Abstract

Semi-formal settlements like Delhi’s unauthorised colonies (UACs), which await regularisation by the state, are characterised by aspirations for housing improvements and enhanced property values. Frustrated by the rigid regulatory frameworks that operate in the binaries of legal/illegal, formal/informal, planned/unplanned and having limited influence over processes of regularisation, UAC residents use ‘transversal logics’ (Caldeira, 2017) to negotiate planning regimes, credit markets and local politics to improve housing, which become their ‘action space’ to meet aspirations for social mobility. This article investigates the role of finance and networks of credit in autoconstruction, with a focus on the work of market actors in navigating market–citizen and market–state boundaries, foregrounded against the relatively well-studied politics of state–citizen relations. It finds that landowners and housing finance institutions, as well as actors within them, navigate regulatory boundaries through innovative partnerships and creative workarounds, and by strategically deploying collective and individual identities. Even as cities like Delhi endeavour to become planned world-class utopias, a multitude of actors continue to reshape the city’s peripheral landscapes through the assertion, dissolution and spanning of multiple boundaries—regulatory, individual–collective, state–citizen, citizen–market and state–market.

Introduction

Delhi, officially referred to as the National Capital Territory (NCT) of Delhi, has eight typologies of settlements 1 that not only determine the categorisation of where one lives but also greatly impact levels of service delivery, quality of life and security of tenure (or lack thereof), among other markers of urban life (Bhan, 2013; Heller et al., 2015). In the last reliable estimate of population along this eight-fold categorisation, which goes back to a 2001 report by the Delhi Urban Environment and Infrastructure Improvement Project (DUEIIP), only 23.7 per cent of the city’s population, less than a quarter, resides in settlements designated as ‘planned’ (Bhan, 2013; CPR, 2015). The rest of the city, over 75 per cent, lives in areas that are marked by some form of tension with planning regulations. This unplanned, informal part of the city is not a unified whole but constitutes a diverse range of settlements. These differences, though significant, do not obscure the fact that a large part of the city and its neighbourhoods, as in many cities of the Global South, have been built through what Caldeira (2017) calls ‘autoconstruction’. Delhi’s urban fabric, then, can be read as uneven, comprising varying interspersed forms of spatial informality and illegality.

Autoconstruction refers to the practice of inhabitants building their homes incrementally over a period of time based on their existing needs and the resources available at certain points of time (Caldeira, 2017). Homes are built temporally—a family, for instance, may construct a single floor to begin with and add more floors as the years pass by, either to accommodate the growing needs of the household or to rent one or two of the floors. Such house building practices render them as ‘agents of urbanization, not simply consumers of spaces developed and regulated by others’ (Caldeira, 2017, p. 5). In the process of autoconstruction, Caldeira (2017) argues that residents build neighbourhoods as they build homes, through ‘transversal logics’ in a mode of production of urban space she calls ‘peripheral urbanisation’. This peripherality is not a physical location on the margins, but a process through which spaces come to be produced and inhabited in the city regardless of spatial location. The concept of transversal logics broadly emphasises the negotiations and engagements by residents with the state, state institutions and the market that bypass or run counter to ‘some dominant official logics’ (Caldeira, 2017, p. 9). This could imply, for instance, getting approvals for legalisation/regularisation for a settlement that the state deems illegal or finding alternate markets to secure credit for home construction outside of the formal credit system. Caldeira’s use of the term ‘transversal’ goes beyond the binaries of formal/informal and regular/irregular to emphasise the constantly evolving and heterogenous nature of urban spaces.

In Delhi, autoconstruction as a mode of housing production has been an outcome of the negligible affordable housing supply (leading to the creation of self-provided homes in informal settlements), exacerbated by several waves of slum evictions and resettlement, in which the state has provided plots of land to displaced households. 2 Much has been written about the autoconstruction practices of the urban poor in the face of evictions under world-class city making (Bhan, 2013; Menon Sen & Bhan, 2008). These studies have emphasised the resilience of the poor and the multiple negotiations that mark the realities of building a house in the city, especially in a context where the land being built on is outside the rubric of what city planners and officials would consider as the ‘planned’ part of the city. Theories of autoconstruction and peripheral urbanisation have contributed to critically nuanced, contemporary understandings of urban politics, steering them away from patron-clientelism (wherein urban improvements take place courtesy the power and sway of elected representatives) to emphasise citizens’ agency to shape and reshape their neighbourhoods through a wide range of negotiations. Much more, however, needs to be unpacked in terms of the processes and actors driving autoconstruction in cities of the Global South.

Given the vastly different conditions under which residents build homes in informal settlements, we contend that an equally critical, yet relatively less known, aspect of autoconstruction is that of access to finance and the networks of credit available to residents of informal settlements. What is the landscape for financing housing in auto-constructed settlements and who are the key actors in this? Which strategies and mechanisms do they deploy in their functioning and what are the regulatory barriers they have to contend/negotiate with? Following what Shatkin (2007) calls ‘actor-centered frameworks of urban analysis’, we foreground the housing finance landscape in auto-constructed settlements as one in which a range of finance institutions—and individuals within these institutions—span state–market and market–citizen boundaries to reshape affordable housing in semi-legal settlements.

This article initiates a conversation around some of these questions by taking up the case of housing finance in unauthorised colonies (UACs) in Delhi. Among the eight settlement categories in Delhi, UACs are prominent and highly diverse spaces of housing production and commercial activity, with an estimated population of 4 million people spread across 1,797 settlements (Economic Survey of Delhi, 2018–2019, cited in CPR, 2015). Such settlements are considered ‘unauthorised’ since they are built in violation of zoning regulations and Master Plan guidelines, unlike slums (officially referred to as jhuggi-jhopri clusters), which are considered to be illegally occupying public land. Considered semi-legal (Zimmer, 2012), UACs have been a visible site of urban politics in the city, owing to citizen articulations for improved services as well as the state’s repeated post facto attempts at regularising them (providing basic services and recognising land titles), often for immediate electoral gains. For instance, provisional regularisation certificates 3 were distributed before the 2008 elections, and regularisation featured in the manifestos of all major political parties during elections in 2013 (Sheikh & Banda, 2014). More recently, in December 2019, The NCT of Delhi (Recognition of Property Rights of Residents in UACs) Bill, 2019, was enacted. Concurrently, the Delhi Development Authority (DDA) announced the Pradhan Mantri—UACs in Delhi Awas Adhikar Yojana, under which it has kick-started the process of providing legal titles to property owners in UACs. These periodic attempts at post facto regularisation and the associated expectations of tenure security form the backdrop for this article’s focus on the role of housing finance processes in transforming these neighbourhoods over time.

This article explores the cases of two areas in East Delhi, namely Mandawali and Lalita Park, a patchwork of UACs and regularised UACs (the oxymoronic term for UACs that have been regularised). We draw on multiple rounds of fieldwork conducted in UACs and regularised UACs in these two areas. During Phase 1, conducted during April–July 2016 and in April 2017, we conducted 72 interviews in Mandawali and Lalita Park to understand urban improvements in the UACs as well as to identify and investigate certain projects of aspirational urban regeneration. The latter follows Leary and McCarthy’s (2013) definition of aspirational regeneration: ‘urban regeneration is area-based intervention which is public sector initiated, funded, supported, or inspired, aimed at producing significant sustainable improvements in the conditions of local people, communities and places suffering from aspects of deprivation, often multiple in nature’ (p. 9). Taking our cue from this, we have conceptualised urban regeneration as a two-way process: how aspirations and desires for change get framed and articulated within a wider context of state-led urban developments/redevelopments (like regularisation, in our case, sites). We asked residents and community representatives, chiefly resident welfare associations, elected representatives and volunteers with political parties about what changes they had seen in the settlement(s) in the past decade and what they expected to see in the future, to whom they articulated demands and expectations for change and what actions had been taken towards their fulfilment.

In Phase 1, we found investments in housing to be key expressions of urban regeneration in these neighbourhoods. In Phase 2, we zeroed in on housing finance as a route to housing improvements, upgrades and reconstruction, using Lalita Park to further explore the distinct processes unfolding in regularised and unregularised parts of the UAC. We interviewed 15 Residents Welfare Association (RWA) members, brokers, builders and real estate agents in Lalita Park to understand the ongoing processes of autoconstruction and housing redevelopment, as well as past experiences and future expectations of regularisation. We also interviewed 12 officials, including chief executive officers (CEOs), branch managers and field agents in a diverse array of housing finance organisations about the products and processes related to housing and construction loans in the broad spectrum of Delhi’s unplanned colonies, attempting to understand the specific vagaries of UACs. Fieldwork for Phase 2 was conducted from March to December 2018 and some follow-up work was undertaken during February–March 2019.

Case Context

Our cases—Mandawali and Lalita Park in East Delhi—demonstrate the variations, temporal changes and internal diversity often seen in UACs. In Lalita Park, landowners from Shakarpur village plotted and sold agricultural land in the early 1970s. 4 Until the 1980s, houses were single-storeyed, and vertical expansions were rare. Coaching institutes preparing young men and women for the chartered accountancy (CA) exams came up in the 1990s and created a demand for rental housing for students, which homeowners began to meet by building more floors for rent. The area became a hub for CA coaching institutes in Delhi, attracting students from the National Capital Region, and is now known as a place for affordable rental housing for students and first-time job seekers. These institutes are housed in multi-storey buildings cheek by jowl with retail stores and restaurants along Vikas Marg, a key connection between Central and East Delhi. They are also seen in secondary lanes alongside travel agencies, property dealerships, cybercafes and photocopy stores. The crowded and narrow tertiary lanes have multi-storey residences, and these too are rapidly being converted into student hostels. Commercial establishments, typically gyms, salons, libraries and grocery stores, are seen in the tertiary lanes as well. Lalita Park is predominantly mixed use in nature, with nearly all plots already built up to G + 3 floors.

Over time, homeowners in Lalita Park have constructed vertically on their plots to leverage emerging opportunities for rent and sale for residential and commercial purposes. Despite these changes, Lalita Park remains a relatively underserviced neighbourhood when compared to the wealthier planned neighbourhoods in its vicinity. In our interactions with them, residents pointed to the poor quality of the water, unclean drains, inefficient waste disposal, unreliable electricity, patchy street lighting, lack of open spaces and persistent issues of safety and security.

In Mandawali too, a cluster of UACs emerged through the plotting and sale of the agricultural lands of the Fazalpur and Mandawli villages. However, it is a far more fragmented, and a large patchwork of settlements spread across three assembly constituencies and four municipal wards. It is located amidst the planned apartment complexes and housing societies of Patparganj, somewhat less advantageously than Lalita Park. Autoconstruction is a key feature of this settlement as well. Most houses are 3–4 storeys high, with commercial businesses concentrated along the main commercial spine of the settlement, namely Mandawali Main Road, which links to two key roads in East Delhi (Patparganj Road and Narwana Road) and the shorter Shiv Mandir Marg. Respondents in certain parts of Mandawali faced repeated demolition in the 1980s, and even today, it is an area neglected by the government authorities. Open drains run along the sides of roads and inner lanes, and criss-crossing electricity wires are visible overhead. ‘DDA and MCD are not very active…(officials) rarely listen to complaints or visit the area for checks, inspections…’ a property dealer narrated.

Our analysis of the interviews shows that local aspirations and desires for urban regeneration get framed within a wider context of state-led urban development/redevelopment measures like regularisation, as well as with reference to more localised infrastructure improvements. In consonance with this, aspirations for change are articulated alongside more routine, everyday negotiations around the quality of services. In the first phase of our fieldwork, we found that physical boundaries between UACs and regularised UACs are often blurred, and residents continue to face substandard infrastructure and service provision despite regularisation. With service improvements no longer a clear benefit of improved tenure, residents appear to have moved away from clientelist politics to more agency-based, often individualistic, articulations of claiming and reclaiming urban space, of which investment in housing is a critical marker. The uneven nature of development and service provision that we observed across Mandawali and Lalita Park demonstrates the temporality and incrementality of UACs, an ‘always in the making’ condition characteristic of peripheral settlements (Caldeira, 2017, p. 5) (see Figures 1–4).

Citizen Agency and the Emerging Politics of Unauthorised Colonies

Consistent with the literature on state–citizen relations, residents in our sites use modes of claims making that not only involve collectivising through protests but also more traditional methods of taking grievances to elected representatives and using networks of jaan pehchaan (social networks) to push forth demands for services and infrastructure improvements (Heller et al., 2015; Ramakrishnan, 2016). While such negotiations have been typically characterised in terms of ‘patron-clientelism’ or vote-bank politics, recent perspectives have introduced the concept of co-production to theorise state–citizen alliances with regard to a range of governance concerns, including, but not limited to, service provision (Bovaird, 2007). Another strand of literature has examined these processes under the rubric of ‘boundary spanning’, looking at the role of individuals who work at the boundaries of their respective organisations (in this case, primarily state agencies and community-led organisations) who impact urban regeneration by creating links, building trust within networks and improving coordination around decision-making and the implementation of complex public issues (Meerkerk et al., 2015; Meerkerk & Edelenbos, 2016).

In our sites, we find a subtle shift in urban politics, with residents being less dependent on patronage from elected politicians and political parties. A relationship of avoidance between the Member of Legislative Assembly (MLA) representing the Aam Aadmi Party (AAP)-led state government and the municipal councillor who represents the Bharatiya Janata Party (BJP)-led municipal corporation has made it hard to navigate the already complex governance structure in Delhi. With the emergence of AAP in the city’s political landscape, the typical party worker has given way to armies of local ‘volunteers’ who are embedded in both the community and the political party. In Mandawali, we found that AAP volunteers resolved grievances, particularly helping with access to primary health facilities, pensions and other entitlements. They also helped pilot the mohalla sabha model that involves public meetings in the settlement, where residents can air grievances and get responses in face-to-face interactions with officials and where budgets also get sanctioned for infrastructure improvements. Lama-Rewal (2019) has referred to this phenomenon as the ‘semi-institutionalization of MLA representatives’ (p. 185). Apart from the party volunteers, we find that non-governmental organisations (NGOs) have also filled the gaps, either as extensions of the state or by providing services that improve connections and interfaces with the state.

Consonant with the more ‘middle-class’ status of UACs, however, we find a different form of collectivisation that is prominent. RWAs, empowered by the Government of the National Territory of Delhi (GNCTD’s) Bhagidari 5 civic participation scheme that was flagged off in 2000, have been the fulcrum of organising initiatives that address aspirational demands such as beautification, park improvements, street lighting and the gating of colonies to improve security. For example, the RWA in Krishna Puri, Mandawali, collected funds from residents to organise a ‘cleaning drive’ to convert a garbage dump site into a chaupal—a seating place replete with green landscape, a water cooler and benches, where residents could gather and socialise.

More importantly, RWAs were designated as intermediaries in the process of regularising UACs as laid down by the GNCTD in 2008 and were ‘responsible for coordination, preparation of layout plans, and for liaison with the concerned agency in respect of various issues pertaining to the regularization process’ (DDA, 2008a, p. 7, cited in Sheikh & Banda 2016). 6 In offering a space for the communities, as represented by RWAs, to express their aspirations and participate, the 2008 regularisation framework made it possible for residents and local authorities to co-produce urban regeneration. The slow and uneven rollout of the regularisation process effectively restricted RWA’s work to meeting aspirations for beautification, security and amenities. Since demands for settlement-level regularisation and services upgrades did not yield immediate results, UAC residents focused on plot-level upgrades and more individualistic articulations about citizenship, expressed through a desire for tenure security, housing improvements and rising real estate values.

We find, therefore, that while representation via elected politicians and volunteers helps residents’ to access basic services and state entitlements, more middle-class aspirations linked to home ownership and real estate values are expressed—though not quite met—through collectives such as the RWA, as Kamath and Vijaybaskar (2009) have also found. Thus, while addressing grievance calls for the state to step in, the rise of middle-class aspirations draws attention to a third critical arena—the market—which is often overlooked in this political landscape. Transversal logics, to borrow from Caldeira (2017), appear, therefore, not only in the interaction with the state and authorities but also with the market when it comes to modes of consumption and credit that produce peripheral spaces like the UAC.

Housing Finance Landscape in Unauthorised Colonies

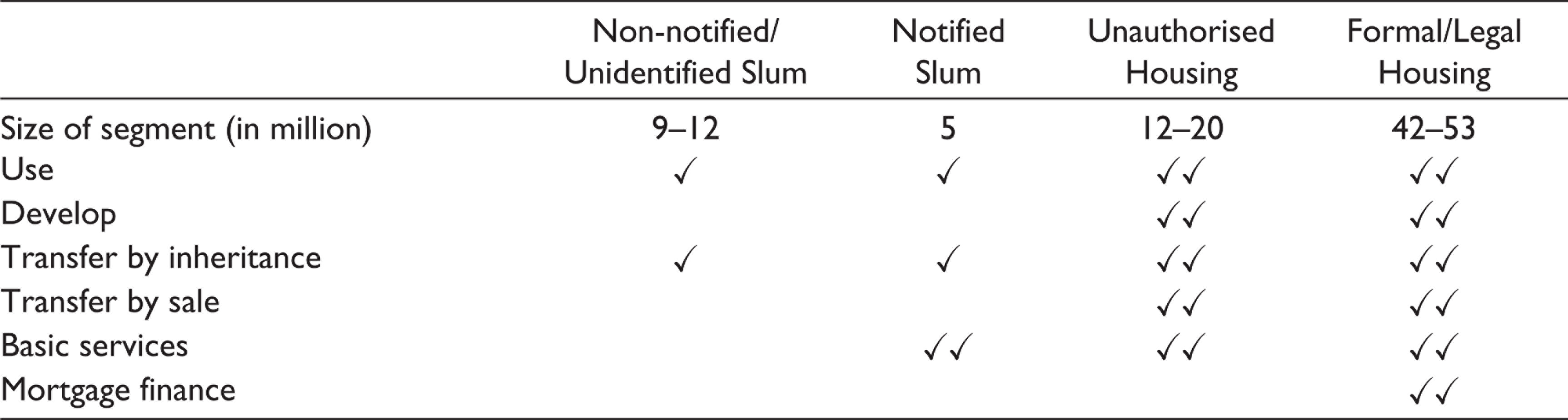

This section elaborates on the ways in which market actors engage with financing landowners in semi-legal settlements like UACs for home improvement and construction. While UACs are more tenure secure than jhuggi-jhopri clusters (see CPR, 2015), landowners are unable to access mortgage finance—the cheapest form of home loan, with income tax benefits—for buying and building homes because they are unable to offer property as collateral. To do this, property would have to be recognised as a financial asset within the formal regulation and revenue system, requiring approved layout plans of the settlement, plot registration and building plan approval for the planned construction. Additionally, the borrower would need to prove his/her ability to repay these loans through a documented credit history established through proofs of income. Indeed, mortgage housing finance, which took off in India in the 1990s, has primarily targeted those working in the formal sector, who can demonstrate proof of adequate income to repay loans, and has steered clear of the lending to those without secure tenure and formal incomes. Nor did they need to include this sector to make profits, as there was a large untapped demand from high-income households buying homes in a growing real estate market. Loans to lower-income households were considered highly risky, likely to result in non-performing assets (NPAs) and uneven payback patterns (see Table 1 for insights on how borrowers are categorised by risk).

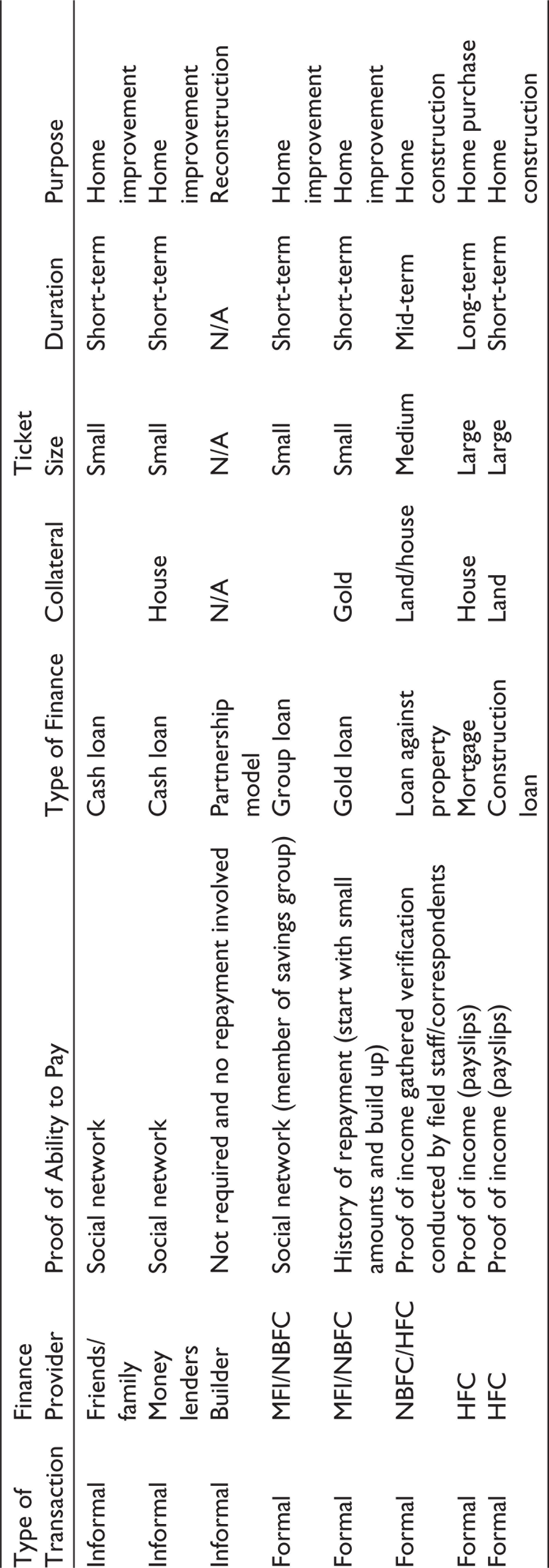

All of these pose significant challenges for residents of UACs. Neither do they have clear housing titles, since these properties are not formally approved and land not registered in revenue records, nor can most residents demonstrate regular and adequate income with documentary proof since they work in the informal sector (see Table 2 to understand how property rights vary across types of settlements). Denied formal finance, households engaged in autoconstruction across the Global South have traditionally combined savings with informal credit from friends, relatives and moneylenders to finance home construction. These lenders belong to the same social network, and trust has played a critical role in enabling this finance (Ferguson & Smets, 2010). However, we find that autoconstruction in UACs is financed by a variety of market actors, who use creative strategies and workarounds to give loans while reducing risks, maintaining trust and ensuring regulatory compliance. Table 3 compiled the housing finance practices we observed in UACs amidst the broadly available options.

Categories of Risk Among Borrowers in Housing Finance

Property Rights and Market Size of Different Types of Housing Settlements

In Delhi’s UACs, the ‘building collaboration’ model is a popular solution, emerging from the lack of formal finance in settlements where land costs and housing demands are rising (Khan, 2019). In this, the homeowner provides the plot, and the builder puts in the money (in cash) to construct several floors. Once completed, the built-up space is shared in a predetermined ratio. In Lalita Park, builders told us that they handed three floors to the landowner, including the ground floor that could be rented out for commercial use, and sold one floor for profit. This model is also prevalent in planned colonies in Delhi, where inherited properties that are hard to subdivide are handed to builders for development. While builders do determine whether landowners have paperwork to establish their claims to the land as owners or users, they are not constrained by the need for a registered property title. Usually, it is sufficient to have a General Power of Attorney (GPA), a system that bypasses the payment of registration charges and is a common mode of transaction that enables homeowners to avoid high registration charges. The partnership model is a completely informal commercial agreement between landowners and builders, usually connected via referrals from trusted people within the owner’s social network. Risk assessment is a function of mutual trust and the expected profits estimated on the basis of the business experience of the builder.

Despite regulatory barriers, the impetus for formal finance to enter peripheral spaces grew in the 2000s. At this time, when the Asian and Latin American financial crises had dampened the enthusiasm of multinational investors who had bet on middle-class consumers in emerging economies, marketing experts began to advocate a foray into the ‘bottom of the pyramid’, positioning it as inclusive capitalism, a way for businesses to lift people out of poverty while making profits. Using a logic of smaller margins and larger numbers, they pushed for innovations in technology, business models and management practices in order to tap into a hitherto unacknowledged market (Prahlad, 2010).

Type of Finance Available in UACs Within the Wider Spectrum of Housing Finance

Financial institutions too began to find ways of expanding their services to low-income customers (Deb et al., 2010), and about 62 per cent of the affordable housing finance is directed at autoconstruction (Das et al., 2018). Over time, a landscape of differentiated practices has emerged in which various institutions and actors, with specific histories and mindsets, have found ways to speculate on a market hitherto considered risky despite the stringent regulatory frameworks.

Over the 2000s, microfinance institutions (MFIs) have worked to extend formal finance to low-income customers by adding home improvement finance to their core portfolio of micro-enterprise lending, while applying existing methods with little or no modifications. The ethos of lending to low-income households also fit well with the development sector mindset of MFIs, many of whom were NGOs to begin with (Ferguson & Smets, 2010; Mitlin, 2007). Post the microfinance crash in late 2010, the housing finance industry went through a restructuring. Only two types of financial institutions were permitted to disburse housing finance: non-banking finance companies (NBFC) regulated by the Reserve Bank of India and housing finance companies (HFC), which are essentially a specialised NBFC licensed under the National Housing Bank (NHB).

The affordable housing finance market was systematically developed by the efforts of a few pioneering companies like Dewan Housing Finance Ltd. and Gruh Housing Finance that began to customise tools for low-income borrowers who worked in the informal economy, like small business owners and daily wage workers (Desai, 2014). MFIs continued to address this demand after getting licensed as NBFCs/HFCs. Moreover, efforts to build a field-based credit assessment model were made by Micro Housing Finance Company, which was incubated by the Monitor Inclusive Markets team with the intention to grow the demand side of the affordable housing market. The NHB’s role in refinancing HFCs and the policy shift towards affordable housing has also supported the growth of this segment of housing finance (Das et al., 2018). Data trends indicate that the role of newly formed NBFCs and HFCs in financing the affordable housing segment has increased as compared to those that branched off from traditional banks. Moreover, new HFCs are targeting self-employed customers and those with informal incomes. 7

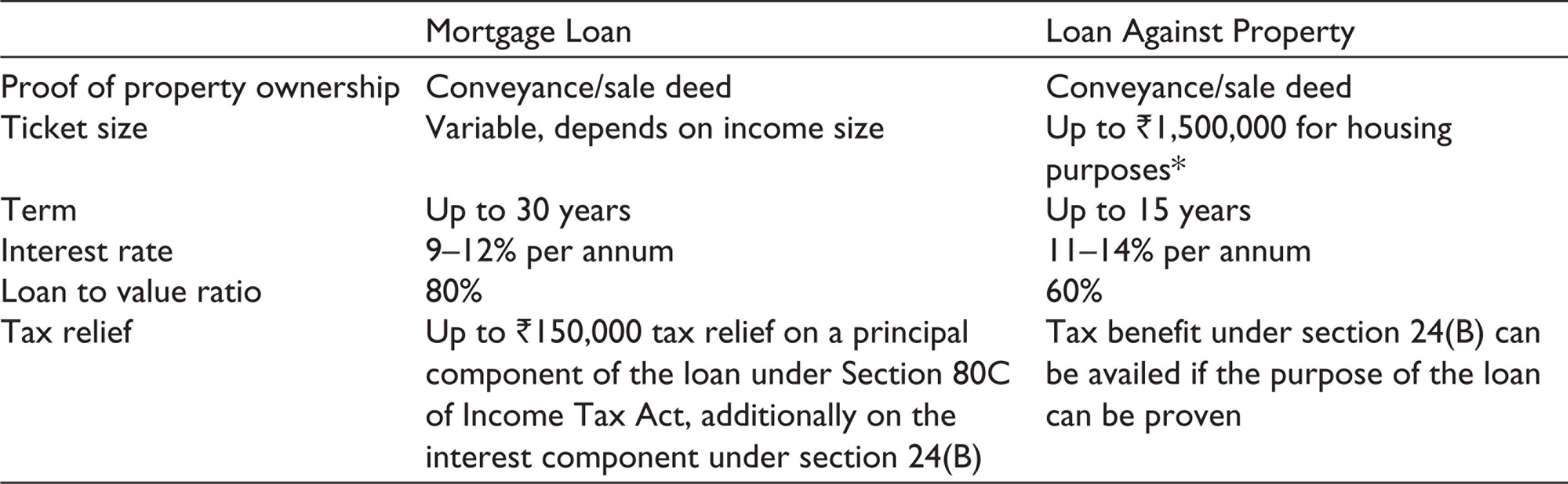

In our field sites, we found that home improvement needs that cost up to ₹50,000, such as installing submersible water pumps, adding a toilet and plastering and tiling exterior facades are often financed through microfinance loans and gold loans, where property is not used as collateral. Property redevelopment is financed through a mechanism called the Loan Against Property (LAP), a product not meant specifically for housing, but which uses the land/house as security to finance anything. Essentially, a LAP is a personal loan widely used to finance businesses or tide over financial crises. They are perceived as higher-risk loans and are offered at higher interest rates. For a comparison of LAPs with mortgage loans, see Table 4.

Comparison of Mortgage Loans and Loans Against Property (LAPs)

In our interactions with HFCs, NBFCs and small finance banks (SFBs), we found that LAPs were being given out in regularised UACs and in those UACs where provisional regularisation certificates had been issued against a sales or conveyance deed. 8 These organisations were, in general, comfortable lending to properties that demonstrated a complete chain of titles up till the present buyer for the past 13 years. Legal experts were hired to conduct this due diligence. LAPs were not given out for properties transacted under the GPA. 9 An HFC branch manager we interviewed indicated that LAP ticket sizes were roughly in the ₹1,100,000–1,200,00 ticket size, for constructing a building 3–4 floors (15 metres) high on an average plot size of 50 sq. m. Property dealers at Lalita Park indicated that LAPs were given at monthly interest rates of upwards of 8.5 per cent, tending to be higher for self-employed applicants. While salaried applicants got loans quite easily, the incomes of self-employed workers were harder to assess. We found that some HFCs were willing to go an extra mile to establish the creditworthiness of those self-employed or with informal incomes, while working strictly within the regulatory constraints for assessing property titles.

The ‘Boundary Work’ of Financial Institutions

Given the experience of MFCs and group-lending schemes, HFCs entering the low-income, semi-informal housing finance segment found innovative workarounds to serve these customers, particularly to provide proof of income and expenditure that met the credit assessment standards of regulators like the NHB. HFC managers identified the need to invest in comprehensive and innovative risk assessment procedures as well as rigorous and regular training of loan officers at the front end of this procedure. The focus shifted from documents to people. Assessing stability (through home visits, interviews with neighbours and banking history) and understanding source of income (through visiting businesses, understanding business models and triangulating estimates by interviewing suppliers and competitions) became the preferred methods. HFCs also began to build databases of likely incomes of informal sector customers by occupation to help create rapid assessment templates (Deb et al., 2010). Two aspects of their operations are notable: first, the role of trust and judgement in income assessments, which contrasts with the culture of precision and meticulous documentation that is the norm in the finance world and, second, the importance of social embeddedness in carrying out these estimations.

The East Delhi branch manager of an HFC, whose origins were in an NGO working on women’s economic empowerment, told us that the crux of lending to the informal segment was assessing the neeyat or character of the applicant to determine their intent to repay the loan. He also drew a direct link between the ‘ground-level’ work of his organisation and their ability to trust people to repay loans. Part of their standard operating procedure for assessing income, for instance, was that field staff met women from the applicants’ households. He felt that women offered a more honest assessment of expenses, which helped them triangulate incomes, which were often over-reported by loan applicants.

This idea of neeyat appears in different ways, sometimes signalling an intent to trust, like above and, at other times, reflecting the prejudices of the officials. Prejudices aside, assessing neeyat requires deep customer engagement that is challenging and costly for large retail organisations. For instance, a senior manager in an NBFC, which is affiliated with a large retail bank, characterised the higher default rates for loans in North India to the ‘brashness’ of people of this region. ‘Handling these loans require a special skill. Even the will is not there’, she told us, describing how her colleagues would quickly pull out files of people in formal colonies with proper tax returns and income slips, but they would hesitate to go through the files of those in a UAC, as the documentation was messy, requiring more elaborate procedures for background checks. ‘We will need to have a full-time team for these loans in the future so that they get the attention they need’, she added.

The groundwork of income assessment is possible because of the social embeddedness, experience and skills of the field agents—actors who are redundant in formal sector lending where documents suffice. HFCs tapping this market for the first time rely on ‘business correspondents’ working with the microfinance sector, who have an intimate understanding of these communities.

Suneeta, 10 who works as a field agent in an HFC (with NGO origins), brings her experience of working in the development sector to her current work. To find customers, she taps into the jaan pehchaan networks and the goodwill associated with the bank’s parent NGO. Her detailed knowledge of informal work and workers’ lives and the similarity of her class position to the loan applicants are also key factors. ‘Itne time se kaam kar rahe hain, toh itna toh pata chal hi jaata hain (I have been working for so long, I simply know this)’, she tells us when we ask her how she can ascertain their incomes. Further, she urges potential clients to reveal their real incomes by building trust through multiple personal conversations and by explaining details of how the housing finance schemes work.

Field agents document this kind of informally gathered tacit information through a personal detail verification form, which includes information about each household member’s duration of stay in the city, income, expenditure, asset ownership and lifestyle indicators in a household roster. Strategies deployed by field agents include home visits and conversations with neighbours, visits to employers in the case of salaried individuals who do not have salary slips, verifying cash registers and tracking stocks and flows of goods for those who own businesses. The HFC branch manager in East Delhi told us that if a rickshaw puller came to the branch to apply for a loan, he would ask him to empty his pockets to verify the daily income he had cited in his application form. Then, he would extrapolate, with adequate checks and balances, to determine his monthly income and repayment capacity. Another field agent working for a different HFC told us that he checked the wholesale transactions of fast-moving products like milk and bread to determine the income of a local grocer. These processes of verification are time consuming, requiring a well-established network of skilled field personnel working on the ground.

Reminiscent of Lamont’s notion of ‘boundary work’, which involves ‘constructing a sense of self-worth by interpreting differences between themselves and others’ (Pande, 2009, p. 157), we find that staff in financial institutions that emerge from NGOs and collectivising movements construct and articulate their work as different from corporatised HFCs and NBFCs, often describing it as ‘helping people’. For instance, we heard articulations like ‘hum chahte hain ki beheno ke paas suvidhaaen honi chahiye (we want our members to get the services)’ and ‘humein duaaien milti hain (we get blessings from people)’. They also refer to their customers as ‘members’, ‘saathi’ (partners) and ‘behene’ (sisters) and represent their work as a response to community demands and in the community’s interest.

Moreover, we also found that these financial institutions took on the role and positions of the state in their work. For example, MFIs often leverage their community to extend state services, for example, by lending for water pumps. Multiple HFCs we interacted with spoke about their success in enabling their customers to access the interest subsidies provided under the credit-linked subsidy component of the Pradhan Mantri Awas Yojana (PMAY, a national housing scheme), which brings down monthly EMIs and eases the financial burden on borrowers. In their narration, they did not talk about this as a business strategy; instead, they perceived themselves as enablers of an important government scheme.

Boundary Assertions, Erasures and Crossings

In Delhi’s UACs, post facto regularisation by the state has resulted in an entanglement of citizens, investors and financiers as they find ways to valorise land. They do these using transversal logics. Homeowners follow rules selectively to autoconstruct homes, landowners and builders co-develop plots of land in the absence of formal finance and financiers find creative ways to lend to those whose creditworthiness is hard to document by the stringent standards laid down by regulators of housing finance.

The concept of boundaries offers a method to disentangle and understand the complex interactions between various actors that represent citizens, the state and the market that we have described earlier. We find boundaries at different locations in the state–citizen–market matrix, but we also find internal ones. In assessing how actors assert, erase and cross these boundaries, we explore a new vocabulary to describe an emerging urban politics in India.

Manoeuvres Within Bounded Regulatory Regimes

Boundaries between state–citizen, market–citizen and state–market are asserted through regulatory regimes, in this case, mainly concerned with land and finance. While regularised UACs and UACs often experience similar levels of services and blurring of spatial boundaries, we also find that notions of land tenure as defined by spatial regulatory regimes do not quite neatly map onto financial regulatory regimes. In fact, the word ‘regularised’ was used very differently by RWAs and residents compared to the representations of financial institutions. While for the former it was used in the sense of a settlement’s status vis-à-vis Delhi’s planning landscape and access (or lack thereof) to formal credit, for the latter it implied the ability to lend in terms of the regulations laid down by the NHB (in case of HFCs) and the Reserve Bank of India (in case of NBFCs).

Regulatory regimes set by government organisations like the NHB and the Reserve Bank of India are stringently followed by financial institutions, that is, in state–market relations. For instance, mortgages cannot be offered unless property titles are clear. However, land regulations are deftly navigated–and even ignored—by market actors such as brokers, builders and individual landowners to enable autoconstruction. These actors understand that the regularisation of UACs, that is, a tenure improvement in the land regulation system, opens the door to the registration of individual plots and enables the creation of sale and conveyance deeds, which, in turn, act as title documentation to unlock housing and construction finance at affordable rates. In contrast, many landowners in regularised UACs continue to use GPA transactions, avoid registering plots and choose to self-finance or rely on informal finance. This could be because high registration costs are more of a disincentive than the relative affordability of a housing loan or because the expected profits from speculative development are high enough to cover the costs of informal finance.

In the context of state–citizen relations, therefore, the boundaries between the regulatory regimes for land and finance are actively navigated, sometimes ignored and erased (like in the partnership model where neither matter) and, at other times, asserted through ongoing efforts at regularisation in the expectation of tenure improvement. While the role of RWAs as boundary spanners in the regularisation process has been somewhat reduced by the recent use of technology for mapping settlement and plot boundaries, in recent fieldwork, we find that a small set of powerful residents play the roles of RWA office bearers, property brokers and party representatives. Thus, while boundaries may be maintained or erased, the actors who control how these boundaries operate on the ground likely remain the same.

Market actors in the space of housing finance also navigate their regulatory landscape in distinct ways. Within the rigid regulatory structures that dictate the burdens of proof on banks and borrowers for specific financial products, as well as the kind of land tenure required for financial institutions to operate, lenders adopt creative strategies to document informal incomes. Hence, they act as boundary spanners at the state–market interface to help a new segment of homeowners meet their aspirations for housing upgrades through autoconstruction. The organisational background and culture of the financial institution influences their perceptions about customers as well as their operations and processes. Assessing informal incomes requires a hands-on approach and embeddedness within communities, which positions HFCs with origins in the not-for-profit sector at an advantage.

Moreover, the conversion of tacit knowledge—gained informally through guesswork and back-of-the-envelope calculations by field agents—into formal documents like verification forms is also a key act of boundary crossing, which drives the entry of HFCs into the bottom of the housing finance market pyramid. While standardisation and digitisation could bring down the costs and time involved in building credit histories, at this time, embedded fieldworkers remain the backbone of housing finance for this segment. This is not different from the dependence of UACs on intermediation and representation by embedded actors like party representatives for service provision. This is a reminder that despite market innovation and political shifts, social boundaries tend to remain intact in these semi-legal urban settlements.

Completing the circle, we also recognise that the state, with its powers of regulation, is a less visible but important partner in market–citizen interactions. By not building formal housing and by charging fees for regularisation, states are active participants in creating settlements like Delhi’s UACs and Maharashtra’s gunthewadis (informal settlements that do not meet the building laws; see Bhide, 2014). The modes through which post facto regularisation of these settlements have taken place, however, indicate a shift of responsibility away from the state to non-state actors like RWAs (Zimmer, 2012).

The Strategic Deployment of Individual and Collective Identities

In Delhi’s UACs, individual aspirations linked to home improvement coexist with collective aspirations in the context of urban regeneration. We find that there is a shift away from older clientelistic modes of mobilisation, and the role of political intermediation and boundary spanning seems to now fall on collectives like RWAs, on party volunteers and even on market actors such as brokers, builders and lenders. Within communities, individual and collective identities are strategically deployed—and blurred—as a matter of choice or in response to regulation.

While RWAs were placed formally at the cusp of the state–citizen boundary in the implementation process outlined for regularisation, on the ground, we find them to be effective boundary spanners in meeting community aspirations related to beautification, security and service improvements. We find a gradation of individual aspirations for housing improvement, ranging from small upgrades like adding toilets and water pumps to adding rooms and floors and constructing, redeveloping, purchasing plots and floors. However, these same individuals often become part of collectives like political parties, RWAs and youth associations to express and negotiate community-based aspirations like better parks and better sanitation. In recent times, individual AAP volunteers have leveraged their embeddedness in the party and community to address grievances and organise mohalla sabhas. While RWAs and party volunteers in Delhi have a relationship of mistrust and avoidance, in their individual capacities as residents, party volunteers, RWA members, brokers and builders are all instrumental in using transversal logics to enable autoconstruction and service improvements in UACs.

The manoeuvring between individual and collective identities was also evident in the context of home improvement finance. Borrowers leveraged collective identities (e.g., using group loans) for home improvement needs. In initiatives led by a prominent NGO working in informal settlements in East Delhi, loans through Joint Group Liability (similar to loans made to self-help groups) were given out to groups of women who relied on networks of trust and familiarity (jaan pehchaan) to avail loans by forming groups and sharing the liability. ‘These women have known each other for as long as twenty-five years or more and have been together through thick and thin’, a project coordinator explained.

Conclusion

How does an analysis of boundaries (and the work that boundaries do) contribute to our understanding of citizenship and urban politics in the burgeoning cities of the Global South? Cities like Delhi endeavour to become planned world-class utopias, but in reality, they are caught in an unending cycle of ‘peripheral urbanisation’, transforming incrementally through the tactics of a multitude of state and private actors on the ground. In the semi-legal UACs of Delhi, residents expected tenure regularisation, a state-led urban regeneration project, to result in infrastructure and service upgrades, but they were most motivated by the legal titles, increase in property values and access to formal finance that would make property redevelopment easier.

The case demonstrates that the boundaries created by regulatory categories do not necessarily coincide with those shaped by spatial and social factors. This is seen in how regularised and unauthorised portions of a settlement blend into each other without substantively different levels of service or in how various kinds of settlements experience incremental house-building activity in similar ways. Caldeira (2017) explains this through ‘transversal logics’ rather than through the concept of informality. She points out that categories like formal/informal and regular/irregular are not binary, but they are shifting and unstable. As we have found, this is partly not only because regulatory frameworks evolve but also because different sets of regulatory frameworks use unique vocabularies and remain bounded. In the absence of boundary crossings between regulatory regimes, it is more difficult to resolve ambiguities.

An examination of boundaries in the processes of urban regeneration on the ground revealed a strategic deployment of individual and collective identities. Homeowners wore multiple hats: as brokers, RWA members and political party volunteers. RWAs—collectives of residents formally registered and empowered by the state—emerged as boundary-spanning actors to enable regularisation. Yet, aspirations related to home improvement and property redevelopment were acted upon by individual landowners, regardless of regularisation. Thus, boundary crossings are enabled when individual aspirations are met through collective agency, as in the case of group loans, or when market-based financial organisations take on the attributes of the state or deploy the state’s discourse to further their activities.

While the state is successful in asserting boundaries through regulatory regimes of land and finance, the boundedness and inflexibility of these regulatory regimes hold residents back from meeting their aspirations for a better quality of life. However, the strategic assertion and dissolution of boundaries by various actors create opportunities for peripheral urbanisation. Landowners used transversal logics to selectively follow or violate development control rules in their autoconstruction projects. Having been denied formal finance, they partnered with builders to finance property redevelopment and thus transformed settlements over time into dense, mixed-use and bustling neighbourhoods.

This article highlights the work of varied actors in the housing finance landscape who span and cross the boundaries between the state, citizen and market to finance autoconstruction and affordable housing. Where a land title was available, but income was informal, financial institutions leveraged tacit knowledge mechanisms to creatively document informal incomes and establish creditworthiness for landowners applying for loans against property. Caldeira’s (2017) observations that peripheral urbanisation takes place not within the logic of planning, but in interaction with it can be loosely applied in this context, where specific regulatory regimes unlock housing finance for previously unserved customers, even without going through the formal planning processes of building plan approvals. These boundary crossings by early movers pave the way to embed these processes into institutional systems and memories, as the impetus to tap into the large unserved market of informal borrowers acquires momentum.

The role of aspiration is key in situations of peripheral urbanisation, as it is this case, as ‘the processes of transformation of peripheral areas offer a model of social mobility, as they become the material embodiments of notions of progress’ (Caldeira, 2017, p. 6). Thus, the expectation that these spaces will improve and one day look like wealthier parts of the city drives the changes today, and the landscapes are ‘continuously remodelled’ to meet these aspirations (ibid). We argue that the home/property becomes the conducive ‘action space’ for residents to meet individualistic aspirations even as collective demands for improvements are also being made in parallel, but with far lower chances of timely intervention. We also contend that the shift to individual aspirations via housing improvements enables residents to depend less on a single form of legality/regulation (of land) that has been elusive for long and expand their options to rely on another form of legality/regulation, in this case, financial.

New strategies and coalitions are likely to emerge in this space as financial organisations continue to experiment with new financial offerings for quasi-legal land tenure situations. At the same time, residents will continue to build incrementally and redevelop their land, working through networks of credit to continuously improve their homes even as they engage in collective modes of bargaining to upgrade community infrastructure, services and resources. In this context, the state’s ongoing efforts to expedite land titling in UACs are a welcome move. It is possible to interpret the subtle shift in the state’s narrative from regularisation to ‘redevelopment’ as an acceptance of the transversal logics of peripheral urbanisation. Conversely, it might signal the imagination of a fresh urban regeneration project to tame the messy realities of peripheral urbanisation and inscribe it within an idiom of planned development. Regardless of the interpretation, it is clear that the assertion, dissolution and spanning of multiple boundaries—regulatory, individual–collective, state–citizen, citizen–market and state–market—will continue to reshape Delhi’s peripheral landscapes through everyday action on the ground.

Footnotes

Acknowledgements

The authors gratefully acknowledge the contributions of colleagues Persis Taraporevala and Asaf Ali Lone, as well as interns Anwesha Mishra, Ashwathy Anand, Indrashish Chakraborty, Manasvi Sharma, Nooreen Fatima, Richa Sinha, Sebastian Lucek, Shruti Yerramilli, Swetha Balachandran and Venkat Sai Oruganti, who were engaged in the larger research project at various stages. We acknowledge the generosity of all our informants who opened up their homes and offices to us as well as the insightful comments of two anonymous reviewers.

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

This article draws upon work conducted by the authors between 2015 and 2019 as part of research on boundary spanning and urban regeneration, funded by grants from the Indian Council of Social Science Research, New Delhi, and the IHS, Rotterdam, Netherlands.