Abstract

Non-banking financial companies (NBFCs) have stayed in the shadows for far too long and played second fiddle to mainstream banks in India. NBFCs or shadow banks, as they are also called, are highly significant for the economy’s growth. However, due to their high vulnerability and susceptibility towards high risk and losses, they have predominantly existed in the shadows of the country’s financial sector and have not come out in the limelight. Moreover, this is not without reason. The recent meltdowns of big corporate houses such as Infrastructure Leasing & Financial Services (IL&FS), Dewan Housing Finance Ltd (DHFL) and Reliance Capital have cast numerous questions about the credibility and genuineness of shadow banks in India. Given such a scenario, the entire shadow banking industry was subject to strict surveillance by the regulator to strengthen the overall financial ecosystem. After the chaos in September 2019, Altico Capital India Ltd, an $800 million realty-based capital-backed housing finance company, surrendered its licence to the Reserve Bank of India (RBI), projecting its incapability to run the business. The company had defaulted on a $91.99 million payout to a Dubai-based bank, followed by defaults to other lenders in the same year. As a result, SSG Capital, a Hong Kong-based company, acquired Altico’s bad debts with a 50% haircut to save the company. It was extremely unfortunate for the overall financial sector, and particularly the NBFC sector, that Altico was not the only company in this situation. Multiple other entities are contemplating liquidating or opting for a resolution plan to ensure a safe exit from their present debt-ridden situation. It is high time now to address the concerns of the NBFCs, rescue them from an early-stage crisis, and rescue the overall financial sector from further drowning before the situation turns out of control.

Introduction

Non-banking financial companies (NBFCs) 1 are an alternative channel to the formal financial system and are equally vital as commercial banks in India. Altico Capital India Ltd is one of the shadow banks in the country’s history that has most recently faced an emergency in its business. This crisis developed as lenders who were previously staggering from one of the world’s most exceedingly terrible advance heaps shrugged off expanding more credit. Altico Capital, the shadow bank, began defaulting on its interest payments in September 2019. Its lenders (Table 1) increased their pressure in several ways, leading the housing finance company to default on several capacities, which compelled it to offer non-performing assets (NPAs) to reimburse the advances. This offer to reimburse the advances was the goalpost that financiers were waiting for before any rebuilding activity, and loan specialists were hanging in tight for crisp financing of $70 billion. With all this, combined with the meltdown of Infrastructure Leasing & Financial Services (IL&FS) in 2018 and Dewan Housing Finance Ltd (DHFL) in 2019, an emergency in the NBFC sector will befall the economy on a large scale.

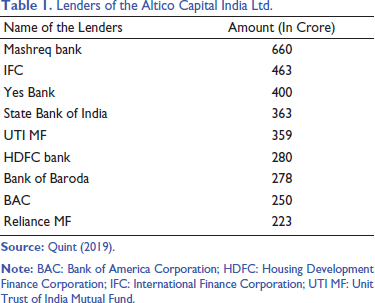

Lenders of the Altico Capital India Ltd.

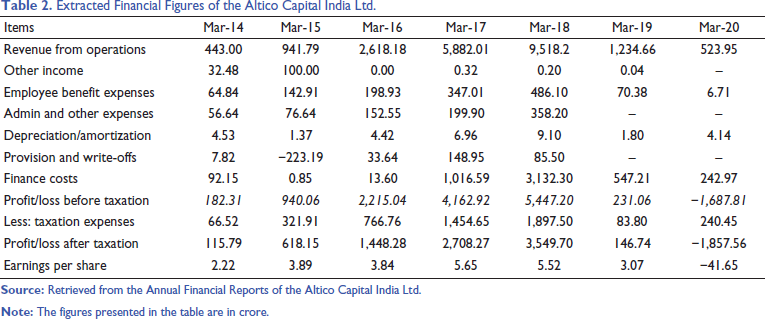

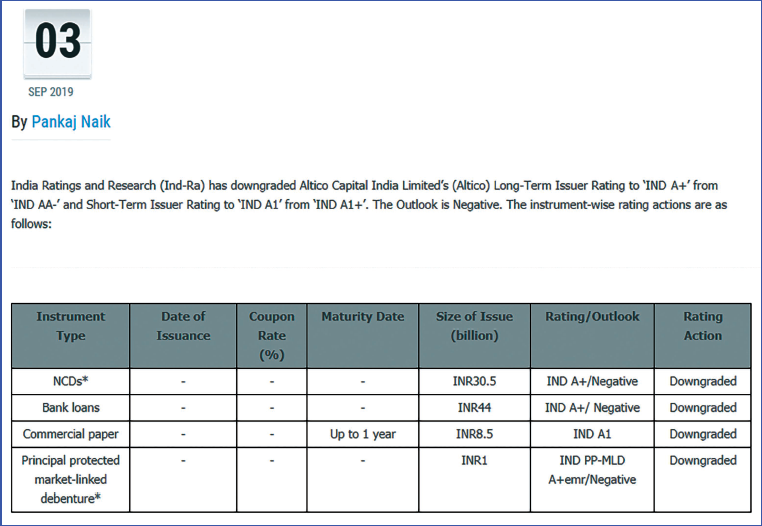

As per the company report, Altico Capital India Ltd defaulted on an interest payment to Dubai-based Mashreq bank of $2.78 million out of $91.99 million of the total aggregate defaulted amount. Altico’s credit book remained at $962.37 million towards the end of 2019 (Table 2). In 2017, the entity multiplied its credit book from its figures in 2016 and then extended it further by 70% in 2018. This rate of growth-development deteriorated when the real estate sector began incurring losses in 2019. With the deterioration, the company incurred a net loss of ₹2,225.94 crore in the financial year (FY) 2020, which initiated preparations for the winding up of the business for which the company was well known (MCA, 2021). The company also formed a steering committee and appointed a resolution advisor to proceed with the resolution plan as per the Reserve Bank of India (RBI)’s mandate. During this stage, Altico represented some terrible advances, which led to the beginning of the obligations book to develop higher and higher. The gross NPAs remained at 1.8% towards the end of 2019. An additional sign of alert was given to Altico due to rising concerns over the delicate acknowledged circumstances. A more significant part of the credit profiles was land developers that could quickly build into NPAs. The company defaulted on repayment of dues to lenders. As a repercussion of this, the company’s credit rating was reduced to default ‘D’ (Figure 1). As a result, rating agencies such as CARE also downgraded Altico Capital to ‘B with a negative outlook’, followed by India Ratings and Research downgraded to ‘IND A+’ from ‘IND AA−’ (Table 3).

Extracted Financial Figures of the Altico Capital India Ltd.

Chronological Financial Irregularities Since 2019.

The above-depicted scenarios pose numerous questions regarding the management of Altico Capital India Ltd and its preparations for the survival of the largest NBFC in India. Upon whom should the responsibility or the blame for the lack of it lie? Is it the Board of Directors or the Regulator who acts as a last resort for these entities?

The Emergence of Shadow Banking in India

The Indian NBFCs (alternatively referred to as ‘shadow banks 2 ’ and ‘non-banking finance intermediaries’) have a long track record of showcasing the path for the future of the NBFCs in the post-independence era. In 1963, the RBI began regulating the NBFC sector by implementing prudential and regulatory measures, although it was subject to various criticisms and comments from time to time. The advent and evolution of these institutions introduced ample opportunities for several non-banking entities to set up their businesses. After Independence in 1947, India experienced the rule of a socialist government that discouraged the establishment of new entities in the land. In addition to this, in the wake of the dissolution of Palai Central Bank and Laxmi Bank in the 1950s and mid-1960s forced the regulator to hit the panic button to protect the depositor’s interest by enacting various regulations to that effect. Beginning with lease financing to hire purchase finance sectors with the efforts of first-line industrialists A. C. Muthiah and Farouk Irani, the country had ‘tasted blood’ and growth in the wake of innovative financial products by setting up NBFCs in India. 3

The post-crisis era, that is, 2007–2008, drew attention towards the non-banking financial entities along with the formal banking sector, as it was evident from the global financial meltdown along with its repercussions and the global aftershocks in a colossal way upon many of the countries/economies of the world. The stringent regulations imposed by the RBI upon commercial banks and the minimal foreign investment exposures of financial instruments help the Indian financial system absorb the economic shocks during the crisis period (FSB, 2013). After the dissolution of a few banks around 1960, many depositors lost their money. The NBFCs also used to rely on deposits. The RBI in 1963 extended its regulatory role by an amendment in the RBI Act 1934. Later, in 1996, after some NBFCs failed, the RBI strengthened oversight of NBFCs. The RBI also decided to prescribe many more public deposits by NBFCs. The RBI brought prudential guidelines for NBFCs. The new regulatory norms primarily targeted the deposit-taking NBFCs rather than the non-deposit-taking ones. However, NBFCs were still lightly regulated, compared to banks. The amended NBFC Act reduced the NBFC count from 55,995 in FY-1995 to only 7,855 in FY-1999. The count of deposit-taking NBFCs also decreased from 1,429 in FY-1998 to 624 in FY-1999. Deposit-taking NBFCs gradually increased much later (RBI, 2021a; 2021b and 2021c).

The year 2011 started with recommendations from Ms Usha Thorat’s committee (Thorat, 2011)

4

on the issues and concerns in the NBFC sector in India. As of 2012–2013, NBFCs in India were being classified into the following categories as follows:

1. Based on financing activities a. Deposit-taking NBFC b. Non-deposit taking NBFC c. Non-deposit taking systemically important Based on non-financing activities d. Asset finance companies e. Loan companies f. Infrastructure finance companies g. Micro finance institutions h. Factoring companies i. Asset reconstruction companies

The glamorous world of NBFCs was not sustained for an extended period. Within a decade, the sector faced a black era with the consecutive collapses of mammoth entities, namely IL&FS and DHFL in India. As a result, many other housing finance companies (HFCs) in the industry either struggled to compete in the market or were liquidated to eliminate the chaos.

Turmoil in the Non-banking Finance Sector

The NBFCs in the recent past have experienced the catastrophic meltdown of several premier HFCs in India, such as IL&FS, DHFL and Reliance Capital, to name a few (RBI, 2020). Their root causes could be retrieved from a standard set of factors, which revolve around liquidity management, asset-liability management and corporate governance issues.

The downfall in the NBFC sector started in India in mid-2016 after the collapse of IL&FS and DHFL. Founded in 1987, 5 IL&FS served to finance infrastructure projects. It enjoyed an ‘AAA’ rating, which helped to mobilize funds. The downfall of IL&FS started after the default of a short-term loan of ₹1,000 crore to the Small Industries Development Bank of India (SIDBI). Soon, 350 group companies with an asset value of ₹7,000 crore began defaulting, which led to a credit downgrade for IL&FS. The asset and liability mismatch and delays in land acquisitions dragged the company into defaults, creating a ripple effect on other NBFCs. DHFL also collapsed in 2018 due to non-payment of short-term debt. The credit pressure led DHFL to sell ₹30,000 crore worth of retail loans. DHFL relied entirely on short-term funds to manage long-term finance, so the immediate need for short-term debt obligations forced it to face the liquidity crunch. The RBI has referred the case to the National Company Law Tribunal (NCLT) under the Indian bankruptcy law. The board stands superseded, and an insolvency professional has been appointed to revive the company. In the same year, Altico Capital, another leading real estate finance company, surrendered its licence due to non-payment of ₹6 crore in interest. Altico Capital’s resolution is also in progress.

The country had experienced severe storms recently, with entities even trying their best to rescue them. 6 Despite all this, the intensity and impact of the meltdown were so high that the regulators were helpless at that juncture and unable to project the path of survival for the overall NBFC sector in time. Even though the global markets experienced economic turmoil after the financial crisis and tried to recover from the same; in close pursuit, if India had not taken proactive measures for the benefit of the existing NBFCs on or before time, then the survival of the shadow banking markets would be at stake in the future. 7 Sadly, this bleeding spillover effect continues, which began with the IL&FS meltdown and the failure of various peer companies such as DHFL, Reliance Capital and Altico Capital in India.

About Altico Capital

Altico Capital India Ltd was incorporated on 28th January 2004 and registered as a non-deposit taking NBFC with the RBI. With a size of more than $800 million (Altico, 2018), Altico Capital has been classified as a systematically important NBFC, according to the financial limits prescribed by the RBI. The primary focus of Altico was to provide secured lending to mid-income and commercial real sector projects across India. In addition to this, the company also offered financial solutions to the infrastructure and other allied sector activities from time to time. Altico Capital envisioned its growth by living up to its goal statement, Financing India’s Future (Altico, 2019a). Over time, the entity began its empire with the extended support of Clearwater Capital, ADIA and Varde Partners. Varde Partners has invested over $55 billion since its inception and is also actively involved in real estate and other major financial allied activities.

The Functionality of Altico Capital

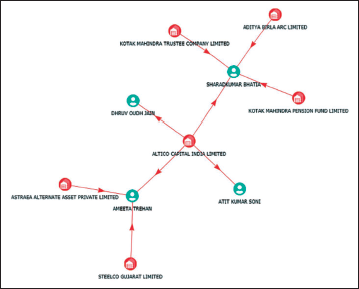

Altico Capital’s major stakeholding lay in the hands of Clearwater Capital, ADIA and Varde Partners, which led the management and day-to-day functioning of the company in India (Altico, 2019g). Clearwater Capital had invested around $6.5 billion over 350 investment channels on both onshore and offshore investments, followed by leading investment partner Varde Partners, who had extended support in corporate credit, mortgages and specialty finance. The named stakeholders had a legacy of around 10–15 years in several areas of India’s housing and infrastructure projects. Altico was initially run by a team of top executives from several fields, indicating the board structure’s efficiency in leading the business. In 2014, Altico appointed the Harvard Fellow Ms Naina Lal Kidwai as an independent non-executive director of the company (Altico, 2019c). However, just after the ratings were downgraded, Ms Kidwai resigned, which greatly affected the company’s image among investors. After her resignation, significant functions lay on the shoulders of these personalities, such as Dhruv Jain as ‘Chief Financial Officer’, Atit Kumar Soni as ‘Company Secretary’, Sharad Kumar Bhatia and Ameeta Trehan as ‘Director’. These people had vast knowledge and relevant experience in the NBFCs and other allied financial sectors in India before joining Altico Capital. Apart from the above positions, the company hired several asset management, credit management and investment management specialists to run the country’s leading housing finance entity with due diligence while conforming to the regulator’s guidelines. The scenario twisted in September 2019 after the stepping down of Sanjay Grewal chief executive officer (CEO), followed by Naina Lal Kidwai (former head of HSBC India) from the Company’s top management by citing the same reason as the CEO mentioned in his statement at the press meet (Table 4) from 2004 to 2020. The scenario altered after the violation of norms by the HDFC bank of ₹200 crore by using it as a general lien, which in turn affected the image of Altico in front of the investor, followed by the default of the interest to the Dubai-based Mashreq bank and the downgraded of the instruments by several leading rating agencies (Altico, 2019e).

List of Appointments of Altico Capital India Ltd from 2004 to 2020.

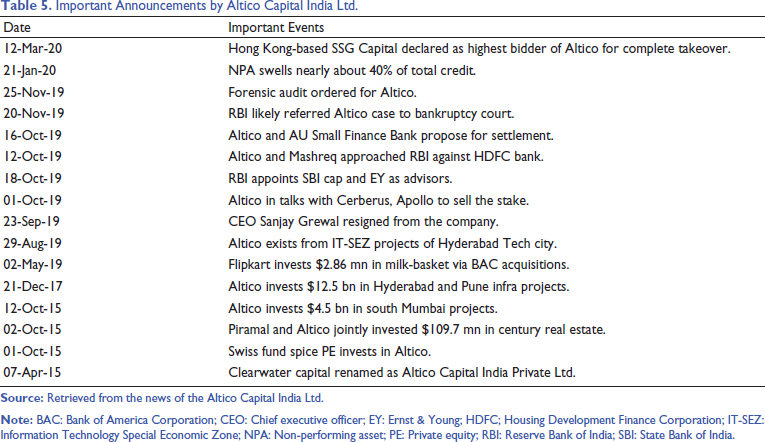

Journey of Altico Capital

Altico Capital, since its very inception, has performed phenomenal growth and achieved many milestones in the past 15 years by way of attaining one target to another from real-estate investments to high-tech Tier-1 city projects in top cities like Mumbai, NCR, Chennai, Bangalore, Pune and Hyderabad. The company had extended its arms in every allied activity related to real estate and project financing, which is evident from the milestones it achieved (Table 5). The company was committed to providing the ultimate innovative financial solutions to the credit market by strengthening the company’s core management. The company had formed a corporate social responsibility (CSR) committee and a remuneration committee and adhered to the related party transactions from time to time. The company faced downgraded ratings and the top management’s exit, which pulled the company into chaos. Now, the stated reasons, including corporate governance issues or the lack of accurately forecasting the future debts of the company, forced the $800 million company, Altico Capital, to make a hasty exit from the market.

Important Announcements by Altico Capital India Ltd.

The Chaos Caused by the Liquidity Crisis

The Indian housing finance sector consists of more than 80 players, whereas only a few dominate the industry, such as HDFC, Dewan Housing Finance, Indiabulls Housing Finance, PNB Housing Finance Limited and LIC Housing Finance. Together, they command a 78% market share. HFCs control an overall market share of nearly 37% by value. The top five (out of the almost 113) HFCs as of December 2020 constituted 27% of the pan-India housing loan book. HFCs, including NBFCs, have the highest delinquencies, primarily due to the stress in the book, with a ticket size of less than ₹15 lakh. The industry witnessed 10.4% growth in the December 2019 quarter over the December 2018 quarter. After seeing steadfast growth of over 20% in 2014–2018, HFCs lending dropped considerably in the second half of fiscal 2019 to less than 10%. This sharp decline resulted from the sector undergoing a severe bout of liquidity crisis, as investor confidence dipped post-September 2018. Funding to the industry was impaired, and at least two large HFCs virtually stopped fresh disbursements.

Market Conditions for HFCs Survival

Moreover, the slowdown in housing sales further skewed demand for mortgage loans. Following the sectoral crisis, the country faced a massive outbreak known as COVID-19, which devastated the world economy financially and socially. Furthermore, the asset-liability mismatch was caused by short-term borrowings used for long-term investments. For a long time, Indian NBFCs have taken a risky approach by borrowing short-term loans and then lending them out over time. The current asset-liability mismatch is a sure recipe for disaster. HFCs provide loans to developers and homebuyers. The only issue was that the Indian housing sector had collapsed, with stalwarts like ‘Amrapali Group’, ‘Supertech’, ‘Reliance Capital’ and others. As a result, the NBFCs’ asset quality was called into question. These companies faced a double curse: their financial health was under increasing scrutiny, which put pressure on their net worth and drove them into insolvency. The lack of tight governance controls, negligent risk management, due diligence and audit mechanisms has resulted in excessive credit accumulation in the NBFC sector. Inadequate provisions have also resulted in errors, such as related party loans to group companies. There were also significant errors by rating agencies. Because of this, many housing finance projects were delayed in their completion as promised; in turn, the RBI has also extended the moratorium period for the NBFCs by considering the country’s current pandemic situation (Figure 3).

The downfall of the $800 million company began soon after the CEO stepped down in 2019. As a result, many investors started questioning the creditworthiness and repayment of the debt obligations owed by Altico Capital. In September 2019, Altico defaulted on $2.78 million as an interest payment to the Dubai-based Mashreq bank, followed by downgrades by the ratings credit rating agencies to the ‘negative’ category. Although the default to Mashreq bank was inevitable, the domestic lender HDFC bank, which had a general lien of $2,000 million already debited from the accounts of Altico Capital out of the $6,500 million raised through external commercial borrowing (ECB) from the Dubai-based bank before the default. Furthermore, the unauthorized deduction of the $2,000 million put the entity in a fix. The RBI later instructed HDFC Bank to refund the said amount to Altico without any deduction. In November 2019, the RBI had planned to refer the Altico Capital case to the bankruptcy court, seeking a resolution window (India Rating and Research, 2019). In the end, a Hong Kong-based firm, SSG Capital, acquired Altico Capital with a 50% haircut to the book debt of the concern. The 15-year-old NBFC surrendered its licence to the regulator so that it would not be allowed to operate in the housing finance business in India (Altico, 2019b).

After the meltdown of IL&FS, DHFL and Reliance Capital, many NBFCs have felt the heat of the meltdown wave, resulting in either a resolution plan or seeking recapitalization support from the government. Keeping the NBFC and overall financial sectors in mind, a comprehensive and detailed recovery and rejuvenation plan is needed. Needless to say, the sooner, the better for the revival of the industry, which contributes to the growth of the nation in a similar way. Suppose the regulator and various government departments do not take preventive measures quickly. In that case, the country will face another financial crisis similar to the one it had experienced.

The mismanagement became painfully apparent in September 2019 when Altico defaulted on an interest payment of around ₹20 crore ($2.8 million) to the Dubai-based Mashreq bank. This default triggered a cascading effect, leading to a sharp downgrading of Altico’s credit ratings, which in turn dried up its access to fresh funding (Altico, 2019d). Additionally, the company’s governance practices came under scrutiny, revealing issues such as a lack of transparency and oversight by the board. Despite having prominent investors and a seemingly robust business model, the misalignment of its financial strategies with market realities and the absence of effective risk management controls have led to its downfall. The default raised broader concerns about the health of India’s NBFC sector, which was already reeling from liquidity crises and governance issues following the collapse of IL&FS in 2018 (Altico, 2019f).

Decision-making Flaws Towards Financial Instability

Altico Capital Ltd, a prominent NBFC in India, faced financial instability and eventual default in 2019 due to a series of flawed decision-making processes and external factors. One of the critical reasons for its collapse was the overconcentration of risk. The company heavily focused on the real estate sector, particularly residential real estate, which is inherently high-risk. This overexposure became detrimental when the Indian real estate market experienced a significant slowdown, leading to delays in repayments from developers and consequently impairing Altico’s cash flows.

Another major issue was the asset-liability mismatch in Altico’s financial structure. The company relied excessively on short-term borrowings to fund long-term real estate projects. This mismatch created severe liquidity challenges as short-term obligations became due while repayments from developers were delayed. Compounding this problem were the company’s inadequate risk assessment practices. Altico’s lax credit appraisal processes allowed it to extend loans to weak and over-leveraged developers, increasing the likelihood of defaults and worsening its financial woes.

Altico’s aggressive growth strategy further contributed to its downfall. The company expanded its loan book rapidly without adequately diversifying its portfolio or strengthening its risk management practices. This approach led to over-leverage and reduced its resilience to sectoral shocks. Additionally, Altico’s reliance on external borrowings, including foreign debt, left it vulnerable to repayment difficulties when cash flows tightened, damaging its reputation and worsening its financial instability.

The management’s failure to address early warning signs also played a crucial role in Altico’s collapse. The rising stress in the real estate sector and increasing borrower defaults were clear indicators of trouble, yet the company delayed taking corrective actions. This inaction left little room for restructuring or recovery. Furthermore, the lack of diversification in revenue streams exacerbated the issue. Altico’s dependence on interest income from the real estate sector made it highly susceptible to sector-specific downturns, which it failed to hedge against.

Corporate governance and transparency issues further eroded stakeholder confidence. Allegations of weak governance and inadequate financial disclosures created trust issues with lenders and investors, accelerating the company’s decline. On a broader level, Altico misjudged macroeconomic conditions, particularly the liquidity crunch in the NBFC sector following the IL&FS crisis in India. This credit crunch compounded its difficulties, highlighting the company’s inability to adapt to changing economic realities.

In conclusion, Altico Capital’s financial instability underscores the importance of prudent risk management, diversified portfolios, robust corporate governance and proactive responses to economic challenges. The case serves as a cautionary tale for NBFCs and other financial institutions, emphasizing the need for sound decision-making and adaptive strategies to navigate complex and volatile economic environments.

Way Forward

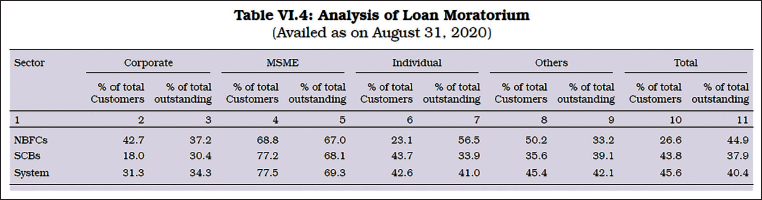

While authorities are still formulating a suitable policy for the sector, ordinary citizens have almost written off the industry as a ‘highly risky’ sector. At the same time, some seek increased restrictions and clampdowns on the entire sector, rather than trying to regulate the business’s risks to turn it into a more profitable enterprise. Well, this is not entirely true, in a sense; while the risks in this sector are higher than those in the commercial banking sector, this is a large part of the overall financial sector in India. The lending status outstanding as of March 2020 for the overall NBFC sector was $23.605 trillion, which shows how systemically important the overall sector is. The NBFCs also cater to a whole host of companies and organizations who cannot avail of credit from commercial banks for various reasons, including the rigidity of processes and systems involved. Interestingly, only 26.6% of NBFC’s customers have availed of the credit moratorium facility extended by the government due to the current COVID-19 pandemic, compared to 43.8% of commercial bank customers (Figure 2), which depicts the inherent strength of the NBFC sector in its lending activities.

The study underlines the significance of the governance framework of Altico Capital Ltd as well as the consequences faced by the entity. Regulatory lapses and liquidity mismanagement also need to be scanned and the way forward is to be provided to the concerned entity for the safe rescue as well as to provide learning for the other HFCs operating in the same vertical. Moreover, the business models of the NBFCs could be compared with the HFCs. Furthermore, the future roadmap could be suggested by the reader by way of considering the previous financials as well as the challenges faced by the company. At last, the regulatory measures and the action taken by RBI to address the crisis in the NBFC sector are to be discussed in a detailed manner, which could be a learning for the other HFCs in India.

Footnotes

Acknowledgements

The authors would like to thank the editor of Emerging Economies Cases Journal and all the anonymous reviewers for their valuable inputs and suggestions for improving this article in the best possible manner. The authors also deeply acknowledge the valuable insights shared by Dr Santosh Gopalkrishnan, Professor at Symbiosis International University, Dubai, for his opportune guidance to complete this case.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.