Abstract

The pattern of dependence between liquidity, durations (orders and trades) and bid-ask spreads in a limit order market are examined in high resolution invoking copulas and graph theory. Using intraday data from a sample of NASDAQ 100 stocks and an experimental design, we study the information pathways in markets in the presence of algorithmic traders. Our results confirm that multivariate analysis is more appropriate to investigate these information pathways. We observe that the strength and nature of the dependence between variables vary through the trading day. We confirm the existence of stylised aspects of algorithmic trading, such as tail dependence in trade durations, a balance between buy and sell side in order durations, liquidity and bid-ask spreads, and the bid-ask spread and liquidity trade-off in the dependence structure.

Keywords

Introduction

Markets trading equity assets have a predominance of algorithmic traders, who prefer using high-speed trading technology. Algorithms trade with low latency, competing and coordinating with other traders in the market. It is important to investigate this activity in high resolution (closer to the natural scale in which the activity occurs). The liquidity conditions and trade and order durations in the market are the attributes of such activity. Intertrade durations summarize the order level activity in the market. Trade data from financial markets presents stylised aspects such as intraday seasonality and clustering. Hence, it offers microstructure researchers ample scope to investigate the underlying economic implications.

The popular method used in market microstructure to carry out such empirical studies is to choose a single variable (price innovations, trade duration or volume) and investigate how it correlates to lagged versions. However, the unit of information in high-frequency limit order markets has moved from trades to orders (O’Hara, 2015), while there is a dearth of studies on interorder or intertrade periods in the microstructure literature.

The motivation for this paper is to extend the microstructure toolkit to intertrade periods. It does so by investigating intertrade periods using high-resolution analysis. High-resolution analysis in market microstructure is an emerging area facilitated by the availability of such data from exchanges. Brogaard et al. (2019) and Pani (2021a) are examples of such research. We report an experimental investigation that uses a public dataset accessible from NASDAQ. The key intuition is that, in high resolution, information flow can be described as a multivariate function of microstructure variables due to the absence of a supply-demand equilibrium. Such an equilibrium is a work in progress constrained by time and communication. The paper uses a queue-theoretic framework to stitch together the input and output parameters of the trading system. Further, it employs pair copula construction to address the multivariate framework.

This study empirically investigates the dependence between trade durations, order durations, liquidity and bid-ask spread (henceforth called spread) of a sample of constituent stocks from the NASDAQ 100 index. We characterise the bivariate dependence relationship and the time-varying nature of the dependence among these variables. The results show that trade durations are the strongest relationships, but there is a tail dependence between bid side and ask side trade durations. Information flow to ask side trade durations is usually mediated through the bid side trade durations.

Order durations are seen to be informationally important, but generally, the dependence is weaker than trade durations. Tail dependence exists in 50% of the dependence pairs. The nature and strength of the dependence is an aspect of the microstructure of the traded stock. Order durations interact with trade durations, liquidity and spread and account for nearly a third of all the dependence pairs. The strength of the dependence relationship between order durations and liquidity is similar for variables on the same side (buy-buy / sell-sell) and the opposite side (buy-sell). Such a balance shows coordination, communication and feedback in markets with the presence of algorithmic traders.

Although the count of spread in bivariate pairs is relatively lower, we find that it is an important variable. The spread is not an active variable in all periods. The relative share is high in the first half of the trading day. There also exists a cross-sectional variation in the relative strength of spread. The change in the relative share of spread comes at the cost of limit order book liquidity. This finding confirms stylised aspects documented in the literature of algorithmic traders shifting from liquidity demand to liquidity supply depending on the spread. Our finding is significant because it is based on recent and a non proprietary dataset.

Our work contributes to the literature in the following ways. First, we show that microstructure research could investigate pathways of information flow by using dependence. In high resolution, we find that a multivariate model to study information is appropriate. Second, we propose a method using copula and graph theory. Using a sample of constituent stocks from the NASDAQ 100, we explore this dependence using pair copula construction and characterise it. Third, we find evidence in our sample of stocks that the intraday relationship between microstructure variables - trade durations, order durations, liquidity and spread is time-varying. Fourth, inspite of using a non-proprietary dataset, our method presents observations that have previously been documented as stylised aspects of limit order markets in the presence of algorithmic traders. Fifth, a high resolution view of the relationship between trade durations, order durations, liquidity and spread in a limit order market is analytically described. Through these we contribute to the growing literature in high resolution studies.

The rest of the paper is structured as follows. Section 2 reviews recent literature as well as early microstructure models related to durations, liquidity and spread. Section 3 explains the model and variables, followed by an introduction to the data for our empirical examination in Section 4. The results and discussions follow in Section 5. Concluding remarks are presented in section 6.

Review of literature

Research in the last few years has added to an understanding of intertrade duration in terms of the impact of liquidity, the role of orders, trades and spread.

Limit order markets

Electronic limit order markets represent a market for immediacy where limit order submitters offer terms of trade to potential market orders. Therefore, limit order submitters must continuously monitor the market for changing conditions or risk being arbitraged by traders who arrive subsequent to them but closer to the trade.

Limit orders are a source of market liquidity (Biais et al. (2015), Pani (2021a)), and price discovery (Brogaard et al. (2019)). Technological advancement has aided this role of limit orders by lowering the costs to monitor the market and cancel or modify limit orders (Hasbrouck and Saar (2013)). The competitive conditions in fragmented markets has encouraged exchanges to offer innovative maker-taker pricing, providing further incentives to traders to place limit orders.

Durations, Liquidity, and Spreads

In limit order markets, determining who demands liquidity and who supplies it is a non-trivial issue. Market makers take positions on both sides of the market, adjusting their spread on either side depending on their inventory, adverse selection risk and other market insights.

Algorithmic Traders (AT)

Hendershott and Riordan (2013) after examining algorithmic traders (ATs) in the Deutsche Boerse in Jan 2008, conclude that ATs consume liquidity when it is cheap (i.e., spread is narrow) and supply liquidity when it is expensive. They explain how technology that lowers monitoring costs helps more activity from ATs towards liquidity supply and demand. ATs break up large orders into child trades that execute when liquidity is high. Therefore the search process does not reveal the total trading interest.

Hasbrouck and Saar (2013) describe how algorithms are used to trade in both agency and proprietary contexts. Institutional investors utilize ATs to trade large quantities gradually over several days to minimize market impact. ATs initiate smaller trades, cluster their trades together and attempt to trade rapidly when bid-ask spreads are small.

Biais et al. (2017), using a proprietary dataset, finds that high frequency traders (traders having access to “fast trading” technology) provide liquidity by leaving limit orders in the book. They posit that market frictions can prevent final sellers from locating final buyers, thus necessitating market making services from intermediaries. Such intermediaries that provide liquidity in fragmented markets need to have the best network linkages and search ability. High frequency trading technology enhances this capability. Delays can occur as all potential buyers and sellers may not be monitoring the market permanently.

Cespa and Vives (2017) note that during a flash crash, illiquidity brings forth more illiquidity. In contrast, during normal market conditions, illiquidity produces a self-stabilizing effect. They note two new kinds of frictions in markets dominated by automated trading - participation friction (liquidity suppliers are not continuously present in the market) and informational friction (access to timely market information).

Contrary to previously prevalent microstructure models, relatively recent literature suggests that informed traders can place passive limit orders to strategically take positions (Collin-Dufresne and Fos (2015), Easley et al. (2016)). Hence, Onur et al. (2017) define market-wide liquidity demand based on information present in trader positions. Trader positions down the book are seen as demanding liquidity but not immediacy. These traders thus demand a favourable price expecting fulfillment by traders who demand immediacy. As a result, the net liquidity demand in the market, measured by the skewness of intraday position changes across market participants, impacts prices. Further, passive positioning incorporates information into prices and reduces market liquidity. This is the premium that immediacy demanders need to pay when they trade (Grossman and Miller (1988)).

Van Kervel et al. (2020) investigates the intuition that institutional investors who need to trade larger amounts at lower costs have an incentive to find natural counterparties. They show theoretically that order splitting allows institutional investors to detect each other right s trading intentions. Such investors can then coordinate their trading in real-time. Investors detect counterparties in real-time and adjust their trading rates accordingly.

High frequency Traders

In the last decade, a large volume of research has focussed on a special class of algorithmic traders called high frequency traders (HFT). Algorithmic traders (AT) are understood to narrow bid-ask spreads (Jovanovic and Menkveld (2011); Malinova et al. (2013)). They change their role between supply and demand of liquidity depending on whether spread is wide or narrow (Carrion (2013)), thus playing a market-making role (Menkveld (2013)) on one side of the market. Subrahmanyam and Zheng (2016) find that limit orders from HFT are informed contrary to traditional understanding, and compute liquidity by measuring the slope of the limit order book (LOB).

Since high frequency traders (HFT) have replaced traditional market makers, they may operate on either side of the market. They choose if they need to hold inventory. Kirilenko et al. (2017) report that they take aggressive positions close to half the time but do not take large positions. Lehalle and Mounjid (2017) compute the order book imbalance using the quantities at best bid and best ask. They note that for stocks with large ticks, this may be sufficient, but for assets with small ticks taking more than one tick increases the predictive power of the imbalance indicator.

Studies without a focus on trader type

Cont and De Larrard (2012) employ a queue theoretic approach to analyse the duration and other quantities of CITIgroup stock dated June26, 2008. Sarkar and Schwartz (2009) measure the correlation between the number of buyer and seller initiated trades to define if the market is two sided or one sided. They find that this measure can explain bid-ask spreads. They also find trades with asymmetric information one-sided. Rosu (2009) model predicts smaller trading activity to generate larger spreads. However, if there are a higher percentage of informed traders, it generates smaller spreads.

Grammig et al. (2011) revisit the problem of duration and information content of trades. They find that as trade intensity increases, the information content of trades tends to decrease. They also find that the adverse selection component of the spread is considerably smaller for trades after short durations. Their explanation is as follows: when spreads are small, and depth at the best quotes is high, the probability of execution of a limit order decreases. Consequently, limit orders become less advantageous. Impatient traders will thus switch to market orders. This crowding out of limit orders by market orders results in an increased trading frequency and shorter intertrade durations.

Gould and Bonart (2016) investigate the bid/ask queue imbalance as a predictor of the direction of mid-price movement. They find the variables to be related.

Methods: Univariate-static to dynamic to multivariate

Hasbrouck (1991) vector autoregressive framework remained the key method for a long period. The method involves investigating how the variable is correlated to its lagged versions. Usually, one variable is investigated at a time. The method adopted in our study looks at the contemporaneous cross-sectional relationship among variables.

Engle and Russell (1998) introduced the autoregressive conditional duration (ACD) model to present a duration analysis in a dynamic framework. Financial market events, such as trades and quote changes, occur in clusters and ACD and ARCH models attempt to study them. Bauwens and Giot (2000) introduced a logarithmic version of the ACD model, implying a nonlinear relation between the duration and its lags.

Dufour and Engle (2000) extend Hasbrouck (1991) vector autoregressive framework to account for time varying transaction intensity when measuring the information content of trades. They find that duration is informative, and higher trading intensity is associated with a higher price impact of trades, a faster price adjustment to new trade related information and a stronger autocorrelation of trades.

The majority of studies to date have predominantly used trades and mid quotes for the analysis. Empirical observations in our experiments and others in limit order books show that trades walk up the book with regularity. Hence, the earlier approaches would ignore a lot of information content of orders. Chakravarty and Pani (2021) introduces a new data handling paradigm to deal with data from limit order markets. This data paradigm can be used to handle data even beyond the best bid and ask to unravel the information content of the limit orders. The following are a few studies that use order book data.

Selected order book investigations

Cenesizoglu and Grass (2018) investigate the differences between bid- and ask-side liquidity in the NYSE limit order book data. Their focus is to observe the changes around the 2008 financial crisis. Their dataset includes millisecond timestamped snapshots of the LOB, including prices and quantities at its first ten levels on the ask and bid sides for stocks traded on the NYSE. A new measure of LOB liquidity called the marginal cost of immediacy (MCI) is computed for both bid and ask side. This measure is defined as the volume-weighted transaction costs (relative to the mid price) of investors instantaneously accepting all ask (bid) offers in the first ten levels of the book, scaled by the total dollar volume they acquire (sells). The paper also uses this to examine asymmetries in order book liquidity. Although the study utilises level II data, its focus is more to explain events in level I, i.e., trades. It attempts to use liquidity measures (liquidity and imbalance) to predict daily returns and monthly returns. In contrast, the focus in the current paper is on the high resolution view.

Hautsch and Huang (2012) analyze order book data of 30 stocks traded at Euronext Amsterdam. The paper models quotes and depth simultaneously and also the trade and order arrival process. Their quote and depth model is estimated by Johansen’ full information maximum likelihood estimator. They show that limit orders have significant market impacts and cause a dynamic rebalancing of the book. The strength and direction of quote and spread responses depend on the aggressiveness (price) and size(quantity) of incoming orders and the state of the book. Cross-sectional variations in the magnitudes of price impacts are well explained by the underlying trading frequency and relative tick size. Passive order placement through limit orders reveals intention and hence incurs significant market impact even if the order is not been executed. Several exchanges offer hidden order types (such as iceberg orders or hidden orders) to participants.

Hall et al. (2003) model the simultaneous buy and sell trade arrival process in a limit order book market using data from Australian Stock Exchange. The variables selected to reflect the state of the order book are market depth, tightness, and the cumulated volume in the bid / ask queue. Changes of the order book induced by limit order arrivals are captured as time varying covariates. The paper finds that the state of the order book has an impact on the buy/sell intensity.

Duration, liquidity, depth and spread - Early microstructure models

How private information is assimilated into the markets has been an important theme for early microstructure models. The idea may be viewed as a model of a semi-strong efficient market. For example, Copeland and Galai (1983), Kyle (1985), Glosten and Milgrom (1985), Diamond and Verrecchia (1987), Admati and Pfleiderer (1988), Easley and O’Hara (1987), Easley and O’Hara (1992).

Trade durations

Easley and O’Hara (1987) brought out the implication that the trade volumes and time between the trades influence prices. Informed traders (traders with private information about the asset’s true value) would wish to trade more frequently and in larger quantities to profit from any valuable information about the asset. Conversely, if prices have incorporated all available information, the frequency of trades and the volumes of trades goes back to their normal values. Trading volumes are only a subset of the liquidity in the market. The intuition in O’Hara (1992) was that a period of no trade also conveys as much information to the market as a period of trades. Hence, one expects autocorrelation in volumes, a correlation between trade durations and volumes and durations affect prices.

According to Admati and Pfleiderer (1988), discretionary liquidity traders choose to trade together and hence we should observe clustering of trading volumes. In the Foster and Viswanathan (1990) model, informed agents choose to trade intensely for fear of losing their advantage with disclosure of public information and market maker’s learning process. Hasbrouck (1991) found that change in prices depended on the trades, the market environment (bid-ask spread) and the current and past prices. A larger trade size and spread imply a larger price revision after the trade. The volume of trade also conveys information. Engle and Russell (1994) find evidence of co-movements among duration, volatility, volume and spread.

Bauwens et al. (2006) analysed stylised facts of inter-trade durations for the tokyo stock exchange. These stylised facts, intra-daily seasonality, clustering, and overdispersion are similar to the NYSE.

Manganelli (2005) confirms Foster and Viswanathan (1990) prediction that in frequently traded stocks, the degree of trade clustering was higher than in less frequently traded stocks. The study considers volumes as a stochastic process and models it using an autoregressive specification. Duration, volume and returns are modelled simultaneously, using a special type of Vector Autoregression to build a system that incorporates causal and feedback effects among these variables. The model is applied to a sample of NYSE stocks.

Liquidity

In general, liquidity refers to whether a stock can be traded without wide price fluctuations. Harris (2003) recognises the four dimensions of liquidity as width, depth, immediacy and resilience. Seppi (1997) relates market liquidity to the temporary or non-informational price input of different sizes of market orders. Dufour and Engle (2000) define liquidity as a market in which trades have a lower impact on prices, and consequently, new trade related information takes longer to be fully incorporated into prices. Short time durations (high trading activity) are related to larger quote revisions and strong positive autocorrelations of trades. When combined with Hasbrouck, it implies that high trading activity is coupled with large spreads, high volume and high price impact of trades. In markets, some liquidity traders may decide to postpone their trading or demand larger spreads and the specialist adjusts prices more rapidly in response to the trader.

When viewed from the perspective of a limit order market, liquidity is related to depth at various levels. At the same time, it is related to the presence and activity of liquidity providers - arbitrageurs and high frequency traders. The accepted understanding in the 80s and 90s was that informed traders trade only on information events, and uninformed traders trade for liquidity reasons. Since the beginning of this century, market design changes have changed the character of the markets decisively. In an electronic limit order book structure, there can be many liquidity providers. Low latency technologies enhance the ability of traders and market makers to monitor changes in market conditions and react rapidly. And regulators have fragmented the market by allowing an asset to be traded in different markets simultaneously.

The demand for immediacy has often been used as a proxy for liquidity demand. When such information was not obvious, classification algorithms were used. Chordia et al. (2002) study the relationship between liquidity and order flow imbalance and market returns.

Various definitions have been used for liquidity in previous studies. For example, volume of shares traded, volume at the best bid or best ask, slope of bids, number of orders on bid or ask side.

Spread and depth

Market depth is also affected by information asymmetry. In Kyle (1985), market depth is proportional to the amount of noise trading but inversely proportional to private information not incorporated in the price. Gromb and Vayanos (2002) show that arbitrageurs able to take positions in different markets can provide liquidity with or without the presence of designated market makers. There seems to be “limits to arbitrage” due to the limited ability to carry inventory. Hence, liquidity shocks have a transient impact on prices. Glosten and Milgrom (1985) and Kyle (1985) show that adverse selection leads market makers to post relatively wider bid-ask spreads.

Huang and Stoll (2001) suggest that the market characteristics of tick size, bid-ask spreads, quote clustering and market depth are endogenous to the market structure. In auction markets, limit orders determine the spreads. Depths are small as the limit orders that narrow spread are small for fear of being “picked off”. ’Depth’ is defined as the quantity bid offered at the inside quote. Pascual and Veredas (2003) using LOB information of Spanish stocks show that the best quotes present the most explanatory power. The book beyond best quotes helps in explaining the aggressiveness of traders. However, information from the book cannot explain the timing of orders.

The Model

In this paper, we incorporate a queue theoretic framework, invoking inventory theory and asymmetric information.

Consider a limit order market. An order is either a bid or an offer (or an action on an existing order). Incoming orders results in asynchronous innovations in bids and offers that we consider as different price series. Some of these orders, designated limit orders, indicate the preferred price for transaction and rest in the order book, till the transaction or order cancellation. Bids (offers) that do not indicate price preference, trade with the immediately available offers (bids). Some messages seek to cancel orders or a modify them.

We consider an order driven market that trades a single asset whose price Y is a random variable. The price is influenced by the order durations (BLAMBDA, ALAMBDA), trade durations (BMU, AMU), liquidity (BIDDEPTH, ASKDEPTH) and the bid-ask spread (BIDASK). The latter is assumed to result from microstructure noise: comprised of inventory costs, order processing costs, information asymmetry, trade asymmetry and impact costs.

Our interest lies in understanding the dependence between these variables, including the buy side (bid) and sell side (ask/offer) stochastic processes. Our focus is not on price discovery but the price formation process. Microstructure models that have looked at information as an endogenous variable usually consider the spread as price proxy.

We investigate the multivariate function in (1)

As in Dufour and Engle (2000), we model the arrival times of quotes (called orders in limit order markets) as random variables that follow a point process. Associated with each quote arrival time, is a vector of observations from the market. This vector of observations includes volume, timestamp and price constitutes an information set. Trade transactions are interspersed with the quote arrivals. All variables of interest can be derived from and are updated with the vector of observations from each quote arrival time.

At time = i, the ith observation vector (x i ) is realized. x i is a vector containing the realized variables. So, x i ∼ f (x i |Ω i ; θ). Ωi denotes the information available at time i. θ is a vector of parameters of interest.

BIDASK: The price innovation in a mark refreshes the limit order book and hence the spread (BIDASK). Before the computation of the spread the order book is sorted on the basis of price and then time. The lowest ask price and the highest bid give the spread.

BIDASK = ASK lowest - BID highest

Unlike quote driven markets where the bids and asks from the dealer arrive synchronously, in order driven markets the spreads may turn out to be negative at times. This issue is more real in the markets dominated by algorithmic traders.

BMU, AMU: The transaction rates (BMU, AMU) is the number of transactions (trades) per unit time. The innovation can be computed as a reciprocal of the duration. These we refer to as realised observations. A transaction is a cross between a resting bid (ask) order and an incoming market ask (bid). The resting order defines the bid or ask marker. If such a distinction is not available in the dataset, a transaction should update both bid side and ask side durations.

Assume there is transaction in which a resting bid order is crossed with an incoming market sell order. This is usually referred to as a bid side trade. Such a transaction will result in an update in the order book. Let, t latest = timestamp of the trade transaction, t bidTrade.last= timestamp of last bidside trade transaction. Define trade duration on bid side as the following:

t bidTrade.duration = t latest - t bidTrade.last

BMU = 1/t bidTrade.duration

In this case there is no update in the AMU. Similarly,

AMU = 1/t askTrade.duration

BLAMBDA, ALAMBDA: The order rates (BLAMBDA, ALAMBDA) similarly is the number of orders (bids/asks) per unit time. These are represented by reciprocal of bid durations or ask durations. Let, t latest = timestamp of the latest bid/ask incoming order, t bid.last= timestamp of last bid. Define bid order duration as:

t bid.duration = t latest - t bid.last

BLAMBDA = 1/t bid.duration

In this case there is no update in the BLAMBDA. Similarly,

ALAMBDA = 1/t ask.duration

BIDDEPTH, ASKDEPTH: Traditionally, orders resting in the order book are considered to be providing liquidity to the market. Orders rest as per the price (buy/sell) embedded. Each price is named a price level. There could be a large number of orders at every price. Transaction priority is given on the basis of time within each price level. Similar to Brogaard et al. (2019) and Pani (2021a) we have considered five price levels each on bid and ask side. While any large order can walk down the order book even deeper than five price levels, we note that in liquid markets orders are usually split into child orders. The liquidity residing in the five price levels is significant.

More important is the question, whether the orders resting at different price levels have equal opportunity to trade in an ongoing auction? The orders residing in the best bid and ask prices have the highest probability to trade in an auction. The chance to get traded decreases as we move away from the best bid and ask in either direction. We arbitrarily choose a linearly decreasing scale to enforce the contribution to liquidity of orders resting in any price level.

We define BIDDEPTH as the cumulative volume demanded in the five best price levels on the bid side, weighted by the distance from the best bid. Without the weighting, this is usually qualified as depth profile. Let n

1to n

5 be the number of orders in the five best price levels in bid side. Here, subscript 1 represents the best bid price level

Where, V ij is the quote volume ordered in the jth bid in the ith price level. w 1 = 1, w 2 = 0.8, w 3 = 0.6, w 4 = 0.4, w 5 = 0.2. We update the BIDDEPTH (liquidity on the bid side) in the book at each incoming event with quote innovations (Orders –bid, ask, or cancel, Trade).

Similarly, we calculate liquidity on the ask side and refer to it as ASKDEPTH.

Orders are considered as the unit of information (O’Hara (2015)). Orders arrive and depart within the intertrade durations. Our purpose is to investigate intertrade durations and events within them at the tick level. The vector of observations associated with these events are timestamped to at least a microsecond and upto nanosecond level resolution in most modern stock exchanges.

Hypotheses

When intertrade durations are viewed in high resolution, there exist information pathways in electronic limit order markets. These pathways can be mapped using the microstructure variables and the dependence between them. The information pathways are dynamic, i.e. a temporal dimension to the dependence between the microstructure variables exists.

In order to investigate the dependence between the variables we use the pair copula construction (Aas et al. (2009)).

Vines and Pair copula construction

Bedford and Cooke (2002) introduced graphical models called Vines or Regular Vines to represent dependent random variables. A regular vine representation although not essential for a pair copula construction comes in handy when dealing with high dimensional distributions. As Bedford and Cooke (2002) explain vines generalize the Markov trees used in modelling high dimensional distributions but differ from both Markov trees and Bayesian belief nets. Vines allow for various forms of conditional dependence. Vines can be used to specify multivariate distributions by specifying various marginal distributions and the ways in which these marginals are to be coupled.

The joint density in (1) can be written as the product of the marginal density. Consider the vector, X = (X 1, X 2, X 3, X 4, X 5, X 6, X 7) of random variables with the joint density function f (x 1, x 2, x 3, x 4, x 5, x 6, x 7). This density can be factorised as:

and this decomposition is unique upto a relabelling of the variables. Thus the insight is that a joint distribution function contains the marginal distribution of individual variables and the dependency structure of those variables. Aas et al. (2009) extend marks Bedford and Cooke (2002) to use copulae to describe the dependency structure with a method now known as ’pair copula construction’.

The following general formula can be used to decompose every term in equation (3) into a product of bivariate pair copula and conditional marginal density. v

j

is an arbitrarily chosen component of the vector v and v

-j is the vector without the component j.

Thus a multivariate density can be factorised and represented as products of pair-copula and several different conditional probability distributions. It is possible to have several different re-parameterisations for any factorisation.

The pair copula construction method that applies the techniques has been implemented in various use cases. See Aas (2016) for a review of the application in finance. The applications include market risk, capital asset pricing, credit risk, operational risk, liquidity risk, systematic risk, portfolio optimisation and option pricing. Our paper adds to literature as it is an attempt to use pair copula construction in market microstructure models using ultra high frequency intraday market data.

We proceed with the following steps: Univariate distributions are chosen. A simplifying assumption generally used to keep the PCC tractable for inference is that the pair-copulae are independent of the conditioning variables, except through the conditional distributions. Since UHF market data is known to display serial dependence, the data series for each variable is fit to a ARMA(1,1)-GARCH(1,1) model. The residuals from this step are used to obtain the u-scores by applying probability integral transformation. A parametric vine copula is fit on the u-scores. First, choose an appropriate vine copula structure. Second, choose appropriate bivariate copulas from the set {indep, gaussian, student, clayton, gumbel, frank, joe, bb1, bb6, bb7, bb8} using the model selection criteria AIC. The set includes the rotation if available in the copulas. We adopt Dismann et al. (2013) to build the structure bottoms up and model the maximum dependence in the first tree (using Prim’s algorithm ((Prim (1957))). The variables represent the nodes in a graph, and copulas represent the edges. We use the empirical kendall’s tau of the chosen bivariate copula families as weights to construct a a tree on all nodes that maximize the sum of the weights of the edges. The subsequent trees are built in a similar manner, under the additional restriction that the proximity condition must be fulfilled. Once the structure for a tree is finalised the parameters for each pair copula are estimated using the R-package, rvinecopulib. Parameter estimation: Aas et al. (2009) proposed a sequential method for which the idea is to estimate the parameters, level by level, conditioning on the parameters from the preceding levels of the structure. We use this in the current paper to reduce the computation intensity due to the large data set and the number of dimensions. Estimation of the joint density or an expression for a general R-vine density is not our stated objective in this paper. We seek to measure the dependence among the variables in intraday context, investigate whether the dependence is time varying and later try to generalise by investigating a sample of stocks. This requires additional steps and measures. We divide a trading day into periods of 15 minutes each for estimation. The estimation is conducted sequentially but is independent of each other. There is no overlap of data. The choice of 15 minutes is arbitrary. Since our updation to innovation from the incoming data into the limit order book is in high resolution, any coarser time period that contains a reasonable number of data points can constitute an estimation interval. We have earlier experimented with much coarser time periods of 30 min, 45 min and 1 hour with concerns on the arbitrariness of choice. Our choice is driven by an assumption that a coarser interval (such as 15 minutes) would make the mapping of the dependence between variables across time more tractable. Such choices even if arbitrary are useful. For example, Conrad and Wahal (2020) have used 10-min non- overlapping window to compute order imbalances. Their empirical investigation is in scale of seconds. Xu and Li (2018) have utilised a 15 min window for examination of liquidity in futures markets and impact on futures prices based on high frequency data. In the empirical Kendall’s Tau, we have a useful measure to map the dependence between variables. We restrict the analysis to Tree 1 of the copula where maximum dependence has been fit. This is from practical considerations - to maintain objectivity and clarity. Using Kendall’s Tau and based on approaches used in graph theory, we construct and define the following measures: Degree: It is the number of edges (bivariate copula relationships) in which the variable is present in tree 1. This measure is a count. Strength: This is a cumulative measure of the absolute value of kendall’s tau. Let the Kendall’s tau of the ith edge be τ

i

. The variables (nodes) on either side of edge be the variables a and b. Share: This measure, a normalised version of strength, gives the share of the node (variable) among the total Kendall’s tau in the tree. It is defined as the strength of the variable normalised by the total Kendall’s tau of all edges in the tree. If there are n edges in a tree, for the variable a, We follow a particular convention to name the extended measures for the variables. For example, consider BIDASK; the above extended variables are “BIDASKdeg ", “BIDASKstr”, “BIDASKshare”. We report the results only for BIDASKshare as it is the normalised measure of BIDASKstr.

Our dataset consists of the quotes and trade messages for a sample of 30 stocks randomly selected from the NASDAQ 100. These stocks are trading in NASDAQ as on 27-March-2019. The dataset is rich as it uses the NASDAQ Itch outbound protocol.

The trade and order messages are timestamped to nano-second resolution and have a unique reference number. This enables the researcher to model the LOB. Further, the trades are referenced to limit orders that are crossed. Orders have buy, sell and quantity markers. The messages also include cancellation orders and modifications to existing orders.

We employ Chakravarty and Pani (2021) data handling paradigm to handle the data. The messages and transactions are resticted to the trading period between 9.30 am to 4.00 pm US Eastern Daylight Time. The data handling paradigm involves the following steps: First, reconstruct the limit order book and identify quotes that do not appear in the top 10 price levels in atleast one auction. These are eliminated as non-microstructure noise. Second, we compute the variables for our experiment at each tick event. Third, we separate the bid and ask series, to further identify the center in both the series and remove outliers and quotes that may not be participating in the auction.

The cleaned dataset which now consists of our variables is used for pair copula construction. The results are processed to create the datasets consisting of the new measures of degree and share of our variables. The descriptive statistics of the dataset consisting of our variables (including the new measures) is presented in Table 1. The number of null values, specifically in ase of BIDASK, BIDDEPTH and ASKDEPTH is striking. Also the range is high for all the variables showing differences in microstructure properties among the stocks in the sample. In section 5 we present and discuss the results obtained.

Descriptive statistics of the variables

Descriptive statistics of the variables

Total No. Of Values: 774, na:0, Total Number of Stocks: 30, Number of periods for each stock: 26

Bivariate relationships

There are 3727 bivariate relationships (edges in a network with the variables representing the nodes) in our sample. They represent relationships with highest measure of correlation (Kendall’s Tau). The count (percentage) of these bivariate relationships and the fitted copulas are presented in this section. Table 2 presents the count of the relationships in the sample.

Copula fitted to Bivariate dependence relationship (percent of total)

Copula fitted to Bivariate dependence relationship (percent of total)

Bivariate relationships and the top 10 fitted copulas pairs contribute to 75.5% of all the relationships in the first tree. The significant pair is between the bid side and ask side trade duration (BMU-AMU). 20.1% of the bivariate pairs is from this pair and these are, to a large extent (19.5%) fitted with the t-copula, suggesting a tail relationship between the two variables. Later in this section we also evaluate the strength (relative strength in the first tree) of these variables. The strong dependence between trade duration is expected based on a large volume of market microstructure literature. However, the nature of the best fitted copula (t-copula) is a significant result. It comments on the nature of trading in the algorithmic world where buyers and sellers trade with strong stop losses and within narrow price bands. It also indicates that there exists thresholds of transaction success or failure at which the traders move between market orders and limit orders. The literature reported in section 2 suggests such changes to be intermediated by changes in spread or liquidity (depth).

Interestingly, bid side durations (BMU) is present in 3 among the top 10 pairs, while the ask side durations (AMU) is related only to BMU. The bid side durations mediate the information pathways between the ask side durations and other variables in many instances - the high BMUdeg (2.08), as given in Table 3, emphaises this point.

Variation in the degree of the variables across 26 periods of 15 minutes each in a trading day. The values are averages of the stocks in the sample.

The following essential pair is the bid side and ask side order durations (BLAMBDA-ALAMBDA: 11.6%). Of this, tail relationships exist in 5.1% of the pairs fitted with bb7, bb8, clayton, and t copulas, while in 4.7% of pairs, explained by frank copulas there is no tail relationship. Thus, order durations are important. This finding is in line with the results in Brogaard et al (2019) and Pani (2021). In an algorithmic trading world, the order durations are more important than liquidity or spread. The fear of stale quotes being picked-off leads to a behaviour of trying to time the arrival. Availability of technology enables the execution. Van Kervel et al. (2020) finds that Institutional investors coordinate their trading in real-time.

When compared with the trade durations, the order durations carry lesser importance and a relatively weaker dependence relationship. This is expected when observed from a queue theoretic framework. Trades are signals with higher precision; they are expected to carry more information, leading to the algorithmic and non-algorithmic traders emphasising the cues from trades, thus reacting through the durations. Orders possess relatively lower precision and maybe some noise. The more sophisticated algorithmic traders use these signals. As discussed in section 5.2 the bid durations (BMU) is a stronger variable. One reason is that it interacts with both order durations (14%). Further the order durations interact with the volume or liquidity variables that may be considered as the relevant inventory (inventory supplied into the limit order book). This paper has considered orders from the five best price levels on the bid side as well as ask side. In market microstructure, the best bid and best ask prices are considered as the expectation of the trade prices. When order durations from the best bid - best ask are considered the current inference may not be obvious. We have not examined this in our current design.

The number of dependence relationships between the order durations and liquidity on the same side (BLAMBDA-BIDDEPTH, ALAMBDA-ASKDEPTH) and the opposite side (BLAMBDA-ASKDEPTH, ALAMBDA-BIDDEPTH) is similar. This block of pairs constitutes 16.9% of the total. The buyers and sellers attain such a balance between them, through coordinated trading responses of the algorithms. Algorithms achieve such optimisation at the trading system level through continuous monitoring, adjusted responses and feedback loops between buy and sell side.

The dependence relationships between the order durations (BLAMBDA,ALAMBDA) with the trade durations (BMU, AMU) and the liquidity or relevant inventory (BIDDEPTH, ASKDEPTH) is 31.4% of the pairs. The BLAMBDAdeg (1.47) and ALAMBDAdeg (1.52) as given in table 3, only emphasise this aspect. The degree measure for the order variables is consistent through out the trading day (other than the first period where is low). The fitted copulas is diverse. We infer that the role of order durations is important, but the nature and strength of the relationship is an aspect of the microstructure of the traded stock.

The liquidity or volume on bid and ask side (BIDDEPTH-ASKDEPTH pair) occupy 7.1% of the pairs. This relationship is described by several copulas, the more prominent in number (3.1%) being t-copula. The strength of the relationship is lower than the trade durations. In the top 10 pairs, the spread (BIDASK) appears only with the depth (BIDASK-ASKDEPTH-4.5% and BIDASK-BIDDEPTH: 4%). A change in spread can change the response of algorithmic traders from liquidity supply to liquidity demand or vice-versa. The spread continues to be an important variable with reasonable strength (discussed in section 5.2). However, we observe that it is not an active variable in all periods leading to lower occurence.

Fitted Copula

While 39% of the pairs are fitted with a t-copula, other pairs are fitted with diverse copulas bb7(6.2%), bb8(15.8%), clayton (7.8%), frank (13.5%) gaussian (4.2%), gumbel (1.8%), and joe (1.7%). That 9.5% of the pairs are independent reinforces why a multivariate analysis is a more appropriate method. There exists heterogeneity in the dependence relationship. The copula parameters, the Kendall’s Tau and its sign, and the rotation parameter (of some of the copulas), capture the heterogeneity. We view the heterogeneity in the description of the dependence through the fitted copula as a store house of qualitative information. Such information is useful for traders operating in any particular stock-exchange pair, but is beyond the scope of this paper.

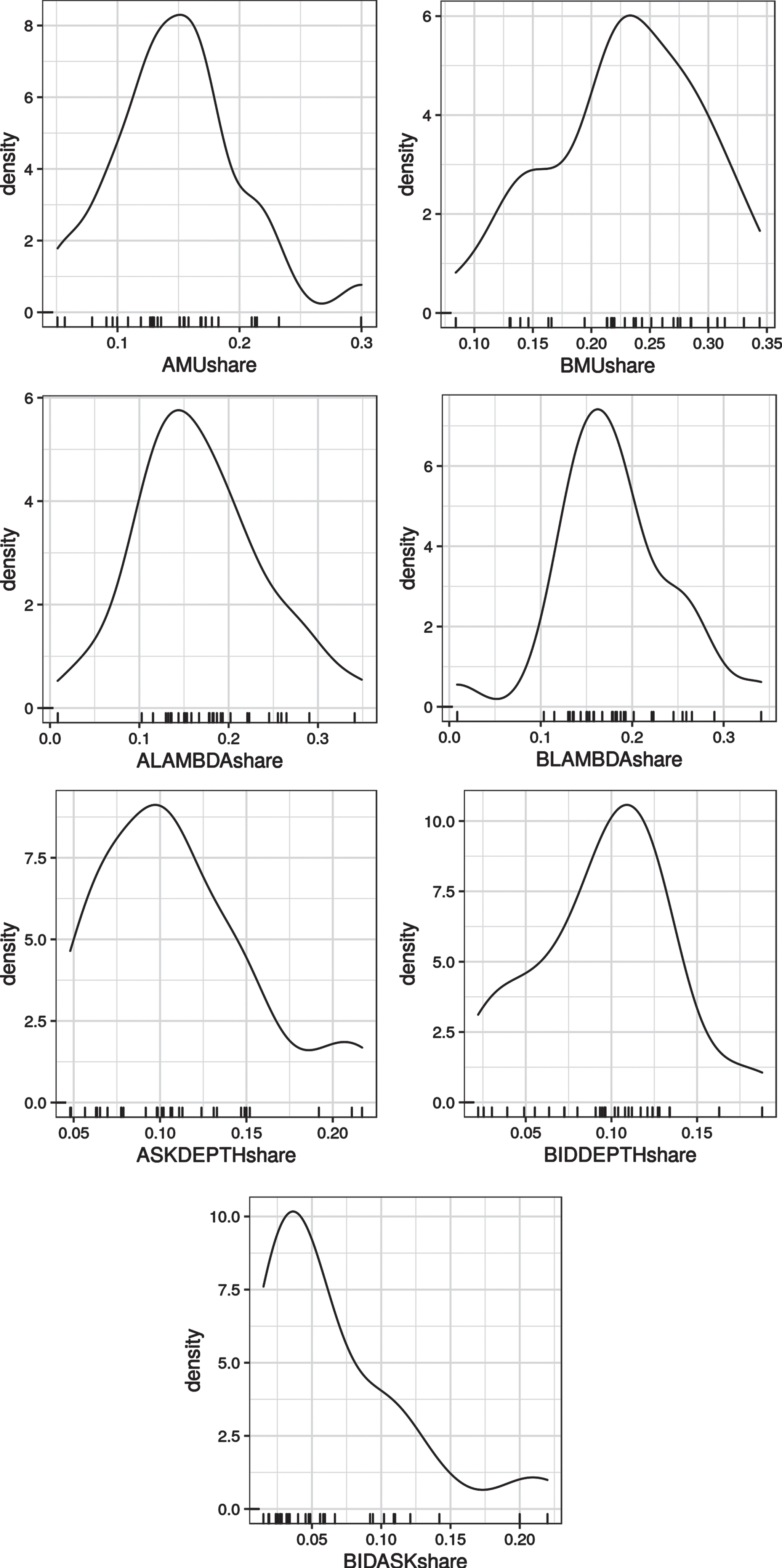

The share of the variable is computed using the normalised cumulative Kendall’s Tau attributed to the variable in the first tree of pair copula construction. Fig. 1 describes the distribution of the strength of the variables. The distributions in Fig. 1 illustrate remarkable properties of limit order markets. The mechanism or market design leads to well defined central tendencies for each variable. At the same time, the presence of outliers in the data illustrates differences arising most likely from market microstructure properties of the markets. The presence or absence of traders, market makers, venues where the stock is traded, tick size, lot size, value of each share, the bid-ask spread. The strength of BIDASK is relatively low along with the presence of outliers. We examine this later in this section.

Description of the share of variables in the dependence structure.

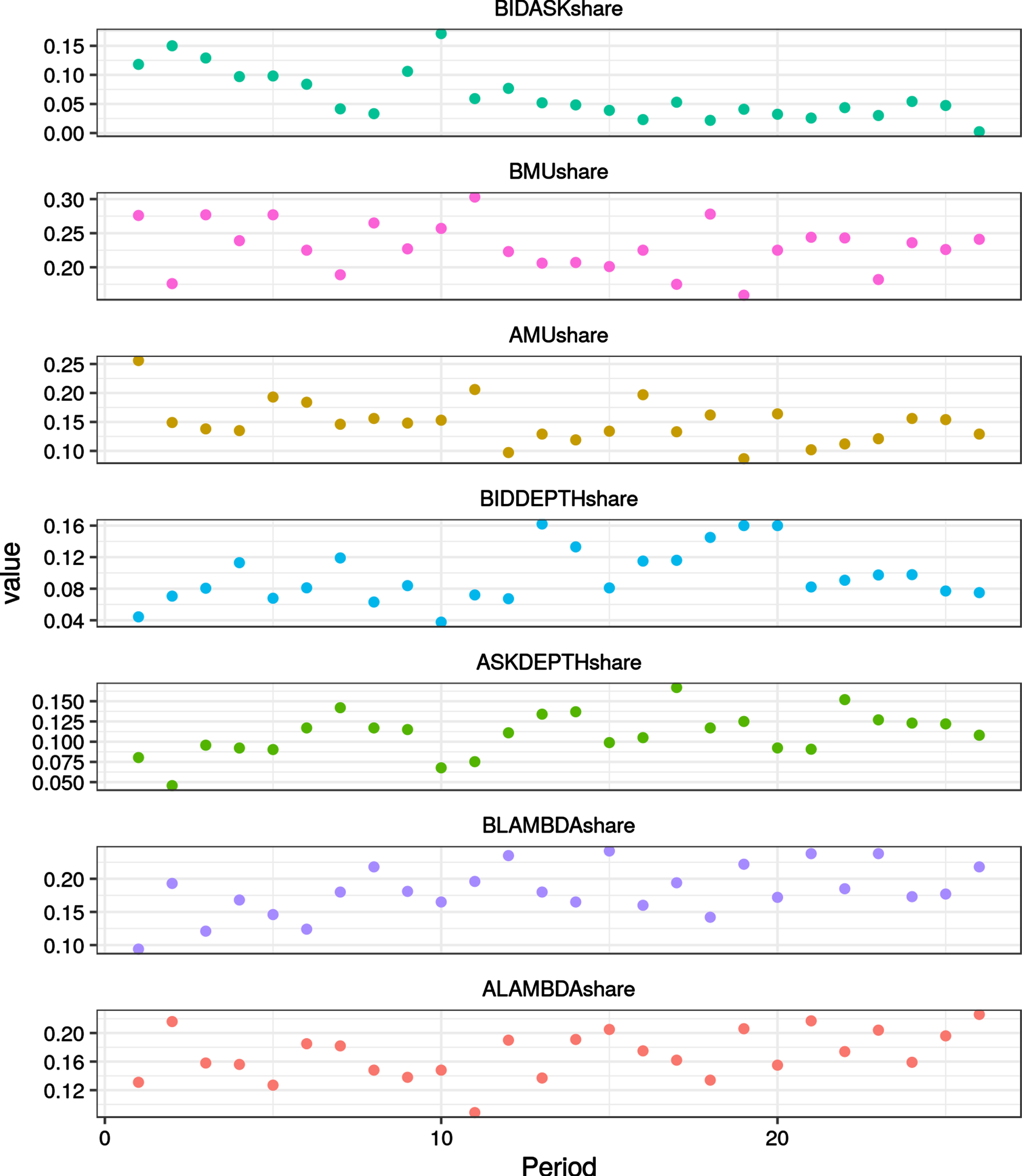

Table 3 gives the degree, the number of variables with which each variable is paired, to describe dependence. Table 4 shows the time-varying nature (dynamic through intraday periods of trading) of the strength of these variables. Additionally, this data is illustrated in fig. 2. The BIDASK has good relative shares in the first half of the trading day and later it has low relative share in the dependence structure. All the other variables show a time-varying nature of relative share in dependence. There are periods where they go out of the dependence structure and periods where they enjoy the highest share in the dependence structure.

Variation in the relative share of the variables across 26 periods of 15 minutes each in a trading day. The values are averages of the stocks in the sample

Variation in relative share of the variable in the dependence structure, across 26 periods of 15 minutes in a trading day. Each data point is the average of the cross-sectional observations of the variable in the period.

Trade durations (BMU, AMU)

On average, BMU has the highest strength with a 23% share. Its strength varies from 15.9% to 30.3% during the day and remains strong through out the day. Similarly, the AMU has share of 14.9% with a range from 8.7% to 25.6% . This supports the hypothesis that an important objective of the trading system is to effect the trades. Pani (2021b) describes a trading system view of the market where conversion of the state of the asset held is the objective of the trading system. Hence, the trading rate needs to satisfy the needs of the traders. Under this model the trading rate is optimised; any other variable, such as order duration, liquidity and spread, would be changed by traders to enable the system to achieve such optimisation.

Spread (BIDASK)

The strength of the trade durations contrasts with the spread (BIDASK is a proxy of the price process), ranging from 0.2% to 17.1% with an average of 6.5% . Above average strength in the BIDASK is observed in the first half of the trading day. Table 3 shows that the first half of trading has above average degree of the variable than the second half. There exist difficulties to evaluate the strength of BIDASK variable in a fragmented market while studying the data from a single exchange.

A cross-sectional variation in the strength and degree of the variable exists (refer appendix - Table 5 and Table 6). The distribution has a fat tail to the right (fig. 3). The distribution is non-normal with skew (1.42) and kurtosis (1.39). Our empirical design does not offer any suitable opportunities to explore this. However, we offer the following comments to facilitate future research. We observe that the range of BIDASK strength is 1.5% to 22% and degree is 0.31% to 1.90% . The outliers with higher strength and degree are VOD, MSFT, AAPL, FOX, SIRI, TSLA, NTES, CTXS, and CTAS. O’Hara and Ye (2011) report that, in 2008, the market shares of the NASDAQ and the NYSE were only 31% and 37% of the trading volume in their listed stocks, respectively. The share of price discovery is higher in NASDAQ for stocks initially listed in the exchange. Even within this group of outliers, there exist individual variation between the relative share of variables. For example, in AAPL, the trade durations have higher share, while in TSLA, the order durations have a high share. Thus, there possibly exists a signature of the microstructure of any individual stock.

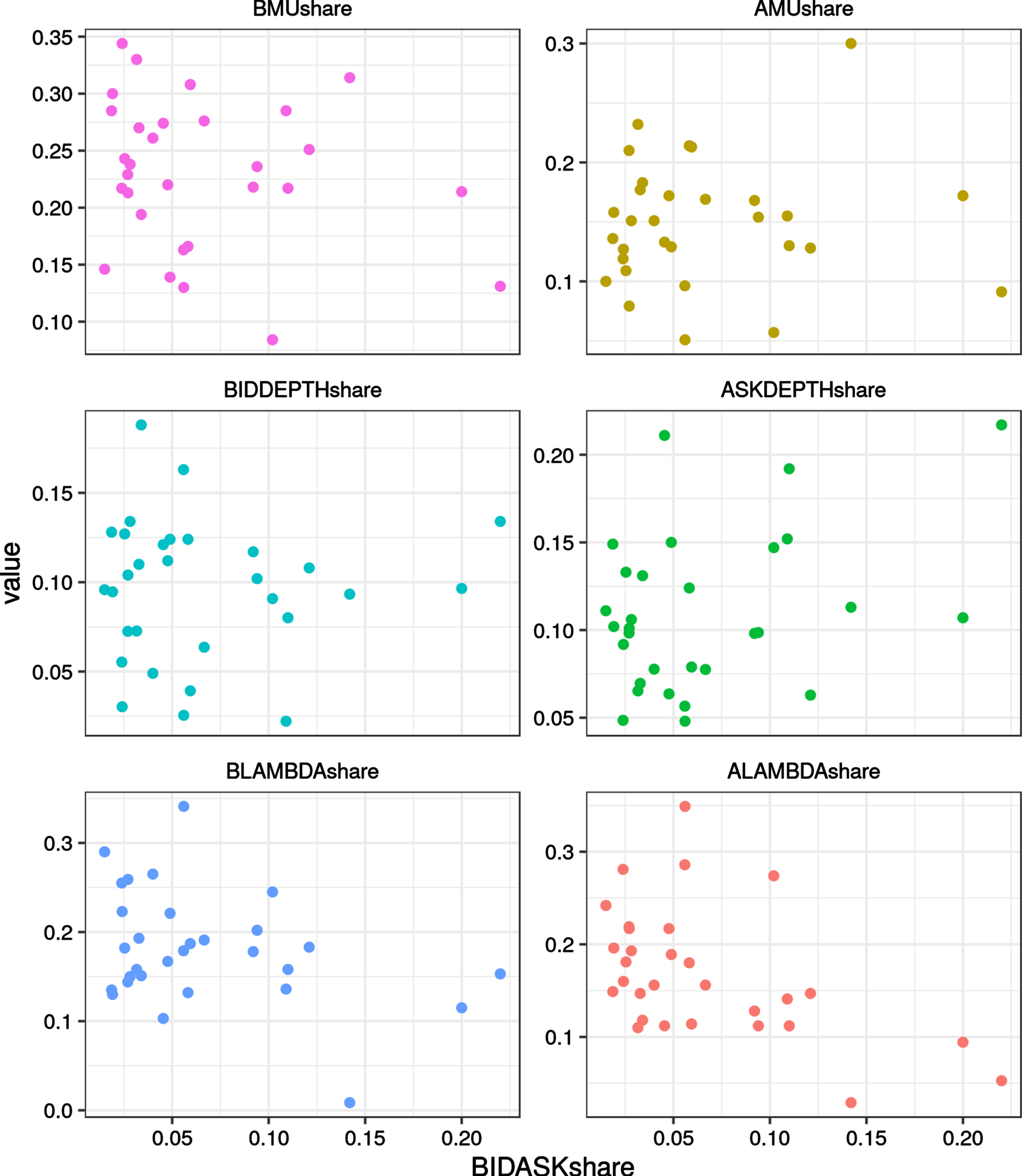

Scatter plot of BIDASKshare and the other variables (this is based on the averages for the stocks, so there is one point plotted for each stock).

Order Durations (BLAMBDA, ALAMBDA)

BLAMBDA (18.2%, range 9.4% -24.2%) and ALAMBDA (16.9%, range 8.9% -22.6%) demonstrate a time varying nature in different periods of trading. They remain important in all the periods.

Liquidity (BIDDEPTH, ASKDEPTH)

The share of BIDDEPTH and ASKDEPTH is lower in the dependent structure. BIDDEPTH (9.6%, range 3.8% -16.2%) and ASKDEPTH (10.9%, 4.6% -16.7%) vary across the different periods of trading during the day, although they do show a relative share in the dependence structure in all periods. From a queue theoretic perspective, one observes that the input could be managed through time arrivals of orders, cancellation and the volume in each order. We have earlier referred to possible coordination or feedback loops between the order durations and liquidity. Communication is the hallmark of any tatonnement process, and in high resolution, we can see it in action.

Strength of spread versus other variables

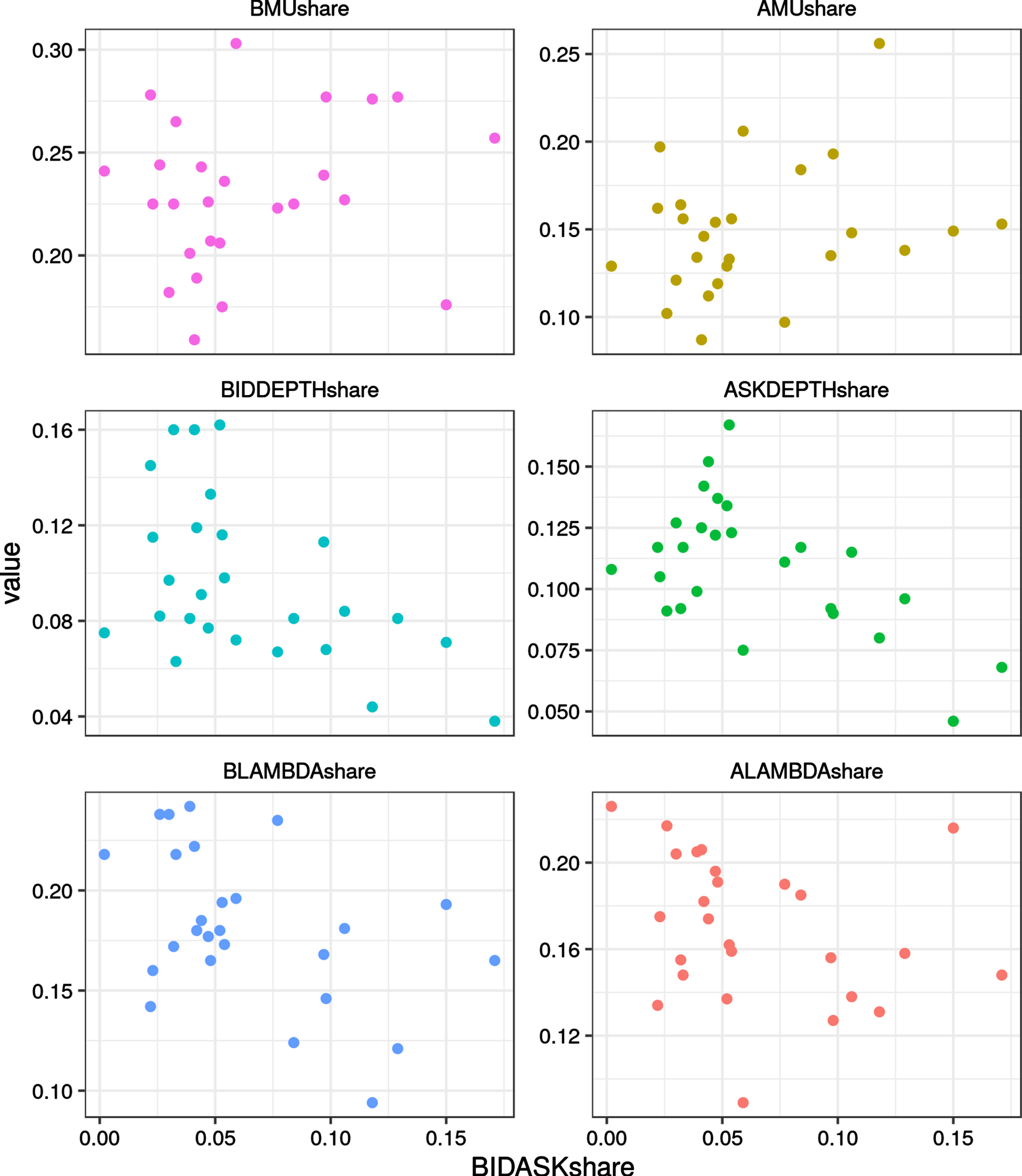

Fig 3 is a scatter plot of the relative share of BIDASK versus other variables in the dependent structure. Each observation is the average at a stock level. Fig 4 gives the average for each period for the scatter plot between Bidask versus other variables. Such a comparison is illustrative because the BIDASK (spread) is generally considered to incorporate friction in trading process (cost of trading, ticksize, pricing, information asymmetry).

Scatter plot of BIDASKshare and the other variables (this is based on the averages for each period, so there is one point plotted for each period).

At the stock level (fig. 3) the spread does not change the range of other variables. However, we can see outliers. The outliers and distant to center data reinforce the individual microstructure characteristics of the trading of the stocks. This is related to the trading ecosystem. In this context, we need to ask: Who trades in the stock?; In which markets is the stock traded?; Are there large traders who generally assume market making roles in the stock? And Do traders observe the stock continuously? Logically, therefore, one would expect more heterogeneity in non index stocks.

In periods (fig. 4) where the share of the BIDASK spread increases, only the share of ASKDEPTH and BIDDEPTH tends lower. Interplay between the bid-ask spread and liquidity is also explained by AT behaviour described in Carrion (2013), Hendershott and Riordan (2013) and Hasbrouck and Saar (2013). The former finds that ATs consume liquidity when the spread is narrow and supply liquidity when it is wider. While the latter finds that when bid-ask spreads are small, ATs initiate smaller trades, cluster their trades and execute trades rapidly.

We investigate in high resolution the liquidity and durations of a limit order market using an experimental design with the help of two recent developments. First, the data handling paradigm introduced in Chakravarty and Pani (2021) that allows us to work with the order book beyond the best bid, best ask level. And second, the pair copula construction method (Aas et al., 2009) offers the methodology to examine dependence structure in a multivariate setup. The present study is one of the applications of pair copula construction to intraday high frequency stock market data. The technique is useful to examine the intraday evolution of the dependence between liquidity, durations and spread. Although this empirical work does not use a proprietary database, the rich public data source in NASDAQ Itch identifies the bid side and ask side activity which served the purposes of this study efficiently.

Market participants, specifically algorithmic traders and institutional traders can benefit from both the methodologies and findings in this paper. Market participants need to constantly weigh in the costs and benefits of aquiring acess to data from exchanges. Firms that operate globally would particularly find our methodology that uses non-proprietary dataset for analysis very useful. Such datasets are released by exchanges around the world. The frequency of such releases is low and hence participants may find it suitable for exploratory analysis. Further, participants who do not subscribe to the level 2 and level 3 data from the exchange can use such analysis from non-proprietary dataset to enhance their understanding of microstructural properties.

The pathways to information flow during trading are embedded in the dependency structure. The strength and nature of the dependence between variables vary through the trading day based on the information flow. The paper characterises such dependence using pair copulas. We are able to weave a complex pattern of dependence that evolves through a trading day, in periods of 15 minutes, between the order arrival rates, rate of trades, liquidity and spread. A queue theoretic framework underlies the model. The liquidity has been defined to include limit orders in the five best price levels on either side and not restricted to the best bid and ask.

For market participants it is important to understand the pathways of information flow in a trading system and their time varying relationships. Success of algorithms and choice of appropriate algorithms depend on better understanding of these properties. When markets are impacted by macro or external shocks long standing relationships among various traders could get affected with entry and exit of traders. Examination of the pathways of information flow can supplement the techniques that traders use currently. In the absence of a market maker the success of any market system depends on such abilities of the traders to infer the actions of other traders.

Among bivariate relationships, the trade durations are the strongest in the dependence structure and occur more often than order durations. Order durations show weaker dependence than trade durations. As a group, the order durations interact with trade durations, liquidity and spread, occupying 31% of the relative share in the dependence structure. We observe evidence of communication, coordination and feedback loops between order durations, liquidity and spread. This finding is in line with the current understanding of limit order markets with algorithmic traders. Our technique presents results from a public dataset, whereas several previous studies have explored these questions using proprietary datasets.

The spread continues to remain important. The variable is not active in all periods, and hence the count of bivariate relationships where it appears is reduced. When the relative share of spread increases, the trade-off comes from the share of liquidity. This is a stylised aspect in markets with algorithmic trading. There exists cross sectional variation in the strength of spread, signifying unique microstructural aspects of individual stocks.

Footnotes

Acknowledgments

We would like to thank Philip Maymin, Managing Editor for his support and patience during the peer-review process. We are also grateful to an anonymous referee for the insightful comments, critical evaluation and suggestions that have helped to improve this manuscript. We also thank participants at NMIMS, School of Business Research Seminar for their comments and suggestions. All errors are our own.