Abstract

In this paper, we argue that current research on carbon regulation neglects the complex interactions of institutional norms and market behaviour that characterise responses to regulatory change. We draw on empirical research undertaken with English housebuilders and housing market stakeholders to examine how transitional pathways towards a low-carbon housing future might be advanced and consider the implications of such for carbon regulation and low-carbon economies. Our core proposition is that carbon regulation research can no longer ignore the impact of institutionally constituted market behaviour in shaping pathways and transitions towards low-carbon futures.

Introduction

The growth of global concern over the anthropogenic impacts of climate change has done much to narrow the focus of environmental concern from the broad idealism of sustainable development to a preoccupation with the management of carbon cycles. The challenge that lies ahead is a significant one. According to Kennedy and Sgouridis (2011) addressing planetary CO2 limits (stabilisation of 350 parts per million) will require the developed world to cut carbon emissions by around 95%. Whilst there is evidence of a slowing in overall global emissions (DECC, 2016) certain regions remain dominant sources of CO2 production and have, as a result, had to review the efficacy of interventions centred on carbon efficiency. In the latest update published by the EUJRC (2015), the EU was found to account for 10% of global outputs with the US and China accounting for 15 and 30%, respectively. The main focus of attention within these regions has, unsurprisingly, been on the built environment (Bulkeley et al., 2010; Carter et al., 2015; Chavez and Ramaswami, 2011; Gill et al., 2007; Hodson and Marvin, 2013). Rydin (2013) attributes this not only to the potential impact that decisions regarding design and construction of individuals buildings might have on carbon reduction, but also the role played by urban layout and associated travel choices.

In response, a persuasive body of literature has emerged which has attempted to indicate the contribution that specific modes of intervention might achieve within the built environment (see, e.g. Dhakal, 2010; Dhakal and Betsill, 2007; Feng et al., 2013; Metz et al., 2007; Pataki et al., 2006; Shukla et al., 2008). This work has contributed to the modelling of carbon futures through the use of scenario-based tools and has identified a range of technical solutions that might ease the carbon crisis. In parallel, state-level actors have advanced a plethora of regulatory and policy-based mechanisms geared towards meeting ambitious reduction targets to be delivered by non-state actors (Bailey and Wilson, 2009; Geels, 2014). To a certain extent, these trends represent a positive move towards addressing climatic impacts, yet they also raise important questions about realisation and effectiveness. We argue that one of the problems of achieving a low-carbon economy is that much of the language of carbon reduction is couched in terms of ‘potential’ and ‘expectation’. Whilst scenario-based approaches and technical solutions tell us what might be possible, they do not necessarily indicate how they will be realised in practice. Similarly, state responses based on mobilising this knowledge do not always acknowledge the complexities and realities of non-state actors, particularly those that are market facing.

One of the key challenges facing market-based actors in the built environment is that they are increasingly being expected to operate within an uncertain institutional setting characterised by the emergence of hybrid forms of governance. Whilst attempts by the state to focus reforms and targets around particular sectors or institutional pathways can be seen as characteristic of what some authors have referred to as eco-state restructuring (Goodchild and Walshaw, 2011; While et al., 2010), it can also be argued that an expectation that downstream actors will deliver market viable innovation retains much of the socio-technical optimism enshrined in ecological modernisation (Huber, 1982; Janicke, 1984; Jänicke, 1986; Simonis, 1988). Here, despite the presence of a harder-edged form of regulatory control, there is an assumption that non-state actors can achieve outcomes that are compatible both for the environment and the economy. This places such actors in a challenging position. Whilst on the one hand they are being co-opted into new institutional pathways with clear behavioural limits, they are also being positioned as the drivers of innovation. In this sense, their power in the low-carbon economy is being enhanced and constrained at the same time. If the shift towards low-carbon governance is to succeed, then this hybrid form of governance will need to overcome the criticism of blind idealism previously levelled at ecological modernisation (Hannigan, 1995; Janicke, 2008).

This challenge is likely to be acutely felt by the speculative 1 housebuilding industry. As buildings and their occupiers are notable contributors to global carbon emissions (Dhakal, 2009; Williams, 2012), housing markets have become one of several sectors targeted for regulatory attention. Approaches have become increasingly target centred and have attempted to achieve transformation though influencing building design and construction, occupational behaviour, energy generation and infrastructure provision (Glaeser and Kahn, 2010). However, due to the vulnerability and institutional complexity associated with housing markets (Adams et al., 2005), it is likely that housing market actors will find the transition to a low-carbon economy particularly challenging. Housing markets are inherently unstable, fragmented and subject to competing priorities surrounding functional utility, short- and long-term value and investment return (Pacione, 2013). As such, the ability of emerging regulation to deliver solutions that are compatible for both the environment and the market will require sensitivity towards the dynamic nature of institutional structures and processes.

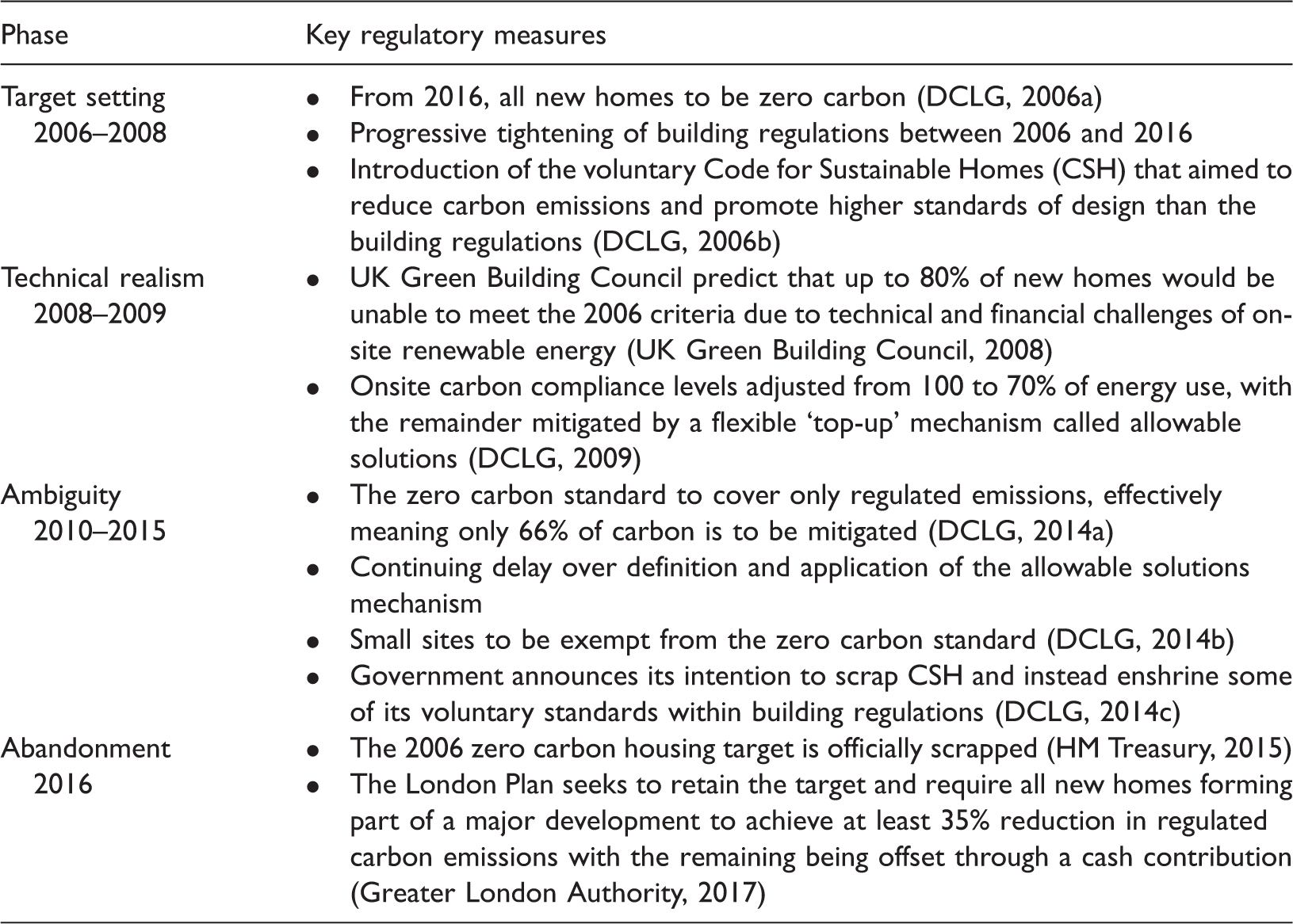

In this paper, we address these issues of institutional complexity. Our aim is to explore how institutionally constituted market behaviours shape pathways for transition towards low-carbon futures. By drawing on the English Government’s attempt to introduce a zero carbon target for new homes (ZCH), we seek to explore the extent to which market-facing actors within the built environment are adequately positioned to respond to increasing levels of state regulation centred on carbon reduction. The target, introduced by the Labour Government in 2006, aimed to ensure that all new homes would be carbon neutral by 2016 (DCLG, 2006a). It was supported by the Code for Sustainable Homes (CSH) (DCLG, 2006b) and later by an allowable solutions mechanism geared towards partial off-site monetary contributions (Zero Carbon Hub, 2011). Although the ZCH target was in line with the ambitions of both the 2008 UK Climate Change Act (CCA, 2008) and the more recent EU Directive on the Energy Performance of Buildings (European Commission, 2010), it was ultimately scrapped by the Conservative Government in 2015 (HM Treasury, 2015). Faced with concerns over feasibility from the outset (RICS, 2016), both the ZCH target and the supporting delivery apparatus were significantly modified over a 10-year period. We show these modifications in Table 2. We suggest this process of revision and ultimate retreat provides a rich opportunity to understand how gradual state-level policy repositioning impacted upon perceived opportunities and constraints for institutional reform in the housing market. This, in turn, affords us the opportunity to establish unique insights into the complexity of market behaviour in the low-carbon transition.

The paper is structured into seven sections. After the introduction, we problematise the low-carbon transition for market-led housing systems, drawing on the English example. We then consider those theoretical perspectives that assist us in understanding how a shift in approach may be achieved and present a novel analytical framework centred on three dominant lines of enquiry: clarity of expectation, change mobilisation and constraint management. We then outline the methodological approach taken and present the results structured around our three dominant lines of enquiry: clarity, change and constraint. Following this, we discuss the results and finally, we conclude with our contribution to knowledge and our recommendations for future regulatory interventions in market-led housing systems associated with carbon reduction.

A contested transition?

A number of authors have argued that a fundamental modification of conventional market operations will be required to achieve regulatory compliance for a zero carbon future. This is said to be necessary in the traditional practices and institutional pathways of a number of key market actors (Meadowcroft, 2005; Osmani and O’Reilly, 2009). Hodson and Marvin (2013) note that the drive for low-carbon futures within the housing sector is especially challenging due to the lack of pre-existing markets for zero carbon homes. Such markets, it is argued, will need to be actively constructed as a basis for creating new spaces of market demand, R&D activity, technological capability, consumer acceptance and financial feasibility. On this basis, some authors have suggested that tackling energy efficiency issues will require ‘a step change in the housing construction process’ (Osmani and O’Reilly, 2009: 4), with an entrepreneurial response by market actors necessary to create new market opportunities and make consumers amenable to a new generation of low-carbon homes (Hodson and Marvin, 2013). Yet, the inherently conservative and highly tuned business model of speculative housebuilders (Payne, 2013, 2015) raises questions over both the necessity and capacity of housebuilders to achieve a form of regulatory compliance that is both technically and commercially acceptable. Whilst the business model is typically dependent on product and process standardisation (Gibb, 1999; Nicol and Hooper, 1999; Payne, 2013), it has to date provided limited evidence of technical and material innovation (Adams and Payne, 2011; Ball, 1999; Payne and Barker, 2015).

Central to the problem faced by market-led housing systems is that the environment has historically been considered a zero-priced resource. This is largely because it has no supply cost and monetary values have not been placed on environmental goods in housing (Bhatti, 2001: 43). Although recent research has explored the way in which the housing market may ‘value’ the environmental resources it uses (Chay and Greenstone, 2005; Mell et al., 2016; Smith, 2010), mainly through attaching a positive value (Bolitzer and Netusil, 2000; Gibbons et al., 2014) and measuring a willingness to pay (Mell et al., 2016), these approaches are targeted towards the consumer and it is possible that unless market forces drive this change, housebuilders may find little reason to shift conventional production processes that seek the ready realisation of profit margins (Bhatti, 2001; Payne and Barker, 2015). This is likely to be particularly true of the speculative housebuilding industry which has, on the whole, traditionally adopted a conservative approach to environmental reforms. In this context, it is unclear whether speculative housebuilders will respond to policy expectations by seeking to absorb market-based incentives or tax reductions within existing institutional arrangements or whether they will explore technical innovation (Bhatti, 2001).

Institutional pressure points for the speculative housing market in a low-carbon economy.

The four phases of English zero carbon housing regulation.

Theorising a low-carbon transition

In order to explore the extent to which market-facing actors within the built environment are adequately positioned to respond to increasing levels of state regulation centred on carbon reduction, we consider those theoretical perspectives which assist in understanding how a shift in approach might be achieved. We suggest that whilst these approaches provide a useful entry point for unpacking pathways for change, the nature of housing market structures and processes means they are better understood in combination rather than isolation. As such we draw on those elements we find particularly persuasive in order to establish a thematic criteria for empirical analysis.

The process of achieving change within the environmental policy arena necessitates the acknowledgement of technical and material constraints and the links between these and society more generally (Elzen et al., 2004; Goodchild and Walshaw, 2011; Kemp et al., 2007). These socio-technical relationships have been the subject of a growing body of literature devoted to advancing varying forms of transition management theory (Berkhout et al., 2004; Rotmans et al., 2001). Central to transition management theory is the recognition that understanding change requires a focus upon not only policy goals but upon socio-economic, political and cultural complexity (Wilson, 2007). According to Geels (2010), this is necessary due to the fact that existing systems (such as those related to housing, energy and transport) display lock-in mechanisms related to system support (favourable regulatory or subsidy mechanisms), existing investments, dominant values and priorities and ultimately, behaviour. Overcoming the resistance of these sectoral systems is hence, often an on-going and dynamic process.

One of the most dominant perspectives to emerge within transition management theory is the multilevel perspective (MLP) (Geels, 2004; Geels and Schot, 2007; Rip and Kemp, 1998). This approach suggests that transitions from one state to another (also referred to as regime shifts) come about through the interaction of three overlapping innovation routes. These levels are defined as niches (the focal point of radical innovation), socio-technical regimes (which accommodate established practices and sets of rules) and finally, the landscape (the exogenous level) (Geels, 2014; Killip, 2013). Typically, these levels map on to micro, meso and macro scales (Geels, 2004; Killip, 2013). The manner in which transitions are achieved within this approach can vary. Where significant alterations occur at the landscape level (war, destabilisation of government, demographic change) dramatic forms of transition can take place. More commonly however, the process of transition is both incremental and experimental. As such, transitions are more normally dependent on a more fluid linkage between niche and regime with a framing role played by the landscape. Geels (2014) describes this as a process whereby niche-level innovations build up momentum using approaches varying from social learning to price signals. This momentum when accompanied by pressure at the landscape level provides the opportunity for regime destabilisation and the breakthrough of socio-technical innovation. Whilst the effectiveness of the regime is often characterised by the search for pathways of influence (Killip, 2013), the effectiveness of landscape pressure will depend to a certain extent on the degree of articulation. Smith et al. (2005), for example, have noted that successful forms of pressure will require not only a coherent focus but will also need to be sufficiently well articulated to promote a response by the regime. This is a key area of contestation for the English zero-carbon housing project where target definition and governmental coordination have become a source of debate.

Despite an initial emphasis within transition management theory on the dynamics of social and technical interactions, recent critiques of the approach have pointed to a narrowing of emphasis which has tended to assert the potential of technical innovation over and above the opportunities and constraints afforded by social and economic realities (Bulkeley et al., 2014). Whilst this has led authors such as Meadowcroft (2009, 2011) and Hess (2014) to argue for the repoliticisation of transition management, others have called for greater recognition of spatial representation (Bridge et al., 2013), urban exchange (Hodson and Marvin, 2012), social justice (Newell and Mulvaney, 2008) and experimentation (Evans and Karvonen, 2013).

The significance of technical innovation has certainly become a dominant feature of much MLP-based research and has come to play a central role in narratives of climate change mitigation and adaptation (Kemp et al., 1998). Such perspectives frequently point to demonstration projects and schemes to highlight the potential of emerging technology in existence at the niche level. Goodchild and Walshaw (2011) have noted that this is particularly true of debates surrounding carbon-based innovations within the housebuilding industry. Examples alluded to include the Beddington Zero Energy Development developed by the Peabody Trust and the Hockerton earth sheltered scheme in Nottinghamshire. Such schemes are frequently presented as examples of the direction that mainstream housebuilding might head. It is arguable however, that an emphasis on the transformative potential of demonstration projects within the housebuilding industry is overstated. In most cases, the schemes pointed to by advocates of low-carbon housing are free of market constraints and standard regulatory practice. This presents significant challenges for integration by institutions operating at the level of the regime (Seyfang, 2010).

Two key responses to the primacy of the niche as a driver of technical innovation are of interest to the manner in which the MLP approach might be reframed to contribute to carbon transformation within the housebuilding sector. First, it is important to acknowledge that the niches hold the potential to transcend the straightjacket of technological provision and become the basis of knowledge brokerage and social adaptation (Bulkeley et al., 2014). In this sense, niches might be seen as social networks, often drawing on third sector experience, which operate on the margins of the mainstream. By adopting a fluid, and less delineated relationship with the regime, they may yield more positive results than can be adopted purely through promotion of new products and systems (Bos and Brown, 2012; Bulkeley and Broto, 2013). Second, there is limited understanding of how the sense of expectation associated with the niche can be combined with an appreciation of the complexity of finding pathways for regime breakthrough (Killip, 2013; Schot and Geels, 2008). Geels (2014), in particular, has argued for a revisionist perspective on MLP which calls for a greater level of exploration and understanding of both the regime and the nature of associated forms of resistance. His argument is centred on a concern that most transition scholars fail to pay sufficient attention to existing regimes and associated actors or ‘conceptualize regimes as monolithic barriers to be overcome’ (p. 23).

These perspectives may potentially serve to re-establish the utility of the MLP perspective in informing carbon transitions. However, we argue that in order that niche-level actors may adopt a greater role in steering social learning, we first need to appreciate the behavioural environment which exists at the regime level. Without an appreciation of the characteristics of the regime and the roles played by complexity and variation, it is unlikely that opportunities for social learning can be triggered. Due to the limited emphasis within the MLP approach on regime structures and processes, we suggest an ability to unpack low-carbon transitions within the housebuilding industry necessitates the consideration of additional yet complementary perspectives. To do this we draw on theories of new institutionalism (NI). This approach questions earlier institutional assumptions that human beings are self- interested, rationally thinking actors (March and Olsen, 2009) and concentrates on the historical–institutional context in which decisions are made (Jordan et al., 2003). Institutions are taken here to mean ‘a relatively stable collection of practices and rules defining appropriate behaviour for specific groups of actors in specific situations’ (March and Olsen, 1989: 948). Institutions matter because they are seen as ‘defining opportunity structures and constraints on behaviour’ as well as being ‘path-dependent path-defining complexes of social relations’ (Jessop, 2001: 1217). It is this emphasis on institutional context that affords a greater understanding of regime-level housing market responses to centrally determined low-carbon targets. This, we suggest, opens up the opportunity to critically evaluate how existing institutional configurations condition and shape low-carbon housing futures to capture the complexity of the transition taking place.

Of particular interest to us is how NI enables an understanding of the role of embeddedness. Institutions are characteristically slow to evolve and change and are conditioned by an allegiance to established norms and values (Jordan et al., 2003), leading to embedded forms of behaviour which can be difficult to change. In this sense, firms do not behave as transformers or reformers (Stiglitz, 1999). Although institutions are not immutable, they do have relatively durable, self-reinforcing and persistent qualities (Hodgson, 1998). Institutions are ‘sticky’ and when faced with external pressures, will tend to look inward and backward in order to look forward (March and Olsen, 1989).

Policy change – purposeful change to formal institutions (and sometimes informal institutions) by state actors – usually involves institutional change (Needham and Louw, 2006) and is overwhelmingly incremental (North, 1990). It can thus be considered as a form of institutional design (Alexander, 2005) and should be informed by an understanding of how institutions and their constituent actors (including organisations) change and can be changed. As institutions frequently default to tried and trusted strategies in the search for continuity (Needham and Louw, 2006), authors such as McLeod (1997) and Payne (2013) have suggested that significant institutional change is likely to be the result of a sense of partnership and common enterprise between the state and market-based actors. Therefore, although institutions may be ‘sticky’ in nature, policy may achieve its intended aims if it acknowledges the presence of institutional pathways (Needham and Louw, 2006; Smith and Lewis, 2011).

Such pathways, however, are not always readily identifiable. New institutionalist perspectives take a strongly disaggregated view of market structures, emphasising the role of context, process and social relations in market activity (Adams et al., 2005). Previous work on the institutional dynamics of housing markets (Adams and Payne, 2011; Payne, 2009, 2013) has indicated differentiated institutional responses to state expectations based on existing behavioural norms. Payne (2013), for example, in exploring housebuilder responses to UK brownfield development targets, showed that institutional stickiness could be overcome in certain instances but was dependent upon the degree of alignment between policy expectation and strategic business priorities, institutional relations and the structure of housing provision.

By leveraging insights from NI to enrich our understanding of regime-level action, our approach overcomes assumptions that reinforce the idea that housing markets and their constituent actors are monolithic or homogeneous entities. This allows us to examine whether new institutional configurations are developing or whether existing institutional interests and configurations can prevail. In turn, our chosen approach enables us to capture the complexity of the transition taking place and assess what challenges are being experienced by market-facing actors within the low-carbon transition.

From an evaluation of the dominant characteristics of both the MLP and NI, we argue that a joint reading of these approaches provides a rich and rewarding framework from which to assess pathways to carbon transformation within the English speculative housebuilding industry. Central to our joint reading is the recognition that whilst transformative change is typically incremental and experimental, it very often takes place in a complex environment in which institutions are both embedded and resistant to change. Our interpretation of these market-based complexities yielded three dominant lines of inquiry. These are summarised as follows:

Methodology

The methodological approach sought to examine the extent to which the speculative housebuilding industry can achieve institutional transition in response to Government policy on zero carbon homes. As part of this research, significant emphasis was placed not only on housebuilding actors, but also the wider systems and process of which they are a part. Using the combined theoretical framework outlined in Table 2, three main research questions were developed around our clarity, change and constraint thesis:

Clarity: to what degree are policy expectations relating to low-carbon transition accepted and understood by housing market actors? Change: to what extent are housing market actors equipped to deliver innovation in response to state-led carbon interventions? Constraint: what institutional constraints in market-led housing systems are limiting policy change and associated levels of effectiveness?

Qualitative interviews were undertaken in two stages. Stage one targeted elite semi-structured interviews with group directors based in the head offices of the UK’s 15 biggest volume housebuilders 2 (by turnover) who together produced approximately 58% of all new homes in 2015 (Housebuilder Media, 2016). Interviews were secured with Group Sustainability Directors, Group Development Directors or Group Technical Directors at 11 volume housebuilders and enabled the examination of how zero carbon housing policy is changing strategic approaches, business behaviours and product outcomes across England.

Stage two sought to interrogate the stage one findings through a series of elite semi-structured roundtable discussions with directors at a range of third sector organisations and businesses with a stake in new housing delivery. Seven round table discussions were secured with directors involved in promoting the interests of spatial planning, market housebuilding, surveying, mortgage lending, green building and zero carbon building. A further roundtable was secured with a leading mortgage lender. The explicit purpose of these stakeholder roundtables was to critically discuss the housebuilder position and gain insight from competing perspectives of the wider institutional system and processes of which housebuilders are a part. This enabled a rich perspective on clarity, change and constraint and yielded insights into the dynamics of regime change. Participants from both research stages have been anonymised at their request and no quotes are attributable.

As stated in the ‘Introduction’ section, the research was undertaken within a fluctuating policy context. This afforded the opportunity to gauge stakeholder perceptions and attitudes in response to changing parameters. Both the interviews and roundtable discussions were undertaken between October 2014 and May 2015, at a time when the 2014 Queen’s Speech had confirmed legislation to allow for the creation of an allowable solutions scheme but before the official scrapping of the policy (DCLG, 2014a). The shifting nature of Government commitment during the duration of the policy is outlined in Table 2, which we have distilled into four key phases and called: target setting, technical realism, ambiguity and abandonment.

Results

In this section, we present the results of our research around our three lines of enquiry: clarity of expectation, change mobilisation and constraint management. This enables us to address our three research questions and assess the degree to which the speculative housebuilding industry can achieve institutional transition in response to Government policy on zero carbon homes.

Clarity

Here, we address research question one – to what degree are policy expectations relating to low-carbon transition accepted and understood by housing market actors – to determine whether sufficient policy coordination existed to enable regime-level behaviour change.

The research indicates that technical innovation by housebuilders was hampered by the lack of policy articulation and coordination from government around its zero carbon message. Housebuilders reported deep frustrations with the policy ambiguity and regulatory uncertainty they had faced since the initial policy announcement in 2006 (see Table 2). Housebuilders argued the lack of a clear policy framework with a common language and a clear timetable for achievable implementation had frustrated their longer term strategic business planning, especially around their engagement in land markets, and had created difficulties in predicting what issues may emerge as a result. One housebuilder noted: … we’re making decisions that we might buy a piece of land today that we might be on for ten years. And how do you then build in costs to that if they’re going to move the goalposts every two years? … at the moment it’s just as it was a couple of years ago, it’s a complete mess … you’ve got the Coalition at one end and the Labour Party at completely the opposite end of the spectrum … we thought we had a path to 2016 but the Labour Manifesto has now just made that very difficult to map out

Change

Research question two considered the extent to which housing market actors are equipped to deliver innovation in response to state-led carbon interventions. In what follows, we reveal that housebuilders may accept change, but require convincing solutions that are market friendly to overcome the durable characteristics they currently display.

The interviews revealed that housebuilders had undertaken a range of exploratory research and development exercises to explore a series of technical innovations to meet the range of policy requirements set out by government since 2006 (see Table 2). This involved housebuilders experimenting with a range of innovative renewable technologies advanced by their supply chains, as well as exploring fabric-based material upgrades to existing house types. A small number of housebuilders interviewed had worked together in consortiums on government-funded exemplar schemes to test build some of these design solutions. However, they were keen to point out these innovative products faced a range of cost and technological constraints that challenged their conventional standardised approach to product design and mass production, which they were resolutely unwilling to compromise on. Nearly all housebuilders interviewed were reluctant to extensively incorporate innovative renewable technologies advanced by their supply chains for reasons of long-term technical and performance efficacy, supply chain capacity, consumer utility or ongoing maintenance and servicing needs. As such, housebuilders revealed they were actively working towards technical solutions that were both practical and cost effective, as one housebuilder stated: ‘… we need something we can manage easily on-site bearing in mind the volumes that we’re doing as a business, we don’t want to create something which is too difficult’.

This approach by housebuilders garnered some criticism from the zero carbon housing stakeholder, who condemned the industry’s reliance on incremental change and its reluctance to utilise renewable technologies or innovative design solutions or to develop new production models. However, the green building stakeholder conceded the business logic of incremental change, acknowledging that housebuilders’ confidence in the government’s seriousness about zero carbon homes had been eroded due to policy ambiguity. They instead called upon government to drive the agenda forward: ‘… what government needs to more than anything is just say this is a serious issue that you need to deal with and then I think they can also help by lending their support to industry initiatives’. ‘… we made the point very strongly that we needed the allowable solutions mechanisms to be in place nearly a year and a half ago. And here we are you know approaching 2015 and that is not in place yet’. … I don’t have a problem with it … by a simple calculation I know how much money I will have to pay to have that as an allowable solution. So, I pay that money to the Bank of Carbon, the Bank of Carbon write me a letter saying I’ve paid and we carry on … business as usual.

However, housebuilders actively capitalised on this institutional turbulence to argue for a scaling back of the government’s carbon regulation ambitions. In particular, housebuilders noted how the recession and the historical undersupply of new homes had ‘helped the conversation’ with government about their viability concerns of achieving the technical innovations necessary to achieve mass production of zero carbon homes. One housebuilder revealed the nature of their discussions with government: But ultimately, now this is for me the crux of the matter, you [the government], want me to deliver a CSH6 home and it’s going to cost £40,000. It’s not me saying it, it’s your [the government’s] advisors saying that. If a home costs me £80,000 to build, for every one that I’m going to build you’re going to lose a half for your zero carbon policy. You want 250,000 homes a year, we currently can only deliver 120,000, so actually it’s not 120,000, I’m going to give you 90,000 homes a year because your zero carbon policy is expensive.

A number of housebuilders admitted they had always expected the 2016 zero carbon target to be pushed back or watered down due to the significant changes that were being asked of them in a relatively short space of time. They highlighted the government’s flawed expectations around the costs and technical feasibility of achieving the target within the particularly volatile post-recession housing market. One housebuilder revealed they, like other housebuilders interviewed, had actively made that point to government during meetings that the zero carbon housing policy failed to understand and accommodate the industry’s incremental approach towards policy adaptation: …it was too big of a step in one go…we’re going to do all that overnight…? You know, it sounds great in principle but in reality, no other industry, or not that I can think of, would go that big of a step in one go.

Constraint

Finally, we address our third research question – what institutional constraints in market-led housing systems are limiting policy change and associated levels of effectiveness – and examine the extent to which the wider modalities of market behaviour conditioned housebuilder responses to carbon regulation. We also report on some recommendations that housebuilders and stakeholders suggested may overcome these market dynamics.

The interviews revealed that the significant additional costs housebuilders faced in delivering policy-compliant zero carbon homes could not, in their view, be captured elsewhere in the housing development process as added value because the market mechanisms they argued were necessary to achieve this – consumer demand and valuation and lending practices – did not exist. Housebuilders argued these market-based constraints had curbed their ambitions of producing truly innovative products deliverable at mass scale because of this cost/value imbalance. Whereas some housebuilders interviewed were actively involved in niche exemplar schemes, they were quick to emphasise their niche technical solutions were not readily transferable to market-based mass production methods. This was mainly due to their exemplar schemes being free from land and housing market constraints owing to government funding support but also due to the lack of market testing of consumer appetite for such technical innovations.

Housebuilders were particularly keen to point out the lack of market signals for zero carbon homes. They perceived their consumers as being unwilling to pay a premium for a more energy-efficient home or consider energy efficiency as a significant purchasing decision, as one housebuilder commented: We still see the problem of that being a cost where you’re not going to see any benefit coming back the other way in terms of the purchaser’s perception. And potentially then seeing any uplift because you are providing a better product. It’s not necessarily perceived as that. There is no strategic advantage and if there were we’d all be doing it already. We wouldn’t need regulation; we wouldn’t need government intervention. If I can sell a home for more money than you I will do it and if that means because I can sell it as zero carbon, I’d already be doing it. It’s very difficult… give somebody a bill for what the running costs are going to be because you’re then hamstrung. And with the age of litigation that we’re in, you’re going to have somebody saying ‘you told me the wrong figure, you told me it was going to cost £3.72 and it’s costing me £3.75 a week. I want some compensation’. And so I think we remain wary of doing things like that.

Beyond consumer demand and consumer behaviour, housebuilders also reported valuation and lending practices as significant constraining factors on their ability to create and realise additional value from the zero carbon housing market. In particular, housebuilders argued there was, at the time of interview, no market mechanism available to them to realise the additional value such properties may yield because the savings on energy bills were immaterial in the valuation process. Until this changed, housebuilders were adamant they were unable to bring such properties to market, as one housebuilder argued: ‘… So we find it very difficult to see how if lenders and valuers do not recognise that additional value, then I don’t see how we can’. When we discussed this with a leading mortgage lender, they revealed why incorporating reduced utility costs into their affordability calculations was limited by consumer behaviour and lifestyle: We still are in the same situation where there is insufficient evidence for this to make lending underwriting decisions based on those efficiencies and therefore we couldn’t say that we’re in a position where we could lend extra money to a customer because they have bought a particular type of environmentally-friendly property.

In our discussions with housebuilders and stakeholders about ways to overcome these market constraints, we received a varied set of recommendations, which largely coalesced around the need for an accelerator to get consumers to buy-in to the concept of zero carbon homes to: (a) drive market demand; and (b) enable additional costs to be recouped as enhanced value. Indeed, the zero carbon building stakeholder candidly revealed the need for more market-based ‘pull’ factors rather than the current sole focus on ‘pushing’ housebuilders to deliver technical innovations, stating: … until that valuation model changes … I think we’re kind of stuffed in a way. And it sounds like I’m a housebuilder but the more I’ve listened to them, the more I’ve thought about it … and I don’t see how you can really create pull and pull is what we need. There’s enough push, it only goes so far.

However, the leading mortgage lender was keen to reiterate the limited scope for changes to mortgage lending practices resulting from energy efficiency due to the dynamics of consumer behaviour towards house purchase decision making. In their mind, the primacy of location prevents homeowners buying just for efficiency. They suggested tax incentives for promoting energy efficiency as a primary factor in house purchase decision making could be effective.

This section has revealed how the wider market dynamics within which housebuilders operate act to constrain their ability to capture the additional cost of zero carbon homes through added value. Our research indicates that the housing market as a whole needs to adapt and change, accounting for the dynamic and complex institutional relations within which policy change is situated and that a single pathway-based approach locked onto ‘pushing’ housebuilders will not work if additional ‘pull’ mechanisms are absent. Whilst there was some disagreement from the stakeholders as to the precise nature of these pull mechanisms, a general consensus on the role of the consumer in driving demand for zero carbon houses was evident. Such views seem to chime with previous industry thinking. The CBI (2015) argue for a more effective policy framework for encouraging consumers to value and pursue energy-efficient homes through consistent and effective incentives. This, they suggest, would enable industry to invest against the policy and regulatory framework to create a market for energy-efficient measures. Similarly, the Zero Carbon Hub (2010) argue for a greater consumer-centric perspective and call for ‘…a clear, beneficial and recognisably secure sales proposition, reflecting innovation rather than risk’ (p. 3), as being central to successful market housing development.

Discussion

The above results provide a unique insight into the challenges being experienced by market-facing actors within the low-carbon transition. Although the built environment has increasingly become the subject of regulatory interventions centred on carbon reduction (Bulkeley et al., 2010; Carter et al., 2015; Hodson and Marvin, 2013) there has, to date, been limited research which explores the tensions that these expectations place upon those market actors targeted for reform. Our research has addressed this gap. Through our focus on the English housing market, we have explored the extent to which housebuilders have recalibrated their business strategies and behaviour in response to the Government’s target for zero carbon homes. As the target and associated apparatus draws on the hybrid characteristics of both eco-state restructuring and ecological modernisation (Goodchild and Walshaw, 2011; Huber, 2000; Jänicke, 1986; While et al., 2010), we have shown how housebuilders were placed in an uncertain institutional environment where innovation was expected within strictly controlled regulatory parameters. Through the use of theories drawn from transition management (Geels and Schot, 2007; Rip and Kemp, 1998) and NI (Jordan et al, 2003; March and Olsen, 2009), we have presented an understanding of the opportunities and constraints experienced by housebuilders in the search for regulatory compliance and have offered a unique insight into the institutional dynamics and interactions of market-led housing systems within the low-carbon transition, which was otherwise absent in the literature.

Our research reveals that housebuilders responded to policy expectations centred around zero carbon housing in two phases. The first phase saw housebuilders engage with research and development in new technology and liaise with actors driving exemplar schemes. The second witnessed housebuilders operating in an increasingly uncertain policy environment in which they felt compelled to explore fabric-first design solutions and experiment with allowable solutions to offset carbon outputs. Neither phase delivered the level of institutional transformation expected by the Government. One possible interpretation of this policy failure is that the zero carbon housing target failed to gain traction, as ambiguity at the landscape scale destabilised momentum gained within the niche. We suggest however, that whilst there is evidence to support this, the situation is more complex and has as much to do with regime interactions and dynamics as it does landscape and niche pressure.

It is certainly arguable that housebuilders were both aware and party to technological innovations being developed by the niche. Yet, in the majority of cases, interviewees expressed concerns not only over the technical viability of solutions, but the conditions in which they were tested. The research indicated that a significant proportion of innovations had been developed as demonstration projects under artificial market conditions. In many cases, such schemes were funded directly by Government and thus were free of normal market conditions. Our findings are consistent with earlier critiques of the role of the niche in achieving transformation, which have drawn attention to the failure of the niche to offer solutions which can be accommodated by the regime (Killip, 2013; Schot and Geels, 2008; Seyfang, 2010). In the case of the English housebuilding industry, there appears to be a clear mismatch between notions of innovation on the one hand and acceptability amongst wider stakeholders on the other. The difficulty of translating consumer preferences into price signals and the ability of lenders and valuers to accommodate such prices suggests that innovation is interpreted by wider housing market actors as a form of enhanced risk. On this basis, regime breakthrough (Killip, 2013) is likely to require an enhanced appreciation of the role of market uncertainty faced by those actors entrusted with carbon transformation.

In much the same way that our research has served to reveal tensions in the relationship between niche and regime, it is also apparent that the ability of the landscape to apply pressure on the regime (Geels and Schot, 2007; Rip and Kemp, 1998; Smith et al., 2005) is open to reinterpretation. The gradual process of regulatory retreat and repositioning by the Government in its attempt to introduce carbon limits is suggestive of both regime-level resistance and a failure to identify institutional pathways grounded in an appreciation of institutional structures and processes. Our research asserts that market-facing institutions are indeed sticky (March and Olsen, 1989) and that much of the failure of the zero carbon housing experiment rests in overconfidence in market flexibility. The process of achieving transformation is therefore revealed as one which is not so much dependant on the ability to unlock institutions as an appreciation of the incremental nature of institutional change (North, 1990). Although the development of an allowable solutions mechanism was seen as both reactive and poorly coordinated, it did demonstrate a reluctant recognition that change would need to accommodate conventional forms of business practice and the role played by design standardisation and mass production.

What does this mean for the regime? Earlier in the paper, we suggested that unless market forces are able to drive change towards low-carbon housing futures, housebuilders may find little reason to shift conventional production processes and adopt innovative technical solutions. Drawing on the work of transition theorists (Geels, 2014; Killip, 2013; Schot and Geels, 2008) we argued that more attention needed to be paid to the dynamics of regime behaviour in order to challenge the monolithic and isolationist interpretations of regime operations and explain why regime breakthrough may not occur within the time frames set by the landscape. Our research on the English housing market supports this proposition and reveals complex institutional configurations and interests at play. These emphasise the resilience of institutions and a resistance to unproven forms of intervention mobilised by the landscape on the one hand and by the niche on the other hand. Our research therefore indicates that a narrow focus on the technical challenges of determining whether zero carbon housing futures can be achieved (see Osmani and O’Reilly, 2009) neglects the complexities of institutional arrangements present within the regime. We suggest that achieving low-carbon housing futures is not simply about targeting dominant market actors and attempting to push innovation through strictly controlled regulatory parameters. Rather, the mobilisation of change at the regime must involve an understanding of the role that disparate or otherwise incumbent market actors (in our case consumers, lenders and valuers) can potentially play in pulling dominant market actors towards achieving policy goals set by the landscape. Change can be acceptable and achievable if convincing solutions based around existing market structures and practices are mobilised with appropriate degrees of space afforded to key market actors. It is arguable that this form of mobilisation might be achieved by giving greater prominence to regime dynamics within transition experimentation.

This paper has offered fresh insights into the structure and character of regime behaviour within the English housebuilding sector through the assertion of the role played by institutional dynamics and interactions. Such insights go some way towards recalibrating and redirecting both political expectation and transition experiments driven by niche-level actors. Our findings show that housebuilders were prepared to engage with carbon-centred coalitions and projects, but that a mandate of technological testing overemphasised the role of ‘push’ rather than ‘pull’ factors. In line with perspectives offered by scholars who have advocated the significance of social learning with transition experimentation (Bos and Brown, 2012; Bulkeley and Broto, 2013; Evans and Karvonen, 2013), we suggest that the promotion of coalitions, which provide adequate appreciation of institutional functionality, may go some way to encouraging behavioural shifts. We see these as distinct from demonstration projects geared towards the promotion of technical feasibility.

If such approaches to low-carbon transition are to be successful, we suggest that a number of criteria will need to be met. First, political choices about goal orientation and the timescales for delivery will need to be both realistic and formed on a reflexive understanding of needs, values and capabilities (Meadowcroft (2009, 2011). Second, experimental coalitions will need to be inclusive and representative of real-world actors (Bos and Brown, 2012). In particular, there is a key role for third sector organisations in brokering niche/regime interactions. Studies in the UK (Hodson and Marvin, 2012) and the Netherlands (Kemp et al., 2007; Kern and Smith, 2008; Loorbach, 2010) have shown that where such conditions have not been met, they have either failed to gain wider societal traction or have allowed the regime to re-appropriate the niche under the illusion of transition.

Conclusion

This paper has explored how institutionally constituted market behaviours shape pathways and transitions towards low-carbon futures. It has questioned the extent to which market-facing actors within the built environment are adequately positioned to respond to increasing levels of state regulation centred on carbon reduction. Through a focus on England’s zero carbon housing policy, we have identified a range of opportunities and constraints which need to be addressed in considering the transformative potential of market-facing institutions in the low-carbon transition. The research undertaken for the paper has shown that the English zero carbon housing experiment ultimately failed to achieve its aim. This was due to a number of factors. These included an overemphasis on the utility of technological demonstration projects, the limited appreciation of the relationship between valuation and market acceptance, and more importantly, the time it took to recognise the incremental nature of policy adaptation.

Our findings challenge widely help assumptions about the capacity of the market to act in response to target-based interventions under a low-carbon transition. We instead draw attention to the need to understand actor behaviour within the wider context of institutional dynamics and wider market modalities. By using England’s housing system to examine market-based complexity in the low-carbon transition, our research offers valuable insights to other market-led housing systems (e.g. the US, Canada and other devolved UK regions), who rely on market practices in urban development. Moreover, our research is useful to future theoretical and empirical analyses of low-carbon transition in alternative institutional settings (such as transport, energy and manufacturing), particularly those examining disaggregated approaches to target setting (e.g. Greater London Authority, 2017).

Although we welcome the overarching policy goals associated with low-carbon transition and maintain that the market can play a key role in delivery, we ultimately call for a revised understanding of how market-dependent actors can be engaged. We suggest that future regulatory interventions associated with carbon reduction need to allow for greater flexibility in market responses in order to allow for the incremental nature of institutional change. Furthermore, there needs to be recognition that market transformation will be dependent on taking a more plural approach to collaboration. On this basis, we argue that future research on low-carbon transformation might consider the roles that can be played by perspectives centred on incremental policy adjustment, enhanced market synergies and a broader interpretation of actor inclusion within state-market coalitions.

Footnotes

Acknowledgements

The authors would like to express sincere thanks to the funders and all participants involved in the research and the three anonymous reviewers for their constrictive comments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was funded by the Economic and Social Research Council via the University of Sheffield’s Impact Accelerator Account (Account #141272) and the Royal Institution of Chartered Surveyors (Project #482).