Abstract

This research seeks to investigate the influence of performance expectancy, effort expectancy, facilitating conditions, habit and hedonic motivation on behavioural intention in the context of chatbot utilization within the banking industry. Additionally, the study explores the moderation effects of age, gender and personality type on the relationships between behavioural intention and use behaviour. The study employs a quantitative survey of banking customers, and the data have been analysed using partial least squares structural equation modelling and artificial neural network. The findings suggest that the use and acceptance of chatbots in banking are influenced by a range of factors, including performance expectancy, facilitating conditions and hedonic motivation. The study also reveals that only personality types can moderate the relationship between behavioural intentions and use behaviour. The study provides insights for banks and other financial institutions that are considering the implementation of chatbots as part of their customer service strategy.

Introduction

The history of chatbots reflects the ongoing progress in natural language processing, machine learning and AI technologies. As the field continues to advance, chatbots are becoming increasingly sophisticated, versatile and integral to various industries and customer interactions (Carvalho & Ivanov, 2023; Kaushal & Yadav, 2023). Chatbots have found numerous applications across various sectors due to their ability to automate customer interactions, provide instant responses and streamline processes (Caldarini et al., 2022; Luo et al., 2022). Chatbots are extensively used in customer service to handle inquiries, provide support and resolve common issues. Chatbots are used in the banking sector to answer customer queries related to account balance, transaction history and basic banking services. They can also assist in money transfers, provide financial advice and help with loan applications. Chatbots are employed in the healthcare industry to offer preliminary diagnoses, schedule appointments and provide information about common ailments. Chatbots are utilized in the travel industry for booking flights, hotels and rental cars. They can provide travel recommendations, answer travel-related queries and assist with itinerary planning. In hotels, chatbots can handle guest requests, provide information about hotel amenities and offer local recommendations. Chatbots are used in HR departments to streamline recruitment processes, assist with onboarding and answer employee inquiries. They can provide information about company policies, benefits and training programmes, enhancing employee engagement and satisfaction.

Chatbots have numerous applications in the banking industry, revolutionizing customer interactions and improving operational efficiency (Adamopoulou & Moussiades, 2020; Jang et al., 2021). By leveraging chatbots, banks can provide round-the-clock support, reduce customer wait times and improve overall customer experience. Chatbots also help banks streamline routine tasks, free up human agents to handle more complex inquiries and reduce operational costs. Banks are using chatbots to perform a number of services, such as customer support, account management, product recommendations, financial planning, fraud detection, loan applications, appointment scheduling and cross-selling and upselling (Nguyen et al., 2021). Research on chatbots in the banking sector has gained significant attention due to the potential of chatbots to transform customer experiences and improve operational efficiency and primarily focuses on understanding customer preferences, improving customer experiences, optimizing chatbot performance and addressing ethical and privacy concerns (Nguyen et al., 2021).

Several studies have investigated the impact of chatbots on customer satisfaction in the banking sector. Research has shown that well-designed and intelligent chatbots can enhance customer satisfaction by providing instant responses, personalized interactions and round-the-clock support (Mehrolia et al., 2023). Chatbots have been found to reduce customer wait times, increase accessibility and improve overall customer experience. Researchers have explored the automation capabilities of chatbots in handling customer interactions. Studies have shown that chatbots can successfully handle routine customer inquiries, such as balance inquiries and transaction history requests, without human intervention (Li & Zhang, 2023). This automation of customer interactions can reduce operational costs, improve efficiency and free up human agents to focus on more complex tasks.

Understanding customer trust and acceptance of chatbots is an important research area (Silva et al., 2023). Studies have found that trust in chatbots can be influenced by factors such as transparency, accuracy and perceived competence (Wang et al., 2023). Building trust with customers is crucial for the widespread adoption and acceptance of chatbots in the banking industry. Researchers have explored the use of chatbots to deliver personalized banking experiences and recommendations (Lappeman et al., 2022). Personalization algorithms and machine learning techniques have been employed to analyse customer data and provide tailored product recommendations based on individual financial needs. Studies have shown that personalized interactions with chatbots can enhance customer engagement and improve cross-selling and upselling opportunities. Research has examined the ethical implications and privacy concerns associated with chatbots in the banking sector. Topics such as data security, privacy protection and responsible use of customer data have been investigated (Bouhia et al., 2022). Studies have explored the optimal balance between chatbot automation and human agent intervention. Research has suggested that a hybrid approach, combining the strengths of chatbots and human agents, can lead to improved customer experiences. Chatbots can handle routine inquiries, while complex or sensitive issues can be seamlessly transferred to human agents for personalized assistance (Vassilakopoulou et al., 2023). Researchers have proposed frameworks and metrics to evaluate the performance of chatbots in the banking sector (Janssen et al., 2022). Evaluation criteria include accuracy of responses, response time, user satisfaction and task completion rates. Such evaluations help banks measure the effectiveness of their chatbot implementations and identify areas for improvement.

While existing research has examined customer satisfaction with chatbots in the banking sector, more studies are needed to explore long-term user adoption and satisfaction (Kwangsawad & Jattamart, 2022). Understanding how customers’ perceptions and attitudes towards chatbots evolve over time can provide insights into improving chatbot designs, functionalities and user experiences. Research on chatbot adoption in the banking sector has been done in European and certain Asian countries; however, limited studies have been done in other parts of the world (Gatzioufa & Saprikis, 2022). A limited number of studies have used the unified theory of acceptance and use of technology (UTAUT2) and have studied performance expectancy (Jang et al., 2021), effort expectancy (Mogaji et al., 2021), facilitating conditions (Yang et al., 2023), hedonic motivation (Cheng & Jiang, 2020) and habit (Husain et al., 2022) as predictors of behavioural intention of users in the banking sector. The moderating effect of age and gender is studied in the paper as in the UTAUT2 model (Dehnert & Schumann, 2022; Dinh et al., 2023; Shandilya et al., 2023a), and the moderating influence of personality type is a novelty of the current study. Research on the moderating influence of age, gender and personality types on the adoption and usage of chatbots in the banking sector is an important and evolving area of study. While limited research has been conducted specifically on this topic, some studies have explored related aspects. The present study has been done with the following objectives:

To assess the current level of adoption and usage of chatbots in the banking sector and identify potential gaps or challenges. To examine the moderating impact of age on the adoption and usage of chatbots in the banking sector and determine whether there are significant differences in attitudes and preferences across different age groups. To investigate the moderating impact of gender on the adoption and usage of chatbots in the banking sector and explore any variations in attitudes, perceptions and behavioural patterns between males and females. To investigate the moderating impact of personality types on the adoption and usage of chatbots in the banking sector and explore any variations in attitudes, perceptions and behavioural patterns of different personality types. To assess the impact of performance expectancy, effort expectancy, facilitating conditions, hedonic motivation and habit on the behavioural intentions of users.

Traditional statistical methods such as SEM and logistic regression may have limitations when it comes to capturing complex and non-linear relationships between variables. These methods are based on certain assumptions that may not hold in all situations (Dreiseitl & Ohno-Machado, 2002). Artificial neural networks (ANNs) possess the ability to recognize patterns and relationships within extensive datasets without the need for explicit programming of specific rules or models. This attribute makes them highly suitable for analysing intricate decision-making processes, such as technology adoption. ANNs can autonomously learn from the data and uncover hidden patterns that may not be easily discernible using traditional statistical methods. By leveraging their capability to capture complex relationships, ANNs can provide valuable insights into the factors influencing technology adoption and facilitate a deeper understanding of the decision-making dynamics involved (Cubric, 2020). The integration of the SEM and ANN approaches, particularly those utilizing single hidden layers, has gained prominence within the field of technology adoption research (Mishra et al., 2023; Shandilya et al., 2023b). This combination of methods has become more prevalent as researchers seek to leverage the strengths of both SEM and ANN to enhance their understanding of technology adoption processes. By integrating SEM, which offers a framework for modelling complex relationships among latent and observed variables, with ANN’s ability to capture non-linear patterns and intricate associations in data, studies in the technology adoption domain can attain a more comprehensive and nuanced analysis of the factors influencing technology adoption (Almarzouqi et al., 2022). Thus, the current study uses a combined SEM and ANN approach to understand the adoption and use of chatbots in the banking industry.

Literature Review

In the wake of the recent global pandemic, the rising prominence of hedonic shopping motivations underscores the pivotal role of phygital integration in elevating the customer financial experience (Aruldoss et al., 2023). This integration seamlessly merges physical and digital channels, presenting a unified approach that caters to diverse preferences and contributes to fostering a more inclusive and accessible financial landscape (Kumar et al., 2023). The ongoing digital technology transformation has sparked a revolutionary shift in the banking sector, fundamentally altering the landscape of financial services (Alsmadi et al., 2022). The acceptance of digital financial services is emphasized to be positively influenced by factors such as financial literacy and awareness (Al-Okaily et al., 2023). The advent of advanced technologies such as artificial intelligence, blockchain and mobile applications has reshaped the way banks operate and interact with customers. Automation and digitization have streamlined traditional banking processes, enhancing efficiency, reducing costs and expediting transactions. Additionally, the rise of online banking platforms and mobile apps has revolutionized customer interactions, providing convenient and personalized services.

The adoption and usage of chatbots in the banking sector refer to the extent to which customers and organizations in the banking industry accept and utilize chatbot technology for various banking-related tasks and interactions. Chatbots are automated conversational agents that use natural language processing and artificial intelligence techniques to engage in text or voice-based conversations with users. The adoption aspect focuses on the decision-making process of customers and banks to implement chatbots as part of their banking services (Lui & Lamb, 2018). It includes factors such as initial awareness, interest, intention and actual implementation of chatbots within the banking sector.

The usage aspect pertains to the actual interaction and engagement between users and chatbots in performing banking tasks (Mogaji et al., 2021). It involves the frequency, duration and effectiveness of using chatbots to complete various banking transactions, seek assistance or obtain information. Understanding the adoption and usage of chatbots in the banking sector is crucial for both customers and banks. Customers can benefit from the convenience, accessibility and speed of using chatbots for routine banking activities, while banks can leverage chatbot technology to provide efficient customer service, reduce operational costs and enhance overall customer experience.

Research in the adoption and usage of chatbots in the banking sector has been a topic of interest for scholars and practitioners alike (Chen et al., 2023; Jang et al., 2021; Mehrolia et al., 2023). Here are some key research areas and findings within this domain:

Performance Expectancy

Performance expectancy refers to the level of acceptance or satisfaction with the performance of a particular product, system or service. It involves assessing whether the performance of the product or system meets the expectations and requirements of the users or stakeholders (Nikolopoulou et al., 2021; Talukder et al., 2020). Research in the banking sector has shown that users expect chatbots to provide accurate and reliable information. The chatbot should also understand user queries correctly and provide relevant and precise responses. It should be able to handle a wide range of banking-related inquiries, such as account balances, transaction history, payment transfers and general banking information. A fast and efficient chatbot contributes to a positive user experience for customers in banks (Andrade & Tumelero, 2022). A limited number of studies have been done on the application of chatbots and different factors influencing behavioural intentions to use chatbots in the banking industry.

Thus, the following hypothesis is framed for our study:

H1: Performance expectancy has a positive effect on behavioural intention to use chatbots in the banking industry.

Effort Expectancy

Effort expectancy refers to the perceived ease of use and the amount of mental and physical effort required by users to interact with a chatbot (Nikolopoulou et al., 2021; Talukder et al., 2020). Effort expectancy is an important factor in determining whether or not a user will adopt a new technology, as users are more likely to use a technology that they perceive as easy to use and convenient In the context of chatbots in banking, effort expectancy can be assessed through the following factors: ease of interaction (Mogaji et al., 2021), simplicity and clarity (Illescas-Manzano et al., 2021), intuitiveness (Kallel et al., 2023) and accessibility and self-service capabilities (Mehrolia et al., 2023).

Chatbot interface has been found to be user-friendly, with clear instructions and easy-to-understand prompts, and chatbot’s responses are easy to comprehend and navigate. Research has also found that chatbots have advanced natural language processing capabilities and can be accessed conveniently, such as through websites, mobile apps or messaging platforms. Chatbots can handle a wide range of banking tasks and inquiries autonomously and, thus, help users in completing their banking activities without needing to involve human agents.

Thus, the following hypothesis is framed for our study:

H2: Effort expectancy has a positive effect on behavioural intention to use chatbots in the banking industry.

Facilitating Conditions

Facilitating conditions refer to the factors that can influence and support the formation of behavioural intentions or the likelihood of performing a particular behaviour (Alomari & Abdullah, 2023). In the context of chatbots in the banking industry, facilitating conditions play a crucial role in encouraging users to engage with chatbot services and take desired actions. If users find the chatbot interface intuitive and accessible, it enhances their intention to engage with the chatbot and seek assistance. The availability and accessibility of the chatbot service are important facilitating conditions. Users should be able to access the chatbot easily through various channels such as websites, mobile apps or messaging platforms (Dinh et al., 2023). Providing round-the-clock availability enhances convenience and encourages users to interact with the chatbot. If the chatbot is able to understand user needs accurately and provide helpful information or solutions in a timely manner, it increases user satisfaction and promotes positive behavioural intentions. Chatbots in the banking industry must comply with stringent security measures to protect user data (Yang et al., 2023). Displaying security certifications, using encryption and clearly communicating privacy policies can enhance users’ trust and their intention to use the chatbot for banking services. Offering seamless integration between chatbots and human support channels (such as live chat or phone support) provides users with a safety net and reassurance that their complex issues can be resolved. This integration can positively impact users’ behavioural intentions, knowing that assistance is available when needed. Personalization features in chatbots, such as addressing users by their names or providing tailored recommendations based on their preferences and transaction history, can enhance user engagement and satisfaction. The ability to customize the chatbot experience according to individual needs can positively influence behavioural intentions. Clear messaging about time savings, convenience, 24/7 availability or access to personalized recommendations can help users understand the value proposition and encourage them to utilize the chatbot services.

Thus, we propose the following hypothesis:

H3: Facilitating conditions have a positive effect on behavioural intention to use chatbots in the banking industry.

Hedonic Motivation

Hedonic motivation refers to the desire for pleasure, enjoyment or emotional gratification that drives individuals’ behaviours (Al-Azawei & Alowayr, 2020). In the context of chatbots in the banking industry, hedonic motivation plays a role in shaping users’ behavioural intentions to engage with and use chatbot services (Ling et al., 2021). Chatbots that are capable of providing personalized interactions and tailored experiences can trigger positive emotions and enjoyment for users (Jiang et al., 2023; Wahyuningsih et al., 2023). Introducing gamification elements into chatbot interactions can make the experience more enjoyable and engaging (Przegalinska et al., 2019). For instance, incorporating rewards, badges or virtual achievements for completing certain tasks or reaching specific milestones can evoke feelings of fun and accomplishment. Chatbots that are designed to engage users in natural, human-like conversations can evoke positive emotions and enjoyment. When users feel that they are conversing with a friendly and responsive virtual assistant, it can create a sense of enjoyment and satisfaction. This positive emotional experience can influence their behavioural intentions to continue using the chatbot for banking-related tasks. In certain situations, users may seek emotional support or empathy when using chatbots in the banking industry.

Chatbots that can recognize and respond to emotional cues effectively, such as expressing empathy or providing comforting responses, can create a positive emotional experience for users. Chatbots can also provide entertainment and deliver engaging content to users (Cheng & Jiang, 2020). For instance, chatbots can share financial tips, news updates or interesting facts related to banking and finance. By offering entertaining and informative content, chatbots can create a pleasurable experience for users, increasing their hedonic motivation and encouraging continued usage. Chatbots that incorporate social interaction features, such as the ability to share financial achievements or ask for advice from friends, can tap into users’ social needs and enhance their hedonic motivation.

By fostering social connections and facilitating social interactions, chatbots can provide users with a sense of enjoyment and satisfaction, leading to positive behavioural intentions (Foster et al., 2022). The overall user experience design of the chatbot, including visual aesthetics, ease of use and interactivity, can significantly impact hedonic motivation. A visually appealing interface, smooth and intuitive interactions and engaging design elements can create a pleasurable and enjoyable experience for users, influencing their behavioural intentions to use the chatbot.

Thus, we propose the following hypothesis:

H4: Hedonic motivation has a positive effect on behavioural intention to use chatbots in the banking industry.

Habit

Habit refers to the automatic and recurring behaviours that individuals develop through repeated performance of a specific action in a given context (Lally & Gardner, 2013). In the context of chatbots in the banking industry, the development of habit can have a significant influence on users’ behavioural intentions to engage with chatbot services (Dinh et al., 2023). When users repeatedly engage with a chatbot for their banking needs, it can become a part of their routine. Habitual use of chatbots can be driven by the convenience, accessibility and time-saving benefits they offer (Nguyen et al., 2022).

As users develop a habit of using the chatbot for various banking tasks, their behavioural intentions become more automatic and ingrained, leading to consistent engagement with the chatbot. Habit formation in chatbot usage can be driven by the perception of efficiency and speed (Kasilingam, 2020). If users consistently find the chatbot to be a quick and reliable source of information or assistance, they may develop a habit of turning to the chatbot first for their banking needs. The perceived time savings and streamlined interactions contribute to the development of habitual usage patterns. Chatbots that simplify complex banking processes and make them more accessible can encourage habit formation (Husain et al., 2022).

By providing easy-to-follow instructions, automating repetitive tasks and guiding users through various banking procedures, chatbots can help users develop a habit of relying on the chatbot for their banking needs, as it simplifies their overall experience. Habit formation is often triggered by contextual cues or reminders. In the case of chatbots, contextual triggers could include receiving notifications or reminders related to banking activities, such as bill payments, account balances or transaction updates. These triggers can prompt users to engage with the chatbot habitually, leading to continued usage. The habit loop consists of three components: cue, routine and reward (Chen et al., 2020). In the context of chatbots, the cue could be a user’s need for banking information or assistance, the routine is engaging with the chatbot to fulfil that need, and the reward is the satisfaction of obtaining the required information or completing a task efficiently. Through repeated cycles of this habit loop, users develop a strong association between their banking needs and the chatbot, leading to habitual usage.

Thus, we propose the following hypothesis:

H5: Habit has a positive effect on behavioural intention to use chatbots in the banking industry.

Behavioural Intentions

Behavioural intentions in chatbots in the banking industry refer to the attitudes and inclinations of users towards engaging with and utilizing chatbot services for their banking needs (Faqih, 2022). Understanding users’ behavioural intentions is crucial for banks to encourage adoption, increase usage and drive desired outcomes (Tan & Leby Lau, 2016). Users’ perception of the usefulness of chatbots in meeting their banking needs is a significant determinant of behavioural intentions. If users believe that chatbots can provide quick and accurate information, offer convenient services and effectively assist with their banking tasks, they are more likely to have positive behavioural intentions towards using the chatbot. The ease of use of chatbots plays a vital role in shaping users’ behavioural intentions. Users’ trust in the chatbot’s ability to handle their banking transactions securely and reliably influences their behavioural intentions. Chatbots that are perceived as trustworthy, with robust security measures, clear privacy policies and accurate responses, are more likely to generate positive behavioural intentions among users. Users’ perception of the efficiency and time-saving benefits of chatbots impacts their behavioural intentions.

Thus, we propose the following hypothesis:

H6: Behavioural intentions have a positive effect on the use behaviour of chatbots in the banking industry.

Three additional hypotheses have been formulated to check the moderating effect of age, gender and personality types on use behaviour:

H7: Age moderates the relationship between behavioural intentions and the use behaviour. H8: Gender moderates the relationship between behavioural intentions and the use behaviour. H9: Personality types moderate the relationship between behavioural intentions and the use behaviour.

Research Methodology

The research methodology employed in this study is based on a quantitative approach and utilized a multi-analysis approach combining SmartPLS and ANN to investigate the effect of various exogeneous variables, adopted from the UTAUT2 model, on behavioural intention and use behaviour. Furthermore, the study investigated the moderating influence of demographic factors such as age, gender and personality traits on the associations between the independent variables identified and the intention to engage in behaviours.

Data were collected through an online questionnaire developed using Google Forms, which was widely shared across different social media platforms to ensure a diverse and comprehensive sample. The study respondents are online banking users from India with a minimum of six months of experience in online banking services. These individuals were specifically selected for their familiarity with online banking services, reflecting a relevant sample group with first-hand experience in utilizing this technology in the Indian context.

We received a total response of 350, out of which 311 were found suitable for analysis. One of the commonly employed methods for estimating the minimum sample size in PLS-SEM is the ‘10-times rule’ introduced by Hair et al. in 2011. This method is based on the premise that the sample size ought to exceed ten times the highest number of links, either within the latent variables or from the latent variables to any observed variable in the model. In the present study, there are six links between variables, and, hence, the sample size of 311 exceeds the required number of samples.

The questionnaire comprised two distinct sections. The initial segment of the survey gathered information regarding the demographic characteristics of the participants, encompassing variables such as age, gender, income, education and personality classification. To assess the personality type of individuals as either introvert or extrovert, a subset of items from the Big Five Inventory (BFI) was applied (John & Srivastava, 1999). While the BFI typically consists of 44 items that assess different personality traits, for this study, seven items specifically targeting introversion and extroversion were adopted and included in the questionnaire. Based on the respondents’ responses to these items, they were categorized as either introverts or extroverts.

The second section of the questionnaire comprised items related to different variables, namely performance expectancy (PE-I to PE-III), effort expectancy (EE-I to EE-IV), facilitating condition (FC-I to FC-IV), hedonic motivation (HM-I to HM-III), habit (HA-I to HA-III), behavioural intention (BI-I to BI-III) and use behaviour (USE-I to USE-VIII). The scale items were adapted from UTAUT2 (Venkatesh et al., 2012). A modified version of the scale has been suggested as UTAUT3 and personal innovativeness has been added as a new variable (Farooq et al., 2017). However, a number of studies have not found personal innovativeness as a predictor of technology acceptance (Gunasinghe et al., 2020a, 2020b; Pinto et al., 2022). So, we have adapted scale items from UTAUT2 in the present study. The study employed a 5-point Likert scale to elicit responses from participants, which enabled them to express their degree of agreement on a spectrum ranging from 1 (representing complete disagreement) to 5 (representing complete agreement).

The data that were gathered underwent a thorough analysis through a process that involved two steps. Initially, the measurement model underwent evaluation through the utilization of SmartPLS, thereby guaranteeing the dependability and authenticity of the constructs. This was followed by the evaluation of the structural model where an examination was conducted on the associations between the independent variables and the intention to engage in a particular behaviour. In order to corroborate the results derived from SmartPLS, an ANN analysis was conducted, thereby furnishing supplementary verification and bolstering.

Additionally, a multigroup analysis (MGA) was conducted to investigate the moderating influence of age, gender and personality type. The present study facilitated a comprehensive examination of the impact of said factors on the associations between the designated predictor variables and the intention to engage in a particular behaviour. The study adhered to ethical principles, such as securing informed consent from participants, preserving anonymity and confidentiality and complying with pertinent ethical standards.

Result

The sample’s characteristics are elucidated through the demographic data provided by respondents. This information is presented in the order it appeared in the initial segment of the questionnaire, which focused on gathering details about respondents’ personal information.

As indicated in Table 1, the survey comprised 58.84% male participants and 41.16% female participants. A predominant segment of respondents fell within the age range of 30–40 years, constituting 58.84% of the total. Furthermore, a substantial portion of the participants, accounting for 47.91%, held graduate-level qualifications.

Demographic Details of Respondents.

Measurement Model

The empirical evidence presented in Table 2 demonstrates the reliability and validity of the constructs. The factor loadings, Cronbach’s alpha (α), composite reliability (CR) and rho_A all surpassed the suggested threshold of 0.70, as recommended by Hair et al. (2017). As per the recommendation of Fornell and Larcker (1981), it can be inferred that the convergent validity was satisfactory since the average variance extracted (AVE) values for all constructs exceeded the suggested threshold of 0.5. To evaluate the discriminant validity, which pertains to the differentiation of constructs, all inter-dimensional correlations were found to be less than the square root of the AVE which is presented in bold (refer to Table 2). In addition, to tackle the problem of collinearity, the researchers analysed variance inflation factors (VIFs) and found that all values were below 5 (see Table 3).

Reliability and Validity.

VIF Value.

Structural Model

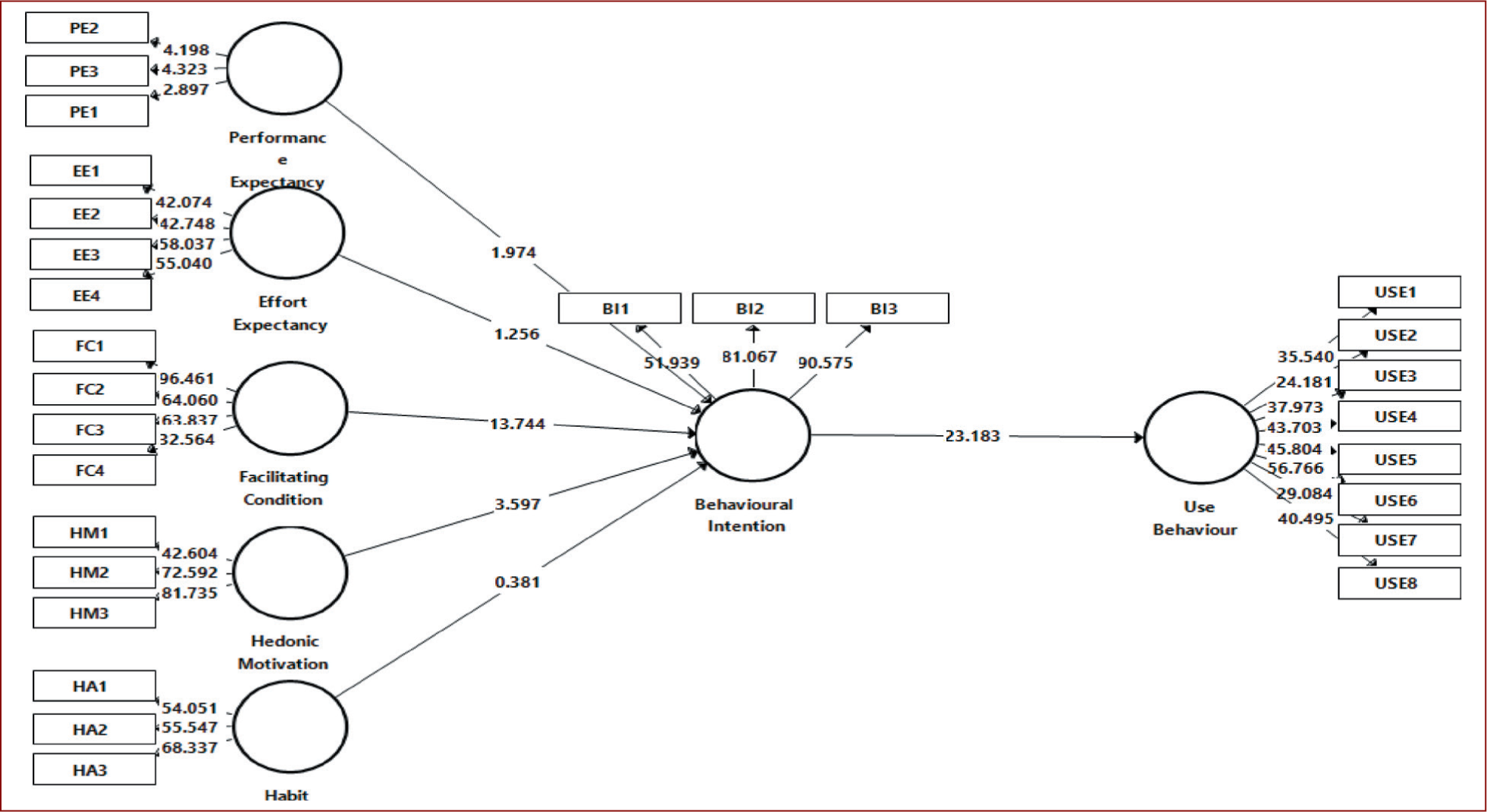

A bootstrapping procedure comprising 5,000 subsamples was conducted to scrutinize the importance of the path coefficients (Hair et al., 2014). Figure 1 indicates that our four hypotheses exhibited significant associations and that the overall model adequacy, as determined through bootstrapping, yielded significant outcomes for these hypotheses.

In order to assess the research hypotheses regarding the significance of the paths, standardized path coefficient (β) values were calculated and are displayed in Table 4. The magnitude of impact (f2) in a structural model association quantifies the extent to which exogenous constructs contribute to endogenous constructs. In accordance with Cohen (2013), our findings indicate positive f2 values for the following relationships: BI → UB 1.370, FC → BI 0.557, HM → BI 0.052, and PE → BI 0.024. Furthermore, the researchers evaluated the model’s predictive validity by calculating Stone–Geisser’s Q2. This was done using the blindfolding algorithm of SmartPLS (Ringle et al., 2015), and outcomes have been displayed in Table 5. According to the study, Q2 values were found to be more than 0, which suggests the predictive significance (Hair et al., 2014) of the construct.

Hypothesis Testing.

The coefficient of determination (R2), which explains the proportion of the variation in the dependent variable that is predictable from the independent variable(s), is depicted in Table 5. It can be observed that the R2 value of behavioural intention is 0.789 and of use behaviours is 0.578.

R2 and Q2.

The findings obtained from the smartPLS analysis indicate that the facilitating condition construct (β = 0.691) exerts the most significant influence on behavioural intention, followed by hedonic motivation (β = 0.175) and performance expectancy (β = 0.072). In addition to the aforementioned findings, an ANN analysis was also employed to provide further validation of the results.

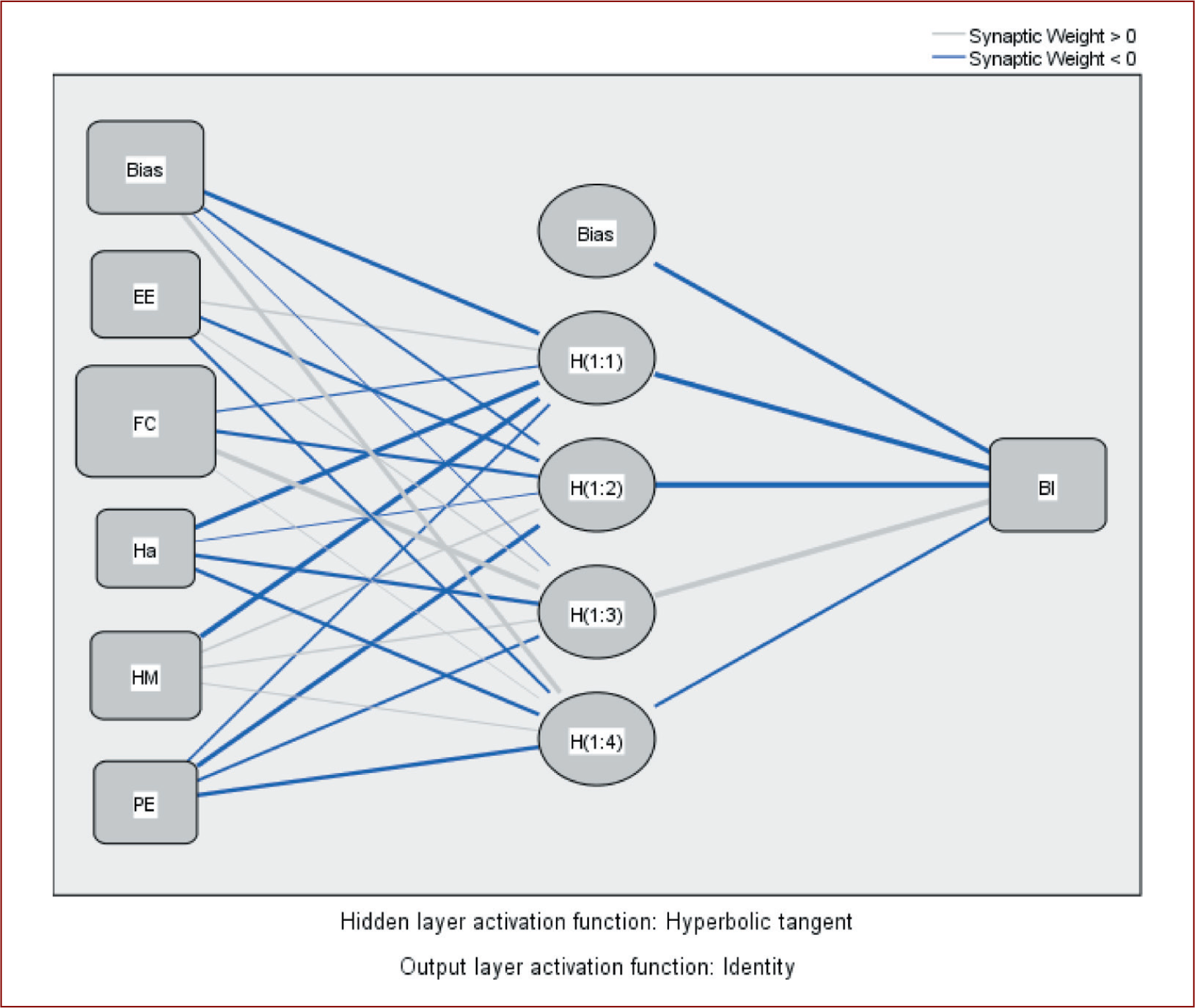

Artificial Neural Network

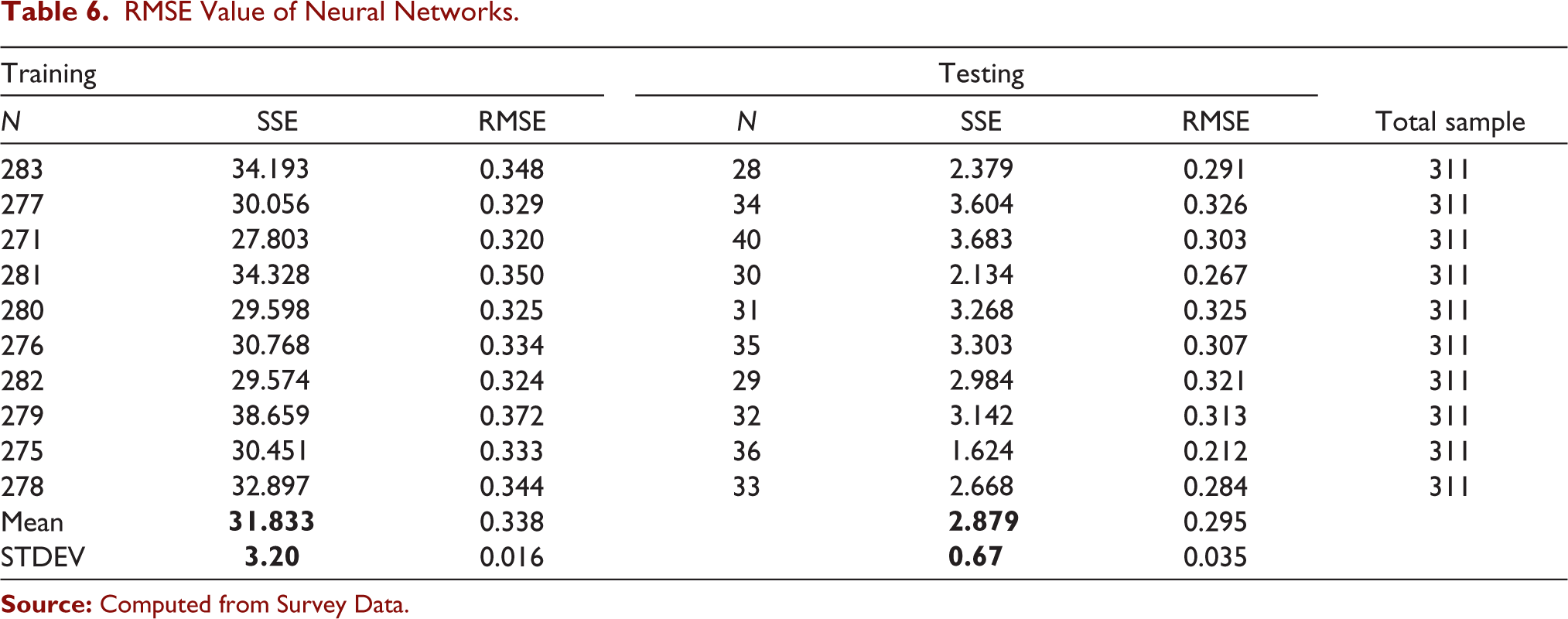

An ANN model was constructed based on the training dataset (refer to Figure 2) to forecast the dependent variables’ values using the independent variables identified in the SmartPLS model. The ANN model underwent training using 90% of the provided dataset, and its efficacy was assessed through the utilization of diverse metrics, such as the root mean squared error (RMSE). The model’s generalization capability was evaluated by employing the testing dataset (10%) for testing purposes. ANN model’s architecture comprised a single layer containing five neurons. The utilized activation functions and optimization algorithm were hyperbolic tangent and identity, correspondingly.

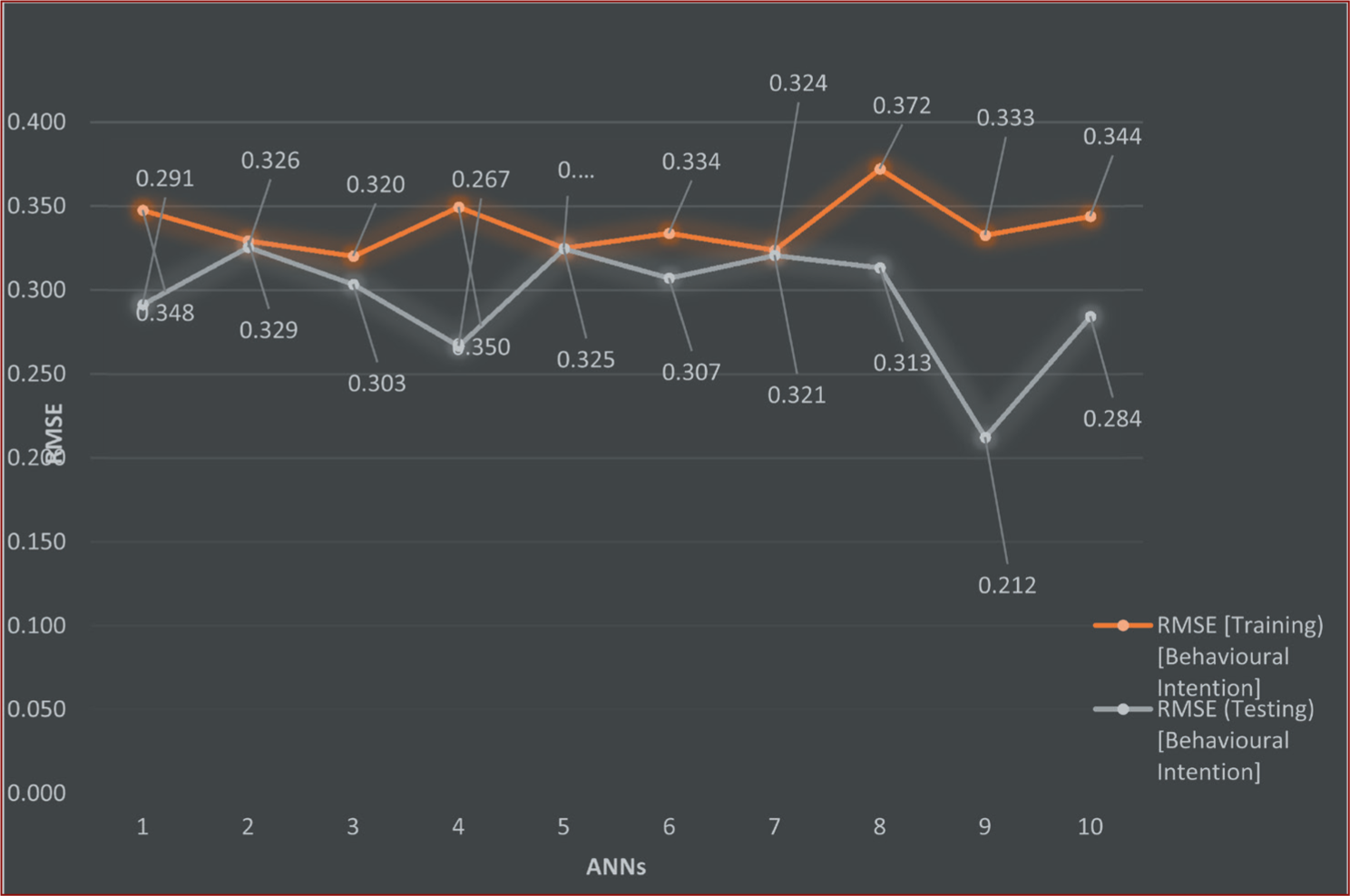

Furthermore, as depicted in Figure 3, it is evident that the RMSE values for the training and testing datasets are notably minimal, measuring at 0.338 and 0.295, respectively.

The RMSE values for a neural network model were computed across 311 samples (see Table 6), using a training dataset comprising 90% of the data and a testing dataset consisting of the remaining 10%. The analysis was conducted iteratively for 10 runs, producing 10 sets of RMSE values. The mean RMSE value for the training set across these runs was found to be 0.338, indicating the average deviation between predicted and actual values during training. Similarly, the mean RMSE value for the testing set was 0.295. The observed values are positioned within a satisfactory range, which suggests that the ANN model exhibits negligible error.

RMSE Value of Neural Networks.

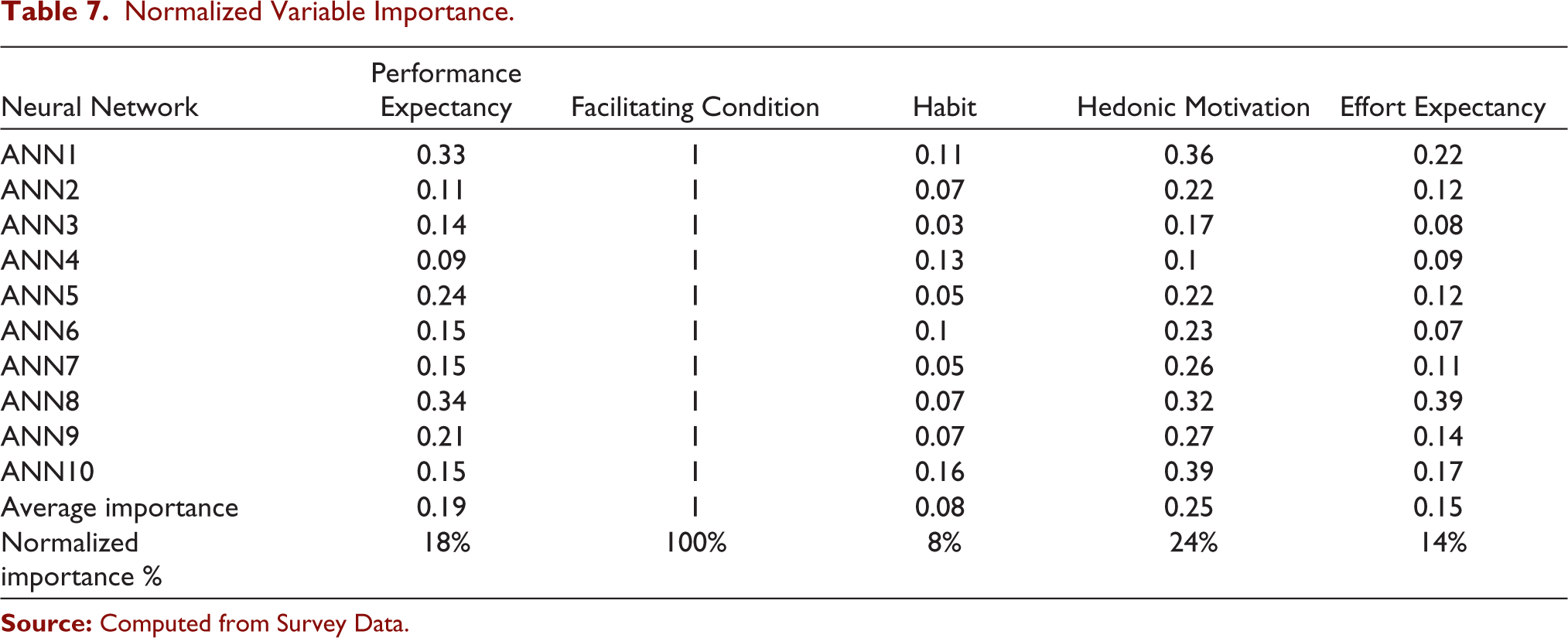

The normalized variable importance analysis was conducted using a multilayer perceptron in SPSS 20, involving ten iterations to ensure the robustness of the findings. The importance of independent variables was determined based on their impact on the model’s predictive performance. The results, averaged over the ten runs, revealed varying degrees of influence from different predictors. Notably, facilitating condition emerged as the most crucial factor with a normalized importance of 100%, underscoring its pivotal role in the model. Following closely were hedonic motivation at 24%, performance expectancy at 18%, effort expectancy at 14% and habit at 8%. Hence, according to the neural network analysis conducted, the most influential factor in predicting the intention to use a chatbot is the facilitating condition (see Table 7).

Normalized Variable Importance.

In other words, the ease and availability of resources necessary for utilizing the chatbot have a strong impact on users’ intention to engage with it. This finding suggests that if the necessary conditions are provided, such as user-friendly interfaces or convenient access to the chatbot, individuals are more likely to express an intention to use it.

Additionally, the analysis reveals that hedonic motivation and performance expectancy are also significant predictors of the intention to use a chatbot, although they have a slightly lesser impact compared to the facilitating condition. Hedonic motivation refers to the pleasure or enjoyment derived from using the chatbot, while performance expectancy refers to the users’ perception of the effectiveness and usefulness of the chatbot in fulfilling their needs.

The results obtained from this analysis align with the findings reported by smartPLS, indicating a consistent relationship between the identified factors and users’ intention to use a chatbot.

Moderation

The moderation of age, gender and personality type plays a crucial role in understanding the relationship between behavioural intentions and usage behaviour towards the utilization of a banking chatbot. Age can significantly influence individuals’ technological proficiency and familiarity with chatbot interactions. Gender, on the other hand, may introduce variations in preferences, expectations and motivations towards using a chatbot for banking purposes. Lastly, personality traits can influence users’ inclination towards technology adoption, their communication styles and their willingness to engage with automated systems.

Hence, by considering the moderation of age, gender and personality type, the present study makes an attempt to understand how these factors interact with behavioural characteristics to shape individuals’ usage behaviour towards banking chatbots.

Regarding age, the participants were divided into two categories: individuals below 40 years old and those above 40 years old. For gender, the participants were grouped into males and females. Lastly, in terms of personality type, the respondents were categorized as either introverts or extroverts based on their responses to the identified items from the BFI.

To investigate the moderating influence of age, gender and personality type, a MGA was conducted. The MGA allowed for an examination of how different groups impacted the relationships among the constructs under investigation. Additionally, a parametric test was employed to determine the significance of any differences observed between the groups. The path analysis provided insights into the effects of these variables on the constructs, while the parametric test assessed the statistical significance of the variations observed among the groups.

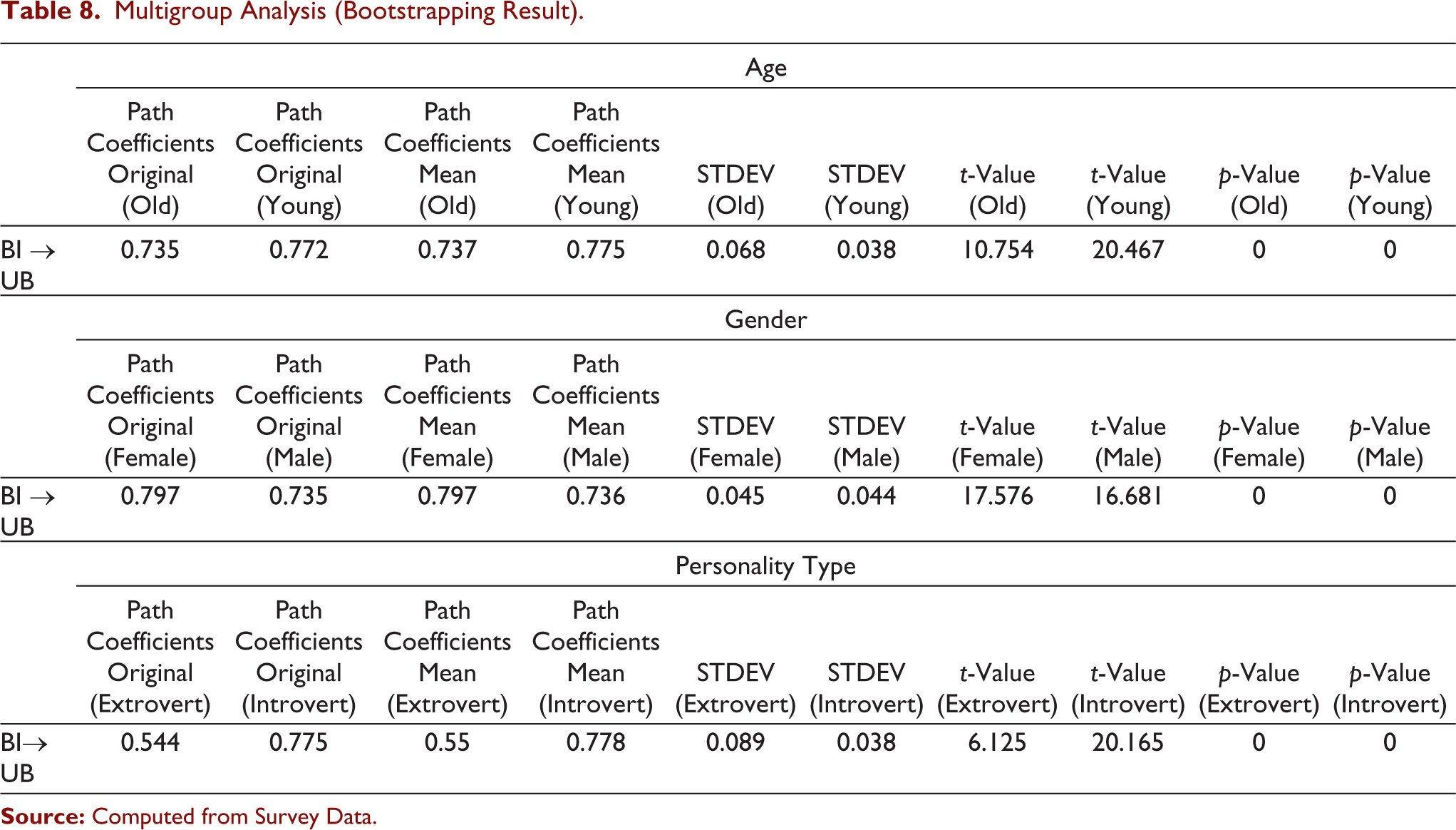

In the first step, the MGA with bootstrapping was applied to examine whether the relationships between the latent variables vary significantly across the identified groups. This analysis aids in uncovering potential moderating effects, revealing whether the relationships hold true for all groups or if they differ based on the subgroup characteristics. This information can be instrumental in understanding the nuanced dynamics and tailoring strategies to meet the diverse needs of different groups within the study population. The results of this analysis are presented in Table 8, indicating that the categories within all the groups were found to be significant.

Multigroup Analysis (Bootstrapping Result).

The MGA explored the impact of age, gender and personality type on intention and usage behaviour, yielding insightful results. Regarding age, both older and younger individuals exhibited substantial and statistically significant associations with the dependent variable, as evidenced by path coefficients (β) of 0.735 and 0.772, respectively. The high t-values (10.754 for old and 20.467 for young) underscored the strength of these relationships, and extremely low p (0.00) indicated their significance. Similarly, gender distinctions yielded noteworthy findings, with females and males both displaying robust and statistically significant relationships with the dependent variable (path coefficients (β) of 0.797 (female) and 0.735 (male), t-values of 17.576 for females and 16.681 for males, and p values of 0.00). Lastly, personality type distinctions revealed significant impacts, with extroverts and introverts showing strong relationships (path coefficients (β) of 0.544 and 0.775, t-values of 6.125 for extroverts and 20.125 for introverts and p values of 0.00). These results collectively highlight the nuanced influence of age, gender and personality type on intention and usage behaviour.

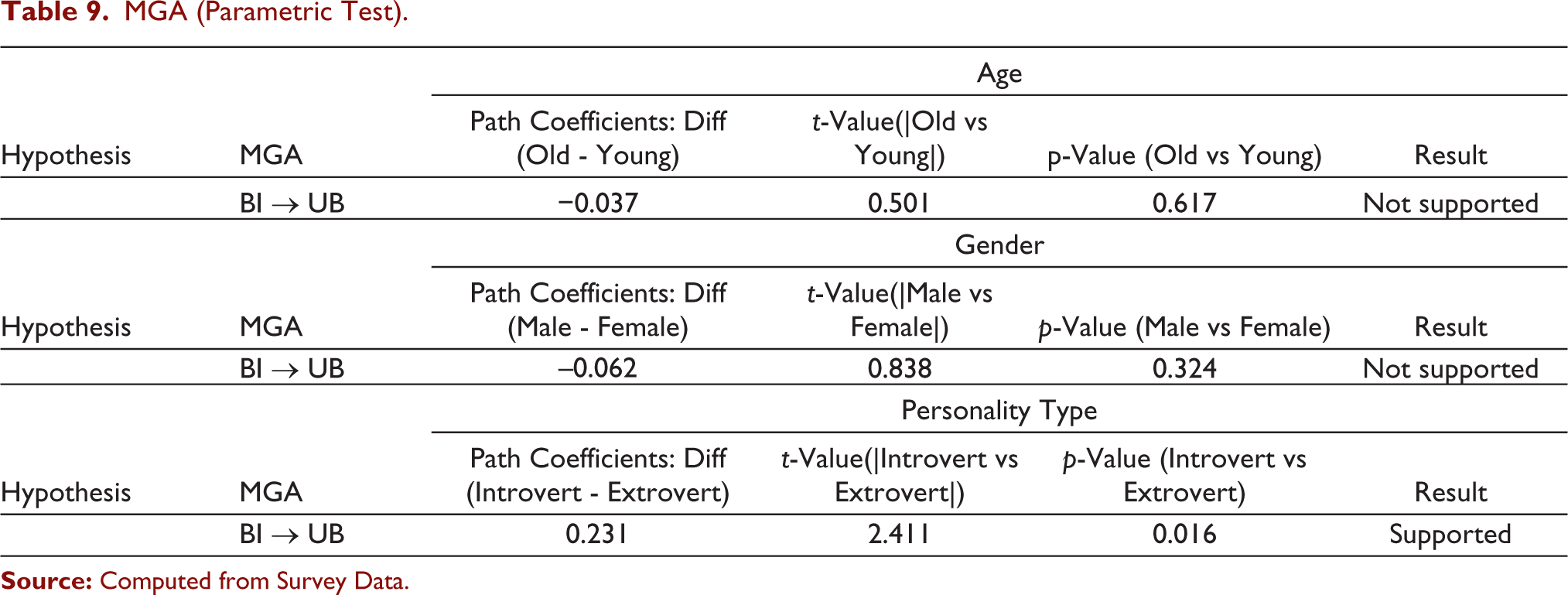

Next, a parametric test was employed to determine the significance of the differences observed between the two categories within each group. This test aimed to assess whether the variations between the categories indicated the presence of moderation. If the difference between the two categories was found to be significant, it would suggest the existence of moderation. Conversely, if the difference between the two categories was not significant, it would imply the absence of moderation.

The results of this analysis provide insights into the moderating role of the variables under consideration (see Table 9). It was found that only personality type exhibited a significant moderation effect on the relationship between the latent variables. This indicates that individuals’ personality traits, specifically whether they are classified as introverts or extroverts, have a substantial impact on the relationship between the variables of interest. On the other hand, the analysis revealed that age and gender did not significantly moderate the relationship.

MGA (Parametric Test).

The results of the MGA parametric test investigating age, gender and personality type as potential moderators between behaviour intention and use behaviour provide valuable insights. The analysis revealed that the difference in path coefficients between old and young age groups, as well as between males and females, did not exhibit statistical significance, suggesting that age and gender differences may not play a substantial role in influencing behaviour intention and usage behaviour in the studied context. However, the moderation hypothesis related to personality type yielded a different outcome, with a significant difference in path coefficients between introverts and extroverts. The t-value of 2.411 and a p-value of 0.016 indicated statistical significance, supporting the notion that personality type serves as a moderator in the relationship between behaviour intention and usage behaviour.

Discussion

The results obtained from the neural network analysis revealed that the facilitating condition was the most influential factor in predicting the intention to use a chatbot. This suggests that the ease and availability of resources necessary for utilizing the chatbot strongly impact users’ intention to engage with it. It also emphasizes the importance of providing user-friendly interfaces and convenient access to chatbot services to encourage individuals to express their intention to use them. The present finding contradicts the findings reported by Al-Emran et al. (2023).

Furthermore, the analysis indicated that hedonic motivation and performance expectancy were also significant predictors of the intention to use a chatbot, albeit with a slightly lesser impact compared to the facilitating condition. Hedonic motivation refers to the pleasure or enjoyment derived from using the chatbot, while performance expectancy pertains to users’ perception of the effectiveness and usefulness of the chatbot in meeting their needs. These findings highlight the significance of considering users’ satisfaction and perceived utility when designing and implementing chatbot services in the banking sector. Previous studies conducted by Eren (2021) in the banking sector have highlighted the significance of performance expectancy as a crucial determinant of intention towards chatbots. Additionally, the relevance of hedonic motivation has been emphasized in the study of Melián-González et al. (2021), which focused on the use of chatbots in the tourism industry. Therefore, the present study aligns with and supports the previous research findings.

The findings of the present study indicate that both effort expectancy and habit do not have a significant impact on the behavioural intention towards chatbots in the financial sector. This result is noteworthy as it deviates from some previous studies that have identified these factors as important determinants (Mohd Rahim et al., 2022).

In previous research conducted in various sectors, including the banking industry, effort expectancy has been found to play a crucial role in shaping users’ behavioural intentions towards adopting new technologies (Farah et al., 2018; Sugumar & Chandra, 2021). Effort expectancy refers to users’ perception of the ease of use and the level of effort required to interact with technology. However, in the context of chatbots in the financial sector, the present study suggests that effort expectancy may not be a significant factor in influencing users’ intention to engage with chatbot services.

Similarly, the concept of habit, which refers to repetitive and automatic behaviours formed through frequent engagement, has been recognized as a significant factor in technology adoption (Alalwan et al., 2015). Habits have been found to play a crucial role in shaping users’ intentions and usage behaviours (de Guinea & Markus, 2009). However, in the specific context of chatbots in the financial sector, the present study does not find a significant impact of habit on users’ behavioural intentions.

The deviation of these findings from previous studies suggests that the adoption and usage of chatbots in the financial sector may have unique characteristics that distinguish them from other technological innovations. It is possible that the specific nature of chatbot interactions in the financial context, where users may have different expectations and preferences compared to other sectors, could influence the relevance and influence of factors such as effort expectancy and habit. These findings highlight the importance of context-specific research when examining the factors influencing users’ intentions and behaviours in adopting new technologies. It emphasizes the need to consider industry-specific characteristics and user expectations when designing and implementing chatbot services in the financial sector.

The findings also indicate that the intention to use chatbots in the financial sector significantly influences use behaviour. Hence, users who have a positive intention to use these services are more likely to actively seek out opportunities to interact with chatbots and engage in financial transactions. This aligns with the notion that intention serves as a motivating factor that drives individuals to take action and utilize the available chatbot services. The significant influence of intention on use behaviour in the financial sector has important implications for financial institutions and service providers (Chiou & Shen, 2012). It underscores the importance of promoting positive attitudes and perceptions of chatbots among users, as these factors can contribute to the formation of a strong intention to use the technology. Financial institutions can focus on highlighting the benefits and advantages of chatbot services, such as convenience, efficiency and personalized experiences, to enhance users’ intention to engage with them.

The results of the MGA revealed that all the identified groups (age, gender and personality type) were found to be significant, indicating the presence of potential moderating effects. However, the subsequent parametric test demonstrated that only personality type exhibited a significant moderation effect on the relationship between the latent variables. This suggests that individuals’ personality traits, specifically whether they are classified as introverts or extroverts, play a substantial role in shaping the relationship between the factors of interest.

The absence of significant moderation effects for age and gender implies that these demographic variables do not significantly influence the relationships between the identified factors and users’ intention to use a chatbot. The finding contradicts the finding of Kasilingam (2020) and suggests that, regardless of age or gender, individuals in the banking sector show similar patterns in their intention to use chatbot services. Therefore, it is essential for banking institutions to focus on creating user-friendly interfaces, ensuring convenience and emphasizing hedonic motivation and performance expectancy, irrespective of demographic differences.

Conclusion

In the contemporary landscape of the banking sector, the integration of advanced technologies such as chatbots has become increasingly prevalent, revolutionizing the way financial institutions interact with their customers. This research aimed to delve into the intricate dynamics of chatbot adoption and usage, specifically focusing on the moderating influences of age, gender and personality types. Through a comprehensive analysis of these factors, this study sheds valuable light on the different aspects of customer behaviour and preferences within the digital banking realm. The research findings revealed a notable moderating impact of personality types on the connection between the latent variables. This implies that the distinction between introverted and extroverted personality traits significantly influences the correlation between the factors under investigation. In essence, individuals’ classification as introverts or extroverts substantially shapes the interrelationship among the variables of interest.

In conclusion, this research significantly contributes to the growing body of knowledge surrounding customer interactions with chatbots in the banking sector. By acknowledging and understanding the moderating influences of age, gender and personality types, financial institutions can refine their chatbot strategies and enhance user experiences. Tailoring chatbot interfaces to align with the diverse needs and preferences of different demographic and personality groups is crucial in ensuring widespread acceptance and utilization of this technology.

Moving forward, it is imperative for banks and financial institutions to invest in continuous research and development, focusing on user-centric design principles. Embracing the multifaceted nature of customer diversity will not only enhance the effectiveness of chatbots but also foster a more inclusive and customer-friendly banking environment. As the digital landscape continues to evolve, staying attuned to these dynamics will be instrumental in shaping the future of chatbot technology and its seamless integration into the banking sector.

Practical Implication

The findings of the present study have several practical implications for financial institutions and service providers looking to implement chatbot services in the banking sector: First, the study highlights the importance of providing user-friendly interfaces and convenient access to chatbot services. Financial institutions should invest in developing intuitive and easy-to-use interfaces that minimize the effort required for users to interact with chatbots. Additionally, ensuring the seamless availability and accessibility of chatbots across different platforms and devices can enhance users’ intention to engage with them. Second, financial institutions should promote the pleasure and enjoyment derived from using chatbot services (hedonic motivation) and highlight the effectiveness and usefulness of chatbots in meeting users’ needs (performance expectancy). By emphasizing these factors, institutions can enhance users’ intention to use chatbots and encourage their adoption in the financial sector.

Third, the study indicates that personality traits, specifically whether individuals are introverts or extroverts, can moderate the relationship between the identified factors and users’ intention to use chatbots. Financial institutions should take into account these personality differences when designing and tailoring chatbot services.

Limitations and Scope for Future Study

The study had limitations to be addressed in future research. Future studies could further explore the underlying reasons for the non-significant impact of effort expectancy and habit in the financial sector. This could involve investigating the specific features and functionalities of chatbots in the financial context, as well as examining user perceptions and preferences regarding these technologies. Understanding these factors in more depth can provide insights into how to enhance user acceptance and adoption of chatbots in the financial sector. Additionally, conducting longitudinal studies can provide a deeper understanding of the long-term effects of chatbot adoption in the financial sector. Tracking users’ intentions and behaviours over an extended period can reveal insights into the sustainability of adoption and identify factors that may influence continued usage or disengagement. As chatbot technology continues to evolve, future research can explore the impact of advanced features such as natural language processing, sentiment analysis or personalized recommendations on user intentions and behaviours. Investigating the effects of these technological advancements on chatbot adoption in the financial sector can provide valuable insights for financial institutions. Lastly, further studies can be conducted on ascertaining the security and privacy concerns of users in determining behavioural intentions of chatbot users in the banking sector. Financial institutions should address users’ security and privacy concerns associated with chatbot services. Implementing robust security measures and transparent privacy policies can help alleviate users’ apprehensions and build trust in the technology. Clear communication regarding data protection and secure transactions can further enhance users’ confidence in utilizing chatbot services and, lastly, financial institutions should offer reliable and easily accessible technical support channels for users who may encounter issues or require assistance while using chatbot services.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.