Abstract

Abstract

This study examined institutions and economic growth in sub-Saharan Africa from 1986 to 2013. Panel data were used for this analysis. Panel pooled ordinary least squares and dynamic generalized method of moment (GMM) models were employed in the estimation of the relationship between institutions and economic growth. This study found that institution has negative impact on economic growth in sub-Saharan Africa as it is positive and statistically significant in both pooled and dynamic GMM. This human capital and money supply also have positive impact on economic growth. Physical capital and interest rates, on the other hand, has negative impact on economic growth in sub-Saharan Africa.

Introduction

Several reforms and policies have been adopted in sub-Saharan Africa to tackle the economic stagnancy in the region but no meaningful development has been taking place compared to other regions of the world. In the literature, a lot of factors have been identified as the sources of economic growth, such as, surplus labor to capital investment and technological change, foreign aid, foreign direct investment, investment in human capital, natural resources, increasing returns from investment in new ideas, and research and development (Sarwar, Siddiqi, & Butt, 2013). The positive or negative impacts of the above-listed traditional sources of economic growth have been well documented in the literature. In the real sense, evidence has shown that the above factors were not totally lacked in sub-Saharan Africa and other regions that are struggling with economic progress. It was this situations that motivated economists all over the world to think that there might be other framework which allow these factors to produce the desired growth in the economy. Recently, researchers have focused on the institutional factors such as the role of political freedom, political instabilityw, voice, and accountability as an important factor in economic growth and development. Institutions as a subject of study are gaining increasing interest among social science researchers around the world. No economic reform could be undertaken without sound institutions capable of implementing it. In recent time, most of the international organizations have included the institutional dimension in their reforms recommendation frameworks. Due to the importance of institutions according to Forum (2008) the World Bank have recently published an interesting report on “Better Governance for Development in the Middle East and North Africa: Enhancing Inclusiveness and Accountability,” while the IMF has chosen “Institutions and Growth in the MENA Region” for its biannual High Level. According to North (1990), it is impossible for growth and development to take place without institutions. Economic progress, maturity, and the growth of markets require an institutional framework that allows transactions to take place in an orderly manner and in which agents know that the decisions they take and the contracts they make will be protected by law, and enforced. Savers, investors, consumers, entrepreneurs, workers, and risk-takers of all kinds need a framework of rules, if rational, optimizing decisions are to be made. They also need some guarantee of economic stability and certainty, which can be provided only by good governance and sound economic policy making. Institutions can reduce the costs of economic activities in the economy. Institutions could lower the transaction costs by providing common legal frameworks (e.g., contracts and contract enforcement, commercial norms and rules), and they can encourage trust by providing policing and justice systems for the adherence to common laws and regulations. When these costs are removed borrowing and lending become easier between banks and the economic agents. The implication of this, in the economy, is that investment will increase which in turn will lead to economic growth. Gone through the literature a lot of studies have examined the relationship between economic growth and institutions in developed countries and various conclusions have been made. But in sub-Saharan Africa not many studies have been carried out which might likely due to lack of access to institutional data unlike developed countries. Therefore, this study is very important as it will shed more light on weather institutions is a factor to be reckoned with while talking about economic growth in sub-Saharan Africa.

Literature Review

Aron (2000) noted in his study that Africa’s disappointing economic performance, the East Asian financial crisis, and the weak record of the former Soviet Union shifted attention on the role of institutions in determining a country’s economic growth. He critically reviews the literature that tries to link quantitative measures of institutions, such as civil liberties and property rights, with growth of gross domestic product (GDP) across countries and over time. An important distinction is made between indicators that measure the performance or quality of institutions and those that measure political and social characteristics and political instability. The evidence suggests a link between the quality of institutions and investment and growth, but the evidence is by no means robust.

Khalil, Ellaboudy, and Denzau (2007) examined the impact of structural, legal, and economic institutions on economic growth in the OECD countries. The results show that their assumptions on the impact of institutions are significantly correct. More than 80 percent of the variation in GDP per capita in the OECD countries can be explained by both economic and institutional determinants. They conclude that suitable legal and economic environment can explain changes of economic growth. Countries can develop faster by enforcing strong property rights, fostering an independent judiciary, attacking corruption, allowing press freedom, and protecting political rights and civil liberties. Economic freedom and enforcement of strong property rights define a healthy environment for economic activity.

Chang (2010) examined the currently dominant discourse on institutions and economic development. He argued that the discourse suffers from a number of theoretical problems—its neglect of the causality running from development to institutions, its inability to see the impossibility of a free market, and its belief that the freest market and the strongest protection of private property rights are best for economic development. Also, he pointed out that the supposed evidence showing the superiority of “liberalized” institutions relies too much on cross-section econometric studies, which suffer from defective concepts, flawed measurements and heterogeneous samples. Finally, he argued that the currently dominant discourse on institutions and development has a poor understanding of changes in institutions themselves, which often makes it take unduly optimistic or pessimistic positions about the feasibility of institutional reform.

Barro (1996) evaluated with panel data the role of social characteristics in determining political regimes using proportions of the population by religion, rates of urbanization, colonial heritage, ethnic differences, income inequality, and social indicators such as life expectancy, actually forecasts which countries are likely to experience declines and improvements in future democracy. None of the above variables is significant (except an indicator for countries in the Organization of Petroleum-Exporting Countries) may be related to Barro’s neglect of the duration of democratic and other regimes, which Clague et al. (1997) emphasized. Several of these variables also have been shown to be relevant in Solow-type growth equations, although with doubtful robustness (Temple, 1999). While Claque et al. conducted a similar study in 1997 and found that the characteristics and stability of political regimes (type and duration) appear to be important determinants of the quality of economic institutions. He highlighted the trade-off between credibility and executive flexibility as a possible explanation for why some democratic regimes do not deliver the goods, while some longer-lived autocratic regimes do. Using annual data to account for frequent changes of regime, the paper found that short-lived democracies are least likely to ensure adequate property rights, while longer term democracies offer better protection for property and contract rights than any other type of regime of any duration.

Knack and Keefer (1997) examined informal institutions using measures of trust and civic norms drawn from the World Values Surveys (Inglehart, 1994). The authors found that in reduced-form growth regressions, singly and together, trust, and civic norms are positively associated with growth and claim a causal role. Specification tests for the robustness of these results found that they are fairly insensitive to changes in specification, exclusions of influential observations, and the use of additional regressors. In the Solow regressions (not reported), these variables lose significance or become insignificant. This could suggest that the investment relationship where both variables, especially civil norms, prove to be important fully captures their (indirect) impact on growth. However, as with other studies surveyed here, the endogeneity of these ordinal indexes and their measurement error raise doubts about a robust causal role for these measures. This probably is considerable measurement error here: some groups are over sampled (higher-status groups), which the authors try to correct, but the five survey questions comprising the civic performance measure may not have been answered truthfully, while the question regarding trust is ambiguous.

Knack and Keefer (1995) used two institutional indexes in growth regressions capturing security of contract and property rights, the International Country Risk Quide (ICRG) index from 1982 and the earlier and hence less endogenous Business Environmental Risk Intelligence (BERI) index (from 1972). They reported some results without statistics to support them. It appears that both institutional indexes are significant in investment regressions during 1974–1989 and 1960–1989, confirming an indirect effect on growth through factor accumulation. There also appears to be weak evidence for a direct efficiency effect on growth. But Lane and Tornell (1996) included two commonly omitted variables, that is, natural resource abundance and institutions in an attempt to explain why some resource-rich countries have lower growth rates than resource-poor countries. They reported reduced form growth and investment regressions, and their results focused on the effects of weak property rights (reflected in estimates of the ICRG risk indicator) and an increase in manufacturing concentration. The coexistence of weak institutions and powerful industrial groups affects growth and investment negatively and significantly.

Methodology

This study adopted the modified Cobb-Douglass production function assuming constant return to scale. This approach has been adopted by several authors including Mankiw, Romer, and Weil (1992), Knight, Loayza, and Villaneura (1992, 1993), and Ghura and Hadjimichael (1996).

Consider the following Cobb-Douglas production function:

where Y represents the output (GDP), A denotes technology progress, K represents physical capital, H stands for human capital, finally L is the used labor force, subscript i indicate cross-sectional units observed for dated periods and the subscript t indicates time. After transforming equation (1) into the intensive form, it becomes:

By taking logarithm of both sides and differentiating equation (2)

To incorporate financial development and institutions into Equation (3), A is decomposed into two separately observable parts. This is due to the fact that increase in money supply encourages technological development which tends to increase the productive sector’s efficiency or increase the productivity of investment and also efficient institutions. Therefore, technology can be decomposed into money supply and institutions.

By substituting Equation (4) into Equation (3), it becomes:

where ‘ms’ represents money supply and ‘ins’ represents institution.

Apart from the money supply and institutional factor, evidence from previous studies has shown that many other factors are significant determinants of real growth. Therefore, inflation and interest rate are included in the model as they also serve as control variables.

We therefore include the error term and the control variables. The equation to be estimated becomes:

Measurement of Variables and Data Source

This study used secondary data while panel data were used for the empirical analysis. These data are for sub-Saharan African countries and covered the period of 16 years (1986–2013). This study made use of the following variables; real GDP—this is measured by GDP calculated by dividing the GDP by the consumer price index. Physical capital (k)—this is measured by gross capital formation. Human capital stock (h)—is measured by primary and secondary enrolments, rule of law, is used as institutional variable—measured by extent to which agents have confidence in and abide by the rules of society, and in particular the quality of contract enforcement, property rights, the policy, and the courts, as well as the likelihood of crime and violence. Inflation is measured by consumer price (annual %). Money supply is measured by Money and quasi money (m2) as % of GDP. Interest rate is measured by Real interest rate. The data were obtained from the World Bank Development Indicator and Worldwide Governance Indicator (WGI). Specifically, data on economic growth, physical capital, human capital, inflation, and interest rate were obtained from the World Bank Development Indicator, while data on institutional variable were obtained from the WGI. The selected sub-Saharan Africa countries included in this study are Benin, Botswana, Burkina Faso, Cameroun, Cape verde, Central Africa Republic, Chad, Congo, Cote d’ivore, Democratic of Congo, Gabon, Gambia, Ghana, Guinea-Bissau, Kenya, Lesotho, Mozambique, Malawi, Mali, Namibia, Niger, Nigeria, Rwanda, Senegal, Swaziland, Sierra Leone, South Africa, Togo, Uganda, and Zambia. These countries were selected based on the availability of data.

Empirical Results

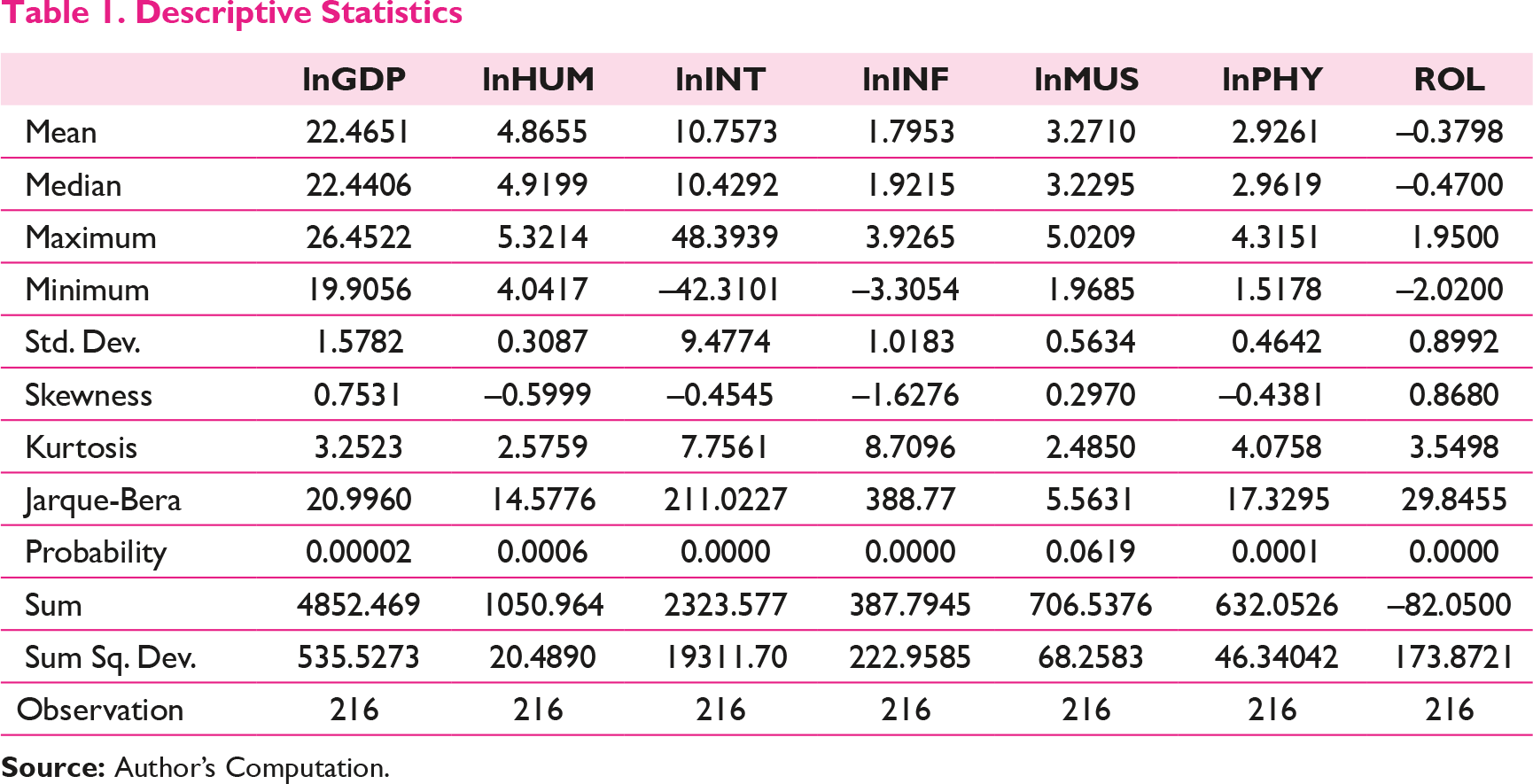

We begin the analysis of the relationship between institutions and economic growth in sub-Saharan Africa with descriptive analysis. The report of the descriptive statistics of the variables from 1986 to 2013 is reported in Table 1.

Descriptive Statistics

The descriptive statistics shows that all the series shows a high level of consistencies as all the mean and median fall within the maximum and minimum values of these series. The descriptive statistics also reveal that the growth rate of GDP is high compare to other variables as the average growth rate is 22.4 percent. Considering the standard deviation (SD) which measures the level of variation or degree of dispersion of the variables from their mean reveals that the actual deviation of the data from their means are very small as all the SDs are very low. This also shows that human capital is the most stable variable compare to other variables. The most volatile variable is the interest rates (9.47 percent). The Jarque-Bera, which is used to test whether the series is normally distributed, shows that the series are not normally distributed apart from money supply because the reported probability which shows that a Jarque-Bera statistic exceeds (in absolute value) the observed value under the null hypothesis is lower than 0.05 and 0.01. Finally, variables like GDP, interest rate, inflation, physical capital, and rule of law are leptokurtic (peaked) relative to the normal as kurtosis of this series exceeds three. However, human capital and money supply are not as their kurtoses are below three.

Correlation

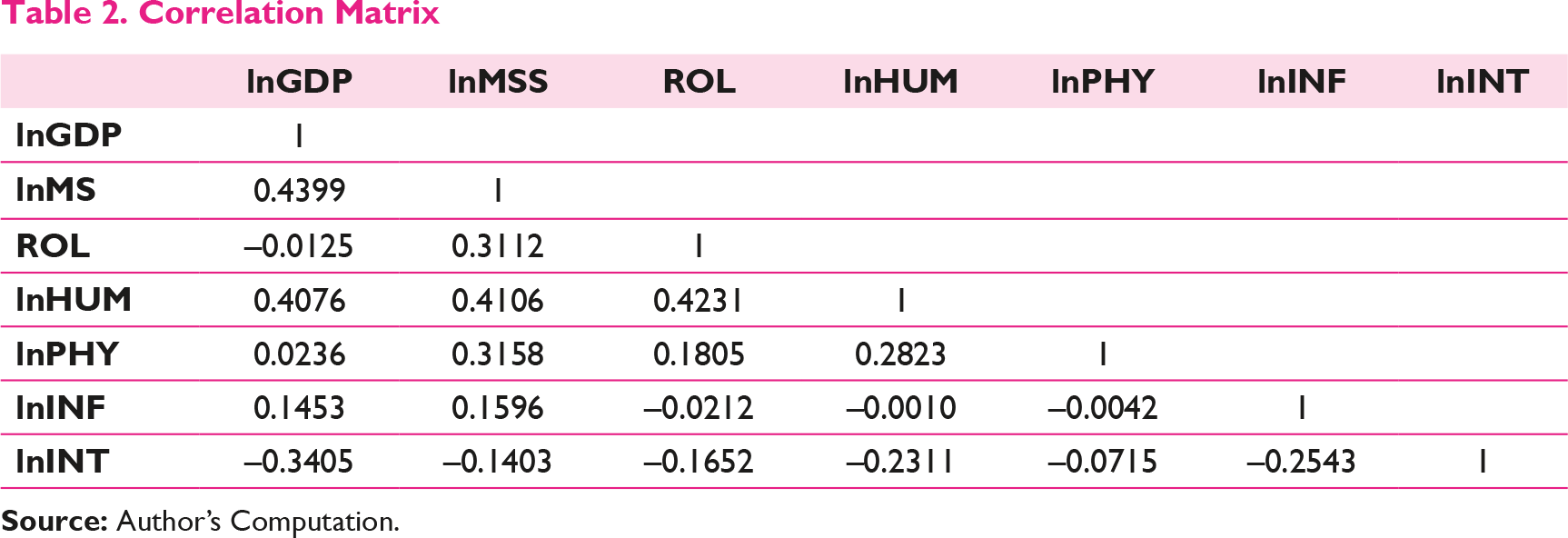

To examine the possible degree of association among the variables, we obtained the correlation matrix of the dependent and independent variables. Table 2 reports the sample correlation matrix of the variables employed in the study. The correlation table gives a preliminary idea of the direction of correlation between the selected variables. In general, the results in Table 2 show that in terms of magnitude, the correlation coefficient is generally high, while some variables have positive correlation, others are negative.

Correlation Matrix

From Table 2, money supply, human capital, physical capital, and inflation are positively correlated with economic growth in sub-Saharan Africa. This means that these variables move in the same direction with economic growth. Institution variable (ROL) has negative correlation with economic growth. This is implying that institution is inversely correlated with economic growth. Interest rate is negatively correlated with economic growth. This result is quite consistent with a priori expectation. High rate of interest discourages borrowing and lending and the implication of this is that the level of investment will be low which in turn could lead to low-economic growth.

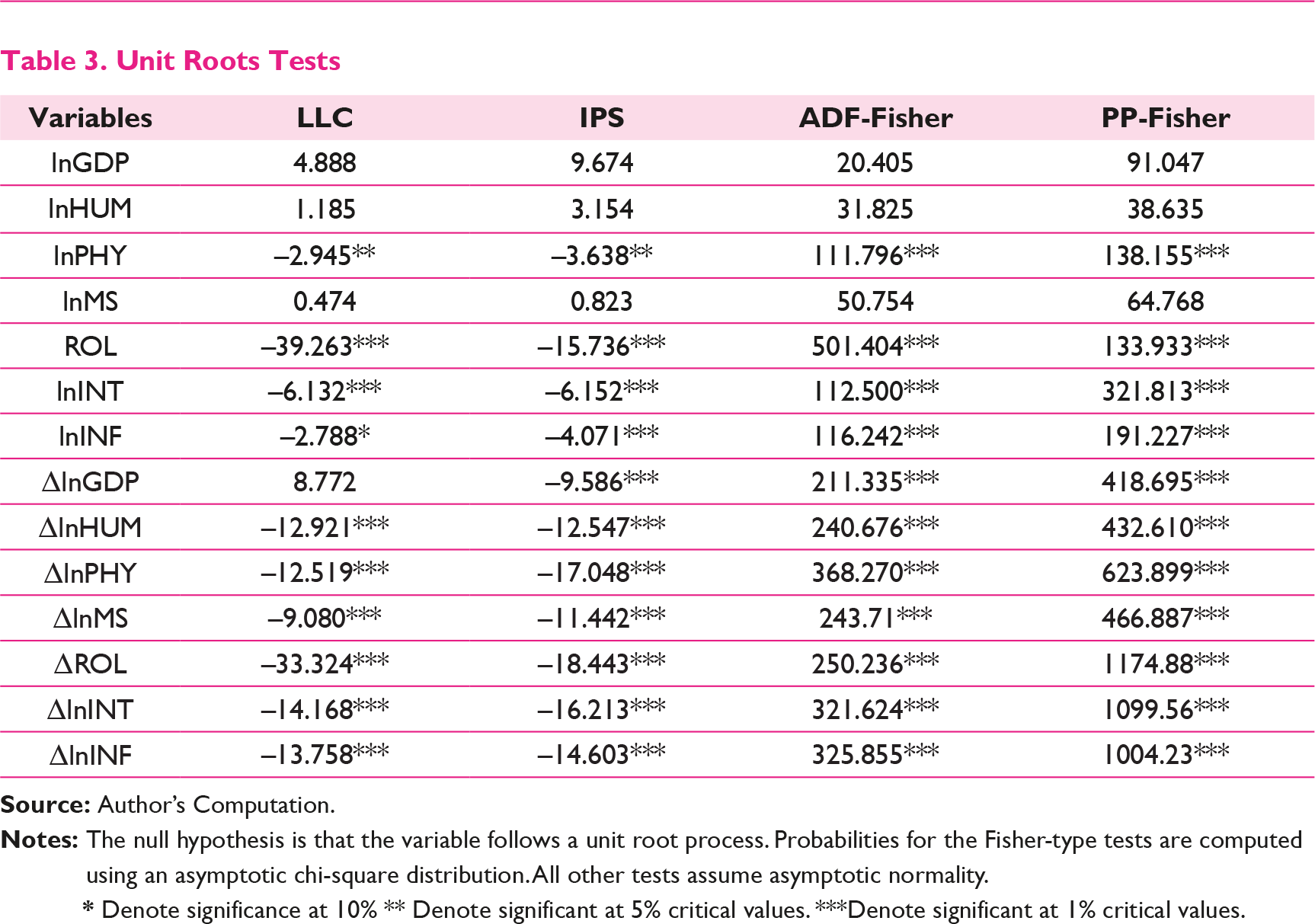

If non-stationarity is not accounted for in the estimation process, it may lead to spurious regression with serious negative consequences for public policy. Due to this, we preformed unit root test based on following panel unit root tests: the LLC (Levin, Lin, & Chu, 2002), the IPS (Im, Pesaran, & Shin, 2003), and the ADF- and PP-Fisher (Maddala & Wu, 1999). The results of the unit root test are presented in Table 3.

The results of unit root tests show that not all the variables are stationary at levels and it also shows that not all the variables are integrated of I(1).

In order to determine the effects of the institutions on economic growth in sub-Saharan Africa, two functional forms of estimation techniques were adopted: the pooled ordinary least squares (OLS) and dynamic generalized moment method (GMM) estimation.

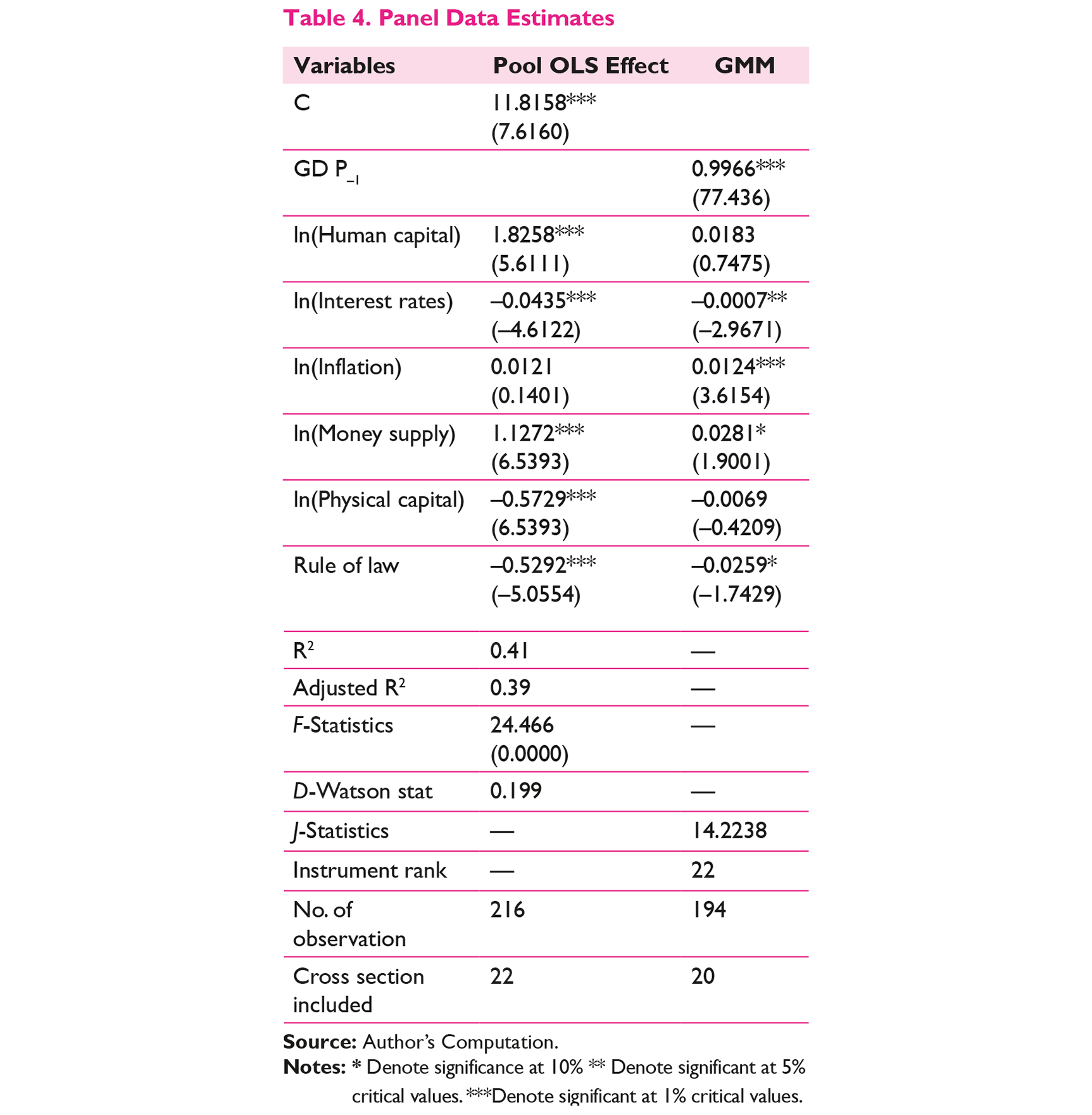

The results of pooled OLS and dynamic GMM estimation are presented in Table 4.

Unit Roots Tests

Denote significance at 10%

Denote significant at 5% critical values.

Denote significant at 1% critical values.

Panel Data Estimates

Denote significance at 10%

Denote significant at 5% critical values.

Denote significant at 1% critical values.

Empirical results of the pooled OLS model show that human capital and money supply are positive and significant at 1 percent significance level while interest rates, physical capital, and rule of law are negative and statistically significant. The positive and significant of human capital shows that human capital is a major factor that to reckon with as growth is concern in sub-Saharan Africa. The positive impact of human capital on growth in sub-Saharan Africa might be due to large labor force. It could also be due to the role of human capital in improving the quality of life and ensuring social and economic progress and also helping the developing country to absorb modern technology and to develop the capacity for self-sustaining growth and development. The positive and significant of money supply shows that money supply positively impacted economic growth during the study period in sub-Saharan Africa. When there is an increase in supply of money in economy, it will result in decrease in interest rates thereby increasing the level of investment. In this way, when extra money is spread in the society the consumers feel richer and will spend more. Industries acknowledge enhancing by ordering more raw materials and increase their production. When the business flourish, the demand of labor and capital goods will be increased. Stock market prices increase and firms issue more equity and debt (Ihsan & Anjum, 2013).

Interest rate on the other hand is negative and statistically significant at 1 percent. This is implying that interest rates has negative impact on economic growth in sub-Saharan. This negative impact of interest rate on economic growth in sub-Saharan Africa might be due to high interest rates as this result shows that 1 percent increase in interest rates will reduce the economic growth by 4.35 percent. When interest is high it will discourage borrowing which will affect the volume of investment and low level of investment will lead to slower economic growth. Physical capital is negative and statistically significant at 1 percent. This implying there is inverse relationship between physical capital and economic growth in sub-Saharan Africa. This negative impact of physical capital might be caused by lack of technological innovation in sub-Saharan Africa. Evidence has shown that sub-Saharan Africa is labor intensive compared to other regions. This is confirmed by positive impact of human capital on economic growth. The negative impact of physical capital on economic growth could also be as result of low-capital accumulation in the region.

Rule of law which is used as measure of institutions is negative and statistically significant at 1 percent. This showed that the rule of law is not well entrenched in the region and this is associated with low economic growth. This result also indicates that the judicial system in sub-Saharan Africa is weak and the property rights are not receiving adequate attention. By implication, it leads to low level of investment as both the local and international investors are discouraged as they do not have confidence to invest heavily in the economy. In addition to this, it leads to increase in the cost and inefficiency through the ineffectiveness and unpredictability of the judiciary. Because going to the court is time consuming and leads to increase in the cost of transactions, the volume of investments get reduced.

Also from the pooled OLS results, R2 and adjusted R2 are 0.41 and 0.39, respectively. The F-statistics which test for the overall significance of the model is relatively high and provides a good fit for the estimated model as their probability is significant at 1 percent. The Durbin-Watson statistics is generally satisfactory indicating non-existence of autocorrelation problem in the model.

The dynamic GMM results in Table 4 show that the lagged GDP has positive and statistically significant impact on the GDP in the current year at p < 0.01. The implication of this is that 1 percent increase in the economic growth in the previous year will lead to 99 percent unit increase in the economic growth of the current period. Human capital under dynamic GMM is positive but statistically insignificant. Interest rate is negative and statistically significant at 5 percent. Inflation is positive and statistically significant at 1 percent contrary to theoretical inverse relationship. Though, recently evidence has shown that inflation has threshold level when it will have negative effect on economic growth (Lee & Wong, 2005). The positive impact of inflation could be as a result of discipline on the part of both government and monetary body to ensure that there is no too much money in circulation and able to successfully control inflation and consumer price index. Physical capital under dynamic GMM is positive and statistically insignificant. Rule of law is negative and statistically significant at 10 percent. This is consistent with the results of pooled OLS.

The negative impact of institutions on economic growth of sub-Saharan Africa could be linked to poor economic performance of the region as no economic reforms and policies will pass the test of time without institutions. Goldsmith (1998) stated that policies cannot be more effective than the institutions that underlie them as institutions helps to determine what policies to be chosen and how they are executed. He further stated that where institutions are weak or ineffective, policy is likely to be the same, which is the true reflection of sub-Saharan African countries. The institutional framework which allows economic progress, maturity, the growth of the market, and making transactions taking place in an orderly manner and in which agents know that the decisions they take and the contracts they make will be protected by law, and enforced are completely lacking in sub-Saharan Africa.

According to North (1990), savers, investors, consumers, entrepreneurs, workers, and risk-takers of all kinds need an institutional framework of rules on which decisions are to be made. They also need some guarantee of economic stability and certainty, which can be provided only by good governance and sound economic policy making. Rodrik (2000, 2008) and Rodrik and Subramanian (2008) highlighted property rights and legally binding contracts, regulatory institutions, institutions for macroeconomic stability, social insurance institutions and institutions of conflict management as at least five main types of market-supporting institutions that are necessary, if not sufficient, conditions for rapid economic progress which according to him are lacked in sub-Saharan Africa. Rodrik (2000) stated that a clearly defined system of property rights, a regulatory apparatus curbing the worst forms of fraud, anti-competitive behavior and moral hazard, a moderately cohesive society exhibiting trust and social cooperation, social and political institutions that mitigate risk and manage social conflict, the rule of law and clean government are institutional arrangements that are conspicuously absent in poor countries. When these are missing in the economy, the economy becomes a graveyard for every policies introduced.

The negative effect of institutions on economic growth is also evident in the area of cost of transaction in sub-Saharan Africa. By implication high cost of transaction leads to low investment which in turn hamper economic growth. Lack of institutions increases the transaction costs due to the lack of common legal frameworks (e.g., contracts and contract enforcement, commercial norms and rules). It also discourages trust due to the absence of policing and justice systems for the adherence to common laws and regulations. The existence of these costs makes borrowing and lending difficult between banks and the economic agents. The implication of this, in the economy, is that investment will reduce which in turn will lower to economic growth.

Conclusion

The aim of this study is to broaden the empirical literature on the relationship between institutions and economic growth by investigating the relationship among these two variables in 30 sub-Saharan Africa. Toward achieving this, pooled OLS and dynamic GMM were employed to investigate the possible relationship between economic growth and financial development. The empirical findings of this study show that an institution has negative impact on economic growth in sub-Saharan African. Inflation, human capital, and money supply are all have positive impact on economic growth in sub-Saharan Africa. Physical capital and interest have negative impact on economic growth.