Abstract

By using indications given by the commodity markets, farmers, growers, or producers can minimize the price risk and avoid a supply gut. The consumers of the output can minimize the price risk and ensure that the demand pressure is appropriately capped. It was in this backdrop that farmers and food grain merchants initiated futures markets in agri-commodities. This article has been successful in documenting the evolution of agri-commodities futures markets in India and their regulatory framework. It also captures the transition toward agri-commodities futures by engaging in a comprehensive survey of extant literature. The market growth analysis indicates that the transition toward agri-commodities futures markets has enabled price discovery and better price risk management. While ensuring price risk mitigation and remunerative returns, these markets also contribute to scaling down the downside risks associated with agricultural lending and, thereby, facilitate the flow of credit to agriculture. Further, they also hold a key role not only in reinvigorating the spot markets but also in triggering the diversified growth of Indian agriculture in line with the consumption pattern. Thus, enabling policies need to be put in place to strengthen the agri-commodities futures markets by streamlining the supply chain.

Introduction

Agriculture and allied sector continue to play an important role in India as they ensure food security of about 1.3 billion people, employing more than 50% of the workforce, and make a contribution of about 15.4% (GoI, 2018) to the country’s gross domestic product. The developments in the sphere of Indian agriculture led to the growth of Indian agri-commodities market. India is the largest consumer of commodities such as precious metals (bullions and silver), metals (copper, zinc, lead, etc.), and agricultural products (cotton, pepper, maize, wheat, sugar, coffee, dairy products, chili, etc.). The existence of commodity markets can be considered as old as Indian history itself. Broadly, commodity markets including agricultural commodities exist in two forms—spot markets and exchange-based markets. In spot markets, the payment and delivery are immediate, and therefore, all transactions are over-the-counter (OTC) transactions, whereas ‘futures’ are standardized financial contracts for the respective commodities traded in the exchanges.

Agricultural producers are prone to several risks such as price, crop and weather/climatic variations, and a number of other natural disasters, which could affect their anticipated income very badly and could have negative effects on the standard of living, ability to build capital, and facility to access credit and repay debts. The uncertainty of commodity prices leaves a farmer open to the risk of receiving a price lower than the expected price for his yield. Often, the price farmers get for their produce at the marketplace does not even cover their investment in farming operations. On the other hand, big farmers are affected equally badly when prices are not attractive or crash at the marketplace. Hence, a way out of this vicious cycle must be found and that is where the commodity markets come in. By using indications given by the commodity markets, farmers, growers, or producers can minimize the price risk and avoid a supply gut. The consumers of the output can minimize the price risk and ensure that the demand pressure is appropriately capped. It was in this backdrop that farmers and food grain merchants in Chicago initiated negotiations for supply of grains at a future date in exchange for cash at a price mutually agreed upon. It is believed that commodity futures have existed in India for thousands of years.

In this context, this article attempts to documents the evolution of agri-commodities futures markets in India and their regulatory framework. Secondly, a structured survey of extant literature has been conducted to capture the transition toward futures. The third objective is to find out the recent trends and developments in Indian agri-commodities futures trading. In order to achieve these objectives, a comprehensive survey of extant literature has been conducted in the first place. Thereafter, content analysis has been applied to focus on the research constructs. Furthermore, secondary data have been extracted from operative Indian commodity exchanges and survey of Indian economy to present the trend analysis of agri-commodities future trading. This article is organized in five sections including introduction and conclusion. The second section depicts the evolution and regulatory framework of agri-commodities markets in India. The third section presents a structured review of literature. The fourth section captures the recent developments of Indian agri-commodities futures trading. The last section presents the discussion and conclusion.

Evolution and Regulatory Framework of Futures Markets

The origin of futures trading is traced to Japan in the seventeenth century, and the Dojima Rice Exchange in Osaka, Japan, is said to be the world’s first organized futures exchange where trading started in 1710. On April 3, 1848, the Chicago Board of Trade (CBOT) was established by 83 merchants to facilitate trade in spot produce and forward contracts. It was only in 1865 that standardized futures contracts were introduced. The Chicago Produce Exchange was established in 1874 and the Chicago Butter and Egg Board in 1898. In 1919, it was reorganized to enable future trading and was renamed Chicago Mercantile Exchange. The primary aim of the Exchange is to bring a large number of buyers and sellers on the same platform for spot price discovery and to make sure that the commodity bought and sold on the Exchange is delivered on time without the counterparty risks to the traders.

Pre-Independence Period

Organized trading in commodity futures in India was reported to have started in the latter part of the nineteenth century at Bombay Cotton Trade Association Ltd (established in 1875). Following cotton, derivatives trading started in oilseeds in Bombay (1900), raw jute and jute goods in Calcutta (1912), wheat in Hapur (1913), and in Bullion in Bombay (1920) (Mukherjee, 2011). However, many feared that derivatives fueled unnecessary speculation in essential commodities and were detrimental to the healthy functioning of the markets for the underlying commodities and, hence, to the farmers. With a view to restricting speculative activity in cotton market, the Government of Bombay prohibited options business in cotton in 1939. Later, in 1943, forward trading was prohibited in oilseeds and some other commodities including food grains, spices, vegetable oils, sugar, and cloth (Seilan, 2010). There were no uniform guidelines or regulations, and trade was dependent on mutual trust and social control. In 1947, the Bombay Forward Contracts Control Act was enacted by the Bombay State for facilitation of trade.

Postindependence Period

The legal framework for organizing forward trading and the recognition of Exchanges was only provided after the adoption of the Constitution followed by a central legislation called Forward Contracts (Regulation) Act 1952. Through a notification issued on June 27, 1969, by exercising the powers conferred upon the central government by the Securities Contracts Regulation Act 1956, forward trade was prohibited in a large number of commodities, leaving only seven commodities open for forward trade. This resulted in a decline in traded volumes on stock markets and led to the evolution of an informal system of forward trading by the Bombay Stock Exchange in 1972. However, this created payment crises quite often. In the 1980s, the futures trading in some commodities such as potato, castor seed, and gur (jaggery) was permitted. In 1992, futures trading in hessian was permitted. Then came the relief in the form of recommendations from the Kabra Committee in 1994 1 . There were a number of other expert committees, including the Shroff Committee, Dantwala Committee, and the Khusro Committee, which laid the foundation for the revival of futures trading. Thereafter, in April 1999, futures trading in various edible oilseed complexes was permitted, and in May 2001, futures trading in sugar was permitted. Another landmark development came in the year 2000 when the national agricultural policy was announced in July. It recognized the positive role of forward and futures market in price discovery and price risk management. This has also expressed support for commodity futures. The Expert Committee (Guru Committee) on Strengthening and Developing Agricultural Marketing (Govt. of India (GOI), 2001) emphasized ‘the need for and role of futures trading in price risk management and in marketing of agricultural produce.’

Physical trading of agricultural commodities in India falls under the jurisdiction of the state governments. Each state has its own Agricultural Produce Market Committee (APMC) Act to regulate physical trading of commodities. The APMC Act requires buyers and sellers to assemble at designated places known as regulated market yards. Each regulated market yard is governed by a market committee, which is expected to facilitate competitive price discovery for farmers. Once a state government declares a particular area to be part of a market committee, all wholesale trading in that area has to be undertaken at the designated regulated market yard only. The failure of APMCs to provide a competitive market has been highlighted in the report titled ‘Final Report of Committee State Ministers, In-Charge of Agricultural Marketing to Promote Reforms’ (2013).

Forward Markets Commission (FMC) used to be the regulatory body to regulate commodity futures trade and control the activities of commodity exchanges similar to how Securities Exchange Board of India (SEBI) regulates the functions of capital market. However, the commodity derivatives market in India has now come under the regulation of SEBI following merger of FMC with it since 2015. Currently, both futures and options are permitted in the Indian commodity derivatives markets. Derivatives trading is permitted in 91 notified commodities, of which derivatives contracts for around 40 commodities are presently offered for trading by the commodity derivatives exchanges. At present, there are 6 national commodity exchanges 2 and 23 regional commodity specific exchanges operating in Indian commodity futures market. Subsequently, SEBI has implemented a slew of advancements within the commodity market space 3 .

Review of Literature

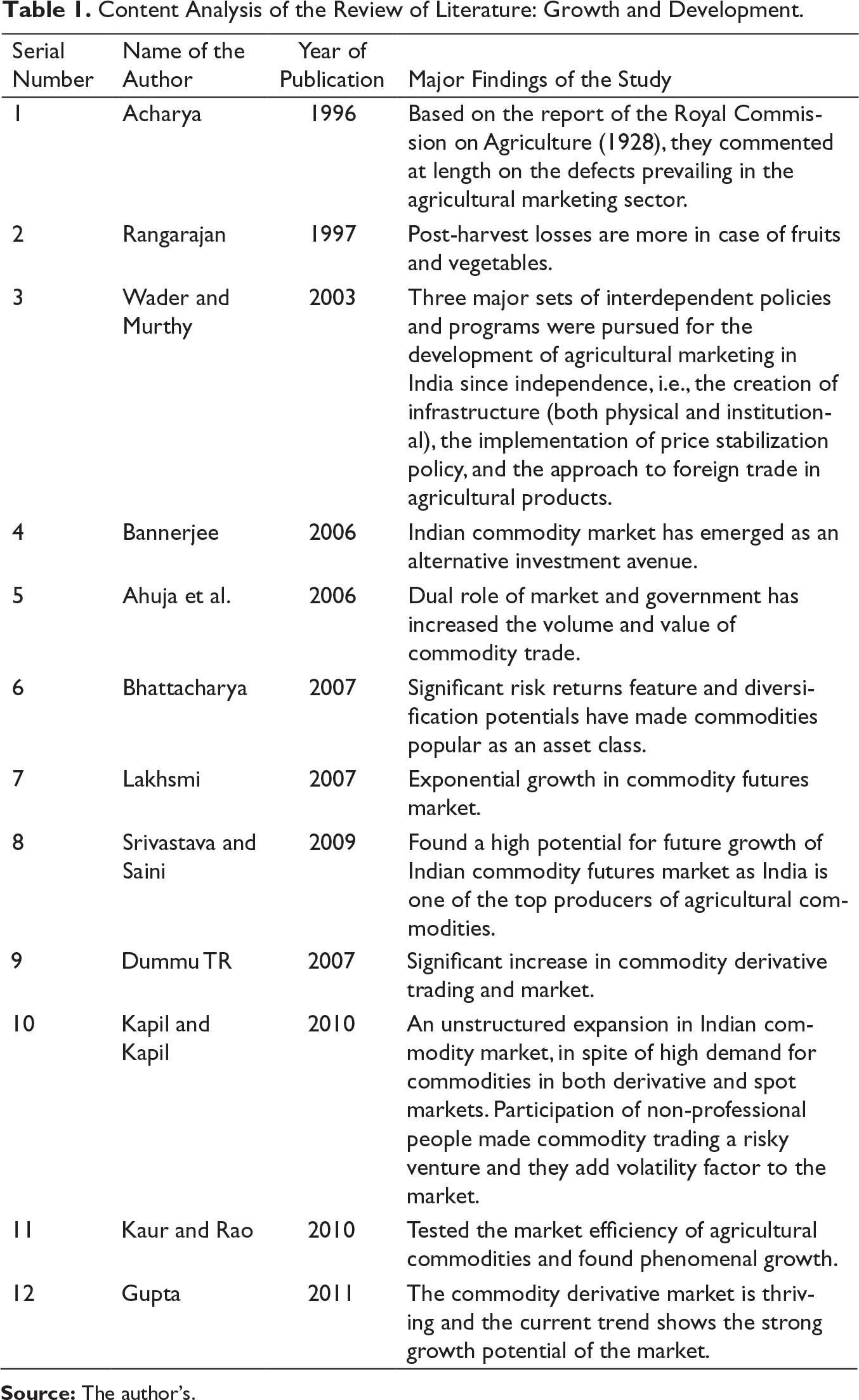

An understanding of futures markets is illustrated by Sharon (2005) wherein he categorized commodity futures into three types, that is, agricultural commodity, energy commodity, and metal commodity, while giving a detailed description on the basis of how it affects commodity futures. It also explains the variation in basis across commodities and reasons for the same. Using commodity futures to hedge the commodity price risk helps in avoiding uncertainty of future cash flows and facilitates locking in the price. In other words, it helps in minimizing the price risk, but not completely avoiding the losses. Sometimes the unhedged position may provide better results than the hedged one. Commodity futures allow both the producers and consumers of agricultural products to manage the price risk that might arise due to various factors. Having experienced agricultural liberalization which has facilitated commodity trading, India is still away from achieving the benefits of commodity markets. In order to develop the commodity market, it is necessary to understand the constraints involved in better development of commodity trading and find out ways of dealing with them. In this backdrop, an attempt has been made to present a review of extant literature in a structured manner for the Indian agri-commodities market to pinpoint the understanding and focus on the market and the constraints. This has been achieved through a content analysis of the available literature and presented in the form of tables under three categories: (a) growth and development, (b) perception and awareness, and (c) price discovery.

Growth and Development

Systemic changes brought about by liberalization, global economic recovery, growing awareness about derivatives trading and their ability to reduce the underlying risk, etc., have caused a revolutionary change in the commodity market. However, as compared to global commodity derivatives markets, the Indian commodity market is still in a developing stage because of various lags between the policies, poor implementation process, lack of awareness, and the improper impact of various reforms. It has been reported that commodity derivatives trading in India has come out of the state of hibernation in the last few years and is progressing (Bannerjee, 2006). Gupta (2011) found that starting from the time it was reintroduced, the commodity derivative market has been growing at a fast pace and promises a solid growth potential of this market. The actual growth pattern will depend upon the efficiency of the regulatory mechanism and attitude of the policymakers. Indian futures markets have achieved a sizeable growth due to removal of ban from commodity trading (Srivastava & Saini, 2009). Dummu TR (2007) found that after the government removed protection from various commodities, there has been a massive progress in trading activity and trading volume in Indian commodity futures market. A large number of studies have supported the fact that commodity derivative market played a significant role in price risk management.

Content Analysis of the Review of Literature: Growth and Development.

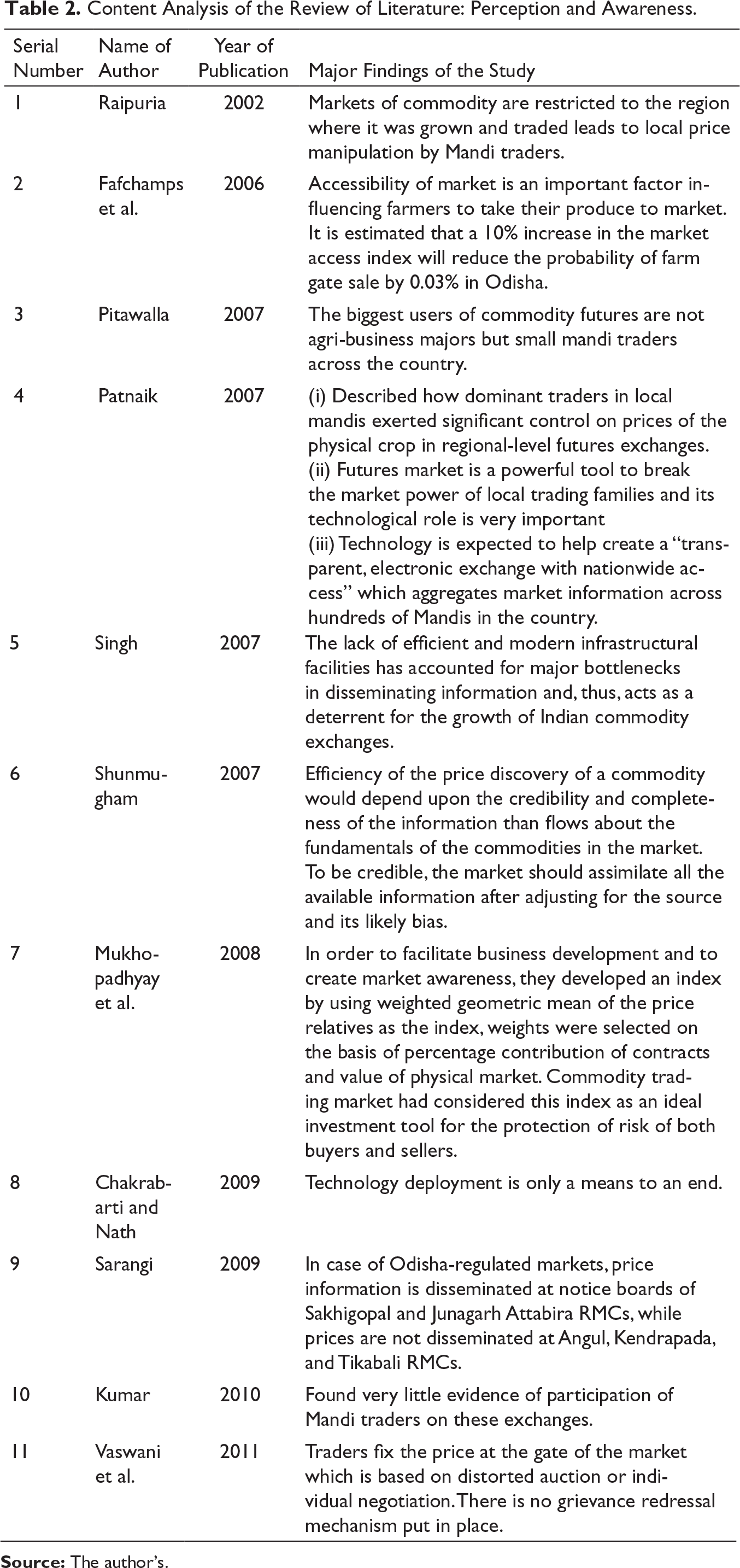

Perception and Awareness

In a significant revelation, Pitawalla (2007) states that ‘small mandi traders across the country are the biggest users of commodity futures and not agri-business majors.’ This indicates the awareness of local stakeholders for wider participation. The first surge of contracts has come from the traditional traders operating out of the 7000 odd Mandis across the country. Furthermore, Patnaik (2007) described how in local Mandis, dominant traders exerted significant control on prices of the physical crop in regional-level futures exchanges. He also explained that ‘futures market is a powerful instrument to reduce the market power of (local trading) families.’ As various participants buy and sell a commodity, they bring information and expectations about the market they may possess to the price. Raipuria (2002) found markets in a given commodity were restricted to the region in which it was grown and traded. This made the trade amenable to local price manipulation by Mandi traders who were the main participants in the exchange. However, Kumar (2010) found very little evidence of participation of Mandi traders on these exchanges. At the same time, it is known that their knowledge about agrarian markets and their everyday participation in physical market activities makes them important players in India’s agricultural production system.

Content Analysis of the Review of Literature: Perception and Awareness.

Price Discovery

Figuerola-Ferretti and Gonzalo (2010) concluded that futures markets contribute to the organization of economic activity in two important ways: first, futures markets facilitate price discovery, and second, they offer mode of risk transfer and hedging. Through application of different methodologies, many scholars such as Tan and Lim (2001), Daigler (1990) and Tse (1999) have studied one market’s dominant role on the other for the purpose of price discovery. According to United Nations Conference on Trade and Development (UNCTAD) (2008) report, policymakers and regulators, especially in emerging markets, have been increasingly looking at the establishment of ‘indigenous’ commodity exchanges in their domestic markets, providing local price discovery and accessible trading and risk management instruments for commodity chain participants with the support of the broader financial and investment communities. This is further elaborated by several authors where it was propounded that price discovery is highly useful to all segments of the economy, as a producer gets an idea of the price likely to prevail at a future point of time and, therefore, can decide between various competing commodities and choose the best that suits him, whereas a consumer simply gets an idea of the price at which the commodity will be available in the future, thus helping him in buying decisions. In their seminal work, Garbade and Silber (1983) concluded that risk transfer and price discovery are considered as two major contributions of futures market toward organization of economic activity. Another revelation by Zhong et al. (2004) stated that in case of efficient markets, new information is assimilated simultaneously into futures and cash markets. One can come to a logical conclusion that financial market pricing theory states that market efficiency is a function of how fast and how much information is reflected in prices. The study by Zapata et al. (2005) suggests that the rate at which prices exhibit market information is equal to the rate at which this information is disseminated to market participants. Thomas and Karande (2001) investigated the castor seed futures market traded on the regional exchanges in Ahmedabad and Mumbai for the presence of price discovery process and concluded that each regional market reacted differently to information in the price discovery of castor seed. They found that although there was no lead–lag relationship found between the spot and futures market in Ahmedabad market, the futures market in Mumbai dominated the spot market heavily. Kumar (2004) employed the Johansen cointegration technique and concluded that futures market was unable to incorporate information from the spot market, whereas Sahi and Raizada (2006) found the dependence of commodity future market on spot market for price determination. By employing the cointegration test to examine the linkages between Indian castor seeds futures and spot market, Lokare (2007) found cointegration of commodity future and spot prices revealing the right direction of achieving the improved operational efficiency at a slow rate. Mahalik et al. (2009) also supported the notion that commodity future market is efficient for price discovery in the case of agricultural commodities. Roy (2008) investigated 32 wheat futures contracts in India and concluded that wheat futures markets are well cointegrated with their spot markets. They also observed bidirectional causality in majority of the wheat futures contracts. This is further validated by Iyer and Pillai (2010) who used two-regime threshold vector autoregression (TVAR) for six commodities to investigate whether futures markets play a dominant role in the price discovery process. Shihabudheen and Padhi (2010) studied six Indian commodities, that is, castor seed, jeera, sugar, gold, silver, and crude oil, for price discovery mechanism and volatility spill overs effect and concluded that futures price acts as an efficient price discovery vehicle for five of the six commodities except for sugar. They also concluded that volatility spill over from futures market to spot market exists for five of the six commodities except sugar. Pavabutr and Chaihetphon (2010) demonstrated that futures prices of both standard and mini contracts lead spot price. The study of Srinivasan and Ibrahm (2012) explored that spot markets of MCXCOMDEX, MCXAGRI, MCXENERGY, and MCXMETAL serve as effective price discovery vehicles. Furthermore, volatility spill overs to futures from spot market are dominant in case of all MCX commodity markets. Chakrabarty and Sarkar (2010) confirmed the cointegration between commodity futures and commodity spot market indices. They emphasized that with the information of any one index, hedging can be done on other commodity indices. Samal et al. (2015) studied the turmeric futures from NCDEX and concluded that futures markets of turmeric help to discover prices in the spot markets.

Karande (2007) proved that commodity futures market performs the function of price discovery and has proven beneficial to spot market by reducing the spot price volatility. The same is also validated by Sinha and Bhuniya (2011). Shah (2007) found that the liquidity is essential for a futures market to function efficiently and to facilitate better price discovery, especially when there are huge agribusinesses trying to hedge on the markets. On the same line, Kaur and Rao (2009) found commodity future and spot prices had tracked each other closely in some agri-commodities, and no significant volatility in the prices of future and spot contracts of those agricultural commodities has been noticed in it. Kumar and Pandey (2013) found that the comparative advantage enjoyed by the futures market in disseminating information, leading to an accurate price discovery and risk management, may help in successfully developing the underlying commodity market in India. Furthermore, this study identified that there are speculators in the commodity market also, but there is nothing wrong in it; rather, speculators help toward price discovery along with hedgers and arbitrageurs. On the other hand, by allowing wider participation through dissemination of information, these exchanges discourage cartelization on the part of local traders and associations. Commodity derivative trading provides better risk management along with price discovery, as Sahoo and Kumar (2009) did not find any evidence supporting the fact that future market causes higher inflation.

Content Analysis of the Review of Literature: Price Discovery.

Trends of Agri-Commodities Futures Trading

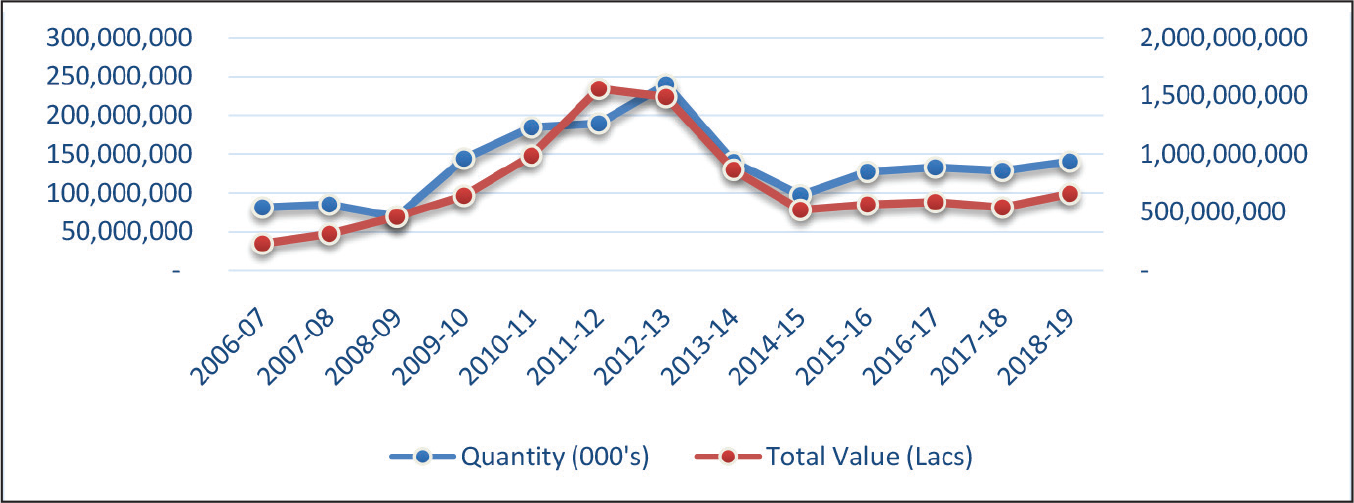

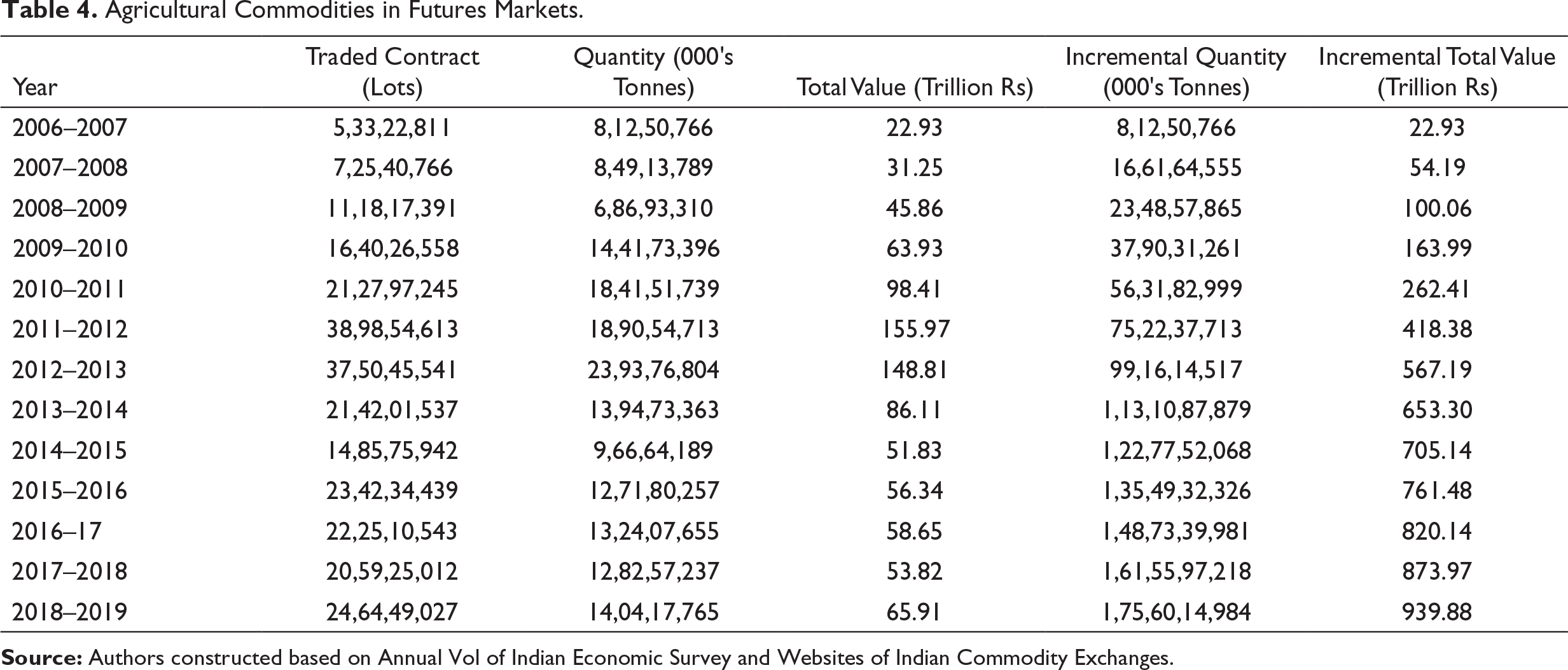

Although India has a long history of trade in commodity derivatives, this sector remained underdeveloped in the past due to government interventions either in restricting or banning many commodity markets from controlling prices. Among the commodity exchanges, NCDEX and NMCE are focusing on agricultural commodities. As on end December 2017, there were 29 agricultural commodities that were allowed by the SEBI to be traded at various commodity stock exchanges. Nevertheless, in the calendar year 2017, India’s Guar Seed futures contract had made it to the top 40 agricultural contracts traded worldwide. The total value of agri-commodities futures had a steady increasing trend till 2011–2012, as depicted in Table 4 and Figure 1. Thereafter, the growth momentum began to show a declining trend till 2014–2015. There was a marginal increase in the value of trade comprising ₹56.36 trillion in 2015–2016. The total value of agri-commodities futures traded in 2018–2019 stood at ₹65.91 trillion from a high of ₹155.97 trillion in 2011–2012 (see Table 4 and Figure 1).

Agricultural Commodities in Futures Markets.

Although agricultural commodities led the initial spurt and constituted the largest proportion of the total value of trade till 2005–2006 (55.32%), this place has been taken over by bullion and metals since then. This was partly due to the stringent regulations, like margins and open interest limits, imposed on agriculture commodities and the dampening of sentiments due to suspension of trade in some commodities (Seilan, 2012). The quantity and value of agri-commodities futures traded are shown in Figure1, which implies that maximum quantity was traded in 2012–2013, whereas maximum value of trading was reported in 2011–2012. Most importantly, the behavior of the quantity and value graph is in the same pattern. This overall analysis of 13 years of data indicated that an archaic market has suddenly turned into an organized, service-oriented set-up producing substantial volumes of trade. This is in line with the findings of several studies which proved that the futures markets have developed steadily, while the spot markets are still largely unorganized (Hegde & Madhuri, 2013; ICAR, 2013). The success of the futures market has ensured toward integration of spot with futures markets, and accordingly, the launch of electronic national spot markets for agro-products had become a reality in 2017. Being in a time zone that falls in the gap left by the major commodity exchanges in the USA, Europe, and Japan has also worked in India’s favor because commodity business by its very nature is a 24/7 business.

Discussion and Conclusion

Both agricultural commodities and agricultural marketing in India are in the domain of states. Most of the states have enacted APMC Act to provide for regulation of agricultural produce markets. These regulated markets have aided in resolving some of the issues and problems. However, the rural markets by and large remained out of their developmental ambit. The agriculture sector needs well-functioning markets to drive growth, employment, and economic prosperity in rural areas of the country. There is an urgent need to garner large investments for the development of post-harvest and cold chain infrastructure nearer to the farmers’ field that would provide dynamism and efficiency to the marketing system. According to the APMC Act, farmers cannot sell directly to ultimate buyers such as processors, exporters, and retailers and, hence, sell their produce to traders or local aggregators. Processors, exporters, and retailers in turn buy from local aggregators. This increases the number of intermediaries and leads to higher costs. Besides these non-value-adding transaction costs, there is a lack of standardization across the regulated market yards in terms of quality or other costs. Different state governments levy different taxes on transactions conducted at these market yards. As a result, the spot prices prevailing at these markets vary widely for a commodity.

Agricultural commodity futures are market-based instruments for managing risks and they help in orderly establishment of efficient agricultural markets. They also serve as a low cost, highly efficient, and transparent mechanism for discovering prices in the future as they provide a forum for exchanging information about supply and demand conditions. The hedging and price discovery functions of future markets promote more efficient production, storage, marketing, and agro-processing operations. Hence, this helps in improving the overall agricultural marketing performance. The transition toward, agri-commodities futures markets has enabled price discovery and better price risk management. While ensuring price risk mitigation and remunerative returns, these markets also contribute to scaling down the downside risks associated with agricultural lending and, thereby, facilitate the flow of credit to agriculture. Besides, through the use of warehouse receipts, these markets obviate the need for collaterals, the lack of which has currently impeded the flow of agricultural credit. They also hold a key role not only in reinvigorating the spot markets but also triggering the diversified growth of Indian agriculture in line with the consumption pattern. Thus, enabling policies need to be put in place to strengthen the agri-commodities futures markets by streamlining the supply chain.

Footnotes

Declaration of Conflicting Interests

Funding

The author received no financial support for the research, authorship, and/or publication of this article.