Abstract

In this article, we build a theoretical model of retail and wholesale trade to analyse the effects of the entry of multinationals in wholesale and retail markets on the size of the domestic retail sector and prices. We show that the domestic retailing sector will expand, the retail price will fall and the wholesale price will go up, if and only if the retailing cost of the MNCs is greater than the retailing cost of the domestic retailers.

Introduction

With vast changes in agricultural and food retailing chains over the past quarter century in the low- and middle-income group countries, foreign direct investment (FDI) in retail has become a controversial issue. In most of these countries, either the wholesale markets or the retail markets or both were under strict state supervision, which got relaxed with the economic liberalizations that took place from the 1980s (Swinnen & Maertens, 2007). Along with this came the surge of globalization and the influx of FDI in various sectors. The introduction of FDI to the retail sector and wholesale market became a matter of critical consideration because in many countries, the retail and wholesale trade taken together provided employment to a sizable proportion of the population. With a large percentage of the population being dependent on the retail and wholesale trade for their livelihood, whether or not to allow FDI has always remained a question of crucial importance.

The purpose of this article is twofold. First, we develop a theoretical model of retail and wholesale trade. Second, we analyse, in terms of that model, the effects of the entry of multinationals in wholesale and retail markets on domestic employment and consumer prices. But before we get into the arguments favouring or disapproving FDI in retail, let us first talk about the agricultural sectors of developing countries in general. The agricultural sectors in the developing countries are generally poor and backward. A salient feature is the presence of middlemen in multiple stages, which causes a wide gap between the price the farmer gets and the price that a final consumer pays. The farmers are small with no market power and are often isolated. They seldom have access to the formal credit markets. On the other hand, the middlemen and the rural moneylenders have market power. The consumers are also fragile and they end up paying a higher price due to market imperfection and presence of middlemen in many stages. The farmers and traders are often too small to have an access to the international market and hence are unable to enjoy the gains from trade. So the reforms in the agricultural sector should help to remove these adversities and not to make the situations of the small farmers and consumers worse.

The proponents of FDI in retail put forward a number of arguments in support of the introduction of FDI to the retail sector. Through such an introduction, it is argued, the agricultural sector will get the much needed exposure to the international market. There will be vertical integration of the supply chain. The exploitative middlemen will be largely bypassed. Direct purchasing from the farmers will ensure that they get better price and there will be more incentive for agricultural investment. Large retail groups will invest in better storage which will reduce wastage as they already have the infrastructure and the know-how, reducing the traditional warehousing role of the wholesalers. Post liberalization, there has been a change in the taste and preference of the urban consumers of the developing countries, and there has been a convergence of taste and preference all over the world. The introduction of FDI will cater to their needs better by ensuring better quality, wider variety of international standard and all these at a lower price.

However, there are some possible drawbacks too. A large number of small traders may lose their livelihood to the uneven competition with the MNCs. For example, in India, given that retail and wholesale trade is the single largest component of the services sector in terms of contribution to GDP at 14 per cent, and that the unorganized retail sector of small and medium retailers employs over 40 million people, by sheer number this will not be insignificant. MNCs can increase price after eliminating competition. Foreign retailers have pointed out that setting up of a manufacturing base in India is difficult since the infrastructure is poor, labour laws are unfriendly and so on. This would mean that the MNCs are not interested in buying from the domestic farmers as much as they are interested in selling to the domestic urban consumers. If the MNCs buy from the domestic farmers, the village market price will go up, increasing rural poverty. Agricultural price may become more uncertain due to higher integration with the world market, reducing the incentive for agricultural investment.

The literature on the experience of FDI in the retail sector sends a highly ambiguous message, although there is a general observation that asset-poor farmers have been losers (Killick, 2001; Reardon & Berdegu, 2008). Studies on the dairy production of the East European countries show contradictory results on whether the small farmers are benefited. While Swinnen, Dries, Noev and Germenji (2006) show that small household dairy farms gain from FDI, Gorton & Guba (2002) show that FDI instituted more formal contracting agreements, promoting the growth of a select number of medium-sized dairy farms and excluding micro-producers. The growth of supermarkets and fast-food sectors since the 1990s in Argentina has resulted in the changing pattern of production in favour of medium and large producers, with evidence of exclusion of small farmers (see Ghezan, Mateos & Viteri, 2002).

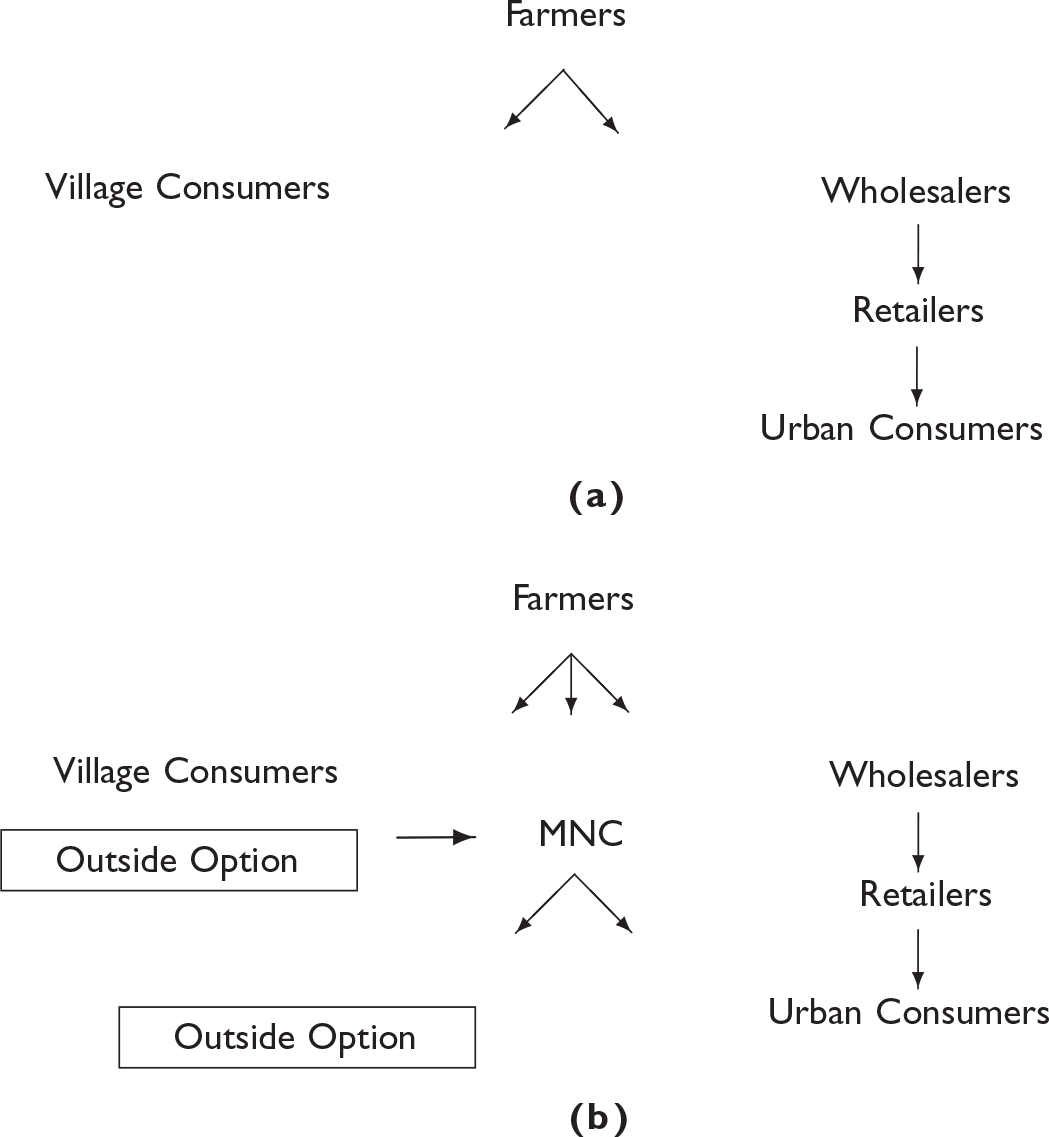

As aforementioned, in this article we propose a theoretical model to find out some of the possible effects of allowing FDI in the retail and wholesale markets. We consider only the agricultural sector, as agro products constitute the maximum of the retail sector. We start with a basic model with an oligopolistic wholesale market, where the wholesalers buy from the farmers in the village market and sell to the retailers in the wholesale market. The retailers in turn sell the output to the urban consumers. The farmers, retailers, urban and rural consumers are price-takers, while the oligopolistic wholesalers are price-makers. We then introduce MNCs who are allowed to buy from the rural market and sell in the urban market. The MNCs are also assumed to be oligopolistic.

In what follows, the second section of the article develops the basic model. In the third section, we look at the the effects of allowing MNCs to buy and sell in the rural and urban markets respectively. The focus is on consumer prices and domestic retailing activity. The fourth section concludes the article.

The Basic Model

We construct a simple model with an oligopolistic wholesaling market. The economy consists of farmers, wholesalers, retailers, rural and urban consumers. The farmers are price-takers, who produce an agricultural good

Before the economy is thrown open to MNCs, the structures of the rural and urban markets are as follows. In the village market, the farmers are price-takers and supply a fixed amount

where

In the wholesale market, the competitive retailers buy from the oligopolistic wholesalers at price

Rewriting the urban demand function,

There are

where

where

Rewriting the

The first order condition for profit maximization will be given by

Summing both sides for all

since

Solving this, we get the equilibrium output and price. The retail market output will be given by

Each wholesaler will sell

The urban retail market price will be

The village market price will be given by

In this section, we find how the autarky equilibrium is affected when MNCs enter in both the village market and the urban market. Let us assume

Note that an MNC is ‘not required’ to sell in the urban domestic market exactly the amount it buys from the domestic rural market. It can sell more than it buys, in which case the country is a net importer. Similarly, it can sell less in the domestic market than it buys from it. In the latter case, the country is a net exporter. The possible imbalance between buying and selling does not apply for domestic large traders, and this is the basic difference between local oligopolist traders and MNCs. Of course, theoretically a domestic trader may have access to the international market to buy and sell agricultural goods. But in that case, it will be identified as a multinational and included in the

Each MNC has the option of selling in the international market at a fixed price

In the village market, it will buy the good until its marginal cost is equated to

where

Solving this, we find the total output bought by the MNCs given

and the output bought by a single MNC is

Similarly, the total revenue earned by a representative MNC when he sells to the domestic retail market is given by

The MNC will equate the marginal revenue with

Solving this, we find the total output sold by the MNCs given

and the output sold by a single MNC is

The profit of a representative wholesaler is given by

Substituting for

The representative wholesaler maximizes (7) with respect to

And for a representative wholesaler, the solution will be

The retail market price will be given by

The village market price will be given by

If we compare (2.3) and (3.2), we see that the difference is

Let us denote the values of the variables before the MNC comes in with ‘tilde’ and the variables after the MNC comes in with ‘hat’. Comparing (5) and (10),

We see that after MNCs come in, the retail market price is the sum of a fraction of the cost difference and the average of the international retail market price and the domestic retail market price before MNC came in. If the MNC sells in the domestic retail market, presumably

Comparing (2.6) and (3.5),

We see that after MNCs come in, the village market price is the sum of a fraction of the cost difference and the average of the international wholesale market price and the village market price before the MNCs showed up. If the MNCs buy from the domestic market, then presumably,

If the retailing cost of the MNCs is less than the retailing cost of the domestic retailers then the domestic retailers will lose out to the MNC on account of higher cost of retailing. If the retailing cost of the MNC is higher than that of the domestic retailers, then the MNC would be more interested in buying from the domestic village market than in selling in the domestic retail market. That would increase the village market price, hurting the village consumers and benefiting the farmers. On the other hand, even with

It may be useful to summarize the intuition behind the results obtained earlier. All the results depend on the sign of

From (10), we see that the urban retail market price will go up when

If the domestic retailing cost is higher than the MNCs’ retailing cost, then more MNCs would find it profitable to enter the domestic retail market, which would reduce the domestic retailing activities further. If the domestic retailing cost is higher, then the urban consumers will face an even higher price as more MNCs enter, and will lose. If the domestic retailing cost is lower, then as more MNCs come in, the village consumers will have to pay a higher price, as now there will be more demand in the village market. Allowing competition among the MNCs need not be good for the domestic retailing sector and the urban and rural consumers.

In this article, we have built a partial equilibrium model in an attempt to see the consequences of allowing FDI in the retail sector. We have a simple oligopolistic wholesale market and a competitive village market and retail market. If now MNCs are allowed to buy goods from the domestic farmers and sell it in the retail market, we find the conditions when the domestic retail sector shrinks. We also find the condition when the farmers and urban consumers can gain, and the rural consumers lose. Finally, we find the conditions where allowing more MNCs might hurt the domestic consumers and the farmers.