Abstract

Savings play a very crucial role in the economic development of a country by financing investment needs. Household savings are the major and dominant component of national savings in Pakistan. The present study aims to analyse the impact of various socio-economic factors in determining the household savings in Pakistan by using the data of Household Integrated Income and Consumption Survey (HIICS) 2015–2016. It has been found that household’s savings tend to increase with income, living in nucleus family, house ownership, receiving remittances from abroad and being involved in agriculture; and saving tends to decrease with an increase in dependency ratio; and wealth has an insignificant role in determining savings in both urban and rural households. However, education and female labour force participation had a positive relationship with saving among urban households but the relationship is insignificant in rural households. Similarly, age of household head hurts saving in urban households and the relationship is insignificant in rural households.

Introduction

Savings plays a very crucial role in economic development by financing the investment needs resulting in higher growth. Over the years, Pakistan is facing low saving rates as compared to other developing countries of the region and saving is hovering around 10% of GDP (Akram & Akram, 2016). Due to limited domestic savings, Pakistan has to rely on foreign saving in the shape of foreign economic assistance (in the shape of grants and loans) to finance the investment needs. The foreign capital is made available by various international institutions with strict conditions, and over-dependency on foreign savings results in making the economy vulnerable to external shocks and long-term reliance on foreign loans tends to destabilize the economy (Akram, 2016).

To explain the saving behaviour, there exist two very popular theories named ‘Permanent income hypothesis’ (Friedman, 1957) and ‘life-cycle hypothesis’ (Ando & Modigiliani, 1963; Modigliani, 1986). While determining the savings, the permanent income hypothesis differentiates transitory income from permanent income. The permanent income is defined as actual income along with expected income over a certain period, while transitory income is the difference between permanent and actual income. According to the permanent income hypothesis, the transitory changes in income do not have any significant impact on the saving and savings are determined by the permanent income (long-term average income). According to the life-cycle hypothesis, lifetime consumption of an individual is being spread over their lifetime by accumulating savings in working years and these savings are used to maintain the consumption level after the retirement period. The life-cycle income hypothesis gives demographic factors critical role in determining the savings.

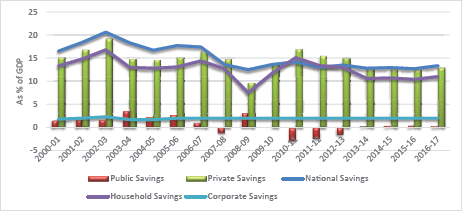

The composition of savings in Pakistan during 2000–2017 has been illustrated in Figure 1. The national saving in Pakistan consists of public and private savings. Due to fiscal deficit since 2006–2007, public savings are in negative or near to zero. Consequently, private savings are 100–130% of national savings.

The private savings comprise of household savings and corporate savings. Since 2000, corporate savings remained stagnant and make only 10%–15% of private savings. It reveals that household savings are the major and dominant component of not only private savings but also of national savings in Pakistan.

Due to the dominance of household savings, the analysis of the household’s saving behaviour becomes extremely important. By its very nature, to analyse the household’s saving behaviour, macroeconomic analysis failed to explore the factors that motivate a household to save. Therefore, it becomes important for the policymakers in Pakistan to analyse the role of various micro-level factors that play a key role in affecting household savings and because of those launch policies that encourage saving. Therefore, the present study aims to analyse the effects of various socio-economic factors in determining the household savings in Pakistan by using the Household Integrated Income and Consumption Survey (HIICS) 2015–2016.

The layout of the paper is as follow: A brief overview of the available literature is summarized in Section 2. Section 3 discusses the methodology and description of the data and variables used in the study. Section 4 presents the empirical results of the study. Conclusions and implications are given in the final section followed by references.

Literature Review

Keeping in view the importance of savings in economic development, the extensive literature on savings and its determinants is available. However, the literature on the determinants of households’ savings is very limited.

As mentioned in the introduction according to the life-cycle hypothesis, savings are highest among working households in comparison to young and old age households. Similarly, Schultz (2007) was of the view that population’s age composition determines the national savings rate and a household’s lifetime utility maximization and their decisions regarding the human capital investment, and fertility plays a major role in determining the individual households’ savings rates. Choukhmane et al. (2017) found that one-child policy in China resulted in 30%–60% of the increase in aggregate savings.

Loayza et al. (2000) suggested that dependency ratio is having a negative while income is having a positive impact on savings. While querying the robustness of the effects of demographic factors on savings, Attanasio et al. (2000) and Hondroyiannis (2006) concluded that unpredictable expenses can change the savings pattern of the old age people. Wakabayashi and Mackellar (1999) in China found that the saving rate has a negative relationship with youth and elderly dependency ratios. Mody et al. (2012) argued that instead of decreasing young dependency ratio may increase the saving rate because young are more likely to build a buffer stock to finance the education of their children.

Lee (1998) found that in the USA, wage rate and female labour supply exhibits a positive impact on savings. Apps and Rees (2001) also come to a similar conclusion that propensity to save tends to increase with an increase in female labour supply.

Evidence from Developing Countries

Household head’s education has been recognized as a proxy for expected future income. The educated households have a lower time preference and they exhibit more patience (in terms of the decision to study and entry in the labour force). It suggests that educated households are more likely to save while they are working to smooth consumption while they are studying (Gandelman, 2017). Sandoval-Hernández (2013) found that in Mexico, education has a negative impact on savings. According to Brata (1999), education had a positive impact on savings and males tend to save more than females. Banerjee et al. (2014) come to the conclusion that households having more children save less.

Burney and Khan (1992) calculated that the propensity to save is higher among rural households in comparison to urban households. It was also found that dependency ratio hurts savings but no significant relationship was found between savings and occupation of households.

Agrawal et al. (2009) concluded that in South Asia foreign savings, dependency rate, income and access to banking institutions play a major role while interest rate has a very limited and inconclusive role in affecting the savings. Samantaraya and Patra (2019) found that in India, education, household income and nuclear family have significantly increased the household savings.

Jongwanich (2010) also found that income has a positive impact on savings in Thailand. Furthermore, the availability of credit and terms of trade have a negative while interest rate and inflation have a positive relationship with savings.

Khan et al. (2013) concluded that expected age, per capita income, increase in years of education and deepening of the financial system have a positive impact on savings; however, the dependency ratio exhibit a negative relationship with saving rate.

The ownership of the house helps in analysing the role of wealth on savings. When a household become the owner of his house then while getting rid of monthly rents they are more likely to save less. However, Peltonen et al. (2009) concluded that buying a house on mortgage results in higher savings by the households.

Rehman et al. (2010, 2011) find that in Multan (a city in Pakistan), female labour participation, household income, dependency rate and size of land ownership have a positive impact on savings. However, family size, education of household head and value of house hurt savings.

Ahmad and Asghar (2004) found that rural as well as urban household’s income had a positive impact on savings. Wealth and dependency ratio had a negative impact on saving behaviour in Pakistan. The education negatively affects savings in overall Pakistan and urban areas, however for rural areas education has a positive influence.

Athukorala and Tsai (2003) found that in Taiwan, household disposable income, bank deposits and access to the credit have a positive impact on savings. Khan and Nasir (1999) found that households employed in agriculture are more likely to save, whereas households employed in the construction sector are less likely to save in comparison to other professions in Pakistan. The study also found that in comparison to urban areas, savings are higher in rural areas. Surpassingly, study concluded that in comparison to literate households, illiterate are more likely to save.

Data and Methodology

The present study analyses the role of different household-level factors in determining how much to save. In economic terms, the difference between household income and expenditure is referred to as household saving. It can be written as:

Wherein S, Y and E represent household’s saving, income and expenditure, respectively, as mentioned in the introduction, Absolute Income Hypothesis and Life Cycle Hypothesis are the two well-known theories and extensively used to explain the consumption or saving behaviours.

We will start our analysis with the Absolute Income Hypotheses. It relates to saving simply with income and other socioeconomic variables. Mathematically, it can be written as:

Where Z is the vector of the household’s socio-economic variables; however, this equation ignores the nonlinear behaviour of savings. Various empirical studies had found that at the low level of income household’s savings are either zero or in negative and it tends to increase at a faster rate after reaching subsistence level (Khan et al., 2016). To capture the non-linear effect of income, Equation 2 can be revised in the following way:

However, there is a likelihood that we may face the issue of heteroscedasticity for Equation 3. To remove heteroscedasticity, we can write saving as a percentage of income. The new specification will take the following form:

The above-mentioned equation is recognized as Keynes (1936) specification of savings. Klein (1951) has suggested an alternative way (lognormal functional form) to avoid non-linearity. The Klein equation for saving can be written as:

Landau (1971) has further extended the Klein (1951) equation. Hence, Equation 5 will take the following form:

The present study will estimate the Equations 4–6 and will be referred to as Keynes (1936), Klein (1951) and Landau (1971) specifications, respectively. The estimation will be carried out separately for urban and rural households by using Zero Inflated Poison Regression (due to negative savours) and logit models. The dependent variable in Zero-inflated Poisson regression is the ratio of saving to income (propensity to save). Wherein for logit model, a binary variable for saving has been created that takes the value of 1 if household saves any amount and zero for zero or negative savours.

The study will use the data of HIICS 2015–2016 conducted by Pakistan Bureau of Statistics, Islamabad. In HIICS 2015–2016, a total of 24,238 households were interviewed. The rural households were 8,083 (33%) and the urban households were 16,155 (67%). A brief overview of different variables that are used in the present study is as under:

Dependency Ratio = (Household Size – Number of Earners)/Household Size

Estimation Results

A Descriptive Overview of the Household’s Savings

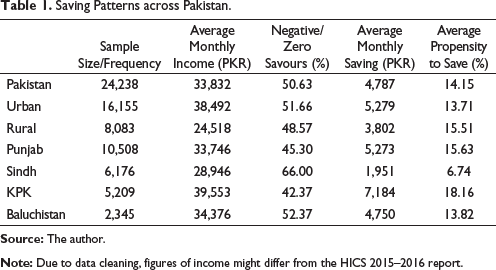

Saving Patterns across Pakistan.

It can be inferred that on average the monthly income of Pakistan households stands at PKR 33,832. The monthly income of urban households (PKR 38,492) is higher in comparison to rural households (PKR 24,518). It is 13% higher from the national average and 57% higher from rural households. Surprisingly, the highest average monthly income was of the households belonging to KPK (PKR 39,553) followed by Baluchistan (PKR 34,374) which are higher than the national average of PKR 33,832. The average monthly income in Punjab is close to the national average while the Sindh recorded the lowest average monthly income (PKR 28,946).

Similar to income patterns at national level, 50.6% of the households in Pakistan are zero or negative savours, this ratio is 51.7% for urban and 48.6 % for rural households. The highest ratio of zero or negative savours is in Sindh (66.0%) followed by Baluchistan (52.4%), Punjab (45.3%) and KPK (42.4%). It reflects that almost half of the households in Pakistan can save some amount.

To further analyse the saving behaviour of the households, Average Propensity to Save (income being saved as a percentage of total income) has been calculated. It has been found that on average in Pakistan about 14% of income is being saved. This ratio is higher for rural households (15.5%) in comparison to urban households (13.7%). Furthermore, in complete contrast to the situation of income, the savings rate of urban households is 4% lower than the national average and it is 13% lower than the rural household’s saving rate. It suggests that to raise savings in the country, the income of rural households must be increased.

Among provinces, the highest saving rate is found in KPK (18.2%) followed by Punjab (15.6%) and Baluchistan (13.8%). Indicating that is contrary to the situation of income, the saving rate is below the national average in Baluchistan. In Sindh, saving rate (only 6.7%) is extremely low in comparison to other provinces and national average and it is 52% below the national saving rate.

Estimation Results

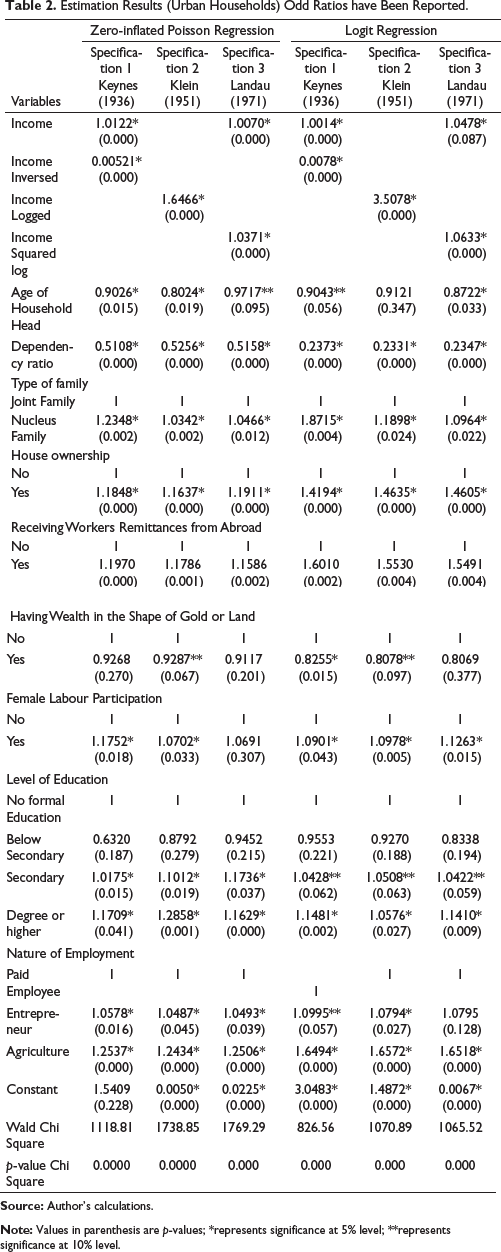

Estimation Results (Urban Households) Odd Ratios have Been Reported.

The results indicate that in urban areas, the income has an odd ratio of greater than one suggesting that income has a significant relationship with savings in all three specifications. The coefficients of inverse household income in case of specification 1 have odd ratio below 1; similarly, log income in specification 2 and log squared income for specification 3 are having the odd ratio of greater than 1 and statistically significant signs. It supports the conventional wisdom that savings increases with the increase in income.

Age of the household head is recognized as an important factor in determining the savings. The estimation results indicate that odd ratio are significantly less than 1 in all the three specifications in case of Zero-inflated poison regression and in two specifications of logit method. It confirms the negative and significant impact of age of household head on the household’s savings. It reveals that as age increases, the household’s likelihood of savings tends to decline. These results also support the life-cycle income hypothesis that at early age households saves to meet the expenditure at later stages of their life because at the retirement age in comparison to income their expenditures are higher.

It has been found that the dependency ratio is having odd ratio below 1 in all the specification in both estimation methods, revealing that the dependency ratio has a negative and significant impact on savings. Dependency ratio represents those members of households that made consumption expenditure without contributing to the income. Orbeta (2006) and Michael (2013) also came to a similar conclusion that household savings are negatively affected by dependency ratio and household size.

The study also finds that living in a nucleus family is having significantly higher odds in comparison to living in a joint family. It reveals that households having a nucleus family are significantly more likely to save in comparison to households belonging to the joint family system in all specifications. In the joint family system, as income and expenditures are shared so there is more likelihood that numbers of dependents are higher in comparison to the nucleus family that result in lowering the savings. Sex of the household head is found to have an insignificant relationship with the household’s savings in urban areas of Pakistan.

It has been found that household with house ownership has significantly higher odd ratios in comparison to household having no house ownership. It indicates that households living in their own houses are more likely to save in comparison to the households that do not own the houses. The past studies also showed divergent behaviours of saving among households who own a house and those who do not own a house. The households who own the house can save the money that would have to be spent on rent; furthermore, they can generate extra income if they rent some portion of their house (Michael, 2013).

It has been found that households that receive remittances from abroad are significantly more likely to save. For many households living in urban areas, remittances are the type of additional income that household receive. Therefore, there is more likelihood that households receiving remittance abroad will save that additional income.

The wealth of the household is having an insignificant relationship with savings most of the specifications. It suggests that an increase in wealth (measured by the value of gold, property, and livestock) do not have a significant impact on savings among urban households of Pakistan. As mentioned earlier, wealth is a stock variable that represents accumulated assets during the lifetime along with inheritance. Wealth is normally used for the consumption smoothing and spending from wealth spread over the entire life. Because of that, impact of wealth on saving is very marginal (De Serres & Pelgrin, 2002; Salotti, 2010).

The study found that households wherein participate in the labour force are having a comparatively higher odd ratio of savings, the results are significant in the first two specifications for both of the estimation methods. So, we can infer that women labour force participation is having a positive and significant impact on the household’s savings. It depicts that households, where women are having financial empowerment, tend to save more. Female labour participation results in increasing the household income considerably and women’s say in the household’s decision-making leading towards increasing the savings of the households.

It has been found that odd ratios of the household heads having education below the secondary level are insignificant. However, the odd ratios of secondary and higher education are significant and greater than 1 suggesting that it has a positive impact on household’s savings in urban areas of Pakistan. It is also important to mention here that odd ratios of education increased gradually meaning that higher education results in more savings and well-educated person spend their income more optimally and make savings to cater for their future needs. It can be concluded that education plays a positive and significant role in household savings.

The study also finds that the nature of employment is having a significant impact on the household’s savings. Entrepreneurs and households working in agriculture are having significantly higher odd ratios in comparison to the households having paid employment. It suggests that households involved in different economic activities have dissimilar saving behaviour. Considering the paid employee as a base category and based on the value of coefficient, it can be concluded that in urban areas of Pakistan, entrepreneurs and households involved in agriculture are comparatively more likely to save.

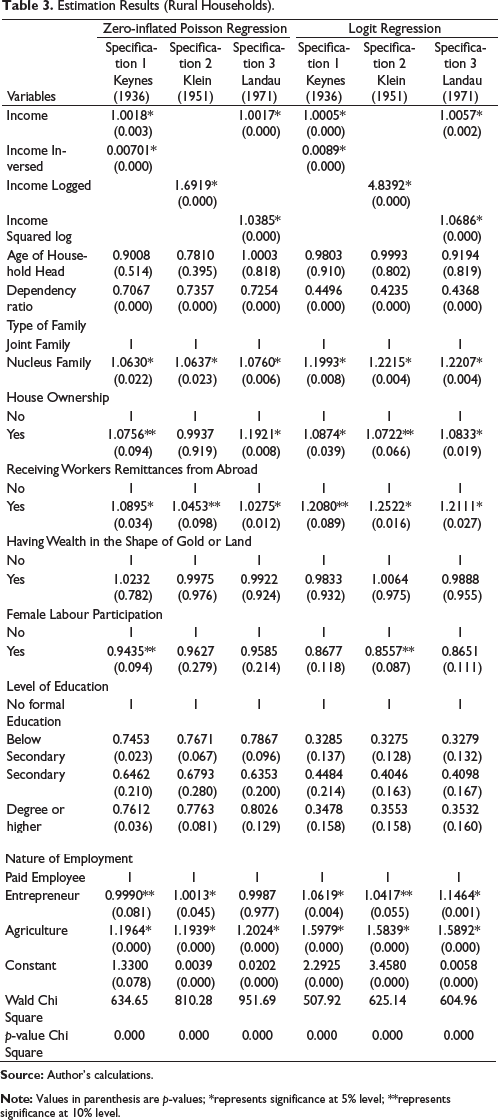

Estimation Results (Rural Households).

Table 3 reveals that in most of the cases, pattern of relationship between different socioeconomic factors and savings are similar to the urban households. It has been found that like urban households, income, living in nucleus family, having house ownership, receiving remittances from abroad significantly increases the likelihood of saving among rural households. Whereas dependency ratio has a negative impact on a household’s savings.

Similar to urban, household’s nature of employment is having a significant impact on the savings and paid employment and entrepreneurs are significantly less likely to save whereas occupation of agriculture is having a positive and significant relationship with household’s savings in rural areas of Pakistan.

However, the study is unable to find any significant impact of age of household head, wealth, female labour participation and education on the household’s savings.

Conclusions and Discussion

The composition of savings in Pakistan reveals that more than 85% of the National savings consists of household’s savings. The present study tries to analyse the role of various individual and household level factors in determining the household’s savings in Pakistan by using the HIICS 2015–2016. The study carried out separate estimations for urban and rural households.

In most of the cases, direction and nature of the relationship between socioeconomic indicators and household’s savings are the same for the urban and rural households. It has been found that income and income square has a positive and significant relationship with the household’s savings in Pakistan; indicating that the household’s savings tend to increase with income. Various earlier studies (including Agrawal et al., 2009, Ahmad & Asghar, 2004, Rehman et al., 2011) also come to a similar conclusion.

However, unlike income study found an insignificant impact of wealth, both in rural and urban households. Reason for this behaviour is that wealth represents accumulated assets during the lifetime along with inheritance and wealth is normally used for the consumption smoothing. When households can accumulate a certain level of wealth then need for more wealth for the consumption smoothing decreased. Therefore, the impact of wealth on saving is marginal or negative (Ahmad & Asghar, 2004; De Serres & Pelgrin, 2002; Salotti, 2010).

The study also concludes that with an increase in age of the household head, they tend to save less (although results are statistically insignificant in rural households). These results support the life-cycle income hypothesis that at early age household saves to meet the expenditures at later stages of their life. Similarly, in line with the expectation, it has been found that household size and dependency ratio exhibit negative impact on household’s savings. These results are also supported by Mody et al. (2012), Agrawal et al. (2009) and Michael (2013).

It has been found that living in a nucleus family is having a positive and significant impact on urban and rural households of Pakistan. In the joint family system, the average household size is 9 whereas the average family size of nucleus families is 6. It suggests that households of joint families have to bear more dependents. Linking this with the earlier finding that dependency ratios and age of household head is a negative impact on savings the people living in the joint family tends to save less in comparison to the nucleus families.

The study also concluded that households that own houses tend to save more. Households who own the house can save the money that would have to be spent on rent; furthermore, they can generate extra income if they rent some portion of their house. Peltonen et al. (2009) and Michael (2013) also came to the similar conclusion that the ownership of house results in increasing the savings.

Study reveals that households receiving remittances from abroad significantly save more. It suggests that for households, remittances are the type of additional income that they receive and they are more likely to save.

The study also confirms that female labour force participation plays significantly positive role in determining the household's savings among urban households. Female labour participation results in increasing the income considerably and women’s say in the household’s decision-making leading towards increasing the saving of household. These results are supported by various earlier studies including Lee (1998) and Apps and Rees (2001). The insignificant impact of female labour participation in rural households seems to be the fact that in Pakistan most of the female contribute in agriculture as a family helper and their contribution do not yield any monetary benefit.

The study concluded that education plays a positive and significant role in household savings for urban households while the role of education is insignificant in rural households. Most of earlier studies also reveal that education plays a positive role in increasing the savings. In urban areas, the coefficient of education at each level increased gradually, meaning that higher education results in more saving and well-educated persons spend their income more optimally and try to save for their future needs.

The nature of employment also has a significant role in determining the household’s savings, both in urban and rural areas. The household involved in agriculture is comparatively more likely to save. Khan and Nasir (1999) also came to a similar conclusion. It suggests that households involved in different economic activities have dissimilar saving behaviour.

There are few important policy implications emerged from the present analysis.

The study has concluded that with the ownership of the house, the savings tend to increase. It suggests that the provision of houses will not only be helpful in providing shelter to the people but it would also help to increase the savings of the households in the long run. Therefore, it is recommended that the government should prioritize the ‘Naya Pakistan Housing project’. It has also been concluded that women’s labour participation tends to increase savings in urban areas while the role is insignificant in rural areas. It reflects that participation in women in the formal sector is helpful in increasing the household savings whereas if women participate in the labour force without any monetary benefit then it has no impact on savings. Therefore, the government may provide formal sector job opportunities to women of rural areas. The households living in a nucleus family also tends to increase savings. Therefore, the government may promote nucleus families in Pakistan. As the people that are involved in the agriculture sector are more likely to save, therefore to increase saving incentives must be given to the agriculture sector. In Pakistan, it is hypothesized that most of the savings are used for unproductive purposes, for example, to purchase property or gold and very limited savings are translated to investment. Hence, there is a dire need that a study may be conducted about the utilization of household’s savings in Pakistan.