Abstract

Green hydrogen and its derivatives have experienced a hype, driven by enthusiasm about their potential as a mitigation option across multiple sectors. Initial optimism is now waning, as reflected in an increasing implementation gap between announced green hydrogen projects and those being realized. However, the speculative dimensions of the industry remain underexplored. Drawing on the concepts of growth machine and fictitious capital, this article investigates the actor coalitions that have driven – and seek to benefit from – the green hydrogen hype. Empirically, we focus on Chile's Magallanes region, where 17 large-scale, export-oriented projects have been announced since 2021, without any final investment decision to date. Our findings show that agencies from energy-import-dependent countries, project developers, local landowners, and national and regional governments mobilized to sustain and amplify the hype in line with their diverse interests. Project developers accumulate anticipated future profits through legally formalized ownership titles, with special purpose vehicles functioning as the central instrument of speculative accumulation ahead of project materialization. Moreover, the regional hype has been fueled by expectations of economic growth, the promise of extending the lifespan of combustion-engine vehicles, and the hope that the region's resource endowments could deliver the cost reductions necessary to make green hydrogen commercially viable. Ultimately, the hype serves to secure ongoing private investment, state support, and public legitimacy, while deflecting scrutiny of project viability and delaying more feasible decarbonization alternatives. Beyond economic viability, the export orientation of these projects generates tensions with local energy needs, raising broader energy justice concerns. Rather than fostering the accumulation of low-emission productive capital, the current trajectory has supported the proliferation of fictitious capital in financialized energy transitions. The analysis underscores the need for governance mechanisms and state capacities capable of selectively concentrating limited public resources in an incipient market for capital-intensive and unprofitable decarbonization solutions.

Keywords

Introduction

Green hydrogen and its derivatives, such as green ammonia, methanol, and synthetic fuels, have received increasing attention as potential emission mitigation options 1 . The green hydrogen industry has been experiencing what many observers describe as a “hype” (Romm, 2025) marked by high societal attention and initial inflated expectations (Fenn and Raskino, 2008; Kriechbaum et al., 2021). These expectations were reflected in a large global project pipeline: by 2024, almost 50 Mt per year of low-carbon hydrogen 2 production capacity had been announced for 2030, which – if realized – would correspond to roughly half of projected global hydrogen demand (IEA, 2024).

Unlike previous hydrogen hypes (Bakker, 2010; Bakker and Budde, 2012; Romm, 2025), the present hype has a distinctive geographical dimension. Many regions in the so-called “Global South”, particularly peripheral regions that offer high renewable energy potential, have become focal points of (inter-)national interest (IEA, 2019; UNIDO, IRENA and IDOS, 2023). In return, the industry seemingly promises new development opportunities to these regions (Dejonghe and Van de Graaf, 2025; Scholvin and Kalvelage, 2025).

Since 2024, however, the green hydrogen hype has entered a “trough of disillusionment” (Fenn and Raskino, 2008; Kriechbaum et al., 2021), characterized by a substantial implementation gap between project announcements and actual deployment. This gap is increasingly acknowledged in the literature, alongside the recognition that trillions of USD in subsidies or regulatory interventions, such as carbon pricing, would be required to render green hydrogen competitive with gray hydrogen (produced from natural gas) or conventional fossil fuels (Johnson et al., 2025; Odenweller and Ueckerdt, 2025). Moreover, it is becoming evident that the hype around hydrogen has produced a speculative bubble tied to techno-optimistic visions of green hydrogen futures, and that many of the announced projects are unlikely to materialize (Klagge et al., 2025; Monteith and Escobar, 2025; Walker and Kalvelage, 2025). Hence, 2025 has seen an increasing number of project cancelations (IEA, 2025).

The drivers of the recent hype surrounding green hydrogen remain poorly understood. Some scholars have argued that incumbent actors, particularly within the fossil fuel sector, promote green hydrogen as a predatory delay strategy, potentially with no genuine interest in project realization (Brauers et al., 2021; Szabo, 2021; Vezzoni, 2024; Wright et al., 2024). However, the role of multi-scalar coalitions in the development of export-oriented green hydrogen megaprojects remains underexamined. Existing research tends to emphasize national and international actors (Kalt et al., 2023; Kalvelage and Walker, 2024; Schorr et al., 2026), while regional and local promoters of green hydrogen have received comparatively less attention (Dorn, 2024; Hine et al., 2024).

Moreover, the speculative dynamics underlying the green hydrogen industry remain insufficiently theorized, despite growing interest in the topic (Cezne and Otsuki, 2025; Hunt and Tilsted, 2024; Monteith and Escobar, 2025). Much of the existing critical literature focuses on the socio-ecological consequences of hydrogen projects and global power asymmetries (DeBoom, 2025; Dejonghe and Van de Graaf, 2025; Flores Fernández, 2026; Kalt et al., 2023; Tunn et al., 2024). Several other studies warn that uneven international financing capacities reproduce structural dependencies between Global South and North countries (Gabor and Sylla, 2023; Scholvin et al., 2025). Yet, what these debates rarely address are the structural barriers undermining project realization – namely, insufficient capital flows and questionable profitability in the context of an emerging market (Klagge et al., 2025) – nor the strategies through which actors sustain capital accumulation despite these realities.

To address these interrelated gaps, this article mobilizes two complementary concepts. First, we draw on the growth machine concept (Molotch, 1976; Logan and Molotch, 2007 [1987]) to examine the regional actor coalitions that have driven – and seek to benefit from – the green hydrogen hype. The growth machine concept directs analytical attention to the place-based coalitions of rentier interests, regional elites, and political actors that mobilize around growth narratives and land-use opportunities. Second, we draw on the fictitious capital concept (Marx, 1971 [1894]) to theorize the speculative dynamics underlying this process. We argue that the hype surrounding green hydrogen has given rise to an inflation of paper assets, sustained not through large volumes of deployed capital, but through the announcement, development and legal formalization of ownership titles in projects – often at early, pre-Final Investment Decision (FID) stages – that may never be realized. Together, these two concepts allow us to connect the political and territorial underpinnings of the green hydrogen hype with its economic and speculative dimensions.

We analyze the dynamics surrounding the promotion and announcement of green hydrogen projects in Chile's southernmost Magallanes region, characterized by abundant wind resources but limited industrial infrastructure and weak local demand. Together with the Antofagasta region, where the eventual development of green hydrogen and derivatives megaprojects is associated with the potential for low-cost solar energy production (Scholvin and Kalvelage, 2025), Magallanes has been identified by the Chilean government and international actors as a potential production and export hub, supposedly offering one of the lowest production costs globally due to its still unexploited, extraordinary wind energy potential (Armijo and Philibert, 2020; IEA, 2019; Ministry of Energy, 2020, 2021). Seventeen export-oriented projects have been announced in the region, which – if realized – would collectively cover approximately 680,000 hectares or more than twice the size of Luxembourg (Mayor of Punta Arenas, 2024). However, none has obtained a FID, reflecting a great economic uncertainty. Therefore, we identify Magallanes as an ideal site for interrogating the coalitions and fictitious capital accumulation underpinning the recent green hydrogen hype.

Against this background, this article asks: Which actors and coalitions have driven and sustained the heightened expectations around green hydrogen in Magallanes, how and why? How can different actors derive value from green hydrogen projects without them being built; and, to what extent is there a gap between the financing needs of announced projects and the capital actually being committed to their development in the Magallanes region?

By answering these questions, we make three contributions. First, following Wachsmuth (2017) and Brenner (2019), we expand the growth machine concept beyond the urban to show how growth coalitions operate at the regional scale, mobilizing green growth narratives to valorize rural land and reposition peripheral regions within energy transition value chains.

Second, combining it with the fictitious capital concept, we demonstrate how green hydrogen projects serve not only as tools for industrial and regional development but also the accumulation of fictitious capital well before material production occurs. Thereby, we develop an understanding of the implementation gap between announced and realized projects not as a failure of policy design or techno-economic challenges but as the outcome of growth coalitions that sustain themselves through fictitious capital accumulation and begin to fracture once the challenges of material implementation become popularly acknowledged. In this way, we contribute to debates on the political economy of green hydrogen (Dejonghe and Van de Graaf, 2025; Hunt and Tilsted, 2024; Vezzoni, 2024) and the role of financial planning tools in the energy transition (Babic, 2024; Baker, 2015, 2022; Klagge, 2020).

Third, we offer a conceptual distinction between the fictitious value of announced projects and actual capital deployment, thereby contributing to research that questions the green hydrogen hype and explores pathways to economic viability (Odenweller and Ueckerdt, 2025; Walker and Kalvelage, 2025). After all, green hydrogen remains a necessary – albeit costly – decarbonization option, at minimum required to decarbonize the existing gray hydrogen market (IEA, 2019).

The article proceeds as follows. The next section introduces the growth machine and fictitious capital concepts, followed by a discussion of the methodology. The subsequent analysis examines the emergence, and regional manifestation of Magallanes's green hydrogen growth machine, and its fictitious capital accumulation. The final section summarizes the main arguments and findings, discusses theoretical and policy implications, and outlines avenues for future research.

Conceptual approach

We draw on two conceptual debates for the analysis. First, we adopt the growth machine concept to analyze actor coalitions and land valuation dynamics associated with export-oriented green hydrogen projects in peripheral regions. Second, we mobilize the fictitious capital concept to highlight the speculative dimensions and financing challenges of green hydrogen projects.

Growth machines and their green and regional variants

The growth machine concept “theorizes the growth coalitions that are shaped for intensifying the exchange value of urban places. It describes the entwined growth-centered goals of modern urban rentiers (place entrepreneurs), politicians, local media, and independent public and quasi-public agency leaders (e.g., transport authorities). These coalitions are supported by auxiliary players such as universities, consultants, and corporate capitalists who are also committed to the economic growth of the city” (Farahani, 2017: 4). The literature emphasizes the centrality of public-private partnerships in structuring these coalitions. Political elites frequently promote specific growth paths aimed at increasing tax revenue, while promising local development, new infrastructures, and other potential benefits (DuPuis and Greenberg, 2019).

Originally developed by Molotch (1976) and later expanded in collaboration with Logan (Logan and Molotch, 2007 [1987]), the concept highlights how hegemonic growth visions are established and institutionalized in cities. Capital accumulation relies more on rents than labor, where actors accumulate value by “gaining access to relatively better […] resource deposits than a rival, and where the price of the resource is set by the costs of production of less well-endowed producers” (Kaplinsky, 2019: 153). Land is the primary resource, valued for its location and properties, prioritizing exchange value over use value that could benefit non-wealthy groups (Logan and Molotch, 2007 [1987]).

Building on this foundation, Dilworth and Stokes (2013: 37) have coined the term “green growth machine” to describe how sustainability discourses are incorporated into growth machines to maintain “a public consensus that land development benefits all city residents”. Urban elites and real estate actors deploy narratives of environmental resilience and green infrastructure to promote projects that may deliver environmental benefits, but also produce green gentrification, exclusion (DuPuis and Greenberg, 2019; Jocoy, 2018), and conflicts (Curran and Hamilton, 2018; Wolch et al., 2014).

Geographers have expanded the growth machine framework in two other important directions. First, they have highlighted the increasing relevance of multi-scalar actors in institutionalizing capital accumulation strategies beyond real estate capital. While traditional research focused on local land-use intensification (centered in real estate capital), more recent scholarship underscores how alliances between global finance capital and place entrepreneurs reconfigure land as a financial-speculative asset and source of fictitious capital accumulation (Farmer and Poulos, 2019). Second, these and other insights have opened space for analyzing how growth machines operate not at a single scale but through the simultaneous articulation of local, regional, national and international actors and networks beyond the urban scale (Brenner, 2019; Wachsmuth, 2017).

Building on this expanded framework, we analyze the multi-scalar coalition promoting green hydrogen in the Magallanes region as a regional green growth machine. Export-oriented green hydrogen projects are inherently land-intensive as they attempt to reduce the costs of green hydrogen production through economies of scale (Walker et al., 2025). This characteristic takes on particular significance in peripheral regions where land values have historically been low and rent-extraction opportunities limited. Unlike typical renewable energy infrastructures dependent on grid integration, green hydrogen facilities can operate independently and export their products by ship, enabling remote territories to integrate into global energy transition value chains (Cezne and Otsuki, 2025; Monteith and Escobar, 2025). While scholarship on the Global South has largely examined renewable energy through the lens of land dispossession and “green grabbing” (Knuth et al., 2022; Scheidel et al., 2023), this article aligns with work examining cases where landowners actively mobilize renewable energy projects as a strategy of land-use intensification and rent generation (Alonso Serna, 2022) – creating rare opportunities for local elites to valorize land that would otherwise remain marginal to circuits of capital accumulation.

We argue that hype plays a crucial role in (temporally) stabilizing green hydrogen growth machines. Given the extraordinary capital intensity of green hydrogen megaprojects, actual realization would require concentrating limited public resources on a small number of projects, inevitably producing winners and losers within the coalition (cf. Walker et al., 2025). A hype-driven phase – characterized by inflated expectations (Fenn and Raskino, 2008) – defers this moment of selection, allowing multiple projects to be announced simultaneously and enabling landowners, regional governments, and national actors to capture returns from anticipated future growth without committing to politically costly decisions.

While hype can stabilize the growth machine, the motives for inflating expectations are different across actors. Renewable energy and technology providers depend on actual project realization to generate returns. They may inflate expectations to improve the conditions for (private and public) capital mobilizations (Funk, 2019). In comparison, incumbent oil and gas companies can benefit from prolonged hype even without project realization: non-realization protects their core business, while holding project titles functions as a hedging strategy, allowing them to exploit opportunities if green hydrogen deployment eventually scales. In this way, delay and speculation are not contradictory but coexist, with hype helping sustain political support and maintain the strategic positioning of (fossil capital) incumbents.

Delay and speculation also work together on a territorial basis: securing access to sites combining high renewable energy potential with port proximity can itself become a source of value or prevent others from gaining competitive advantages (Walker and Kalvelage, 2025; Walker et al., 2025). Crucially, the growth machine does not depend on project realization to generate returns – through legal formalization of land rights and the circulation of future value expectations, valuation happens in the present, well before the hype cycle enters its disillusionment phase. We conceptualize this dynamic through the lens of fictitious capital.

Project development and financing as fictitious capital accumulation

In Marxian political economy, capital is commonly differentiated into money capital, productive capital, and commodity capital. Following De Brunhoff (1990), we use real capital as shorthand for capital directly engaged in production and circulation. We distinguish real capital from fictitious capital, which denotes “the conversion of a flow of expected future income into a given capital value in the present as an ownership title” (Palludeto and Rossi, 2022: 550). Marx introduced the concept to highlight that financial capital can be accumulated relatively independently from productive (real) capital, with financial valuations often diverging from the underlying real economy. Once expectations of future returns vanish and titles representing fictitious capital can no longer be sold, the capital becomes devalued (Marx, 1971 [1984]: 443).

Marx distinguishes several types of fictitious capital, encompassing debt titles, government bonds, and shares. Despite its analytical potential (for a review, see Durand, 2017), the concept remains seldomly used in energy transition research. An exception is Baker (2015), who argues that debt and equity titles in renewable energy projects in the South African energy transition resemble a form of fictitious capital. As these titles can be traded on secondary markets, they become increasingly detached from the physical asset they represent. This detachment is similarly observable in the financial arrangements underpinning green hydrogen projects (Hunt and Tilsted, 2024).

Most large-scale renewable energy and green hydrogen projects are developed using project finance approaches. Project developers establish special purpose vehicles (SPVs) – dedicated legal entities holding project's assets and development rights, including land lease contracts (Baker, 2022; Hunt and Tilsted, 2024). We conceptualize equity shares in SPVs as fictitious capital, not because projects have necessarily reached FID or are bankable, but because the legal formation of the SPV transforms future revenue expectations into formalized ownership claims that can circulate prior to the formation of real capital. Project value therefore depends on risk perceptions and future revenue expectations rather than realized production. Therein, early-stage investments are considerably more speculative than later-stage ones, as technical, environmental, and regulatory uncertainties gradually resolve throughout the project lifecycle (Engelmann and Rohrmeier, 2022).

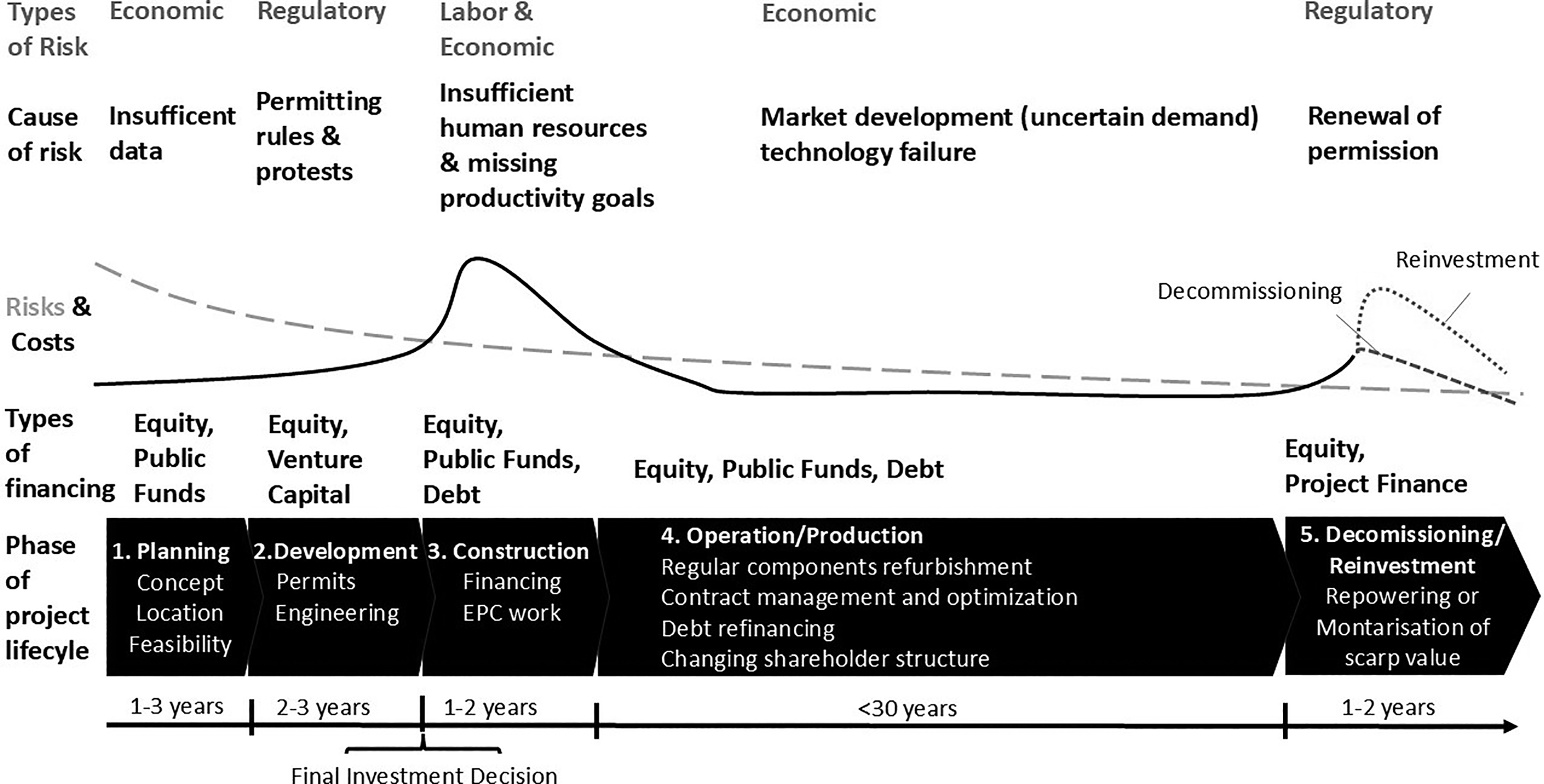

Large-scale green hydrogen projects are particularly suited to speculative capital accumulation due to their extended lifecycle and cost structure (Figure 1). Early-stage development involves limited expenditures – site identification, land negotiations, and feasibility studies – allowing developers to launch multiple projects and formalize them as SPVs before full bankability is established and before major construction costs are incurred. As a result, understanding the number and scale of announced projects as speculation helps to explain the pronounced implementation gap observed by Odenweller and Ueckerdt (2025).

Lifecycle of an export-oriented green hydrogen project (the authors, based on: Engelmann and Rohrmeier, 2022; Walker et al., 2025).

SPVs also allow developers to raise financing independently of the parent company's creditworthiness. Financing is secured against the business case of the SPV itself, which can improve financing conditions for capital-intensive renewable energy projects (Craen, 2023; Klagge and Nweke-Eze, 2020; Lee and Saygin, 2023). However, access to debt financing generally requires long-term offtake agreements that guarantee revenue streams – a significant obstacle given that green hydrogen will remain far from cost-competitive with gray hydrogen beyond 2030. 3 While gray hydrogen globally costs between 1.50 and 2.50 USD/kg, green hydrogen is projected to cost two to nine USD/kg by 2030 (IEA, 2024), with International Energy Agency estimates placing Chile at the lower end of this range (IEA, 2019). However, real-world demonstration projects in Europe currently report significantly higher costs, ranging from 9.80 to 14 EUR/kg (FfE, 2025; TNO, 2024). Even the Hydrogen Council – the industry's global lobby association – acknowledges that green hydrogen remains at least twice as expensive as gray hydrogen across regions (Laity, 2024).

These estimates cover only production cost, excluding processes and infrastructures that can substantially increase overall costs such as conversion into derivatives (ammonia, methanol, synthetic fuels), transport, export and import terminals, storage facilities, pipelines, or specialized shipping capacity. 4 Given these cost uncertainties and the expected price gap to fossil-based alternatives, few buyers are willing to sign binding, long-term offtake contracts (Ason, 2024; Collins, 2022).

Buyer commitment is thus typically contingent on state intervention through regulatory mandates, subsidies, or contracts for difference (Nyangon and Darekar, 2024). Assuming green hydrogen can be delivered at twice the cost of gray hydrogen, making export-oriented projects competitive would require subsidies covering at least half of total project costs (Craen, 2023; Lee and Saygin, 2023). Such support may take the form of producer-side subsidies in export-oriented countries (e.g., capital grants or tax incentives) or demand-side instruments in importing jurisdictions, such as Carbon Contracts for Difference (CCfDs) or renewable consumption mandates. Against this background, we evaluate the financing needs of the planned projects in the Magallanes region and the adequacy of existing subsidy schemes.

Integrating growth machines and fictitious capital

Together, the two conceptual approaches are analytically complementary: the growth machine explains who drives the hype and how, while fictitious capital explains how and why some actors within the growth machine seek to generate economic returns without requiring project realization. The hype and associated speculations on hydrogen development, within this conceptual approach, is neither merely a cognitive nor a purely financial phenomenon – it is a politically engineered condition that simultaneously serves coalition-building and potential capital accumulation. As long as ownership titles retain exchange value, the growth machine has rational incentives to sustain the hype and speculation around a green hydrogen economy even as implementation gaps widen. Applied to Magallanes, we examine how this growth machine has institutionalized itself, how fictitious capital has accumulated through project development, and what the structural limits of this trajectory are given persistent cost uncompetitiveness.

Methodology

We developed and refined our conceptual approach iteratively in the course of studying the development of the green hydrogen and derivatives industry in Chile's Magallanes region. Chile offers a particularly insightful case for analyzing hydrogen development: It was among the first countries to publish a dedicated national hydrogen strategy with a strong export orientation, actively promoting itself as an attractive destination for green hydrogen investment (Ministry of Energy, 2020). Chile has attracted project developers, particularly in the Antofagasta (highest full load hours of solar energy globally) and Magallanes (one of the highest wind energy full load hours globally) regions (IEA, 2019; Palma-Behnke et al., 2021).

We conducted empirical research in the Magallanes region between 2022 and 2024. Following a qualitative approach, our data collection efforts focused initially on systematic document analysis of public and private websites and documents. This included national policy documents such as the 2020 National Hydrogen Strategy and the 2024 Green Hydrogen Action Plan, and related documents available on the Ministry of Energy and Chilean Economic Development Agency (CORFO) websites, information on projects currently undergoing environmental assessment available on the Environmental Impact Assessment Service (SEA) website, regional planning documents, and gray literature from consultants and NGOs.

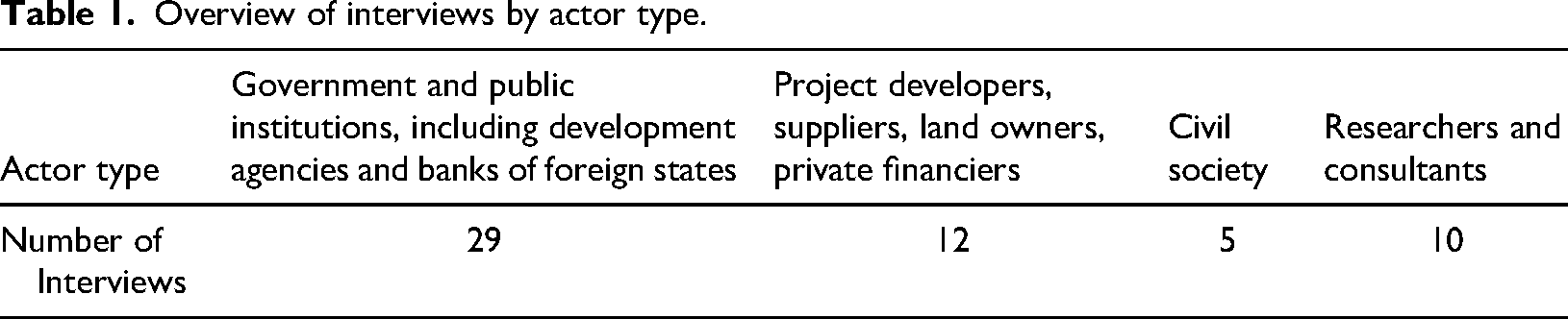

The core of our empirical material are 56 semi-structured expert interviews, conducted in the Magallanes region and in Chile's capital, Santiago, supplemented by online interviews (Table 1). Interviewees represented a broad spectrum of actors involved in or implicated by the envisioned green hydrogen industry, such as government officials and representatives of public institutions at the national and regional levels, project developers, technology and service suppliers, private financiers, landowners, and consultants. The interviews centered around the positive and negative expectations the interviewees associated with the green hydrogen industry for sustainable (regional) development and the challenges and opportunities they see in regard to the materialization of the industry. We analyzed the data using Kuckartz's (2014) structured content analysis, defining deductive categories based on the growth machine and fictitious capital frameworks, and refining them inductively through the empirical material.

Overview of interviews by actor type.

Analysis

This section first analyzes the development of Chile and the Magallanes region's green hydrogen growth machine. In a second step, we use the fictitious capital concept to assess the accumulation dynamics enabled by this growth machine and the challenges it faces in transforming speculative project visions into real capital.

The green hydrogen growth machine in the Magallanes region

We begin by tracing the historical articulation of Chile's green hydrogen growth machine before analyzing its regional embedding in Magallanes and the associated tensions.

The genesis of Chile's green hydrogen growth machine

The emergence of public-private alliances around green hydrogen in Chile and the Magallanes region exemplifies what growth machine theory identifies as multi-scalar coalitions formed to intensify capital accumulation by revaluing land and resource-based assets. At the national level, this coalesced primarily around shared growth-oriented objectives between international and domestic actors. According to former Ministry of Energy officials, “the idea of producing hydrogen and its derivatives originated with the German International Cooperation Agency (GIZ) from 2014 onwards, driven by Germany's interest in future renewable energy imports and Chile's interest in monetizing its vast renewable energy resources” estimated in more than 70 times Chile's renewable installed capacity (Santana, 2014; Ministry of Energy, 2022; Palma-Behnke et al., 2021; Schröer, 2014). 5

Initial coalition building occurred through GIZ's collaboration with Chile's Economic Development Agency (CORFO) from 2015 onward, exemplified by CORFO's Strategic Solar Program. Ministry of Energy officials interviewed explained that “this program was pioneering in seeking to leverage northern Chile's solar potential for low-emission hydrogen production targeting both domestic mining demand and maritime export of derivatives, and involved several Chilean universities alongside major mining corporations” (see as well: CORFO, 2017, 2018). Key moments of institutional consolidation followed in 2017, when GIZ organized the first green hydrogen conference in Chile and the Chilean Hydrogen Association (H2 Chile) was formed in 2018. H2Chile emerged from GIZ's conferences and includes over 100 member companies representing the full hydrogen value chain today.

The prominent role of foreign agencies, particularly GIZ, in promoting this growth machine was acknowledged by CORFO officials, one of whom stated: “GIZ started alone and from there we joined later. In 2019, GIZ published a study calling for country-wide initiatives to grow this market from a niche sector to a potential backbone of the national economy like the current mining sector” (see also: GIZ, 2019). These discursive framings reflect what Logan and Molotch (2007 [1978]) describe as the construction of “hegemonic growth visions” and exemplify how growth machines align domestic and global accumulation projects (Brenner, 2019). In the same period, CORFO commissioned the first green hydrogen roadmap. As a former Ministry of Energy official critically noted “the roadmap's overly optimistic and largely misleading projections motivated the energy minister to commission a national strategy from McKinsey, a key contributor to the Hydrogen Council, the industry's global lobby, to drive green hydrogen development in Chile” (similarly I_ civil society_4, I_researcher_3).

The Strategy, launched in 2020, set ambitious goals such as producing the world's least expensive green hydrogen by 2030 and establishing Chile among the top three global exporters by 2040 (Ministry of Energy, 2020: 14). The strategy further suggested that green hydrogen would enable Chile to “transition from being a country historically based on non-renewable resources to a nation that adds green value to its exports” (Ministry of Energy, 2020: 14). The state positioned itself as a growth-machine articulator, actively facilitating, promoting, and coordinating multisectoral efforts to establish this emerging industry. A first co-financing call in 2021 awarded subsidies to ENEL Green Power, Engie and Linde. As a former CORFO official described it, this was intended to be “the initial kickoff to accelerate the development of the green hydrogen industry in Chile (…) and meet the goal of being leaders in the production of this fuel from our country to the rest of the world”. This approach has been continued in the current government's Green Hydrogen Action Plan 2023–2030 (Ministry of Energy, 2023d), which envisions advancing industrialization plans and productive linkages around the green hydrogen and derivatives industry (Carrasco et al., 2026; Scholvin and Kalvelage, 2025). As one CORFO representative put it, “the major difference between the Strategy and the Action Plan was that we wanted to promote an industrial policy around green hydrogen to avoid creating an enclave economy like copper or even photovoltaic energy” seeking instead to “generate industrial fabric and local capacity to meet the derived demand for certain parts and components of electrolyzers and wind turbines” (similarly I_government_10, 16).

The Magallanes regional growth machine early formation: Territorial advantages, strategic positioning, institutionalization, and multi-scalarity

Building on the national growth vision, the multi-scalar growth machine frames the sector as a potential cornerstone of future regional prosperity. Key policy and consultancy reports identified regional capacity factors for wind power generation above 50–60%, estimating the wind power potential around 126 GW, which could supply 13% of global hydrogen demand (Ministry of Energy, 2017: 19, 2021). These conditions underpin optimistic green hydrogen cost projections of around USD 1.94/kg in Magallanes (Armijo and Philibert, 2020; IEA, 2019; Ministry of Energy, 2020), lending technical legitimacy to the region's strategic positioning within the global hydrogen economy. The regional scale of the growth-machine vision (Wachsmuth, 2017) is evident in statements from multiple regional government representatives (I_government_2, 7, 8), of which one indicated that “the installation of the industry in the region will allow for the diversification and greening of the regional productive matrix in line with the requirements of the global energy transition”.

This vision articulates various actors, including regional political elites, state enterprises, international corporations, academic institutions, and industry associations, aiming to capitalize on the region's exceptional wind energy potential through the construction of large-scale infrastructure – including wind farms, electrolysis plants, ports, and desalination facilities – in the “underutilized” plains north and south of the Strait of Magellan. Beyond the wind potential, the region's physical disconnection from Chile's central grid is central to the coalition's framing of Magallanes as an export-oriented energy frontier (Flores Fernández, 2026). As a former regional Ministry of Energy official explained “wind energy integration into the national electricity grid is not economically attractive because the regional energy system, which operates as an island, is largely self-sufficient in subsidized natural gas – rendering wind energy uncompetitive except for large-scale production such as that planned for the export-oriented green hydrogen and derivatives industry” (similarly Interview (I)_public institution 6, I_project developer_1, 3).

As a regional energy expert explains, the regional coalition's formation “can be traced back to early initiatives such as feasibility studies conducted by HIF (Highly Innovative Fuels) in collaboration with research centers at the regional University of Magallanes, in a partnership that continues to the present day” (confirmed by I_public institution_3). In 2022, HIF established a pilot plant for synthetic fuel production based on green hydrogen, powered by a single wind turbine and developed in partnership with Siemens, ExxonMobil, Gasco, Enap, Enel, and Porsche. Despite its pilot character, the project has been publicly framed in expansive terms to lend credibility to optimistic expectations (Ariztía and Undurraga, 2026). When the pilot plant opened, Porsche emphasized that “the potential of eFuels is huge. There are currently more than 1.3 billion vehicles with combustion engines worldwide. Many of these will be on the roads for decades to come, and eFuels offer the owners of existing cars a nearly carbon-neutral alternative” (Porsche, 2022). In this context, eFuels function as a promised alternative decarbonization pathway – or at least as a persuasive narrative – that can help defer or soften pressures toward rapid electrification, despite the limited material scale of current production.

HIF and other companies have established ties with the local population through the maintenance of offices and active staff. As one regional public agent explained, “HIF and other companies have hired several professionals from the petrochemical industry and sought to establish relationships with the broad spectrum of Magellanic society as they announce their projects – to show that they mean business. But in the end, little to nothing has come of it”. 6

Crucially, the growth machine has also succeeded in securing access to land through early lease agreements between rural private landowners (estancieros) seeking to obtain rental income or land appreciation. Given that the Magallanes region is experiencing a drought that undermines the productivity of its land for sheep grazing, local landowners have embraced new growth strategies promising regional economic diversification (Flores Fernández, 2026; Walker et al., 2025). Lawyers from the region interviewed for this research recount that “little by little, scouts began arriving seeking to sign contracts with estate owners – not to develop projects themselves, but to later sell or transfer them to developers in a speculative move” (confirmed by I_project developers 4, 8). From the landowners’ perspective, signing lease agreements with potential developers “promises additional rental income from degraded or underutilized lands while maintaining existing agricultural activities – and since many developers wanted access, we were able to negotiate good terms and obtain some rents, although the bulk depends on whether something is actually built and operated” (confirmed by I_project developers 4, 8). These accounts exemplify the growth machine's logic of land-use intensification and local actors’ integration for hypothetical future rent accumulation, echoing dynamics identified by Brenner (2019) and DuPuis and Greenberg (2019).

The institutionalization of the regional growth machine was formalized with the launch of CORFO's “Regional Transform Program: Magallanes Green Hydrogen” in September 2021. Led by the regional government, the program created an executive committee composed of CORFO's regional director and other regional private-public actors (CORFO, 2021). The Magallanes Green Hydrogen Producers Association (H2V Magallanes) – created in 2023 – brought together six project developers: Total Energies, EDF, HNH, TEG, Consorcio Austral, and Acciona & Nordex. Another pivotal moment of consolidation was the signing of the so-called “Magallanes Pact” in late 2023 (Figure 2 right), which brought together government ministers, undersecretaries, and H2V Magallanes to focus on capacity building, workforce and infrastructure development (Ministry of Energy, 2023a). It was soon followed by the state-owned company ENAP's announcement for a 1 MW electrolyzer facility in Cabo Negro and port terminals reconversion (ENAP, 2024). Moreover, the Ministry of Transport´s strategic logistical-port infrastructure plan proposed a portfolio of initiatives to address gaps in port and road infrastructure to enable future exports.

Left: President Boric and Ursula von der Leyen sign the EU-Chile agreement to promote renewable hydrogen development in Chile (Team Europe Project) in June 2023. Right: President Boric signed the “Magallanes Pact” together with the ministries of Energy, Economy, Public Work, the Regional Governor of Magallanes and regional representatives of the potential industry in December 2023. Source: Ministry of Energy (2023b) and H2Chile (2023).

The growth machine's multi-scalar nature is particularly evident in its (public) financing and diplomacy. The so-called Team Europe project for the Development of Renewable Hydrogen in Chile, launched during European Commission President Ursula von der Leyen's 2023 visit (Figure 2 left), mobilized €8 million – half from the EU, half from the German Federal Ministry for Economic Affairs and Climate Protection (BMWK). In addition, a dense web of MoUs and bilateral agreements has been established with Germany, France, Japan, the United States, and the EU, alongside provisions in trade agreements and technical cooperation (Ministry of Energy, 2023c).

While public (international) financing supports the green hydrogen growth machine, the financial sector – identified by Farmer and Poulos (2019) as playing an increasingly important role in growth machines – is notably under-represented. 7 While some public development banks have signaled willingness to mobilize financing, and the investment firm Copenhagen Infrastructure Partners is invested in one of the projects in the region (see below), the broader financial ecosystem remains largely absent. The limited involvement of commercial banks raises questions about how projects could realistically transition from the planning stage to construction, as large-scale investment projects typically require substantial debt financing. For example, in the capital-intensive Chilean mining sector, syndicates of banks typically assemble to finance large mines through SPVs (Cunningham, 2025).

Tensions, contradictions and initial decline

The trajectory of the envisioned regional green growth machine also reveals tensions between its export-oriented focus, local development needs, and socio-environmental impacts. While earlier energy planning documents had emphasized the potential role of wind power in decarbonizing the regional energy matrix and supporting isolated rural communities (Ministry of Energy, 2017), the political and institutional realignment toward green hydrogen has instead prioritized the mobilization of Magallanes’ wind resources for export via green hydrogen derivatives.

Following the classic growth machine dynamics described by Logan and Molotch (2007 [1987]), the coalition prioritizes the exchange value of the region's wind potential and available land over its use value for local communities 8 , raising questions about the distribution of benefits, local democratic participation, and environmental conservation (Flores Fernández, 2026; Norambuena et al., 2022). A member of a regional NGO argued that “The scale of the projects is completely out of proportion for the region and depends on a level of investment that will not materialize anywhere given the price of green hydrogen and its derivatives (…). As such, the whole narrative around land value appreciation, potential benefits and industrial development that underpins local support for the industry is nothing but a tall tale – one that lacks technical, economic, or socio-environmental viability” (similarly I_civil society_1, 4). Regarding the distributive aspects linked to the hype, biodiversity experts who have closely followed the advancement of the projects contend that “The eventual installation of giant wind farms, desalination plants and increased shipping traffic would affect the region's flora and fauna and its unique landscape, with only marginal employment benefits, while the main beneficiaries would be the importing countries, which could green their economies but at an enormous cost that they would be externalizing” (similarly I_public institution_20).

These tensions echo broader challenges regarding socioeconomic inequalities identified in research on green hydrogen elsewhere (Dejonghe and Van de Graaf, 2025; Kalt et al., 2023; Tunn et al., 2024). Recent developments highlight these tensions more concretely. HIF and ENEL withdrew from an environmental assessment after receiving numerous critical observations from public agencies and civil society (HIF and ENEL, 2022). Since then, public scrutiny has intensified, as evidenced by the mobilization of locals and NGOs, which submitted hundreds of observations on pending projects (Flores Fernández, 2026). While HIF's e-fuels plant and wind farm (372 MW) received their environmental approval in late 2025 and early 2026, HNH and TotalEnergies suspended their assessments, citing the extensive observations received (Diario Financiero, 2025). HNH reactivated the assessment in April 2026, while Total maintains its suspension until December 2026.

Contradictions of the regional growth machine are not limited to external critique. Internal fractures have begun to surface. According to a renewable energy developer “the excessive political focus on imaginary technologies like hydrogen has often relegated real sector technologies and problems to the background, such as focusing on the defossilization of the primary energy matrix or transmission bottlenecks” (similarly: I_civil society_3, I_public institution_2, 3). In other regions with potential local demand like the Chilean north, the shift toward more feasible decarbonization technologies has already revealed the fragility of the hype. For example, while the mining sector in the north initially explored green hydrogen applications (CORFO, 2018), a national government representative observed: “The truth is that mining is no longer interested in green hydrogen […] mining companies want to talk about electrification first. The hydrogen problem is fundamental: if you can electrify directly, it will always be more efficient. Why would they want hydrogen buses and trucks if they can electrify? […] It's cheaper, easier, and more efficient” (see for a technical explanation: Romm, 2025).

As indicated in earlier sections, the regional green hydrogen association constituted a key articulation point within the regional growth machine. However, this coalition has been slowly unraveling. In 2024, HIF withdrew from the H2V Magallanes Association arguing it would concentrate on its own projects. HNH Energy followed in early 2026, citing the need to reduce costs and exposure during a critical period for the sector. The final blow came in February 2026, when TotalEnergies left the association. With the departure of its last developer with an advanced project, the association was left without any major project developers and subsequently declared an indefinite recess (Prensa Austral, 2026). Representatives of the association justified these facts by citing “the absence of a consolidated market for green hydrogen and its derivatives, with no firm buyers or clear signals of international demand capable of sustaining large-scale, capital-intensive projects such as those being developed in Magallanes” (EMOL, 2026).

As lease contracts with landowners appear increasingly likely to be deactivated, associated service agreements will similarly unravel, reducing promises of productive transformation to a deferred promise. Nevertheless, the Chilean government, while redirecting its strategy towards domestic demand that remains difficult to articulate in Magallanes, remains cautiously hopeful about the sector's longer-term prospects (Ministry of Energy, 2026). When asked why the state was devoting such significant financial, institutional, and reputational resources to an industry characterized by deep market uncertainty, a CORFO official indicated that “Our policies and strategies respond to the possibility that European announcements and policies will work out, and to having done everything possible so that our country positions itself as a relevant producer and exporter”. These political bets could explain governmental reluctance in the face of signals of waning hype, illustrating – as Kuchler and Bridge argue for the case of shale gas promotion in Poland and the UK – “that political incumbencies were not interested in predicting or controlling the future, but rather benefited from, and sought to sustain, the existing conditions of uncertainty” (2023: 8). At least for a few years, sustaining the illusion of imminent cost competitiveness has enabled certain actors within the growth machine to accumulate enormous amounts of fictitious capital as examined in the next section.

Green hydrogen projects as fictitious capital

As discussed in the section “Growth machines and their green and regional variants”, actors participating in growth machines do not necessarily pursue identical objectives. While they converge around a shared development narrative, their strategies differ with regard to project realization and the accumulation of fictitious capital. In the case of the Magallanes green hydrogen growth machine, these differences are particularly visible among project developers, whose business models vary substantially depending on their financial capacity and position in the project development chain.

Two types of project developers operate within the growth machine: First, larger actors (Acciona & Nordex, RWE, TotalEnergies) capable of financing the multibillion-dollar construction phase given equity requirements; second, smaller firms (e.g.,: HIF, Rtb, Consorcio Austral, GH Energy) that create SPVs and advance early stages (e.g., pre-feasibility and feasibility studies), aiming to sell projects to larger investors once their value increases. In this process, value is added to project titles by advancing through early planning stages: completing studies, securing permits, or entering environmental assessment reduces uncertainty and increases the perceived likelihood that a project will ultimately be realized (Engelmann and Rohrmeier, 2022). The value of project titles therefore depends not only on the physical assets they may represent in the future, but also on evolving assessments of project feasibility and risk. These assessments are in turn shaped by broader public perceptions: periods of hype reflect positive expectations about project feasibility and thus inflate the valuation of project titles, whereas phases of disillusionment signal declining expectations and can lead to their rapid devaluation.

By selling project titles on to other companies, project developers can convert fictitious capital (ownership titles) into real capital (i.e., financial returns). As one of the smaller project developers explained: “The idea is not to develop the project entirely […] as that would be impossible […]. Instead, we are […] currently in advanced discussions to sell the project to a […] consortium of companies […] what we want […] is for the consortium to allow [us, the Chilean firm] to continue developing the project, but no longer as owners, only as project developers” (similarly I_project developer_4, I_consultant_8).

One project developer, GH2 Energy, successfully sold its project to Nordex and Acciona Energy (H2VMagallanes, 2024). As a regional industry representative indicates, “Other developers, such as Consorcio Austral, have managed to mobilize early-stage financing through sales of SPV shares and invested in baseline environmental studies”. While we could not obtain information on the sale prices of these project titles, they are likely small compared to the billions in capital that the projects require for completion; nevertheless, even a small fraction of those billions represents a substantial sum for a small project developer. At the same time, the fact that such transactions took place indicates that, at least at that stage, investors and acquiring firms still considered the projects sufficiently plausible to justify purchasing these titles. As one project developer noted: “Of course, public funding is scarce and the economic challenges are enormous, but we believe in the future of the industry and are confident that we will realize our project in the coming years” (similarly, I_project developer_6, I_public institution_6, I_public institution_7).

To assess the gap between the fictitious value, the projects would acquire after construction, the resulting financing needs, and the capital actually committed in the Magallanes region, we compiled a project inventory and estimated the financing and subsidy requirements of the projects using available benchmarks. We then compared these estimates with the subsidies provided by the state to close the competitiveness gap with gray hydrogen.

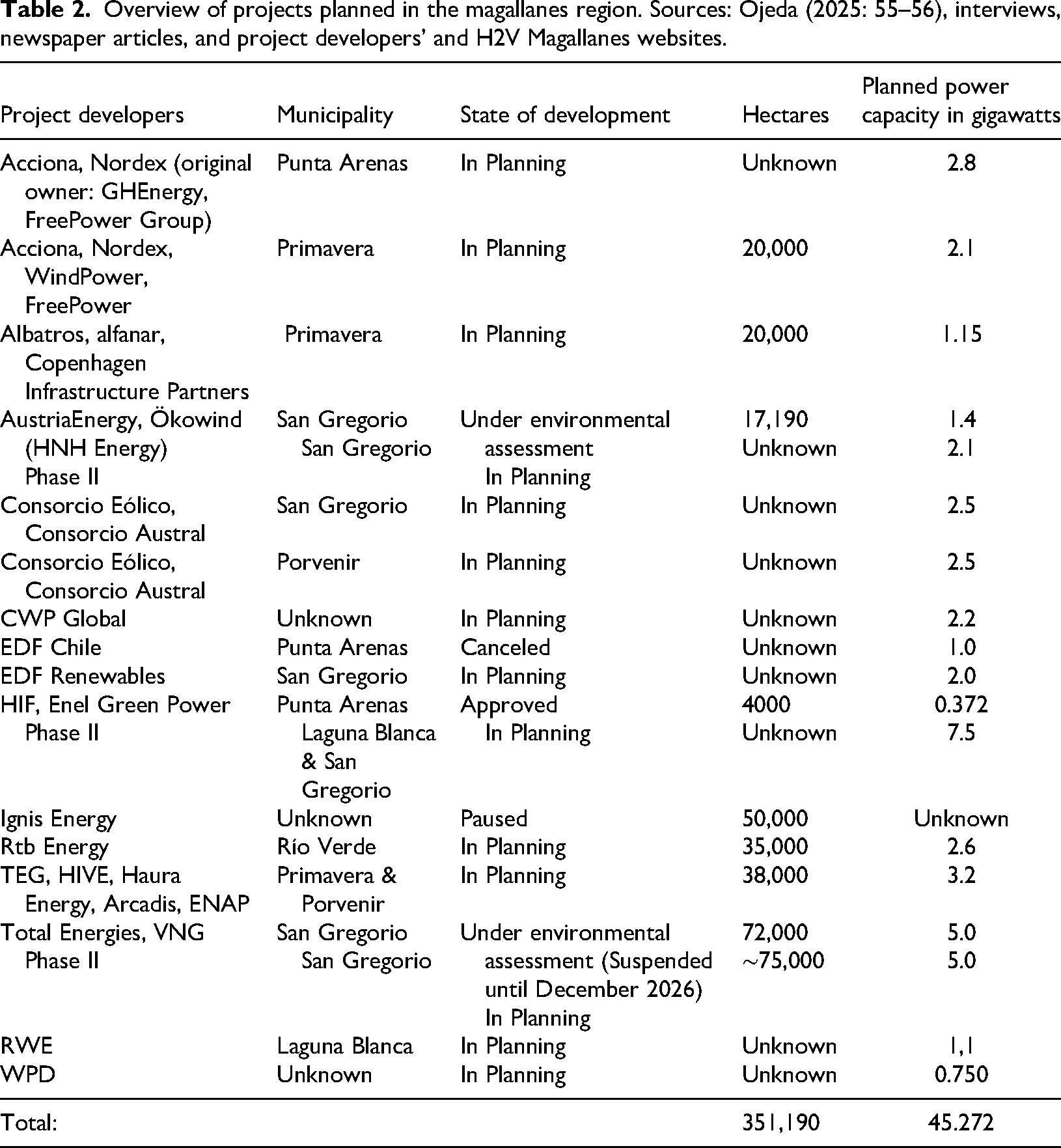

We identified 17 large-scale export-oriented green hydrogen and derivatives projects in Magallanes, totaling approximately 45 GW (Table 2) – about 2.6 times Chile's non-conventional renewable capacity and nine times its national wind capacity (CNE, 2025). Most project announcements span 0.75–2.8 GW, with two major exceptions: HIF (7.5 GW) and TotalEnergies (10 GW), based on all their planned project phases. The first phases of both projects are now in environmental assessment stages. All companies – except HIF that seek to produce eFuels – plan to export green hydrogen via ammonia, given it is technologically easier and economically cheaper to transport than pure hydrogen (Kojima and Yamaguchi, 2022). For its part, a recent government report indicates that by 2026, projects totaling approximately 23.2 GW in planned power capacity – equivalent to 10.3 million tons/year of green hydrogen output – are scheduled to enter environmental assessment. Over the long term, the report projects a regional maximum of up to 52 GW of wind capacity, supporting roughly 23.4 million tons of green hydrogen production per year, based on both announced and planned initiatives (Ministry of Transport and Telecomunication et al., 2024: 33).

Overview of projects planned in the magallanes region. Sources: Ojeda (2025: 55–56), interviews, newspaper articles, and project developers’ and H2V Magallanes websites.

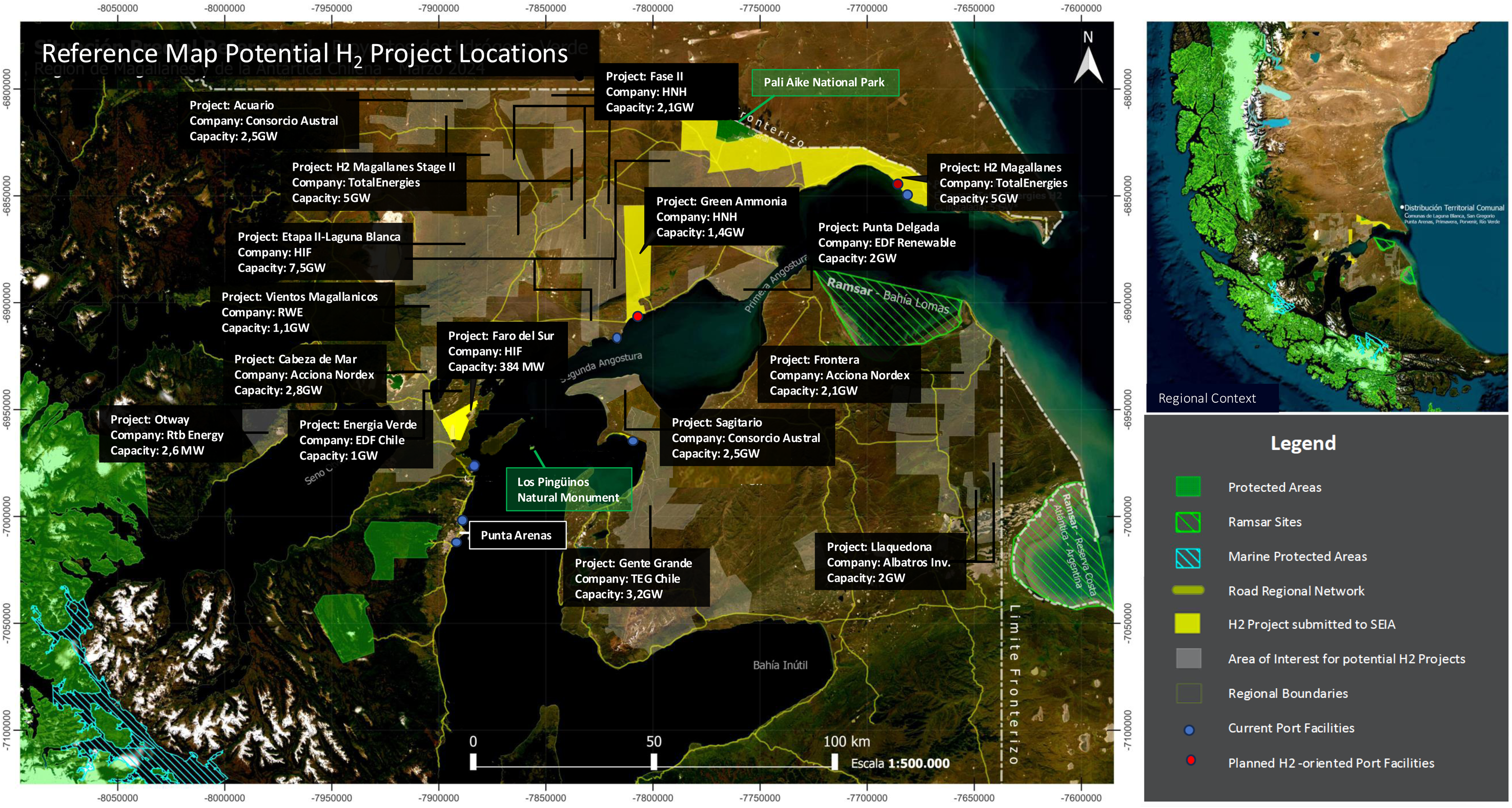

The announced projects cover a broad surface of the regional plain on both sides of the Strait of Magellan (see Figure 3). While only around half of the projects’ locations and expansion are publicly known, the following map gives an indicative idea of the land use intensification the projects would imply (see also: Flores Fernández, 2026; Walker et al., 2025).

Map of potential project locations, including the largest projects identified in Table 2. Own elaboration based on developer companies and H2V Magallanes websites, and reference property situation maps developed by CORFO and Flores Fernández (2026).

To valorize their SPVs, several corporate scouts have secured lease agreements with private landowners in areas with high wind energy potential as well as coastal proximity for desalination infrastructure and export. As a lawyer familiar with the negotiations explains, the interest of the landowners (estancieros) is tied to the materialization of real capital and ensuring that the projects are carried out in order to obtain the agreed-upon rents, while for the prospective developers “Securing these lease agreements, together with progress in community commitments and environmental permits, among other steps, allows the beneficiary company to position itself more favorably for eventual financialization” (similarly I_project developer_3).

To assess the structural gap between the financing and subsidies needed to realize the announced projects and the real capital actually mobilized, we draw on the figures presented in the section “Project development and financing as fictitious capital accumulation”. Assuming that developing an export-oriented green hydrogen project with 1 GW of power capacity costs roughly USD 2 billion 9 (Craen, 2023; Gielen et al., 2023), and that at least half of this investment must come from public subsidies to close the competitiveness gap (Laity, 2024), each GW would require about USD 1 billion in state support. Based on this benchmark, making the projects submitted to environmental assessment in Magallanes (about 6.8 GW of power capacity) economically viable would demand around USD 6.8 billion in subsidies. These figures exclude supportive infrastructures, such as planned port and road expansions (Agendamaritima, 2023), and rise to USD 23–52 billion if we consider the government projections (Ministry of Transport and Telecomunication et al., 2024), or USD 45 billion if all the projects outlined in Table 2 were to receive the necessary financial support.

In any of the preceding scenarios, the public subsidies announced by the Chilean government and its international partners are currently insufficient to finance more than one or two projects in the Magallanes region. In 2023, Chile announced a USD 1 billion “Facility” program administered by CORFO, though its operationalization remains pending. The Facility pools debt financing from the Inter-American Development Bank (USD 400 million), World Bank (USD 150 million), German Development Bank (USD 100 million), and European Investment Bank (USD 109.67 million) (Ministry of Energy, 2023b). The Chilean government planned to use the Facility to leverage private financing through concessional loans, with no direct equity investments foreseen, underscoring the limited scope of state intervention. As one government representative noted: “And for the state to invest? No. What is actually being done is creating incentives to support these initial projects, ultimately aiming to lower the final cost of hydrogen or [of] the project itself. […] Basically, these are [loans offered at] concessional rates that are lower than market rates”.

The USD 1 billion Facility could, in theory, support a single 1 GW project but only if the entire amount was allocated as direct subsidies. However, rather than concentrating resources in a single project, the government has opted for distributing its resources across regions (Scholvin and Kalvelage, 2025). As clarified by a government official: “What the Facility does is not to finance all green hydrogen projects. In fact, as a general rule, it will cover up to 10%, but it sends a signal to the market – a signal that the Chilean state is committed to engaging in the green hydrogen industry in the long term”. This strategy presents a structural dilemma. On the one hand, 10% of the Facility's value – amounting to USD 100 million per project – is far below what is required to finance multibillion-dollar projects and make them cost-competitive. On the other hand, Chile's national budget (approximately USD 85 billion) constrains the state's ability to assume the financial risk of focusing its limited resources on a single large-scale initiative (cf. Scholvin, 2025). For the same reason, the government does not want to hand out the money as subsidies but as loans. As noted by an industry representative: “Of course, these are loans, and while $1 billion is a considerable amount, for example, there is already a project undergoing environmental evaluation with an estimated investment of USD 2.5 billion […] Chile is a middle-income country, making it difficult for the government to make a large financial commitment to developing the industry” (similarly I_project developer_3). Hence, a financing gap exists both in regard to the scale as well as the willingness of the state to fully assume the cost gap between green and gray hydrogen.

This financing gap reflects a broader underestimation, within parts of the national government, of the degree to which project developers depend on state funding. In this line, government representatives indicate that: “I think that when projects start going through environmental impact studies, as we’re seeing now, there's a bit more seriousness […] I imagine that if it [a project proposal] comes from a company like HIF, which already has a plan, a pilot plant, and has gone through an initial Environmental Impact Assessment with a second attempt on the way, one would think there is more certainty about it” (similarly: I_public institution_7,8). This contrasts with the view of government representatives at the regional level, who are more skeptical about the desirability and feasibility of the industry. As one regional government representative states: “It is very likely that the number of proposed projects will grow from 15 to around 25, but in the end, no more than two or three will probably be executed. […] However, even one or two projects may be too much for the region” (Walker et al., 2025: 5).

International support may play a compensatory role, though such subsidies remain limited. An exception could be the German federal government, which has established the H2Global funding scheme. This mechanism conducts competitive international tenders to allocate public subsidies for green hydrogen and its derivatives (Kalvelage and Walker, 2024). As of mid-2025, H2Global is running continental tenders – including one specifically targeting Oceania and Latin America – to distribute up to EUR 484 million in direct subsidies. While developers in Magallanes are eligible to compete, the high investment volumes required mean that at most one project could secure financing through this mechanism.

Against this background, it appears highly unlikely that more than two projects in the Magallanes region could secure enough subsidies, reach a final investment decision and proceed to construction, even under optimistic assumptions. One project might be realized through a concentrated national support package, while another might access international funding. The remaining projects will therefore remain fictitious capital, whose value is likely to decline as the projects’ missing business case and their inability to secure subsidies becomes evident. Reflecting this assessment, the national government recently revised the goals of its green hydrogen strategy downward, now aiming – more modestly – for at least two industrial-scale projects to reach FID by 2030 at the national scale (Ministry of Energy, 2026: 54).

Taken together, these trends reflect a broader disillusionment with the green hydrogen hype and its speculative underpinnings, both in the Global South and globally, marked by an increasing number of project cancelation and abandonments (IEA, 2025: 7). As the hype cycle fades, the growth machine unravels and the coalition fractures: large-scale projects may be canceled (like EDF´s Energía Verde Austral), or enter indefinite hibernation, awaiting more favorable market/financing conditions or policy frameworks that may or not materialize (Diario Financiero, 2026). Smaller developers, meanwhile, confront the fictitious nature of their ventures and tend to dissolve altogether as their SPV ownership titles devalued. Landowners in turn, watch their anticipated green source of land valorization slip away, prompting them to seek alternative strategies.

Conclusions

Our analysis demonstrates that the green hydrogen industry has evolved into a complex growth machine, successfully mobilizing climate imperatives and green industrialization narratives to legitimize new forms of speculative development (Carrasco et al., 2026; Flores Fernández, 2026). Yet it remains constrained by the structural limitations of the sector, which produce persistent tensions between ambitious announcements and material implementation (Johnson et al., 2025; Odenweller and Ueckerdt, 2025).

Answering our first research question – who drives and sustains the green hydrogen hype in Magallanes, how and why – we find that a sophisticated multi-scalar coalition has emerged, encompassing actors ranging from local landowners, national and regional governments to international agencies and diverse companies. The Magallanes case illuminates how contemporary growth machines have evolved to incorporate environmental sustainability imperatives while maintaining their fundamental orientation toward exchange value maximization and rent capture (Dilworth and Stokes, 2013). This represents an adaptation of traditional growth machine strategies to emerging green industrial sectors in rural and peripheral areas. In particular, export-oriented green hydrogen projects promise the growth machine opportunities for land-use intensification, transferring dynamics primarily observed in urban energy transitions of the Global North to some of the most peripheral regions globally (Huber and McCarthy, 2017; Walker, 2022).

Regarding why the identified actors and coalitions have driven and sustained the hype, our findings point to differentiated motives despite a shared vision. Governments that have politically invested in the green hydrogen agenda have made it part of their policy legacy, making uncertainty a useful tool for postponing reckoning with its actual viability. For developers, maintaining the hype preserves manifold opportunities – mobilizing financing and subsidies, greening their portfolios and enabling continued investment in fossil assets (e.g., TotalEnergies) – while sustaining the expectation that fictitious capital tied to early-stage projects may eventually materialize as real capital.

Addressing our second research question – how can different actors derive value from green hydrogen projects without them being built – we find that SPVs function as the central tool enabling speculative accumulation in advance of actual project materialization. Through SPVs, project developers can commercialize ownership stakes long before construction begins, creating forms of capital that can be accumulated independently of underlying productive assets (Baker, 2022; Hunt and Tilsted, 2024).

By answering our last research question – to what extent is there a gap between the financing needs of announced projects and the capital actually being committed to their development in the Magallanes region? – our empirical analysis provides a distinctly regional perspective on the “implementation gap” identified in recent literature (Odenweller and Ueckerdt, 2025). Despite 17 large-scale project announcements implying a fictitious multi-billion-dollar value for the regional industry, available financing mechanisms suggest that under optimistic assumptions only one or two projects in the Magallanes Region are likely to secure sufficient funding. This disconnect between announcement and financing realities shows how the hype functions as a political instrument to secure state support while deferring scrutiny of economic and socio-ecological viability (Szabo, 2021; Vezzoni, 2024).

Our article highlights a broader gap in the rapidly growing social science literature on green hydrogen, which has so far engaged only limitedly with the material and financial foundations of the industry and the question of its economic feasibility (Walker and Kalvelage, 2025). The concept of fictitious capital (Baker, 2015; Durand, 2017; Palludeto and Rossi, 2022) provides a useful lens to interpret these dynamics, distinguishing between the speculative future value attributed to the industry, the valuation of present-day ownership titles, and the comparatively limited real financial flows observed in practice. However, this study examines the articulation, peak, and ongoing phase of disillusionment associated with the green hydrogen hype, but therefore does not capture a potential ‘enlightenment’ phase within the hype cycle, in which a ‘technology reveals its actual value and diffuses more widely’ (Kriechbaum et al., 2021: 2). Future research should critically engage with the economic feasibility of hydrogen projects across different scales and contexts, helping stakeholders develop a more realistic understanding of the industry's viability and the conditions under which hydrogen might genuinely contribute to just and sustainable regional development. Research should also identify ways of deploying limited public funds more effectively to support hydrogen projects needed to decarbonize the existing gray hydrogen market.

This work highlights that the central challenge is not only in which sectors to pursue green hydrogen (Johnson et al., 2025), but how to (better) govern hypes and distinguish productive positive expectations from unproductive speculation. While the technology may represent a necessary component of industrial decarbonization, technological hypes may also hinder rather than accelerate decarbonization efforts (Hunt and Tilsted, 2024; Szabo, 2021; Vezzoni, 2024), making the development of governance mechanisms capable of identifying and curbing predatory delay a pressing priority.

Moreover, our research highlights a fundamental challenge in the current phase of the energy transition: as relatively low-cost decarbonization options – such as electrifying ground transport – are increasingly implemented, more expensive challenges, like decarbonizing energy-intensive sectors including hydrogen production, remain (Walker and Coulomb, 2026). We find that societal consensus appears to persist only while overly optimistic expectations promise benefits for all. However, once these expectations are confronted with reality, support can quickly erode, stalling progress. In this context, a key challenge is to use periods of hype as windows of opportunity to assemble the substantial capital required for these costly decarbonization efforts, especially as both public and private investors have recently become far more cautious about mobilizing investment – let alone subsidies – for green hydrogen (IEA, 2025). Therefore, further research should explore how to address these high-cost decarbonization challenges and develop governance mechanisms that ensure effective progress as well as a fair distribution of both benefits and costs.

In this sense, the article contributes to debates on energy justice (Kalt et al., 2023; Wolch et al., 2014) and transition governance (Klagge et al., 2025) by showing how speculative, project-based transitions can crowd out alternative decarbonization pathways, locking political attention and resources into uncertain futures while foreclosing more grounded approaches to regional energy needs. A reorientation would require shifting from promotional support for the sector as a whole toward selective and adaptative evidence-based backing for projects with credible pathways to operation, while simultaneously investing in decarbonization alternatives that address Magallanes’ actual decarbonization challenges and ensure local beneficiation.

Our analysis showed that if the state's intention was to promote projects at the scale envisaged by project developers, it would have needed to concentrate the available grants on one or two key projects to make them cost-competitive. Moreover, support would need to have been provided not in the form of concessional loans, but as non-repayable grants to be more effective. By relying on concessional loans while simultaneously aiming to support multiple projects, public resources were spread too thinly. This finding reflects the limited state capacity to develop a governance strategy capable of identifying the most promising project developers and projects, and of concentrating public resources on those initiatives — or alternatively, of opting for the scaling of smaller projects by prioritizing demand in the first instance. As other authors have previously argued, such state capacities are particularly important for linking the energy transition with territorial development (Carrasco, 2025; Carrasco and Madariaga, 2026; Collington, 2026). Rather than relying on hydrogen strategies developed by actors such as McKinsey – who simultaneously produce hydrogen strategies for industry lobby associations – the state should have the capacity to evaluate the technical expertise and material interests of project developers, to set them in competition with one another, and, on this basis, to concentrate its limited resources on selected projects and bring them to fruition. The Namibian state can serve as an instructive example in this regard – despite its very limited resources (Kalvelage and Walker, 2024). These observations point to key research needs: what capacities do states require to steer energy transitions through periods of hype and confront high-cost decarbonization challenges, and how can state capacity be built?

Highlights

Green hydrogen hype in Magallanes is driven by multi-scalar coalitions seeking to develop the region as export hub Export-oriented megaprojects tend to prioritize international markets while constraining domestic policy autonomy and local energy needs Speculative or fictitious capital accumulation around these projects occurs through ownership trading before actual construction begins Current speculative dynamics may delay genuine decarbonization efforts both globally and locally Declining hype opens opportunity to prioritize feasible peripheral development paths within the transition framework over speculative capital accumulation

Footnotes

Acknowledgements

We thank our interviewees for their time and the valuable insights they provided.

Benedikt Walker would like to acknowledge funding by the German Research Foundation (DFG) through funding for the project “Governance of the German hydrogen economy and the globalization of the German energy transition” (grant number 524816877).

Cristián Flores Fernández would like to acknowledge funding by the Deutscher Akademischer Austauschdienst (DAAD) (grant number 57552340) and by the Humboldt-Universität zu Berlin.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Deutsche Forschungsgemeinschaft, Deutscher Akademischer Austauschdienst, (grant number 524816877, 57552340).