Abstract

Abstract

Corporate Social Responsibility (CSR) has received increased attention in the recent past as a means for sustainable development. CSR has largely been viewed as a voluntary exercise. However, the Companies Act, 2013 has made it mandatory for a certain category of companies to spend 2 percent of their average net profit in the past 3 years on CSR activities. If a company fails to spend the mandated amount on CSR activities, it is required to explain the reasons for the same in the Board’s report. India thereby became the first and the only country in the world to have mandatory CSR spending. The Act also prescribes the activities that would be eligible for this purpose.

The year 2014–2015 was the first year of operations for these provisions. The article aims to critically review the requirements of the Companies Act, 2013 in this regard and assess the implementation of CSR spending requirements in the maiden year of operations.

Mahatma Gandhi with his social approach to all human problems desired that business and industry should be conducted in the interest of the community, and businessmen should consider themselves servants of society. According to him, only when a man looks upon himself as a servant of the society, his earnings can be good and his venture can be constructive. Businessmen should thus earn and spend for the sake of society. They should run their business for the benefit of the society as trustees of the society. This is the basis of what is known as the Trusteeship Theory of business. Businessmen should conduct the affairs of business as trustees entrusted with the task of managing their business to serve the common interests of society. The Trusteeship Theory is further supported by the Stakeholder Theory promulgated by R. Edward Freeman (2010). The Stakeholder Theory argues that besides shareholders there are other stakeholders and that the business has an obligation to meet their expectations as well. Shareholders are but one of a number of stakeholder groups. Like customers, suppliers, employees, and local communities, shareholders have a stake in and are affected by firm’s success or failure (Heath & Norman, 2004).

In line with the Trusteeship Theory and Stakeholder Theory, the concept of Corporate Social Responsibility (CSR) has evolved and received increased attention in the recent years. From shareholders’ wealth maximization, the corporate focus has shifted to meeting the stakeholders’ expectations including the society at large. The companies are realizing that they must engage with their stakeholders for achieving sustainable growth. To illustrate, the corporate governance policy of ITC Limited states:

Since large corporations employ vast quantum of societal resources, ITC believes that the governance process should ensure that these resources are utilised in a manner that meets stakeholders’ aspirations and societal expectations. This belief is reflected in the Company’s deep commitment to contribute to the “triple bottom line,” namely the conservation and development of the nation’s economic, social and environmental capital.1

Retrieved December 10, 2015, from

CSR in this sense appears to be a voluntary initiative by the socially conscious companies. United Nations Industrial Developmental Organization (UNIDO) states that

Corporate Social Responsibility is a management concept whereby companies integrate social and environmental concerns in their business operations and interactions with their stakeholders. CSR is generally understood as being the way through which a company achieves a balance of economic, environmental and social imperatives while at the same time addressing the expectations of shareholders and stakeholders.2

What is CSR. Retrieved December 10, 2015, from http://www.unido.org/what-we-do/advancing-economic-competitiveness/competitive-trade-capacities-and-corporate-responsibility/csr/o72054.html

There is a realization that every firm for the purpose of production of goods or rendering of services uses the resources of the society which represents the opportunity cost of those resources to the society. This may be referred to as Marginal Social Cost (MSC). Through value addition, the firm contributes by way of benefits to the society. This may be referred to as Marginal Social Benefit (MSB). The society will allow a firm to operate only up to the point where MSC = MSB. When MSC starts exceeding MSB, society will put brakes on such activities through law or other regulatory measures. Further, there is an increasing belief that people who have a good environment, education, and opportunity make better employees, customers, and neighbors for business than those who are poor, ignorant, and oppressed. A responsible management has to, therefore, ensure that the business subserves various groups effectively and efficiently. These days, it is not enough for a company to merely be profitable; it also needs to demonstrate good corporate citizenship through environmental awareness, ethical behavior, and sound corporate governance practices. Thus, it will be in the interest of the companies to assume social responsibility.

As a voluntary exercise, the companies are free to decide their CSR policy, the type of projects and programs they would like to implement, and the amount of money that they would like to spend toward CSR activities. However, the Companies Act, 2013 has incorporated certain provisions that provide the mandatory guidelines to be followed by a certain class of companies in this regard. The Act also mandates a certain percentage of profit to be spent on CSR activities. India thus became the first and probably the only country in the world that provides for mandatory CSR spending. As mandatory CSR spending is unique to India, and 2014–2015 being the first year for which companies’ annual reports are available, not much work has taken place on the subject. This study aims to fill that gap.

The provisions became applicable with effect from April 1, 2015. As 2014–2015 was the first year of implementation, this article aims to examine the implementation of CSR spending norms. The article has been divided into five sections. The second section discusses the requirements of the Companies Act, 2013, and the Income Tax Act, 1961, as applicable to CSR spending. The third section describes the research methodology and data used for this study. In the fourth section, the empirical results of the study are presented. The conclusions and recommendations are summarized in the fifth section.

Requirements of the Companies Act, 2013 and the Income Tax Act, 1961

The Companies Act, 2013

Section 135 of the Companies Act, 2013 prescribes the requirements of CSR on certain companies. The section prescribes three distinct criteria based upon the total assets, total turnover, and the net profit of the company to determine the applicability of these provisions (see Figure 1).

A company meeting any of the above criteria is required to follow the requirements of Section 135. The provisions apply to all companies meeting the criteria, including the private as well as unlisted companies.

The obligations of a company covered under Section 135 are depicted in Figure 2.

If a company fails to spend the prescribed amount as aforesaid, it is required to specify the reasons for the same. It may be noted that there are no penal provisions for not spending the prescribed amount. The company is however required to give reasons in the annual report.

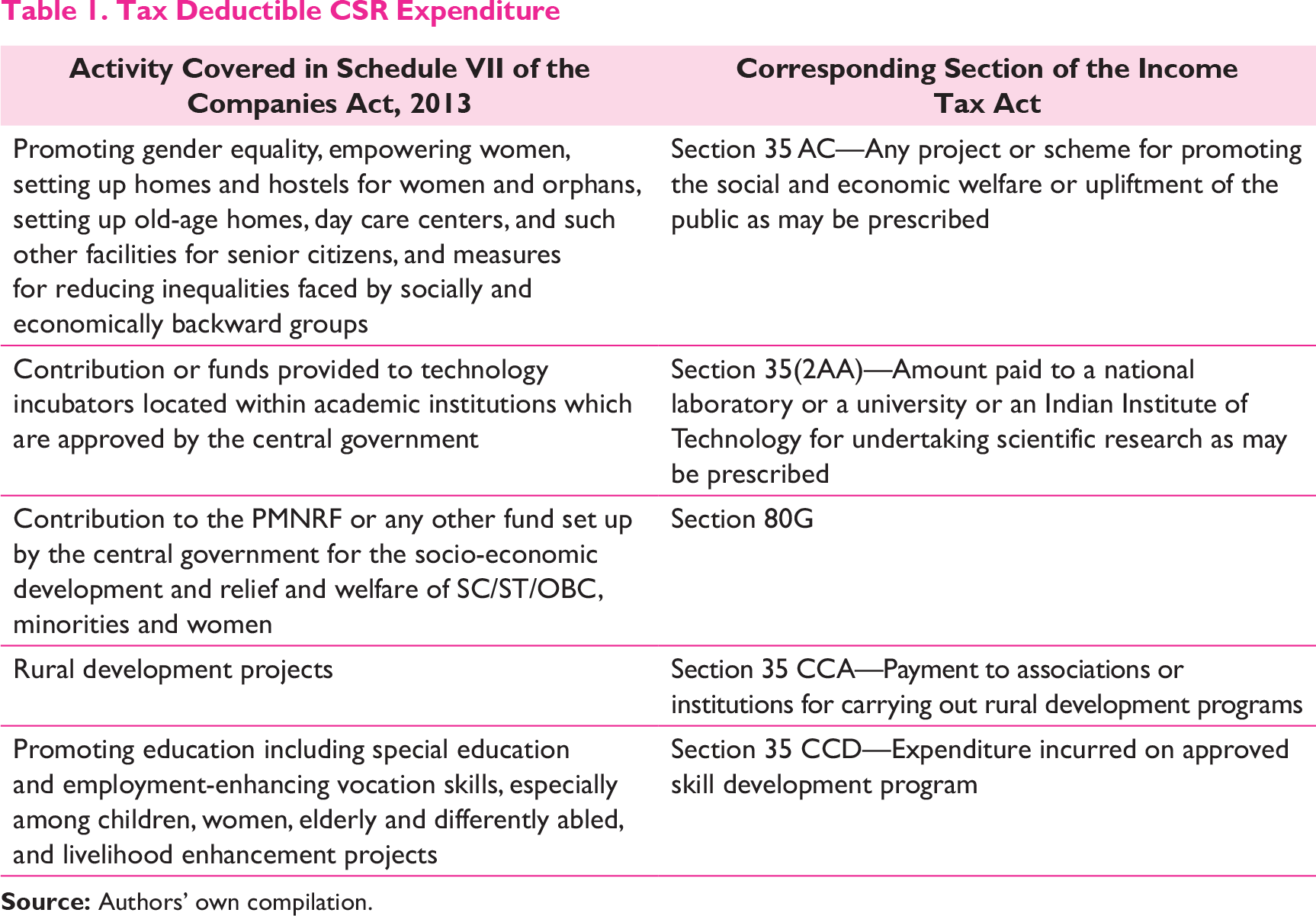

The activities that are eligible to be included in the CSR are specified in the Schedule VII Act. The activities specified are as follows:

eradicating hunger, poverty, and malnutrition, promoting preventive health care and sanitation including contribution to the Swachh Bharat Kosh set up by the central government for the promotion of sanitation and making available safe drinking water; promoting education, including special education and employment-enhancing vocation skills, especially among children, women, elderly, and the differently abled and livelihood enhancement projects; promoting gender equality, empowering women, and setting up homes and hostels for women and orphans; setting up old-age homes, day care centers, and such other facilities for senior citizens and measures for reducing inequalities faced by socially and economically backward groups; ensuring environmental sustainability, ecological balance, protection of flora and fauna, animal welfare, agro-forestry, conservation of natural resources, and maintaining the quality of soil, air, and water including contribution to the Clean Ganga Fund set up by the central government for rejuvenation of the River Ganga; protection of national heritage, art, and culture including restoration of buildings and sites of historical importance and works of art; setting up public libraries; and the promotion and development of traditional arts and handicrafts; measures for the benefit of armed forces veterans, war widows, and their dependents; training to promote rural sports, nationally recognized sports, paralympic sports, and Olympic sports; contributions or funds provided to technology incubators located within academic institutions which are approved by the central government; contribution to the Prime Minister’s National Relief Fund or any other fund set up by the central government for socio-economic development and relief and welfare of the Scheduled Caste, the Scheduled Tribes, other backward classes, minorities, and women; rural development projects; and slum area development.

Section 135 requires the company to give preference to the local area and areas around it where it operates, for spending the amount earmarked for CSR. Expenditure incurred on activities which are not covered by the activities stated in Schedule VII would not be considered as CSR expenditure.

Companies are permitted to collaborate with other companies to implement CSR projects and programs. Likewise, rules also permit a company to set up a trust, society, or Section 8 company for carrying out CSR activities. A company may carry out CSR activities through trusts, societies or Section 8 companies not set up by the company itself provided that such an organization has at least a 3-year track record of undertaking similar programs or projects.

As per the CSR Rules and clarifications issued by the Ministry of Corporate Affairs in this regard, the following expenditures are not considered as CSR spending:

Expenditure on activities undertaken outside India; Expenditure on activities in the normal course of the business of a company; Expenditure incurred exclusively for the benefits of the employees or their families; Contribution, directly or indirectly, to any political party; Expenditure to fulfill the requirements of any Act, regulations, etc.; Sponsorship of a one-off event, sponsorship, charitable contribution; and Contribution to any fund other than that covered by the Schedule VII.

The Income Tax Act, 1961

As per Section 37(1) of the Act, expenses incurred by the assessee for the purpose of business or profession are allowed as deduction in computing the income chargeable under the head “Profits and gains from business and profession.” However, as per the explanation inserted to Section 37(1), it states that the expenditure incurred in pursuance of Section 135 of the Companies Act, 2013 shall not be allowed as deduction in computing the taxable income.

Tax Deductible CSR Expenditure

Research Methodology and Data

The study uses the content analysis of the annual reports of Indian companies to quantify the CSR spending in the year 2014–2015. The study focuses on the companies that are included in S&P BSE 500 index of the Stock Exchange, Mumbai (BSE). “The S&P BSE 500 index is designed to be a broad representation of the Indian market. Consisting of the top 500 companies listed at BSE Ltd., the index covers all major industries in the Indian economy.”3

Retrieved December 11, 2015,

Out of 500 companies, data about CSR spending is available for 374 companies. The information regarding the average net profit and CSR spending was obtained from ACE Equity Database. Out of 374 companies in the sample, 31 (8.3 percent) are in public sector and the balance 343 (91.7 percent) are in private sector.

Empirical Results

CSR Spending

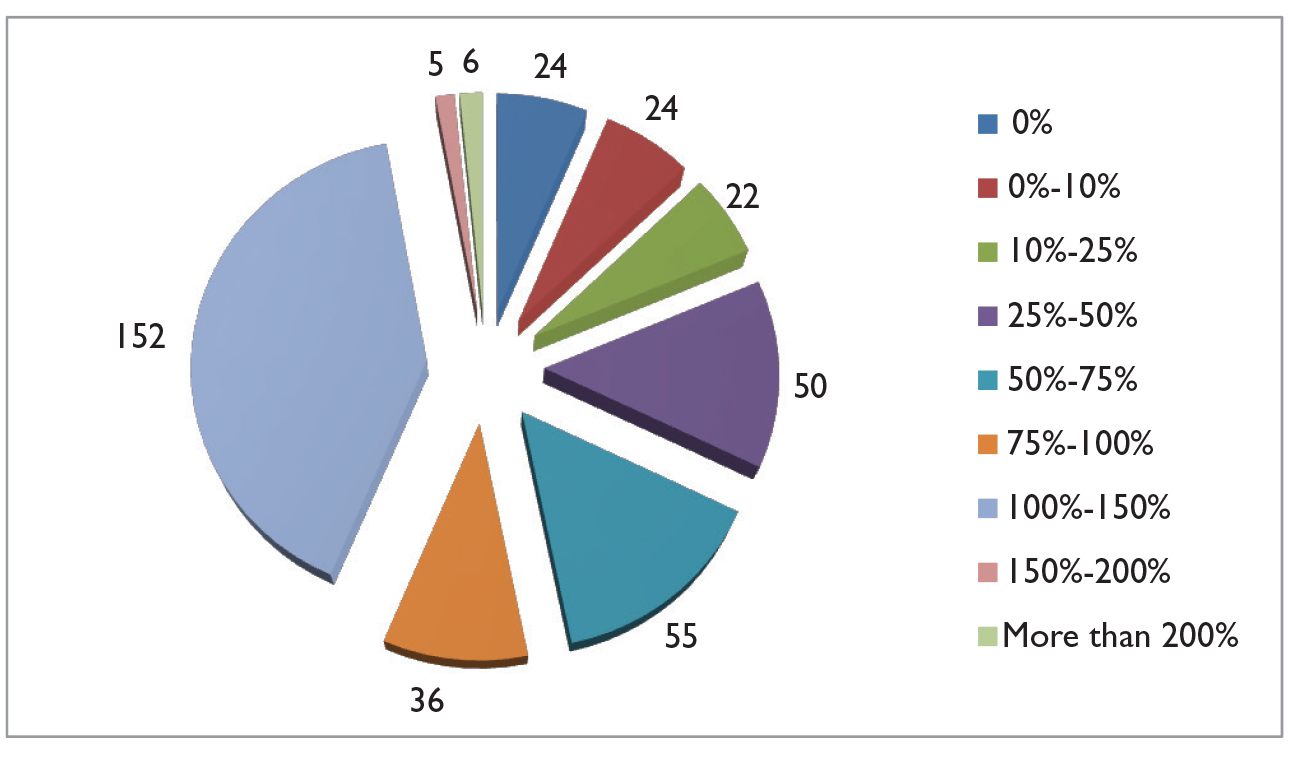

The sample companies earned an average annual net profit of `3,935 billion in the last 3 years. The 2 percent mandatory CSR spending comes to `79,920 million. As against this, the actual CSR spending comes to `59,420 million, which is approximately 74 percent of the required amount. 163 (44 percent) of the companies spent equal to or more than the required amount whereas the balance 211 (56 percent) companies failed to spend the required amount. There are 24 (6 percent) companies in the sample that did not spend anything on CSR during the year. The frequency distribution of the amount spent as a percentage of the mandatory limit is given in Figure 3.

It could be observed that in the first years of implementation, 199 companies (53 percent) have spent more than 75 percent of the mandated amount though there are no penal provisions for not spending the mandated amount.

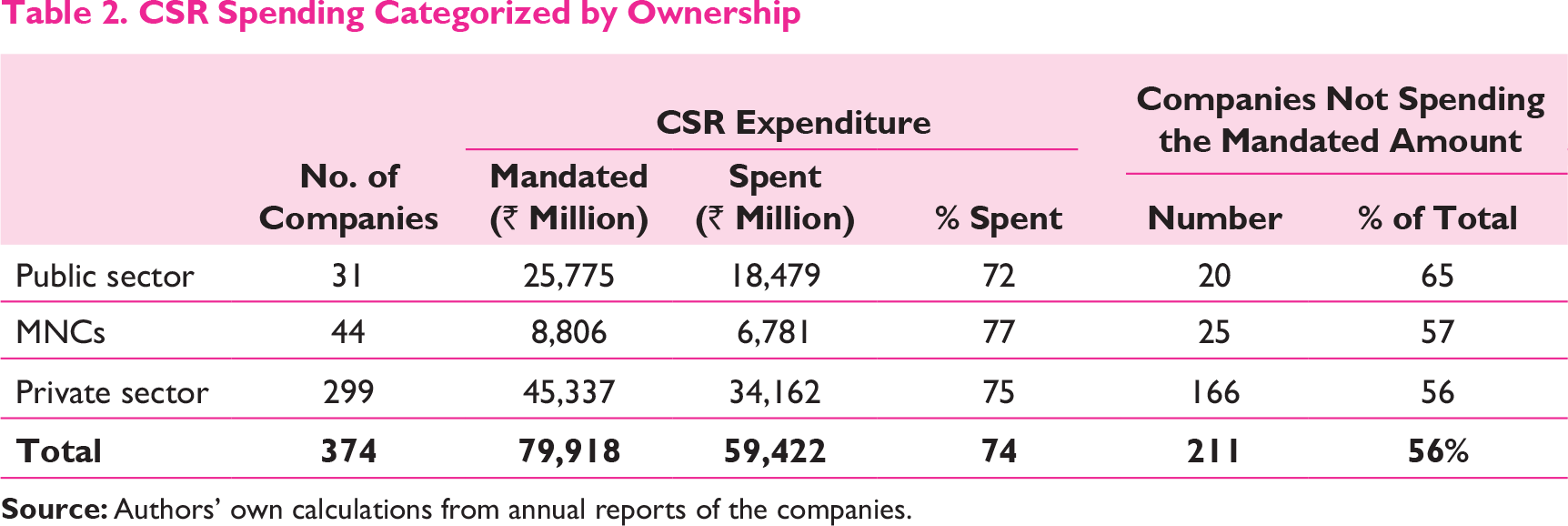

CSR Spending Categorized by Ownership

The sample of 374 companies has been divided into three subgroups based upon the ownership pattern—public sector companies (PSUs), multinational companies (MNCs), and other private sector companies. The details of CSR spending by these three groups are presented in Table 2.

CSR Spending Categorized by Ownership

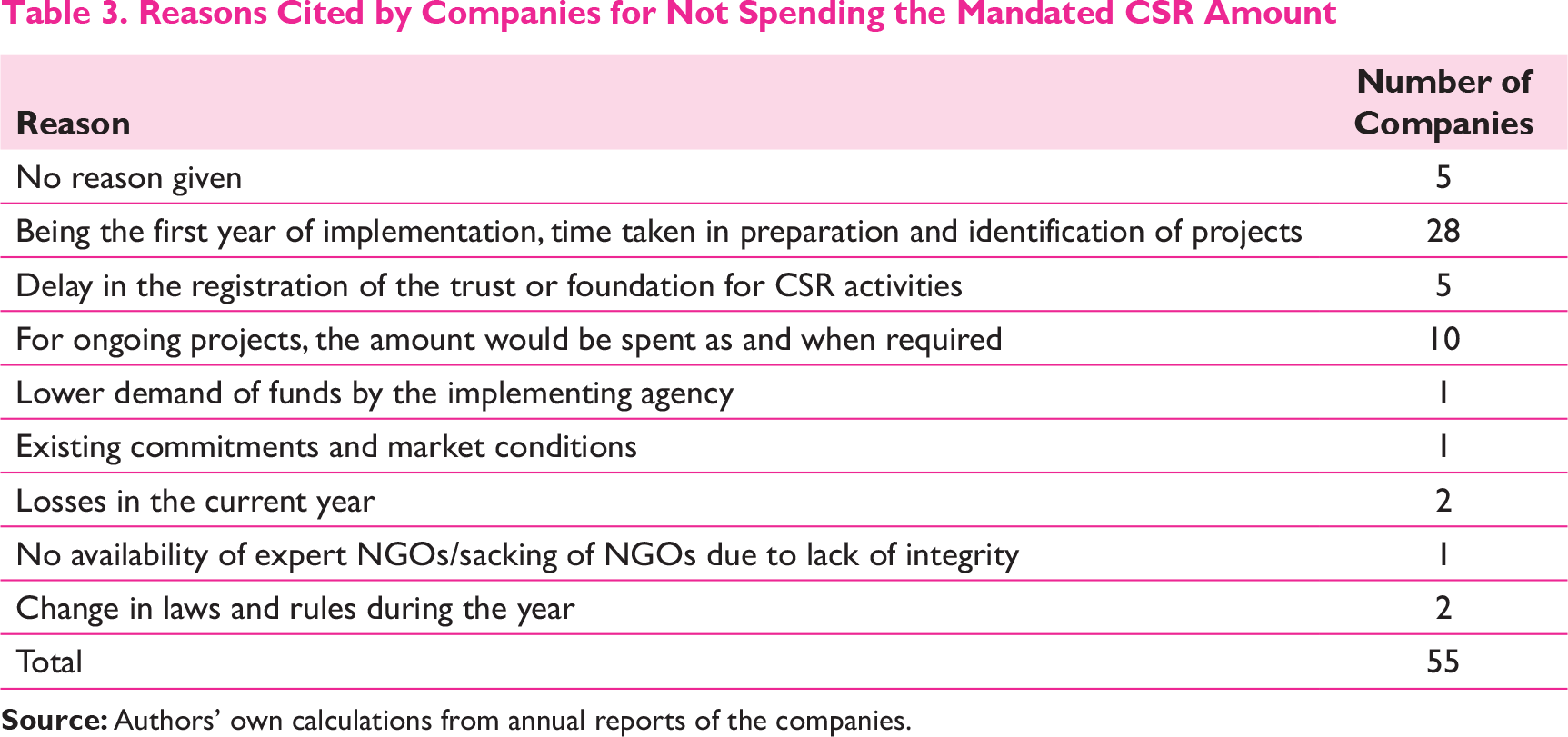

Reasons for Not Spending the Mandated Amount

Reasons Cited by Companies for Not Spending the Mandated CSR Amount

As this was the first year of implementation, majority of the companies have cited the time taken in the formulation of policies, identification of projects, and implementation agencies as the reasons for not spending the mandated amount. The reasons cited by the companies also highlighted practical difficulties like non-availability of expert non-governmental organizations (NGOs), lack of integrity on the part of the NGOs, and the gap between the amount committed and the amount spent. A company might have committed the mandatory amount on a CSR project, but due to the nature of the project the same might not be entirely spent. Losses in the current year were stated by two companies as the reasons for not spending the required amount. It may be observed that some of the companies have failed to give reasons for not spending the CSR amount. Not citing the reasons in the Board’s report does attract penal provisions.

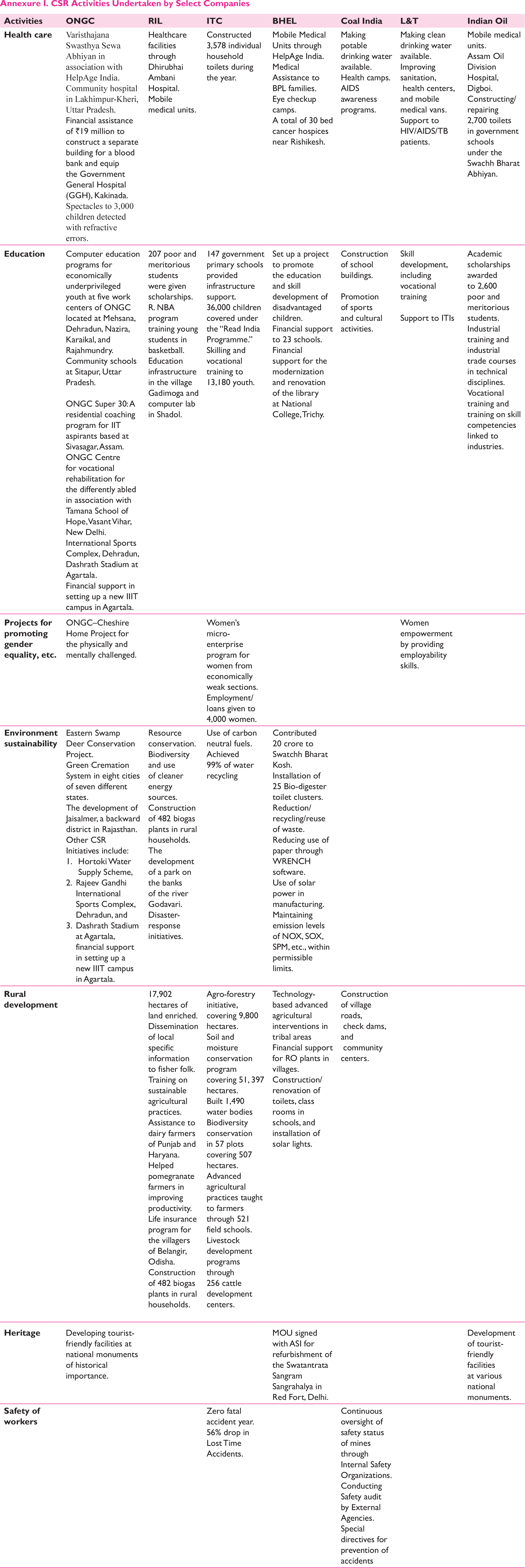

CSR Activities Undertaken by Select Companies

In this section, we present the CSR activities undertaken by select companies pursuant to Section 135 and Schedule VII of the Companies Act, 2013. The activities undertaken by seven select companies are presented in Annexure I. As could be observed from the Annexure I, these companies have undertaken CSR activities in the areas of health care, education, gender equality, environment sustainability, rural development, heritage, and the safety of workers. As 2014–2015 was the first year of implementation of mandatory CSR spending, companies are still in the process of formulating their CSR policies. A clearer direction on CSR activities would emerge in the coming years.

Conclusions and Recommendations

It is heartening to observe that even in the absence of any penal provisions, Indian companies have made efforts to meet the requirements of mandatory CSR spending. In aggregate, companies have spent 74 percent of the mandated amount and over two-thirds of the companies in the sample have spent more than 75 percent of the mandated amount on CSR activities. MNCs have marginally performed better than the PSUs and other private sector companies. Companies with an affiliation to Indian business groups have met the targets better than the other companies.

As the expenditure on CSR is not tax deductible, it may prove to be a dampener to CSR spending. To encourage the companies to spend more on CSR activities, the government needs to consider making such expenditure tax deductible. Further, contribution to the PMNRF and other trusts, as well as expenditure under Sections 30 to 36 of the Income Tax Act, 1961 provides deductions to the company and therefore is more tax efficient. This would lead the companies to take advantage of these sections rather than undertaking CSR activities themselves. Especially, the smaller companies would find it more convenient to contribute to funds like PMNRF and avail full tax deduction. This would not be conducive to generate the much-needed culture of CSR in the corporate India.

There is also concern about the misuse of these “outsourcing of CSR” provisions by unscrupulous companies by giving donations to trusts. As per media reports,

According to one person, the modus operandi is simple. If a company is obligated to spend, say, Rs 10 Crore4

1 crore = 10 million.

Retrieved December 14, 2015, from http://economictimes.indiatimes.com/articleshow/49474584.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

The regulators would need to keep a check on these practices.

Currently, the CSR spending is linked to the average profit in the last 3 years without any reference to the current year’s profit. There are 15 companies in the sample that have reported a loss for the year 2014–2015 and have a positive average profit as per Section 135 and are therefore obligated to spend on CSR. It would be unfair for the shareholders if these companies are mandated to spend on CSR even in the face of reported losses for the year. To illustrate, the average net profit of Jindal Steel and Power Limited amounted to `23,986 million, requiring `479 million to be spent on CSR. However, the company suffered a loss of `3,106 million for the year 2014–2015. In such a case, the company may be well within its rights to not spend the mandated amount and cite the current year’s losses as the reason for not spending the required amount on CSR.

Similarly, a company may be earning profits but the Return on Equity (ROE) may be very low. In such a case, any contribution to the CSR activities based upon the accounting profits would be at the expense of the shareholders. In fairness to the shareholders, the contribution to the CSR activities should be linked to the excess profits, that is, excess of profit over normal profit on the shareholders’ funds. The government may fix a normative return on equity (say 3–4 percent higher than the yield on government bonds). The average profit over the normal profit would be a fairer basis for CSR spending. In our sample, there are 124 companies with ROE of less than 10 percent. As these companies are not even earning the normal returns that may be expected by the shareholders, the mandatory CSR contribution further reduces the returns available to the shareholders.

As per the requirements of the Companies Act, 2013, the company not spending the prescribed amount on CSR is required to explain the reasons for the same. Losses suffered in the year or low ROE are justified reasons for not being able to spend the mandated amount. The companies however need to note that though there is no penalty for not spending the mandated amount, not explaining the reasons for not spending would attract penal provisions. The companies which have failed to meet the spending norms must explain the reasons in the Board’s report to avoid getting penalized. Not citing a reason or simply stating that efforts would be made in future to spend the amount does not meet the requirements of Section 135.

To conclude, making CSR spending mandatory has shown the desired results in the first year of implementation itself. Notwithstanding the difficulties in identification of the requisite projects and activities and in setting up the necessary vehicles for the same, corporate India has spent 74 percent of the mandated amount. Variety of projects has already been undertaken by companies covering permitted CSR activities. The experience gained by the companies would lead to even better compliance with the laid down norms. The government also needs to take a lenient view if a company fails to spend the mandated amount due to lack of adequate profit or low ROE. The companies need to make sure that the reasons for not meeting the spending norms are adequately explained in the Board’s report, not only to escape penal provisions but also to convey the same to the stakeholders. Implementation of these norms may prove to be a game changer in the times to come.

CSR Activities Undertaken by Select Companies

Footnotes

Authors' Biography