Abstract

This article discusses the nine research studies compiled for the Journal of Creating Value (JCV) special issue, which has embarked on securing a deeper understanding of the divergent aspects of defining, measuring and maximizing value. Altogether, the nine studies collectively offer insights in this regard that are applicable to a wide range of organizations. This special issue runs the gamut of management actions in terms of value management and prepares companies for the future. The proposed classification framework in this article categorizes the nine studies based on their focus on value creation potential and value appropriation potential. Further, this article identifies and delineates future research directions that extend beyond the path forward identified by each of the studies themselves. Overall, this article is aimed to serve as a guide to understand and appreciate this special issue on a topic of vital interest.

Introduction

Value creation is a core precept of any business. The constant marketplace global upheavals (e.g., geopolitical changes, economic fluctuations, global healthcare crises) bring to the fore the importance of value in all aspects of business functioning. While such major global occurrences show a discernable impact on value generated in the overall business enterprise, the importance of value is also imperceptibly felt otherwise. Examples such as enhancing product quality standards (e.g., government regulations and policies), focusing on environmental, social and governance (ESG) aspects (e.g., reducing carbon emissions), introducing technology-driven solutions for business challenges (e.g., using new-age technologies for creating valuable offerings) are actions that are typically ongoing and continuous (in some cases, even subtle) that gradually add value for business and consumers.

Creating superior value (e.g., firms delivering valuable offerings for their customers) is a critical task for companies to survive in increasingly competitive markets. This can help firms deepen their knowledge of the nature of value-creation processes and the factors that may accelerate or drag these processes. Such efforts are expected to have a significant bearing on the efficient use of resources, along with important general economic and social consequences.

While value may be a constant feature throughout all areas of a business environment, it is perhaps best exemplified when multiple stakeholders are involved. In this regard, the value concept gets escalated to the stakeholder value concept wherein, value is observed to be the net accrued benefits (tangible and intangible) over the associated costs that firms and individuals realize in a commercial exchange process (Kumar & Rajan, 2017). In relation to this, research has shown that building better relationships with stakeholders can lead to an increase in shareholder value (e.g., Gifford, 2010; Hillman & Keim, 2001). Put simply, effectively managing stakeholders can subsequently lead to the creation of shareholder value. Table 1 provides examples of value-creating opportunities for firms through their stakeholders.

Examples of Value Creating Opportunities in a Business Setting.

As listed in Table 1, firms benefit from a wide range of stakeholder actions in deriving value. The creation of value typically occurs over two phases—first, a business attempts to generate value for its customers (typically by working with other stakeholders), and second, secures some of that value (e.g., by way of profits) thereby generating value for itself. Such a ‘value dyad’ signifies the ongoing value environment firms create for themselves. These two value actions are generally described as value creation and value appropriation, respectively. Prior research has investigated the distinction between value creation and value appropriation resulting in important insights for value management (e.g., Bowman & Ambrosini, 2001; Mizik & Jacobson, 2003). Conceptually, value creation and value appropriation have been presented as two sides of the same coin wherein, value creation refers to the total net value (i.e., total outcomes minus total inputs) created in a collaborative effort among exchange partners, and value appropriation refers to the net value that a focal firm claims successfully (Wagner et al., 2010). Subsequently, the collective impact of the value creation and value approximation actions is expected to lead to the creation of shareholder value.

Accordingly, the Journal of Creating Value (JCV) has designed a special issue under the theme ‘Defining, Measuring, and Managing Value’ to invite critical attention to the measurement and management of value. Nine papers were accepted which, altogether, provide a kaleidoscopic look into the concept of value management. Each article in this issue explores value from the standpoint of either value creation (i.e., value delivered by the firm to its stakeholders such as customers) or value appropriation (i.e., value retained by the firm for its own growth). In doing so, each article here explores how value can be measured and managed from its respective standpoint. Considering that each of the articles approaches value from a contextual vantage point, the articles collectively present a rich view of how value is created/appropriated, and consequently managed. Moreover, with each of the articles presenting managerial implications on value measurement and management, the practical value of this special issue is clearly established for the reader. In effect, these articles point towards a more systematized understanding of value creation and value management, leading up to shareholder value, in terms of both theoretical rigour and managerial efficacy.

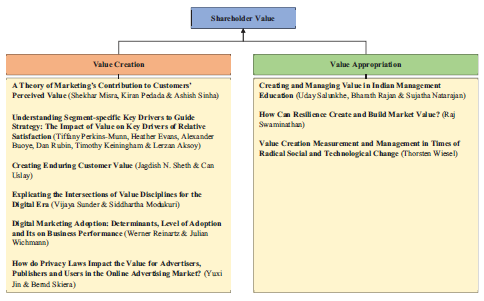

The papers presented within the following classification framework (Figure 1) establish a conceptual through-line for the special issue and broach all relevant aspects of value management. The proposed framework establishes the key motivation for this special issue, that is, how firms can use value creation and value appropriation to create shareholder value in a sustained manner. Accordingly, the framework classifies the papers into two categories: (a) value creation and (b) value appropriation. These dual approaches subsequently lead to the sustained generation of shareholder value. Such creation of shareholder value is essential to keep the overall business ecosystem healthy and thriving. The power of the proposed classification framework lies in its simplicity and its broad-based nature to accommodate a wide range of industries, contexts and business conditions.

Value Creation

Value creation, from a customer perspective, has been conceptualized as an increase in use value or a decrease in exchange value, typically arising out of an innovative offering, which can increase consumer surplus (Priem, 2007). Put simply, value creation is something that customers ‘got’ (i.e., benefits) compared to what they ‘gave up’ (i.e., costs or sacrifices) (Zeithaml, 1988). Also known as perceived value, several studies have focused on this repeatedly and have enriched the knowledge base (e.g., Anderson et al., 1993, 2007; Wilson, 1995). Recently, Kumar and Reinartz (2016, p. 37) define perceived value as customers’ net valuation of the perceived benefits accrued from an offering that is based on the costs they are willing to give up for the needs they are seeking to satisfy. Exploring this aspect of value, that is, creating value to the customers, six studies in this special issue find a place here. Collectively, these articles provide new knowledge on the creation and management of value. Brief synopses of these articles are presented here.

Misra et al. (2022) investigate the concept of customer-perceived value and the role of marketing in shaping this concept. They advance a theoretical framework and present propositions that identify how marketing creates value, specifically by reducing the various types of market imperfections. The authors consider the cost of customers and benefits to customers in advancing the proposed framework. Specifically, they posit that the value to customers is reduced by perceived risk. Based on this, they advance theoretical and managerial implications for managing customer value and designing marketing activities.

Perkins-Munn et al. (2022) advance a procedure for identifying the distinct key drivers of relative satisfaction for customer segments defined in terms of value. Using customer survey data from a bank, the authors identify segment-specific key drivers of relative satisfaction of customer segments identified by subjective, user-defined value-based segments and objective, data-derived segments (through latent class analysis). They find that while subjective, ad-hoc approaches to value-based segmentation are adequate, they offer suboptimal results for determining the segment-specific key drivers of relative satisfaction. Instead, they find that segments derived from latent class analysis provide an optimized basis for identifying a customer base’s heterogeneous key drivers of relative satisfaction. Based on these findings, they identify managerial implications regarding resource allocation to valuable customers.

Sheth and Uslay (2022) define and discuss value, customers and processes to create value. They achieve this by distinguishing between three business philosophies (product-centric, competition-centric and customer-centric), three types of customers (user, payer and buyer) and three primary types of value (performance, affordability and service) based on these customers’ preferences. Through this, along with a good blend of business examples, they identify 10 processes that can create value for customers. They conclude the study by identifying research questions that future studies can use to investigate value creation measurement.

Sunder and Modukuri 2022) investigate the value disciplines in the digital age. They argue that customers in the digital age look not only for more of what they value but also look for different forms of value concurrently. As a result, they present that becoming skilful in one value discipline is not likely to be sufficient for firms to gain a competitive advantage in this digital age. Considering this, the authors make the case to explore the value discipline intersections by studying real-world companies that have created value in practice. To do so, they focus on explicating the intersections between the three traditional value disciplines—operational excellence, product leadership and customer intimacy. They discuss these intersections using business examples. They conclude the study by identifying implications for theory and practice.

Reinartz and Wichmann (2022) investigate value creation in the platform era. They build on the concept of customer engagement value to propose the participant engagement value that can apply to the platform context. In doing so, they adopt the perspective of a platform provider to develop the participant engagement value concept. Specifically, they delineate a range of value components originating from a platform’s consumers and suppliers and generating monetary/non-monetary as well as direct/indirect value for the platform provider. The authors present this concept (along with the individual components) to aid managers in assessing and managing the sustainability of the platform. The authors conclude the study by identifying future research areas.

Jin and Skiera (2022) investigate how privacy laws impact the value for advertisers, publishers and users in the context of advertising. The authors consider three important privacy laws—GDPR, CCPA and PIPL—and compare their impact on the value for three actors of the online advertising market, that is, advertisers, publishers and users. In doing so, they use a set of criteria to create a legal strictness score for each of the three laws to derive their similarity. Subsequently, they examine the exchanges between advertisers, publishers and users to (a) define the value for one actor by another actor (e.g., the value created or destroyed for users by publishers), (b) examine the existing literature to describe the effects of privacy laws on value and (c) quantify the total effects of legal strictness for each actor by adding up all effects on value—the sum of effects on value. Finally, they derive the changes in value by multiplying the legal strictness score and the sum of effects on the value that yield the effects that each privacy law has on each actor. Overall, the study concludes that stricter privacy laws bring larger negative changes to the value for actors. Specifically, the study found that GDPR and PIPL are similar and stricter than CCPA. As part of the implications for the companies, the study notes that the differential effects of privacy laws on the value for various actors provide more information for regulators who must balance the value for all actors when introducing new privacy laws or amendments.

Value Appropriation

Although value creation is understood from the customer’s perspective, value appropriation can be understood from the firm perspective. That is when value is delivered to customers, it can result in increasing overall payments received (e.g., through an increased volume of customer purchases) by the stakeholders that constitute the firm’s value system. Such an increase provides the focal firm opportunities to capture or retain a portion of the payments (Priem, 2007). This occurrence is understood as value appropriation. In this regard, Mizik and Jacobson (2003) contend that value appropriation, in addition to value creation, is necessary for a firm’s financial success. Particularly, they offer that value appropriation provides firms the ‘…ability to restrict competitive forces (e.g., erect barriers to imitation) so as to be able to appropriate some of the value that it has created in the form of profit’ (Mizik & Jacobson, 2003, p. 63). With this contextual background, three studies in this special issue explore the value appropriation aspect across various contemporary business contexts. Put together, these studies provide new insights into value appropriation and its potential consequences on shareholder value. Brief synopses of these articles are presented here.

Salunkhe et al. (2022) investigate the creation and management of value in Indian management education. Extending the stakeholder engagement concept, for an Indian management institute, they (a) define value, (b) identify nine value categories in which value can be created and managed, (c) advance a stakeholder engagement approach in creating and managing value, (d) identify and categorize value measures as contiguous and future measures and (e) recognize the resources and capabilities needed to create and manage value. To develop this study, the authors adopt the view that the quality and quantity aspects of management education indicate a value problem, that is, value to the students, value to the institution and value to the society. Following the development of the proposed approach, the authors present a discussion focused on ways to maximize value for the Indian management institution, and the conditions required for maximizing value creation in Indian management education. They conclude the study by identifying areas for future research.

Swaminathan (2022) investigate how companies can build business resilience that can create value. The study offers that resilience can be built by developing core capabilities that can place them on the part of sustainable value creation. Specifically, the study identifies the pursuing of two paths—absorptive and adaptive—that are part of the core capabilities of an organization. The absorptive path involves redundancy, robustness and agility as its key components, while the adaptive path involves resourcefulness, adaptability and flexibility as its key components. Based on these two paths, the study argues that building resilience is a continuous process that involves focusing on revenue growth, margin growth and retained earnings simultaneously to create value. Specifically, the study offers that building resilience is much more than effective risk management and includes a proactive focus on the business needs vis-à-vis the external environment. Following this, the study presents industry examples to discuss the creation of business resilience and concludes by identifying strategies that firms can consider for navigating uncertain times in their pursuit to create value.

Wiesel (2022) investigates the creation and measurement of value during radical social and technological change. In the discussion of business during radical social and technological change, the study identifies a set of characteristics firms will have to contend with and their consequences. Based on these, the study advances value-to-customer and value-to-firm as the approaches through which firms can still manage to create value in such uncertain times. Particularly, the study offers that looking at the future cash flow stream (using forward-looking metrics such as customer lifetime value [CLV]) will provide firms with the ability to close the gap between CLV and customer equity (CE) and shareholder value. For instance, regarding the SaaS subscription models, the study offers a direct link between CLV/CE with shareholder value. For instance, the value of Netflix went down due to a reported loss in customers. While the loss in customers is small, the value lost for Netflix is about 15%. In this regard, the study identifies the key performance indicators and the related measures of market success that can create value.

Conclusion and Future Research

Ongoing research efforts will continue to explore the various facets of value creation and value approximation by firms. While each paper accepted for this special issue moves the needle on this stream of research, they also identify the future possibilities that can unlock even more knowledge on these topics. In addition to general directions for future research suggested by the articles in this issue, we propose the following research areas for future research to consider.

Misra et al. (2022) conceptualize and advance the positive impact of marketing on customer perceived value. Particularly, they claim that marketing ‘…plays the critical role of resolving these imperfections by reducing customers’ search cost and reducing uncertainty through better matching and customer engagement’. They arrive at this conclusion by advancing key propositions related to customer search costs and customer engagement. In this regard, future research can focus on testing these propositions through empirical means. Therefore

RQ1: What are the boundary conditions that govern marketing’s continued positive impact on customers’ search costs and customer engagement?

Perkins-Munn et al. (2022) advance a procedure to identify the drivers of relative satisfaction for customer segments for value creation. Their study creates possibilities for several related studies regarding customer segmentation and value creation. In this regard, it would be interesting to know how multinational corporations can use this approach when dealing with multiple customer segments across different country markets. For instance, it is possible that even within emerging markets, one can expect substantial variation among customer segment characteristics. Therefore

RQ2: What type of variation in the identification of the key drivers can be expected for firms operating within and across developed and emerging markets?

Sheth and Uslay (2022) propose 10 processes through which businesses create value. They achieve this by first defining value and the roles of customers in using the offerings. Particularly, the study classifies the 10 processes into 3 types of value-creating buckets—performance, affordability and service—so that value is created for the firms. In this regard, the topic of ensuring environmental sustainability while pursuing value-creating endeavours arises. Therefore

RQ3: In designing global sourcing strategies, how much value does sustainable sourcing options, such as upcycling and recycling, contribute to the overall value potential?

Sunder and Modukuri (2022) identify strategic intersection areas between the value disciplines so that firms can unlock newer sources of value potential, particularly in the digital era. proposes 10 processes through which businesses create value. While the evolving digital era presents numerous opportunities for identifying value creation potential, a vast majority of firms are still in the ‘transitionary zone’ from the non-digital to digital mode of operations. Put simply, firms are varied in their journey of infusing a digital mode of functioning. Therefore

RQ4: Of the four intersection areas identified, are there any intersection areas that are easier than the others for firms to explore value creation opportunities as they continue their digital journey? For such areas, what are the unique resources and capabilities needed for such firms to tap the hidden value?

Reinartz and Wichmann (2022) propose a platform-based valuation framework for facilitating value creation. Current platform models are largely driven by technology at the core. In this regard, the role of technology would be critical in creating newer value. Therefore

RQ5: Are there any new-age technologies (e.g., artificial intelligence, robotics, blockchain, etc.) that are more suited (than others) to helping platforms realize value potential?

Jin and Skiera (2022) review three privacy laws and evaluate their impact on value for the actors in the advertising industry. They argue that stricter privacy laws decrease the value creation potential for the actors, with the decline in value being the largest for the publishers. Such a finding indicates a need to identify a balance in the value creation among all actors. Therefore

RQ6: When implementing each of the privacy laws, is there a mechanism through which each of the actions of the actors be quantified so that a more fair and equitable distribution of value be attempted?

Salunkhe et al. (2022) investigate the Indian management education industry to determine how value can be created for the management institute. Spurred by the pandemic, the edtech industry is witnessing a boom. This development also shows increasing signs of complementarity between the traditional education system and the edtech companies. In this, a key feature that distinguishes edtech companies from the traditional players in the reliance on various technology tools. Therefore

RQ7: What technologies (including new-age technologies) can traditional education providers (i.e., universities and colleges) adopt so that value creation potential for the management institute is enhanced?

Swaminathan (2022) focus on identifying resilience-creating mechanisms that can contribute to overall value capture for the firms. In this, the adaptive and absorptive paths have been identified as potential avenues for building resilience. However, the pursuance of these paths would require firms to follow certain rules/practices for the deployment of resources. Therefore

RQ8: What resource optimization rules can be developed that can be used to maximize resilience, thereby leading to value appropriation? Additionally, what management skills (e.g., technical, managerial, operational, etc.) should companies develop to optimize their resource deployment so that the development of resilience is ensured?

Wiesel (2022) focuses on measuring and managing value during times of radical social and technological changes. However, as indicated by the papers accepted for the Special Issue, given the granular nature of the cultural and political differences across countries, achieving generalization can be challenging. While each country market may possess unique elements, further granular distinctions between different country markets could exist. Therefore

RQ9: Can, and if so how, do the country-level cultural, infrastructural and political factors impact (e.g., direct effect or moderating effect) the proposed value appropriation prospects during times of radical social and technological changes? What might those impacting factors be?

Footnotes

Acknowledgement

We thank Bharath Rajan for his assistance in the preparation of this article. We thank Renu for copyediting the manuscript.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.