Abstract

Public-private partnership (PPP) has emerged as a new mode for governments to attract potential partners in infrastructure construction, in which the investment allocation is a complex problem. This study explores an approach to managing the uncertainty involved, in the assessment and investment-allocation decisions of PPP projects. Real options and game theory are applied to dispose the uncertainties related to flexibility and distribution of investment in PPP, and these two methods were organically integrated as a new model. The Real Option- Game Theory (RO-GT) model, capable of flexibly handling investment-allocation risk in PPP projects into account. Black Scholes (B-S) real options model and Nash equilibrium are used to analyze the data. The results of RO-GT model indicate that the value of flexibility plays a significant part to the total investments. Additionally, the case study of Beijing metro line 4 reveals a proper allocation plays an important role in the long-term operation of PPP projects. The study is a significant supplement to the existing literature that supports in negotiating the exact investment in PPP projects. The new model provides the PPP stakeholder groups with a quantitative decision making model and an available approach to eliminate the uncertainties of investment allocation in PPP projects.

Introduction

Society requires infrastructure development for human development. For infrastructure developments, the available funding from traditional sources falls far short of the investment needs [1, 3]. Governments all around the world have dedicated significant shares of the public budgets to infrastructure development and maintenance. Few years ago, the booming demands of infrastructure suffered due to economic crisis which led to falling of government revenues and inhibited the development of already planned infrastructures projects. Facing with the stress of a burst need in infrastructures, while with constrained budget, it is the dilemma that governments face. Public-private partnership (PPP) is capable to make significant help to develop a true societal human system by developing private capital in the implementation of infrastructures [4, 5].

A public-private partnerships (PPP) refers to a contractual arrangement between public and private entities through which inputs and outputs of the public and private sectors are allocated in a complementary manner thereby sharing the risks and rewards in providing optimal service delivery and good value to citizens [6, 7]. International Monetary Fund (IMF) outlines PPP as an arrangement in which the private sector participates in the supply of assets and services traditionally provided by the government [8]. Regarding the essential characteristic of PPP is to share risks and benefits with private sectors in infrastructures’ construction, as well as absorb their capital and management experience for achieving a more efficient public service, since the 1980s, most of the infrastructure projects around the world have adopted the PPP mode [9–11]. For instance, in terms of Olympic Stadium in Sidney, Ekurhuleni high speed railway in South Africa and the Bird Nest in China, PPP plays a vital role in their construction.

While, a series of questions have arisen in the process of applying PPP mode, among which the knotty investment allocation and complex assessment are two vital ones [4, 12]. Investment allocation in PPP projects means distributing the construction funds among all participants [13, 14], as a Specific Purpose Vehicle (SPV) composed of all stakeholders in a specific PPP projects would be formed to design, implement and operate the program together. However, the purposes of the government and private investors in a PPP project are different [15, 16], which may undermine the coordination and integration within the Special Purpose Vehicle and further impact the success of PPP project. Exploring approach to find the balance point between public and private sector has been studied by scholars previously. Lei, Sun (2010) adopted bargain game model to analysis the optimal risk allocation of PPP [17]; Sastoque (2016) outlined a proposal for risk allocation in social infrastructure projects applying PPP by making experts interviews [18], Chou, Jui-Sheng (2015) revealed the key drivers of an equilibrium allocation in PPP by comparing cross-country cases [19]. Diversified methods have been used to facilitate a sustainable distribution of responsibility among stakeholders, but most of them are congregating in the risk allocation area and few studied has been conducted the allocation in financing field, especially those with mathematical models giving quantitative clue [20, 21].

The process of negotiating the final capital injected by each stakeholder is complex, particularly when it is worked out on the basis of whole investment valuation which including complicated uncertainties derived from huge and miscellaneous contracts and fluctuating contexts, and specially, difficult to value [22]. A long-term infrastructure PPP necessitates a scientific and impartial mechanism that is able to accommodate high degrees of uncertainty and distribute it reasonably [23]. Almarri Khalid (2014) suggested that improving the risk simulation approach facilitate to clear the investment appraisal process [24]. Burke Richard (2015) drew guarantees provided by Government reduced significant uncertainty [25]. While, there has always a deficiency in the methodology that could measure it with an algorithm to further support the scientific allocation, which makes potential investments vacillate by the door of PPP projects, circumventing a series of uncertainties embedded in long recovered circle construction and arbitrary investment-allocating mechanism but expecting to share revenue simultaneously. A win–win scenario to attract social funds, the major source of investment in PPP projects, with persuasive model and reciprocal allocation need to be pursued for a brilliant and broad prospect of PPP, as well as infrastructure construction [26, 27].

In current implementation of PPP, lack of appropriate allocation mechanism and uncertain resource assessments are two main causes of failures in PPP projects (Asian Development Bank, 2012). For example, in Columbia Toll Road project, the unscientific investment allocation made the public sector burdened overweight capital debt, and the over-optimistically evaluation of revenue led the situation for public sector even worse, which result in nearly hundred million dollars’ debt had to be assumed by government. Thus it can be seen that a rational allocation of investment and accurate forecast of total investment are critical basis for success of the whole PPP project. However, in its practical implementation, a gap between the need and an available scientific model always lead to the share being decided subjectively in negotiating table. Additionally, traditional investment evaluation methods used in PPP contracts fail to evaluate the managerial flexibility induced by uncertainty [28], which caused deficiency and nuisance in future cooperation.

The purposefulness of this study is to explore a model that scientifically allocate investment between public and private sector, which take the complexity embodied in PPP settings and future flexibilities into assessment. In order to achieve the purpose of this study, it is organized as follow. First, an introduction of current PPP assessment and investment allocation is presented. Then, review a great deal of literatures and separately discuss the application and applicability of real option and game theory in the appraisal and allocation field of PPP projects. Based on all above studies, an illustration of methodology design is given in the third part to give a whole skeleton of research and model. This is followed by the description of RO-GT model about how the PPP evaluation and investment allocation is decided. To exemplify the practical application of the innovative mode, a real case study of China is introduced in this study. Finally, the paper close with concluding section and a discussion about further direction

The purpose of this manuscript is to explore an approach which is capable of comprehensively and scientifically allocating and assess the investment in PPP projects. It may fill in the gap in this area and further provide clue for decision making at beginning stage of PPP projects.

Literature review

PPP evaluation with real option

With the uncertainties embedded in large scale investments and long recovery cycles, including future political risks, construction risks, operational risks and other unsteadiness of context, it is a very complex task to effective appraisal the financial value of PPP contracts [28, 29]. Traditionally, methods such as discounted cash flow (DCF) including net present value (NPV) and internal rate of return (IRR), as well as benefit/cost ratio (B/C), which are liner and static in nature and built on the hypothesis that PPP is a now-or-never opportunity, make the dynamic market, social and natural environment, namely some possibilities in the future neglected [30, 31]. It leads to a deficiency in evaluation of PPP projects without taking the uncertainties and flexibilities specialized in PPP into the appraisal. Myers and Turnbhll (1977) argued that the traditional DCF approaches regard future cash flows as invariable and managers neglect all the future uncertainties [32]. Martins, José (2014) pointed that techniques do not allow capturing the inherent value of flexibility [33].

Uncertainty is not only a potential hazard as traditional approaches regarded, which lowering the asset value, but also harbor a series of possibilities and flexibilities [34, 35]. Real Option (RO) is able to value these uncertainties without partiality when calculating the total value of the project [33]. Given the similarity and corresponding between call option and investment opportunities, real option have become widely adopted in academic research, Narita explore a model to analyze economic incentives for carbon dioxide storage with real options [36], Shi Song adopt it to evaluate the uncertainty and new apartment price setting [37], among which investment assessment and decision making are the most frequently adoptedarea.

Real option explore a new and more convincing valuation and decision making of an investment in projects, as discussed by Baranov (2015) [38], Rau (2016) [39] and Gao Yongling (2013) [40]. With the popularity of PPP mode in recent years, there has been a renewed interest in its application in this field, for real option approach views an investment opportunity in real capital as an option rather that obligation, which caters to the symbiosis and flexibilities harbored in PPP projects well, moreover, the price movement of PPP option obeys geometric Brownian motion well. Both of the features contribute to improve economic efficiency and satisfy large investment [41]. Abundant researches (Gabriel J (2016), Wang, Chao (2013), Hassan (2012)) on learning PPP have been conducted with using real option in last decades [42–44].

Based on all the correspondence between real option and evaluation of PPP projects, it is increasingly accepted and employed by scholars in learning various subjects in PPP projects. Whereas, in previous research, real option was used along and the scope of application was limited in value assessment, but it is able to exert more important role in the PPP projects. In this study, real option is adopted for giving a scientific and reliable appraisal in PPP valuation, and then the result will be taken as a vital basis to cooperate with other method to allocation investment between public and private sector.

Investment allocation of PPP with Game theory

A PPP refers to a contractual arrangement between public and private entities through which the skills, assets, and/or financial resources of each of the public and private sectors are allocated in a complementary manner, thereby sharing the risks and rewards in order to seek to provide optimal service delivery and good value to citizens [1, 10]. Thus, the allocation of input, risk and outcome is an important step which is widely studied by scholars. Stilianos Alexiadis (2014) tackled investment allocation by using the theory of optimal control [45], Jui-Sheng Chou (2012) investigated the major contributing factors of successful investment allocation [46]. When focus in PPP mode, there is a special purpose vehicle (SPV) comprises the public and private sector play as a project consortium to conduct the specific infrastructure project. Although the SPV aligns public and private sectors as a whole, in the contractual negotiation stage, all parties manage to facilitate collaboration, and meanwhile pursue for their own profits by conjecturing action of each other and then deciding the optimal corresponding reaction. Hence, the final share equity and investment allocation is a result of the interactions between the public and private sectors. Game theory (GT) suits the allocation strategy analysis under condition of multiple participants’ corporation well[47, 48].

Game Theory (GT) is a method for studying strategic situation, where the outcomes that come from action each participant are not just decided on decision making, but also the reactions of others. It provides well-behaved solution mechanisms for resolving the conflicts among players in a negotiate situation [49]. There are four main elements in a game: players, strategies, orders and payoffs. In PPP projects, players and strategies respectively refer to public and private entities, the choice of investment ratio allocation In the bargain model, we make a hypothesis that each player is completely rational, which means each participant will pursue for the maximization of individual interests, and direct a strategy profile which will reach their optimal solution. While, in the bargain of PPP projects between the public and private sectors, both players wish to reach an agreement in contract, it is not common to have negotiation impasse caused by fully maximizing their own profit. Since both players wish to contribute to the corporation, they take interest of the other into account while achieving their own profits. Thus, a cooperative game theory is more reasonable in analyzing the bargaining model between public and private sectors in PPP projects. The same theory and model is applied by Qing Fang and Luo Li (2014) in their study about the expenses payment allocation between medical insurance and hospital [50].

While every participant in bargain game chooses an optimal strategy, the group of players’ optimal strategies achieves Nash Equilibrium. It is a crucial point in bargain game as it is acceptable to each participant, and meets the maximal interest of players when they have to accommodate the unknown actions of the others, which is the optimal status in PPP cooperative relationship. It is now receiving more and more attention by scholars in PPP field. According to the Nash Equilibrium calculated from cooperative bargain game model, Sun Lei (2010) conducts a study on risk allocation on PPP project financing [17], Glumac (2015) studied the negotiation outcome of brownfield redevelopment within PPP mode [51]. This study is meant to find a scientific Nash Equilibrium of investment allocation in PPP projects which contains the flexibilities in future.

Methodology

The purpose of this study is to build a comprehensive model which is capable to allocate the investment between the public and private sectors optimally with embedding uncertainties, on the basis of summarizing and comparing previous studies in relevant field, and further demonstrate its applicability with practical cases. The study focuses on the features of PPP investment allocation and assessment, among which uncertainties and multi-partner negotiation are two important and intractable ones. Then game theory and real option are employed to cope with them, according to literature review and feasibility analysis. The innovated model would handle the two main features, i.e. investment assessment and allocation, which are associated with each other, as a whole based on merging game theory and real option together. A more scientific and comprehensive model for investment allocation and assessment in PPP would provide a more practical approach for stakeholders in PPP projects to design and conduct specific infrastructure. It may suggest the basis for policy development and implementation of PPPs. The following four purposes were addressed: To describe the importance and difficulties consisted in investment allocation and appraisal of PPP; To explore the effective method for investment allocation and appraisal challenge in PPP respectively; To establish a new model for exploring the optimal strategy of investment allocation which is based on appraisal with flexibilities in PPP; and To demonstrate the workability of the novel model. It is able to provide clue and insights for both sectors in PPP projects and reach a win- win scenario.

Research design

Quantitative method was used to assess the investment distribution of PPPs by considering the indispensable data basis including total appraisal assessment and allocation ratio in PPP investment negotiation. Real option and game theory have been tested in evaluating appraisal or allocation in PPP by previous scholars like Anamari-Beatrice and Hjaila [28, 52], but they should be studied as a whole rather than separately, for gross investment and ratio of per involvers are two key indicators in deciding the capital injected by public or private sectors, which work jointly. To achieve this purpose, qualitative research to identify the main feathers and quantitative method to deal with them by data processing are expected to combine to form a new approach. This study explores the RO-GT model differently from previous studies for calculating the optimal investment distributed to public and private sectors with taking value of uncertainties into consideration. This process is able to get the quantitative result in form of specific numbers for promoting a reciprocal and sustainable cooperation in PPP projects.

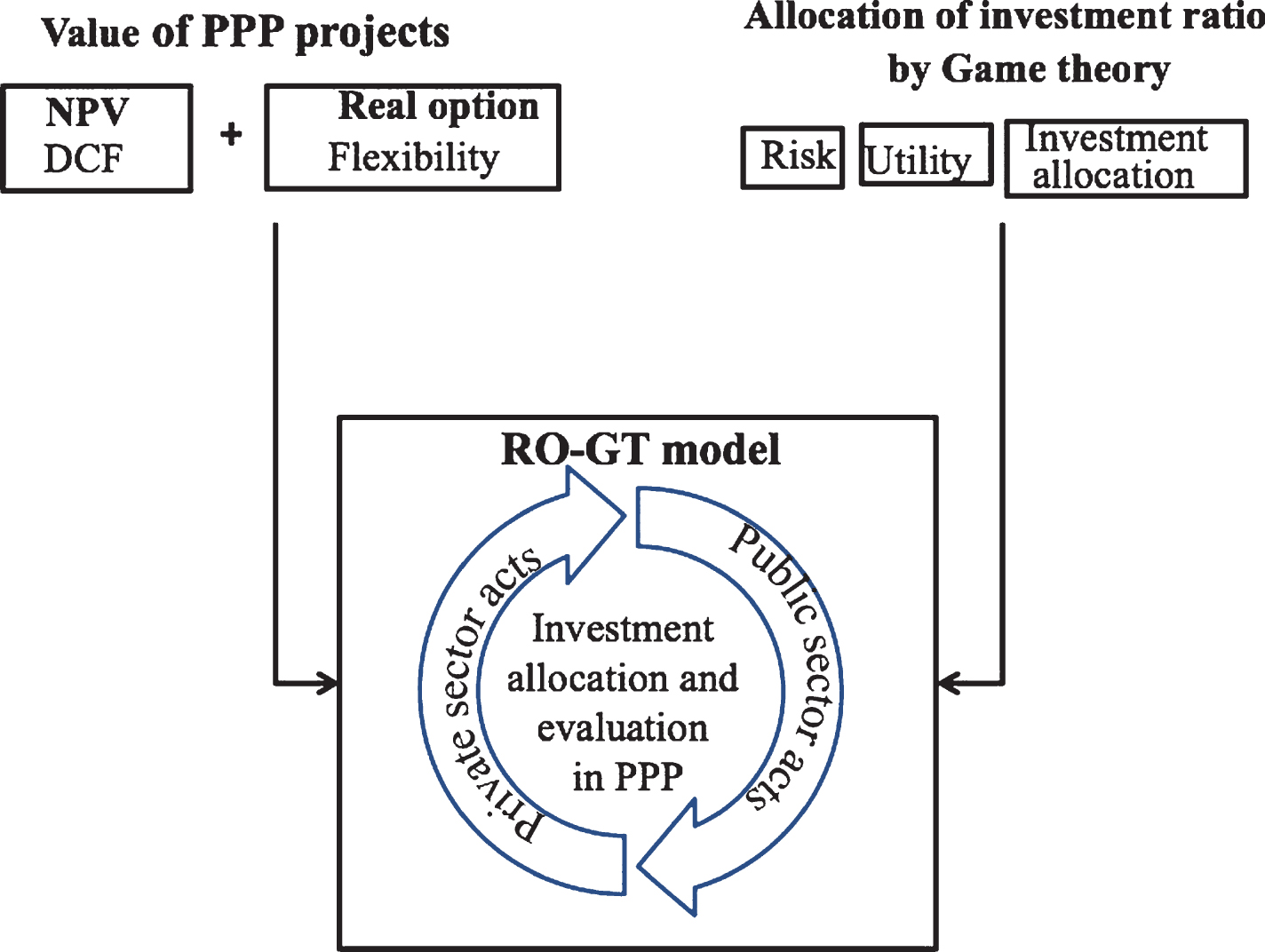

Model frame

The application of real option in evaluating uncertainties and game theory in analyzing bargain process has long been discussed by scholars [34, 53]. For giving a scientific and systematic investment allocation and evaluation for the public and private sectors in PPP projects, the current study is the first to integrate the two methods into a model. Initially, the real option procedure will handle the flexibilities in PPP as a potential option in the future and supplement to its Discounted cash low part, and ultimately give an overall assessment of the value of specific PPP which count in uncertainties. After that, the game theory plays a vital role in making a practical analysis to the allocation ratio decided in investment bargain process in contract decision making stage, which aims at reach a maximal utility of both sectors in PPP. When the calculative process of these two methods organically combine together, the new RO-GT model is formed. The integral structure of RO-GT model is shown in Fig. 1.

Main Structure of RO-GT Model.

By using the RO-GT model, it is possible to directly obtain the final investment amount of both public and private sectors in PPP projects with taking uncertainties into account. RO-GT model may help to an agreement and optimal decision making for participants in the negotiation stage in PPP projects, and give some suggestion for improvement scheme during the implementation of PPP or an alternative approach to support the final acceptance report.

Major parts of data in RO-GT model is get from real condition of specific projects and its contexture financial policy. Secondary data was collected from project reports and national state data through internet. To ensure the consistency and accuracy, all the figures were transformed into a set of international measure unit, and then they would generate an ultimate investment allocation result after running on the RO-GT model, which support the decision making in PPP.

In RO-GT mode, a number of equations included that are included in real option and game theory method are involved in the data analysis process. Initially, to explain the application of real option in evaluating uncertainties and set the foundation for further calculation, mathematical formulas relevant with Geometric Brownian Motion, as well as its transformation, are referred, before the introduce of B-S real option model and a set of related formulas. In order to achieve the Nash equilibrium of bargain game, a number of variables and equations was used to analysis the negotiation process in PPP. Finally, an equation set will be generated as a counting procedure of the RO-GT model. The overall data analysis process is a data process flow for attaining the optimal investment allocation scheme. Matlab software was applied to simplify and assist the calculation procedure.

Model establishment

In financial options, it is a tacitly approve that the price of stock obeys Geometric Brownian Motion [54, 55], for that there is an equal possibility for change of price proportion regardless of its current price, which is a foundation in real option. In this study, we regard the value of PPP projects as its price and note it as V in current time t, so the movement of value follows the equation of Geometric Brownian Motion as shown in equation (1):

In the above formula, parameter μ refers to the expected investment yield; parameter σ means the volatility of projects return rate; and z means random Brownian motion. According to Ito Theorem [56], the formula can be transformed into the equation shown in equation (2):

Thus, ln P follows Brownian motion with drift, and it follows normal distribution when restricted between a random time t and specific moment T, it can be expressed as equation (3):

Here VT denotes the value of PPP project at a specific moment T, V is the value at current time t, φ (c, d) represents a normal distribution with a mean c and the standard deviation d. Based on the characteristic of normal distribution, the changes in ln V

T

obey the normal distribution shown in (4):

Black and Scholes (1973) make a breakthrough in giving an accurate formula to European call option and European put option [57]. For evaluating the value of uncertainties in PPP projects, an assumption that we are in a risk neutral market should be made here. As the pricing formula of option in B-S real option model, in a risk neutral market, its expected value is equation (5):

Here

Now take the distribution of VT into the above formula and evaluate the integral of the right side of the above equation, then the result is presented as equation (7). d1 and d2 in equation (8) and (9) here is introduced to simplify the formula of p:

N (x) in equation (7) is the cumulative distribution function of Standard normal distribution variables whose mean value is 0 and standard deviation is 1. At this point, the value of option in PPP projects is obtained. It will be used as a vital input parameter in the further establishment of RO-GT model.

Since the final investment amount is influenced by share allocation ratio and total investment, the DCF value and option value will be distributed as a whole between the public and private sector. In PPP projects, both sides contribute to a successful collaboration; a cooperative game analysis helps to systematically dissect the bargain process.

Considering the private investors possess only part of the options value, in the RO-GT model, a distribution coefficient of total value, which denoted as s1 is introduced to represent the ratio of private sector; accordingly, s2 denotes the ratio of public sector. In the cooperative game, agreement, coordination and negotiation are involved in bargaining model, so it is the allocation scheme including the strategy decision of both parties which decides the final result, but not personal choice. Therefore, we denote the allocation scheme as s = (s1, s2), in which s1, s2 respectively indicates investment ratio of private and public sector. This allocation scheme is constrained by some impartial condition, for this reason, the following two requirements need to be satisfied: ➀ ≤ s1, s2 ≤ 1; ➁ ≤ s1 + s2 ≤ 1. A set of available allocation strategy S can be expressed as S ={ (s1, s2) |0 ≤ s1 ≤ 1, 0 ≤ s2 ≤ 1, s1 + s2 ≤ 1 }.

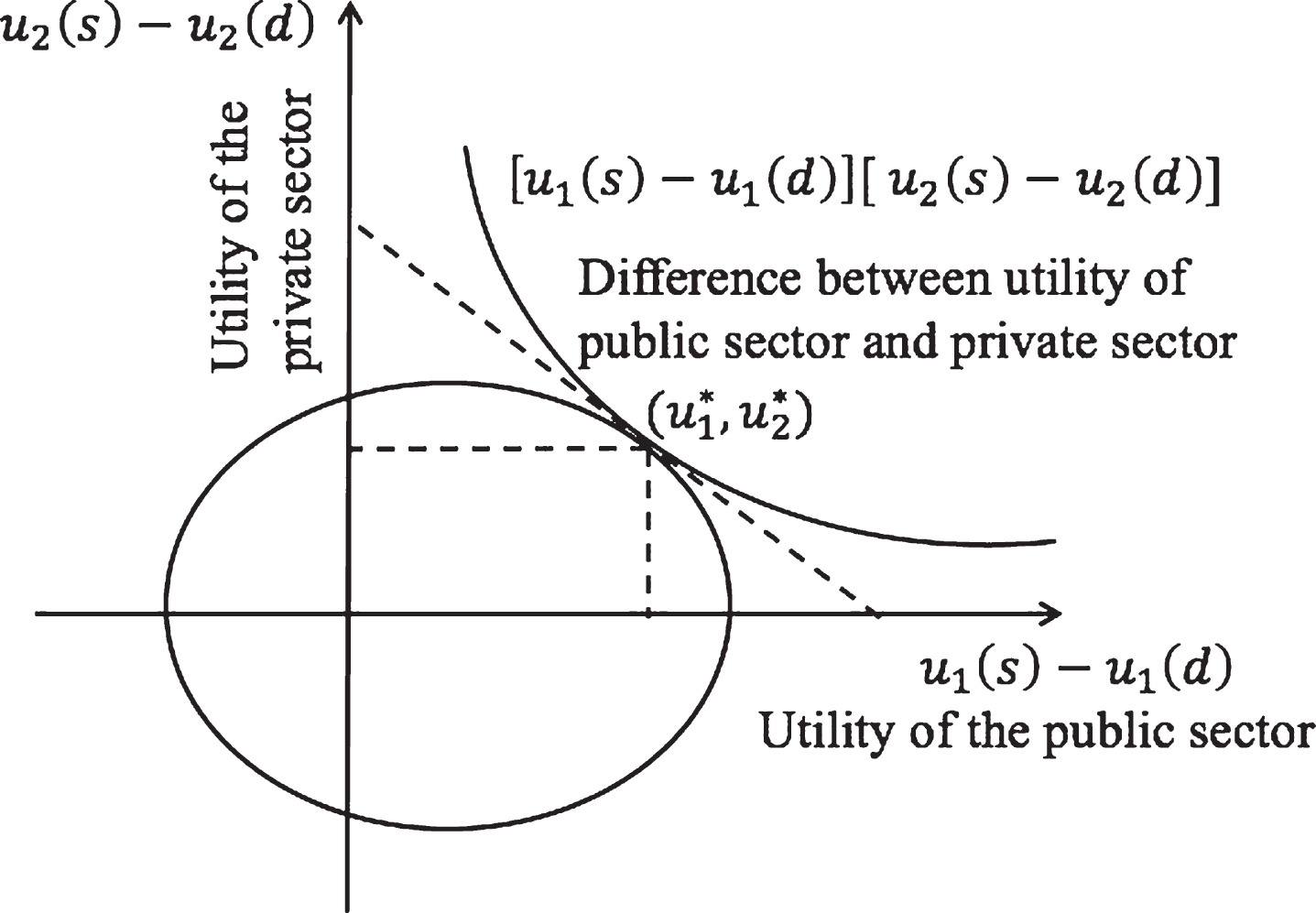

In a bargain game of PPP project, the value evaluation benchmark for both participants may be different, and it influences the final strategy profile and bilateral utility, especially when there are conflicts of interest between the two entities. Therefore, the utility u1 and u2 is an important indicator need to be taken into account which is decided by the allocation scheme s = (s1, s2), that is u1 = u1 (s1, s2) , u2 = u2 (s1, s2). Negotiation impasse is an available and possible situation when at least one of players fails to get extra profit compared with dragging out of the cooperation. We mark this specific negotiation impasse point as d = (d1, d2), d1, d2 respectively refers to the ratio allocation of private and public sector in negotiation impasse point. In a viable bargain game, at least one allocation scheme s ∈ S is feasible to bring about more utility than noncooperation and satisfied, which means u1 (s1, s2) ≥ u1 (d1, d2) , u2 (s1, s2) ≥ u2 (d1, d2).

Nash solution is employed to find the Nash equilibrium in bargain game of PPP projects which means an optimal choice of both parties. According to Nash theory, the unique optimal solution of the bargain game, which meets Pareto efficiency, symmetry, un-deformed by linear transformation and independent of irrelevant alternative at the same time, is the solution of following constrained optimization problems as shown in (10) [58]:

Solution of the above model is the Nash equilibrium of the bargain game in PPP projects. As shown in the Fig. 2, the point

Nash equilibrium of two-person bargain game.

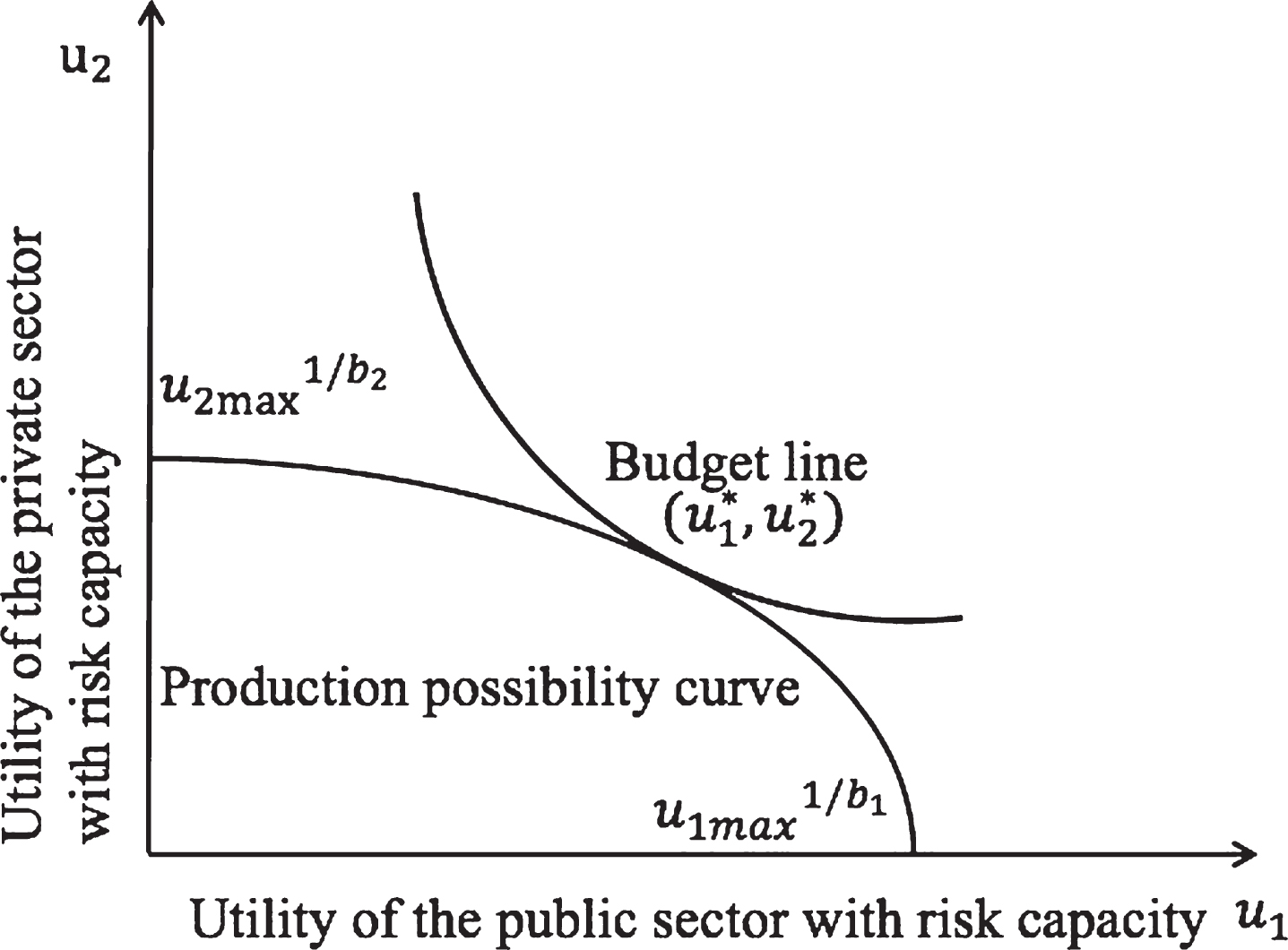

As to the practical implementation of PPP projects, a negotiation impasse indicates that the public and private sectors are failed to reach cooperation, so they cannot gain any profit from nonexistent projects. On the other hand, in successfully carried out PPP projects, the utility of each side is not only related to their investment allocations, but also involve their risk capacities. Therefore, two hypothesizes need to be made here in order to enable the RO-GT model well-suited to concrete process of PPP bargain. Firstly, a breakup in collaboration will cause the specific project fail to take into practice, then the earnings and capital input of both sides form PPP is null, thus, the negotiation impasse point d = (d1, d2) is equal to d = (0, 0). Secondly, the utility of parties in PPP projects is share ratio and risk related. The risk capacity of the private and public side is respectively denoted as b1, b2, both ranges from 0 to 1. The relation among utility u, investment ratio s and risk capacity b obeys

On the ground of all above analysis and hypothesis, n the specific conditions that must be satisfied in the RO-GT model: s1 + s2 ≤ 1, s1 and s2 can be manipulated as

Nash equilibrium of risk capability related bargain game in PPP.

The optimal allocation scheme which reaches the maximal utility in PPP projects is the solution of following constraint optimization problem in equation (11):

By means of Lagrange multiplier method, the result can be calculated:

At this point, real option value p and optimal allocation of investment ratio are solved which are vital input parameters of RO-GT model. The final investment evaluation of each participant is a product of its investment proportion and the flexibility-related value. Further, the flexibility-related value which includes uncertainties and opportunities in the future is a sum of budgetary investment estimate E and its real option value. Consequently, the final expression of investment evaluation of private sector I1 and public sector I2 derived from RO-GT model is shown in equation set (13), and the meaning of each indicator is listed in Table 1:

Symbol and meaning of each variable in RO-GT model

Background

Beijing metro line 4 is a monument under implementation in the form of PPP mode in China. Designing budgetary estimate of this PPP project is 15.3 billion, of which 30% is invested by private sector and 70% percent is contributed by the government. Since the allocation is decided by policy and experience, this case study is intended to give a more scientific and practical allocation and investment allocation based on the RO-GT model.

A special purpose vehicle (SPV) is set up by three companies to incorporate to run the construction of Beijing metro line 4 project. MVA Company makes a prediction of passenger flow during the operation time and shows that in the early stage (around 2010) it will be about 710 thousand person-time per day. In the longer term (around 2034), it will surge to about a million person-time per day. Franchise period of this PPP project is 30 years calculated from the trail operation. Processing and termination of franchise should be subject to items in PPPcontracts.

RO-GT analysis

According to the analysis structure of RO-GT model and the given basic information, specific political and market environment of the certain decision making time are relevant factors which influence the final outcome of investment allocation. Several vital input parameters can be extract from the contextual background as follows: the value of project at current time is equal to its discounted cash flow in the 30-year franchise according to its passenger flow and calculated to be V = 4.12 billion; exercise price of PPP project means the total investment X = 15 . 3 billion; a specific moment in the future means 30 year between trial operations and the end of the franchise, decision making time is 4 years before its trial operations for that the construction of Beijing metro line 4 lasts 4 years, thus,T - t = 34; volatility of projects return rate in that time is σ2 = 0.09 [41]; risk free rate r = 5.76%, which was drawn from the data of bank in that specific year; budgetary investment estimate of Beijing metro line 4 is 15.3 billion.

With regard to the risk capacity of the public and private sector in Beijing metro line 4 project, the special purpose vehicle is made up of three different companies which impact the risk capacity of participants. Although it enhances their ability in resisting risks, the private sectors will be unwilling to take on risk due to their relative separate pursuits of interest and a game relationship that exists among them, therefore, this study assumes the risk capacity of private sector b1 = 0.2. On the other hand, the public sector is the initiator of Beijing metro line 4 project who holds the final ownership of this PPP project. If the contract terminates because of catastrophic defaults or risks, the public entity is responsible for the later construction and purchase for the relevant constructed facilities. On the whole, the public sector is more bound and capable to take risks, therefore in this study the risk capacity value of public sector is assumed to be b2 = 0.7. All the related parameters in RO-GT model are now available and after plugging them into the model, the ultimate investment allocation of this PPP projects can be obtained straightly as shown in equation (14):

The results of RO-GT model show that the optimal investment ratio of private and public sector in Beijing metro line 4 project is 0.22 : 0.78, and their investment evaluation are 4.07 billion invested by the private sector and 14.25 billion funded by the public sector.

In the actual implementation of Beijing metro line 4, the investment ratio of private and public sector is 0.3 : 0.7, private sector funded a bit more than 0.22 : 0.78, which is evaluated from RO-GT model. Besides, the actual budgetary investment estimate is 15.3 billion, a bit less than 18.32, a sum of investment assessed by private and public sector derived from RO-GT model. Beijing metro line 4 indeed suffered financial challenges during its operation [60]. Due to the very low metro fare and limited commercial exploitation of the subway underground, the public sector has to burden a huge financial subsidy to keep its daily operation and financial subsidies more than 600 million per year to ensure profits of private sector. In the end, it caused a disguised additional investment and the investment ratio changed and titled to the public sector. MaoYihua (2009) studied the same case with real option and reached a same conclusion that real option gained value to the PPPproject [30].

The difference between data from actual implementation and from RO-GT model shows that the value of uncertainties could bear a great impact on the total investment, it is the same with the conclusion of Krüger (2012) and Liu, Jicai (2014) [29, 31]. Additionally, the public sector should have undertaken more investment than its actual implementation according to RO-GT model, which may contribute to mitigate the potential financial risk. The case study of Beijing metro line 4 proves the scientificity and availability of RO-GT model. To some extent, if the RO-GT model could be applied in earlier stage of PPP projects, some problems could be avoiding as what suffered to Beijing metro line 4 as a more investment allocation would promote a more sustainable cooperation and healthier capital running.

The application of PPP mode is getting more popular all around the world, and especially in those countries which they are facing gaps between the need of large-scale infrastructure and the financial capitals involved. A win-win investment allocation mechanism and comprehensive assessment are critical factors for attracting potential partners and guaranteeing a sustainable collaboration of PPP projects.

This study presented a model as an innovative avenue to evaluate the integral value of PPP projects which include its flexibilities in the future, and rationally allocate it between public and private sectors. Some literatures have studied relevant area before, Stefan Anamari-Beatrice (2014) emphasized on the value of flexible concession in PPP [28], Jicai Liu (2014) focused on the evaluation of restrictive competition in PPP [29] and Glumac (2015) analyzed the negotiation process of PPP [51]. The RO-GT model pioneers a new approach which is able to cover various uncertainties, risk capacity and negotiation to obtain a comprehensively optimal investment allocation scheme between public and privatesectors.

RO-GT support a quantitative clue for participants in PPP projects to comprehensively check the value of PPP projects, as well as provide an optimal investment ratio distribution among investors which is conducive to avoid unexpected funding and inefficiency in working of funds. Case study of Beijing metro line 4 shows that flexibility in PPP project takes up a considerable proportion of total investment, it is consistent with the result drawn by MaoYihua (2009). It also reveals that the scientific budgets and investment allocation influence the operation of PPP projects in long run. The current study focused on a metro line project of China, while the same method can be extended to other types of PPP projects in other counties. The RO-GT model is a generally applicable method to all PPP projects.

The RO-GT model delivers a quantitative reference for decision making in the feasibility research and negotiation stages in PPP projects. It reinforces the basis towards a more efficient running of capital and a reasonable risk allocation between the entities in PPP projects.

Practical application and future directions

This study has some practical and theoretical implications. In theory, this study fill in the gap in existing list that model analysis with data support falls far behind the theoretical study in PPP field [20]. The innovate model to allocate investment including uncertainties, risk capacity and utility of both sides also pioneer a new block in PPP field which offer reference and direction for further researches.

The current study has significant practical implications; this study explores an avenue to allocate investment scientifically with flexibilities and risk capacity considered with the innovative RO-GT model. Given the fact that infrastructure PP projects are likely to face a series of changes due to complex and incomplete contracts, as well as multiple participants, it is critical for the consortium to measure it and be proactive to avoid unexpected cash flow. The RO-GT model provides an opportunity for both government and consortiums to learn the real value of PPP project which embody various flexibilities in its full-life-circle, thereby judiciously make decision and reasonably allocate investment between public and private sector. The quantitative model can provide data basis for feasibility research, preliminary implementation strategy and negotiation stage in PPP, and facilitate a multi-benefit scenario by eliminating arbitrary decision make and nonsense bargain. Besides, a use of RO-GT model in under construction PPP projects offer a better solution to take precautionary and remedial actions as soon as possible by comparing the practical data with the results derived from RO-GT model. Furthermore, it is hoped the widely use of this approach can promote a fairer and more efficient negotiation between public and private sector, and help government to facilitate the formation and implementation of cooperation in PPP, then drive PPP evolution advance.

A considerable point facilitates the practical application of RO-GT model is that it can be easily converted from classical discount cash flow process, for most of their parameters are similar and related. On one side, it keeps the transparency of traditional methods which prevails in its availability and embedded information sharing. Another, it enhances the ability in revealing the invisible value of PPP projects. Above those characteristic contribute to the application and extension of RO-GT model.

Whereas, conducting PPP project is a complex process. This study needs to be highlighted three important points for future excellence in current conception. Firstly, this research considered the flexibilities in full-life-circle PPP as a whole, in order to make the RO-GT model more integrated and quantifiable. Theoretically speaking, if divides it into several stages to analyze, the evaluation will be more precise. Secondly, in current manuscript RO-GT model studied on just two sectors i.e. public and private. For future generalization of application of PPP mode many other parties will be involved in the investment and results may be different valuable. Third and last important point, in case study part of current research, we only include Beijing metro line 4 case study. Future studies may include more other cases and the results will be different and more generalization.In further work of this study, more efforts will be paid in multiple stage analysis, multi-stakeholder negotiation and investment allocation, and additional cases will be learned.