Abstract

The purpose of this study is to examine the role of trust on the CSR and brand-equity nexus in the banking sector of Bangladesh. Using the convenient sampling method and structured questionnaire, the study conducted an online survey of 275 customers of private commercial banks from Bangladesh. This study applied structural equation modelling (SEM) to define the complete structural model to analyse the direct and indirect relationships between study constructs. The results reveal a positive and significant impact of CSR on brand equity. Regarding the mediating effect of trust, the study found a significant impact of trust on the CSR components and the brand-equity nexus. The study’s outcomes enrich the existing literature as a dimension of trust is added as mediating effect on the CSR and brand equity relationship in Bangladesh.

Introduction

Over the last few decades, corporate social responsibility (CSR) has been regarded as an important brand management tool by researchers and practitioners (Ali & Kaur, 2021). Along with traditional marketing activities, CSR is commonly used as major marketing tool for the brand equity. CSR is an essential portion of brand equity (BE) as it can build the positive image in the customer’s mind and finally impact on the purchase decision (Ali & Kaur, 2021; Baalbaki & Guzmán, 2016). Additionally, CSR activities could benefit companies by creating moral capital and supporting intangible assets like BE (Melo & Ignacio, 2011). Vishwanathan et al. (2019) argued that customers not merely prioritize the products but rather give importance to company practices also. In order to enhance the reputation in the market place, policy-makers advocate for the involvement of sustainable business activities (Khan et al., 2021). As a part of the service industry, banking organizations’ brand value can be enhanced by undertaking CSR events like promoting social programs and welfare activities. After the global financial crisis, CSR can be used as an important tool to rebuild the trust and corporate image for the banking sector (Kaeokla & Jaikengkit, 2013; Roberto Scharf et al., 2012).

In the banking sector, trust plays an indispensable role in constructing brand loyalty (Ndubisi et al., 2007). Trust can increase the repurchase behaviour and long-run relationship with the customers (McDonald & Rundle‐Thiele, 2008). In the recent days, banking sectors are using CSR as their major marketing strategies for satisfying their customers. Kim and Lee (2019) argued CSR activities enhance trust of customers which lead to higher brand credibility. Park et al. (2014) mentioned the importance of examining the impact of trust on CSR activities. From a CSR viewpoint, trust has been regarded as an anticipation of customers about ethical behaviour or socially responsible activities from companies (Vlachos et al., 2009). Most of the previous studies have taken corporate reputation and brand credibility (Hur et al., 2014); customer satisfaction (Hsu, 2012); corporate branding as mediating variables between CSR and brand-equity association. Thus, mediating mechanism of trust is a new area of interest of the researchers (Chaudhuri & Holbrook, 2001). Only a few researches, that is, the study of Fatma et al. (2015) examined the mediating influence of trust between CSR and BE. But their study only showed the effect of CSR as a single construct and did not consider various dimensions of CSR in creating trust and BE. A recent study of Huo et al. (2022) examined the role of CSR in improving sustainable purchase intentions and showed the mediating roles of brand trust and brand loyalty in the context of textile industry of Pakistan. In their study, brand trust was identified as a possible link between CSR and brand loyalty. Bugandwa et al. (2021) emphasized more rigorous studies are required to explore the relationship between the CSR and trust. Therefore, we can say that trust raised as a potential mediator between CSR and brand-related outcomes.

Following other developing countries, the Central Bank of Bangladesh started CSR and green banking operations in 2008 (Bangladesh Bank, 2015). Hence, banking sector is the pioneer of starting CSR activities in Bangladesh. That initiative in the financial sector encouraged to accelerate the wisdom of CSR arrangements of financial institutions through direct budgetary expenditure and financial inclusion efforts (Bangladesh Bank, 2015). As per CSR-spending guidelines of the Central Bank of Bangladesh, banks, and non-bank financial institutions have to expend 2.5% of their net profits on CSR activities (Bangladesh Bank, 2015). As illustrated in the annual report (2019–2020) of the Central Bank of Bangladesh, the total amount of CSR expenditure by banks and non-bank financial institutions was BDT 9399.67 million in the financial year 2020; where banks expended BDT 9255.1 million. (Bangladesh Bank, 2022a) According to Ahmed (2020), CSR activities have become a global phenomenon which also made these practices an influential sign of brand image. Therefore the emphasis on CSR in Bangladesh would be beneficial not only for developing corporate governance, community development and environment management but also for economic development and ensuring long-term BE (Ahmed, 2020). As the banking sector is a competitive sector and huge commercial banks already operate in Bangladesh, it is now very tough to create long-term BE in this sector. Many banks offer varieties of selection criteria and effortless switching options to customers. As a result, consumer behaviour is also changing day by day. Customers are now seeking trustworthy banks, which fulfil the banking need of a customer as well as the need of a broader environment, that is, society and beyond. From this standpoint, authors realize that it is high time to determine the effect of CSR in creating BE in Bangladesh banking sector.

Based on the above rationale, the current study offers a deeper understanding by examining a conceptual model postulating the direct and indirect (through trust) relationships between CSR components and BE. This study was conducted to fulfil two specific objectives. The first objective is to examine the effect of customer perception of CSR components on BE. Second, this study analyses the mediating mechanism of trust in CSR components and BE interactions.

By providing empirical evidence through the present study, it is hoped that existing research on CSR can be extended to a new dimension as, such kind of study is very rare in Bangladesh. This gap will be filled by the current research by showing how CSR influences BE through mediation of trust. Among the various contributions of this study, the most important one is that as stated by Vogel, 2006 — CSR influences are varied among various service sectors. This article empirically examines the impact of CSR’s four dimensions on BE and customers’ trust in association with the banking service industry where little research has been done. Another contribution of this research is that it highlights the significance of CSR insights for building BE through the explanation of how organizations can expand their understanding of CSR activities and how they can make successful brand-building strategies. So, this unified investigation may assist the decision-makers in understanding the CSR components and their effects on BE and the influence of trust on this effect. The results of the study will be practically applicable to prospective CSR approaches aimed to boost BE.

This research article is designed as follows: the second section offers a review of existing literature and a conceptual framework indicating the hypothesized relationships among CSR, BE and trust. Then, data and methodology of the study has been included in the third section. Next, in the fourth section the results of the analysis has been given with a comprehensive discussion in the fifth section. Then, study limitations with future research directions are presented in the sixth section. At last, conclusion and managerial implications are added in the seventh section.

Literature Review and Conceptual Framework

Literature Review

All types of organizations consider CSR a universal idea, and banking organizations are reasonably being delicate to its advantages (Fatma & Rahman, 2015). According to Poolthong and Mandhachitara (2009), banking companies are involved in CSR activities to attain an optimistic customer insight about the service quality. Most importantly, customers are now emphasising business’s social value and expressing their preference of CSR in banking and other service sectors (Fatma & Rahman, 2016). Perez and Bosque (2013) mentioned that community development, legal and ethical concerns, social banking, etc. are now standard practices of banks in addition to their traditional offering of economic benefits. In the Bangladesh banking industry, Khan et al. (2009) conducted a study concerning CSR activities and found that banks voluntarily accepted CSR reporting and customers possess positive reactions to CSR actions. In addition, Mahbuba and Farzana (2013) stated that a remarkable advancement of CSR activities in the banking sector of Bangladesh had been witnessed.

According to Orlitzky et al. (2003), CSR offers both outer (corporate reputation, BE) and inner (capabilities, competencies) rewards by acting as an organizational resource. If intangible resources (e.g., BE, corporate reputation) is exceptional, worthy and unique they can sustain the competitive advantage (Hur et al., 2014). Guzman and Davis (2017) studied the effect of CSR on BE and found that CSR influences BE via customers’ attitudes formed by differential effects of two forms of brand–cause fit. A study by Hsu (2012) on life insurance policyholders in Taiwan found that policyholders’ perceptions of CSR performance positively affect corporate reputation, BE, and customer satisfaction. A similar study in the context of Indian banking industry by Fatma et al. (2015) revealed that CSR has a direct influence on corporate reputation and BE. Customers’ perceptions of CSR can influence BE and brand performance (Lai et al., 2010).

Morgan and Hunt (1994) stated that trust remains when one has an assurance of others’ integrity and reliability. In addition, Nelson and Kim (2021) stated that trust is indispensable for enhancing cooperation. From the consumer perspective, trust is assumed as the belief of consumers that companies will execute all activities according to their expectations (Park et al., 2014). Delgado‐Ballester and Luis Munuera‐Alemán (2001) defined brand trust as the assumption of security while choosing a brand. In addition, Singh and Agarwal (2013) indicated CSR programs are organized to shelter company reputation and encourage consumer trust. Vlachos et al. (2009) revealed that distrustful buyers are seriously impacted by unfavourable CSR actions that directly affect their buying intention and trust. They also suggested that trust can positively affect the CSR and financial performance relationship. According to Le et al. (2021), consumers who hold trust on the brand are predicted to have a positive outcome. Previous branding researches proved that, powerful brands can form a strong communication, and satisfy the promises made (Batt et al., 2021). A critical study by Kim et al. (2015) explored that CSR perception of consumer is the precursor of brand trust, which also have a mediation effect on the relationship of CSR, reputation, and corporate hypocrisy. Besides the significance of trust on CSR actions, trust is also central to BE as it could be a vital figure of any fruitful relationship (Morgan & Hunt, 1994).

Some previous studies (Hur et al., 2014; Muniz et al., 2019) investigated the relationship between CSR and BE. But, facts regarding the clarification of CSR and customer-based BE are very rare. Hence, there is a dearth of research to identify the influence of four major CSR components (economic, legal, ethical and philanthropic) on BE. Furthermore, the mediation effect of trust on BE through specific CSR components is unrevealed yet. Hence, a gap is identified as how trust influences the relationship between CSR components and BE. Moreover, in developing countries like Bangladesh, there is a scarcity of empirical study on this issue. Identification of these research gaps encouraged the authors to conduct the current research.

Conceptual Framework

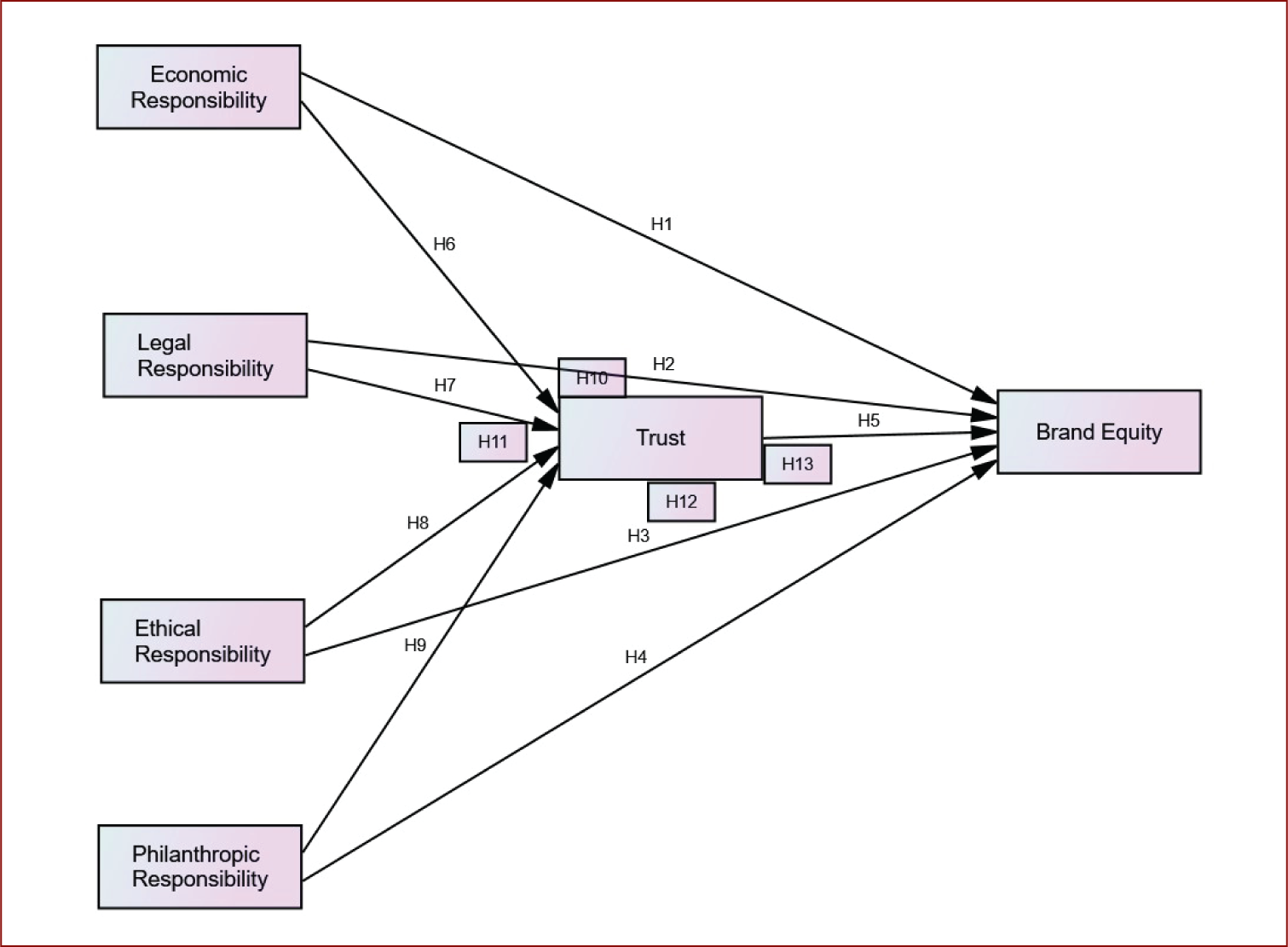

Based on the above justification, the present study proposes a conceptual model incorporating four predictor variables (i.e., economic responsibility, legal responsibility, ethical responsibility and philanthropic responsibility) as the components of CSR with one mediating variable (trust) to test the effect of CSR on BE of private commercial banks of Bangladesh (Figure 1).

Hypothesis Development

Based on the proposed model, thirteen hypotheses were developed to test in this study. The supports behind the hypothesized relationships with related literature are included.

Moreover, philanthropic activities in the practice of donations are regarded as CSR in developing countries (Crane & Matten, 2012). Regarding the long-term brand relationship, philanthropic activities affect customer’s and other stakeholder’s perception about the business (Brammer & Millington, 2005). Furthermore, Rodríguez et al. (2017) investigated the dimensions of CSR and BE and confirmed that CSR has four dimensions as stated by Carroll (1991) and BE been reflected in traditional categories. In addition, they showed the existence of a significant relation between CSR and customer-based BE. Basing on the discussion about CSR and brand-equity relationship, the following hypotheses were proposed:

Chen and Park (2020) examined the relationships among BE, satisfaction and use intention from the perspective of Chinese tourists by taking trust as a moderating variable. They revealed that brand image and brand awareness in airline’s BE have a positive impact on satisfaction. In addition, their study confirmed that, trust has a positive effect as a moderating variable in relation to BE and satisfaction. Besides, the study of Delgado‐Ballester and Luis Munuera‐Alemán (2005) revealed that brand trust is embedded in the result of previous experience with the brand. They also stated that trust is positively related to brand loyalty, which positively relates to BE. Although their result of brand trust does not show a full mediation effect recommended by Morgan and Hunt (1994), it helps to explain BE better. According to Song et al. (2019) trust is considered as a critical part of a business as the corporate image is shaped by trustworthy undertakings of a firm. Chen (2009) explored that trust, brand image and satisfaction are positively related to BE. Likewise, Ambler (1997) stated that customer trust is a significant factor of BE. Furthermore, Jevons and Gabbott (2000) and Kim et al. (2008) showed that BE is positively affected by customer trust. Credibility as well as trust is considered as a key factor of BE (del Barrio-García & Prados-Peña, 2019). Brand credibility can influence brand credibility by refining insights of brand quality and usefulness (Spry et al., 2011). They also claimed that credibility upholds customer-based brand equity (CBBE).

Thus the following hypothesis was postulated:

A recent study by Sharma and Jain (2019) examined the effect of perceived CSR initiatives on consumer-based BE and brand loyalty where they found positive and direct relationships between CSR and consumer trust as well as consumer trust and CBBE. Besides, Hansen et al. (2011) empirically proved that CSR is related to trust in top management. A study on CSR communication process by Kim, 2017 confirmed the positive influence of CSR communication factors on consumers’ CSR knowledge, trust and perceptions of corporate reputation.

Therefore, embracing the four main components of Carroll’s CSR model, the following four hypotheses were proposed:

Based on the above discussions, the following four hypotheses were proposed:

Data and Methodology

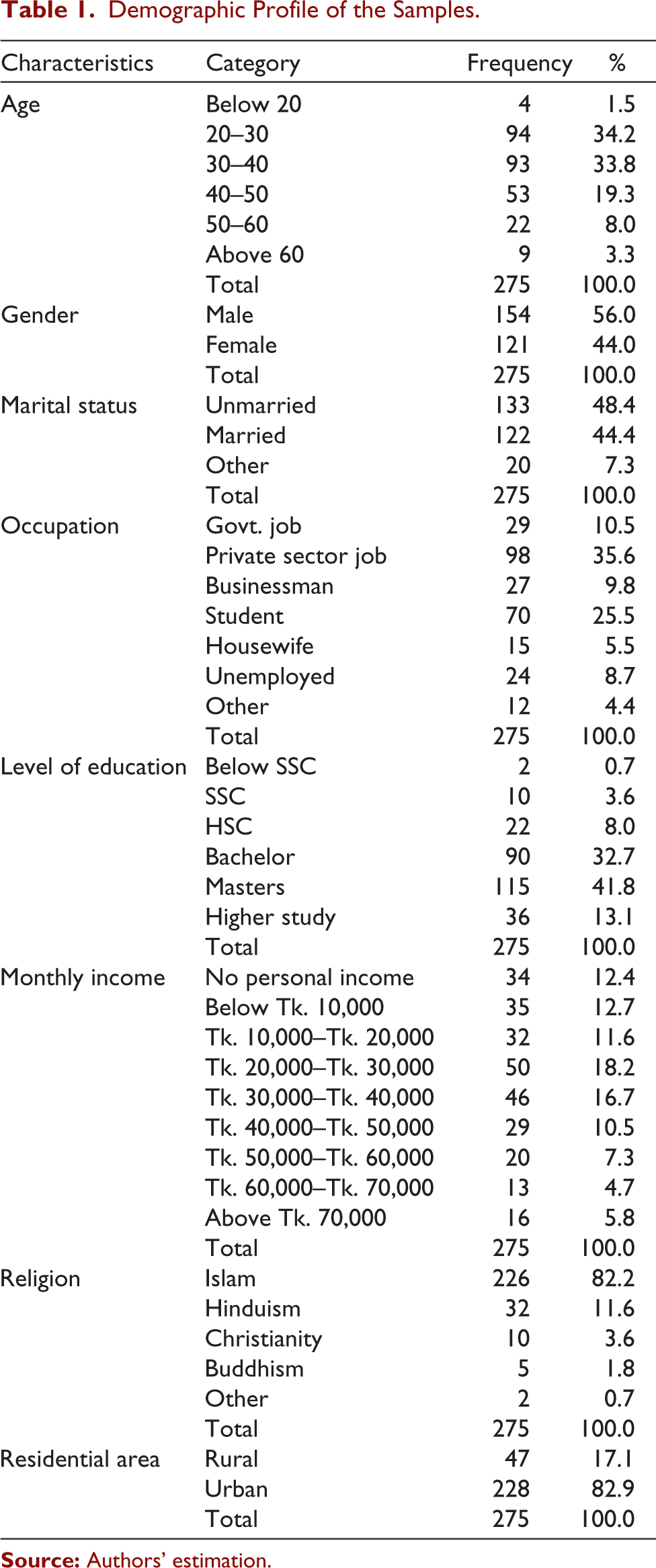

Kline (2005) gave sample size guidelines for structural equation models. He said that a sample of 100 is small, a sample of 100–200 is medium, and a sample over 200 is large. This study is taking appropriate sample size based on population size as well. The target population of this study is the customers of private commercial banks of Bangladesh. Cross-sectional data were collected by following the convenience sampling method. Regarding the sampling unit, there are 43 private commercial banks currently operating in Bangladesh (Bangladesh Bank, 2022b) and data collection was done covering all the banks through an online survey. Initially, 290 responses were gathered from the online survey. This study mainly focused on structural equation modelling (SEM). Structural equation modelling has one important requirement that 15 respondents should be included for each of the factor assessed (Hair et al., 1998). Therefore, 290 sample size fulfils this condition. Among the 290 responses, 15 had to be discarded because of respondent error. The remaining 275 is regarded as the sample size of the study. The sample profile of the study is included in Table 1.

Demographic Profile of the Samples

Among 275 samples, the highest proportion (34.2%) belonged to the age category of 20–30, followed by 30–40 years (33.8%). At the same time, responses from the below 20 years and above 60 years are lowest (1.5%–3.3%). The majority of the respondents were male (56%) and unmarried (48.4%). Regarding occupation, the maximum respondents were private-sector job holders (35.6%) followed by students (25.5%). About 41.8% of respondents had a master’s degree followed by bachelor degree (32.7%), and the majority (18%) had mid-ranged personal income (Tk. 20,000–Tk. 30,000). A vast majority (82.2%) of the respondents were Muslims and lived in the urban area (82.9%) of Bangladesh.

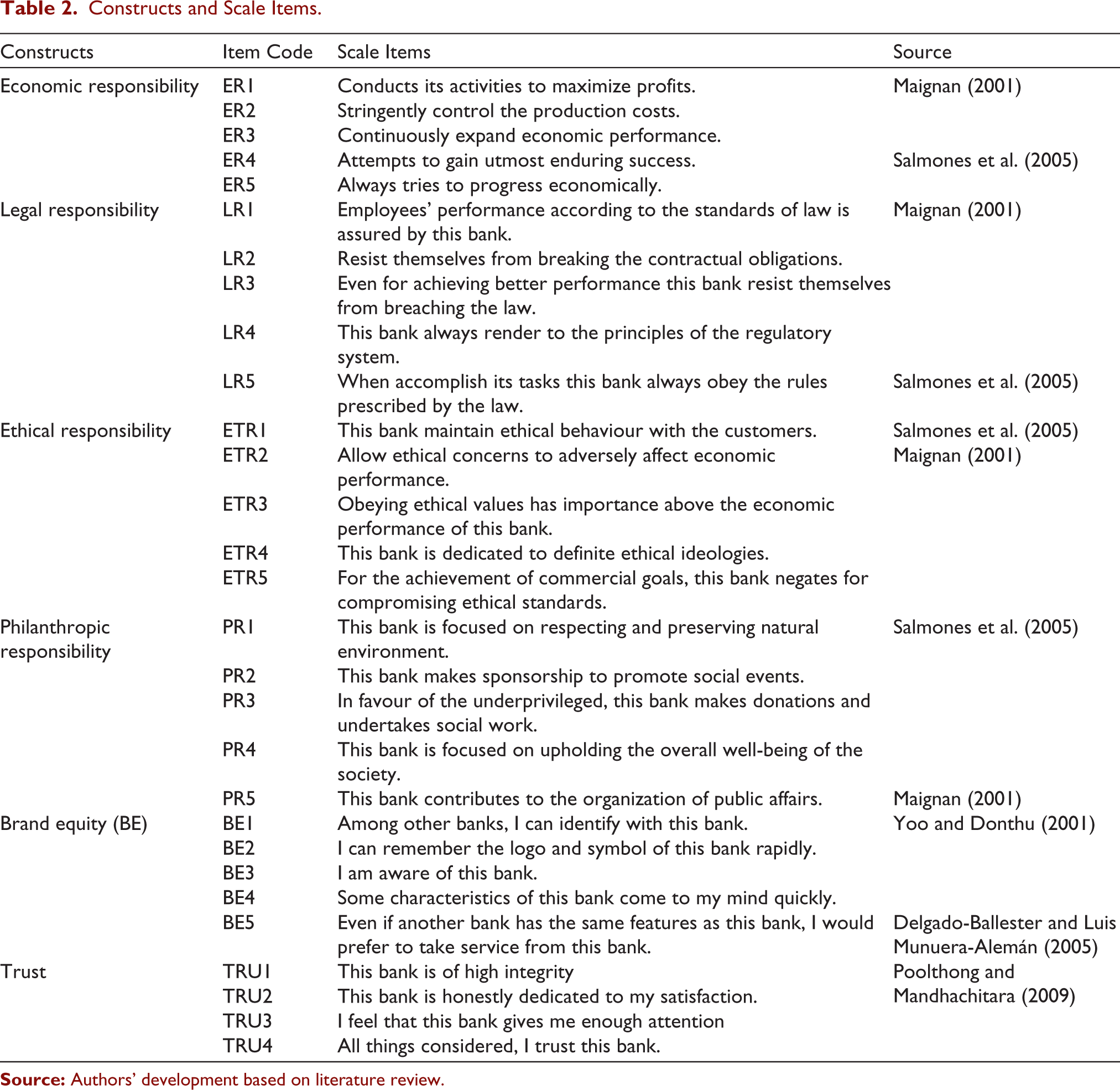

The main instrument used in this study was a structured questionnaire including seven sections. A 7-point Likert scale was used to measure the items as Likert’s scale is recommended for assessing marketing and brand-related studies (Brakus et al., 2009). Respondents’ familiarity of CSR initiatives undertaken by the particular bank facilitated to collect consistent reliable and valid answers. For further understanding, instructions had been provided at the beginning of the questionnaire and brief explanation of various terms had been included with the questionnaire items. Besides, confidentiality of respondent data was guaranteed.

In this study, authors followed Carroll’s definition (1979) of CSR and applied his four-domain pyramid framework due to the vast acceptance and application by many theorists and empirical investigators (i.e., Strong & Meyer, 1992). To measure the four components of CSR, the items were adapted from Maignan (2001) and Salmones et al. (2005)’s survey instrument.

Between the two approaches (perception related and behaviour related) to measure customer-based BE, authors omitted behavioural variables as there is only a weak link of CSR to behavioural variables (Bhattacharya & Sen, 2004). As stated by Yoo and Donth (2001), because of the absence of discriminate validity, it is needed to group brand awareness and brand associations. Recommended by Yoo and Donth (2001), the strength of CBBE was tested by Washburn and Plank (2002). They indicated that, the best parsimonious model can be created when brand awareness and brand associations are combined. Moreover, Keller (1993) also explained BE as a distinct construct where brand awareness and brand associations are merged. So, in this study BE was measured with the four-brand awareness items proposed by Yoo and Donthu (2001) and one-brand association item by Delgado‐Ballester and Luis Munuera‐Alemán (2005), which were in line with the definition of BE proposed by Keller (1993).

In this study, authors accepted a multi-dimensional approach to measure trust as suggested by Morgan and Hunt (1994) and Sirdeshmukh et al. (2002), which were vastly applied in previous researches (e.g., Chaudhuri & Holbrook, 2001; Delgado‐Ballester & Luis Munuera‐Alemán, 2001). Precisely, trust was measured by four items following Poolthong and Mandhachitara (2009) study. All the measurement scale items are presented in Table 2 with corresponding sources.

Constructs and Scale Items

This study applied SEM, a multivariate approach to analyse covariance structure, latent variable analysis, CFA, path analysis and structural relations in a linear manner (Hair et al., 1998). Using AMOS tools, SEM was done to estimate the strength of causal linkage between the variables. Subsequently, SEM was conducted to define the complete structural model to analyse the direct and indirect relationships between study constructs. Using MLE (maximum probability evaluation), this research carried out SEM to understand the estimation of the model parameters. Chi-square, goodness-of-fit (GFI), adjusted goodness of fit index (AGFI), comparative fit index (CFI), root mean square error of approximation (RMSEA) and standardized chi-square (Bollen, 1989; Jöreskog, 1969) were used for the study’s model fitness. Finally, the mediation test was performed through cumulative effects, direct effects and indirect field variables.

Results of the Analysis

Composite Reliability and Average Variance Extracted for Constructs

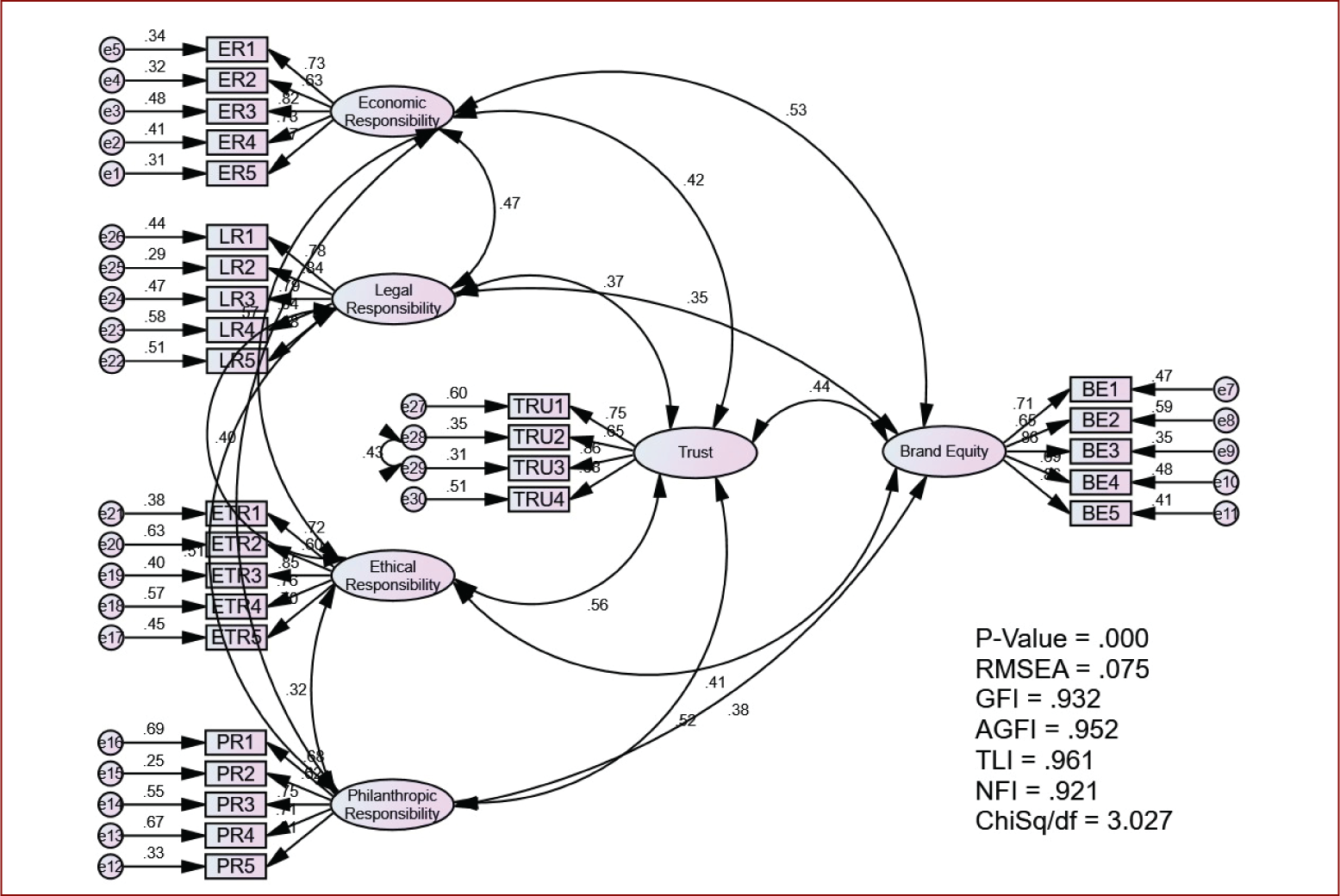

To explore sampling adequacy, this study has been done Kaiser-Meyer-Olkin (KMO) and Bartlett’s test of sphericity, where the results are variance explained = 40%, KMO = 0.912, Bartlett’s test of sphericity (BTS) chi-square = 1935.40 (p = 0.000). The results show that the sample is suitable for factor extraction (Hair et al., 1998). A measure of content validity is ‘how illustrative and comprehensive the pieces were in making by the scale’ (Bohrnstedt, 1970). By examining the process by which scale objects were made, this investigation appraised them (Straub, 1989). After conducting a thorough assessment of the literature, which helped to define the items and constructs, this study conducted a number of tests utilizing SEM in order to verify the relevant validity (Hoyle & Smith, 1994). The convergent validity of a model is increased when the factor loading is higher. Higher discriminant validity may result from improved content validity and increased average variance explained (Alam et al., 2014; Borsboom et al., 2004). To supplement the validity scores, a CFA was performed.

Besides, composite reliability (CR) of the scales was measured, and it is found that all CR values are greater than recommended cut-off point of 0.60 (Bagozzi & Yi, 1988). Next, average variance extracted (AVE) was assessed to test convergent validity. Suggested by Hair et al., 1998, this study further assures the validity of constructs as all of the AVE values are not smaller than 0.50. In addition, the researchers conducted discriminant validity by incorporating the correlation score between the components and testing the confidence interval (Kline, 2005). Similarly, the researchers in this study estimated the variables’ confidence intervals which is 95%. This study’s discriminant validity was reinforced by the absence of any such value in any of the intervals studied (Torkzadeh et al., 2003).

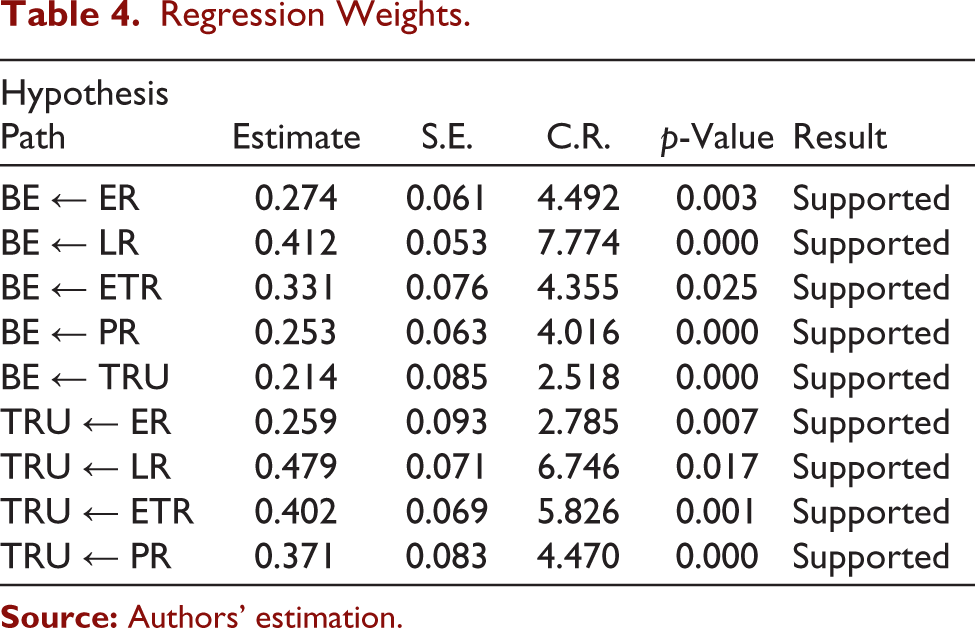

The path coefficients of the structural model are presented in Table 4. The path coefficient value of 0.15 and higher is considered statistically significant (Hair et al., 1998). Following this standard, this study showed that standardized path coefficient between economic responsibility and BE is 0.274, which confirmed the acceptance of hypothesis one. Likewise, this study showed the relationship between legal responsibility and BE as the standardized path coefficient is 0.412. Hence, hypothesis two is accepted. Similarly, hypothesis three is also accepted in this study as the standardized path coefficient between ethical responsibility and BE is 0.331 (p ≥ 0.05).

Regression Weights

In this study, the significant positive relationship between philanthropic responsibility and BE is ratified (standardized path coefficient is 0.253), which supports hypothesis four. Next, hypothesis five is also accepted because standardized path coefficient between trust and BE is found to be 0.214. This study also confirms a significant positive relationship between economic responsibility and trust (standardized path coefficient = 0.259). Therefore, hypothesis six is also accepted. It is found that the standardized path coefficient is 0.479 between legal responsibility and trust, which confirms the significant positive relationship between these two constructs. Therefore hypothesis seven is also accepted. The standardized path coefficient between ethical responsibility and trust is 0.402, which assures the existence of a significant positive relationship. So, hypothesis eight is also supported. This study also confirms that a significant positive relationship exists between philanthropic responsibility and trust as the standardized path coefficient is 0.371. Therefore, hypothesis nine is also accepted. So, all hypotheses regarding direct relationships of the proposed model are established in this research.

Findings and Discussion

The result section indicates that four CSR components have direct and positive impacts on BE. This finding is similar to the finding of Hafez (2018) who also conducted study in the context of Bangladesh banking industry. Furthermore, this outcome is in agreement with the previous research of Lai et al. (2010) and Hur et al. (2014). Among the four CSR components, legal responsibility shows the highest impact on creating BE. The possible explanation behind this finding may be customers now think that banks should not operate to fulfil the earnings motive only and conform to the legal guidelines and policies below which commercial enterprise ought to perform. Besides, Carroll (1991) also stated that companies are expected to chase economic operations following the basis of law. Furthermore, legal responsibilities get highest priorities in developed economies among other magnitudes of CSR (Rahim et al., 2011).

Next, ethical responsibility shows the second-highest impact on creating BE. The probable cause behind this finding may be banks are now offering almost the same services, and customers are influenced not only by their offerings but also their ethical behaviour. Rahim et al. (2011) stated that unless just following laws and regulations, economic and ethical responsibilities are reflected as principal values of CSR. Then the economic responsibility has the third-highest impact. This finding is contrary to the existing literature. It is considered that economic responsibilities are gaining the greatest importance in developing and developed countries as prescribed by Carroll’s original work (Planken et al., 2010). Among the four components of CSR, philanthropic responsibility shows the lowest impact to build BE though the relationship is significant. Therefore this finding contradicts the findings of Visser (2005) and (Flandez, 2013) because they showed that in case of developing economies, philanthropic responsibility is regarded as the most imperative aspect in the customer decision-making process, after quality and price. The possible explanation behind our finding in developing countries like Bangladesh is that philanthropic or voluntary donations may be beyond the customer’s expectations.

The study results also showed that customer trust has a direct and positive impact on BE, which is similar to the previous study (Chen, 2009). Besides, this study also confirmed that different components of CSR (economic, legal, ethical and philanthropic responsibilities) have a direct and positive impact on building customer trust in banking activities. This finding is similar to the previous findings (Sharma & Jain, 2019), who also found positive and direct relationships between perceived CSR and BE; consumer trust and BE, and perceived CSR and consumer trust. Similarly, Iglesias et al. (2018), Tian et al. (2011) and Singh and Verma (2019) also found a direct relationship between CSR and customer trust.

The most important finding of this study is the mediating role of trust in the relationship between CSR components and BE. However, some previous studies tested and confirmed the mediation effect of corporate image and brand awareness (Hafez, 2018), brand awareness, brand image, brand loyalty, and purchase intention (Singh & Verma, 2019) between the relationship of CSR and BE rather than testing customer trust as a mediator. Therefore, the present finding is in line with Fatma et al. (2015), who also demonstrated the mediating role of trust between CSR and BE. Their study showed that CSR activities build consumer trust in a company, which positively impacts BE and corporate reputation. But, their study did not show the effects of four individual CSR components. The present research finds out the mediator role of trust in between the relationship of each of the CSR components and BE.

Regarding the indirect relationships, legal responsibility shows the highest degree of impact, and ethical responsibility offers the second-highest degree of effects to build customer trust in banking services. This finding agreed with previous finding of Kim et al. (2021) who showed that legal and ethical responsibility has the highest meaning for brand trust. But philanthropic responsibility shows more impact than the economic responsibility to build trust. This means that the power of indirect effect (through trust) is higher for the philanthropic responsibility than direct effect to create BE. So, it is evident that impacts of specific CSR components have been changed when customer trust is considered, which is the most interesting finding of this study.

Limitations and Future Research

Notwithstanding that this study is an extensive attempt, some limitations exist, which directs for more research on this issue. This study was conducted only considering the customers of private commercial banks of Bangladesh, which might restrict the generalization of the result just in private commercial banks. Hence, further research can be conducted by also taking the customers of state-owned banks, specialized banks, and other types of financial institutions that undertake CSR activities. Meanwhile, this study was conducted by taking samples mainly from the metropolitan area. The sample size was restricted to 275 and just cross-sectional data was utilized with a convenience sampling technique. So it is suggested that, forthcoming investigation should be directed by taking a larger sample covering also the rural-area customers. As this research is limited to Bangladesh context only, future cross cultural and cross-country research should be directed to examine the proposed model. Next, this study was conducted in regard to the customer’s perception about CSR activities. Future research should be conducted by embracing the actual CSR programs. Finally, with the incorporation of additional consumer-oriented and market-based factors such as customer awareness, emotional attachment, brand performance and corporate branding, the range of the proposed model could further be expanded.

Conclusion and Managerial Implications

This study accomplished the stated objectives by testing the proposed model postulating direct and indirect (through trust) relationships between CSR components and BE. Rather than accepting the integrated approach of evaluating CSR at aggregate level, this study considered the solitary effects of CSR dimensions in brand-equity formation. Besides, indirect connections among them mediated through trust. To sum up, four types of CSR activities can create trust in banking activities, resulting in brand-equity formulation. To enhance the BE of private commercial banks in Bangladesh, current study outcome can be regarded as a foundation.

It is evident from this study that private commercial banks can enhance BE through different CSR practices and trust can boost this enhancement significantly. Thus, it is suggested by this study that CSR regarding banking sector should not be simplified with a combined measure of CSR because each type of CSR component builds BE directly and indirectly through trust.

From the managerial view point, present findings possess diverse implications for the current and future CSR-oriented banks. To begin with, each of the CSR components help in improving marketing performance (BE) of the banks. So it is suggested that through increasing concern in the field of economic, legal, ethical and philanthropic responsibilities, and banking sector can form BE. Managers must be focused on CSR and donate more funds in social activities as customers trust socially accountable businesses. In particular, legal and ethical responsibility of CSR has the most significant impact on improving BE. So, bank authority should be concerned about following the legal and ethical work environment, which may include following the laws and regulations, increasing transparency, behaving properly to customers and understanding the differences between right and wrongdoings.

Next, banks should closely monitor their activities and ensure that they are not operating only for profit maximization but also for helping the society. Rather than viewing customer trust as a temporary public relation measure, it is now necessary to accept it as a meaningful and enduring activity. In this way, deliberately overseeing CSR exercises to create trust may bring about ideal results. Our discoveries could give significant bits of knowledge to directors concerning the vital function of CSR in developing customer–brand connections.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.