Abstract

While alternative lending by fintech and bigtech firms has become an important source of credit, its impact on aggregate household indebtedness has received limited research attention. This study examines whether alternative lending affects country-level household indebtedness and whether this relationship is shaped by financial development, particularly access to credit. We use a System GMM approach on a panel of 34 OECD countries from 2013 to 2019 to estimate the association between household debt-to-income ratios and alternative lending volumes, including interactions with country-level indicators of financial development and access to credit. To explore transmission channels, we add loan-level evidence from 157,651 loans from 2009 to 2020 originated by Bondora, a large European marketplace lending (MPL) platform, and test how borrower quality among new and recurring borrowers varies with financial development. Our findings reveal, that alternative lending is significantly associated with country-level household indebtedness, with a positive relationship in countries with easier access to credit and a negative one in relatively low-access settings. Loan-level evidence is consistent, showing that in high-access countries Bondora more often serves riskier and more indebted borrowers and attracts lower-creditworthiness first-time borrowers, potentially increasing household indebtedness. We contribute by demonstrating a non-monotonic relationship between alternative lending volumes and household indebtedness and identify the potential underlying mechanisms. Our findings imply that in high-access environments, alternative lenders complement banks by serving lower-quality borrowers, calling for stronger consumer protection. In less developed financial systems, alternative lending may substitute for bank credit.

Keywords

Introduction

The credit market serves as the primary mechanism for financial intermediation, facilitating the flow of capital from lenders to borrowers through various debt instruments. While traditionally dominated by commercial banks, this market encompasses a much wider array of institutions. This broader ecosystem, often referred to as “alternative lending”, comprises any credit intermediation operating outside the traditional banking system. Historically and globally, a significant share of alternative lending has been provided by non-digital entities, including cooperatives, credit unions, retail store financing, and auto loan providers (Madeira, 2023).

Over the last decade, however, digital innovation has fundamentally restructured this landscape (Thakor, 2020). Entrants into the digital credit space typically follow two distinct structural paradigms: fintech and bigtech. While fintech firms are specialized, digitally native entities designed to unbundle specific financial services, bigtech lenders are large technology conglomerates that leverage vast user ecosystems and proprietary non-financial data to facilitate credit (Cornelli et al., 2023). To isolate the impact of technology-driven intermediation, our analysis focuses exclusively on this digital subset. This scope encompasses bigtech credit alongside diverse fintech models, including marketplace lending (MPL), digital balance-sheet lending, and automated invoice trading.

The volume of alternative lending has experienced robust growth, with global flows reaching approximately $800 billion in 2019 (Cornelli et al., 2020). This sector has emerged as a prominent alternative to traditional bank intermediation, particularly in the Baltic states and the United Kingdom, where the ratio of alternative credit to GDP increased twelvefold between 2013 and 2019 (Cornelli et al., 2020). Beyond its growth, recent literature documents significant socioeconomic externalities, linking alternative lending to shifts in income inequality (Hodula, 2023), bank lending dynamics (Hodula, 2022), and carbon emissions (Appiah-Otoo et al., 2022). While these findings highlight the sector’s role in driving macroeconomic change, micro-level evidence on household welfare remains bifurcated. One strand of literature suggests that alternative credit may exacerbate financial distress and over-indebtedness (e.g., Chava et al., 2021; Wang & Overby, 2022; Yue et al., 2022), whereas others argue it alleviates liquidity constraints through improved credit access (Danisewicz & Elard, 2023). Despite these insights into idiosyncratic outcomes, the implications of alternative lending for aggregate household indebtedness at the country level remain largely unexplored.

From a theoretical perspective, this topic can be understood within an asymmetric-information framework combining credit rationing, household liquidity constraints, and lender heterogeneity (Stiglitz & Weiss, 1981; Zeldes, 1989). Digital lenders alter the effective credit supply by relying on scalable, hard-information screening, which contrasts sharply with traditional banks’ relationship-based, soft-information models (Berg et al., 2022; Berger & Udell, 2002; Thakor, 2020). This technological divergence enables alternative lenders to target distinct borrower segments, meaning their macroeconomic impact depends heavily on a country’s baseline financial access (Jappelli & Pagano, 1994). If digital lenders primarily compete for a borrower pool that overlaps with traditional bank clientele, their growth may simply crowd out bank lending, yielding limited changes to aggregate household indebtedness (Tang, 2019; Dell’Ariccia & Marquez, 2004). Conversely, if they penetrate segments underserved by banks, they are more likely to fund marginal borrowers and drive aggregate credit expansion. Existing empirical evidence supports both substitution and expansion effects depending on regional characteristics and banking-sector structure (e.g., Havrylchyk et al., 2021; Hodula, 2022; Jagtiani & Lemieux, 2018; Kowalewski & Pisany, 2022; Maskara et al., 2021; Ueda et al., 2022). This empirical ambiguity underscores the need to understand how existing financial access dictates market segmentation and, ultimately, household debt levels.

To this end, we advance the literature by shifting the analytical focus specifically to aggregate household debt-to-income ratios in a cross-country setting. This approach distinguishes our study from recent work by Hodula (2022) and Kowalewski and Pisany (2022), who primarily examine institutional bank lending dynamics. In our primary empirical exercise, we evaluate a panel of 34 OECD countries over the period 2013 to 2019. We measure household indebtedness via the household debt-to-income ratio and proxy the proliferation of alternative lending using country-level volumes of fintech and bigtech credit from the Bank for International Settlements (BIS). Crucially, the boundaries of this dataset align with our overarching definition, capturing the broad spectrum of fully digital alternative finance models.

We combine these data with access indicators from the IMF’s Financial Development Index. Within this context, we define financial development as the overall maturation, depth, and efficiency of a country’s formal financial institutions and markets, and financial access specifically as the ease with which individuals and households can utilize these formal financial services, primarily traditional bank credit. To estimate the relationship between these variables, we employ a System GMM framework to address the inherent persistence of household leverage and the potential endogeneity of credit supply (Blundell & Bond, 1998). Our results reveal that alternative lending is significantly associated with aggregate household indebtedness, though this relationship is highly contingent upon the prevailing financial environment. Specifically, alternative lending is positively associated with household leverage only in economies with comparatively high traditional financial access; in lower-access settings, this relationship reverses.

We then turn to the mechanism underlying this heterogeneous country-level pattern. The framework outlined above suggests that the aggregate debt effect depends on which borrower segment alternative lenders serve relative to banks. In countries where access to traditional credit is already broad, further growth among standard bankable borrowers is limited. Here, alternative lenders may gain market share mainly by targeting more marginal borrowers whom banks are less willing to finance, thereby expanding total credit. In countries with more restricted access to credit, alternative lenders may compete more strongly for a borrower segment that overlaps with traditional bank clientele, resulting in credit reallocation rather than expansion. This interpretation implies that the borrower quality of alternative lenders should vary systematically with financial access across countries.

Prior studies establish that alternative lenders cater to a distinct borrower pool relative to traditional banks, a form of market segmentation frequently attributed to country-specific institutional characteristics (De Roure et al., 2022; Di Maggio & Yao, 2021; Dolson & Jagtiani, 2024; Dömötör et al., 2023; Jagtiani et al., 2021). To our knowledge, the direct relationship between alternative lenders’ borrower quality and a country’s level of financial access remains unexplored. This motivates our second research question: Does the borrower quality of alternative lenders systematically deteriorate as a country’s financial access increases?

To examine this mechanism, we complement the country-level analysis with loan-level evidence from Bondora, a large European marketplace lending (MPL) platform. Bondora acts strictly as a digital matchmaker, directly connecting borrowers with investors without holding loans on its balance sheet. While Bondora represents only a single MPL platform within the broader digital lending ecosystem, its cross-country footprint allows us to observe the same borrower segmentation that we theorize in the country-level analysis. Using 157,651 loans originated between 2009 and 2020 across countries with varying degrees of financial access, we examine whether borrower quality varies systematically with the financial environment. We approximate borrower quality using relative interest rates, debt-service burdens, and the incidence of first-time borrowers without outstanding debt but with low creditworthiness. The results support our proposed mechanism: in countries with easier access to bank credit, Bondora more frequently lends to lower-quality borrowers and lower-creditworthiness first-time customers.

This paper contributes to the literature in four ways. First, it shifts attention from borrower-level outcomes to the aggregate relationship between alternative lending and household indebtedness. Second, it shows that this relationship is conditional on the degree of financial development and, crucially, access to traditional credit. Third, it extends theories of asymmetric information in household finance by demonstrating that the macroeconomic association of alternative lending depends on existing financial access and the degree of market overlap with traditional banks (Jappelli & Pagano, 1994; Stiglitz & Weiss, 1981; Zeldes, 1989). Fourth, it provides loan-level evidence on a plausible transmission mechanism, showing that the borrower segment served by an alternative lender varies systematically with the macro-financial environment.

The remainder of the paper is organized as follows. The following section reviews the literature and develops the hypotheses. Thereafter, the cross-country analysis is presented. The next section investigates the borrower-level mechanisms using Bondora data. We then discuss the results, draw policy implications and identify limitations. The final section concludes.

Literature Review and Hypotheses

This section develops three testable hypotheses about the relationship between alternative lending and household indebtedness based on the outlined theoretical framework and related empirical studies. First, if alternative lending changes households’ effective access to credit, it should affect household indebtedness at the aggregate level. Second, because alternative lenders interact with traditional banks and need not serve the same borrower segments, this effect should depend on financial development and access to credit. Third, if the aggregate debt effect of alternative lending varies across financial environments, borrower composition is a plausible mechanism through which this heterogeneity arises.

To derive the first hypothesis, we turn to borrower-level studies on alternative lending and household financial outcomes. From a credit-rationing perspective, these studies are informative because any change in households’ effective access to credit should first become visible in individual borrowing behavior, debt burdens, and financial distress. This area has been extensively, though sometimes controversially, explored, particularly in the U.S. market. On the one hand, Wang and Overby (2022) and Chava et al. (2021) suggest that alternative lending may relax borrowing constraints in ways that elevate debt burdens, thereby eroding household financial stability, defined as their capacity to absorb economic shocks without defaulting on obligations. Chava et al. (2021), for example, show that borrowers who obtain alternative loans subsequently exhibit lower credit scores and higher default and bankruptcy rates than comparable borrowers using traditional bank credit. Wang and Overby (2022) exploit variation in the approval of a large alternative lending platform across U.S. states and find that the spread of alternative lending is associated with increased insolvency filings. On the other hand, Danisewicz and Elard (2023) show that bankruptcy filings increased significantly in some U.S. states following a decline in alternative lending, indicating that reduced access to alternative lending can also worsen household outcomes.

There are also some important studies outside the U.S. Yue et al. (2022) show for China that the rapid growth of digital finance improves access to credit but also increases the likelihood of household financial distress. Yuan et al. (2024), using a panel of 100 countries from 2006 to 2019, find that in countries with a higher degree of fintech development, expansions in household debt are more likely to be associated with financial crises. Overall, this literature suggests that alternative lending changes households’ effective access to credit and thereby affects indebtedness and financial stability. Most studies indicate that the emergence of alternative lending leads to a relaxation of effective borrowing constraints that is associated with higher debt, although some findings indicate that these effects may be stabilizing in certain settings. We therefore expect alternative lending to have a significant effect on household indebtedness at the country level and we formulate the following hypothesis:

Alternative lending significantly affects household indebtedness at the country level by altering households’ effective borrowing constraints.

The second relevant strand of literature examines the relationship between alternative lending and traditional bank lending. This strand is central because the aggregate debt effect of alternative lending depends not only on whether it changes credit access, but also on how it interacts with the incumbent banking system. Once lenders differ in screening technologies and in the borrower segments they serve, the effect of alternative lending on household indebtedness should depend on whether alternative lenders primarily substitute for bank credit within segments already served by banks or complement existing credit supply by extending loans outside those segments. This distinction should vary with financial development and access to credit, which shape both the tightness of borrowing constraints and the degree of overlap between digital lenders and banks. Where access to bank credit is limited and borrowing constraints are more binding, alternative lending may overlap more strongly with traditional lending and therefore reallocate credit across lenders. Where access to bank credit is already ample, alternative lenders may differentiate more strongly from banks and expand total household borrowing by funding additional, more marginal borrowers.

Several studies, particularly for the U.S., examine whether alternative lending complements bank lending by expanding into underserved areas. Jagtiani and Lemieux (2018), using loan-level data from Lending Club, show that fintech lending has increasingly expanded into areas with highly concentrated banking markets and fewer bank branches. Similar evidence is provided by Avramidis et al. (2022), Ueda et al. (2022), Maskara et al. (2021), and Havrylchyk et al. (2021). Havrylchyk et al. (2021) and Maskara et al. (2021) find that fintech lending grows more strongly in areas with restricted access to credit, measured by branch density and market concentration. Avramidis et al. (2022) show that fintech lenders fill gaps created by branch closures and increase lending to lower-risk consumers, while Ueda et al. (2022) find that fintech borrowers are more likely to have experienced unmet credit demand from traditional banks. Jagtiani et al. (2021) add mortgage-market evidence showing that alternative lenders lend more frequently to borrowers with weaker credit scores and in areas with higher denial rates. Together, these studies suggest that alternative lending can increase access to credit and expand supply where traditional banking leaves gaps.

Evidence from outside the U.S. reinforces the view that the growth of alternative lending depends on the surrounding financial environment. Claessens et al. (2018) show in a global country-level panel that alternative lending grows rapidly in countries with more concentrated banking markets. Oh and Rosenkranz (2020), using a sample of 62 advanced and emerging economies, find that alternative lending expands more strongly in countries with limited access to formal financial services. These findings indicate that access to traditional credit helps shape both the growth of alternative lending and its likely effect on household indebtedness.

Several studies also directly analyze the relationship between alternative lending and traditional bank lending. Hodula (2022) finds that alternative lending significantly affects bank lending volumes, but that the direction of this relationship depends on banking-sector characteristics. In less stable or more concentrated banking systems with limited access to credit, higher alternative lending volumes are associated with lower bank lending volumes, consistent with a crowding-out effect. By contrast, in more stable and competitive banking systems, alternative and traditional lending tend to grow alongside each other, pointing to a more complementary relationship. Kowalewski and Pisany (2022), using bank-level data on consumer lending combined with country-level alternative lending volumes, similarly show that the interaction between alternative and bank lending varies with financial development: in developed countries, bank consumer lending declines with alternative lending growth, whereas in emerging countries bank lending increases alongside alternative lending. Taken together, this literature suggests that the relationship between alternative and traditional lending is not uniform across countries, but depends on the structure and accessibility of the existing financial system. This is consistent with a market-segmentation view of credit markets: when overlap with bank lending is strong, alternative lending is more likely to reallocate credit across channels, whereas in settings where alternative lenders differentiate from banks, it is more likely to complement existing supply and increase aggregate household indebtedness. Therefore, we formulate the following second hypothesis:

The effect of alternative lending on household indebtedness depends on a country’s financial development and access to credit, becoming more positive in countries with higher financial development or better access to traditional credit.

To explain the heterogeneous country-level relationship between alternative lending and household indebtedness, we next consider borrower composition as a possible mechanism. If alternative lenders mainly compete for a borrower pool that substantially overlaps with bank clientele, their expansion is more likely to reallocate credit across lending channels than to increase total household borrowing. If, by contrast, they expand by serving more marginal borrowers whom banks are less willing to finance, alternative lending is more likely to add new credit and thereby contribute to higher household indebtedness. The literature on borrower quality is therefore informative because it helps identify the segment in which alternative lenders expand. More generally, models of competition with imperfect screening suggest that entry by additional lenders can increase the number of funded borrowers while lowering the average quality of those accepted, especially if entrants compete at the margin for riskier segments (Broecker, 1990).

Numerous studies on the borrower quality of alternative lenders focus on the U.S. market. Dolson and Jagtiani (2024), Di Maggio and Yao (2021), Jagtiani et al. (2019), and Cornaggia et al. (2017) examine the unsecured personal loan market and show that alternative lenders are particularly active in the high-risk segment, suggesting that they compete with banks especially for riskier borrowers. Jagtiani et al. (2019) provide one explanation for this pattern, showing that alternative lenders, due to superior screening technologies and the use of alternative data, can identify high-quality borrowers even among consumers classified as nonprime. Dolson and Jagtiani (2024) extend this view by comparing credit offers from banks, fintech lenders, and other nonbank lenders and find that alternative lenders more frequently target underserved consumers, such as households with lower incomes, lower credit scores, or a history of bankruptcy. Di Maggio and Yao (2021) further show that alternative lenders, especially in the initial phase of market entry, lend more often to subprime borrowers in order to gain market share, although borrower composition improves over time.

Evidence from outside the U.S. points in a similar direction while also suggesting that borrower quality depends on market conditions. De Roure et al. (2022) study the unsecured personal loan market in Germany and find that alternative lenders charge higher interest rates and serve a riskier borrower segment than traditional banks. At the same time, they show that when banks are hit by negative shocks and tighten lending, alternative lenders step in and lend more frequently to less risky borrowers. This indicates that the borrower segment served by alternative lenders varies with the state of traditional credit supply. Dömötör et al. (2023), using loan-level data from Bondora, also document substantial cross-country variation in borrower quality, with somewhat better borrower quality in Estonia than in Finland or Spain. Taken together, these findings suggest that alternative lenders often serve lower-quality borrowers, but that borrower composition is not fixed and may depend on country-specific credit market conditions.

Overall, this literature suggests that the borrower segment targeted by alternative lenders varies with the surrounding financial environment. In countries with more restricted access to credit, alternative lenders may compete more strongly for borrower segments that overlap with traditional bank clientele, implying a reallocation of credit across channels rather than a strong deterioration in borrower quality. In countries with easier access to bank credit, by contrast, further expansion among already bankable borrowers may be more limited, so alternative lenders may grow mainly by targeting more marginal and lower-quality borrowers. If so, borrower quality should decrease with a country’s financial development and access to credit. Therefore, we formulate our third hypothesis:

Alternative lenders’ borrower quality decreases with a country’s financial development or financial access.

Country-Level Analysis

To test the first two hypotheses, we gauge the effect of alternative lending on the household debt-to-income ratio in a cross-country setting by estimating the following model:

Data

Measuring Household Indebtedness

To measure household debt, we use the logged Debt-to-Income ratio obtained from the OECD database. The ratio is calculated as the outstanding debt (primarily mortgage loans, consumer credit, and other accounts payable) of households (including non-profit institutions serving households such as charities, foundations, trade unions and other non-governmental organizations) in relation to the net disposable income. The lagged value of the Debt-to-Income ratio is included, because it is plausible that a household’s debt and income in the current year are affected by its last year’s debt and income. This assumption is supported by Dumitrescu et al. (2022), who find evidence that the household debt of the previous year has a persistent impact on the current level of household debt.

Measuring Alternative Lending

To measure Alternative Lending, we gathered data on the total volume of alternative market finance, sourced from the Bank for International Settlements (BIS) and originally compiled by Cornelli et al. (2023). This dataset provides annual alternative lending volumes for a wide range of countries, with alternative lending defined as the sum of fintech and bigtech lending. Both types of lending enable credit through online platforms, where loan origination and processing are carried out entirely via digital channels. In addition to traditional financial criteria, like the credit history or the household debt-to-income ratio, alternative lenders often use unconventional data sources (e.g., online spending behavior or social media) or advanced machine learning algorithms to screen loan applicants (Cornelli et al., 2023). Fintech lenders’ main business area is the operation of a loan marketplace by connecting borrowers with lenders, who may be private or institutional investors. By offering investors details on loan risks and borrower characteristics, as well as implementing screening procedures, fintech lenders help solve problems of asymmetric information. In contrast to that, bigtech lenders are large companies, often international or global in scope that operate in the technology sector. These companies have a range of business lines, most of which are non-financial, such as e-commerce, social media, telecommunications, or advertising. Bigtech firms lend either directly, retaining the credit risk on their balance sheet, or in partnership with financial institutions (Cornelli et al., 2023). For our analysis, we follow existing literature and neglect the differences between fintech and bigtech lending (Cornelli et al., 2023; Hodula, 2023; Ozili, 2023), as we focus on the relationship between alternative lending and household indebtedness, and how financial development and access might mediate this relationship.

The alternative lending volumes are constructed by combining country- and year-level fintech lending data from the “Global Alternative Finance Database” of the Cambridge Centre for Alternative Finance (CCAF) with bigtech lending volumes based on estimates by Cornelli et al. (2023). The “Global Alternative Finance Database” contains survey-based transaction volume data across various classifications of alternative finance, including fintech lending. Cornelli et al. (2023) define fintech lending as the sum of all digital loan-based business models, including consumer, business, and property lending. The business lending category also encompasses invoice trading, debt-based securities (bonds), and mini-bonds.

To collect the necessary data, the CCAF conducts annual online surveys, asking fintech lending platforms to report the volume of loans originated in the previous year. 3 Due to a significant drop in the number of participating companies in 2020, potentially skewing the fintech lending volume for that year, we limit our analysis to data up to 2019 (Ziegler et al., 2021).

The bigtech lending data covers 37 firms 4 involved in online lending activities as of the end of 2018. These volumes are primarily collected through personal contacts with companies and central banks, as well as publicly available sources such as annual reports.

To our knowledge, the BIS alternative lending dataset is the most comprehensive and in-depth data source available for analyzing alternative lending at the country level. The dataset’s academic quality is supported by its use in numerous recent studies on various aspects of digital finance (e.g., Adugna, 2024; AlSuwaidi & Mertzanis, 2024; Cuadros-Solas et al., 2023, 2024; Girardone et al., 2024; Hodula, 2022, 2023, 2024; Le et al., 2023; Rapih et al., 2023).

Our Alternative Lending category includes both lending to households and lending to businesses. At first glance, this may seem counterintuitive for an analysis of household indebtedness. However, financing a small business or startup can significantly impact the finances of the owner. This assumption is supported by Rivero Wildemauwe and Sanroman (2022), who show that the type of employment within a household (entrepreneur or employee) significantly influences household debt levels. Additionally, Sabato et al. (2021) find that in the United Kingdom, small to medium-sized enterprises (SMEs) predominantly use alternative lending as a form of financing.

For our analysis, we deliberately exclude Chinese alternative lending volumes due to concerns about fraudulent activities, such as Ponzi schemes, often associated with Chinese alternative lending platforms, as well as doubts about the accuracy of their submitted data (Huang & Pontell, 2023). Furthermore, in 2019, the Chinese government introduced strict regulations that classified several forms of alternative lending as illegal, leading many platforms to shut down and causing the alternative lending market in China to collapse (Ran et al., 2025).

Control Variables

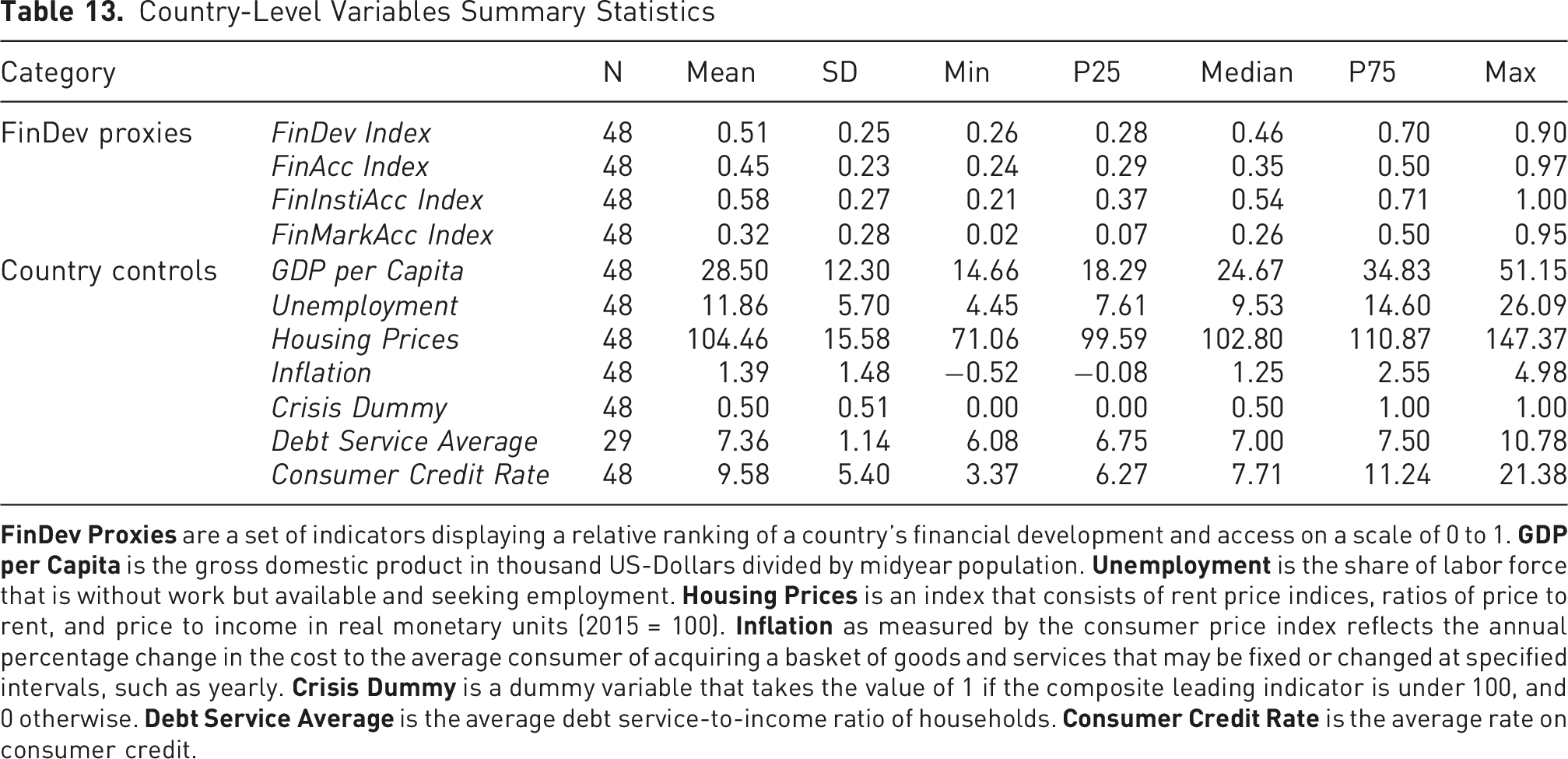

Country-Level Summary Statistics

Measuring Financial Development and Access

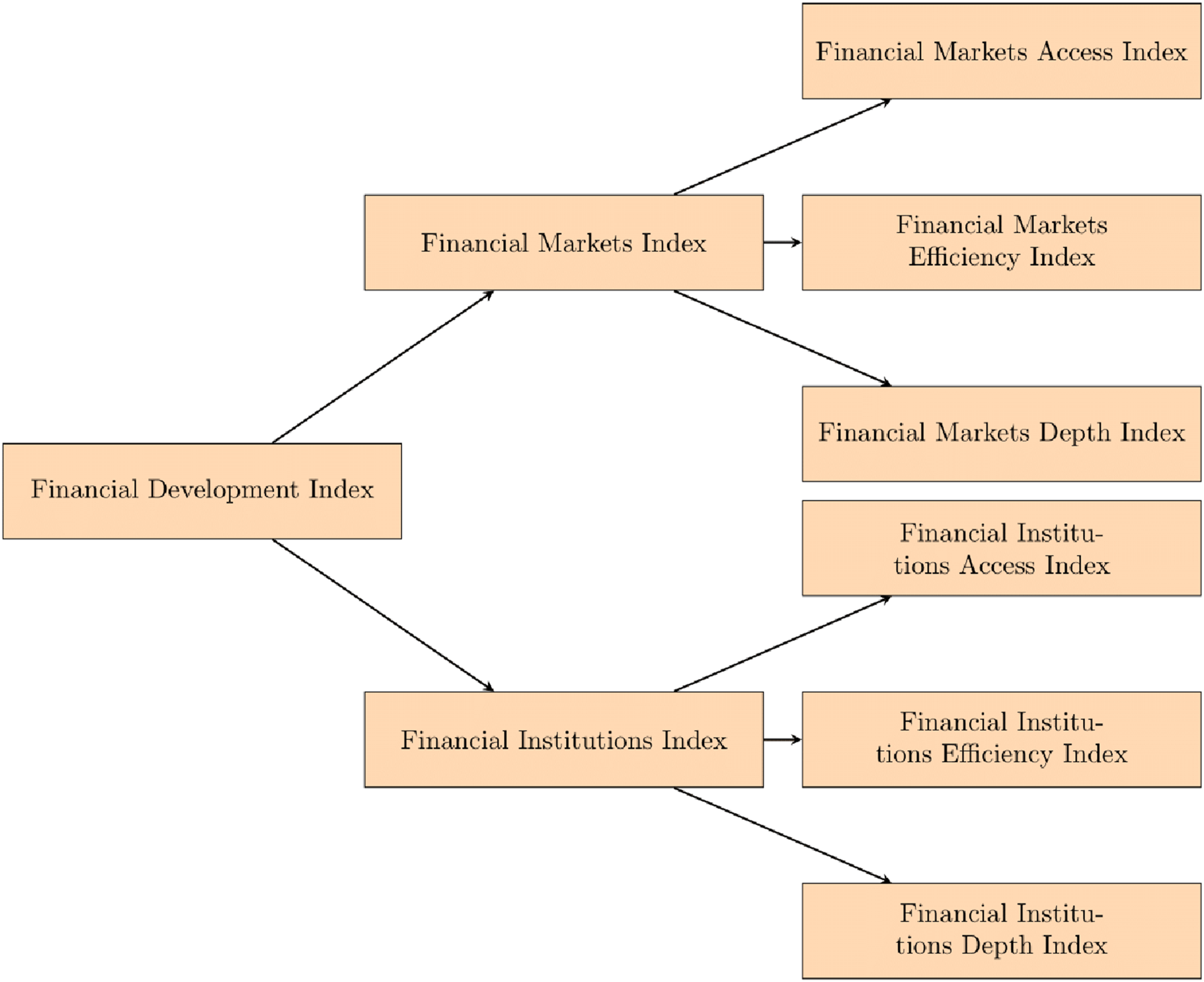

As measures of a country’s financial development and access, we utilize the indices provided by the IMF’s “Financial Development Index Database” (Svirydzenka, 2016). This database offers nine different indices that track a country’s financial development annually in terms of depth, access, and efficiency. These indices are hierarchical, with the overall “Financial Development Index” (FinDev Index) at the top, combining information from all sub-indices to measure the financial depth, access, and efficiency of a country’s financial markets and institutions. 5

At the second level, the “Financial Institutions Index” and the “Financial Markets Index” measure the depth, access, and efficiency of financial institutions (e.g., banks) and financial markets (e.g., stock markets), respectively. At the third level, the depth, access, and efficiency of financial institutions and markets are measured separately. For financial institutions, the depth index measures the size of financial institutions relative to GDP, the access index measures the availability of bank branches and ATMs, and the efficiency index evaluates profitability using indicators such as return on assets or return on equity. For financial markets, the depth index assesses the size of stock and debt markets relative to GDP, the access index tracks how often those markets are used to raise capital, and the efficiency index is measured by the stock market turnover ratio. All indices are normalized on a scale of 0 to 1, with higher values indicating a higher degree of financial development.

Since the literature suggests that overall financial development - and especially financial access through traditional channels like banks - affects the dissemination of alternative lending (e.g., Avramidis et al., 2022; Bazarbash & Beaton, 2020; Claessens et al., 2018; Havrylchyk et al., 2021; Hodula, 2022; Jagtiani & Lemieux, 2018; Maskara et al., 2021; Oh & Rosenkranz, 2020), we use the “Financial Development Index” (FinDev Index) and the “Financial Institutions Access Index” (FinInstiAcc Index). Specifically, we focus on a country’s financial access through bank branches and ATM density, as those measures are commonly used to approximate access to credit (Avramidis et al., 2022; Jagtiani & Lemieux, 2018; Maskara et al., 2021; Ozili, 2019).

To measure financial access more broadly, we construct a “Financial Access Index” (FinAcc Index) by combining the two sub-indices that measure access for financial institutions (FinInstiAcc Index) and financial markets (FinMarkAcc Index), assigning equal weights to each. Following Hodula (2023), we introduce the FinAcc Dummy, a dummy variable that takes the value of 1 if a country’s FinAcc Index is higher than the median for the sample in a given year, and 0 otherwise. We interact alternative lending with this dummy variable to investigate whether alternative lending affects household indebtedness differently in countries with low financial access (FinAcc Dummy equals 0) compared to those with high financial access (FinAcc Dummy equals 1). For a detailed description of all indices in the “Financial Development Index Database”, see Table 7 of the Appendix.

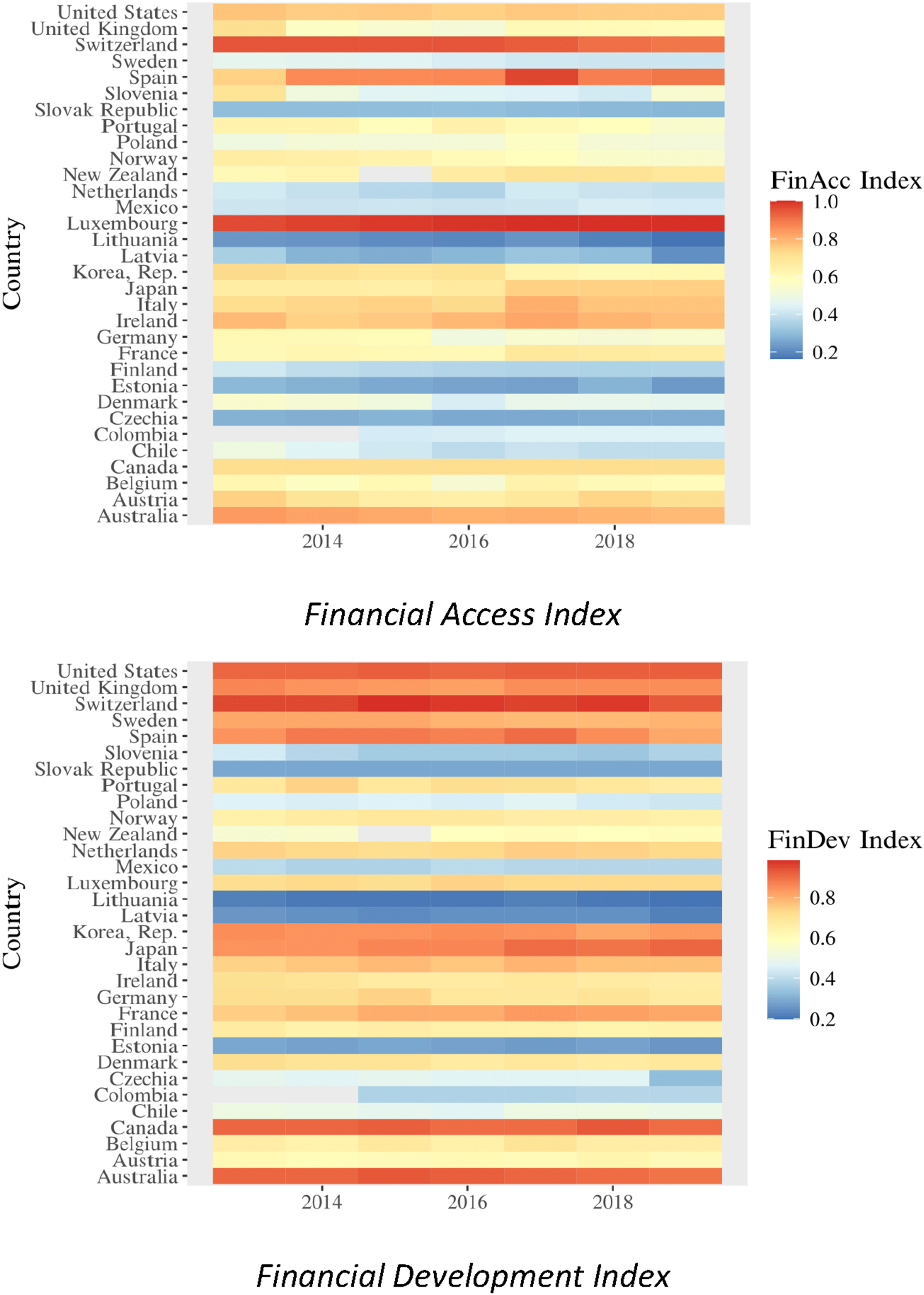

Given that we primarily focus on developed OECD countries, one might assume that the countries in our sample all exhibit high levels of financial development and access, with limited variance across time and between countries. This could raise concerns about the usefulness of the indices in our analysis. However, Figure 1 shows the distribution of the “Financial Development Index” and “Financial Access Index,” revealing significant variance across both time and countries in the sample. Heatmap of the financial development index and of the financial access index. This visualization shows the development of the financial development index and the financial access Index for all countries in the sample over the entire observation period (2013 to 2019)

Our sample includes countries that are financially well-developed with strong access to credit (e.g., the USA, UK, Canada, Australia, and Switzerland), as well as countries with comparatively lower financial development (e.g., Lithuania, Latvia, and Estonia), where “Financial Access” values are around 0.2. This variance, both within and between countries, indicates that the “Financial Development Indicators” provide sufficient variation for a valid analysis.

Methods and Identification

Estimating equation (1) and identifying the impact of Alternative Lending on the household Debt-to-Income ratio is complicated by several factors. First, incorporating the lagged dependent variable in equation (1) results in biased Ordinary Least Squares (OLS) estimates due to the so-called “dynamic panel bias” (Nickell, 1981). This bias arises from correlation between the autoregressive term and the error term, as unobserved country-specific effects are included in both. An efficient and unbiased estimation can be achieved by using the “System Generalized Method of Moments” (System GMM) estimator. This estimator uses differences of the further lagged Debt-to-Income ratio (

We choose the “System GMM” approach over the commonly used “Difference GMM” approach, proposed by Arellano and Bond (1991), because when the dependent variable exhibits persistence and the time period under consideration is short, “Difference GMM” tends to yield biased and inefficient estimates (Blundell & Bond, 1998). This is particularly relevant for our analysis, as Dumitrescu et al. (2022) suggests that household debt is persistent, and our observation period spans only 7 years. To further address the relatively small sample size, we apply a small-sample correction to our estimation.

Moreover, the “System GMM” approach is widely used in finance research, particularly in studies on digital finance in comparable settings (e.g., Andrianaivo & Kpodar, 2012; Gulcemal, 2021; Hodula, 2023; Saygin & Iskenderoglu, 2022; Sun & Chen, 2022; Yahaya et al., 2023; Yao & Song, 2021), underscoring the method’s reliability and relevance.

A second potential threat to proper identification arises from endogeneity concerns. Due to the use of low-frequency data (annual observations), Debt-to-Income, Alternative Lending, and the control variables are likely to be determined simultaneously (Dumitrescu et al., 2022; Hodula, 2023). For example, household indebtedness may affect the demand for credit, and therefore influence Alternative Lending. To account for this simultaneity, we lag the explanatory variables. Despite using lagged values, there may still be bias due to omitted variables. Factors such as the stringency of insolvency laws (Jarmuzek & Rozenov, 2019), government spending, healthcare and education quality (Demir et al., 2022), demographic structure (Yue et al., 2022), and cultural elements like religion and risk tolerance (Branten, 2022; Breuer & Salzmann, 2012; Massó Lago & Abalde Bastero, 2020; Renneboog & Spaenjers, 2012) could affect both alternative lending volumes and the household Debt-to-Income ratio.

Due to sample size limitations, it is impractical to include all these factors in the “System GMM” models. Although country-specific fixed effects could capture many of these relatively stable factors, they are infeasible in this model due to high degrees of freedom loss and an increase in instruments, which could invalidate the estimation. To assess the impact of these country-specific effects, we perform a panel instrumental variable estimation of equation (1) without the lagged household Debt-to-Income ratio but include country-specific fixed effects as a robustness check. Since we no longer need to instrument the lagged dependent variable, the fixed effects are manageable and estimable via OLS.

To address the outlined endogeneity problem - specifically, omitted variable bias within the “System GMM” models - we use societal willingness to adopt new technologies as an instrument for the lagged value of Alternative Lending and the interaction term, isolating endogenous from exogenous variation. High technology openness may indicate a greater propensity to use alternative lending rather than traditional banking. To proxy for this openness, we use three instruments: the number of fixed broadband subscriptions (Broadband), mobile phone subscriptions (Mobile Phone) - previously validated as effective instruments for alternative lending levels (Andrianaivo & Kpodar, 2012; Demirguc-Kunt et al., 2018; Ghosh, 2016; Hodula, 2022, 2023; Sheng, 2021) - and the share of a country’s rural population (Rural Population) (Havrylchyk et al., 2021). Fixed broadband and mobile subscriptions indicate demand for internet-based applications and possibly greater adoption of digital lending (Hodula, 2022, 2023). Rural Population is motivated by (Havrylchyk et al., 2021), who found that alternative lending spreads more quickly in urban, densely populated areas than in rural ones, possibly due to network effects and innovation diffusion dynamics.

To be valid instruments, these variables must strongly explain Alternative Lending and be exogenous - that is, unaffected by omitted variables and not directly influencing household indebtedness. We test instrument relevance through a joint F-test in the first-stage regression, where Alternative Lending is regressed on all exogenous variables, including the three instruments. We argue that these instruments are exogenous. Mobile Phone and Broadband are unlikely to directly impact household indebtedness in the developed OECD countries in our sample, where internet access is both widespread and easily available (Demirguc-Kunt et al., 2018). Similarly, given the short observation period, Rural Population is unlikely to affect variations in Debt-to-Income across countries.

The validity of all instruments (i.e., differenced lags of the Debt-to-Income ratio, Rural Population, Broadband, and Mobile Phone) can be assessed using the Hansen test of overidentifying restrictions (Blundell & Bond, 1998). To confirm instrument validity, the null hypothesis should not be rejected. We also report the total number of instruments used, as a general rule of thumb suggests that the number of instruments should not exceed the number of countries to avoid biased estimation (Roodman, 2009).

Results

Effect of Alternative Lending on the Household Debt-To-Income Ratio

Note. *p

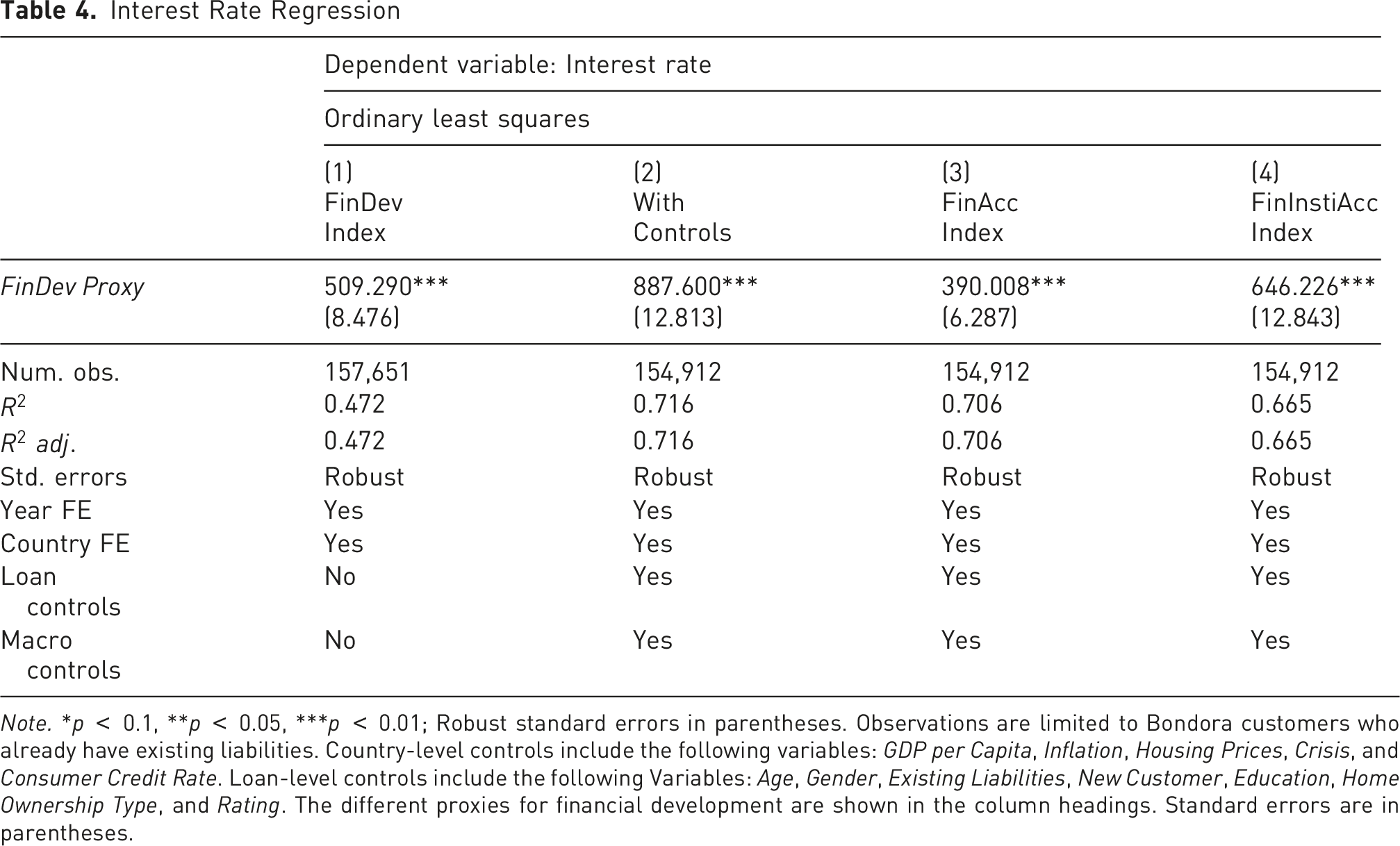

Interestingly, the coefficient for Alternative Lending is negative across all model specifications. Moreover, Alternative Lending becomes significant only when a proxy for financial development or access is included in the model, suggesting that financial development or access may play a crucial role for the effect of Alternative Lending on household indebtedness. For example, in the model that includes the financial development index (FinDev Index), the estimated coefficient for Alternative Lending is −0.365. This indicates that an increase in Alternative Lending by one standard deviation is associated with a 6.57% decrease in the Debt-to-Income ratio in the following year. 6

Furthermore, in column (3), the interaction term with the FinDev Index is not significant, suggesting that a country’s financial development is unlikely to affect the relationship between Alternative Lending and household indebtedness. This is somehow surprising, because the financial development index combines information about the depth, access and efficiency of a country’s financial markets and institutions.

Examining columns (4) to (6), which include interaction terms for a country’s financial access, puts the negative effect of Alternative Lending into perspective. Here, the coefficients of all interaction terms are significant and positive, indicating that the overall effect of Alternative Lending on Debt-to-Income depends on the degree of a country’s financial access. In column (4), for example, the marginal effect of Alternative Lending becomes positive when a country’s financial access index exceeds a threshold of 0.47, which includes access to both financial institutions and capital markets. At this level of financial access, an increase in Alternative Lending leads, ceteris paribus, to a rise in Debt-to-Income in the following year. This threshold is exceeded by 24 countries in our sample at least once during the observation period. 7

For instance, if a country’s FinAcc Index is at or above the 75th percentile, this is associated with an increase in Debt-to-Income of at least 6.06% when Alternative Lending volume increases by one standard deviation in the previous year. Conversely, if a country’s FinAcc Index is at or below the 25th percentile, the Debt-to-Income ratio decreases by at least 1.09% under the same conditions. The coefficient for the interaction term with the FinAcc Dummy (column (5)), which categorizes countries based on whether their financial access is above or below the median, is also significant and positive. For countries classified as having “high access to finance”, a one-standard-deviation increase in Alternative Lending in the previous year leads to a 6.14% rise in Debt-to-Income. In contrast, for “low access to finance” countries, the Debt-to-Income ratio decreases by 3.92%.

In column (6), the marginal effect of Alternative Lending on Debt-to-Income becomes positive when the FinInstiAcc Index exceeds 0.65 index points. This threshold is met by 20 countries in our sample at least once. If a country’s index value is at or above (below) the 75th percentile (25th percentile), the Debt-to-Income ratio increases (decreases) by at least 3.45% (3.73%) when alternative lending volume rises by one standard deviation in the previous year. This finding suggests that access to financial institutions, such as banks, plays a critical role in shaping the impact of Alternative Lending on household Debt-to-Income.

Regarding the model specifications, the adjusted

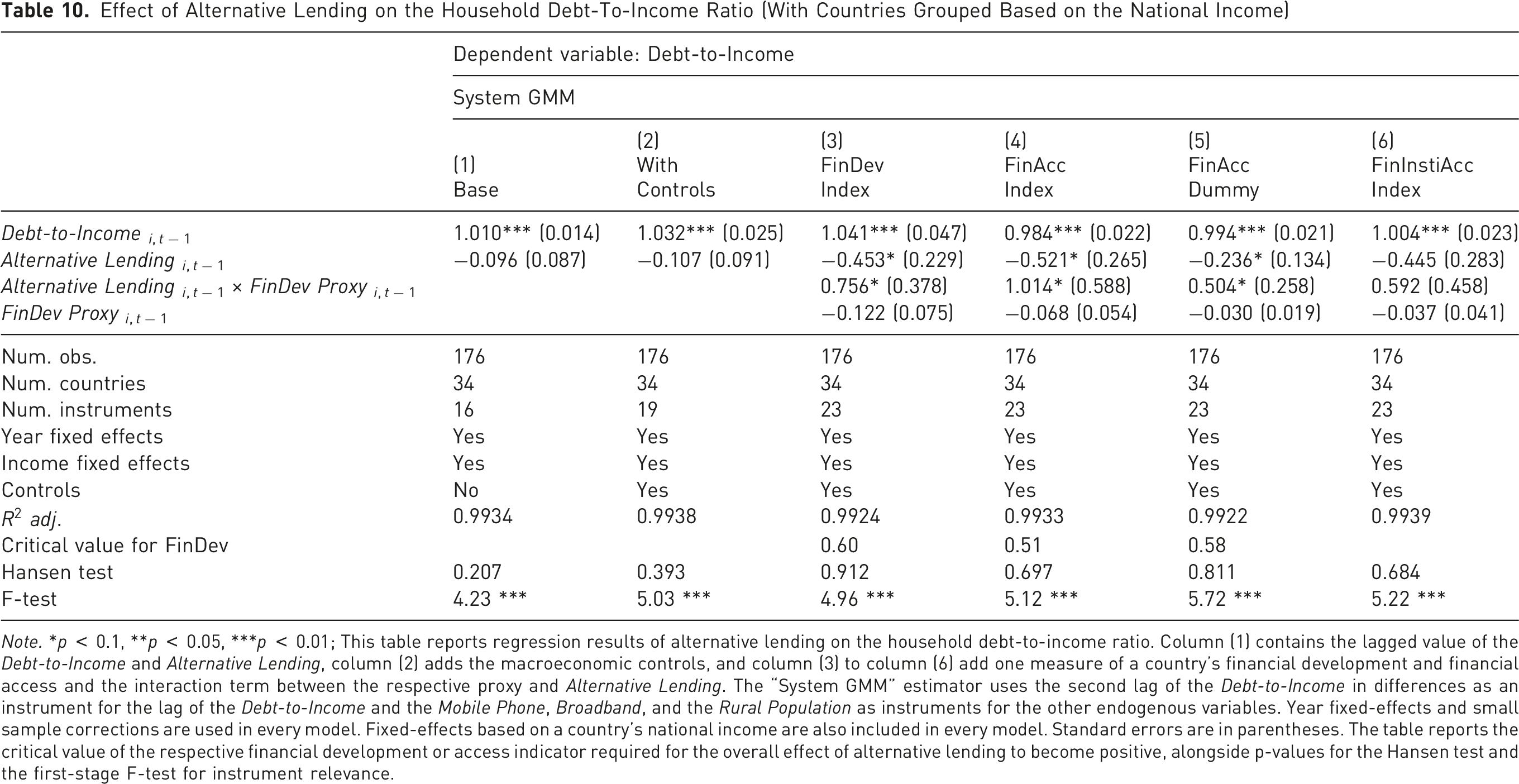

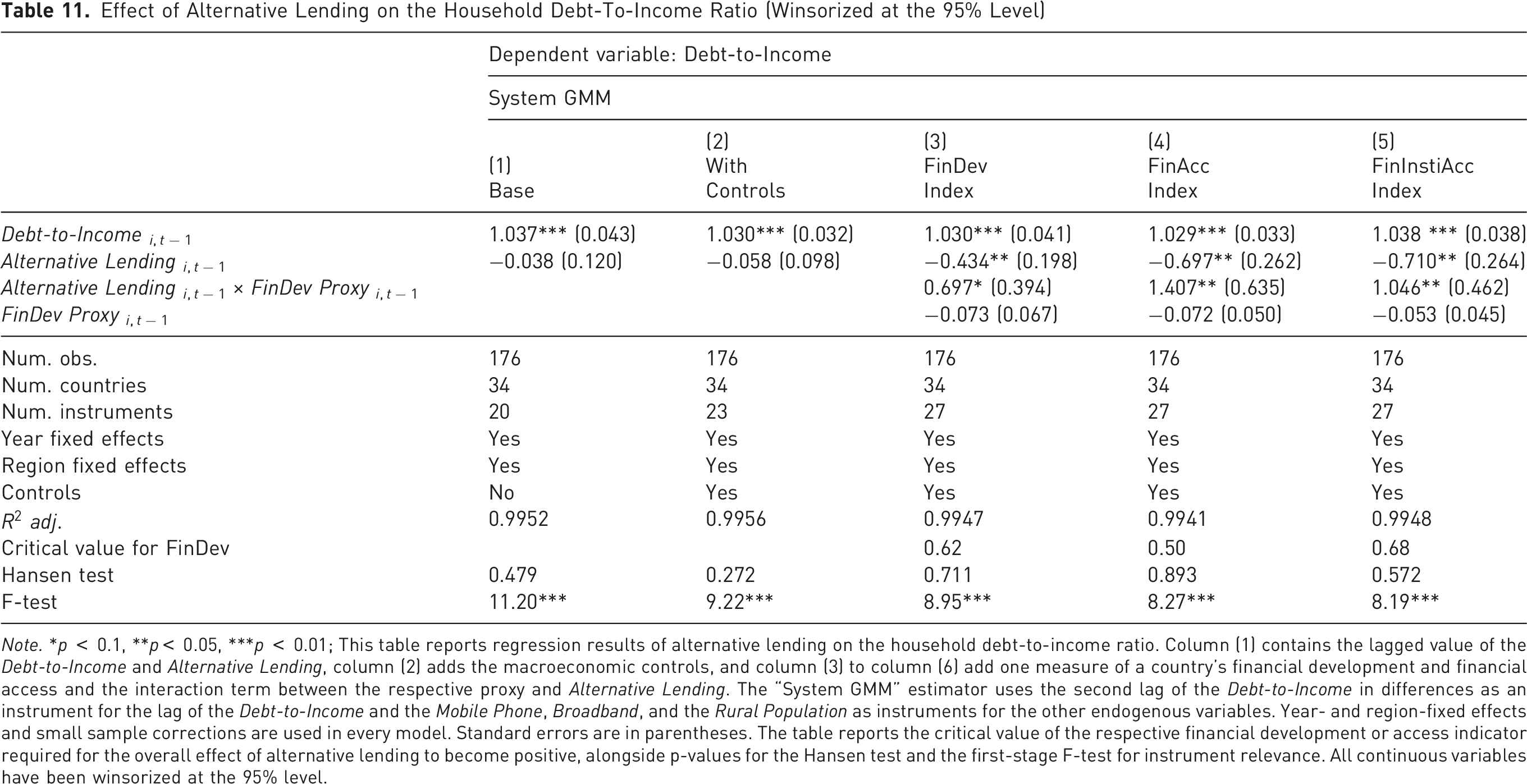

To further evaluate the robustness of our country-level results, we perform several additional tests. First, we exclude regional fixed effects and group countries by income level to address unobserved heterogeneity that may arise from different stages of economic development. 8 Additionally, we winsorize all variables at the 95th percentile to control for outliers that could influence results. The results of these adjustments are presented in Tables 10 and 11 in the Appendix. Our findings remain largely robust across specifications, though the financial development index (FinDev Index) now becomes significant and exhibits an effect on the relationship between Alternative Lending and Debt-to-Income similar to the financial access indicators.

To address the limitation that our “System GMM” specification cannot include country fixed effects due to sample size constraints, we implement a Two-Stages Least Squares (2SLS) approach with country-specific fixed effects. This panel instrumental variable estimation allows us to thoroughly control for the time-invariant unobserved heterogeneity. As in the “System GMM” estimations, we use Broadband, Mobile Phone, and Rural Population as instruments for Alternative Lending and the interaction terms. Due to the persistent nature of the Debt-to-Income ratio, country-specific fixed effects may capture overlapping information, leading to potential collinearity. To mitigate this issue, we exclude the lagged Debt-to-Income ratio. Results for this approach are provided in Table 12 in the Appendix. Again, the findings remain consistent: although the financial access dummy is no longer significant, other financial access indicators retain significance with the expected sign. This suggests that, even when directly accounting for cross-country differences, the mitigating effect of a country’s financial access on the relationship between Alternative Lending and Debt-to-Income remains robust.

Overall, the results confirm Hypothesis 1, as Alternative Lending significantly affects household indebtedness across the estimated models. However, the direction of the effect remains unclear, as it depends on a country’s financial access and is not consistently positive. Hypothesis 2 is confirmed with respect to financial access and, to a lesser extent, financial development, as only financial access consistently exhibits a positive mediating effect across all model specifications.

Loan-Level Analysis

To analyze the mechanisms underlying our country-level results, specifically whether the borrower quality of alternative lenders declines with greater financial development or access to credit, granular data are essential. Aggregated macro variables cannot identify which borrower types predominantly utilize alternative lending, precluding a direct assessment of borrower quality dynamics. To address this limitation, we leverage an extensive loan-level dataset from Bondora, a leading European alternative lending platform. 9 Bondora is an international MPL platform operator that primarily provides consumer credit in Estonia, Spain, Finland, and the Netherlands. From 2014 and 2015, Bondora was briefly active in Slovenia. Because Bondora operates exclusively as a marketplace lender, our micro-level analysis focuses on this specific sub-dimension of alternative lending.

The platform provides detailed information on issued loans, including payment history, debt maturities, and secondary market transactions, through publicly available reports. Bondora’s main dataset includes 112 loan-level variables that detail borrower characteristics at loan origination, loan terms, the bidding process, and current repayment status. Leveraging Bondora’s multi-country operations over several years, we analyze how financial development and access at the country level affect Bondora’s borrower profile. We use Bondora as a proxy for alternative lenders to explore a possible explanation for the country-level results. Specifically, we examine whether, in countries with comparatively high financial development or access, Bondora increasingly serves lower-quality borrowers and those underserved by traditional financial institutions.

To do so, we begin by extracting measures of borrower quality from the Bondora loan-level dataset. For each measure, we then perform a regression analysis to examine how the borrower’s quality is influenced by its country’s level of financial development or access to credit.

Data

Our dataset for the analysis consists of 157,651 observations, spanning the period from 2009 to 2020. To construct the dataset, we combine micro- and macro-level data of different sources: (1) Loan-level Bondora data, (2) Country-level controls (World Bank, OECD), and (3) Country-level proxies for the degree of financial development (IMF).

First, we select relevant variables from the Bondora loan-level dataset to assess whether a borrower is likely of lower quality, i.e., has lower creditworthiness or is possibly underserved by traditional banks. We use three dependent variables related to creditworthiness and the likelihood of obtaining a loan or being neglected by banks. First, we examine the Interest rate, which reflects both loan terms and borrower quality. Higher interest rates for similar loan terms suggest a higher risk premium, indicating lower creditworthiness. We use the maximum Interest rate accepted in the loan application. Second, we use the debt service-to-income ratio (Debt Service) as a proxy for indebtedness, with higher values indicating a greater likelihood of bankruptcy and thus lower creditworthiness. Debt Service measures how much of a person’s monthly income is dedicated to debt service and is chosen over Debt-to-Income used in the country-level analysis, as Bondora does not report Debt-to-Income. However, the two variables are closely related and strongly correlated. 10 Third, we construct a dummy variable, Debt-free Borrower, taking a value of 1 if a new customer has no outstanding liabilities and 0 otherwise. Controlling further for the borrower’s credit grade enables us to examine the platform’s reliance on reaching new, high-risk borrowers without prior liabilities across different markets.

For loan-level controls, we include variables identified in the literature as good predictors of borrower quality, loan terms, and performance: Bondora’s proprietary loan rating (Rating) (Jagtiani & Lemieux, 2019), borrower Education, Age, and whether the borrower is a new customer on the platform (New Customer) (Byanjankar et al., 2015). We also include borrower Marital Status, Gender, Employment status (Lin et al., 2017), number of Existing Liabilities, Home Ownership type, and Use of Loan. All variables are recorded during the application process and loan issuance. Additionally, we clean the loan-level data of erroneous observations (e.g., borrowers’ underage, invalid categories, missing values).

Second, since we are analyzing different countries, we add country-level variables that the literature and our prior results suggest are relevant controls for household indebtedness: GDP per Capita, Housing Prices, and Inflation (Dumitrescu et al., 2022). Additionally, we include a crisis indicator dummy (Crisis), based on the composite leading indicator that signals turning points in business cycle fluctuations (OECD et al., 2008). Critical to the analysis are country-level controls for the average interest rate on consumer credit (Consumer Credit Rate) and the average debt service-to-income ratio (Debt Service Average), which enable us to compare the loan terms and borrower quality of Bondora customers with those of the average country-level lender. Due to data limitations, Debt Service Average is unavailable for Slovenia, which we exclude from our analysis; this exclusion is minor due to the small number of observations (296).

Third, we include country-level financial development and access proxies from the “Financial Development Indicators” database (Svirydzenka, 2016), as used in the preceding country-level analysis (see the previous section for a detailed variable description).

Loan-Level Summary Statistics

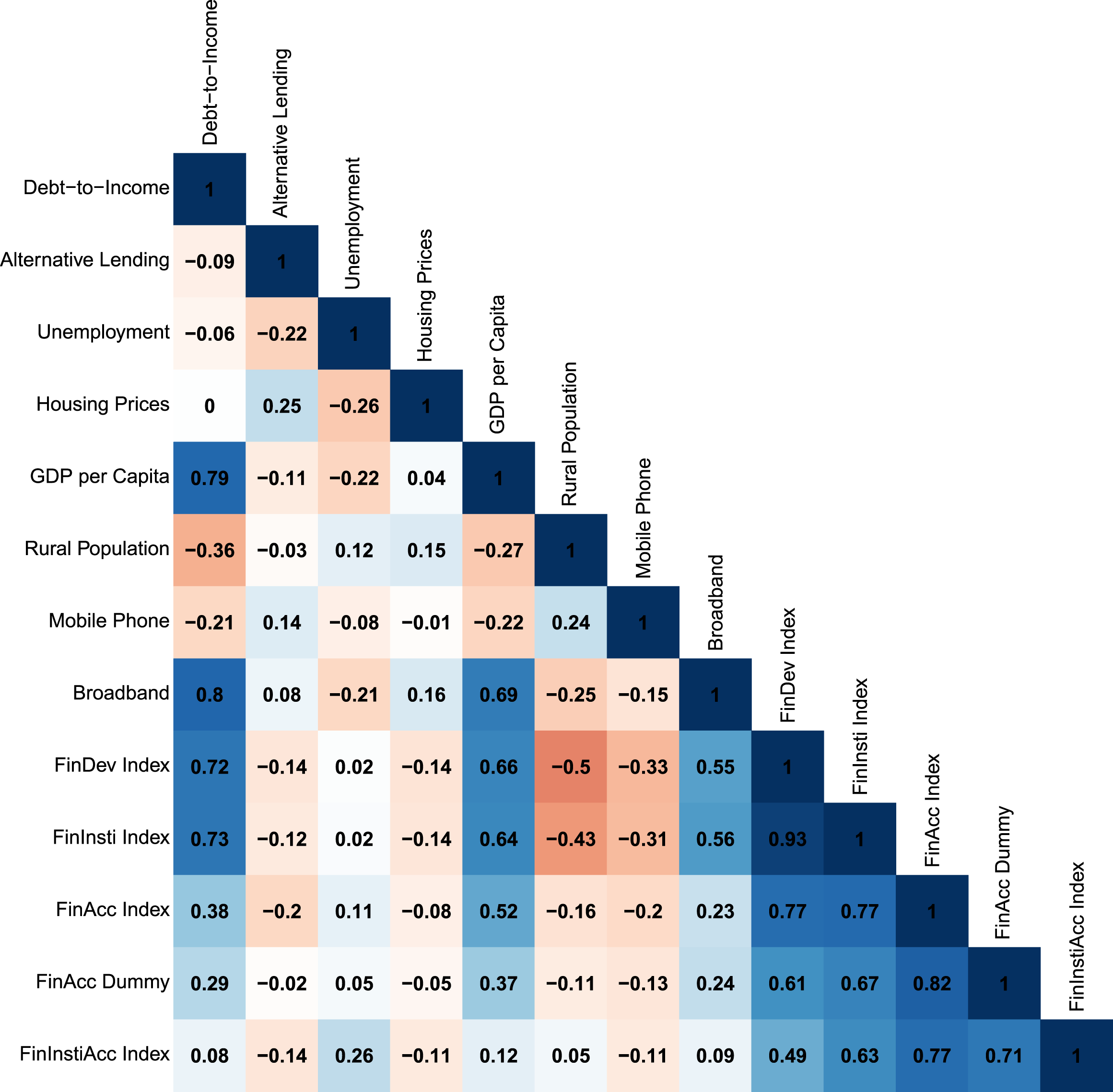

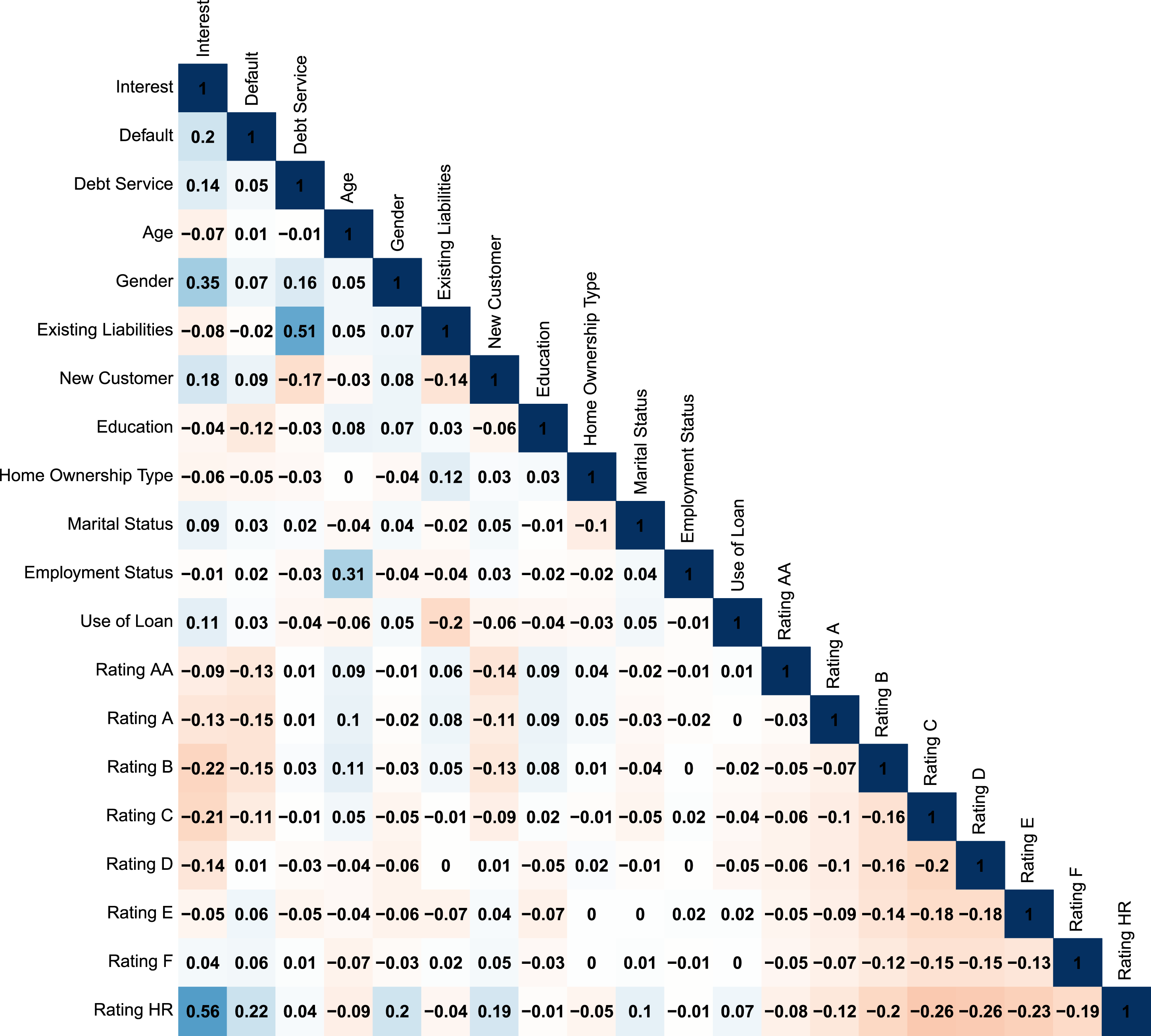

It is worth noting that the number of observations for different variables varies substantially because Bondora only reports certain variables for limited time periods. For instance, Debt Service data are available from 2011 to 2017, resulting in a total of 34,358 observations, while Marital Status, Employment Status, and Use of Loan are reported over similar periods. A correlation matrix of the loan-level variables is provided in Figure 6 of the Appendix.

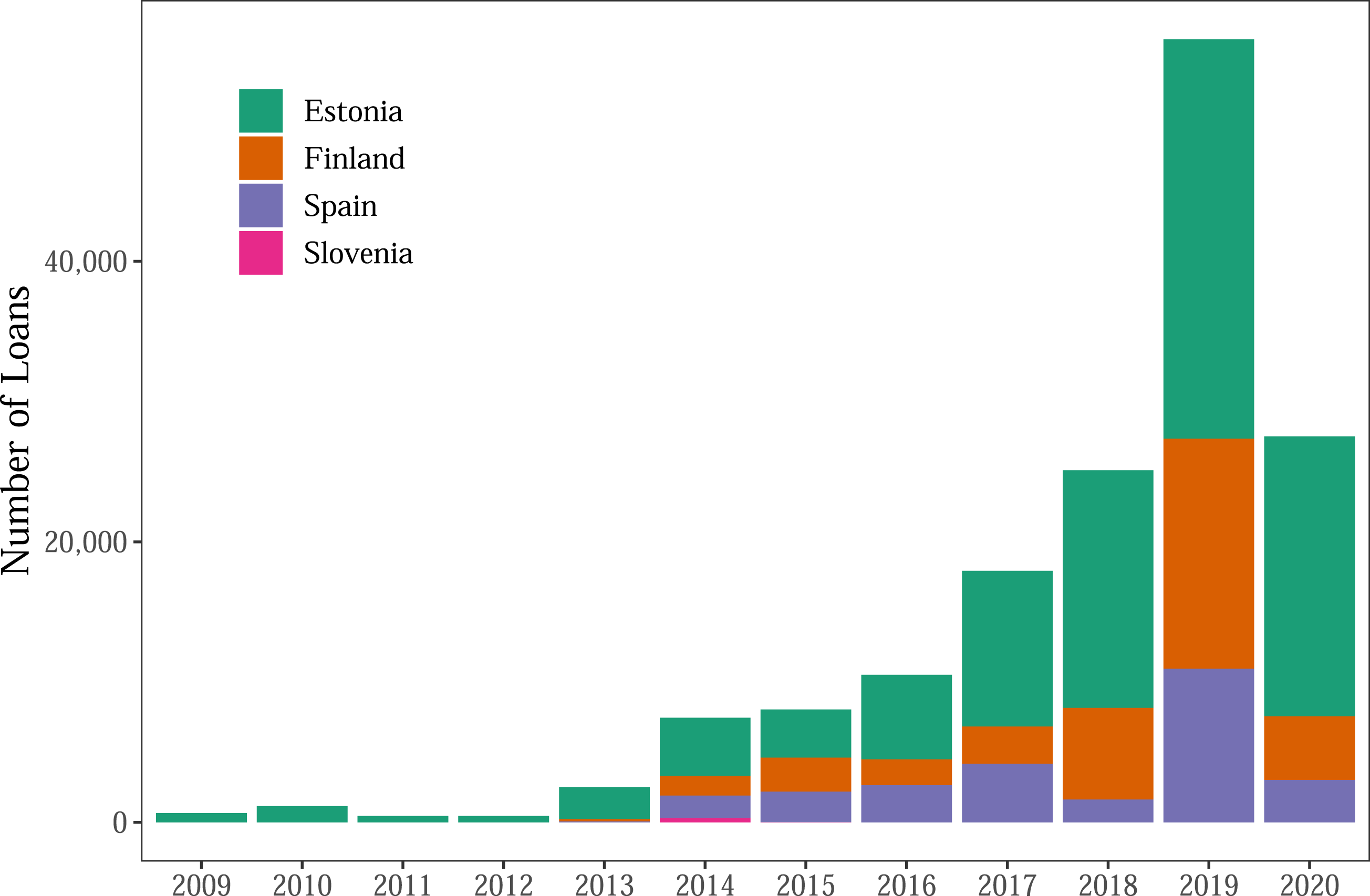

Bondora entered (and exited) its markets in Estonia, Finland, Spain, Slovenia, and the Netherlands at different times. Figure 2 provides an overview of the number of loans originated through Bondora per year in each country. The number of loans grew exponentially from 2012 to 2019 but declined sharply during the COVID-19 pandemic in 2020. The Netherlands is not included in our sample, as Bondora only began lending there in 2022. Bondora’s primary markets are Estonia and Finland, which account for 60% and 23% of total loans originated and 55% and 32% of total loan volume (in U.S. dollars), respectively, over the observation period. Number of originated Bondora loans per country and year

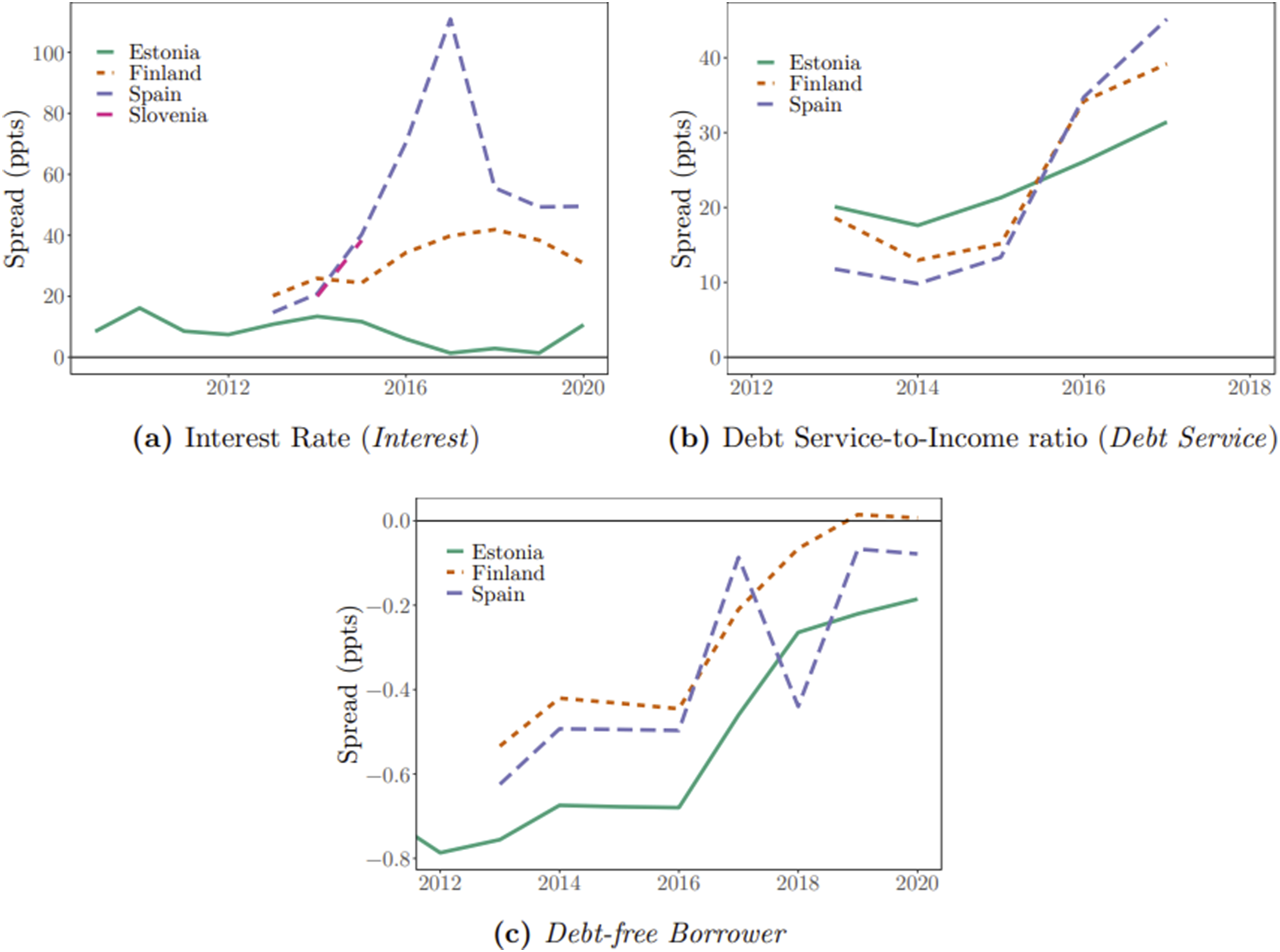

To gain insight into how the creditworthiness of Bondora’s borrowers has evolved over time and across countries, relative to the average borrower at the country level, we calculate spread measures for the three variables related to borrower quality: (1) Interest: We subtract the country-level variable (Consumer Credit Rate) from the country-year average of the loan-level variable (Interest). Positive values indicate that Bondora charges higher interest rates than the country average. (2) Debt Service: Similarly, we subtract the country-level variable (Debt Service Average) from the country-year average of the loan-level variable (Debt Service). Positive values here suggest that, on average, Bondora serves customers with a higher debt burden than the country average. (3) Debt-free Borrower: To construct this measure, we calculate the proportion of new Bondora borrowers with no pre-existing liabilities in each country and subtract the corresponding national share of individuals without bank credit. We source this country-level benchmark data from the World Bank’s Global Financial Development Database. A positive differential indicates that Bondora disproportionately attracts borrowers with no outstanding liabilities relative to the national baseline.

Figure 3 illustrates the development of the spread measures throughout the observation period. The interest rate spreads are positive for all countries, indicating that Bondora, on average, charges higher interest rates than the country average. Between 2013 and 2017, the interest rate spreads for Spain and Finland widened, then slightly narrowed thereafter. In contrast, Estonia’s interest rate spread remained relatively constant at a low level throughout the observation period, even showing a slight negative trend. Spread measures of the dependent variables and the equivalent on the macro level. Spread between the average Debt Service-to-Income ratio (Interest rate, Share of people that have not borrowed any money from a traditional financial institution) at country-level and the average Debt Service-to-Income ratio (Debt Service) (Interest rate (Interest), share of new customers without outstanding liabilities (Debt-free Borrower) of Bondora customers (Bondora loans)

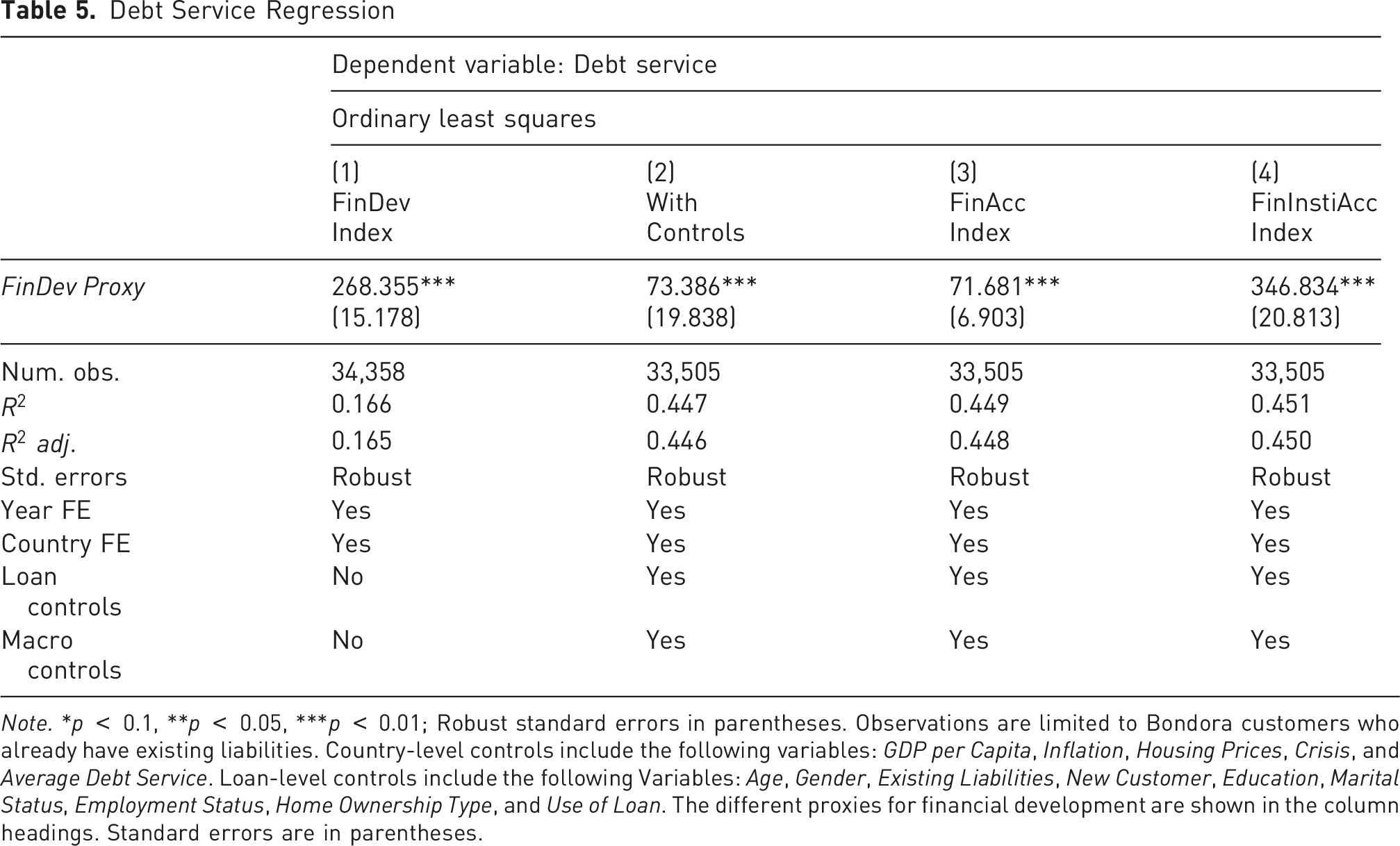

The debt service-to-income ratio is also positive for all countries, indicating that, on average, Bondora customers carry a higher debt burden than the country average. This spread widened from 2013 to 2017 across all countries, suggesting a deterioration in the quality of Bondora’s borrower pool relative to the national averages.

The debt-free borrower spreads are negative but increasing, meaning that the share of new Bondora borrowers without existing liabilities is lower than the share of individuals on the national level without existing bank credit. For our hypothesis to hold true, we would expect that in countries with a higher degree of financial development or access, Bondora would more frequently attract customers who are underserved by traditional banks, specifically, those with lower creditworthiness or those completely new to borrowing.

Descriptive analysis of the spread measures hints at this relationship. In Estonia, which has the lowest FinAccess (0.29), Bondora borrowers exhibit a lower debt burden, pay lower interest rates, and are more likely to have existing relationships with banks compared to the country average. This suggests a higher quality borrower structure compared to Finland and Spain, which have higher FinAccess (0.83 and 0.37, respectively).

However, these stylized facts could also stem from other country-specific factors, such as home bias (since Bondora is headquartered in Estonia) or inherent differences in loan terms compared to the country average, or they could be randomly driven. Therefore, we conduct an in-depth analysis to determine whether Bondora’s borrower structure significantly differs due to a country’s financial access or development, employing several regression analyses.

Borrower Structure Analysis

As financial development and access to credit through traditional channels increase, we hypothesize that Bondora will need to fill a market gap by servicing customers, whom banks may be unwilling to lend to due to lower creditworthiness, ultimately leading to a rise in household indebtedness. In terms of the interest rate charged by Bondora, this would imply that, controlling for loan terms, the interest rate would increase with a country’s financial access. We expect a similar relationship for the Debt Service of borrowers. Regarding the Debt-free Borrower measure, we anticipate that as a country’s financial access rises, the probability of Bondora targeting new customers without existing liabilities (particularly those with low creditworthiness) will also increase, despite the limited pool of unserved customers.

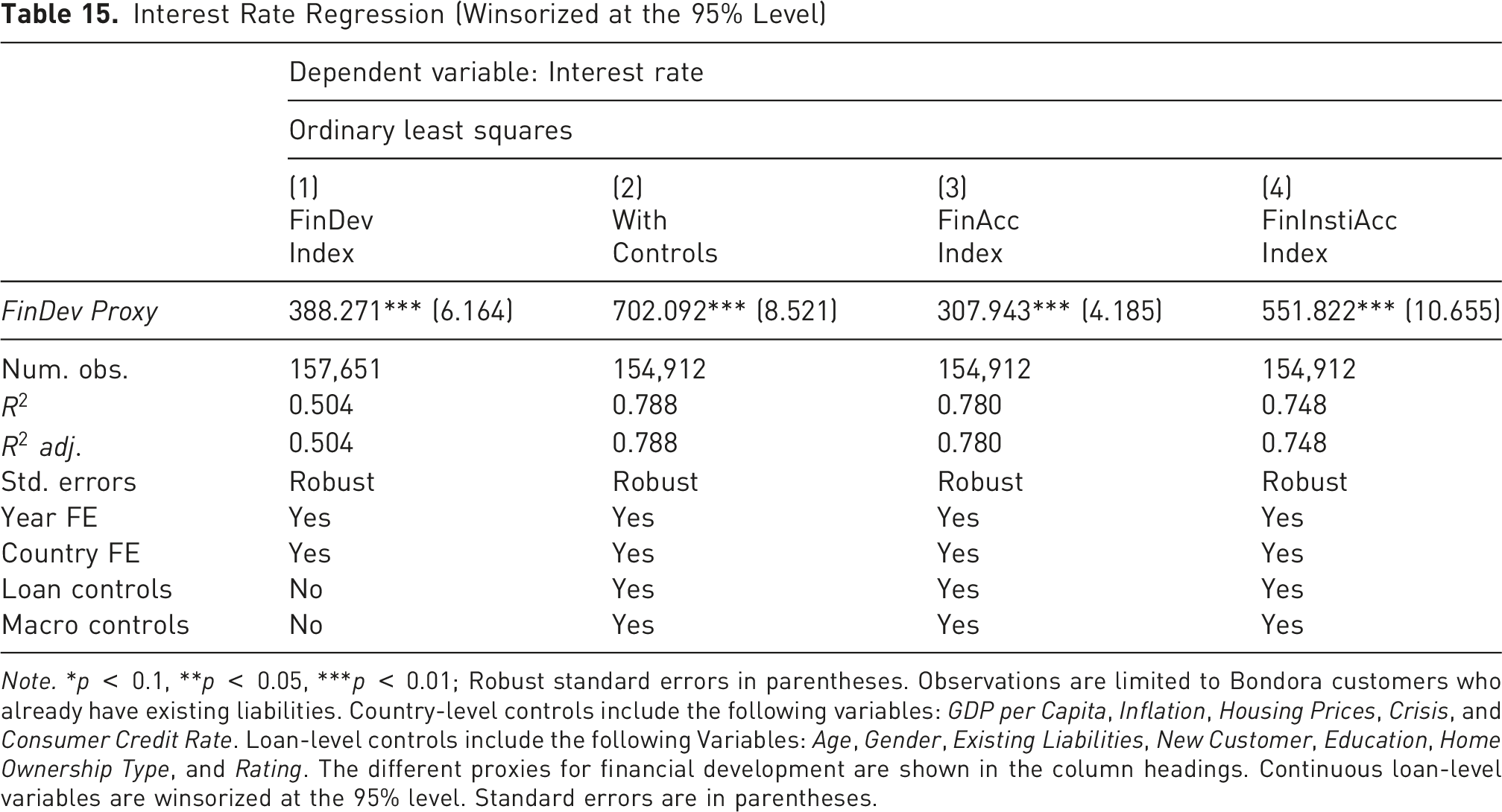

Interest Rate Regression

Note. *p

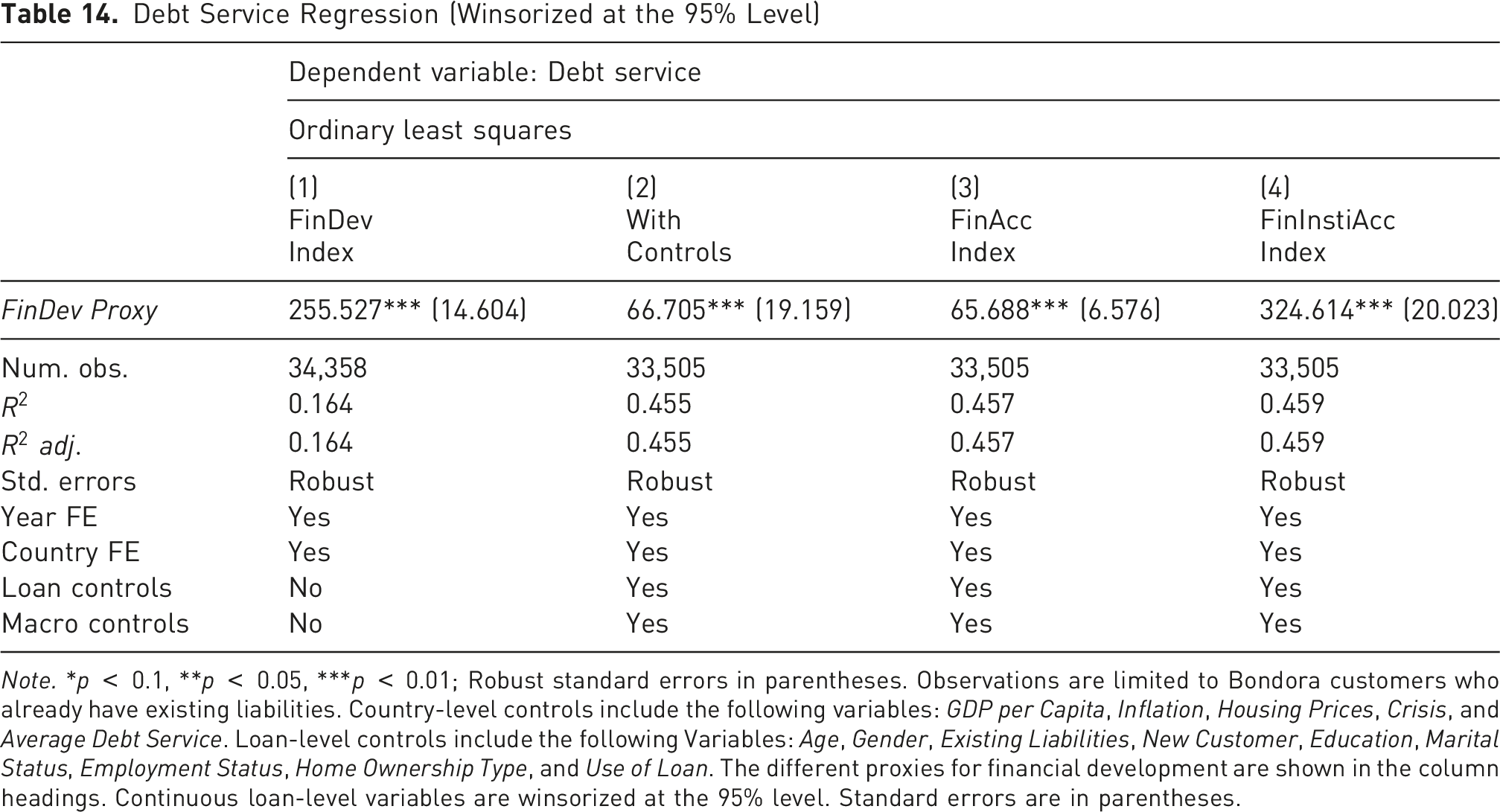

Debt Service Regression

Note. *p

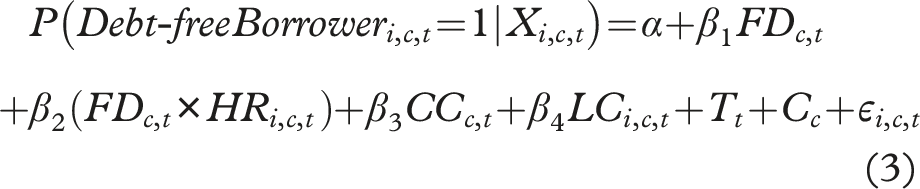

To test the hypothesis related to the debt-free borrower measure, we estimate the following logistic regression model via Maximum Likelihood:

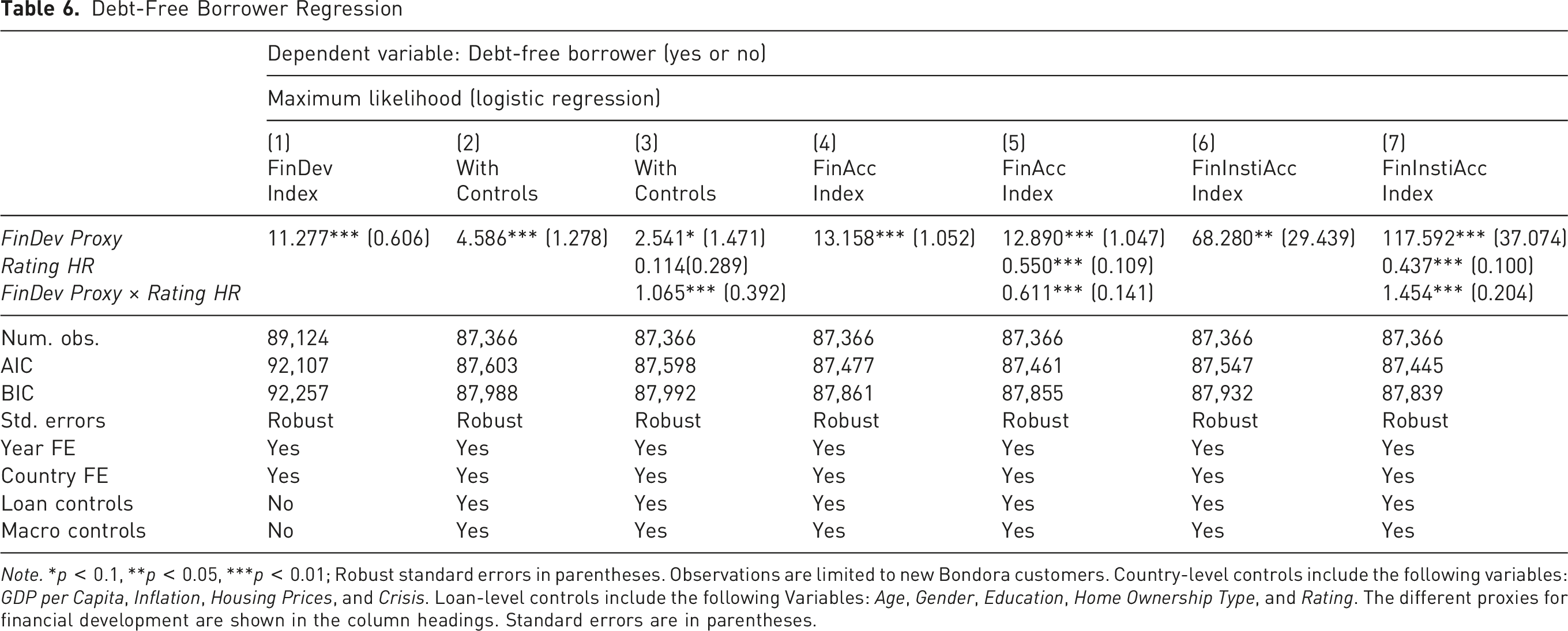

Debt-Free Borrower Regression

Note. *p

All proxies for financial development, as well as the interaction terms, are positively and significantly associated with Debt-free Borrower. As a country’s financial development and access to credit increase, the likelihood that a new Bondora customer has no existing liabilities rises. This likelihood increases even more strongly if the new customer is classified as high risk. These findings suggest that in countries with high levels of financial development or access, Bondora tends to lend more frequently to new customers with no existing liabilities who are categorized as high risk.

Such new customers, who may be in poor financial health, could experience an increase in household indebtedness, potentially contributing to the observed rise in household debt at the country level. Additionally, the results hold economic significance. For example, an average marginal increase in the FinInstiAcc Index by 0.01 points is estimated to raise the likelihood that a new Bondora customer has no existing liabilities by approximately 20.78 percentage points.

Consistent with Hypothesis 3, we find that borrower quality at alternative lenders declines with greater national financial development or access. This supports the mechanisms driving our country-level results. While the study is limited to Bondora, a single MPL platform operating in a select number of European countries, the platform’s lending dynamics clearly illustrate this macro-level shift: as national financial access expands, Bondora commands higher interest rates and increasingly caters to heavily indebted borrowers or high-risk customers with no existing liabilities. This trend could lead to a spike in household indebtedness among borrowers and potentially raise aggregate household debt if similar patterns emerge across other alternative lenders.

The limited sample size raises a concern that results may be influenced by country-specific effects, such as “Home Bias”. However, this is unlikely because we include country-specific fixed effects in all regression analyses, specifically accounting for these factors.

Discussion

Relation to Literature and Theory

Our findings have implications both for the theoretical framework applied in this paper and for several strands of the emerging literature on alternative lending.

First, the significant association we find between alternative lending and household indebtedness supports the credit-rationing view that aggregate borrowing outcomes depend not only on households’ demand for credit, but also on lender-side supply conditions (Stiglitz & Weiss, 1981). From this perspective, the emergence of alternative lenders matters because it changes the effective set of credit options available to households and therefore affects aggregate household indebtedness.

Second, this effect is heterogeneous across countries. We find that alternative lending is positively associated with household indebtedness in countries with comparatively high financial access (and, to a lesser extent, higher financial development), whereas the relationship turns negative in lower-access settings. This pattern is consistent with the liquidity-constraints component of the theoretical framework (Jappelli & Pagano, 1994), according to which the effect of a new lending channel should depend on the tightness of borrowing constraints in the existing financial system. It also helps place earlier borrower-level evidence into a broader perspective. Studies such as Wang and Overby (2022), Yue et al. (2022), and Chava et al. (2021) show that alternative lending can worsen household financial outcomes by contributing to higher debt burdens and financial distress, whereas Danisewicz and Elard (2023) show that an adverse shock to alternative lending can also worsen such outcomes. Our country-level results suggest that alternative lending is not uniformly destabilizing. Its aggregate debt effect depends on the financial environment in which it expands. This helps explain why earlier studies reach different conclusions, even though they examine closely related phenomena. Our results also add to the literature on the interaction between alternative and traditional bank lending. In particular, they support and extend the findings of Hodula (2022), who shows that the relationship between alternative and bank lending depends on banking-sector characteristics. Our country-level findings point in the same direction, as the effect of alternative lending on household indebtedness varies systematically with financial access.

Third, the results of the loan-level analysis indicate that in countries with easier access to bank credit, alternative lenders more often serve borrowers of lower quality. This finding provides a plausible mechanism for the country-level results and is consistent with the lender-heterogeneity and market-segmentation elements of our applied framework (Tang, 2019; Berger & Udell, 2002; Dell’Ariccia & Marquez, 2004). It suggests that alternative lenders do not simply replicate traditional banks, but affect credit allocation differently depending on how strongly their borrower pool overlaps with that of banks. In countries with broad access to traditional credit, standard bankable borrowers may already be largely served by banks. In such environments, alternative lenders may expand mainly by targeting more marginal borrowers whom banks are less willing to finance. Our loan-level results also refine earlier evidence that alternative lenders often concentrate on high-risk borrowers (Cornaggia et al., 2017; Di Maggio & Yao, 2021; Dolson & Jagtiani, 2024; Jagtiani et al., 2019) by showing that this tendency is itself conditional on the surrounding financial environment. In this respect, our results are also consistent with De Roure et al. (2022), who show that alternative lenders can shift toward better-quality borrowers when financial access decreases.

Our findings also qualify the broader claim that alternative lending democratizes finance through improved accessibility. We do not find evidence that the effects of alternative lending are uniform across financial environments. In lower-access settings, alternative lending is not associated with higher household indebtedness and borrower quality appears comparatively stronger, whereas in higher-access settings alternative lenders more often serve marginal and lower-quality borrowers and are associated with higher household indebtedness. This suggests that alternative lending should not be viewed as uniformly democratizing finance, but rather as having heterogeneous effects that depend on the surrounding financial environment.

This point is especially relevant with regard to the outcomes for previously unserved borrowers. In our loan-level analysis, Bondora more often serves first-time borrowers without outstanding liabilities but with low creditworthiness in countries with easier access to bank credit. This pattern does not fit a simple notion of financial inclusion, in which alternative lending mainly broadens sustainable access for underserved but otherwise viable households (Sarma & Pais, 2011). Instead, it suggests that in well-developed financial systems, alternative lenders may reach borrowers who are excluded not only because of lack of access, but also because of weaker credit quality. In such cases, broader access to alternative lending need not coincide with an improvement in borrowers’ financial resilience and may instead increase debt vulnerability.

Policy Implications

The findings have several policy implications. In countries with weaker banking systems and more restricted access to traditional credit, policymakers may view alternative lending as a potentially useful complement to the overall credit infrastructure. In such settings, the results do not suggest that a larger alternative lending sector is associated with rising aggregate household indebtedness, which indicates that policies that allow for the prudent development of alternative lending may support broader credit-market development without necessarily increasing aggregate household debt burdens.

In countries with broad access to traditional credit, however, the results point to a different policy challenge. Here, alternative lending is associated with higher household indebtedness and lower borrower quality, which suggests that regulators should pay closer attention to consumer protection, underwriting standards, disclosure requirements, and affordability assessments. This is particularly important where alternative lenders expand toward more marginal borrowers who may be more vulnerable to financial distress. More generally, our findings suggest that the regulation of alternative lending should be sensitive to country-specific financial conditions rather than based on a one-size-fits-all view of digital credit as either uniformly beneficial or uniformly harmful.

Limitations

The paper has several limitations. Although we study household indebtedness, our results do not directly identify household overborrowing or financial distress. An increase in indebtedness does not automatically imply unsustainable borrowing, just as a decline in indebtedness does not automatically indicate improved welfare. The interpretation of the debt effect therefore requires caution.

The country-level analysis is restricted to OECD countries. Although these countries still exhibit substantial variation in financial development and access, they are, on average, relatively advanced financial systems. Future research could extend the analysis to a broader set of countries, including less developed financial systems, to assess whether the mechanisms identified in this study also apply in other institutional settings.

A further limitation concerns our measure of financial access. The financial-institutions access index, also included in the financial access index, captures physical access to traditional banking through indicators such as bank branch density and the number of ATMs (Svirydzenka, 2016). As a result, it may not fully reflect the actual access households have to bank credit if banks provide credit increasingly through digital channels despite a limited physical presence. At the same time, this limitation is likely less severe for the period examined in this study. Our sample covers 2013 to 2019, a phase in which traditional banks were still undergoing digital transformation rather than already operating as fully digitalized lenders, while fintech and bigtech firms were the more distinct carriers of digital lending innovation (Dehnert, 2020; Thakor, 2020). This issue may become more important in more recent years as research suggests that traditional banks have recently more often adopted digital lending technologies and, in some cases, partnered with fintech lenders in origination processes, thereby reducing the distinction between bank lending and alternative lending (Elliehausen & Hannon, 2024). In particular, partnerships between fintech-lenders and banks now combine banks’ balance-sheet and regulatory position with fintech-lenders online origination and underwriting technologies. As the boundaries between alternative lenders and traditional banks become more blurred, physical proxies such as branch density and ATMs may become less informative about effective access to credit. Future research should therefore revisit both the measurement of financial access and the mechanism identified in this paper, especially whether alternative lenders continue to expand more strongly toward marginal borrowers in high-access environments once traditional banks themselves adopt increasingly similar digital lending processes.

Moreover, the loan-level evidence relies on a single platform, Bondora, and is restricted to a limited number of European countries. Additionally, the Bondora dataset captures only the MPL segment of alternative lending. This constrains the external validity of the borrower-quality mechanism. Additionally, the analysis does not directly compare alternative lenders with traditional banks within the same borrower populations. It therefore remains possible that some borrower-quality patterns reflect broader country characteristics rather than alternative lending specifically. Relatedly, future work could distinguish more clearly between fintech and bigtech lending, between household and business loans, and between platform-specific and market-wide effects. A broader comparative design including multiple alternative lenders and traditional banks would help assess the generalizability of the patterns documented here.

Conclusion

Our country-level analysis reveals that alternative lending, despite being a relatively new form of credit provision, already influences aggregate household indebtedness. We observe, that this relationship depends on a country’s level of financial development and access to traditional credit channels, such as banks. When a country reaches a certain threshold of financial development and households have relatively easy access to financial resources, the effect of alternative lending on household indebtedness turns positive, reinforcing the debt-increasing impact of alternative lending. These results align with existing literature, that outline the importance of banking system characteristics on the effect of alternative lending. A limitation to these findings is that our sample includes only OECD countries, all of which have relatively high levels of financial development.

Our additional loan-level analysis supports the country-level findings and also sheds light on possible mechanisms explaining these results. As financial access increases, alternative lenders increasingly extend credit to individuals with potentially lower credit ratings. This behavior is evident for Bondora, as higher financial development or access to credit correlates with increased interest rates and a greater likelihood of serving high-risk customers with no outstanding liabilities. The interpretation of these results is constrained by the focus on a single platform and limited variability at the country level.

Further research could expand this analysis to include non-OECD countries, utilize alternative loan-level datasets, and explore the underlying mechanisms in more detail. These findings also have policy implications: In countries with weaker banking systems and more restricted access to traditional credit, alternative lending may support credit-market development without necessarily increasing aggregate household debt burdens. In countries with broad access to traditional credit, however, alternative lending is associated with higher household indebtedness and lower borrower quality, suggesting a need for closer attention to consumer protection, underwriting standards, disclosure requirements, and affordability assessments. Overall, the regulation of alternative lending should reflect country-specific financial conditions rather than a uniform view of digital credit.

Footnotes

Acknowledgments

We sincerely thank the individuals and groups whose inputs have shaped and enhanced this study. We are grateful to the participants of the 6th Workshop in Applied Economics for Young Researchers 2024 in Hannover, Germany; the Fintech Conference 2023 in Cardiff, Wales; the European Alternative Finance Research Conference 2022 in Utrecht, Netherlands and the UniCredit/HVB Doctoral Seminar 2022 in Osnabrück, Germany for their valuable comments and suggestions. Special thanks go to the members of our department for their valuable contributions. We gratefully acknowledge financial support of the Volkswagen foundation and the Lower Saxony Ministry for science and culture. Moreover, we thank the Universitätsgesellschaft Osnabrück e.V. (Osnabrück University Society) for its financial support for conference participation. The views expressed here are those of the authors and not necessarily those of the funding institutions.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Volkswagen foundation (Nieders. Vorab) and the Lower Saxony Ministry for science and culture (Grant number: 76251-14-2/21 (ZN3746)). The views expressed here are those of the authors and not necessarily those of the funding institutions.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The underlying data set of the paper is gathered from public sources such as Bank for International Settlement, Organisation for Economic Co-operation and Development (OECD), International Monetary Fund (IMF) and Bondora public reports.

Use of AI

We used Grammarly and ChatGPT to check the manuscript for grammar and spelling mistakes. Otherwise, no AI Tools were used.

Notes

Author Biographies

Appendix

Financial development indicators. The figure illustrates the hierarchical structure of the IMF’s financial development indicators Correlation matrix of the country-level data Correlation matrix of the loan-level data

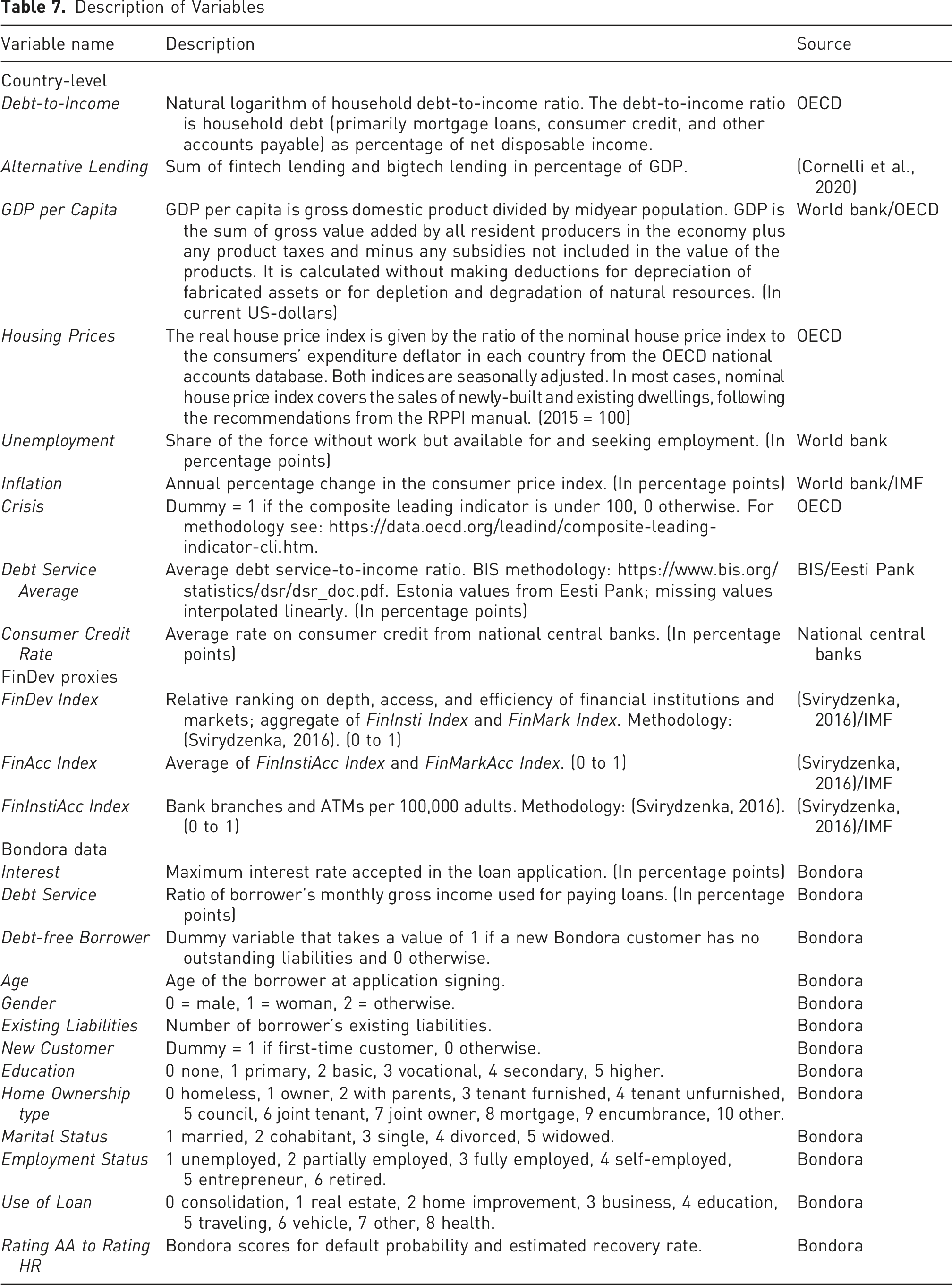

Description of Variables Countries Exceeding the Threshold of FinAcc Index so that Alternative Lending has a positive Effect on Debt-To-Income 1 indicates that a country exceeds the threshold of 0.47 index points of the FinAcc Index in the year under consideration, 0 otherwise. Countries Exceeding the Threshold of FinInstiAcc Index so that Alternative Lending has a positive Effect on Debt-To-Income 1 indicates that a country exceeds the threshold of 0.65 index points of the FinInstiAcc Index in the year under consideration, 0 otherwise. Effect of Alternative Lending on the Household Debt-To-Income Ratio (With Countries Grouped Based on the National Income) Note. *p Effect of Alternative Lending on the Household Debt-To-Income Ratio (Winsorized at the 95% Level) Note. *p Effect of Alternative Lending on the Household Debt-To-Income Ratio (Two-Stage Least Squares Without Lag of Debt-To-Income Ratio, With Country Fixed-Effects) Note. *p Country-Level Variables Summary Statistics Debt Service Regression (Winsorized at the 95% Level) Note. *p Interest Rate Regression (Winsorized at the 95% Level) Note. *p Debt-Free Borrower Regression (Winsorized at the 95% Level) Note. *p < 0.1, **p < 0.05, ***p < 0.01; Robust standard errors in parentheses. Observations are limited to new Bondora customers. Country-level controls include the following variables: GDP per Capita, Inflation, Housing Prices, and Crisis. Loan-level controls include the following Variables: Age, Gender, Education, Home Ownership Type, and Rating. The different proxies for financial development are shown in the column headings. Standard errors are in parentheses.

Variable name

Description

Source

Country-level

Debt-to-Income

Natural logarithm of household debt-to-income ratio. The debt-to-income ratio is household debt (primarily mortgage loans, consumer credit, and other accounts payable) as percentage of net disposable income.

OECD

Alternative Lending

Sum of fintech lending and bigtech lending in percentage of GDP.

(Cornelli et al., 2020)

GDP per Capita

GDP per capita is gross domestic product divided by midyear population. GDP is the sum of gross value added by all resident producers in the economy plus any product taxes and minus any subsidies not included in the value of the products. It is calculated without making deductions for depreciation of fabricated assets or for depletion and degradation of natural resources. (In current US-dollars)

World bank/OECD

Housing Prices

The real house price index is given by the ratio of the nominal house price index to the consumers’ expenditure deflator in each country from the OECD national accounts database. Both indices are seasonally adjusted. In most cases, nominal house price index covers the sales of newly-built and existing dwellings, following the recommendations from the RPPI manual. (2015 = 100)

OECD

Unemployment

Share of the force without work but available for and seeking employment. (In percentage points)

World bank

Inflation