Abstract

Research suggests that financial crises are inherently and mostly communication problems, making it crucial to study how central banks deploy crisis communication strategies for reputation management. This study proposed financial crisis communication conceptual framework to examine how the Central Bank of Ghana communicatively managed the financial industry reputation during the Ghanaian banking crisis. Findings revealed that whereas the Central Bank of Ghana deployed justification, differentiation, shifting blame, and attacking the accuser strategies to manage its own reputation, it used corrective action, good intentions, and minimization strategies to manage the reputation of the financial industry at large. Implications for practice are discussed.

Keywords

Introduction

In recent times, central banks have been increasingly recognizing the importance of communication in ensuring transparency and accountability to stakeholders and reducing uncertainties surrounding monetary policies in the financial markets (Hayo et al., 2015). This recognition has led central banks to invest heavily in efforts to improve their communication with the financial markets (Hayo & Neuenkirch, 2015). As a result, the financial communication literature has mostly examined how central bank communication influences financial market outcomes (Coeure, 2017; Reeves & Sawicki, 2007). For example, Ehrmann and Fratzscher (2007) found that central bank communication significantly affected interest rates. Financial crises present communication challenges for central banks, and some scholars (e.g., Fassin & Gosselin, 2011; Jameson, 2009) have suggested that financial crises are inherently and mostly communication problems, making it crucial to understand how central banks deploy crisis communications strategies for reputation management during financial crises. However, limited research has examined the financial setting of developing countries like Ghana, creating an epistemic gap. The present study sought to examine the crisis response strategies of the central bank of Ghana during the banking crisis.

Between 2017 and 2019, Ghana experienced a banking crisis that has been described as one of the country’s biggest economic crises, costing the government more than US$2 billion to protect investments of customers and restore economic stability (Tindi & Obeng-Hinneh, 2023). Responding to the crisis, the Central Bank of Ghana revoked the licenses of nine indigenous banks and also introduced several structural reforms to stabilize the banking industry and retore stakeholder confidence in the industry (Dwamena & Yusoff, 2022). Throughout the crisis, the Bank of Ghana (BoG) used press releases and speeches as important messaging strategies to convey information to stakeholders of the financial industry and the general public. The present study has two aims. First, this study used Hong et al.’s (2023) integrated crisis response framework to qualitatively examine the press releases and speeches of BoG to determine how BoG used its crisis response strategies to communicatively manage its own reputation and that of the financial industry during the banking crisis. Second, although a financial crisis is different from other types of corporate crises because of its intensified complex nature and industry spillover effect (Jin et al., 2018), extant research is yet to articulate financial crisis communication (FCC) as a conceptual framework for better theorizing of financial crises from a communication perspective. Hence, this study made an initial attempt to articulate FCC conceptual framework to determine the effectiveness of BoG’s crisis response strategies.

Conceptualizing Financial Crisis Communication

Financial communication is very crucial because (1) it contributes to the stability and growth of an organization and an economy in general, (2) it helps to maintain and improve the credibility of an organization, (3) it helps to reduce uncertainties among stakeholders of the organization, and (4) it helps an organization to be more transparent and accountable to its stakeholders (Hayo & Neuenkirch, 2015; Hearit, 2018). Financial crises, however, pose serious challenges for communication leaders and effective financial communication (Hayo & Neuenkirch, 2015). In fact, some scholars (e.g., Fassin & Gosselin, 2011; Jameson, 2009) argue that financial crises are inherently and mostly communication problems. For example, Fassin and Gosselin (2011), in their examination of factors leading to the collapse of the Fortis Bank during the 2008 global financial crisis, suggest that incomplete information can lead to “misinterpretation, suspicion and mistrust, and to the perception of unfair treatment” (p. 187), thereby causing a financial crisis.

A financial crisis has two distinctive features: intensified complexity and industry spillover effect (Jin et al., 2018; Johansson & Nord, 2017). As intensively complex in nature, a financial crisis has a “widespread and long-lasting impact on the society” (Jin et al., 2018, p. 575) and also tarnishes the credibility of many key institutions within the financial industry. Additionally, the complex financial systems, which are usually difficult to understand, contribute to the intensified complex nature of a financial crisis (Jin et al., 2018). The implication is that a financial crisis may require a complex response strategy to manage. Second, the industry spillover effect feature indicates that a financial crisis does not only affect the reputation of an organization responsible for the crisis but also affects reputations of other organizations within the financial industry. This phenomenon, classified in the literature as reputational common (Frandsen & Johansen, 2018) or industry reputation (Winn et al., 2008), challenges the traditional understanding of reputation where an organization manages its own reputation. In this regard, a financial crisis may require a more collective approach to manage all conflicting response strategies of competing organizations within the financial industry (Frandsen & Johansen, 2018).

The proposed FCC conceptual framework has two dimensions: communicative complexity (CC) and collective reputation management (CRM). The aim of this framework is to consolidate all the literature focusing on financial crises under a broader umbrella for better theorizing of a financial crisis to advance research and practice in crisis and business communication. The first dimension is CC, which refers to communication activities that address the diverse stakeholders’ needs and the connections among those needs during a financial crisis (Kleinnijenhuis et al., 2015). A financial organization does not only address both its own needs and those of its immediate stakeholders but also the needs of other stakeholders within the financial industry, making a financial crisis a complex one to manage. On the other hand, other corporate industries with less complex systems where the credibility of one organization is not linked directly to another organization within the same industry might require a less complex communication effort. Thus, we argue that for a financial organization that is involved in a crisis to successfully ensure its reputation, it should deploy a communication approach that seeks to address all the diverse public needs including those of the larger stakeholders of the industry and the connections among those needs in a more systematic manner.

The second dimension is CRM, which refers to communication activities that seek to manage both the reputation of the organization causing the crisis and that of the financial industry. The current conceptualization of CRM in the financial crisis context is different from that of Winn et al. (2008), in that the former recognizes the need for an organization responsible for the crisis to manage both its own reputation and that of the industry, whereas the latter focuses on the collective efforts of all organizations regardless of which organization is responsible for the crisis in managing only the industry reputation. The current CRM dimension is also different from reputational common and crisis communication of meta-organizations. Reputational common is when stakeholders are unable to differentiate the performance of one organization from another because the reputations of all organizations are tied to one another (King et al., 2002). Hence, organizations within the same industry seek to help their stakeholders to differentiate their performances from others during crises. Crisis communication of meta-organizations views crises from the perspective of meta-organizations and intermediaries where trade associations mediate between member organizations and stakeholders during crises (Frandsen & Johansen, 2018). Building on these conceptual definitions, this CRM dimension focuses on how a financial institution involved in a crisis can deploy a communication strategy that manages both its own reputation and that of the financial industry.

Crisis Response Strategies and Reputation Management

In times of crises, organizations take steps to manage their reputations (Lee & Atkinson, 2019; Zhu et al., 2017). Image restoration theory (IRT) and situational crisis communication theory (SCCT) are two dominant crisis communication theories that help to assess how organizations successfully and effectively manage their reputations during crises (Benoit, 2015; Coombs et al., 2019). William Lyon Benoit, a renowned political communication scholar, developed the IRT as a message-driven rather than a situation-driven theory. In other words, the theory focuses on what an organization can say when facing a crisis (Benoit, 1997). IRT is premised on two assumptions (Benoit, 2018). First, it assumes communication as a goal-oriented activity that should be salient, clear, and reasonable to achieve at the time the goal was made (Benoit, 2016). Second, it assumes that maintaining a positive reputation is one of the central goals of communication (Benoit, 2016). The need to maintain a favorable image motivates individuals or organizations to respond to persuasive attacks resulting from disappointments, mistakes, accidents, or dissensions (Benoit, 2016). IRT provides five broad crisis response strategies for restoring damaged reputations: (1) denial with two variants (simple denial and shift blame); (2) evasion of responsibility with four variants (provocation, defeasibility, accident, and good intention); (3) reducing offensiveness with six variants (bolstering, minimization, differentiation; transcendence, attack the accuser, and compensation); (4) corrective action; and (5) mortification (Benoit, 1997, 2016). The denial strategy is used by an organization to simply deny crisis responsibility and shift blame. However, when an organization is not able to deny its responsibility for the crisis, it uses the evasion of responsibility strategy to reduce its perceived responsibility of the crisis. The reducing offensiveness strategy is used to lessen the negative feelings (perceptions) toward the organization. The corrective action is used by an organization to demonstrate its commitment of rectifying the problem(s) associated with the crisis and putting in measures to prevent a recurrence of the crisis. Lastly, organizations use mortification strategy to admit responsibility for the crisis and ask for forgiveness.

Timothy Coombs, a renowned crisis communication scholar, developed SCCT in 2007 by drawing from the attribution theory. SCCT focuses on the attribution of crisis responsibility, that is, who is responsible for the crisis and to the extent to which an organization or person can be held responsible for the crisis (Coombs, 2007; Coombs & Tachkova, 2023). The determination of crisis responsibility is examined within the scope of three clusters: victim (weak attribution of crisis responsibility), accidental (minimal attribution of crisis responsibility; the actions of the organization contributing to the crisis were unintentional), and avoidable (high attribution of crisis responsibility; the organization intentionally caused the threatening situation to stakeholders) (Coombs, 2020). SCCT provides 10 crisis response strategies for managing damaged reputations under four clusters: denial (attacking the accuser, denial, scapegoating), diminishment (excusing, justification), rebuilding (apology, compensation), and bolstering (reminding, ingratiation, victimage) (Park, 2017). The denial strategy allows the organization to refute responsibility for the crisis. Diminish response strategy allows the organization to create the impression that the crisis is not as bad as perceived or that there was nothing the organization could do to prevent the crisis. Rebuild is used to improve the reputation of the organization, and it involves the show of care and support for crisis victims (Coombs, 2007). SCCT argues that a successful crisis communication effort should match the crisis response strategies to the appropriate crisis type (i.e., victim, accidental, and avoidable crisis) (Hong et al., 2023).

A recent study has combined IRT and SCCT to form an integrated crisis response framework comprising both defensive (i.e., denial, shifting the blame, justification, minimization) and accommodative strategies (bolstering, corrective action, apology) to examine the impact of universities’ crisis response strategies in the context of the COVID-19 pandemic (Hong et al., 2023). The crisis communication literature suggests that while defensive strategies are most appropriate and effective for victim and accidental crisis situations, accommodative strategies are most appropriate and effective for preventable crisis situations (Hong et al., 2023). Utilizing Hong et al.’s (2023) integrated crisis response framework, this study examined how a central bank used its crisis response strategies to manage its reputation and the overall reputation of the industry during a banking crisis.

Study Context and Aims

The banking industry of Ghana began in 1896 during the colonial period with the establishment of the Bank of British West Africa (BBWA), currently known as the Standard Chartered Bank (Dwamena & Yusoff, 2022). Following the success of BBWA, the Barclays Bank was established in 1925 to compete with BBWA (Osei et al., 2019). These two expatriate banks functioned as commercial banks by providing financial services to the colonial governments and their enterprises from the 1920s to the 1950s (Osei et al., 2019). After Ghana attained independence in 1957, the Bank of Ghana was established as the central bank to manage the currency of the country and supervise the operation of all banks in the country (Obuobi et al., 2020). Between 1957 and 2000, several legislations and banking laws were introduced to facilitate the establishment of many state-owned and private-owned commercial banks (Amenu-Tekaa, 2022). In 2015, the Bank of Ghana (BoG) conducted asset quality review (AQR) of all banks. The findings of the report revealed that 10 banks were undercapitalized, had high levels of nonperforming loans, had poor corporate governance practices, and had poor credit risk management practice (Dwamena & Yusoff, 2022). Based on these findings, BoG withdrew the licenses of nine banks leading to the banking crisis of 2017 to 2019. In that same time period, BoG also undertook significant structural reforms by raising the capital requirement and strengthening the regulatory laws that led to the reduction of the total number of banks from 36 to 23. The government spent over GH¢12 billion (around US$2 billion) to restore lost investments and protect depositors’ funds in the nine collapsed banks (Tindi & Obeng-Hinneh, 2023). Throughout the crisis, BoG used press releases and speeches to communicate these reforms and license revocations to stakeholders and the general public. The present study sought to understand how BoG communicatively managed its reputation and that of the financial industry during the banking crisis given that little research has examined the financial setting of a developing country like Ghana.

Furthermore, literature has heavily examined banks with scarce scholarly attention to how financial regulators (i.e., central banks) communicatively manage their reputations during crises although central banks as regulators perform distinct functions. Whereas banks perform the functions of accepting deposits, granting loans and advances, and acting as agents for their customers including utility functions, central banks perform the functions of overseeing the monetary policy and currency of a country and also regulating banks, financial institutions, and payment systems of the country. The implication is that central banks, unlike banks, can introduce and implement structural reforms during crises to stabilize the financial industry. For example, in the case of Ghana, the laws of the country allowed the central bank to introduce structural reforms and revoke the licenses of nine banks to sanitize and stabilize the financial sector during the recent banking crisis. Thus, examining how BoG communicatively managed its reputation and the overall reputation of the financial industry during the 2017-2019 banking crisis could provide valuable insights for financial and business communication leaders and crisis communication scholars. The present study utilized Hong et al.’s (2023) integrated crisis response framework and the proposed FCC conceptual framework to examine how BoG used communication to strategically manage both its organizational and industry reputations by asking the following research questions:

Research Question 1: What crisis response strategies did the central bank deploy during the banking crisis in Ghana?

Research Question 2: Were the crisis response strategies effective in managing the reputation of the central bank and that of the banking industry?

Method

This study utilized a qualitative research approach to “uncover and interpret” (Merriam & Tisdell, 2016, p. 25) meanings embedded in the crisis response strategies deployed by BoG to manage its reputation and that of the financial industry. Second, the qualitative method allowed the researchers to conduct an in-depth analysis into the crisis response strategies of BoG. The analysis focused on press releases and speeches because past research suggests that organizations use press releases and speeches as important messaging strategies to convey information to their internal and external stakeholders (Hearit, 2018). Two press conference statements, two press releases, and six speeches from August 2017 to December 2019 were retrieved from BoG’s website and a news media organization in Ghana. BoG used the press conference statements to announce license withdrawals of nine banks and reforms to the general public. BoG used the press releases to respond to claims made in the news media by the former deputy governor of BoG and to also announce a new consolidated bank to the general public. Additionally, BoG used the speeches to announce key reforms to professional stakeholders at the annual dinner and conference of the Ghana Chartered Institute of Bankers. The press conference statements including the first press release were retrieved from Graphiconline, a public online news media organization. The second press release and six speeches were retrieved from the official website of BoG.

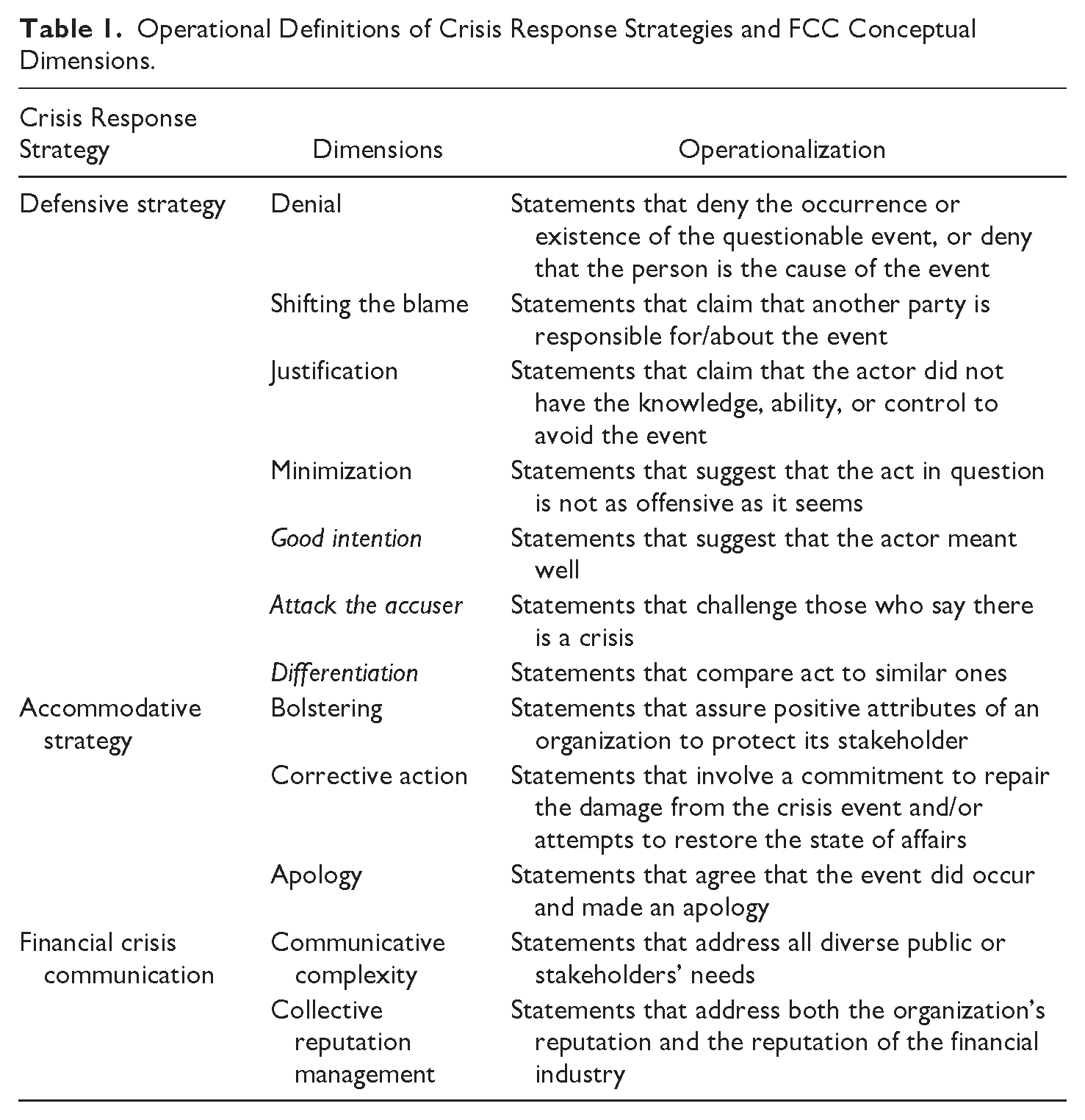

Guided by an integrated crisis response framework and the FCC conceptual framework, a deductive thematic analysis was utilized to allow the researchers to identity new themes that “did not fit within existing [crisis response strategy] typologies” (Frederick et al., 2021, p. 134), and further analyses were conducted on those emerging themes. Specifically, Hong et al.’s (2023) combined IRT with SCCT to form an integrated crisis response framework comprising both defensive strategies (i.e., denial, shifting blame, justification, and minimization) and accommodative strategies (i.e., bolstering, corrective action, and apology). Expanding Hong et al.’s (2023) framework, the current study added good intention, attack the accuser, and differentiation to the defensive strategies to have a more comprehensive crisis response framework. Furthermore, this study utilized the dimensions of the proposed FCC conceptual framework (i.e., communicative complexity and collective reputation management) to examine the effectiveness of BoG’s crisis response strategies in managing its own reputation and that of the banking industry. See Table 1 for the operational definitions of all the crisis response strategies (adapted from Benoit, 2016; Hong et al., 2023) and the dimensions of the FCC conceptual framework.

Operational Definitions of Crisis Response Strategies and FCC Conceptual Dimensions.

To conduct the qualitative content analysis, Braun and Clarke’s (2006) thematic analytical approach was utilized to enable the researchers to identify, analyze, and report themes within the data. First, the first author retrieved the press releases and speeches in word documents and read and reread these documents to familiarize himself with the data. Notes were taken to produce a list of ideas that was used to generate initial codes from the data. The data were coded around the crisis response strategies and the dimensions of the FCC conceptual framework. The first author manually coded the data to “indicate potential themes” (Braun & Clark, 2006, p. 89). After a preliminary analysis by the first author, the researchers met to review and discuss the identified crisis response strategies and the dimensions of the FCC conceptual framework to ensure they accurately captured and reflected the strategies and dimensions used by BoG. Of the 10 crisis response strategies, the analysis produced seven strategies that were employed in the press releases and speeches. Finally, to boost the credibility of this study’s findings, some portions of the speeches and press releases (i.e., data) were quoted in the narrative of the results as supportive evidence (Miles & Huberman, 1994).

Results

The Crisis Response Strategies of the Bank of Ghana

The qualitative content analysis revealed that BoG used both defensive and accommodative crisis response strategies. Seven crisis response strategies were used. The defensive strategies included shifting blame, justification, good intention, minimization, differentiation, and attack the accuser. Corrective action was the only accommodative strategy used.

Corrective action

BoG employed the corrective action strategy to demonstrate their commitment to minimizing the impact of the banking crisis on stakeholders, customers, and the economy of the country by implementing a comprehensive set of reforms which included directives on financial holding companies, proper corporate governance practices, fit and proper person’s directive, and capital requirement directive for compliance. Also, BoG explained in its press statements that it was working together with state enforcement agencies to retrieve all funds and assets from loan defaulters, shareholders, and directors and to also prosecute any persons who contributed to the challenges that led to the collapse of nine banks. Specifically, BoG noted that, “Currently, there are fifty-two (52) cases in the various courts in the country, 50 of which have been assigned to specific judges/courts.” This demonstrates the institution’s readiness to crack the whip to ensure discipline in the banking industry. Lastly, BoG announced that they had taken some administrative actions (e.g., dismissal and suspension) against some of their staff who were involved in issuing fraudulent licenses to some of the collapsed banks. This action was an attempt to boost the public confidence in the current management because of the general public’s accusations that BoG was partly responsible for some of the issues leading to the banking crisis.

Justification

BoG cited the banking laws to justify their decision to revoke the licenses of nine banks leading to the crisis. Specifically, the governor of BoG argued that they had to take that decision because those banks had breached the BoG Act 918 of 2016 and the Banks and Specialized Deposit-taking Institutions Act 930 of 2016. For example, in the maiden press conference to announce the revocation of licenses of two banks on August 14, 2017, BoG argued, The Banks and SDI Act, 2016 (Act 930) provides that undercapitalized banks be given 180 days to correct their capital position. Significantly undercapitalized banks are requested to reach a minimum capital adequacy of 5 percent in 90 days and 10 percent in 180 days. In the case of insolvent banks and banks that are likely to become insolvent, the Bank of Ghana is mandated to revoke their licenses.

In the above statement, BoG further suggests that even though those banks were given several opportunities through notifications to raise more funds to meet the minimum capital requirement by the law, they failed to meet that requirement. Additionally, BoG justified their decision by citing the Asset Quality Review (AQR) of banks report that was released in 2015 to assess the financial performance and corporate governance practices of all banks in Ghana. This report revealed that those banks had poor financial performances and poor corporate governance practices. In a nutshell, BoG appeared to communicate to their stakeholders and the general public that their decision to revoke licenses of nine banks was based on both the banking laws and conclusive evidence.

Good intentions

BoG used the good intention strategy to reduce the perceived responsibility of revoking the licenses of nine banks that led to the banking crisis. Through its various statements, BoG suggested that the revocation decision would not only help to strengthen and stabilize the banking industry but would also help to facilitate the economic transformational growth of the country. Also, BoG argued the revocation decision was intended to protect customers from losing their monies in those collapsed banks and 3,500 staff from losing their jobs. For example, in their maiden press conference, BoG noted, “Failed banks become serious sources of risk for the entire financial system and the economy as a whole and must be made to exit before they collapse the whole system.”

Minimization

BoG used the minimization strategy to downplay the impact of the license revocations on the financial sector, saying in August 2017 when revoking the licenses of two banks, “While no systemic challenges to the financial sector arose from the dissolution of two banks, it is useful to understand the underlying factors and reposition the sector to avoid the same mistakes in the years ahead.” This statement seems to direct attention from the revocation to factors that contributed to the dissolution of the two banks. In other words, BoG was reframing the narratives surrounding the license revocations.

Shifting blame

BoG blamed the previous management of BoG and the collapsed banks for the banking crisis. First, the current management of BoG blamed the previous management for failing to take mitigating actions when the 2015 AQR report revealed that some banks were significantly undercapitalized. Specifically, the current management argued in their press statements that if the previous management had implemented the International Monetary Fund’s recommendations together with findings from the AQR, the banking crisis could have been prevented. For example, in the second press release, the current management noted, “We have no evidence on record to show that the previous management took steps to mitigate the risk of failure of these institutions, as it was required to do under the Banks and Specialized Deposit-Tracking Institution, Act 930.” Additionally, the current management blamed the previous management for not using the institution’s resources to strengthen its supervisory role in the banking industry but rather used those resources to build guesthouses and hospitals. In other words, the previous management neglected their core functions and duties. Second, BoG blamed the collapsed banks for their poor corporate governance practices, insider dealings, misreporting, and other practices that put depositors’ funds at risk. In a nutshell, the current management of BoG used the shifting blame response strategy to indicate that they were not responsible for the banking crisis.

Attacking the accuser

In August 2019, the ex–deputy governor of BoG, Dr. Johnson P. Asiama, accused the current management of BoG for mishandling the current situation leading to the banking crisis. In that same month, BoG issued a press release to attack its ex–deputy governor, saying that instead of taking bold actions to prevent the crisis, he and the previous management gave out public funds to the collapsed banks whose “shareholders dissipated these funds on private ventures at the expense of depositors, employees, taxpayers, and other claimants.” This suggests that the former deputy governor and the previous management failed to ensure that these banks used the public funds for the intended purposes. Also, BoG attacked other persons who accused them that their reforms were unfairly targeting certain indigenous banks for a political expedient by saying, “These reforms have rather sadly been misconstrued as being driven by some unseen hands to score political objectives.” In dealing with this misunderstanding, BoG mentioned a report conducted by a reputable independent professional service (KPMG International) into the financial conditions of the collapsed banks to explain that these accusations were untrue and that their reforms were based on conclusive evidence.

Differentiation

The current management of BoG differentiated their actions from those of the previous management. Specifically, while the current management’s actions sought to protect customers’ monies and solve the underlying factors causing the banking crisis, the actions of the previous management caused the banking crisis. For example, in a press release, the current management noted, What he [the former deputy governor] fails to admit is the fact that the swift and decisive action taken by the Addison-led management team [current management] provided relief for other segments of the financial system through the funds provided by the Government for depositor payouts. Dr. Asiama also conveniently failed to state the truth that the majority of the MFIs and Savings and Loans/Finance Houses that failed had started showing signs of insolvency long ago, some as far back as 2012 and as was the order of the day, the “do-nothing” approach was at play.

The above statement suggests that unlike the current management, the previous management failed to take any actions to prevent the banking crisis when the signals were so glaring to avoid.

Effectiveness of the Bank of Ghana’s Crisis Response Strategies

This study examined whether the crisis response strategies deployed by BoG might be effective in managing its reputation and that of the banking industry by using the proposed FCC conceptual framework. The FCC conceptual framework has two dimensions: (1) communicative complexity (CC) refers to a communication strategy that identifies and addresses all the diverse public (stakeholders) needs and the connections among those needs; and (2) collective reputation management (CRM) refers to a communication strategy that manages both the organizational level and industry level of reputations.

The thematic analysis of press releases and speeches revealed that BoG used a complex communication strategy that attempted to address the needs of many diverse stakeholders affected by the banking crisis. The first stakeholders were the Ghana Association of Bankers and the Chartered Institute of Bankers. These professional stakeholders were concerned about how BoG would restore public confidence and trust in the banking industry. BoG used speeches to assure them that it had undertaken some structural reforms that were beginning to yield some positive outcomes. The second stakeholders included customers (both depositors and debtors) of the collapsed banks. BoG used press releases and conferences to assure 1.5 million customers that they would not lose their monies and also encourage those who took loans from the collapsed banks to pay their debts at certain designated banks across the country. The third stakeholders included staff of the collapsed banks. BoG used press conferences and speeches to assure 3,500 staff of the collapsed banks that they would not lose their jobs and would be reintegrated to designated banks across the country. The fourth stakeholders included the taxpayers and government. The government spent over GH¢12 billion (around US$2 billion) of taxpayers’ monies to restore the investments of customers of those collapsed banks. BoG used speeches and press conferences to assure the taxpayers and the government that they would properly account for those monies. The fifth stakeholders included international institutions including the International Monetary Fund (IMF) and Swiss Secretariate for Economic Affairs (SECO). BoG used speeches to assure these stakeholders that it was undertaking some reforms to strengthen the banking industry to become a viable player in the economic growth of the country.

Furthermore, the thematic analysis revealed that BoG used its crisis response strategy for collective reputation management, that is, managing both its reputation and that of the banking industry. Specifically, BoG used justification, differentiation, shifting blame, and attacking the accuser strategies to manage its own reputation. The common theme across these four strategies was that the current management of BoG was not taking responsibility for the issues leading to the banking crisis and all decisions regarding the license withdrawals were justified by the banking laws and conclusive evidence. For example, BoG blamed the shareholders and directors of the collapsed banks for their poor corporate governance practices, insider dealings, and obtaining license under false pretense, leading to the withdrawal of their licenses. On the other hand, BoG used corrective action, good intentions, and minimization strategies to manage the reputation of the banking industry. For example, BoG consistently mentioned that it had undertaken a comprehensive structural reform to strengthen the banking industry and also build public confidence in the industry.

Discussion

This study has two purposes. The first purpose was to understand how a central bank communicatively responded to a banking crisis as past research suggests that organizations take steps to manage their reputation during crises (Lee & Atkinson, 2019; Tomastik et al., 2015). The findings revealed that BoG used six defensive strategies (i.e., shifting blame, attacking the accuser, justification, good intention, minimization, and differentiation) and one accommodative strategy (i.e., corrective action) to manage its reputation and that of the banking industry. Some scholars have articulated that for an effective crisis communication management geared toward reputational repair, it is imperative to use a combination of strategies (Benoit, 2015; Frederick et al., 2024). Research also suggests that an organization uses accommodative strategies when it admits responsibility for the crisis (Coombs, 2019). However, in this particular situation, BoG employed the corrective action in combination with defensive strategies, not to necessarily admit responsibility for the crisis but rather to communicate that it is their responsibility as the regulator of the banking industry to introduce reforms to protect victims of the crisis (i.e., customers and staff) and the overall banking industry from collapsing. This ensured that BoG’s crisis response strategies did not contradict its overarching narrative that it was not responsible for the banking crisis. These findings reflect suggestions by crisis communication scholarship that applying defensive strategies to low responsibility crisis situations are more appropriate and effective for reputation management (Coombs, 2007; Coombs & Holladay, 2001). This combination of defensive and accommodative strategies by BoG might have been successful for managing its reputation and that of the industry.

The second purpose of this study was to determine whether BoG’s crisis response strategies might be effective in managing its reputation and that of the industry by using the proposed FCC conceptual framework. Findings suggest that the crisis response strategies of BoG seemed effective. Specifically, in its press statements and speeches, BoG identified all the diverse stakeholders and their needs and tailored its crisis responses to each stakeholder need. This might lead each stakeholder to form positive attitudes and perception toward BoG and its organizational reputation as the tailored messaging literature suggests that messages tailored to specific needs of individuals are more persuasive and effective than messages not tailored to individual needs (Rains et al., 2019). Furthermore, BoG used its crisis response strategies to manage both its reputation and that of the banking industry as prior literature suggests that a financial crisis affects both the organizational and industry reputations due to its spillover effect (Jin et al., 2018). Specifically, justification, differentiation, shifting blame, and attacking the accuser strategies were deployed by BoG to manage its own organizational reputation, while good intention, corrective action, and minimization strategies were used for the banking industry reputation management. This finding is consistent with the crisis communication of meta-organizations (Frandsen & Johansen, 2018) and industry reputation (Winn et al., 2008) literature, which has suggested that a successful crisis response strategy should differentiate between organizational level and industry level of reputations and address each level and not just the organizational level. Hence, differentiating between the organizational and industry reputations and employing different but more comprehensive crisis response strategies to manage each reputation might have been an effective and successful approach by BoG.

Implications for Theory

This study extends crisis communication theorizing to the financial crisis context by proposing the FCC conceptual framework for better theorizing of financial crisis from a communication perspective. The FCC conceptual framework has two dimensions. The first dimension is CC, which contributes to our understanding that a financial crisis likely impacts many different stakeholders with diverse needs, making it more complex than other types of corporate crises to manage. This complex nature of a financial crisis suggests that a one-size-fits-all crisis response approach might not be effective in addressing all these diverse public (stakeholders) needs. Understanding all different stakeholders’ needs to tailor crisis response messages to each stakeholder’s needs might be an effective approach for managing the reputation of a financial institution facing a crisis. The second dimension is CRM, which contributes to our understanding that a financial crisis does not only impact the reputation of the organization responsible for the crisis but also impacts the reputations of other organizations within the financial industry including the overall financial industry reputation because of its spillover effects (Jin et al., 2018). This challenges our traditional understanding of reputation by helping to differentiate between corporate level and industry level of reputation and how to manage each level (Frandsen & Johansen, 2018). Thus, the CRM suggests the organization responsible for the financial crisis collaborates with other organizations within the industry to develop a more consistent and collective response strategy to manage its own reputation and that of the financial industry. This collective approach might be more effective than the individual approach in managing both organizational and industry reputational damages.

Implications for Practice

The study has several implications for practice. First, financial and business communication leaders could employ the FCC conceptual framework to guide them in planning and designing their crisis response strategies during crises. Second, the findings suggest that in a financial crisis situation, an organization deals with not only its own reputation but also the industry’s, which may require different crisis response strategies. For instance, defensive strategies such as justification, differentiation, shifting blame, and attacking the accuser might be appropriate and effective for managing the organizational reputation when the central bank is not responsible for the crisis. However, these defensive strategies might not be appropriate and effective for managing the organizational reputation when stakeholders perceive the central bank to be responsible for the factors leading to the crisis. Concerning the industry reputation, combining the defensive strategies (such as good intention and minimization) with the accommodative strategy (such as corrective action) might be appropriate and effective for the central bank to manage. Third, the findings suggest that there are many different stakeholders with different needs during a financial crisis and that a one-size-fits-all crisis response approach might not be effective in addressing all the diverse needs. Central banks should identify all different stakeholders affected by the financial crisis and understand their various different needs so that they can tailor their crisis response messages to these diverse needs. For instance, crisis response messages highlighting decisions taken to address the legitimacy and credibility of the entire banking industry might be appropriate for the professional stakeholders (i.e., bankers, directors, and shareholders). Crisis response messages highlighting the enforcement of the banking laws and proper accountability and transparency in using public funds might be appropriate for the government and taxpayer stakeholders. Also, crisis response messages assuring that no customer and staff of the collapsed banks would lose their monies and jobs might be appropriate for those stakeholders.

Limitations and Directions for Future Research

This study is not without limitations. First, because of the content analysis nature of this study, we could not examine how the central bank’s communication strategies influenced public perception about the organizational reputation to determine the effectiveness of the crisis response strategies. Future research could use surveys to understand the influence of the central bank’s communication strategies on public perceptions of organizational reputation including factors that could mediate or moderate this relationship. Furthermore, this study only used the proposed FCC conceptual framework as a benchmark to qualitatively assess whether the central bank’s crisis response strategies were effective in managing its own reputation and that of the banking industry. Future research could develop scales for the communicative complexity and collective reputation management dimensions of the proposed FCC conceptual framework and empirically test their validity and influence on organizational reputation during financial crises. Findings from such studies could help ascertain the usefulness of the FCC conceptual framework for financial and business communication leaders when designing communication strategies during financial crises.

Conclusion

The study’s findings demonstrate the usefulness of the FCC conceptual framework in guiding financial and business communication practitioners when planning and designing their crisis response strategies during financial crises. The study suggests that central banks should not use a one-size-fits-all crisis response approach but should rather identify all stakeholders with their unique needs and tailor the crisis response strategies to the diverse stakeholders’ needs during financial crises. Additionally, central banks should differentiate between organizational and industry levels of reputation and use their crisis responses to address each level of reputation. For example, defensive strategies might be effective in managing the central bank’s reputation when the regulator is not responsible for the crisis. On the other hand, using both defensive and accommodative strategies might be effective in managing the financial industry’s reputation during a crisis. Importantly, financial institutions should be aware of the best practices and recommendations for financial crisis management before a crisis happens.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.