Abstract

Abstract

The soundness of the banking system is necessary for economic advancement and financial stability. In the contemporary era, the Indian banking system has suffered from the accumulation of substantial non-performing assets (NPAs), especially in the public sector banks (PSBs). This article examines the financial determinants of bad loans in the Indian PSBs with the help of panel data regression analysis. Panel dataset of 21 Indian PSBs for eight years from 2010 to 2017 is used for the study. For analysis, net non-performing assets (NNPAs) as a dependent variable and financial indicators as independent variable are used. Using the random effect model, it is found that credit–deposit ratio, loan maturity, and return on assets have a negative relationship with NNPAs. These factors have an association with a lower level of NPAs. Operating expenses and capital adequacy ratio have an insignificant effect on NNPAs. On the other hand, factors such as priority sector loans, collateral values, and non-interest income have a positive impact on NNPAs. These factors are an indication of a higher level of bad loans and are adding to the accumulation of NPAs in PSBs.

Introduction

In the post-crisis period, non-performing assets (NPAs) have been making headlines in India. The Indian banking system has suffered because the accumulation of substantial NPAs (bad loans), especially in the public sector banks (PSBs) and higher NPAs, has adversely affected the health of banking system. The Indian banking system is beleaguered with NPAs, and continuous rise of NPAs is a chronic problem in the Indian banking sector. Reserve Bank of India (RBI) data shows that PSBs’ overall net non-performing assets (NNPAs) ratio (6.9%) stood against the private sector banks (2.2%) and foreign banks (0.6%), respectively, at the end of the financial year 2017. PSBs have higher NPAs compared to private and foreign sector banks.

The primary motivation for the present study is to identify the determinants of bad loans of PSBs in India. This study empirically investigates the determinants of bad loans in the Indian PSBs by applying panel data analysis. The study uses credit–deposit ratio, loan maturity, return on assets, priority sector loans, collateral values, non-interest income, operating expenses, and capital adequacy ratio as financial indicators. These factors are taken into consideration for each bank separately for all the 21 banks selected.

Rest of the article is divided into four sections. The second section provides an overview of the literature review. Next followed by the third section that describes the data, variables, and econometric model. The fourth section discusses the results. Finally, the fifth section concludes the study.

Literature Review

The existing literature on the determinants of NPAs of banks shows that banks’ NPAs are influenced by bank-specific and macroeconomic factors. There are several empirical studies that explained the determinants of NPAs for a group of countries’ perspective. Beck, Jakubik, and Piloiu (2015) studied that real GDP growth, share prices, the exchange rate, and the lending interest rates are the macroeconomic variables that have significantly influenced the non-performing loans (NPLs) across 75 countries during the past decade. Messai and Jouini (2013) investigated the problem that loans change negatively with banks’ profitability and the growth rate of GDP. Furthermore, NPAs had positively changed with the unemployment rate in three countries (Italy, Greece, and Spain) from 2004 to 2008. Nkusu (2011) analyzed the macroeconomic variables’ influence on NPLs by using two interrelated approaches. First, panel regressions reveal that adverse macroeconomic developments are associated with rising NPL of 26 advanced economies. Second, the panel vector autoregressive model investigate the feedback between NPL and its macroeconomic determinants. Espinoza and Prasad (2010) explained the risk taking and efficiency are associated with NPLs of 80 banks in the GCC region.

Ćurak, Pepur, and Poposki (2013) examined the factors of NPLs in South Eastern European banking. The analysis contains both macroeconomic and bank-specific factors. The results determine that lower economic growth, higher inflation, and higher interest rate are associated with higher NPLs. Additionally, the credit risk is affected by bank-specific variables such as bank size, return on assets, and solvency. Dimitrios, Helen, and Mike (2016) studied the income tax, and the output gap significantly influence the NPLs in the European banking. Tanasković and Jandrić (2015) revealed that a negative correlation between increases in GDP and an increase of the NPL ratio. Along with GDP, foreign currency loans ratio and levels of exchange rates are positively associated with the increment of NPL ratio in selected CEEC and SEE countries in the period of 2006–2013. Erdinç and Abazi’s (2014) investigation revealed that among the macroeconomic determinants, the increase of NPLs is likely to real GDP growth, inflation and credit growth rate, and among the bank-specific factors, profitability and interest rate. Skarica (2014) had also explained the determinants of the NPL ratio in selected European emerging markets. GDP, unemployment, and the inflation rates are the leading causes of substantial levels of NPLs. Some empirical investigations on NPAs have also been carried out for various countries individually. Kjosevski and Petkovski (2017) examined that the return on assets and the return on equity have a significant effect on NPL. Furthermore, domestic private sector credit, GDP growth, unemployment, and inflation have a significant effect on NPLs of 27 Baltics banks for the period of 2005–2014. Garr (2013) investigated the financial sector growth and government borrowing has an association with lower NPA of Ghana banking while management inefficiency and GDPPC have a positive relationship. Abid, Ouertani, and Zouari-Ghorbel (2014) examined the determinants of household’s NPLs in the Tunisian banking sector. Their conclusions reveal that the real GDP growth rate, inflation rate, and the real lending rate influence the level of NPLs. Moreover, ROE and inefficiency have added analytical power when incorporated in the baseline model. De Bock and Demyanets (2012) studied that real GDP, currency devaluation toward the US dollar, and weaker terms of trade and outflows of a debt-creating capital drive to a more significant level NPLs in the banking sector. Moreover, Ghosh (2015) reviewed that bank profitability, GDP, and real personal income growth rates reduce NPLs. Inflation, capitalization, unemployment rate, US public debt, poor credit quality, cost inefficiency, and banking size significantly expand the NPLs. Ha and Hang (2016) suggested that both macroeconomic and bank-specific variables determined NPL of 29 Vietnamese commercial banks. Economic growth, inflation, bank profitability, liquidity, and credit growth significantly influence the NPLs. Louzis, Vouldis, and Metaxas (2012) analyzed the determinants of NPLs in the Greek banking sector using dynamic panel data analysis and revealed that NPLs in can be explained mostly by GDP, unemployment, interest rates, public debt, and management quality. Rahman, Asaduzzaman, and Hossin (2016) reviewed the NPLs’ increases with sensitive and priority sector’s loan while unsecured loans, profit per employee, and investment deposit ratio have a significant adverse impact on NPLs of commercial banks in Bangladesh. Shingjergji (2013) explained the main macroeconomic variables in the NPLs’ level in the Albanian banking system. The hypothesis motivates this study that macroeconomic variables affect the NPLs’ level. Vithessonthi (2016) examined that large banks drive the observed effects of credit growth on NPLs. Also, credit growth and NPLs do not affect the profitability of 82 publicly listed commercial banks in Japan.

There are various studies about determinants of NPAs. In the Indian perspective, Chavan and Gambacorta (2016) noticed that loan growth has a positive connection with a rise in NPLs of Indian banks. Also, the interest rate and growth of the economy have a significant effect on NPL. Patra and Padhi (2016) explore the Indian banks that got influenced more in comparison to the foreign banks with the change in macroeconomic conditions. Dhar and Bakshi (2015) had scrutinized the NPAs of 27 PSBs between 2001 and 2005 and opined that bank-specific variables such as net interest margin and return on assets play significant roles in determining the accumulation of bad assets. Furthermore, Misra and Dhal (2010) analyzed interest rate, maturity and collateral and bank-specific variables had a notable influence on NPLs of India’s PSBs in the nearness of macroeconomic shocks. Bank performance has an inverse linked with NPAs and straight related to a capital adequacy ratio in Indian banks (Bittu & Dwivedi, 2012). More, private banks and foreign banks have resources regarding their performances in better credit control. That intimates that banks’ privatization can lead to better management of credit risk (Swamy, 2012).

In the Indian perspective, some investigations were done on Indian commercial banks considering both public and private sector banks as one group. Other studies were concentrated on PSBs only. The present study explains the determinants of bad loans of PSBs taking into account of the current state of affairs, because of the rampant growth of NPAs among the PSBs during the last decade and not much research was conducted in this context. The present study is undertaken to fill the current gap.

Methodology

This section describes the data, variables and the regression model that are applied to examine the effects of financial ratios on NPAs.

Data and Variables

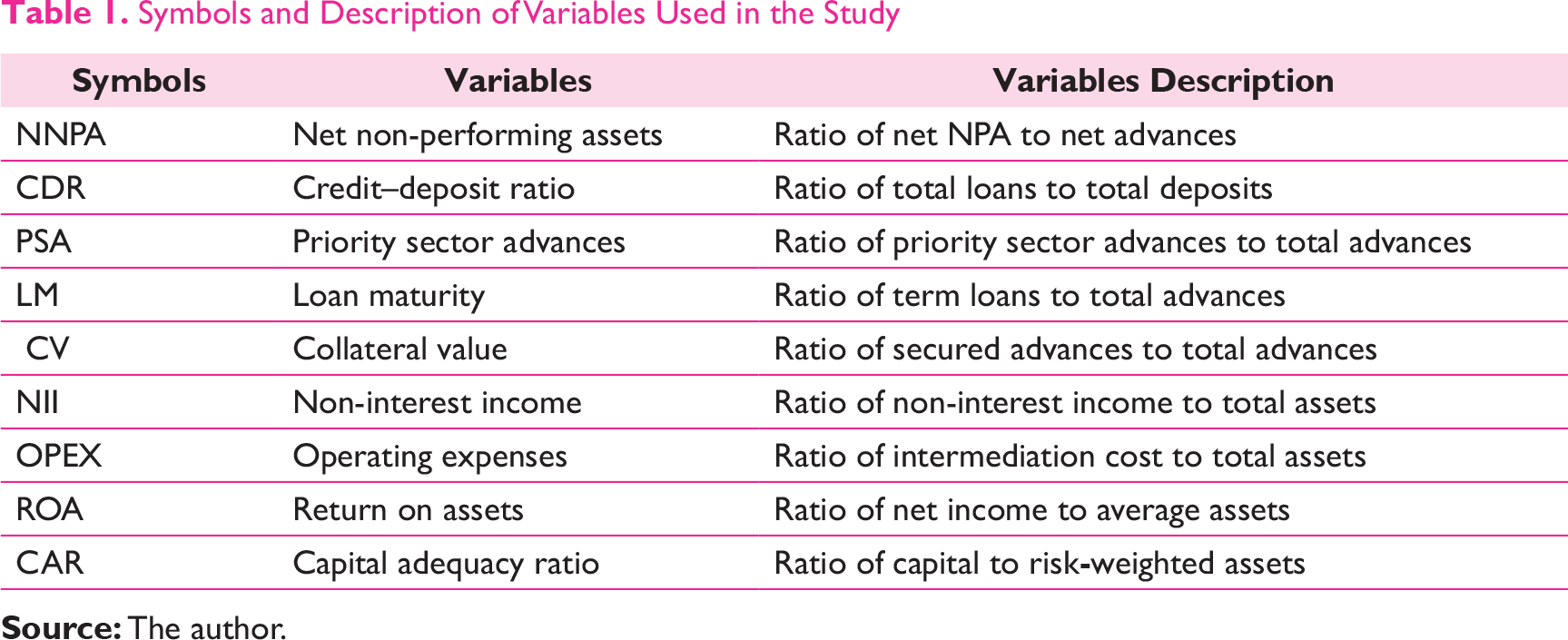

This article examines the financial determinants of bad loans in the Indian PSBs with the help of panel data regression analysis. Panel dataset of 21 Indian PSBs for eight years from 2010 to 2017 is used for the study. Data is gathered from the issues trends and progress of banking in India published by the RBI. For analysis, NNPAs as a dependent variable and financial indicators, such as credit-deposit ratio, loan maturity, and return on assets, priority sector loans, collateral values, non-interest income, operating expenses, and capital adequacy ratio, as independent variable are used (see Table 1).

Econometric Model

Based on the review of the literature, most of the studies applied to panel data regression model. Panel data presents extra informative data, including variability, limited collinearity between the variables, more degrees of freedom and even efficiency (Baltagi, 2005). This analysis applied the random effect and fixed effect panel data models, and they are being tested by Hausman test to check which model is relevant whether fixed or random effect model.

The fixed effects model represents the relationship among an explanatory variable and the dependent variable where each entity has a vital role in predicting the result in the method. The random effects model varies from the fixed effects model as the variation across objects is considered to be random and uncorrelated with the independent variables added in the model.

The following regression model is applied to identify the determinants of bad loans of PSBs:

NNPA it = α it + β1CDR it + β2PSA it + β3LM it + β4CV it + β5NII it + β6OPEX it + β7ROA it + β8CAR it + µit

where i = 1, …, 21 is the individual bank index; t = 1, …, 8 is the time index; α it = intercept; β1 to β8 = coefficients for independent variables; µit = error term.

Results and Discussions

Symbols and Description of Variables Used in the Study

Descriptive Statistics of Variables

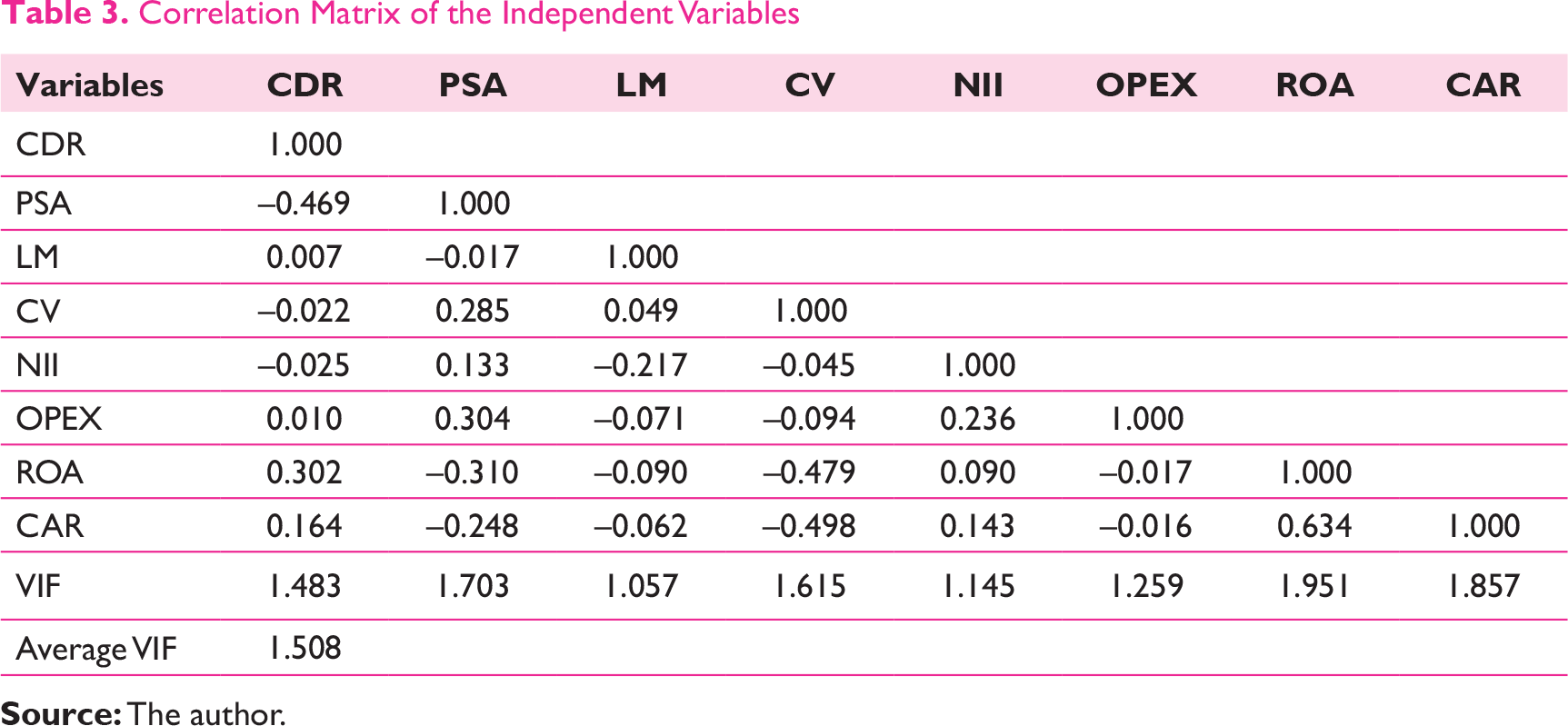

Correlation Matrix of the Independent Variables

Hausman test: The Null hypothesis is that the favored model is a random effect. The alternate hypothesis is that the appropriate model is a fixed effect. From the Hausman test, chi-square value is 13.326 and p-value is 0.1011 which is insignificant, so fails to reject the null hypothesis. Random Effect model is appropriate for the present study.

Results of Random Effect Mode

Loan maturity and NNPAs have a negative relationship between them. Moreover, loan maturity had a negative influence on the NNPAs. Long-term loans would help in minimizing NPAs. Longer-term loan contract gives the better relationship between borrowers and banks (Misra & Dhal, 2010). Collateral value and NNPAs both have a positive relationship with them. Also, a collateral value significantly influences the NNPAs. Banks were provided loans against secured advances, which will lead to the growing NPAs.

Non-interest income has a positive relationship with NNPA and significant impact on NNPAs. It implies that for one unit change in non-interest income, there is 2.138 units change in NNPAs with the same direction and this result was consistent with the empirical findings of Chavan and Gambacorta (2016). Non-interest income is much contributing to the increasing NPAs. Operating expense has a positive relationship with NNPAs. Operating expenses does not have significant influences on the NNPAs. There is a negative association between ROA and NNPAs. ROA has a substantial impact on NPAs. The negative relationship indicates the higher profitability of banks to help in reducing NPAs. This result was also confirmed by Bittu and Dwivedi (2012) and Kjosevski and Petkovski (2017). There is a positive association between CAR and NNPAs, but the capital adequacy ratio does not influence the NPAs of banks.

Conclusion

This panel data study gives information about what factors influence the bad loans of PSBs in India. From the panel regression model, it was found that credit–deposit ratio, loan maturity, and return on assets have a negative relationship with NNPAs. These factors have an association with a lower level of NPAs. NPAs could be managed with return on assets, loan maturity, and credit–deposit ratio. Return on assets estimates the profitability of business on its total assets. Bank profitability depends on efficient management of bad loans. Operating expenses and capital adequacy ratio have an insignificant effect on NPAs. On the other hand, factors such as priority sector loans, collateral values, and non-interest income are having a significant impact on NNPAs. These factors are an indication of a higher level of bad loans and are adding to the accumulation of NPAs in PSBs. Overall, these outcomes suggest that banks should provide adequate notice to variables such as priority sector loans, collateral values, and non-interest income to manage the bad loans of PSBs.

Bad loans influence the lending activity and performance of the banks. The outcomes of the study are in line with the conventional view of the banking literature and contribute valuable insight to banks. From a policy perspective, the lending policy encompasses relevant financial factors, such as priority sector loans, collateral values, and non-interest income, which have a significant impact on banks NPLs. The banks should control these variables. Furthermore, NPLs could be managed with loan maturity, credit–deposit ratio, and return on assets.

The present study has some limitations: the most critical limitation of this study is that the variables used in the study do not incorporate the macroeconomic variables. Also, the present study has considered only PSBs in its purview. In the future research, a model could be constructed using macroeconomic factors. Further, a similar or more extensive study can be extended to private and foreign sector banks and compare them.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.