Abstract

This article attempts to analyse the issue of caste discrimination, with a special focus on the experience of business enterprises in the Guntur district of Andhra Pradesh. It tries to examine the discrimination faced by scheduled caste business owners (SCBOs) of the non-farm sector, especially of business enterprises in the sale market, based on a field study conducted in Guntur district. The study is based on a sample of 225 respondents, comprising 150 Scheduled Caste (SC) and 75 non-SC/Scheduled Tribe (ST) business owners. A structured questionnaire was followed for the interview. The objective of this article is to understand the nature and pattern of discrimination existing among business owners. In the present day, even though SCBOs are allowed in business enterprises, they still face economic discrimination in markets. The present study has found that there is an existence of discrimination in the sale market as about 61.7% of respondents reported that their caste background affects their sales and access to the common market. The immediate impact of discrimination is evident from the existing disparities in profits between SCBOs and other business owners (OBOs). If identity negatively affects profit expectations, the chance of survival in small business will be very low for the underprivileged group. This is why, this article seeks to examine whether caste background affects the profitability of businesses significantly or not?

Introduction

The economic characteristic of the caste system in India is the fixation of economic rights related to occupation, especially for each caste by birth, and continues through inheritance. The distribution of economic rights is unequal among caste groups, including those relating to work, property rights, wages and access to education. These occupations are not only fixed and unequally distributed but also maintain a hierarchy by treating a higher caste as superior and a lower caste as inferior (Ambedkar, 1936).

The immediate effect of the caste system can be seen in two ways; first, complete exclusion or denial of certain social groups, such as lower castes, by higher castes in hiring or sale and purchase of factors of production (land, capital assets, various services and inputs required in the production process, consumer goods and services like education, housing, health services). The complete exclusion is unrelated to productivity and other economic attributes. Second, selective inclusion but with differential treatment to excluded groups reflected in differential prices charged and received for input factors, consumer goods, price of labour such as wages, price of land or rent, interest on capital and rent on residential houses, as well as prices or fee charged by public institutions for services such as food items, water, electricity and other goods and services. Therefore, selective inclusion with differential treatment against the low castes is discrimination, which refers to any disparity in treatment between individuals based on their group membership rather than their characteristics (Thorat & Newman 2010).

Caste and Economic Discrimination

Economic discrimination can be understood through theories of discrimination. There are mainly three theories of economics of discrimination. First, Becker’s (1957) taste-based theory; according to this theory, an individual has a taste for discrimination from which they derive utility or satisfaction. The taste for discrimination comes from prejudices that a group holds against the other group. The employer has a taste for discrimination in hiring and treating the employees; likewise, employees have a taste for discrimination against employees belonging to another group. In the consumer market, consumers have a taste for discrimination against the members of another group. The consumer’s preferences in buying goods and services ‘depends not only on prices, speed of service and reliability but also on sex, race, religion, and personality of the sales personnel’. To operate their taste for discrimination, they are willing to forgo their benefits and individuals try to show their taste for discrimination by knowing their individual characteristics. But in Arrow (1972) belief-based theory of discrimination, the employers do not know about the employee’s productivity and they tend to have some beliefs and prejudice against some groups, which result in discrimination. According to identity theory by Akerlof and Rachel (2010), identity is made up of social categories and their norms. Social categories describe who individuals are, whereas norms suggest how they ought to act, interact with or regard others. These norms are discriminatory and show that an individual in the absence of others in some group enjoys a gain. The identity theory maintains that social categories and their norms would decide how someone in those social categories would behave. It also perpetuates the distinction between ‘us’ and ‘them’. The division of ‘us and them’ based on a norm, which is called oppositional identity with an expression of differences, results in discrimination. The taste-based, belief-based and identity theories of discrimination show that discrimination results from prejudice, which produces stereotypical false beliefs by the dominant group about a subordinate group.

In the Indian context, Ambedkar emphasised that caste is an important identity that has resulted in two forms of discrimination. The first form of discrimination is the complete exclusion of certain social groups, such as lower castes by higher castes, in exchange for factors of production, businesses and services. The second form of discrimination is the inclusion of certain social groups with differential treatment. Therefore, discrimination refers to any disparity in treatment between individuals based on their group membership rather than their characteristics.

Review of Literature

There have been attempts to show systematic evidence, which can be classified into two categories, evidence based on secondary data sources and field surveys in India. There is empirical evidence of discrimination based on secondary data sources in the non-farm market, which includes understanding the social composition of business enterprises based on certain characteristics. Thorat and Sadana (2010) found that in rural India, household enterprises account for 71% of total enterprises. The Scheduled Caste (SC) and Scheduled Tribe (ST) households operate a relatively higher proportion of household enterprises as compared to Other Backward Classes (OBCs). About 67% of total enterprises owned by the SCs were own account enterprises (OAEs), compared to 61% for the STs, 60% for the OBCs, and 49% for others. In turn, the SC and the ST owned a smaller share of establishments (hired worker-based enterprises) as compared to the OBCs and higher caste. The SCs own about 32% of hired worker enterprises, compared to 51% for higher caste. A similar pattern is observed in urban India as well. The percentage share of hired worker-based enterprises was 33% for SC, 38% for ST, 40% for OBC, and 51% for higher caste. Iyer et al. (2013) showed that there exist inter-caste differences in ownership of enterprises.

Harriss-White et al. (2014), based on an analysis at three regional levels, found that there is a variance in the participation of Dalits in business activities. Their participation in business activity is low in the northern and southern belts, while it is high in the ‘central’ belt. There are differences in the owning of registered manufacturing micro, small and medium enterprises (MSMEs), where ‘SCs and STs are under-represented compared to their population shares, OBCs are equal to their population share, and “Others” and Hindu upper castes (non-SC-ST-OBC Hindus) are over-represented’ (Coad & Tamvada, 2012). Deshpande and Smriti (2016) assessed caste-based discrimination in small household businesses. They found that 55% of the disparities in incomes can be because of discrimination, and possessing more assets can be the reason for the income gap between SC–ST and non-SC/ST.

Field-based surveys have explored the nature and pattern of discrimination in business enterprises; for instance, Thorat et al. (2010) analysed the pattern of discrimination in rural markets in both market and non-market spheres; 73% of SC sellers reported discrimination in the sale and purchase of vegetables and milk due to the notion of the impure status of low caste untouchables, particularly in consumer goods. Jodhka (2010) analysed that in the sale market, more than one-third, about 38% of the businesses, were located in areas in their caste locations. Dalit enterprises were predominantly engaged in small grocery shops and they were mostly located in Dalit-dominated residential areas. A very low percentage, about 6%, operated from completely non-Dalit areas, such as marketplaces and other higher-caste residential locations. Some of the Dalits in his study felt that they have experienced discrimination through prejudices. The locally dominant communities who are traditionally engaged in the businesses ‘don’t like Dalits into a business’ and ‘they hate us’. Some others reported that they are regarded as outsiders or odd actors. In the sale market, if their caste name is known or revealed, it decreases the consumers and affects their business negatively.

Thorat et al. (2013) found that SCs need to pay higher prices for the inputs. Supply is not on time, and sellers will supply the inputs with bad quality. Related to the sale of output, most of the SCs (57%) are unable to sell on credit due to the feeling of higher caste customers that their quality of goods is inferior and the quantity is inadequate, hence affecting the sale of goods. Dignity/status problems and the preferences of the people are reasons for the denial of purchasing from SC shops. Regarding the location of shops, about 60% of SCs and STs have reported that their shops are situated in their locality. Only 20% of STs and 43% of SCs reported that their shops were located in a common place.

Thorat and Prashant (2014) extended the study to the nature and forms of discrimination, as well as the notions behind discriminatory and irrational behaviour of higher castes persons towards SCs in the form where in the case of Orissa, discrimination in the purchase of milk by SCs was relatively high than the sale of milk. This is because of the prevalence of cultural taboos that the people in Orissa believe that if anyone sells milk to an SC customer, their cattle would die or would stop giving milk. Further, SCs have reported instances of discrimination in the inputs market ranging from delayed supply of inputs to a complete refusal to supply the same to them because of their caste. SC is also denied access to formal and informal agencies of credit, while access to formal credit agencies is denied more on the grounds of lack of security rather than caste prejudices in the formal markets.

Prakash (2015) analysed the experiences of Dalit entrepreneurs in six states of middle India. In markets, for instance, in sale markets, a Dalit entrepreneur from Jaipur said that due to his low caste origin, nobody from the Baniya traders would buy their products. Some case studies of Dalit food entrepreneurs in Pune and Jaipur informed that the promotion of their caste by the upper caste had reduced their sales. In the credit market, nearly 80% applied for credit, of which 65% were rejected. More than 85% applied for credit from government agencies, over 50% were rejected. Therefore, these entrepreneurs obtained credit from informal sources with high interests and mortgaged their assets. About 30% are obtaining credit from their caste persons at 2% on average, and about 87.7% obtain credit from outside their caste at a 10–12% interest rate.

From the review of literature, we can summarise two things: that there exist disparities in the ownership of enterprises where the share of SCs is under-represented. Though there are some studies analysing the nature of discrimination in input where it is found that SC business owners are paying high prices for the inputs and in the sale market, the discrimination in terms of denial of purchases from SC shops. The extent of discrimination in which the consequences of discrimination on cost, revenues and profits has to be analysed. It is very important to understand discrimination quantitatively as the main objective of business is to earn profit, which depends on the cost and revenues of the business. These are economic outcomes of a business, which need to be addressed because it has two implications. First, low-profit margins will affect their competitiveness with high-caste businesses. Second, most of the scheduled caste business owners (SCBO) are economically weak and to operate the business, they depend on borrowings from money lenders at high interest rates. If they earn low profits, not sufficient to pay the interest rates, it is highly probable that they will exit from the business. If identity adversely affects profit expectations, the chance of survival in small business will be very low for the underprivileged group. This is why, this article seeks to examine whether caste background affects the profitability of businesses significantly or not? This is to note that the caste mechanism purely works on the basis of the factors determined by birth. A business owner coming from the SC may be denied fair access to the factors of production due to the stereotypes determined by social identity. Therefore, it is necessary to address this issue in order to ensure that working of the competitive market is not adversely affected due to the existence of caste-based discrimination.

Data and Methodology

The analysis is based on both secondary and primary data. In secondary data analysis, Economic Census Data (2013) is used, which provides data on both agricultural and non-agricultural business establishments in the economy. It provides all the information about the number of business enterprises, number of employed by all the sectors, activity and social group wise. It also provides data of business enterprises at state-level, district-level, mandal/tahsil-level and village-level. This data is used to understand the participation of SCBO in the businesses.

Primary data are collected to understand the nature and pattern of discrimination faced by SC business owners in the markets. The size of the SC population and business enterprises owned by SCs is drawn from the Census of India and the Economic Census.

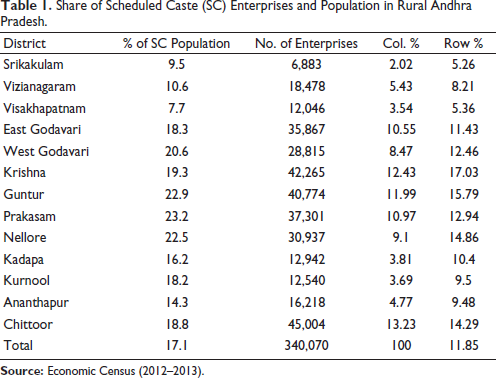

The Andhra Pradesh state has been selected because it is one of the top five states which own the highest share of enterprises in India, such as Uttar Pradesh (11.43%), Maharashtra (10.49%), West Bengal (10.10%), Tamil Nadu (8.60%) and Andhra Pradesh (7.25%). Guntur district has been selected based on two indicators; first, on the basis of SC population, and second, on the basis of SC-owned enterprises. The total average SC population in India is 16.6% and the average SC population of Andhra Pradesh in rural areas is 19.2%. Guntur district has been taken for the analysis as it has 22.9% of the SC population in rural areas followed by Krishna (19.3%) and Chittor (18.8%).

Second, there are five districts, namely Chittoor, Krishna, Guntur, East Godavari and Nellore, which comprise more than 50% of the enterprises. Among these, the share is high in three districts, namely Chitoor (13.25%), Krishna (12.43%) and Guntur (12.0%). Guntur district has been selected for the field survey (see Table 1).

Share of Scheduled Caste (SC) Enterprises and Population in Rural Andhra Pradesh.

Based on these two considerations, the share of SC population and the share of enterprises owned by SC. The samples are taken from the large villages of Kollipara and Mangalagiri mandals (Mandal/Block) in Guntur district of Andhra Pradesh. These two mandals are selected because of the highest number of SC-owned business enterprises, such as tailoring, retail trade (grocery shops) and eateries (hotels) (see Table 2).

Top 10 Mandals with the Highest Scheduled Caste (SC)-owned Enterprises in Four Activities.

All the villages of Kollipara and Mangalagiri are selected according to their highest share of business owners from SC and non-SC/ST. For tailoring, the villages of Kollipara mandal are taken, where about 28.0% from village Thumuluru and other villages such as Danthaluru (12%), Vallabhapuram (12%), Munnaggi (14%), Chivuluru (14%), Kollipara (6%) and Athota (4%). For retail trade, the villages of Kollipara mandal are taken, where about 30.0% from the village of Munnagiand and other villages such as Athota (18%), Vallabhapuram (12%), Thumuluru (12%), Danthaluru (12%), Chivuluru (10%) and Kollipara (6%). For eateries (hotels), the villages of Kollipara and Mangalagiri mandals are taken, such as Chemudupadu, Makkivari pet and Ratnalacheruvu about 18% and other villages such as Baptistpet (12%), Bommuvaripalem (12%), Munnagi (10%), Kollipara (6%) and Gandalam pet (6%).

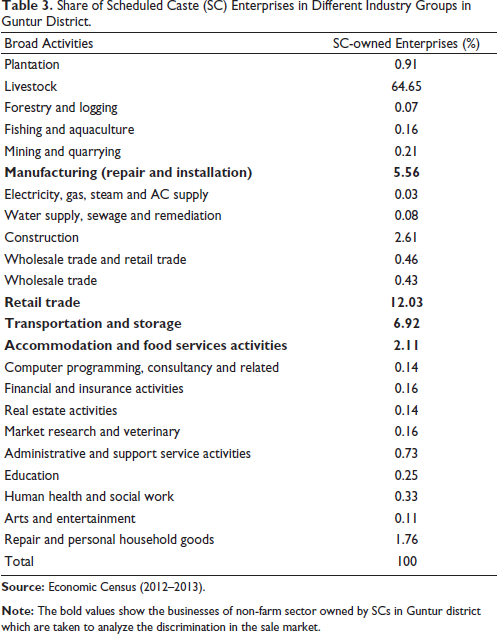

To analyse the discrimination in the sale market, three types of own account micro businesses, such as tailoring, retail trade (grocery shops) and eateries (hotels), which are predominately owned by SCs, were taken for the study. These businesses are selected based on the Economic Census (2013). It shows that in the Guntur district, these businesses such as manufacturing, retail trade, transportation and food services, have a comparatively higher share of SC. For instance, SC owns a business of 11.5% in manufacturing, 12.6% in retail trade, 22.8% in transportation and 9.9% in accommodation and food services (see Table 3).

Share of Scheduled Caste (SC) Enterprises in Different Industry Groups in Guntur District.

A purposive sample method is used, and 225 samples comprising SCBO (150) and other business owners (OBOs) (75) are taken for the study. OBO includes other than SC/ST business persons. Each business type consists of 75 respondents, of which, SCBO is about 66.7 and OBO is about 33.3%.

From the field-based studies, it is found that due to caste background and the concept of purity and pollution associated with the SCs, they face discrimination in the market. Therefore, as the present study focuses on analysing the discrimination faced by SCBO, more samples of SCBO were taken to get more information related to discrimination, so that findings can be more reliable. In the field survey, snowballing technique is used to know the social group of the business owners.

A purposive sampling technique has been used to select the respondents to understand their experiences related to discrimination in different markets such as input and sale markets.

The ‘audit method’ has been used to measure discrimination directly to identify the circumstances under which discrimination occurs. There are three distinct methods for capturing the discrimination, namely the telephonic audit, in-person or face-to-face audit and recording of experiences through case studies. The present study was conducted through face-to-face interviews of SCBO who had actually experienced the discrimination. The focus is to capture the nature of discrimination and unequal outcomes in different markets related to business enterprises.

The structured questionnaire was used in the interviews which included open-ended questions in order to capture the experience of discrimination in input and sale markets. The question revolved around the impact of discrimination on the business, the reason for the discrimination in the input and output market if they are facing it, the reason for not getting space in the market, and the localities dominated by the higher caste and the reason for the low number of higher caste customers. The close-ended questions were asked to understand the relationship among the variables. The focus is to map the process which results in the discrimination. To understand the extent of discrimination, quantitative questions were included, such as information on the quantity of inputs purchased, actual prices paid for the purchase of inputs, and prices received from the customers. The observation method is used to understand the interactions and behaviour between discriminated persons and discriminating groups in the markets.

This is to note that inputs in this study imply raw material and consumption goods. For instance, there are some inputs which are raw materials such as threads, buttons, scissors and tape required for tailoring. In eatery businesses, there are some inputs which are raw materials, such as rice, wheat, idly flour, popper seeds, green gram, oil, gas and paper plates. All the business owners in eateries are using second-quality inputs such as rice, wheat, idly flour, popper seeds, green gram, oil and other inputs of first quality. The business owners purchase these inputs at respective prices in the wholesale market. As the same product is being purchased from the same market, the quality of the input is the same for every business owner. There are some inputs which are packed consumption goods in retail trade (grocery shops) such as packets of biscuits, sweet items, food ingredients, eggs, mixture packets, dry items, curry items, chilli, shampoo, tobacco items, toothpaste, toothbrush, beverages and milk items brought and sold in their respective business localities. There is no scope for difference in the quality of these inputs also.

The term price is used for the prices of the input and output. So, the prices of the input will figure in the cost of the business owners, while the price of the output will be used to calculate their profit. In the sale market, outputs are referred to as consumption goods, such as packets of biscuits, sweet items, food ingredients, eggs, mixture packets, dry items, curry items, chilli, shampoo, tobacco items, toothpaste, toothbrush, beverages and milk items in the retail business, whereas in the tailoring and eatery businesses, these outputs are made from the inputs. As these are retail traders, the input and output remain the same, and the profit is earned due to the difference in the purchase and sell prices. The outputs in the tailoring business are shirts and trousers, and idly, dosa and chapathi are the outputs in eateries (hotels).

To analyse profits, two variables, such as total income received from the sale of products and services and total cost incurred from the purchase of products and inputs, are collected. The total cost was calculated by taking all the inputs which business owners purchase and the prices they have paid per month. Similarly, revenues are calculated by taking into account the prices received of each input and quantities of products which the business owners sell per month. Profits are calculated per month by taking the difference between total revenue and total cost per month. For the data analysis, the arithmetic average is used to analyse the disparities in the profits. Percentages of business owners are calculated in relation to discriminatory aspects between social groups.

Findings of the Present Study

The analysis is based on three types of businesses, namely tailoring, retail trade and eateries. Even though these three types of business are different in nature, they are similar in terms of investment, and also, the products are of the same kind in the respective business groups. All the business owners, irrespective of caste, buy their inputs from the same wholesale markets located in the Tenali or Kollipara mandal. In the wholesale markets, there are two communities such as the ‘Komatis or Baniyas’ and ‘Reddys’ dominant in running the wholesale markets.

Understanding the concepts of economic discrimination, based on the second concept which is selective inclusion but with differential treatment, the concepts related to discrimination in business enterprises can be analysed in different markets such as input and sale markets. In the input market, it is measured when the low caste pays higher prices for the purchases and receives lower prices of their products and goods as compared to market prices which results in the disparities in the cost of business. Discrimination in the sale of goods and services is a denial of the sale of outputs and products by higher caste groups to lower caste groups and a refusal to buy from the low caste sellers which results in disparities in the profits of business.

Tailoring

There are some inputs which are raw materials, such as threads, buttons, scissors and tape, required for tailoring. All the business owners are using the same quality of inputs in this business. They purchase these inputs every 10 days. They buy the minimum required quantity of inputs sufficient for 10 days. The SCBO sells at lower prices as compared to OBO. For instance, in tailoring, on average, per one pair of men’s clothes (shirt and trousers), the SCBO charges ₹300–350 and the OBO charges on average ₹350–450. They reduce their prices with the expectation that more consumers will be attracted and demand for their products will increase so that they can earn more profits.

Retail Trade

There are some products which are consumption goods in retail trade (grocery shops), such as packets of biscuits, sweet items, food ingredients, eggs, mixture packets, dry items, curry items, chilli, shampoo, tobacco items, toothpaste, toothbrush, beverages and milk items, brought and sold in their respective business localities. All the business owners are selling the same quality of the product in this business. They buy the minimum required quantity of inputs sufficient for 10 days. It is important to note that these businesses operated by SCBO and OBO are the same kind in terms of investment and prices which they sell at maximum retail price (MRP) in retail trade only.

Eateries (Hotels)

There are some inputs which are raw materials, such as rice, wheat, idly flour, popper seeds, green gram, oil, gas and paper plates. All the business owners in eateries are using second-quality inputs such as rice, wheat, idly flour, popper seeds, green gram, oil and other inputs of first quality. They buy the minimum required quantity of inputs sufficient for 10 days. It is reported that all the business owners in eateries are using the same second-quality inputs such as rice, wheat, idly flour, popper seeds, green gram and oil. Second quality implies that these inputs are made in the second reaping in the first cropping or sowing. They sell the items such as idly, dosa and chapathi per plate. Plate is referred to the quantity of items which is different for each item. For each item, on average, SCBO charges a lower price than OBC. For instance, SCBO charges ₹10 per plate for idly and OBO charges ₹15–20 per plate. Similarly, SCBO charges ₹5–10 for dosa and OBO charges ₹10–20 per plate; SCBO charges ₹10 for chapathi per plate and OBO charges ₹15 per plate on average. The SCBO charges lower than OBC with an expectation to attract and improve demand for their products and hence would earn more profits.

Based on the responses, it is observed that all the business owners, irrespective of caste, buy all the inputs from the same wholesale sellers in the wholesale market. For example, there are some products which are consumption goods in retail trade (grocery shops) such as packets of biscuits, sweet items, food ingredients, eggs, mixture packets, dry items, curry items, chilli, shampoo, tobacco items, toothpaste, toothbrush, beverages and milk items, bought and sold in their respective business localities. The quality of these packed products does not differ due to the fact that they are supplied from the same company. Similarly, both groups of businesses purchase eatery items from the same wholesaler. Given that the wholesaler is the same for both SCBO and OBC, the quality of these products also remains the same.

Disparities in Profits

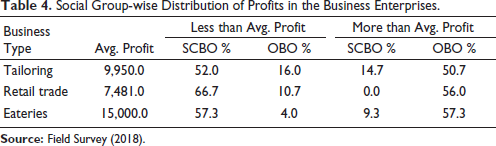

The average profits in each business type were calculated to understand the disparities in the profits. The average profits in tailoring, retail trade and eatery businesses are ₹9,950.0, ₹7,481.0 and ₹15,000.0. Based on the average profits, we have divided two groups, high-earning and low-earning groups. The high-earning group earns more than the average profit and the low-earning group earns less than the average profit. The data show that there are huge disparities in the profits between SCBO and OBO in the tailoring business. When we compare across social groups, a high percentage of SCBO, about 52.0%, are earning below the average profit of ₹9,950.0 but the share of OBO in this group is very low, about 16.0%. On the other extreme, the share of OBO earning more than the average profit is about 50.7% but SCBO comprises a very low per cent, about 14.7%. Therefore, the data reveal a high concentration of SCBO in low profit groups and vice-versa (see Table 4).

Social Group-wise Distribution of Profits in the Business Enterprises.

Similarly, in the retail trade business, a high percentage of SCBO, about 66.7%, are earning below the average profit of ₹7,481.0, but the share of OBO is very low, about 10.7%. Therefore, most of the SCBOs belong to a low-earning group. The share of OBO earning more than the average profit is about 56.0%, but no SCBO is earning more than the average profit. Therefore, most of the OBOs belong to the high-earning group (see Table 4). Likewise, in eatery business, a high percentage of SCBO, about 57.3%, are earning below the average profit of ₹15000.0, but the share of OBO is very low, about 4.0%. The share of OBO earning more than the average profit is about 57.3%, but SCBO comprises a very low per cent, about 9.3%. Therefore, most of the OBOs belong to the high-earning group and most of the SCBOs belong to the low-earning group in eateries also (see Table 4).

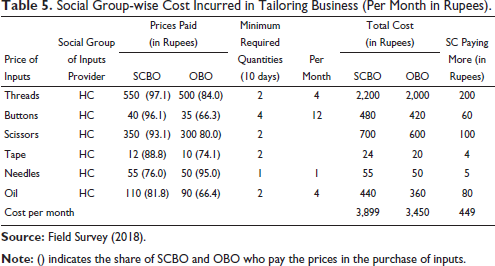

From the above analysis, we found that most of the SCBOs belong to the low-earning group and most of the OBOs belong to the high-earning group. There are mainly two factors; first, it is clear from the input market that SCBOs are paying more prices and due to this, the cost of SCBO is higher than the OBO. For instance, in tailoring, on average, about 88.8% of SCBOs are paying more prices than OBOs, which increases the cost of purchase. For the inputs, such as threads, buttons, scissors and tape also, the SCBOs are paying more prices for each input. They are paying a higher price for each input, that is, thread boxes, buttons, scissors, tape, needles and oil. The high price of input results in a higher cost for SCBO than OBO. At an aggregate level, the total cost of the tailoring business per month for SCBO costs about ₹3899, whereas it costs about ₹3,450 for OBO. Thus, SCBOs are paying more of ₹449 (see Table 5).

Social Group-wise Cost Incurred in Tailoring Business (Per Month in Rupees).

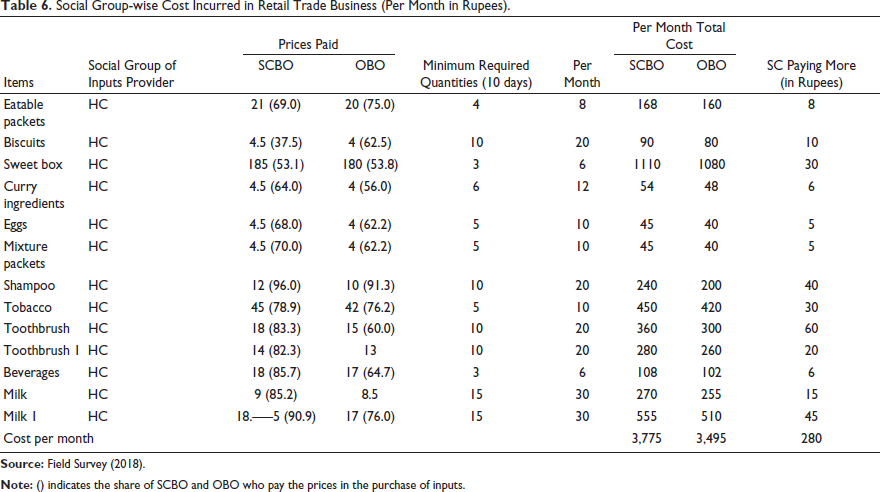

Similarly, in retail trade, on average, 74.2% of the SCBO is paying more prices for each input. The total cost of the retail trade business per month for SCBO is about ₹3,775, whereas it costs about ₹3,495 for OBO. Thus, it is obvious that SCBOs are paying more by ₹280 due to which the cost of SCBO is higher than the OBO (see Table 6).

Social Group-wise Cost Incurred in Retail Trade Business (Per Month in Rupees).

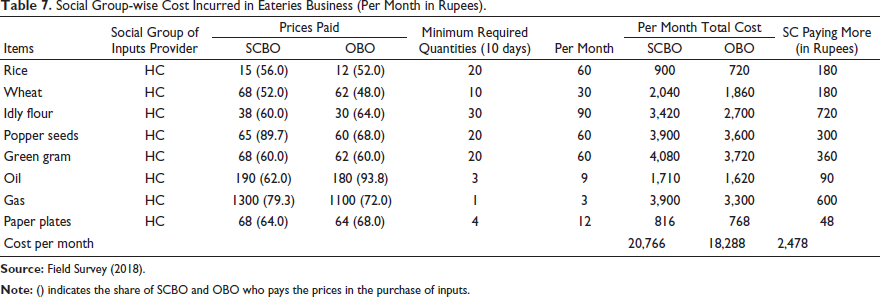

In eateries also, almost 65.3% of respondents among the SCBO are paying more prices for each input. The total cost of the eatery business per month for SCBO costs about ₹20,766, whereas it costs about ₹18,288 for OBO, which resulted in a gap of ₹2,478 in the total cost between SCBO and OBO (see Table 7).

Social Group-wise Cost Incurred in Eateries Business (Per Month in Rupees).

The operational mechanism of caste discrimination in the input market can be understood from the responses of the business owners which revealed that caste works as a mechanism for discrimination with SCBO which results in low profit prospects. These business owners are SCBO and OBO. The wholesaler and OBO most often belong to the same caste background, which creates a favourable condition for the OBO. As the business owners regularly purchase their inputs from the same wholesale sellers, it is very easy to recognise the caste of business owners. The discussion of the wholesale sellers and OBO while packing the inputs revolves around their business operation. These business owners share about their business losses and debt problems with money lenders who belong to a higher caste. However, the wholesalers do not interact with SCBO due to caste-based stereotypes. So, these business owners’ wholesale sellers do not share complete information about the prices of inputs with SCBO. The SCBO also do not bargain due to their weak economic condition. If the SCBO asked about their variation in prices, they say that they have brought with the same prices and even we are not taking any profits. Since all the inputs are non-durable goods, they do not have fixed market prices, and these prices keep on varying every day. Importantly, there is no provision of displaying the prices in the wholesale markets; therefore, information asymmetry exists in the input market.

Second, from the sale market, the response reveals that caste is the main reason for the unequal profit despite businesses being the same. A very low percentage of higher caste persons buy goods from the shops owned by SCBO, compared with high caste shop owners. Out of the total customers of SCBO, 17.9% are from non-SC/ST and about 9.3% of customers from other than higher caste, while the high percentage of buyers from all castes purchase from OBO business owners, about 82.1%. Alternatively, the percentage of own caste’s customers is high among the SCBO owners, 95.3%, compared to 4.7% for OBO. Thus, SCBOs are highly dependent on their own caste customers (see Table 8).

Distribution of Consumers in the Business Enterprises.

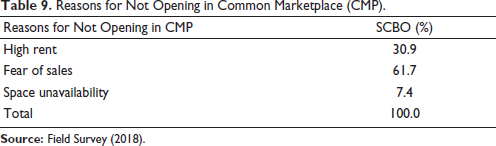

One of the important reasons for the denial by the higher caste is the location of SCBO. It is observed that about 94.1% of SC businesses are located in residing places, whereas 81.5% of OBO businesses are located in common marketplaces. So, the advantage of location also attracts more customers for OBO compared to their SCBO counterparts. On being asked about the reason for not opening shops in the common marketplace, 61.7% of SCBO respondents reported that they fear about sales due to their caste background. A notable number of them answered ‘how can higher caste buy our products and services’.

Further, the long distance of NSCBO hamlets from SCBO, as reported by 26.7% of SCBO, also works as a barrier in selling goods and services to the OBO locality. Thus, the caste-based segregation results in an unfavourable location for the SCBO. The responses reveal that the concept of purity and pollution based on caste practice in the village operates as an obstacle in the businesses of SC respondents (see Table 9).

Reasons for Not Opening in Common Marketplace (CMP).

There are three reasons for the ability of the OBO to sell in all caste spaces, to access credit or other material inputs at lower costs in the businesses. First, Damodaran (2008) argued that in India, certain castes and communities have traditionally been business communities, and entrepreneurs from these communities start with clear natural advantages; in that, they possess insider knowledge, know-how and strong business networks passed down through generations. Second, Thorat and Sadana (2010) argued that the nature of the caste system allowed the other castes in owning property rights and owning business or undertaking production activities. Thus, the advantages of it still continue and its positive impact can be seen in the ownership of caste spaces, to access credit or other material inputs at lower costs and private enterprises by other castes. Third, Shah et al. (2006) argue that the stigma of untouchability and the notion of the impure status of low-caste untouchables have traditionally advantaged the other caste persons to sell in all caste spaces. Prakash (2015) reported in some case studies, Dalit food entrepreneurs shared that the publicity of their caste by the upper caste had reduced their sales and in turn, it has increased the upper caste sales.

Thus, the caste mechanism affects these businesses, both in the input and output markets. The caste background creates a virtual segregation in the market. The suppliers of the factors of the production belong to the high caste background. So, they remain biased towards their own caste businesses, which results in unequal bargaining power among the different caste groups.

In the output market, the location and background of the customers play an important role. The villages are segregated on the caste lines. The low-caste businesses do not get space in the main market. So, they locate their businesses in their own hamlets in the village. Thus, these businesses get customers from their own hamlet comprising a low caste population who lack sufficient purchasing. Further, customers belonging to the high caste generally avoid purchasing from these businesses due to the distance and the existing caste-based untouchability. In such circumstances, these businesses are left with the choice of selling their product at low prices to attract customers, which results in low profit.

Conclusion and Policy Suggestions

The purpose of the present article is to explore the caste-based discrimination experienced by the SCBO in the market transactions. The root cause of discrimination lies in the norms that govern the economic organisation of the caste system. These norms of the caste system have many consequences. One of the consequences of the caste system is the unfavourable inclusion but with differential treatment to low caste (SCs) in different market and non-market exchanges. It is also found that such kind of differential treatment to SCs in the different markets of business enterprises (Thorat, 2013). Therefore, it is important to understand the nature and pattern of discrimination faced by SCBOs in the different markets of business enterprises. The study is based on the experiences of 225 business owners in the sale market from Guntur district in Andhra Pradesh. To capture the nature of discrimination in sale market, interviews based on both quantitative and qualitative tools have been conducted.

It is evident from the results that the SCBOs are facing discrimination in the sale markets due to their caste background. Discrimination can be seen in three ways. First, in terms of the high price paid by SCBO, which increases the cost for them. Second, most of the SCBOs are located in their own locality, that is, they are not operating in the main common marketplaces due to financial constraints. Jodhka (2010) also made a similar observation that location is an important barrier for SCBO. The immediate impact of this kind of discrimination is that it reduces sales, resulting in low revenues. The consequence of discrimination is evident from the huge disparity in profits between SCBO and OBO. Third, even though the state- or centrally-sponsored schemes are available for supporting the business owners financially, a high share of the SCBO is not able to avail these schemes due to their caste background.

These results indicate that caste-based discrimination still persists but in a modified form. This discrimination results in low earnings and hence a high tendency of poverty among SCBO. In order to address it, there is a need to develop affirmative action in order to ensure fair participation of SC in self-employment. One of the ways may be in the form of fixed quotas in proportion of the population of the discriminated groups in state-sponsored schemes. Any policy of reservation for the non-farm sector will have to address the issue of discrimination in various markets and should come up with anti-discriminatory measures covering all markets. Policies are also needed to meet the problems, such as access to infrastructure, space and other amenities, and to improve the sale of goods and commodities.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.