Abstract

An Asian-style futures is settled by an Asian-style settlement procedure, more specifically, it is settled against the arithmetic average of the underlying asset prices taken over the settlement period. In this paper, we propose a practical trading strategy based on an integer programming technique to exploit the mispricing opportunity of Asian-style index futures over the settlement period using a proxy of the underlying asset. The integer program can detect mispricing, construct an arbitrage portfolio by using the proxy and dynamically maintain the arbitrage portfolio. Hang Seng Index Futures (HSI Futures) of the Hong Kong market is used to test the trading strategy. The historical data of HSI Futures shows that there is a positive relationship between the magnitude of mispricing and the time to maturity over the settlement period. Moreover, our empirical findings show positive profitability of the trading strategy.

Keywords

Introduction

An Asian-style futures is a futures contract with its settlement price calculated using an Asian-style settlement procedure, which is the arithmetic average of the underlying asset prices taken over the settlement period, typically the expiration day. Table 1 lists some exchanges and their futures that use an Asian-style settlement procedure.

Exchanges and their Asian-style settlement procedure

Exchanges and their Asian-style settlement procedure

In this paper, we propose a practical trading strategy to perform Asian-style index futures arbitrage over the settlement period using a proxy of the underlying asset. Arbitrage related activities on the expiration day could result in unusual price movementsand trading volumes of the underlying asset, which is generally referred to expiration day effect. Here we will report some of the existing studies on the expiration day effect in different markets from around the globe. In the U.S. market, Stoll and Whaley (1987) indicate abnormally high trading volumes concentrating within the “triple witching hour” and a significantly higher volatility among index constituent stocks on the expiration day as derivative contracts are settled against the closing price of the underlying index. In June 1987, the settlement price is changed to be the opening index of the day after the expiration day. Herbst and Maberly (1990) find that the change of settlement price shifts the high volatility effect to the opening. Chamberlain et al. (1989) study the Toronto market and they report abnormally large trading volumes and volatility on expiration days and price reversals following the expiration of derivative contracts. In the Swedish market, Alkebäck and Hagelin (2004) find significantly higher trading volumes of OMX Index constituent stocks on expiration days than on other days, where OMX Index futures are settled against the volume-weighted average index on the expiration day. Vipul (2005) reports that in the Indian market, prices of the underlying stocks are suppressed on the day before expiration of options and futures but bounce back on the day after expiration. In the Hong Kong market, Chow et al. (2003) show that there is a higher volatility and lower average five-minute returns of Hang Seng Index on expiration days than on other days. Fung and Yung (2009) find trading intensifies in terms of both volume and frequency concentrating around the quotation time marks, and order imbalance patterns on some expiration days. They also provide evidences indicating that arbitrage and direction-related trading activities are concentrated in large-capitalization stocks.

To take advantage of a mispricing opportunity, arbitrageurs need to take an offsetting arbitrage position in order to replicate price movements of the underlying asset. In a risk-free manner, one may employ a whole basket of constituent stocks, along with their corresponding weights. However, the profitability of such arbitrage strategy has been questionable in the sense that it is difficult to trade the exact weights and trade every constituent stock. Hence arbitrageurs usually use a sub-basket of the constituent stocks. Previous works have examined using constituent stocks to construct an arbitrage portfolio and their findings differ. Modest and Sundarsesan (1983) find that with the existence of transaction cost, the price of index futures fluctuates within a band around its fair value without occurring any mispricing opportunity even for the most favorably situatedarbitrageur. On the other hand, Yadav and Pope (1994) report magnitudes of mispricing often exceed the estimated transaction costs. Moreover, researchers report similar results under short sale constraints. Chung (1991), Chan and Chung (1993) and Fung and Draper (1999) find that short sale restrictions in cash markets hinder arbitrageurs from exploiting index futures underpricing and thus result in slower price adjustments. After the introduction of ETF, Richie et al. (2008) show that persistent mispricing opportunities do exist when using the SPDR ETF as a proxy for the S&P 500 index. They also find that insufficient volume sizes are the key limit of performing arbitrage.

While there are studies reporting the expiration day effect as well as examining index futures mispricing, this paper extends previous works by proposing a practical trading strategy for Asian-style futures arbitrage using a proxy of the underlying asset. Since the delta of an Asian-style futures decreases at each time mark where the price quotation is taken, arbitrageurs need to unwind the offsetting position at each time mark in order to track the decreasing delta. Our strategy can perform the unwinding automatically. In particular, the trading strategy is an integer program which can perform mispricing detection, arbitrage portfolio construction and dynamic maintenance of the arbitrage portfolio. Hang Seng Index Futures (HSI Futures) in the Hong Kong market will be used to test the profitability and effectiveness of the trading strategy. First back month contracts will be used as the proxy in the test.

The rest of the paper is organized as follows. In Section 2, we derive the fair value of an Asian-style futures during the settlement period. Section 3 introduces a practical trading strategy. Section 4 discusses factors that could erode the profitability of an arbitrage opportunity and suggests a solution. Section 5 summarizes the process of using the trading strategy. Section 6 describes the data of HSI Futures used for back-testing. In Section 7, we analyze the patterns of mispricing of the HSI Futures on the expiration day. Section 8 shows the empirical results of applying our trading strategy to perform Hang Seng Index Futures arbitrage. Section 9 concludes our findings.

The fair value of a plain vanilla futures contract is given by the current underlying asset price multiplying the interest rate and the dividend lost. On the other hand, an Asian-style futures contract is settled against the arithmetic average of the underlying asset price quotations taken over the settlement period. Due to the Asian-style settlement procedure, the fair value of the Asian-style futures contract during the settlement period is different from the plain vanilla futures contract.

Taking partial differentiation on both sides of (1) with respect to S

t

, one obtains the delta of the Asian-style futures at time t:

In actual circumstances, a futures contract exhibits no arbitrage opportunity if the following condition holds:

If the lower boundary of (3) is violated (i.e.

In this section we introduce a practical trading strategy which is an integer program to exploit the mispricing opportunity using a proxy of the underlying asset. In general, this trading strategy can be applied to any Asian-style futures arbitrage during the settlement period. The integer program can detect mispricing, construct an arbitrage portfolio and dynamically maintain the arbitrage portfolio.

Integer Program

At time t on the expiration day, where t

n

≤ t < t

n+1, the integer program is formulated as:

The optimal solution of the integer program gives us an initial position on the futures contract and the proxy (

The objective function of the integer program (4a) is used to detect mispricing and maximize the payoff once a mispricing occurs. Proposition 1 shows that the integer program will not generate a buy singal and a sell signal of the futures contracts at the same time.

Moreover, when (3) is violated, i.e.

Explanation of the Constraints

Firstly for (4b) and (4c), the middle expressions are the delta of the arbitrage portfolio at time t and the future time marks t i (for i = n + 1, n + 2, . . . , N) respectively and their magnitudes are bounded by ∊ t i . Hence (4b) and (4c) are used to restrict the delta of the arbitrage portfolio under the endurance level of the investor. Since we use the proxy instead of the underlying asset to perform arbitrage, we need to keep the magnitudes of the delta below the endurance level. Note that the delta of the index futures contract will not change between two consecutive time marks, so it is sufficient to restrict the delta at each timemark.

Secondly, (4d) is used to keep the trading quantities of the futures contract from exceeding the quantities that the market can offer.

Thirdly, (4e) is used to keep the position on the futures from exceeding a capital control set by the investor. Since the position on the futures and the delta of the arbitrage portfolio are bounded, the position on the proxy is bounded as well. Hence by setting the capital control on the futures contracts, the position of both futures and proxy are restricted from exceeding the investor’s capital.

Maintaining the Arbitrage Portfolio

In (2) one can see that the delta of the Asian-style futures is decreasing during the settlement period, so we need to keep unwinding the position on the proxy in order to maintain the arbitrage portfolio. In fact the integer program can also be used to maintain the arbitrage portfolio. The output K 2,t i for i = n + 1, n + 2, . . . , N gives the investor the position of the proxy they should hold in different time. In other words, the value of (K 2,t i - K 2,ti-1) tells the investor how much proxy they should unwind at future time marks t i for i = n + 1, n + 2, . . . , N.

Moreover, if one already has an arbitrage portfolio and the integer program spots a mispricing, then a new arbitrage portfolio will be constructed. The integer program will output a set of new K 2,t’s and the old K 2,t’s will be updated. So the investor can maintain the new arbitrage portfolio according to the new output of the integer program.

Non-profitable Mispricing Opportunity and Solution

In the last section, we introduce the trading strategy to exploit mispricing opportunities. However, we have not considered some factors that can erode the profitability.

In Section 4.1 we address two factors when implementing the strategy in practice, namely that the arbitrage portfolio is not delta neutral and the delta of the proxy may deviate after the arbitrage portfolio is set up. Both of the factors may erode the profitability or even cause a loss. In Section 4.2, we introduce an approach to filter out the non-profitable mispricing opportunities. In particular, the case of using next expiring futures contracts as a proxy to perform arbitrage of expiring futures contracts is used as an illustration.

Factors Eroding the Profitability

The optimal value of the integer program is equal to the amount an arbitrageur can receive using the underlying asset to perform arbitrage. However this strategy employs the proxy to construct the portfolio, the actual payoff the investor can receive is differ from the optimal value of the integer program, e.g. in some cases the optimal value is positive but the actual payoff is negative. In view of this, Theorem 2 gives a condition on the optimal value such that the trading strategy is guaranteed to be profitable. For simplicity of notation, we only show the case of t = t n , while the general case t n ≤ t < t n+1 follows easily.

When δ

t

< 0, an arbitrageur gains more than the optimal value of the integer program. Conversely, if δ

t

> 0, the arbitrageur gains less than the optimal value. Moreover if δ

t

> Q

t

> 0, the optimal value is positive but the mispricing opportunity is not profitable. For the case of using the first back month futures as the proxy to perform arbitrage on the front month futures, (5) suggests two factors causing the actual payoff to be different from the optimal value: firstly, the arbitrage portfolio is not delta neutral; secondly, the “delta” (

For the first factor, as the arbitrage portfolio is not delta neutral, any price movement of the underlying asset causes the value of the arbitrage portfolio to change. If the price of the underlying asset moves in an unfavorable direction, the value of the arbitrage portfolio will drop. For the second factor, the fair value of a first back month futures contract is given by the current price of the underlying asset multiplying the interest rate and dividend lose. Hence theoretically the delta of the first back month futures contract is given by the price of the first back month contract divided by the price of the underlying asset. In reality the price of the futures contract may include noise, hence we call the ratio

When Q t > δ t , Theorem 2 guarantees that the trading strategy is profitable. However, one needs to know future prices S t i , i = n + 1, n + 2, . . . , N, in order to calculate the threshold δ t and it is impossible to know them in real practice. In view of that, we conservatively estimate the threshold δ t and require the optimal value of the integer program to be greater than an estimated threshold in order to filter out non-profitable mispricing opportunities.

In this paper, we conservatively estimate the threshold δ

t

by

We first collect the “delta” of the next expiring futures at each passed time mark to form a set of data

Moreover, we consider a prediction interval of α

t

at a confidence level θ which is to be chosen by the investor in practice. The prediction interval is given by

In this section we summarize the process on how to implement our strategy by using the proxy. It is given as pseudocode in Algorithm 1.

Process of implementing the strategy

Process of implementing the strategy

In this paper, Hang Seng Index Futures (HSI Futures) of the Hong Kong market will be used to examine mispricing patterns on the expiration day and test our trading strategy. The HSI Futures was introduced in May, 1986. Its underlying asset is Hang Seng Index (HSI), a capitalization-weighted index consisting of 50 major stocks of the Hong Kong market. The futures contracts are traded in Hong Kong Exchanges and Clearing Limited, and expire on the day before the last business day of every month. It has a contract multiplier of 50 Hong Kong dollars per index point. An Asian-style settlement procedure is used to calculate the settlement price of the HSI Futures, which is the arithmetic average of the HSI quotations taken every five minutes on the expiration day, rounding down to the nearest whole number. The majority of trading volumes of the HSI Futurescontracts are concentrated in front month contracts and first back month contracts.

Our data consists of every two seconds quotations of the HSI and tick-by-tick bid/ask quote records of the HSI Futures on the expiration days in the period from Jan 2013 through June 2015, which provides in total 30 expiration days to study. More specifically, it is a historical intraday data recording the price of the HSI and the HSI Futures on the expiration days from 9:35 a.m. (first HSI quotation is taken) to 4:00 p.m. (market closing).

Pattern of Mispricing of HSI Futures

In this section we examine patterns of mispricing of the Hang Seng Index Futures (HSI Futures) on the expiration days. In Sections 7.1 and 7.2, we examine the frequency and the magnitude of mispricing of the HSI Futures on the expiration days respectively.

Frequency of Mispricing

Transaction cost is an important factor to be considered before performing arbitrage, as high transaction costs may completely erode the profitability. In view of this, we examine the frequency of mispricing at different levels of transaction costs. Table 2 reports the frequency of mispricing signals at four levels of transaction costs: 0, 1 index point, 0.0077% and 0.1077% for a total of 9, 750 observations. In particular, these 4 levels correspond to no transaction cost, brokerage’s rates of transaction costs for trading index futures, ETFs and stocks in the Hong Kong market respectively. It is worth noting that since we consider bid-ask quotes of the index futures instead of trade quotes, it is possible to generate a neutral signal even with 0 transaction cost (no mispricing occurs when (3) holds). In fact, 18.5% of the observations are identified as no mispricing with 0 transaction cost. Almost 60% and about half of the observations are identified as mispricing when the transaction costs are 1 index point and 0.0077% respectively. When transaction costs increase to the level of trading stocks, the proportion of mispricing drastically drops. Only 0.2% of the observations are recorded as mispricing at 0.1077% transaction costs, implying arbitrage opportunities using constitute stocks are scarce even for brokers. This observation is similar to the finding of Modest and Sundarsesan (1983) in the U.S. market, where the actual futures prices fluctuate within a bounded interval without showing any arbitrage opportunity when trading index constituentstocks.

Frequency of mispricing

Frequency of mispricing

Although there is only a few mispricing opportunities at the rate of the transaction costs of trading index constituent stocks, the opportunities with trading index futures and ETFs are abundant due to relatively low transaction costs. This shows the potential of ETFs and the first back month futures being used as a proxy to construct the arbitrage portfolio.

No significant difference between the frequency of underpricing and overpricing is observed at 0, 1 index point and 0.0077% rate of transaction costs. The binomial test however indicates that the frequency of underpricing is significantly greater than the frequency of overpricing at 0.1077% rate of transaction costs with a p-value of 0.0013. This shows consistency with current “Regulated Short Selling” in the Hong Kong market, where short sale of stocks could not be made below the current best askprice.

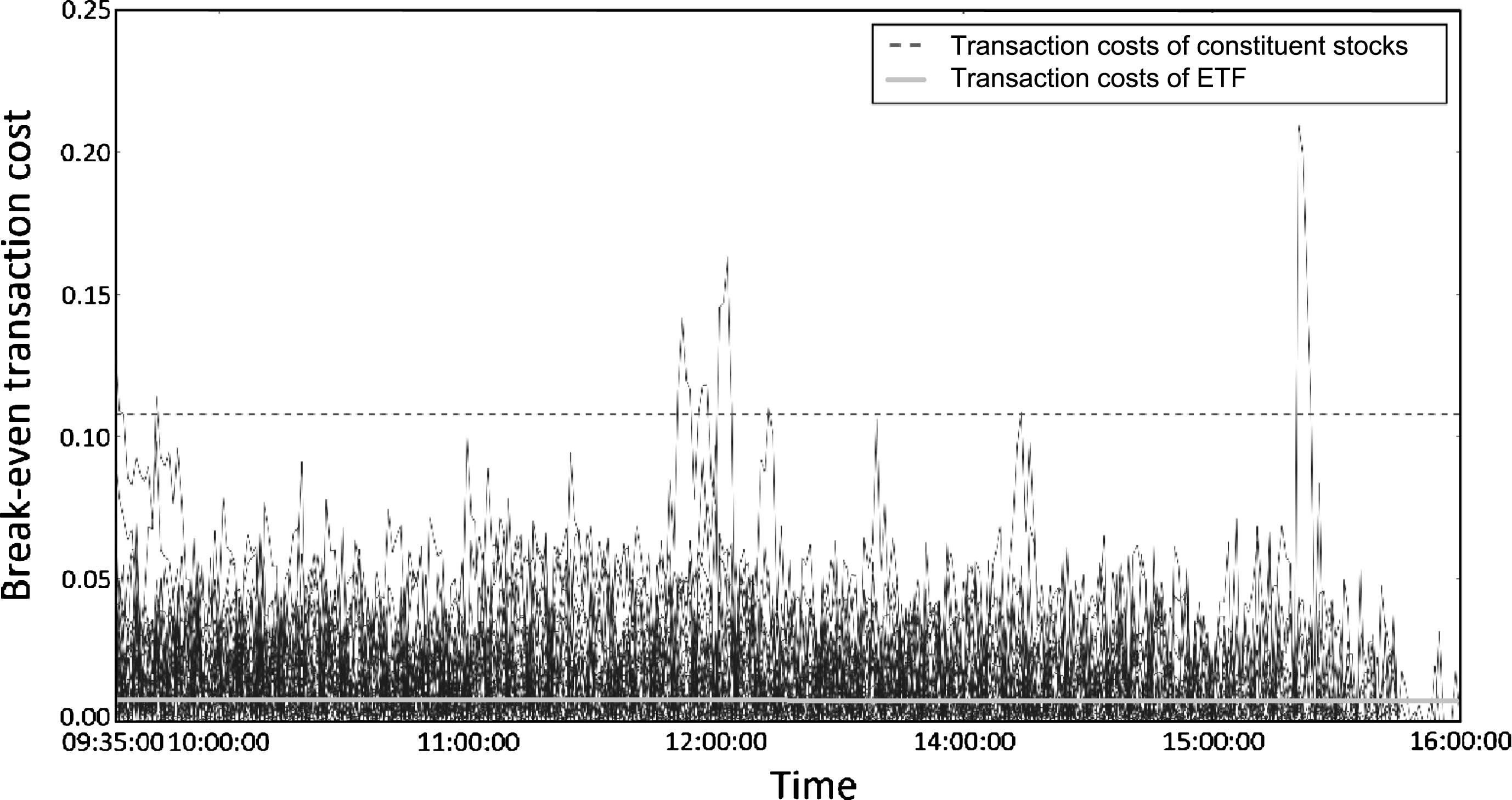

Figure 1 shows the rate of break-even transaction costs versus time. The upper dashed and lower solid horizontal lines represent the rate of transaction costs of trading stocks and ETFs for brokerage firm respectively. Each curve represents the rate of break-even transaction costs at different time on one expiration day and there are a total of 30 curves in the figure to represent 30 expiration days. We note that no substantial increasing or decreasing trend of the break-even transaction costs is observed over the whole period in the expiration days.

Break-even transaction costs over time.

Figure 2 shows the magnitude of mispricing at 0 transaction cost versus time for the 30 expiration days. Each curve represents magnitude of mispricing over time on one expiration day and there are 30 curves to represent 30 expiration days. A trend of decreasing magnitudes of mispricing with closer time to maturity can be observed. In the former-part of the expiration days the magnitudes of mispricing are relatively greater, some unusually large mispricings are also spotted. In the latter-part of the expiration days, the mispricings are converging to zero and they eventually become zero at the market close. This observation is consistent with findings of Mackinlay and Ramaswamy (1988) and Yadav and Pope (1994), implying the existence of factors influenced by time to expiration. Possible factors include risk of offsetting the index futures with only a proxy of a whole basket of constituent stocks, which is greater with longer time to maturity. Since price movements of the underlying index is not perfectly duplicated, arbitrageurs may bear potential loss at each five-minute mark when unwinding the offset position so they have to look for a greater margin of deviation with longer time to maturity. Another factor could be transaction costs involved in trading proxy. Because of the decreasing delta of the futures contract, a smaller amount of proxy is needed to construct an arbitrage portfolio with closer time to maturity. Hence fewer transaction costs are needed, arbitrageurs can then profit from a smaller size of mispricing with closer time to maturity.

Magnitude of mispricing over time.

As we discussed in Section 7.1, the arbitrage opportunities on the expiration days are scarce using constituent stocks due to costly transaction costs of stock trading in the Hong Kong market, there are, however other assets featuring low transaction costs available in the market, e.g. ETFs and the first back month futures contract. Moreover, there are a decent amount of mispricing using these assets. This shows a potential of using these assets as a proxy to perform arbitrage.

In this section, we report the empirical results of applying our trading strategy discussed in Section 4 to back-test the historical data mentioned in Section 6, i.e. intraday data of HSI Futures on the expiration days from January 2013 through June 2015. In particular, we look for arbitrage opportunities of the front month contracts and use the first back month contracts as the proxy. Tables 3 to 6 summarize the profit and the number of trades on each expiration day by applying our trading strategy with 90% , 95% , 99% and 99.9% confidence level respectively where the past η = 250 days historical daily HSI price data is used to calculate the VaR. More specifically, a 90% confidence level means that we take both θ and ξ equal to 90% in calculating

Empirical result with 90% confidence level

Empirical result with 90% confidence level

Empirical result with 95% confidence level

Empirical result with 99% confidence level

Empirical result with 99.9% confidence level

For the parameters in the integer program, there are N = 66 time marks for the HSI Futures on the expiration day. We consider an arbitrage portfolio consisting of 66 front month index futures contracts as 1 set of arbitrage portfolio. Also we set the capital control C = 66 × 2 =132, i.e. one can at most possess 2 sets of arbitrage portfolio at the same time. In addition, we put one more restriction: we can only set up one set of arbitrage portfolio at any one time. We set the endurance level ∊

t

= 0.05 at any time t for the delta of the arbitrage portfolio. We set up an arbitrage portfolio if the optimal value of the integer program Q

t

is positive and greater than the estimated threshold

By using our trading strategy, one can generate positive total profit among all 4 confidence levels. The total profit with 90% , 95% , 99% and 99.9% confidence levels are 27647, 26265, 10430 and 51 index points respectively. This shows a risk premiumrelationship between the total return and the confidence level — the more risk you are willing to bear, the more return you can generate. Moreover, if one increases the confidence level, the estimation of the threshold will increase. Hence more mispricing opportunities will be filtered out and there are less number of trades. When the confidence level increases to 99% , all trades with negative return are filtered out and all trades can yield a positive return. Suppose the deposit required for trading each index futures contract is 3000 index points (a conservative estimation of deposit for the Hong Kong market), one needs 792, 000 index points as an initial capital since the capital control for front month contracts is C = 66 × 2 =132 in the integer program and we need the same amount of first back month contracts. For such initial capital and for the case of 90%, 95%, 99% and 99.9% confidence level, our strategy can generate an average daily return of 0.12%, 0.11%, 0.04% and 0.0002%respectively.

The trading strategy introduced in this paper is simple to implement—it is based on an integer programming technique and there are many libraries available for integer programming. Moreover our approach requires only little market information: daily data of the underlying index and intraday data of first back month futures and underlying index on the expiration day. Both data are easily accessible and even "small investors" who lack of market information can use our strategy.

In this paper, we propose a practical trading strategy for Asian-style futures arbitrage. In particular, our trading strategy is an integer program which uses a proxy to construct the arbitrage portfolio. Since the arbitrage portfolio is not delta neutral and the delta of the proxy may vary after the portfolio is set up, we introduce a threshold to filter out somenon-profitable mispricing opportunities. HSI Futures of the Hong Kong market is used to test our trading strategy. We first examine the pattern of mispricing of the HSI Futures on the expiration days. We show that there is a trend of decreasing magnitude of mispricing when time approaches maturity. Moreover, we find that there is a decent amount of frequency of mispricing, showing some potential arbitrage opportunities. Empirical results show that one can generate trades that are profitable using a conservative estimation of the threshold. Our strategy is general enough not only to be applied to the HSI Futures, but also to any futures with an Asian-style settlement procedure.