Abstract

Abstract

Pradhan Mantri Fasal Bima Yojana (PMFBY) is an area-based crop yield insurance scheme introduced in Odisha in Eastern India since kharif, 2016. The present study aims to identify the factors that determine the adoption of PMFBY among farmers and examine the operational efficiency of the scheme. The study is based on a field survey conducted in the drought-prone Bolangir district in Western Odisha. A total of 200 households were interviewed with questionnaires, which included 80 loanee and 80 non-loanee PMFBY users and 40 non-users. Probit regression is fitted to identify the factors that determine the adoption of PMFBY. Higher caste farmers with greater farm size, larger household incomes and indebtedness and risk-averse farmers are more likely to adopt PMFBY. Farmers having more dependence on non-farm income are less inclined to buy crop insurance. Farmers cite various reasons for dissatisfaction with the scheme such as: delay in compensation payment, large loss assessment unit and non-coverage of individual and independent risks.

Introduction

Agriculture in India is a highly risky venture primarily due to uncertainty in production. Contrary to industrial production, crop production takes place in the open field and depends on various climatic parameters such as rainfall, temperature, sunshine, humidity, etc. Any deviation from the requisite quantity of these parameters at various growth stages of plants affects crop production adversely. Extreme weather events such as drought, flood, cyclone and storm surge inflict huge crop loss and destabilise rural livelihoods. Moreover, infestation of pests and plant diseases cause crop failure. Sometimes, erratic input supply and technology failure also reduce the crop yield. Thus, the small-holder farmers operate in a very risky environment and these risks are unpredictable and thereby non-preventive in nature. Therefore, the government takes many measures to reduce risk and provide buoyancy to agriculture. Various risk mitigation actions taken by the government include promoting cultivation of drought- and flood-resistant crop varieties, intercropping, extending irrigation facility, drought proofing, flood control, watershed management and launching crop insurance schemes.

Farmers also adopt many strategies to manage agricultural risks (Singh, 2010). Risk can be managed by avoiding, preventing, sharing, transferring and spreading it. Farmers can avoid risk by opting for alternative livelihood opportunities in the non-farm sector. Some risks can be prevented by taking advance action like preventive pest control. Risks can be shared by giving land on lease to tenants. Risk can be transferred by insuring the crop yield and through forward contract. Risk may be spread through diversified farming and mixed cropping.

In spite of taking all precautionary measures, when there is crop loss ultimately, crop insurance comes to the rescue of the farmer. Crop insurance is a risk transfer mechanism and a risk adaptation measure that transfers the risk from the insured farmer to the insurer company. Farmers pay a small nominal amount as premium for insuring their output against an uncertain larger amount of loss, which will be compensated by the insurance company in the event of crop damage due to non-preventable risks. Insurance has great potential to provide income support to farmers, both by protecting them when shocks occur and by encouraging greater investment in crops, which increases their yield and farm income. Therefore, there is a great need for crop insurance to provide economic support to farmers, stabilise their farm income, induce them to invest in agriculture, reduce their indebtedness and decrease the need for relief measures in the event of crop failure (Hazell, 1992).

In India, during the last two decades, climate change has emerged as a major threat to agricultural development and rural livelihoods. Climate change has manifested itself in terms of gradual increase in temperature, variability in rainfall and, more importantly, increase in frequency, intensity and duration of extreme weather events such as flood, drought, cyclone and storm surge. As a result, production risks have increased substantially. Odisha, located on the east coast of India, is considered as the climate change hotspot of the country because of its long coastline, high dependence on agriculture, low irrigation coverage and high incidence of mass and chronic poverty.

Various crop insurance schemes have been implemented by Government of Odisha since 1979: Pilot Crop Insurance Scheme (PCIS), Comprehensive Crop Insurance Scheme (CCIS), National Agricultural Insurance Scheme (NAIS), Weather Based Crop Insurance Scheme (WBCIS), Modified National Agricultural Insurance Scheme (MNAIS) and the latest Pradhan Mantri Fasal Bima Yojana (PMFBY). In the increased risky environment of climate change, globalisation and commercialisation of agriculture, there is a need to analyse the effectiveness of the above crop insurance schemes in general and PMFBY in particular and suggest innovative insurance products to cater to the changed needs of the farmers. The principal objectives of this article are to identify the factors which determine the adoption of PMFBY and examine the operational efficiency of PMFBY with micro-level data from Bolangir district in Odisha.

Operational Mechanism of PMFBY

Following the guidelines of Government of India, Odisha has implemented PMFBY in all the 30 districts since 2016, which replaced NAIS and MNAIS. PMFBY provides comprehensive insurance coverage against crop loss on account of non-preventable natural risks such as (a) natural fire and lightning; (b) storm, hailstorm, cyclone, typhoon, tempest, hurricane, tornado, etc.; (c) flood, inundation and landslide; (d) drought and dry spells; (e) pest/diseases, etc. This scheme is compulsory for loanee farmers who have availed crop loans from institutional sources of finance, and non-loanee farmers can also insure their crops voluntarily. The objectives of the scheme are to provide financial support to the farmers in the event of crop failure, to stabilise their income, to encourage them to adopt innovative and modern agricultural practices and to ensure flow of credit to the agriculture sector.

In PMFBY, the risk coverage of crop cycle has increased, which includes not only crop loss during plant growth stage but also prevented sowing and post-harvest losses. Inundation has been incorporated as a localised calamity in addition to hailstorm and landslide for individual farm level assessment. An area approach has been adopted for settlement of claims for widespread damage. For more effective implementation, a cluster approach has been adopted under which a group of districts with variable risk profile have been allotted to an insurance company through bidding for a longer duration up to 3 years.

Notified insurance unit has been reduced to village/village panchayat for major crops. Uniform maximum premiums of only 2 per cent, 1.5 per cent and 5 per cent are to be paid by farmers for all kharif crops, rabi crops and commercial/horticultural crops respectively. There is provision of individual farm level assessment for post-harvest losses against cyclonic and unseasonal rains for crops kept in the field for drying up to a period of 14 days.

The scale of finance in each district for each crop forms the basis for calculation of sum assured. This roughly corresponds to costs incurred in cultivation of crops and gives farmers adequate financial protection without any capping as followed in earlier schemes. The sum assured has doubled in the case of PMFBY in comparison to earlier schemes.

PMFBY is an actuarial model-based scheme wherein token premium is charged from the client farmers, and government pays the balance premium quoted by insurance companies selected by states through transparent bidding. However, the full liability of payment of claims lies with the insurance companies.

The claim amount is credited electronically to the individual farmer’s bank account. Remote-sensing technology, smartphones and drones are used for quick estimation of crop losses to ensure early settlement of claims. A crop insurance portal has been launched. This is used extensively for ensuring better administration, co-ordination, transparency and dissemination of information. Firm attention and ample publicity are given to increasing awareness about the schemes among all stakeholders and to appropriate provisioning of resources for the same. The government is keen to improve the implementation of the scheme by focusing on timely settlement of claims. There are penal provisions on agencies which cause delays in release of claims to farmers.

However, the low participation rate of farmers in crop insurance schemes is a major concern of the government. In Odisha, during 2013–2014, the total coverage of crop insurance was 1.37 million hectares which includes 1.24 million hectare during kharif season and 0.13 million hectare during rabi season. The proportion of gross cropped area (9.05 million ha) under crop insurance was only 15.13 per cent. In addition to that, more than 90 per cent of insured farmers were loanee farmers, compulsorily covered under crop insurance schemes. Voluntary adoption of crop insurance as a risk management tool remains appallingly low. Causes of low penetration include the lack of insurance literacy and the complexity of insurance products on the one hand, and low willingness and ability to pay by the customers on the other. In this context, this article attempts to critically examine the factors that determine farmers’ adoption of PMFBY in drought-prone Bolangir district in Odisha. This study also assesses the performance of PMFBY with micro-level data collected through a field survey.

Study Area and Methodology

In order to identify the factors that determine the adoption of PMFBY among farmers, a field survey was conducted in drought-prone Bolangir district in Western Odisha. Bolangir is a tribe-dominated district known for its high incidence of mass and chronic poverty. Manifestations of poverty in this area are persistent crop failures, starvation, malnutrition and migration. Severe droughts and floods also often visit this region in quick succession.

In Bolangir district, agriculture is very much vulnerable to agricultural risks mainly because of low rainfall and erratic rainfall patterns. The normal annual rainfall in the district is 1289.8 mm, which is lower that the average state rainfall of 1451.2 mm. Only 20.6 per cent of gross cropped area was irrigated during 2013–2014 (Government of Odisha [GoO], 2014–2015), which was lower than the state average (38.9%).

To find out the determinants of adoption of PMFBY, a stratified multi-stage random sampling technique was followed to select the households for field survey. In the first stage, Bolangir district has been chosen as the study area as this district shows greater vulnerability to drought as compared to other districts in Odisha. In the second stage, Bangomunda block was selected from the district. In the third stage, from this block, six villages, namely, Bhalumunda, Jurabandh, Sangamara, Turekela, Tentelpara and Kuturabeda, were selected according to high coverage of PMFBY. Finally, 80 loanee PMFBY users, who were compulsorily covered under PMFBY, and 80 non-loanee PMFBY users, who voluntarily purchased PMFBY, were randomly chosen from the selected villages. To explore the reasons for non-adoption of crop insurance, 40 non-users of PMFBY were also randomly selected. Thus, a total of 200 households were included in the study. Primary data were collected from these households by direct interview method with the help of structured questionnaires. Data were collected for 2016–2017 rabi and 2017 kharif seasons.

Survey Findings

Socio-economic Profile of Insurance Users and Non-users

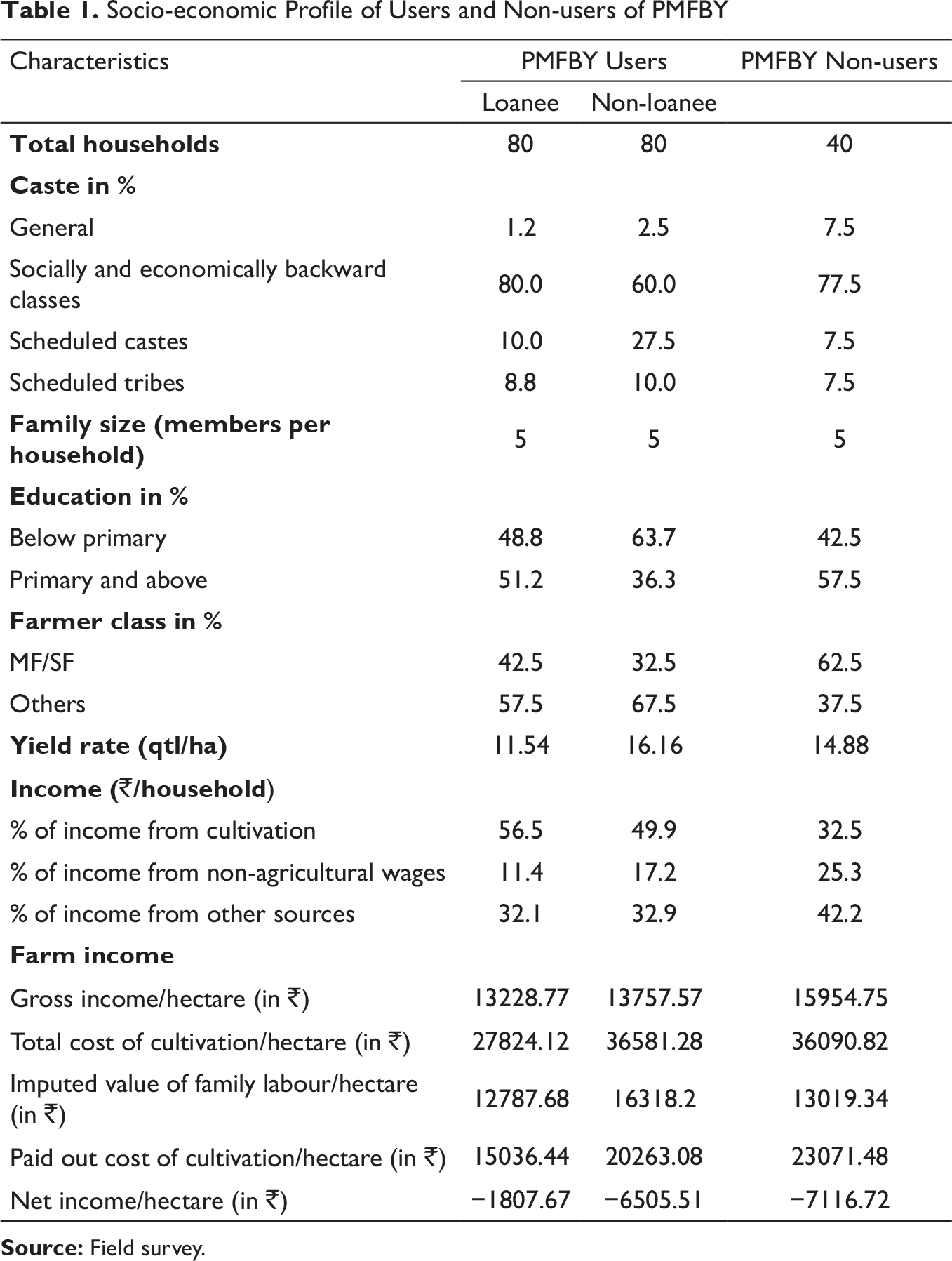

The operational efficiency of any crop insurance scheme depends on its adoption rate. The adoption of insurance in turn depends on various socio-economic characteristics of farmers which include their social configuration, education level, sources of income, size of land holding, asset ownership and farm income. Therefore, the socio-economic profile of insurance users and non-users in the study area have been examined and presented in Table 1.

A comparison of the socio-economic characteristics of users and non-users of crop insurance reveals that the majority of the loanee (80%) and non-loanee (60%) PMFBY users and non-users (77.5%) belong to socially and educationally backward classes (SEBCs). However, the percentage of Scheduled Caste (SC) and Scheduled Tribe (ST) insurance users is greater in the case of non-loanee (37.5%) than that of loanee (18.8%) insurance users. Thus, the lower caste farmers are more risk-averse and are voluntarily adopting crop insurance as a risk management tool. The proportion of farmers having education of primary level (class 5) and above is 51.2 per cent in the case of loanees, 36.3 per cent for non-loanees and 57.5 per cent for non-users. Thus, it cannot be concluded that farmers with higher literacy rate have adopted insurance. As regards size of land ownership, a higher percentage of non-users are marginal and small farmers (62.5%), owning land less than 2 ha in comparison to loanee (42.5%) and non-loanee (32.5%) insurance users. With regard to sources of income, cultivation is the major source of income for all the sample households. Nevertheless, the percentage of income from cultivation to total income is substantially greater for loanee (56.5%) and non-loanee (49.9%) insurance users than for non-users (32.5%). Thus, the farmers who are more dependent on agriculture to earn their livelihood are buying insurance.

Socio-economic Profile of Users and Non-users of PMFBY

During kharif 2017, the per hectare yield rates of paddy for loanee and non-loanee insurance users and non-users were 11.54 quintals, 16.16 quintals and 14.88 quintals, respectively (Table 1). Non-loanee insurance users thus have a higher yield rate, demonstrating that progressive farmers come forward to insure their crops voluntarily. However, as the survey year was a drought year, almost all the households had a below-normal yield. According to the farmers, the normal yield of kharif paddy in their villages is 29 qtls/ha. Because of low yield owing to drought condition, the net income per hectare of kharif paddy arrived at by subtracting the cost of cultivation from gross income is found to be negative for all sample households. Among the users of crop insurance, the amount of loss incurred by non-loanees (₹6,506/ha) is greater than that incurred by loanees (₹1,808/ha), which has prompted them to adopt crop insurance voluntarily. However, it is observed that the highest amount of loss is borne by non-users (₹7,117/ha), which indicates their inefficiency in paddy cultivation (Table 1).

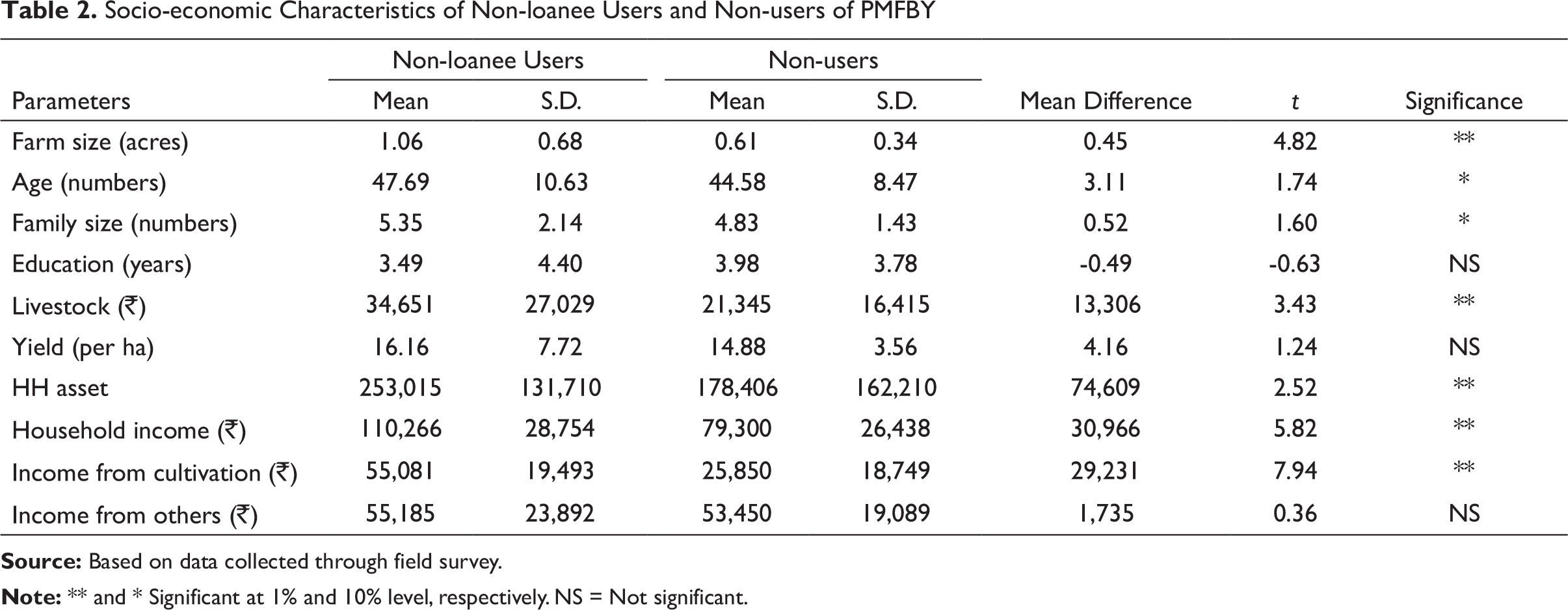

Differences in Socio-economic Characteristics of Non-loanee Users and Non-users

In this section, an attempt is made to find out whether there is a significant difference among the socio-economic characteristics of the non-loanee users and non-users of PMFBY. For the loanees, the option of buying the insurance does not arise as they are compulsorily covered under the scheme. On the other end, the non-loanees have purchased crop insurance voluntarily, whereas the non-users have not gone for insurance. Therefore, the t-test was applied to find out the level of significance between mean difference of various socio-economic variables of the non-loanee users and non-users of PMFBY (Table 2).

The t-test statistics show that there is positive and significant difference between most of the socio-economic characteristics of non-loanee users and non-users of PMFBY, which include farm size, age, family size, value of livestock, yield per hectare, asset holdings, household income and income from cultivation. However, there is no significant difference in education level, yield and income from other sources between non-loanee users and non-users of crop insurance. Contradicting the usual expectation, the mean value of years of education indicates that non-users of PMFBY have a higher level of education than non-loanee users. This may be due to occupational diversification adopted by educated non-users to manage risks, as the share of non-farm income in total household income is greater for them than for non-loanee insurance users (Table 2).

Determinants of Adoption of Crop Insurance

Socio-economic Characteristics of Non-loanee Users and Non-users of PMFBY

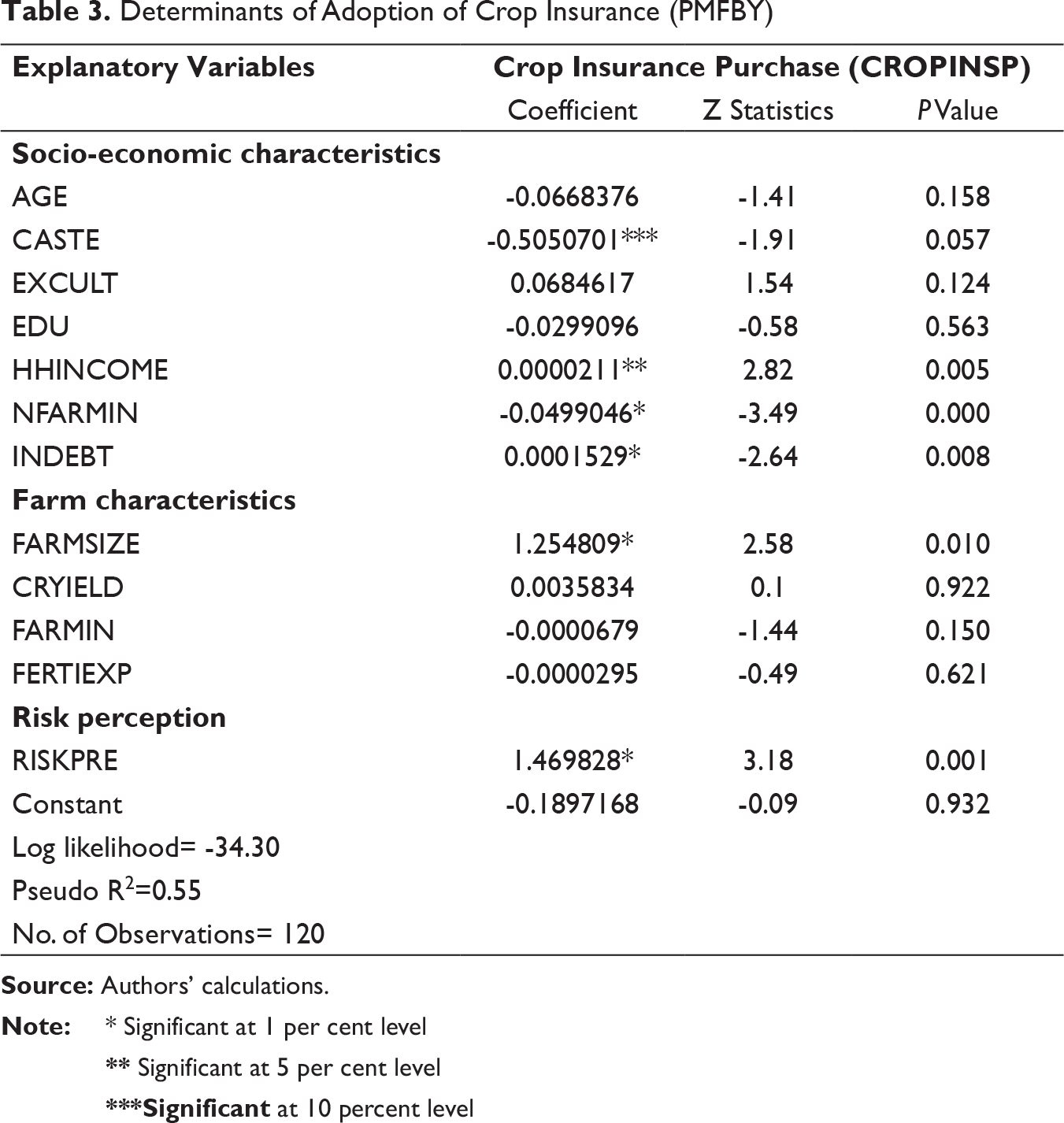

In the above context, a probit regression equation is fitted to identify the determinants of adoption of crop insurance by the farmers. The regression equation is estimated only for non-loanee users (who purchase insurance voluntarily) and non-users of crop insurance. The loanee farmers, for whom crop insurance is compulsory, are excluded from the analysis, as buying crop insurance is not a choice variable for them. The dependent variable is the crop insurance, adoption behaviour = 1 if opted for insurance and adoption behaviour = 0 if not opted for insurance. The explanatory variables are shown in the probit regression equation as mentioned below.

CROPINSP= f (AGE, CASTE, EXPCULT, EDU, HHINCOME, NFARMIN, INDEBT, FARMSIZE, CRYIELD, FARMIN, FERTIEXP, RISKPRE)

where CROPINSP is crop insurance purchase, which can take the value of either 0 or 1.

AGE = age of the farmer in years

CASTE = whether the farmers belongs to SC/ST; if yes = 1, if no = 0

EXPCULT = number of years of experience in the cultivation

EDU = number of years the farmer has received education

HHINCOME = total income of the household

NFARMIN = percentage of non-farm income to total income

INDEBT = amount of the outstanding loan

FARMSIZE = size of operational holdings

CRYIELD = actual yield per hectare

FARMIN = gross farm income

FERTIEXP = expenditure of aggregate fertilizer per hectare in rice production

RISKPRE = risk perception of the farmer; 1 denotes risk-loving and 5 denotes risk-hating

As shown in Table 3, the above explanatory variables have been grouped under three heads: (a) socio-economic characteristics, (b) farm characteristics and (c) risk perception of the farmers.

The estimated results of the probit model are given in Table 3. The results reveal that among the socio-economic variables considered for the analysis, the caste of the farmer, household income and proportion of the non-farm income are statistically significant and show expected signs. Farmers belonging to higher caste and having higher household income are more likely to insure their crops. Farmers more dependent on non-farm income are less inclined to buy crop insurance. It is also observed that there is a significant and positive relationship between indebtedness and adoption of crop insurance. Coefficient of age of the farmer (negative) and experience in cultivation (positive) also show the expected signs, but their values remain statistically insignificant.

Determinants of Adoption of Crop Insurance (PMFBY)

** Significant at 5 per cent level

***Significant at 10 percent level

With regard to the farm characteristics that determine the adoption of PMFBY, the farm size and crop yield exhibit expected signs; thus, farmers with higher farm size and higher crop yield are more likely to insure their crops. Furthermore, the coefficient value of farm size is also statistically significant; however, crop yield is statistically insignificant. The remaining explanatory variables (gross farm income from cultivation and expenditure of aggregate fertilizer per hectare in rice production) under the farm characteristics category, neither show expected signs nor are significantly correlated to adoption of PMFBY.

With reference to the risk perception of the farmers, the outcome of the probit model also exhibits expected sign and is also statistically significant. Thus, the adoption of the crop insurance depends on their perception of risk; the more risk-averse farmers insure their crops (Table 3). Overall, the pseudo R2 obtained from the analysis indicates that the independent variables included in the probit model explain 55 per cent of variations in farmers’ adoption or non-adoption of the PMFBY.

Rationale Behind Adopting Crop Insurance

The insurance users in the study area furnish various reasons for adopting crop insurance. The non-loanee users of PMFBY appeared to be more inclined to avoid risk because of which they had voluntarily opted for the crop insurance. Both the loanee and non-loanee users cited that the low premium amount induced them to go for crop insurance. Some users also indicated that they were influenced by the advice of the progressive farmers. Moreover, they considered crop insurance as an instrument for reduction of risk, and having financial security was their main motivation for adopting insurance.

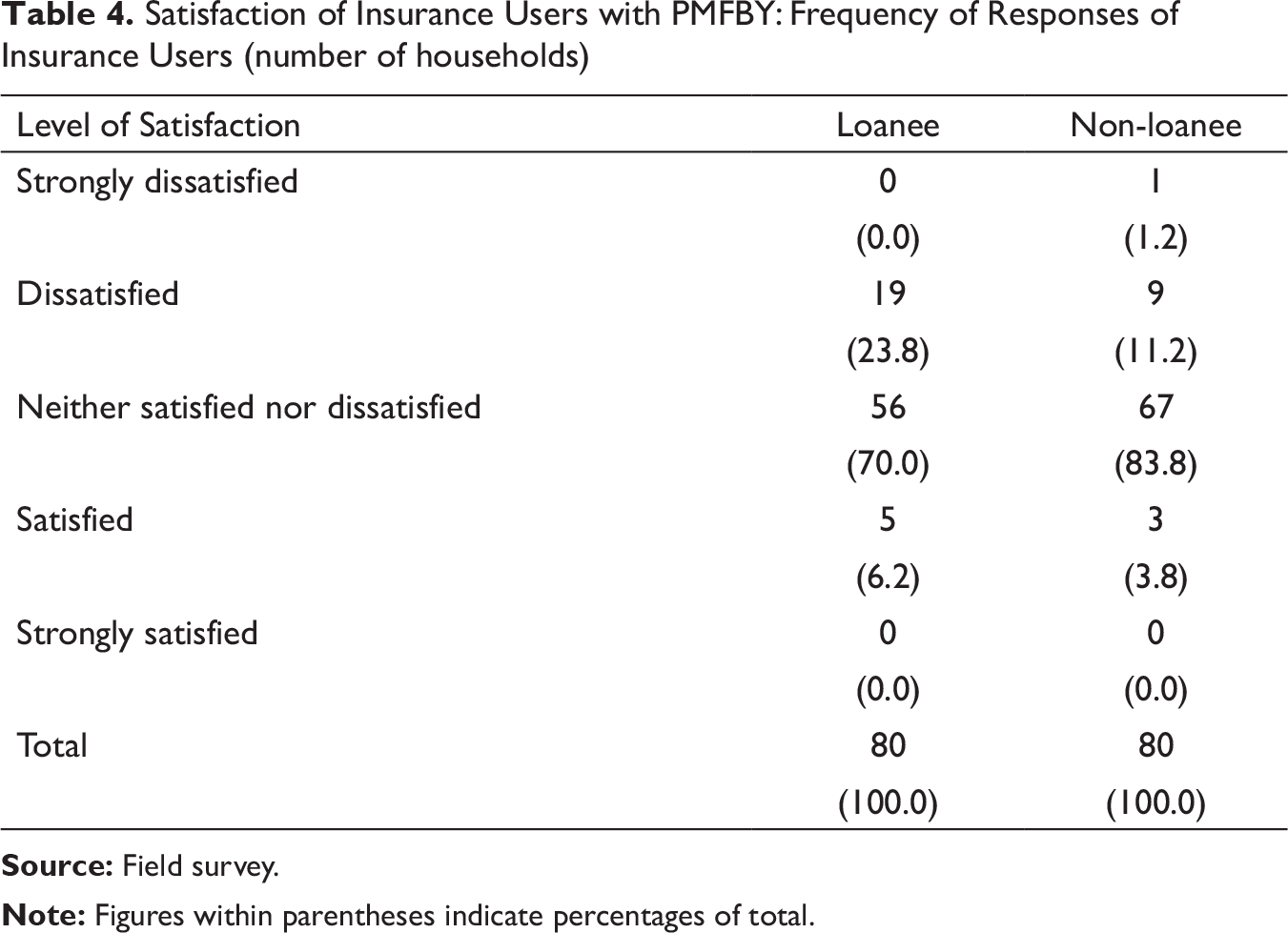

Though there is an utmost need for crop insurance in the risky environment of the study area, farmers are not coming forward in large numbers to insure their crops. Hence, the efficacy of the PMFBY, currently under implementation in the area, is assessed by evaluating the level of satisfaction and dissatisfaction of insurance users with the scheme. An attempt has also been made to identify the causes of dissatisfaction and non-adoption.

Satisfaction with Crop Insurance

Satisfaction of Insurance Users with PMFBY: Frequency of Responses of Insurance Users (number of households)

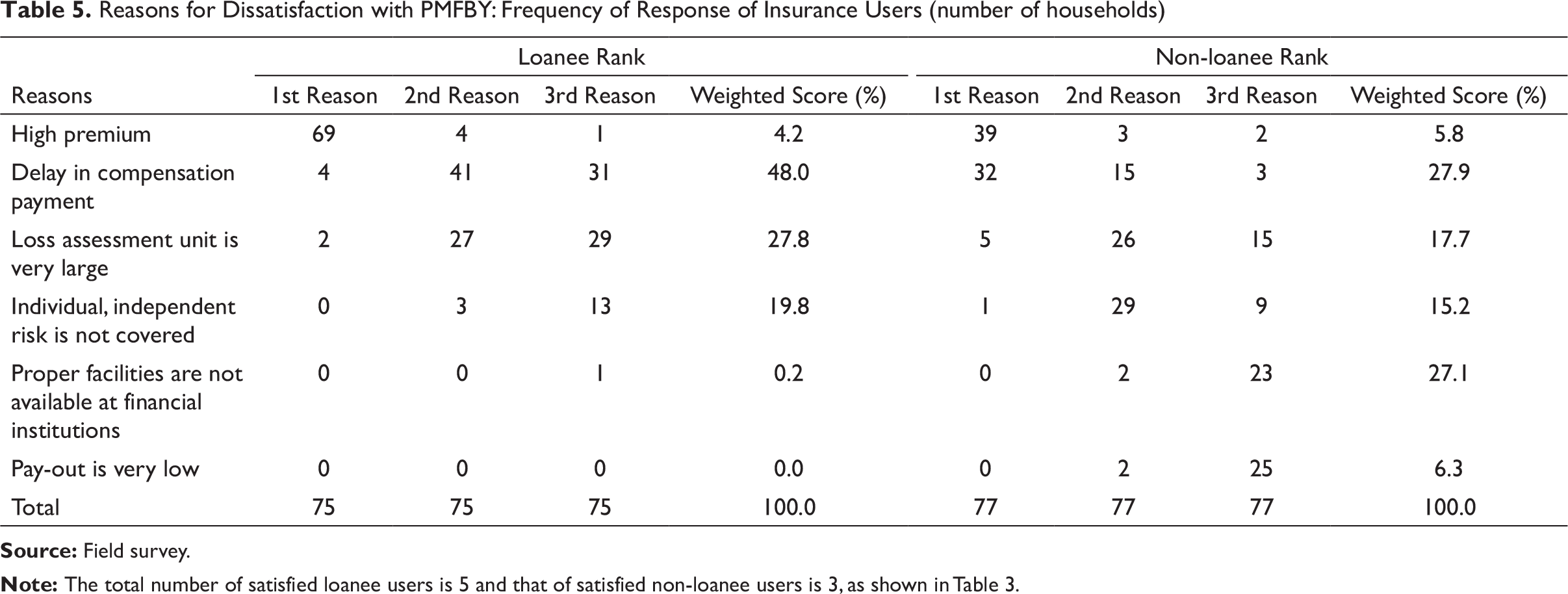

Reasons for Dissatisfaction with PMFBY: Frequency of Response of Insurance Users (number of households)

In order to find out the reasons for their dissatisfaction, the insurance users were asked to rank the three most important reasons as 1st, 2nd and 3rd. The percentage-weighted score is calculated by assigning the value of 3, 2 and 1 to the most important, second most important and third most important ranks, respectively. Table 5 gives the data on the frequency of responses and the percentage-weighted score on various causes of dissatisfaction.

The major reason for dissatisfaction as reported by both loanee (48%) and non-loanee (27.9%) insurance users was delay in compensation payment. Estimation of crop yield on the basis of crop cutting experiments was a time-consuming process. Furthermore, the insurance users complain about individual, independent risk not being covered under the scheme and express their dissatisfaction relating to the unit area of loss assessment being very large. The non-loanees (27.1%) were also discontented because of non-availability of proper facilities at financial institutions (Table 5).Overall the PMFBY failed to stabilise the insurance users’ income and provide them economic support during adverse circumstances.

Why Non-adoption of Crop Insurance?

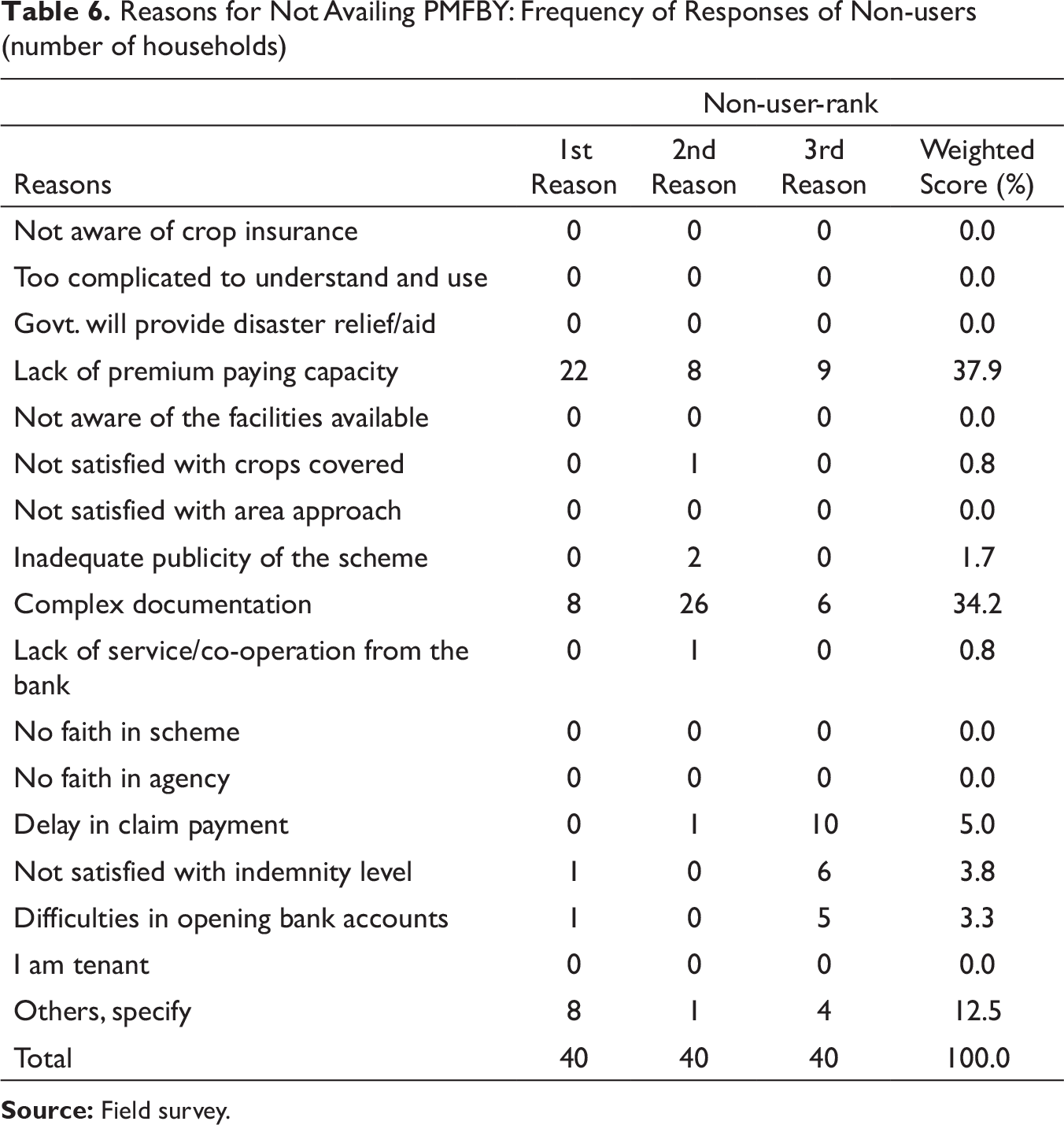

The farmers in the study area who were not covered under PMFBY were interviewed to understand the reasons for their non-adoption. Table 6 gives the data on the frequency of responses and the percentage weighted score on various causes of non-adoption.

The two most important reasons for not taking up insurance as reported by the respondents are: lack of premium paying capacity (37.9%) and complex documentation (34.2%). Moreover, they also complained that the time duration within which they must go for insurance was too short. A few non-users also claimed delay in payment of the claims, dissatisfaction with indemnity level and difficulty in opening bank accounts as other reasons behind not taking up crop insurance (Table 6). However, none of the respondents cited unawareness as a cause of non-adoption of PMFBY.

Improving Scheme Performance

Reasons for Not Availing PMFBY: Frequency of Responses of Non-users (number of households)

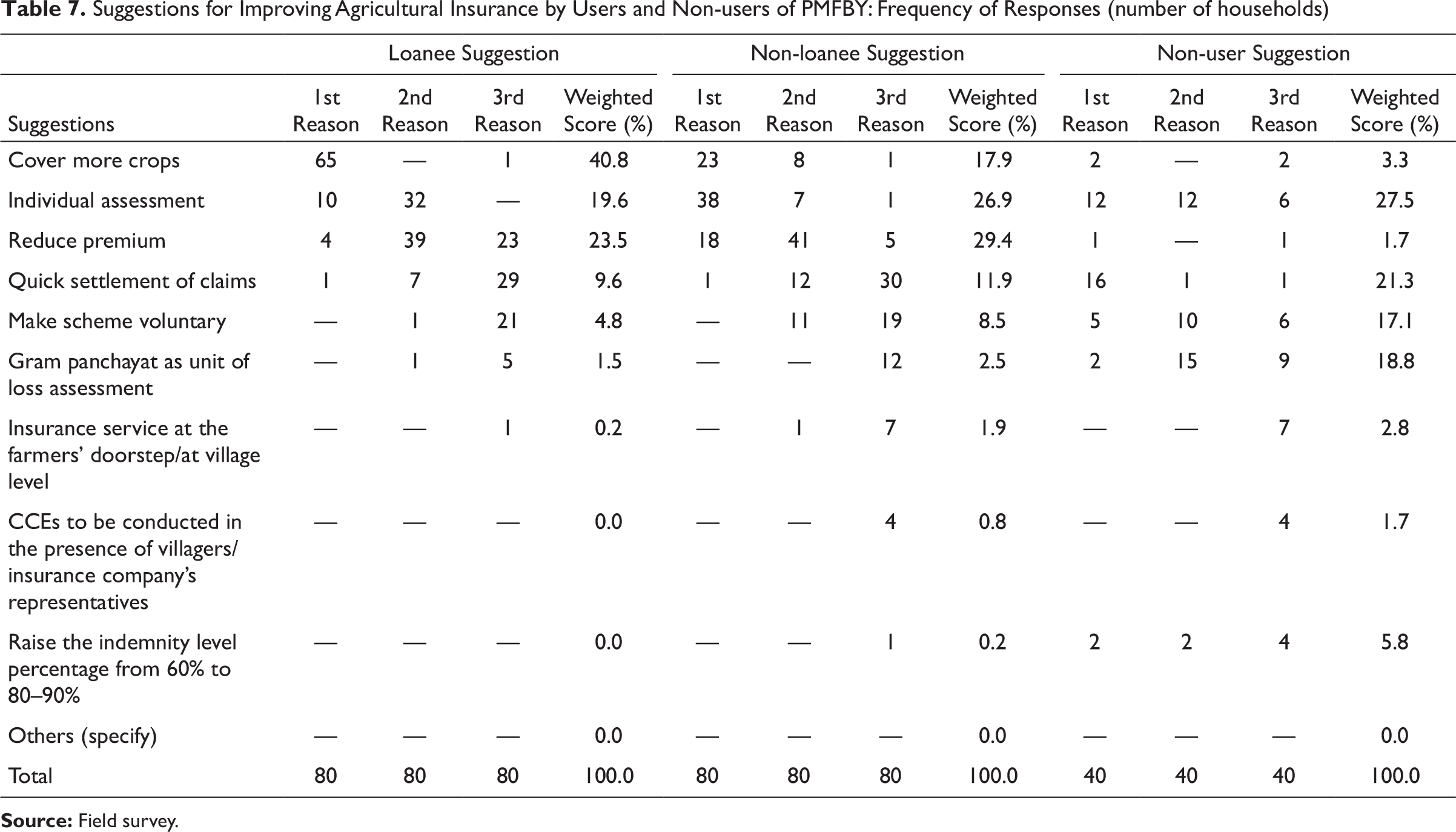

Suggestions for Improving Agricultural Insurance by Users and Non-users of PMFBY: Frequency of Responses (number of households)

Conclusions and Policy Implications

The results of the regression analysis on adoption behaviour of insurance reveal that higher caste farmers with greater farm size, larger household income and indebtedness and risk-averse farmers are more likely to adopt the PMFBY. Farmers more dependent on non-farm income are less inclined to buy crop insurance. Young farmers have a positive attitude towards experimenting with the insurance. Cultivators with more experience in cropping also are more likely to insure their crops.

However, progressive farmers with higher gross farm income from paddy cultivation and greater expenditure on fertilizers are less inclined to adopt PMFBY; the plausible explanation may be that as a major part of their household income comes from sources other than cultivation, they are least bothered about their income from cultivation. Another major diversion noted is that the level of education is negatively correlated with the adoption of PMFBY; the probable reason behind such a finding is that with increase in years of education, farmers branch out to other non-farming activities and start up small businesses as a long-term risk management strategy.

Despite being one of the important tools of risk management, PMFBY has not gained wide acceptance in the study area. The survey findings reveal that a significant proportion of insurance users were not satisfied with PMFBY. As low as 6.2 per cent of loanees and 3.8 per cent of non-loanees expressed their satisfaction with the scheme. The important reasons for dissatisfaction with the scheme as reported by insurance users were delay in compensation payment and very large loss assessment unit. The users also complained about individual and independent risks not being covered under PMFBY. The non-users had not adopted the insurance primarily due to lack of premium-paying capacity and its complex documentation.

In the study area, insurance facility was available only for cultivation of paddy; however, the farmers expected that insurance coverage should as well be extended to cash crops such as cotton and sunflower grown in the area.

As PMFBY is an area-based agricultural insurance scheme, it does not cover independent and individual risks. It is suggested that the public sector may address catastrophic covariate risks and provide multi-peril insurance where the subsidy requirement is high, while the private sector may be encouraged to provide insurance products for less severe events and for individual, independent, idiosyncratic and localized risks at actuarial premiums. The coverage of crop insurance can be increased by the active participation of banks, co-operatives, non-governmental organizations (NGOs), Panchayati Raj institutions (PRIs), self-help groups (SHGs) and microfinance institutions in awareness creation as well as by providing the service at the doorstep of the farmers through insurance agents.

Footnotes

Acknowledgement

The principal author is grateful to the Indian Council of Social Science Research, New Delhi for awarding Senior Fellowship for full-time research, which enabled her to prepare this paper.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.