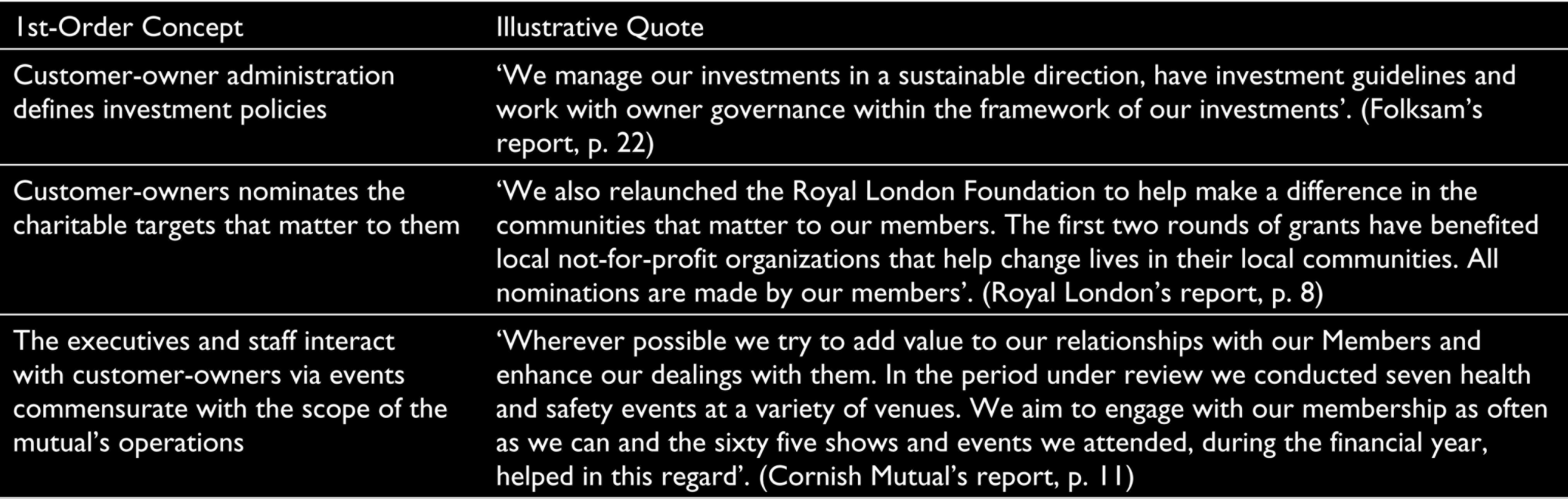

Customer-owners can steer the co-operative in line with the values of their community. With regard to achieving this through administrative bodies, the source data specify the mutual’s investment function as one of the areas of value-based decision-making. As a vital part of an insurance company, the operations side of investments should be left to the professionals hired for this purpose; however, strategic policies and guidelines can be defined at board level. This allows customer-owners to take part in contemplating how assets are to be invested. Furthermore, symbolic value grows as customer-owners define investment policies consistent with their personal principles and community values. This possibility is described in the annual report of the Swedish mutual Folksam (p. 22):

We manage our investments in a sustainable direction, have investment guidelines and work with owner governance within the framework of our investments.

Direct Use of Voice

The first avenue identified by which customer-owners can have a say lies in the realm of deciding on which kinds of corporate social responsibility initiatives to support. In our data, many mutuals explicitly give their customer-owners an opportunity to nominate charitable targets. This arrangement yields added benefit in supplying the management of the mutual with information on important targets of development and support in the community. In the end, this is a channel by which customer-owners can directly influence local vitality in accordance with their values. Greater symbolic value can thus arise. The annual report of Royal London (p. 8) illustrates this nicely:

We also relaunched the Royal London Foundation to help make a difference in the communities that matter to our members. The first two rounds of grants have benefited local not-for-profit organisations that help change lives in their local communities. All nominations are made by our members.

Finally, the annual reports refer to mutuals arranging physical events centred on issues that are important for the local communities. The events also offer the customer-owners a means of direct interaction with the executives and staff. Direct feedback provided via such channels has potential to increase customer-owners’ sense of control and power in relation to local needs and issues (cf. Talonen et al., 2018). The Cornish Mutual annual report refers to this (p. 11):

Wherever possible we try to add value to our relationships with our Members and enhance our dealings with them. In the period under review we conducted seven health and safety events at a variety of venues. We aim to engage with our membership as often as we can and the sixty five shows and events we attended, during the financial year, helped in this regard.

Discussion and Conclusions

This examination is the first attempt to construe an intellectual framework illustrating how managers of mutual insurance companies communicate the hedonic value of ownership to their customer-owners. The article contributes in earlier scientific discussion in at least three ways. First, it increases our understanding of the concrete processes linked to hedonic value creation in a customer-owned company. With the existing research being conceptual, our study adds empirical flesh around the bones by studying managerial communication. Second, the article identifies concrete processes that relate specifically to mutual insurance company as one form of a customer-owned company. This strengthens the expansion of research on mutual insurance from previously dominant economics and accounting perspectives to other disciplines as marketing and management. Third, the framework offers a solid base to spur continuous discussion on the implications of ownership in hedonic value creation in the context of insurance.

The analysis of the data also points out to various shortfalls in managerial thinking. First, no voice-dependent processes related to emotional value creation was identified. Reflecting the market control-linked processes, one would have expected to find processes regarding use of voice as well; for example, enabling customer-owners to practise strategic considerations on the insurance policies or to direct how personnel should be trained and educated would have been logical ideas coming out from the data. Furthermore, one may have expected that customer-owners were offered a possibility to have a direct influence on how their personal data gathered by the mutual are used. Lack of managerial communication in this dimension is rather interesting. In general, this may illustrate a shortfall in managerial understanding on how to use customer-owners as envisioners of the mutual’s future and providers of input in the development of the mutual.

Second, while several aspects of hedonic value creation are put forward in the annual reports, there is only limited amount of information regarding their impact in practice; for example, is it possible to measure the impact, and if so how? Furthermore, it remains unclear whether there were any negative side effects related to the communicated processes; for example, have there been any challenges in engaging customer-owners in the administrative posts, or nominating charitable targets. In the annual reports, the processes were put forward in a positive manner.

Limitations and Future Research

Our research was necessarily limited, with each area of limitation opening new and interesting avenues for future work. First, the data did not provide concrete examples of voice-dependent mechanisms on the emotional value dimension. This is not wholly surprising: the literature recognizes that mutuals and other co-operatives may find it challenging to establish specifically direct channels of influence when the number of customer-owners rises and the company gets bigger (cf. Somerville, 2007; Spear, 2004; Vierheller, 1994). Scholars and practitioners are encouraged to undertake efforts to identify means of enhancing direct use of voice in mutuals. Also, it would be interesting to consider the root causes for the challenges to develop these means in practice.

Second, our article focused on how managers communicate the value of customer ownership to the customer-owners. Consequently, the design of the study did not consider how customer-owners perceive the value of ownership. Scholars are encouraged to follow this path and move towards studying customer-owners and their perceptions. In the end, whether ownership provides value for customers is defined by the customers.

Third, despite using international data, the aim of this study was not to compare results between countries. During the analysis process, however, certain inter-country differences became apparent; for example, some countries seemed to display ‘closer’ mental proximity of the mutual and its customer-owners. One possible reason for this might lie in those mutuals being more tightly bound to certain professions and being highly familiar with the customer-owner niches they concentrate on serving. This, in turn, may influence the thinking linked to hedonic value creation. Consequently, one can believe that a comparative approach could produce further useful insights on this issue.

Fourth, insurance industry-focused scholars are invited to advance our understanding of the implications of this company form. As our results show, managers of mutual do recognize the influence of customer ownership and it is well reported in the annual reports. Consequently, it is important to enhance our understanding of the logics such as how different organizational forms operate, what are their characteristics, and what should one think about their advantages and disadvantages.

Finally, due to language barriers, only English and Finnish language annual reports were analysed. This provided some limitations for the study. Consequently, it would be beneficial that scholars put forward analyses regarding other geographical contexts as well; for example, countries where mutuals are used in organizing microinsurance could provide intriguing cases to complement and fulfil the findings of this article.

Implication for Managerial Use

Our findings point to challenges encountered by mutuals with regard to communicating the role of voice-dependent mechanisms in value creation. This is especially evident with regard to the emotional dimension of value. Since use of one’s voice can be regarded as an important means of customer-owners exercising and perceiving control (e.g., Tuominen et al., 2009), mutuals are encouraged to explore this area. According to prior literature as well, transparent and clear means of applying direct influence could increase the sense of empowerment among customer-owners and their sense of truly owning the mutual (cf. Fuchs et al., 2010; Talonen et al., 2018b). Cultivating this could contribute significantly to supporting customer-owners’ loyalty to the company (Jussila & Tuominen, 2010).

Footnotes

Acknowledgements

Author Dr Antti Talonen gratefully acknowledges the support of the Foundation for Economic Education for writing of this article.

Appendix

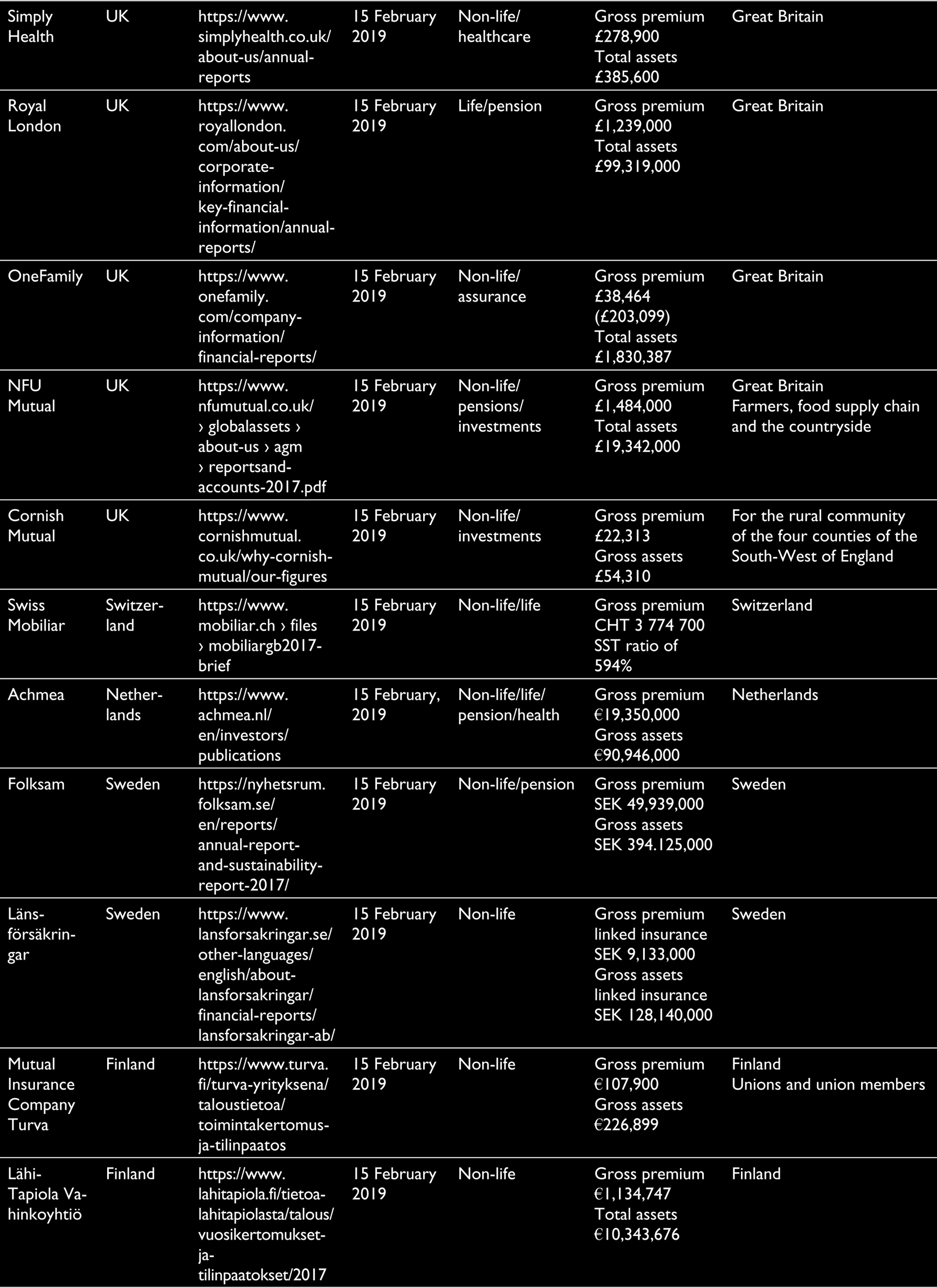

The Annual Report Sources Used in the Research

| Name of the Mutual | Country of Origin | Location of/Path to the Annual Report | Date of Data Access | Line of Insurance (non-life/life/pensions) | Annual Premium/Assets (in thousands) | Customer-Owner Segment (profession/industry/georgraphical area) |

| IPB Insurance | Ireland | 15 February 2019 | Non-life | Gross written premium €162,200 Total assets €1 270 025 |

Ireland |

|

| American Agriculture Insurance Company | USA | 15 February 2019 | Non-life | Written premium US$363,000 Total assets US$1,338,000 |

America For farmers and agricultural companies |

|

| Aegis | USA |

|

15 February 2019 | Non-life | Gross written premium US$1,344,705 Total assets US$6,512,136 |

North America Energy Industry |

| EMC Insurance Group, Inc. | USA |

|

15 February 2019 | Non-life | Premium US$607,158 Total assets US$1,681,940 |

USA |

| Securian | USA |

|

20 March 20 2020 | Life | Premium, policy and contract fees US$4,588,000 Total assets US$51,232,000 |

USA |

| Thrivent | USA | 15 February 2019 | Life Mutual fund/investment |

Total premium US$5,020,628 Total assets US$90,968,818 |

USA Christians |

|

| UIA (Insurance) Limited | UK |

|

15 February 2019 | Non-life | Gross premium £23,949 Total assets £83,328 |

Great Britain |

| Simply Health | UK |

|

15 February 2019 | Non-life/healthcare | Gross premium £278,900 Total assets £385,600 |

Great Britain |

| Royal London | UK | 15 February 2019 | Life/pension | Gross premium £1,239,000 Total assets £99,319,000 |

Great Britain | |

| OneFamily | UK | 15 February 2019 | Non-life/assurance | Gross premium £38,464 (£203,099) Total assets £1,830,387 |

Great Britain |

|

| NFU Mutual | UK | 15 February 2019 | Non-life/pensions/investments | Gross premium £1,484,000 Total assets £19,342,000 |

Great Britain Farmers, food supply chain and the countryside |

|

| Cornish Mutual | UK |

|

15 February 2019 | Non-life/investments | Gross premium £22,313 Gross assets £54,310 |

For the rural community of the four counties of the South-West of England |

| Swiss Mobiliar | Switzerland | 15 February 2019 | Non-life/life | Gross premium CHT 3 774 700 SST ratio of 594% |

Switzerland | |

| Achmea | Netherlands |

|

15 February, 2019 | Non-life/life/pension/health | Gross premium €19,350,000 Gross assets €90,946,000 |

Netherlands |

| Folksam | Sweden | 15 February 2019 | Non-life/pension | Gross premium SEK 49,939,000 Gross assets SEK 394.125,000 |

Sweden | |

| Länsförsäkringar | Sweden | 15 February 2019 | Non-life | Gross premium linked insurance SEK 9,133,000 Gross assets linked insurance SEK 128,140,000 |

Sweden | |

| Mutual Insurance Company Turva | Finland |

|

15 February 2019 | Non-life | Gross premium €107,900 Gross assets €226,899 |

Finland Unions and union members |

| LähiTapiola Vahinkoyhtiö | Finland |

|

15 February 2019 | Non-life | Gross premium €1,134,747 Total assets €10,343,676 |

Finland |

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.