Abstract

Abstract

Indian economy witnessed high inflow of capital for start-ups in current fiscal year through venture capital (VC) investment. From different Indian VC deals, it is evident that VC investors prefer to invest jointly. In other words, joint investment or co-investment or syndication is a common trend in Indian VC industry. VCs adopt this strategy to minimise their future uncertainties as a part of the control mechanism. In this study, an attempt is made to find out different determinants of this syndication strategy. The samples taken in this study are retrieved from Venture Intelligence database for the period 2005–2014. The data are analysed through linear regression and binomial logistic regression. Two empirical models have been developed. The derived models validate different control variables and deal with specific characteristics to comprehend the rationale of syndication mechanism. The findings of the study indicate that the past experience and the number of industry exposure of a VC in IT and ITES industry are the major predictors for a syndication decision. Subsequently, the precautionary investment attributes like number of investment round, stage funding, etc. draw the interest of potential co-investors in a syndicated deal. Syndication mechanism benefits the VC investors through sharing of risk of investment in a start-up and preparing them for a successful exit. Extant literature supports the results as Indian VC investors prefer to share the risk profile of a start-up business and adopt different risk diversion mechanisms to attract co-investors in the deal. Furthermore, the joint investment by investors drag more funding amount and also create more human capital for efficient management of the investment in VC-backed portfolio.

Introduction

In a venture capital (VC) deal, a contract is designed to minimise uncertainty that possibly will come up in future due to volatile business environment. Venture capitalists play an intermediary role between the source of fund and utilisation of fund and manage it to optimise the future value of fund at the utility end. A contract between a VC and an entrepreneur firm is designed to minimise agency cost and informal asymmetry, where the venture capitalist set various provisions in it to handle different unpredictable situations (Lerner, 1994b; Puri, & Zarutskie, 2011).

According to the study of Cumming (2007) and Cumming and Macintosh (2003), an optimal VC contract structure cannot be generalised across market of all the country as there exist huge difference in institutional features, legal structure, etc. in different countries. As Indian VC industry is very different from many developed country, the characteristics of VC contract are also quite different. Considering the highly unpredictable and uncertain business environment for a start-up business, venture capitalists prefer to diversify their risk of investment through including more investor in their prospective portfolio (Robinson & Sensoy, 2011; Sahlman, 1988). This phenomenon is known as ‘syndication’. In India, this concept is widely adopted in VC industry. Most of the Indian VC deals are found syndicated having more than one VC investor. According to Lerner (1994a), one of the main rationales of syndication decision is selection hypothesis of VC firm. Presence of more than one investor in a deal evaluates the entrepreneur firm more accurately. This could bring clarity for further stage of investment decision.

It is well understood that a large pool of resources could be gathered for investment with the cumulative experience of the investors through syndication (De Clercq, & Dimov, 2004; Deli, & Santhanakrishnan, 2010). This is the reason that syndication is an important aspect in a VC contract and support for higher return from an investment.

Our study focuses on which facets of VC deal leads to syndication decision in a deal. The analysis of this study covers two aspects of syndication practice. In first part, we have tried to find out the determinants of syndication decision. Through this, we have identified those parameters whose presence affects the probability of occurrence of syndication. Second part analyses those distinguishing features of a VC deal which can catch the attention of other VC investors.

By studying these, we can better find out different key variables that effect the syndication decision. In India majority of the deals go for syndication process through including other investors. Analysing the determinants of syndication decision could help to understand its impact on VC return in future research.

Prior Research and Hypothesis Development

Lerner (1994a) argues that syndication process adds value to the organisational performance, where the organisation gets the benefit of value certification. Previous studies on existence of syndication support the fact of valuation certification as they believe that more advantage could come up by sharing risk through investment in group (Cestone, Lerner, & White, 2007; Lerner, 1994a). As information asymmetry leads to uncertainty of firm value, Lockett and Wright (1999, 2001) argued that to handle such uncertainty in future value return, VC investors prefer for syndication of the deal. For them, it is a strategy to curtail the uncertain outcomes and sharing of risk.

In a deal with entrepreneur firm, VC uses syndication as a strategy. In their study, Barney, Busenitz, Fiet and Moesel (1996) explained that when VC invests in a firm at its early stage, the investment is majorly invested to make good and experienced management. Hellmann and Puri (2002) also argued that the VC firm made investment in human capital at the early stage of the firm by security professional management. To fulfil the requirement of human capital is a constraint for VC firms. So, they go for syndication to deal with these human capital constraints.

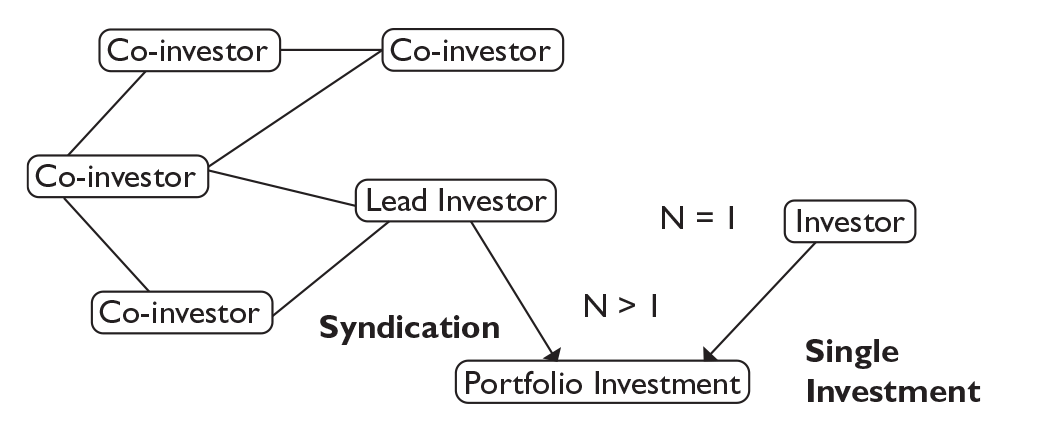

In our study, our sample of VC deals consists of 137 VC investments where 64 per cent VC deals were syndicated. In such deals there exists more than one link of investors with the investment firm. There exist two kinds of link in the structure: one is of portfolio company with each investors and another is among each investors. This could be due to large social network among them. It is evident that with larger network that exists for a VC firm, it is possible to drag more resources for investment in portfolio company. The number of investors involved in a VC deal represents the number of existing links. In other words, this clearly indicates presence of larger resources and more experienced human capital as shown in Figure 1.

Our article aims to find out those determinants which affect the pool of resources and establish several links in a single VC deal. Syndication is generally used by VC firms to increase their performance and reduce their risk of underperformance (De Clercq & Dimov, 2008; Jääskeläinen, Maula, & Seppa, 2006; Lerner, 1994a; Lockett & Wright, 2001). Baker (2000) explained that increase in number of round signifies the success of previous round of investment in the firm. From these above literature, we hypothesise the followings:

H1: Experienced VCs go for syndication strategy.

H2: Size of investment plays a significant role in syndication decision.

H3: Getting fund for higher number of round attract new VC investors in a deal.

Data and Methods

We have taken 139 number of VC deals having 337 rounds of investment between 2005 and 2014 in Indian firms that have received at least one round of financing, either from Indian or foreign investors. All the deals-related information is obtained from Venture Intelligence database. The data are extracted as it is available in the database and quantified the qualitative data through coding the facts.

It is found that out of 139 number of deals, 101 deals are syndicated having more than one number of investors. Only 25 per cent of the deals are standalone investment from which 5 per cent of the deals receive successive round of investment.

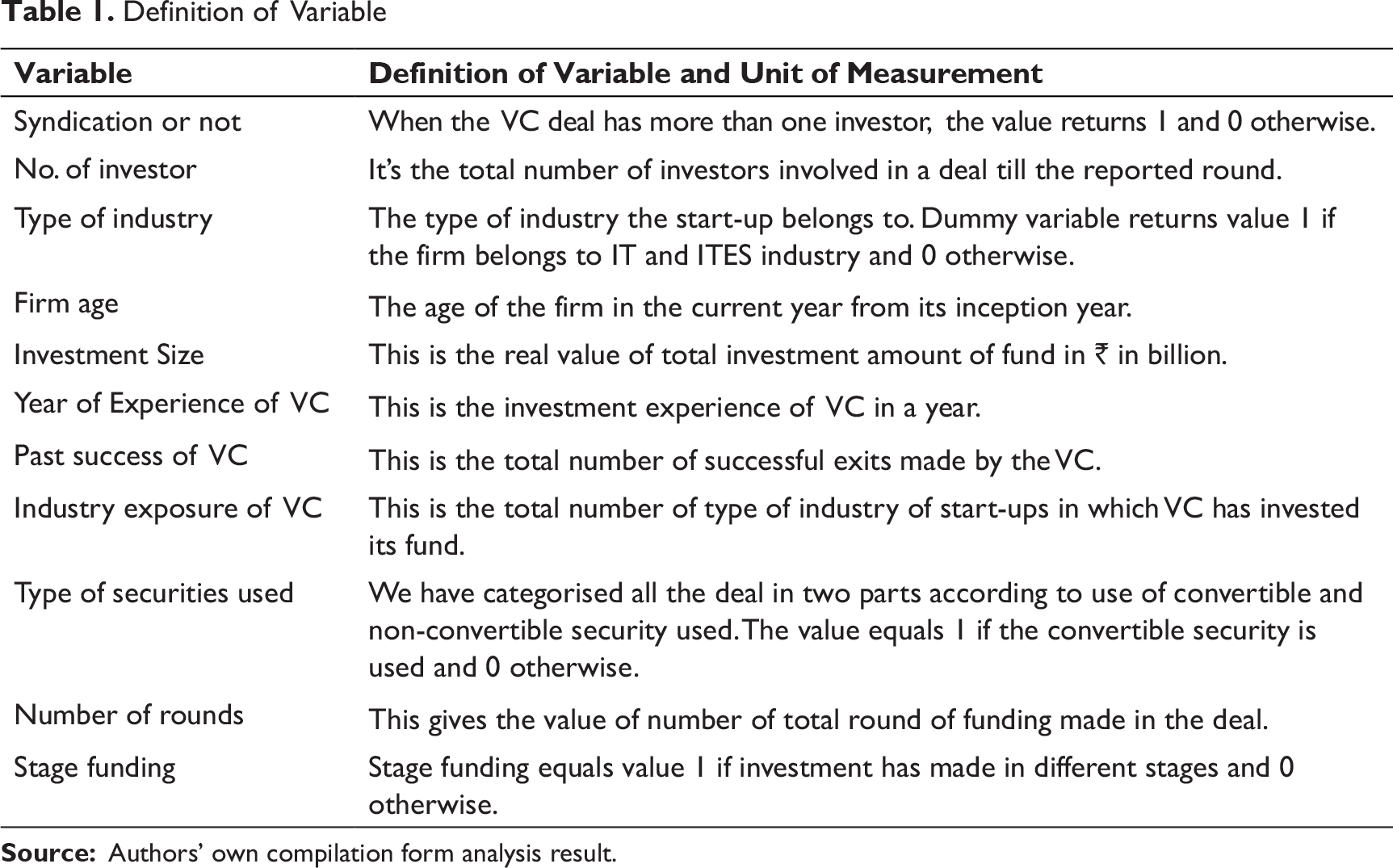

Definition of Variable

Analysis for Predictors of Syndication Decision

Descriptive Statistics

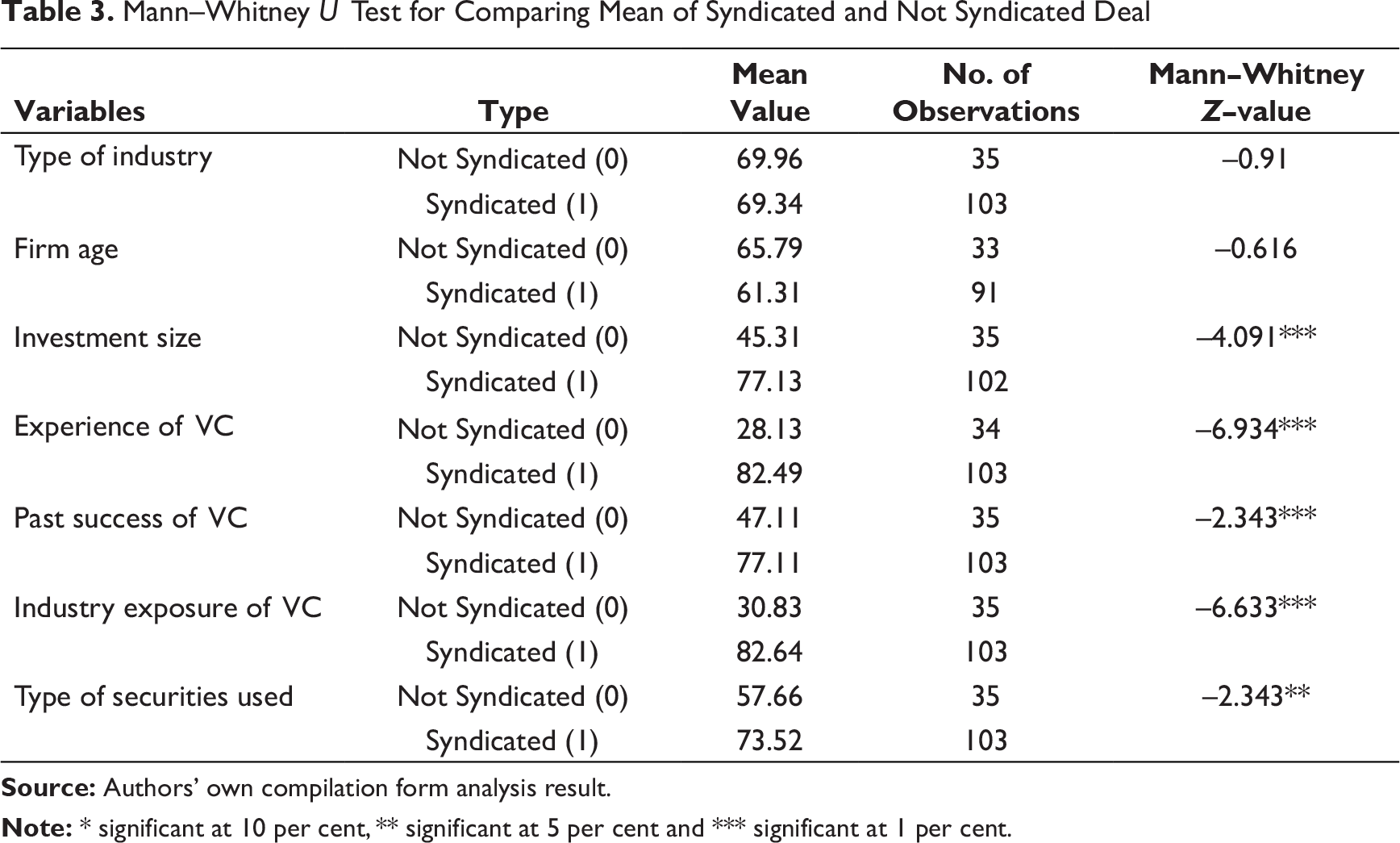

Mann–Whitney U Test for Comparing Mean of Syndicated and Not Syndicated Deal

In first model, we have taken industry type, age of the firm and size of investment as independent variable. In this case, only size of investment is coming out as a significant predictor with pseudo R2 = 17 per cent.

In second model, we have taken some VC characteristics like its past experience, past success and their number of industry exposure (it is cumulative if number of VC, N > 1) and type of security used for the deal. We found that except type of security, all these variables with size of investment are significant. The pseudo R2 value of this model is 0.58, which indicates that 58 per cent of variability could be explained through these four independent variables. The coefficient of past success of VC (–0.98), past experience of VC (0.27) and industry exposure of VC (0.29) explain that there is a significant relationship of these variables with VC’s syndication decision.

The coefficient of past success of VC (–0.98) indicates that more successful VCs are less likely to go for syndication strategy. Whereas indicators such as the investment size, past experience of VC and their industry exposure are significant. This support the finding of Casamatta and Haritchabalet (2007), where they explained that VC’s experience is the major indicator for forming of syndication decision.

Analysis for Number of Resource Pooling (Number of Investors)

The existence of information asymmetry problem between investor and entrepreneurial firm increases the risk profile of a portfolio investment. Hochberg, Ljungqvist & Lu (2007) pointed out that approximately one-third of VC-backed firms don’t survive after the first round of investment. The probability of survival is high if the number of round of investment increases. This might be due to resolve of aforesaid problem of information disclose (Admati, Anat & Pfleiderer, 1994). This information asymmetry problem could be resolved in due course of time. As the number of round increases, this information gap gets small and likelihood of syndication becomes high. The involvement of more than one investor involves more human capital and leads towards better management of the portfolio firm (Ferrary, 2010).

Binomial Logistic Regression, N(139)

Ordinary Least Square, N(139)

In second model, we have added three more variables such as past experience of VC, past success of VC and number of industry exposure of VC and found that investment size, past experience of VC and number of industry exposure of VC are significant variables. The R2 value of this model increased to 0.55 more than the first one (Table 5).

In next model, we have added some contract-specific variables like number of round of investment, stage funding or not and type of security used for investment in the deal with the previous variables. This model comes as a better fit compared to previous two models having R2 value 0.67. This model can explain 67 per cent variability of the dependent and independent relationship. The investment size, past success of VC, industry exposure of VC, number of round of investment and staged funding decision are the significant variables which affect the pooling of more number of investors. Through syndication, other investors invest with lead investor and uphold the development of the firm.

So the combination of finding of these entire model explains that adoption of various control mechanism in a VC contract by an experienced VC attract other investors to invest in the same portfolio in the next investment round (Dahiya & Ray, 2012). Indian VC deal witnessed involvement of multiple investors from the initial investment round. This may be due to involvement of experienced VC in the specific investment.

This proves our hypothesis that use of some control features drags more resources through involvement of more number of investors.

Discussion

VC investment processes and their contractual features are very confidential and complex matter. In India, many of its aspects are yet to be unturned. The deals information available in Venture Intelligence database reveal the fact that approximately 70 per cent of VC deals have multiple investors. We analyse the determinants that lead to syndication for the deal and involvement other interested co-investors for investment.

Unlike the previous study, different firm characteristics like age and type of industry of the firm are not found significant for syndication decision by the VC investor in this study. Rather it is the outcome from the know–how of experienced VC investors. We have measured this experience in three ways. First, the number of years of investment experience; second, the number of past success where they exit from the investment successfully and third, the number of industry exposure through which investment in different firms belongs to different industry. All this measures of experience are found significant in opting for group investment or co-investment decision.

Furthermore, the number of investors present in a syndicated deal is an important fact to understand the available resources, both in the form of financial and human capital. This creation of resource link not only depends on past experiences of VC investors but also on the control strategy adopted by the lead investor. Round of investment and stage funding decision are the major sign to have many resource link. As the number of round increases, the probability of success of investment becomes more explicit. This attracts other investors to put in their fund in that investment opportunity.

Syndication strategy is one of the control rights that is mentioned in the VC contract and VC can execute this option according to the need of situation. Again, other control rights like round investment and stage funding have a significant effect on its mechanism.

Conclusion and Scope for Future Research

From social network theory, Granovetter (1973) and Granovetter (1985) found that a formal contract is determined through the pre-existing social links. Such embeddedness makes this investment less risky. Furthermore, the reduction of uncertainty across time through syndication is supported by Admati et al. (1994). The situation at the time of investment is quite different after first round of investment and in subsequent rounds also. A more experienced and exposed venture capitalist can better understand such consequences.

The statistics of Indian VC deal clearly shows that most of the deal involve multiple investors in different stages, especially in case of early stage investment. Unlikely in other countries, older and more experienced VC investor go for syndication decision in India. Again, presence of more number of social link supports not only through financial inflow but also through involvement of more skilled human capital. No doubt an experienced VC has more social connections but a proper design of contract and use of different control rights can pool more financial resources for the portfolio firm and make the deal more attractive and successful.

Investors prefer to invest in stage in an uncertain business rather to put the entire fund at a time. They appraise the business over time and release next round of fund. The increase in number of round of investment indicates proper and efficient utilisation of earlier fund invested in previous rounds. This is the key attraction point which drags other investor to the particular investment.

The relation of size of investment with syndication process clearly signifies that syndication process not only drags more human capital but also enhances size of investment fund. The combination of these two resources could face the constraints of business operation of portfolio firm. But how far the presence of other control rights in a VC contract still affects on the deal flow is still a scope of future research in Indian VC industry context, as the clarity in this aspect is very stumpy. As network embeddedness of the firm influences its performance (Echols & Tsai, 2005), the statistical validation of this hypothesis in VC industry of India is yet to be established.