Abstract

UK governments of all political colours have sought to improve productivity in health care by introducing pro-competitive reforms in the National Health Service (NHS) during the last two decades. The first wave of reform operated from 1991 to 1997. The second wave was introduced in England only in the mid 2000s. In 2010, further reform in England, intended to increase the extent of competition, was proposed by the Coalition administration. But the effect of competition on productivity in health care and in particular on the quality of health care remains a contested issue. This paper reviews the evidence, focusing on robust and recent evidence, on the use of competition as a mechanism for improving quality. The consensus is that competition will increase quality in health care, but that institutional details matter. Given this, we end by discussing whether the current plans to make the buyers of care family doctors and other professionals and to allow some local price variation are likely to be beneficial in the UK context of full public funding for health care.

Introduction

Health care is one of the most important industries in developed countries, both because of its size and impact on wellbeing. Historically, health care has been provided through centralized, non-market means in most countries outside the USA. However, recently market-oriented reforms have been adopted or are being considered in many countries, including the UK (England), the Netherlands, Belgium, Israel, and Australia, despite a lack of strong evidence on the effects of market reforms in health care. In the USA, markets have long been used for the delivery of health care. However, massive consolidation among hospitals has led to concerns about the functioning of these markets. These developments raise questions as to whether pro-market reforms are an appropriate way of improving outcomes in health care.

A central concern about the functioning of markets in health care is whether competition will deliver the socially optimal quality of care.1,2,6 Quality is a major issue in health care. First, the effect of quality on an individual's wellbeing can be very large. Second, due to the widespread presence of insurance against health care expenditures (the USA), or provision of care free of charge (UK, Europe), health care consumers are not exposed to the full expense associated with their health care decisions so that quality looms larger in consumer choice than price.

Despite these doubts, UK governments in the 2000s have seen pro-competitive reforms as a key way of improving health care productivity in England (though, for reasons of devolved responsibility for health at national level, not in Scotland, Wales or Northern Ireland). In 2006, under a Labour administration, the English NHS adopted a payment system in which hospitals were increasingly paid fixed, regulated, prices for treating patients (‘Payment by Results’ [PbR], which is similar to the Medicare hospital payment system in the USA) and mandated that all patients requiring treatment be given the choice of five different hospitals (‘Choose and Book’). Prior to this reform, the local public agencies responsible for purchasing health care on behalf of the population in their area engaged in selective contracting with hospitals, bargaining over price and quantity. The reform therefore provided patients with more choice, both via the mandated five alternatives and the end of selective contracting, and moved hospitals from a market determined price environment to a regulated price environment. This reform programme has been taken forward by the succeeding Coalition government which is introducing, at the date of writing, further reforms which seek to extend the extent of competition. The components of this reform include the explicit encouragement of greater provider diversity, including use of the private and third sectors, moving the purchasing budgets from primary care trusts (PCTs) which act for family doctors (general practitioners [GPs]) to clinical commissioning groups (CCGs) directly involving GPs and other health professionals, and greater emphasis on regulation of market structure. 3 In addition, in a move to further increase the scope of the tariff and build on the PbR system, the proposals include a plan to allow non-mandatory local variation of service specification and the related price under rules set out by Monitor (the new NHS sector regulator). For such services outside the national tariff, local prices will be determined by CCGs and may be governed by rules set by Monitor and the NHS Commissioning Board (the new body responsible for overseeing commissioners of NHS services).

Given the potential boldness of these reforms, it is worth reviewing the evidence on the effect of competition in the UK and elsewhere. To this end, we bring together evidence on the use of competition in health care markets, including the emerging lessons from the Labour changes of the 2000s in England. We then consider the lessons from this evidence for the current direction of policy. The paper is organized as follows. Section 1 briefly reviews the theoretical support for the use of competition on the provider side of health care markets and notes the USA evidence. Section 2 focuses on the most robust and recent evidence from the UK. Section 3 is more speculative and discusses the potential role of price competition in the English NHS market.

The theoretical support for competition and empirical evidence from the USA

In the last few years a relatively small, but important, literature has emerged on competition and quality in health care markets.4–6 Economic theory suggests that competition will increase quality in markets with regulated prices (provided price is above marginal cost). The models largely derive from analyses of industries subject to price regulation up until the 1970s and 1980s, e.g., airlines and taxis, but there are also some models specific to health care. 6 The intuition of all these models is as follows. Price is regulated, so firms compete for consumers on non-price dimensions, i.e. ‘quality’. If the regulated price is set above marginal cost at some baseline level of quality, then firms will increase quality to try to gain market share. This will continue until profits are zero. There is empirical evidence to support this prediction from the USA. This comes from the USA Medicare programme and mostly from treatment of heart attack patients. The most prominent study of markets with fixed prices is by Kessler and McClellan, 7 who examine the impact of market concentration on mortality for Medicare heart attack patients. They find that mortality is substantially and significantly higher for patients in more concentrated markets. Kessler and Geppert 8 find that high risk Medicare patients' heart attack mortality is higher in highly concentrated markets, while there is no such effect for low risk patients. Tay 9 estimates a model of hospital choice for Medicare patients and finds that demand is responsive to quality, again measured by heart attack mortality, implying the potential for quality competition. Shen 10 also finds less market concentration in the Medicare market reduced patient heart attack mortality during the 1990s.

While the majority of the USA evidence from Medicare finds that competition increases quality, there are also some papers which come to the opposite conclusion. Gowrisankaran and Town, 11 using similar methods to Kessler and McClellan, 7 find that mortality is higher for Medicare heart attack and pneumonia patients receiving care in less concentrated markets in the Los Angeles area. Mukamel et al. 12 find no effect of market concentration on mortality from all causes for Medicare patients.

When prices are market determined, however, there is no general theoretical prediction of the effect of competition on quality. Quality could be too low or too high. 4 For example, if buyers place more emphasis on price (perhaps because it is more easily measured), this could lead to competition on price at the expense of quality. On the other hand, the opposite is also possible, for example, the so called ‘medical arms’ race model in which hospitals compete on technology to attract high quality staff whilst passing costs on to relatively price-insensitive employers. The empirical literature in the USA which examines the impact of competition on quality with market determined prices is smaller but mirrors the theoretical indeterminacy. For example, Sari 13 finds that competition is associated with better outcomes, while Volpp et al. 14 find that market oriented reforms in New Jersey were associated with worse outcomes. Nonetheless, Vogt and Town, 5 and more recently Gaynor and Town, 6 determine that the preponderance of the empirical evidence shows that competition leads to better patient outcomes.

The common feature of the USA studies is that they all use variation in market structure for identification. Put another way, they examine the impact of changes in market structure in already operating markets. This strategy, however, carries with it a problem that is hard to overcome: market structure may be endogenous to quality. For example, the presence of a high quality hospital in a market may deter entry by others. If this is the case, analysis of the relationship between market structure and outcomes would conclude that concentration results in higher quality, whereas in fact the direction of causality is the opposite one.

Evidence from England in 2000s

The fact that pro-market policies have been introduced by reform in the UK means that that the UK experience provides a source of evidence that is not contaminated by this potential problem. In addition, local health care markets in the UK are characterized by less complexity than perhaps those of the USA, making lessons from the UK potentially more portable to countries with NHS-type systems wishing to introduce market-oriented reforms on the supply side and also perhaps to social insurance systems where there is universal health insurance.

In 2006, the NHS in England adopted a system in which hospitals were paid fixed, regulated, prices for treating elective patients (similar to the Medicare hospital payment system in the USA) and mandated that all patients requiring treatment be given the choice of five different hospitals. Prior to this reform, the local public agencies responsible for purchasing health care on behalf of the population in their area engaged in selective contracting with hospitals, bargaining over price and quantity of services. The reform therefore provided patients with more choice, both via the mandated five options and the end of selective contracting, and moved hospitals from a market-determined price environment to a regulated price environment. We focus on the emerging quantitative research: other papers in this issue examine more qualitative studies of the impact of the choice policy.

Cooper et al. 15 and Gaynor et al. 16 adopt the same research design, also used by Propper et al. 17 to study the 1990s NHS internal market. They exploit the fact that the reforms of the mid-2000s were introduced by policy onto an existing market structure. Because health care is a good that individuals wish to consume close to home, there are more hospitals in urban areas where population density is high. Thus hospitals located in urban areas will be in less concentrated markets. But before the pro-competitive policy was introduced, these hospitals did not compete. However, after the policy was introduced, competition was possible in less concentrated (urban) markets and less possible in more concentrated (rural) markets. Thus the effect of concentration can be inferred from the change in behaviour of hospitals located in more or less concentrated markets pre and post reform.

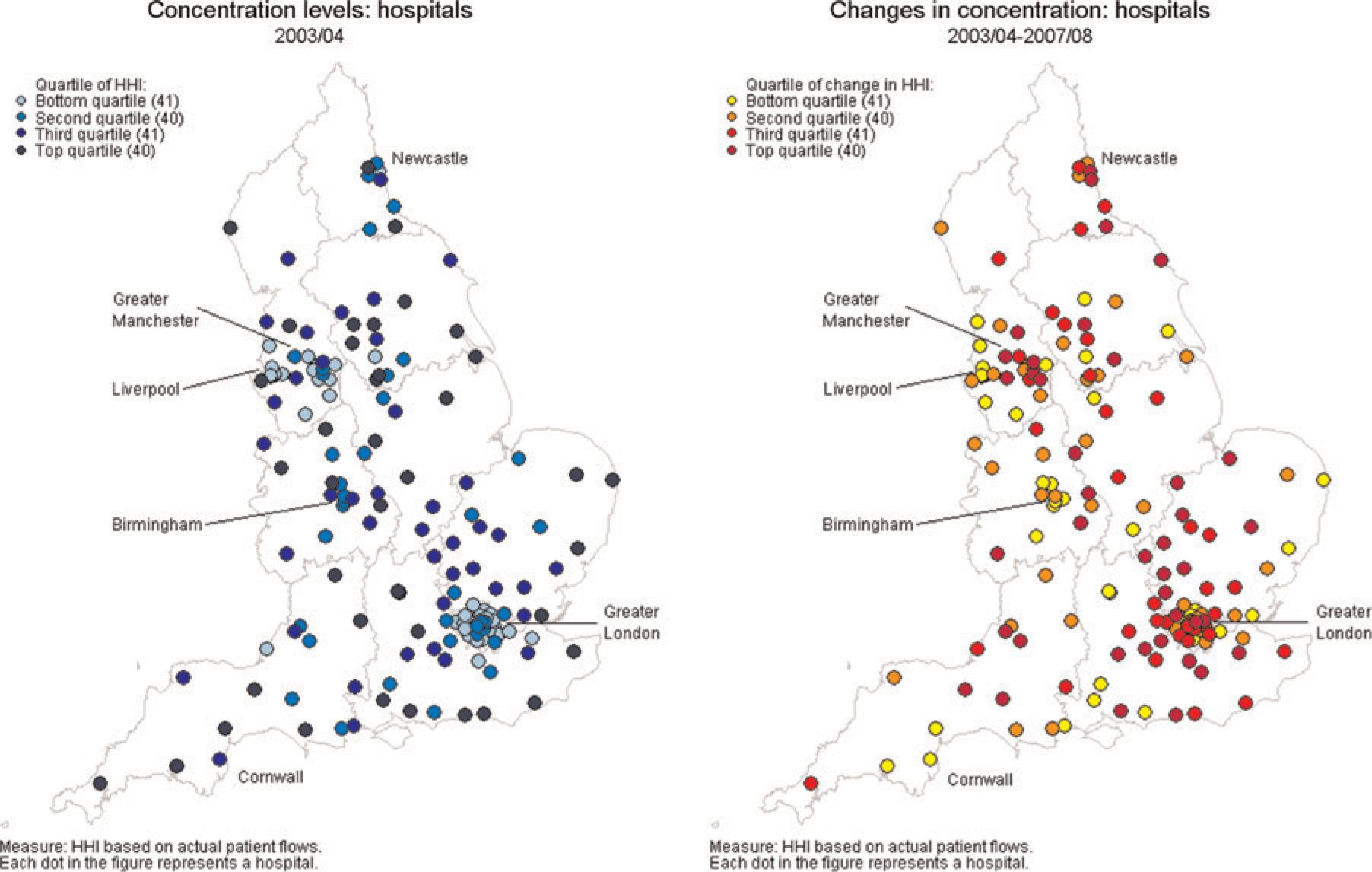

Gaynor et al. 16 begin by establishing whether the reforms did lead to change in travel patterns by patients. If no changes in travel patterns are observed, then regardless of potential for competition, we would have to conclude that no competition actually occurred. They find this not to be the case. Gaynor et al find that travel patterns have changed such that market concentration fell for almost all hospitals, particularly those located in and around urban areas. The left hand map of Figure 1, taken from Gaynor et al 16 , shows the extent to which hospitals in England face potential competition as measured by a standard measure of market concentration. This is the Herfinahl-Hirschman Index (HHI), which is the sum of the squared market shares of all hospitals in a geographical market. The dots in the figure represent quartiles of the distribution of the HHI, where light blue is the lowest quartile, i.e., the least concentrated, and dark blue is the top quartile, i.e., the most concentrated. The right hand map shows where the greatest changes in market concentration occurred in the two years after the policy was implemented. The darkest red dots show the most change in concentration (top quartile of change) and the yellow dots show the least change.

Market concentration pre-reform (2003) and changes in concentration 2003–2007. HHI = Herfinahl-Hirschman Index

From the left hand panel, it is clear that the most potential for competition is in the urban areas (those hospitals marked in light blue), but from the right hand one it is clear that the hospitals which experienced the greatest decrease in market concentration (those marked in red) were located both in urban areas and in the suburban areas around major cities. In other words, changes in travel patterns affected hospitals in, and in a relatively wide area around, the conurbations of England. Gaynor et al. also looked at which hospitals were attracting patients post-reforms and found that hospitals which, pre-reforms, had shorter waiting lists and those which had higher clinical quality (as measured by lower death rates for patients admitted with heart attacks), had larger increases in patient numbers post-reforms and drew their patients from a larger number of local areas than hospitals with lower patient quality pre reform. These travel pattern changes suggest that, despite concern over the penetration of the ‘Choose and Book’ hospital appointment system, that the reforms did cause some movement towards higher quality hospitals.

In more formal statistical analyses, Cooper et al. 15 and Gaynor et al. 16 both found that hospitals facing potentially more competition had a larger increase in clinical quality post-reform as measured by the decrease in death rates following emergency admissions for heart attack than hospitals which faced less potential competition. Gaynor et al. also looked at measures of access and expenditure and found that patients in hospitals which faced more potential competition had lower lengths of stay and that these quality improvements were achieved without any increase in total hospital expenditure. On the other hand, they found no impact of the reform on some other measures of clinical care or on waiting times.

Based on these results, Cooper et al. and Gaynor et al. concluded that the ‘Choose and Book’ regime, coupled with the DRG regulated price regime, had led to an improvement in clinical quality. However, the change in quality was small. Gaynor et al. estimate that the value of the life years saved equated to around 0.2% of the NHS budget. This small effect would be expected for a policy that was in operation only for a couple of years at the time of evaluation. However, Gaynor et al. note that the effect of larger changes in market concentration could be considerably larger. Such gains however would require a substantial reduction in market concentration and thus changes in purchasing patterns. We return to this issue in the final section.

Cookson et al. 18 examined the impact of the policy on equity. Using small area socioeconomic data between 2003 and 2008 they looked at the change in the association between elective hospital utilization and small area deprivation over the period when the pro-competition reforms were phased in. They estimate the policy effect from the three-way interaction of market dispersion, deprivation and time. They find an initial negative association between market dispersion and elective admissions in deprived areas. Pro-competition reforms reduced this negative association slightly. They conclude that increased competition in the NHS between 2003 and 2008 did not undermine socioeconomic equity in hospital care and, if anything, may have very slightly increased utilization of elective inpatient care in deprived communities.

These three studies exploit the change in policy to examine the impact of potential competition on quality. Bloom et al. 19 provide recent evidence of better performance of hospitals in less concentrated markets from a rather different perspective. In a study of management quality in the NHS, they found that hospitals with better management practices also had better performance, as measured by a range of indicators of clinical quality, financial performance, waiting times, ratings from the government regulator of hospital quality and staff satisfaction. In addition, they found that hospitals in less concentrated markets had better management practices than those located in more concentrated markets. While their data are cross sectional, Bloom et al. 19 exploit the fact that hospitals in marginal political constituencies in England are less likely to be closed down to identify the causal impact of competition. They therefore argue that lower market concentration leads to higher management quality, which is associated with better outcomes and better financial performance.

These positive views of competition contrast with two earlier studies of the impact of market concentration on clinical quality in the NHS internal market regime of the 1990s. One 20 is a cross-sectional analysis, so is subject to the same identification problem as cross-sectional USA studies. The other 17 uses the same identification strategy as Gaynor et al. 16 and Cooper et al. 15 to examine the impact of the internal market on UK hospitals. In contrast to the more recent research, they found that market concentration was associated with lower clinical quality, again measured by case-mix adjusted deaths following emergency heart attack admissions. But they also found that waiting times fell more in less concentrated markets than in less.

What might explain these different conclusions as to the impact of potential competition on quality in the NHS? The answer would seem to lie in the institutional structure of the market and, in particular, in differences in the regulation of price, the amount of information available to buyers of health care and possibly the concerns of the buyers of health care. In the Labour reforms from 2006, prices are set externally by the DRG tariff. Quality information, while inevitably partial, has been available on an increasing basis since the late 1990s and the early 2000s, when the Department of Health started making public information on the performance of individual hospital trusts. Waiting times, which had been a major source of concern throughout the 1990s and into the first half of the 2000s had been brought down dramatically over this period, in part due to strict waiting times targets. 21 Buyers of health care were therefore able to focus on health quality, as waiting lists were no longer a major concern and prices could not be negotiated with the sellers of care. In the early and mid-1990s by contrast, waiting times were extremely long and of concern to the buyers of health care, public information on quality was virtually non-existent, and prices were negotiable. It is therefore not surprising that the outcome of negotiations between buyers and sellers of health care was to focus on waiting times at the expense of less easily observed health care quality. 22

Challenges for the next wave of English NHS reforms

The Coalition government at the time of writing (2011) is keen to increase the pace of market-oriented reform in the English NHS. To this end, as noted in the Introduction, the government wishes to give the commissioning role to CCGs and to encourage wider plurality on the provision side, where appropriate. Given this, it is helpful to speculate about what we can learn from the literature and the factors that may be at work in the USA and how those may translate to England.

Evidence from the USA clearly shows that competition leads to substantially lower prices.5,23,24 The evidence on the impact of competition on quality when prices are market-determined is less clear-cut. But in the USA, prices are negotiated by price-sensitive insurers. These insurers have strong incentives to obtain lower prices, since their customers, typically employers, are responsive to price differences. Insurers, however, do not engage in sole-source contracting. They contract with sets, or networks, of hospitals. Patients are thus free to exercise choice of hospital within a network (which is often quite broad). Hospitals thus have an incentive to compete on quality in order to attract patients within a network. As a consequence, there are both price and quality incentives in play.

In the English context, this suggests a few things. First, if purchasers do not benefit from lower prices, then their financial incentives will be weak and they will not drive price competition. The arrangements for who will purchase are currently not yet certain. But if they are to be CCGs, the fact that GPs already keep surpluses from their practices and are private contractors means that CCGs will presumably be able to keep at least some of the surpluses from their purchasing activity. They, therefore, will have financial incentives to seek lower cost providers. Lower cost provision may of course come in the form of provision by GPs themselves, where there is an alternative to hospital care. This, of course, is one of the arguments for CCGs – that they will bear the financial cost of referral and, therefore, will be more likely not to refer to hospital when it is not necessary.

Second, competition for patients would also provide an incentive for GPs to be price-sensitive and, to the extent that patients can observe quality, be sensitive also to quality in their choice of health care provider. It is not yet clear the extent to which CCGs will compete for patients. At present, competition for patients between GP practices is still limited. It is flagged that this will be increased. But if all GPs in a local area are in the same CCGs, then even if there is competition between practices for patients there will not be competition between CCGs for patients. This may need regulatory oversight and perhaps encouragement of entry into the commissioner market by the Department of Health.

Third, patients will still need to have hospital (or other care provider) choice as CCGs may have an incentive to direct patients to lower cost as opposed to higher quality providers, though it is hoped that regulation will prevent this. Patients will also have to be well-informed in order to direct their own choices. This may be difficult if GPs are both the ones providing advice, providing primary care, referring patients and profiting from choice of hospital. In this context it may be that the selection of CCGs as price negotiators is unfortunate. It might be better to divorce the price negotiation and the hospital referral choice function in order to minimize the conflict between profits from lower prices and selecting the best quality hospital (or other care) for patients.

Finally, the behaviour of CCGs is to be regulated by the government. It is important that this regulatory role does not stifle initiative among commissioners. Brereton and Gubb 25 argue that micro-management of the market and, in particular, of the purchasers has been excessive and has limited the extent of productivity gains from competition. If high levels of central control continue, it may be the case that quality gains from any competition will remain rather small.