Abstract

This article presents a model of the impact of stakeholder relations on corporate sales performance, with environmental sustainability playing a moderating role between these two constructs. Correlation analysis and multivariate regression are used to assess these relations. Gleaned from the 2013 International Manufacturing Strategy survey project, empirical data are analyzed with the SPSS software. The results confirm that stakeholder relations, particularly customer and employee relationships, have a significant positive effect on corporate sales performance. And environmental sustainability significantly moderates the impact of business relations on supplier and corporate sales performance. The unique insights the results provide can help business enterprises enhance their stakeholder relations and thereby improve their sales performance. Stipulated too are recommendations for practice and implications for future research.

Keywords

Introduction

With increasingly global economic activities, science and technology continue to upgrade. Capital, labor force, information, technology and other essential factors of production flows gradually across corporate boundaries. More and more businesses enterprises realize that any businesses enterprises cannot be completely isolated to carry out long-term business activities in competitive environment. Keep cooperation with external organization is a main way to keep competitive advantage and develop [1]. Practice has proved that businesses enterprises and their many stakeholders (employees, customers, suppliers, etc.) formed the complex relations has become the essence to the development of modern businesses enterprises’ [2]. Choi holds that good stakeholder relations can bring a sustained performance advantage to businesses enterprises and support other resources to produce performance advantages [3]. Therefore, how to maintain a better stakeholder relations and improvement corporate performance turn into urgent issue that businesses enterprises need to consider.

Corporate performance is efficiency and performance in businesses enterprises operating period includes many types. In the past, scholars usually use corporate financial performance in study of corporate performance [4]. The comprehensive literature on corporate social performance, especially stakeholder relations, shows that the company’s good relations with various stakeholders raise its financial performance [5]. On the basis of resource-based view of businesses enterprises’, Ruf thinks that good relations between firm and stakeholders is a rare, unimaginable and irreplaceable resource that helps the enterprise acquire and maintain performance advantage [6]. Sanjit also based on resource point of view shows that good or bad relations between business enterprises and stakeholders affect corporate brand building and then affect corporate performance [2]. Management commitment of stakeholder interest management will promote strategic decision-making, which will affect the financial performance of enterprises [7]. The strategy mentioned here is a set of integrated, coordinated conventions and actions designed to develop core competencies and gain a competitive advantage. In the past, most of positive relations between stakeholder relations and corporate financial performance were described. Scholars tend to choose corporate financial performance as a measure of corporate performance and rarely study the impact of stakeholder relations on other aspects of corporate performance. In the same time business enterprises ignore factors that can affect relations between the stakeholder relations and corporate performance. Environmental sustainability is reflected attitude of business enterprises to environment here and also is one dimension of corporate social responsibility [8]. Enterprises actively assume responsibility to environment maybe bring positive impact on its financial performance [9]. By studying the mechanism of environmental sustainability, stakeholder relations and corporate performance would help business enterprise to take measures to strengthen relations with stakeholders.

Through literature review and definition of research problem, this article firstly explores the relations between stakeholder relations and corporate sales performance, especially employee relations and customer relations. Second, elaborate environmental sustainability’s moderating effect in stakeholder relations and corporate sales performance. Last, with the support of International Manufacturing Strategy Survey 2013, test the moderating effect. We hope that this study can provide practical management recommendations for enterprises through analysis.

Literature review

Stakeholder relations and corporate sales performance

Stakeholder theory popular from Freeman, and he defines stakeholders as groups or individuals that could influence organizational goals [10]. Carroll proposes that stakeholders are people who have made one or more bets in company. They can exercise their rights to company’s assets or property in name of ownership or law [11]. Stakeholders are people who have a relation with an organization. Hill holds stakeholders are groups who have legitimate claims to business enterprises. They establish contact through existence of an exchange relation: they provide critical resources to business enterprises in exchange for satisfaction of individual interests [12]. Clarkson proposes that stakeholders refer to groups and individuals with power, ownership or interest in the past, present, or future business and business activities that narrow the scope of stakeholders in a certain sense [13]. He assumes that stakeholders should be divided into two main components: the main stakeholder group and the secondary stakeholder group. The main stakeholder group is who directly affect survival and development of business enterprises and operation, mainly shareholders, suppliers, investors, employee, consumers, etc. The secondary stakeholders is not directly start business transactions with business enterprise, affecting business management, production operations and produce impact on business activities such as environmental protection groups, government, non-profit organizations. Donaldson, Wood and other scholars from their own point of view summed up the current knowledge of different situations, putting forward some different but related theoretical issues and future research direction [14]. According to Post’s view, stakeholders can be divided into trading partners, creditors, employees, consumers, suppliers and other trading partners, as well as government, non-profit organizations and general public [15]. This article accepts Post’s and Clarkson’s view use employee relations, customer relations and suppliers relations to measure relations between firms and stakeholders. These three can directly affect the survival and development of business enterprises and operation.

In the literatures, various definitions of corporate performance are put forward. For corporate performance Bradach and Eccles propose an evaluation system of financial performance and nonfinancial performance [16]. Alexander and Buchholz use the market as a measure of corporate financial performance [17]. Accounting can only reflect historical performance of business enterprise. There are differences in accounting procedures and easy to manipulate results by manager [18]. Market measurement concerned about performance of market, not impacting by accounting methods and you can visually see economic business is good or bad. On the basis of these, this article measures corporate performance by sales. Corporate sales performance is the total annual sales of business enterprises.

Stakeholders are also part of business enterprises cannot be ignored. Business enterprises whether could handle the complex relations with stakeholders related to the improvement of corporate performance and competitiveness. Company maintain good relations with their various stakeholders may be a valuable resource [19]. Stakeholder management research also shows that stakeholder relations constitute organizational resources to help business enterprises develop new capabilities [20]. Good stakeholder relations except directly impacting on company’s sustainability performance and also can serve as complementary resources to protect them from other core resources and help to sustain other resources produce performance advantage [2]. They mention in their study that good stakeholder relations will help them recover performance after business enterprises experienced poor performance [3]. Graves and Waddock consider that companies are consciously fulfilling their social responsibilities would make relations between firm and its stakeholders close and that corresponding corporate performance would be better [21].

Businesses with different roles stakeholders such as employees, customers and suppliers will produce different chemical reactions. McWilliams holds that employees with strong working skills are likely to be good performance resources. If these employees are more satisfied with their business, they will also reduce employee motivation to leave and arise them work hardly. Then result in a positive impact on corporate performance [22]. Employees will be more efforts to improve the effectiveness of company [23]. Brown and Dacin propose that if companies have a good relation with customers, customers will increase their demand and accept company’s premium products [24]. Waddock prove that positive customer relations about product quality and safety may lead to increase sales or lower costs associated with stakeholder relations [9]. If companies and suppliers friendly, suppliers will more willing to share knowledge and promote common development [25]. Companies maintain good relations with stakeholders, such as close ties with employees, customers and suppliers. Companies will get their positive returns, which can be used as a measure of business management standards [26]. Bert and Yangqin make a significant correlation between the stakeholder relations and the firm’s financial performance in his study [27].

Stakeholder relations are core part in business enterprises through the above analysis. It will not only affect implementation of corporate strategy but also affect the brand to establish and performance of all aspects of business enterprises. In terms of measuring corporate performance, scholars often use financial performance, such as asset returns and Tobin’s q coefficients. This article assumes that stakeholder relations have impact on other aspects in business enterprise and argues that stakeholder relations can positively influence corporate sales performance. Therefore, propose following hypothesis: Stakeholder relations can positively affect corporate sales performance. The relation with employee can positively affect corporate sales performance. The relation with customer can positively affect corporate sales performance. The relation with supplier can positively affect corporate sales performance.

This assumption can be divided into three sub-assumptions:

Environmental sustainability

Sustainability refers to a process or state that can be maintained for a long time [28]. Environmental sustainability refers to carry out relevant environmental measures to keep sustainability, reflecting in business enterprises [8]. That also is one attitude to environment and one aspect of corporate social responsibility. KLD divides corporate social responsibility into nine dimensions, but five are often used in research including community relations, attitudes towards women and children, employee relations, attitudes towards the environment, products and services [9]. KLD claim that every aspect of corporate social responsibility is crucial and companies cannot ignore. Environmental sustainability is not only has an impact on the natural environment, but also have core role in other aspects of enterprise. This article holds that the degree of environmental sustainability is enterprise whether consider impact on environment other aspects of emissions, whether use environmentally and friendly materials in the process of manufacture products or provide services. These actions would keep environment sustain development which business enterprise might break.

When environmental sustainability in business enterprises is high such as in the process of producing products to actively consider impact on environment and use environmental and friendly materials can bring benefits to business enterprise [29]. In high level of environmental sustainability, close stakeholder relations will bring positive impact to business enterprise and thus have a positive impact on performance [26]. The degree of environmental sustainability is the embodiment of business enterprise’s attitude towards environment. It is part of social responsibility of in business enterprises. Business enterprises actively fulfil responsibility through considering environmental factors, energy saving and emission reduction in the process of manufacturing products and service then corporate performance could be increased [30]. Alison and Tyson propose that initiatively take social responsibility activities bring greater value to business enterprise [31]. In the high degree of environmental sustainability, business enterprises and stakeholders might contact closely. Stakeholders with high loyalty will support business enterprise actively and corporate sales performance will continue to rise [32]. Therefore, propose following hypothesis: Environmental sustainability has a positive moderating effect in stakeholder relations and corporate sales performance. Environmental sustainability has a positive moderating effect in employee relations and corporate sales performance. Environmental sustainability has a positive moderating effect in customer relations and corporate sales performance. Environmental sustainability has a positive moderating effect in supplier relations and corporate sales performance.

This assumption can be divided into three sub-assumptions:

Control variables

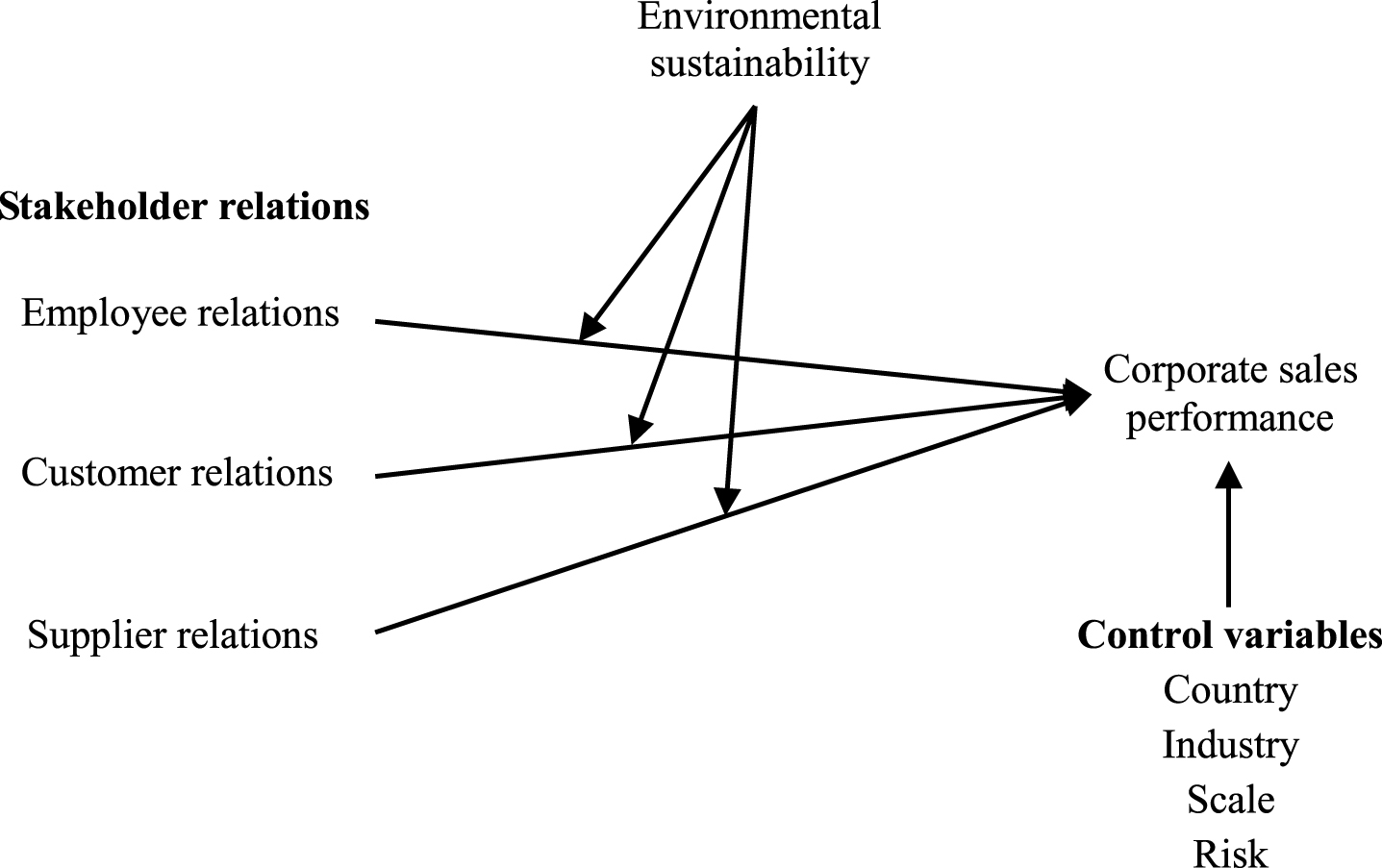

This article chooses scale, risk, industry and country as control variables. The size of scale is considered to be a factor that can influence corporate social and financial performance [33]. Waddock measures size of this scale by the number of employees and also expect that risk and industry are another two factors that affect social and corporate performance [9]. The capability of adapting risk will affect carry out a series of activities, revenue and expenditure and market construction. There are some differences in business enterprises’ attitude to environment and stakeholder among companies in different industries. Previous studies show that industry and national significantly impacts stakeholder relations and corporate sales performance [34]. Business enterprises from different industries, their enterprise mission, business goals, products or services are also mostly different. Business style and habits might are different in different countries or areas. For example, their attitudes to the same thing may have multiple results. Therefore, we adapt scale, risk, industry and country as control variables. Risk refers to the extent of the impact Fig. 1.

Theoretical model.

Questionnaires and Data Sources

The data used in empirical analysis comes from the International Manufacturing Strategy Survey in 2013. In this survey totally collected 674 manufacturing enterprises from 23 countries (regions). The IMSS questionnaire is distributed to industrial sector of ISIC28-35 according to International Standard Industrial Classification. Samples are usually representative business enterprises in the region or country. The questionnaires and surveys of these enterprises increase the quality of questionnaire and improve reliability and credibility of survey data. The sample distribution is shown in Table 1.

IMSS 2013 sample distribution

IMSS 2013 sample distribution

Many scholars use KLD database to measure the relations between business and stakeholders. For example, Waddock uses owner, attitudes towards employees, relations with community, product and environmental policy in KLD data to show business enterprises and stakeholder relations. This articla uses relations with employees, customers and suppliers to measure relations between firm and stakeholders and describes relevant indicators according to IMSS-VI survey, as shown in Table 2. Among them, relations with employee are compared with competitors. Relations with customers and suppliers refer to the state of business enterprises. All of following indicators are in the form of a five-point scale, reflecting the level of performance in survey on the issue.

Variables measurement

Variables measurement

Many scholars study financial performance of enterprise is extensive. This article chooses corporate sales performance as corporate performance. Corporate sales performance refers to performance of business and manager over a period of time, and performance of manager is mainly reflected in the sales [35]. Therefore, this article uses sales measure corporate sales performance.

Environmental sustainability is one aspect of corporate social responsibility. Scholars always use “environmental protection measures” to measure this variable. On this basis, this article uses a similar item to depict this variable, that is the importance of “providing more environmentally and friendly products” when acquiring orders, mainly compared to the previous three years to describe the business environment attitude. A five-point Likert-type scale anchored at 1 = “totally disagree” and 5 = “totally agree” was used.

Reliability is used to evaluate stability and reliability of questionnaire. IMSS questionnaire is a relatively mature questionnaire with certain stability and reliability. In practical problems, Cronbach’s alpha values are often used for reliability estimation. Usually when Cronbach’s α is greater than 0.8, indicating that this survey is fully acceptable and less than 0.5 is unacceptable. In this article, Cronbach’s α values are found to be greater than 0.5 and indicators are in line with reliability requirements.

Validity refers to the extent which measured results reflect desired content. Validity is usually measured using factor analysis methods and usual validity should be not less than 40%. In this article, we carry on factor analyze about stakeholder relations, corporate sales performance and environmental sustainability by SPSS and calculate that all the cumulative variance contribution rate more than 40%, which indicates that questionnaire used in the research has good validity Table 3.

Internal reliability and construct validity analysis

Internal reliability and construct validity analysis

Descriptive and correlation analysis of variables

The mean, standard deviation and correlation coefficient of variables involved in this study are shown in Table 4. It can be seen that there is a strong correlation between stakeholder relations and corporate sales performance. At the same time, the three dimensions of stakeholder relations and corporate sales performance also have a strong correlation.

Descriptive statistics and correlations

Descriptive statistics and correlations

*P≤0.1; **≤0.05; ***≤0.01.

As can be seen from Table 5, variables’ VIF is far less than 10. It indicates that the model has low multiple collinearity. The regression coefficient between employee relations and corporate sales performance is positive and significant (β= 0.197, p < 0.01). Employee relations can positively affect corporate sales performance, assuming that hypothesis 1a is verified. Customers relations has a significant positive effect on corporate sales performance (β= 0.167, p < 0.01), assuming that hypothesis 1b is verified. But supplier relations has not significant effect on corporate sales performance (β= –0.089, p > 0.01), hypothesis 1c isn’t verified. Therefore, hypothesis 1 is not completely supported.

Moderation effect

Moderation effect

In this article, independent variables and moderators can be regarded as continuous variables. And this article uses hierarchical regression analysis method to explore moderating effect of environmental sustainability on stakeholder relations and corporate sales performance. The regression results of moderating effect of environmental sustainability on stakeholder relations and corporate sales performance are shown in Table 5. The model’s significance, regression coefficients of regression equation, R2 and ΔR2, and exchange coefficient are also shown in Table 5. It can be seen from it that sig F change value of third equation is less than 0.05, and interaction coefficient of employee relations and corporate sales performance is not significant (β= 0.053, P > 0.01). Thus environmental sustainability couldn’t play a positive moderating role in employee relations and corporate sales performance, hypothesis 2a isn’t verified. The interaction coefficient of customer relations and corporate sales performance is not significant (β= –0.052, P > 0.01). Thus environmental sustainability couldn’t play a positive moderating role in customer relations and corporate sales performance, hypothesis 2b isn’t verified. The interaction coefficient of supplier relations and corporate sales performance is positive and significant (β= 0.076, P < 0.01). Thus environmental sustainability plays a positive moderating role in supplier relations and corporate sales performance, hypothesis 2c is verified.

Discussion

In this study, two conclusions are drawn from empirical research. First, relations between business enterprises and employee can positively affect corporate sales performance and relations between business enterprises and customer can positively affect corporate sales performance. Second, environmental sustainability has a positive moderating effect on supplier relations and corporate sales performance.

First, employee relations and customer relations both have a positive impact on corporate sales performance. This is consistent with the views of Hillman, Graves and other scholars, stakeholders will have a positive impact on business [20, 22]. High stakeholder relations that are more harmonious stakeholder relations, especially with employees and customers, will contribute to a better performance of corporate sales. The relations with employee are mainly reflected in employee’s satisfaction with all aspects of business enterprises. Employees will consciously work hard, fulfil their duties and all departments actively cooperate in condition of business enterprises pay more attention on working atmosphere, relations among employees and promotion of space and benefits are acceptable. Thus corporate sales will be a breakthrough [36]. The corporate sales performance will naturally improve. Business and customer to maintain a good relation, such as after-sales service; front-line staff with a warm and full attitude towards customers when they in purchase of products or experience in process of service; customers to maintain close relations after purchase or experience to send new product or service information, discount promotional information, etc. These will promote customer satisfaction and their loyalty to enterprise. And then these would greatly increase the customer’s consumption in business enterprises, thereby enhancing enterprises’ sales [37]. Therefore, business enterprises which pay more attention to the relations with stakeholder might stay excellent sales. Building positive relations with major stakeholders can help companies get profits.

Second, environmental sustainability has a positive moderating effect on stakeholder relations and corporate sales performance. Especially, environmental sustainability has a positive moderating effect on supplier relations and corporate sales performance. Environmental sustainability is reflected business enterprises’ attitude to environment and it is closely related to the attitude of enterprise to its stakeholder [38]. Business enterprises actively consider the impact on environment and initiatively take environmental sustainability measures in production or service process. For example, use environmentally friendly materials, treat sewage and optimize resource allocation. These indicate that business enterprises attach importance to its relations with outside world. In this situation if business enterprises and stakeholders have close relations in some aspects, corporate sales performance would have been positive effect. Firm could receive trust of stakeholders, especially customer trusts if the relation with stakeholders is close. The customer will actively consume, which will have the positive impact on sales performance [20]. In Hypothesis 1c, supplier relations have no significant impact on corporate sales performance, but we cannot deny the role of stakeholders in production of business. This phenomenon may be due to under the influence of environmental sustainability, supplier relations’ negative impact on corporate sales performance and positive effects of the interaction between the two are mutually neutralized. Therefore, we cannot deny the importance of the relations between enterprise and supplier. Business enterprises and suppliers need to maintain cooperation to achieve logistics, information flow sharing, which is conducive to business enterprises to maintain cost advantages, quality stability and form a solid foundation for corporate sales [39]. In previous studies, many scholars have suggested that corporate social responsibility will positively affect business performance and related enterprise strategies and attitude towards environment is one aspect of social responsibility [40]. Business enterprises’ attitude to environment is not similar. One enterprise with positive view and their stakeholder relations could be close. Business enterprise with employees and customers will be more closely and harmonious than others. With efforts of employees and customer support and trust, corporate sales performance will be greatly improved. Business enterprises emphasize on environmental sustainability, but their relations with stakeholders are not strong. Their sales performance may not be high. Thus, the attitude of business enterprises to deal with environment will affect relations between stakeholders and corporate sales performance, which has the positive moderating effect in them.

This study has two implications for management practice. In increasing globalization of economy and socialization of production transactions between enterprises, business enterprises and their stakeholders are interdependent and mutual restraint, forming a dynamic and complex system that contains various factors, which will have an important impact on management decision and production operation of business enterprises. This means that business enterprises need to focus on and meet interests of stakeholders and establish good relations with various stakeholders. First, this study affirms the impact of enterprises and stakeholder relations on corporate sales performance. Different stakeholders have different interest requires. Business enterprises enable make virtuous ways to different stakeholders. If exist close relations between business enterprise and stakeholder, such as an employee, a customer, etc., employees and customers are able to recognize this business. Customers will buy product or consume actively. And their sales performance will naturally rise. In an increasingly competitive market environment, business enterprises cannot be isolation if they want to survive and develop. Businesses not only maintain good relations with employees, customers, suppliers, but also keep right ties with government, communities and nature. Specifically, provide nice working atmosphere for employee; promote space and opportunity to achieve personal value; build online platform to provide a lot of trustworthy information channels; actively participate in charity activities; reduce the distance with public and establish active image. Second, this study verifies moderating role of environmental sustainability in relations between stakeholder relations and corporate sales performance. The higher degree of environmental sustainability, the stronger relations with stakeholders and the positive impact will be emerged. Every enterprise should have positive attitude towards environmental protection and take relevant measures, such as use human pollution-free environmentally friendly materials; optimize allocation of resources, improve utilization; strengthen waste water treatment. Improve environmental sustainability in the process of product or service. Business enterprises take responsibility initiatively for environment and actively contact with stakeholders. Not only will make earth more beautiful, but also bring performance improvement.

Conclusion

This article researches the impact of stakeholder relations on corporate sales performance, and explores the moderating role of environmental sustainability. The empirical analysis shows that employee relations and customer relations have positive effect on corporate sales performance. This article also reveals the moderating effect of environmental sustainability in stakeholder relations and corporate sales performance. The results of this study will enable companies to clearly see the positive commitment to environment, as well as the importance of good relations with stakeholders, and provide support for the relevant decisions.

This article has the following theoretical significance. First of all, previous studies on stakeholder relations and corporate performance focus on financial performance, while the article focuses on corporate sales performance. There are a few literatures about relations between stakeholder relations and corporate sales performance. Secondly, in this article test the moderating role of environmental sustainability between stakeholder relations and corporate sales performance. Highlight the impact of environmental sustainability on corporate performance and stakeholder relations. And provide a basis for future research.

This article examines stakeholder relations including employees, customers and suppliers’ relations. But stakeholders are more than three categories, so in further study, elements of stakeholder relations need to be considered more detailed and accurate than before. The IMSS survey is a comprehensive survey involving lots of countries and content. The indicators selected in this study are qualitative indicators. The research object give a score for question (score from 1–5) and on behalf of business in the performance of the problem. The advantages of this study are that number of samples is large, content is rich and research problem is comparatively strong. But there are some limitations. For example, different respondents may assume different criteria for the same problem, and thus give the answer according to their own assumptions, assuming that the differences in the standard may have an impact on the comparison results. This not only requires the IMSS investigation team to continue to improve in the future work, but also in process of research through collection of other data, etc. to modify model and data, so as to ensure more accurate research.

Footnotes

Acknowledgments

I would like to express my gratitude to all those who helped me during the writing of this article. My deepest gratitude goes first and foremost Professor Tian Yezhuang. I do appreciate his patience, encouragement, and professional instructions. I also owe a special debt of gratitude to Professor Chrisvoss of London Business College and Professor Perlindberg of Camels University in Sweden who launched International Manufacturing Strategy Survey (IMSS). This article uses survey data of IMSS VI in 2013.