Abstract

BACKGROUND:

The challenges of ever-changing technological and financial landscape call for experienced, open-minded and visionary SME managers to match the pace and be innovative to enhance firm competitive advantages. The challenges are even more rampant in Africa, characterized by noticeable technological and financial vulnerability demanding special attention.

OBJECTIVE:

This study focused on analyzing the impact of African SME use of ICT and the use of financial services on firm innovation performance. The study further, explore the mediating effect of firm manager’s experience on the firm use of ICT and financial services-innovation performance relationship.

METHODS:

Utilizing data from the enterprise survey portal, a total of 11504 SMEs from 27 countries are involved in the analysis. The analysis employed multiple regression models using SPSS 23, and the mediation effect analysis employed the Sobel test of mediation.

RESULTS:

The general results indicate a significant association of firm use of ICT and financial services on its innovation performance, with exception of the variable of firm website ownership, which had an insignificant association with its ability to introduce new products/services. Also, the results depict the SME manager’s experience to significantly mediate the firm use of ICT and use of financial services-innovation performance relationship, but out of ten, only two models had an insignificant mediation effect of the manager’s experience on the firm having its own website-innovation performance relationship.

CONCLUSION:

The study results provide a profound impact of the relevant SME managerial experience on the ability to well manage the cotemporally dynamic resources like technology and finances for enhancing firm innovation which results in increased competitive advantage.

Keywords

Introduction

Enshrouded with many challenges the entrepreneurial display of the African economy is marked with the formation of SMEs which has been an undeniable option for many individuals for making returns and as survival means, due to the lower countries’ employment bases [1, 2]. But in turn, SMEs have become the backbone of the economies they thrive in through notable contributions [3–5]. These SMEs are not excepted from the effect of the global trends of technology dynamics and the changing financial landscapes, which have forced entrepreneurs to censure their traditional ways of operations and therefore grasp new challenging ways of operations [6]. The use of technology within the African SMEs may still be a challenging phenomenon and the adoption stages are at a differing pace though share the same contests [7]. On the other hand, the financial landscape is changing now and then. There is an inception of various financial products targeting individuals and firm users [8]. Technologies at another level seem to merge with finances as many of the financial products are technologically based.

SMEs in Africa are typically characterized by informal structures, inadequately and unsystematic developed accounting and administrative procedures, sometimes unreliable decisions making the process [9]. And in most cases, entrepreneurs with very good ideas and fast-paced growth during the initial stages may lack the relevant experience to sustain the firm in the long term. SMEs’ innovative performance requires a high level of experience and expertise. With these challenges, the expertise and characteristics of the firm managers become a vital need for the firm to succeed. The technological innovations that can foster SMEs’ innovativeness need experienced, open-minded and visionary executives. To face the challenging financial landscape for analyzing the cost and benefits of various financial products requires high empathy for knowledge and understanding [10, 11]. As we move from firm access to technology and financial services, a discussion surrounding how firm managers’ competence and experience manipulate contemporary technological resources and the emergent accessible financial products for firm innovativeness builds up. The influence of executive manager characteristics on the success of organizations has been empirically exemplified in the literature [12–15]. [16] argues that there is a close relationship between the firm decision-makers and the inclination towards better performance. There are several views that have connected the problems that SMEs face to the manager/owner characteristics. For instance, [17, 18] expound on the dynamic relationship between the firm operating environment and the entrepreneur’s characteristics. In this sense, they recognize SMEs as unique entities. Also [19] found that there is a high correlation between the owner/manager’s mentality and their firm financial performance.

Prior studies emphasizes have focused on the impact of firm use of ICT on innovation (e.g. [20–23]. Other scholars have attempted to evaluate the association of access and use of SME financial services with their general performance (e.g. [24–26]. And on the other tier, most of the scholarly studies have ventured to study firm financial structures and the use of technology theories [27, 28]. Some have attempted to study the use and access to financial services and technology [29–31]. To our best of knowledge, we scarcely observed literature integrating firm management competency and experience to determine how they are able to manage accessible ICT and financial services as important factors for enhancing firm innovation performance. Therefore, this study caters to this gap by analyzing the impact of African SMEs’ use of technology and financial services on innovation performances under the umbrella of the owner/manager’s experience. The study model crystallizes on how the human factor at the firm level is able to manage the dynamic resources to enhance firm competitive sustainable advantages. Specifically, we want to examine what is the contribution of firm use of ICT in innovation performance in Africa SMEs? What is the influence of firm use of financial services on innovation performance in African SMEs? Does the firm manager’s experience mediate the use of ICT-innovation performance relationships for SMEs operating in Africa?

The rest of the paper is organized as follows. First, the study focuses on the discussion of the theoretical context, hypothesis development, and explanations of the variables used in the study. Second, the researcher embarked on explaining the methodological approaches whereby the descriptive, multiple regression and Sobel test for mediation are exemplified. Third, the results and the hypothetical respective discussion of the results are presented, concluding with the presentation of the mediating role of the manager’s experience results. Lastly, the study is concluded by providing the holistic theoretical and practical contributions of the study, implications, limitations, and opportunities for further studies related to the phenomenon.

Theoretical context and hypothesis development

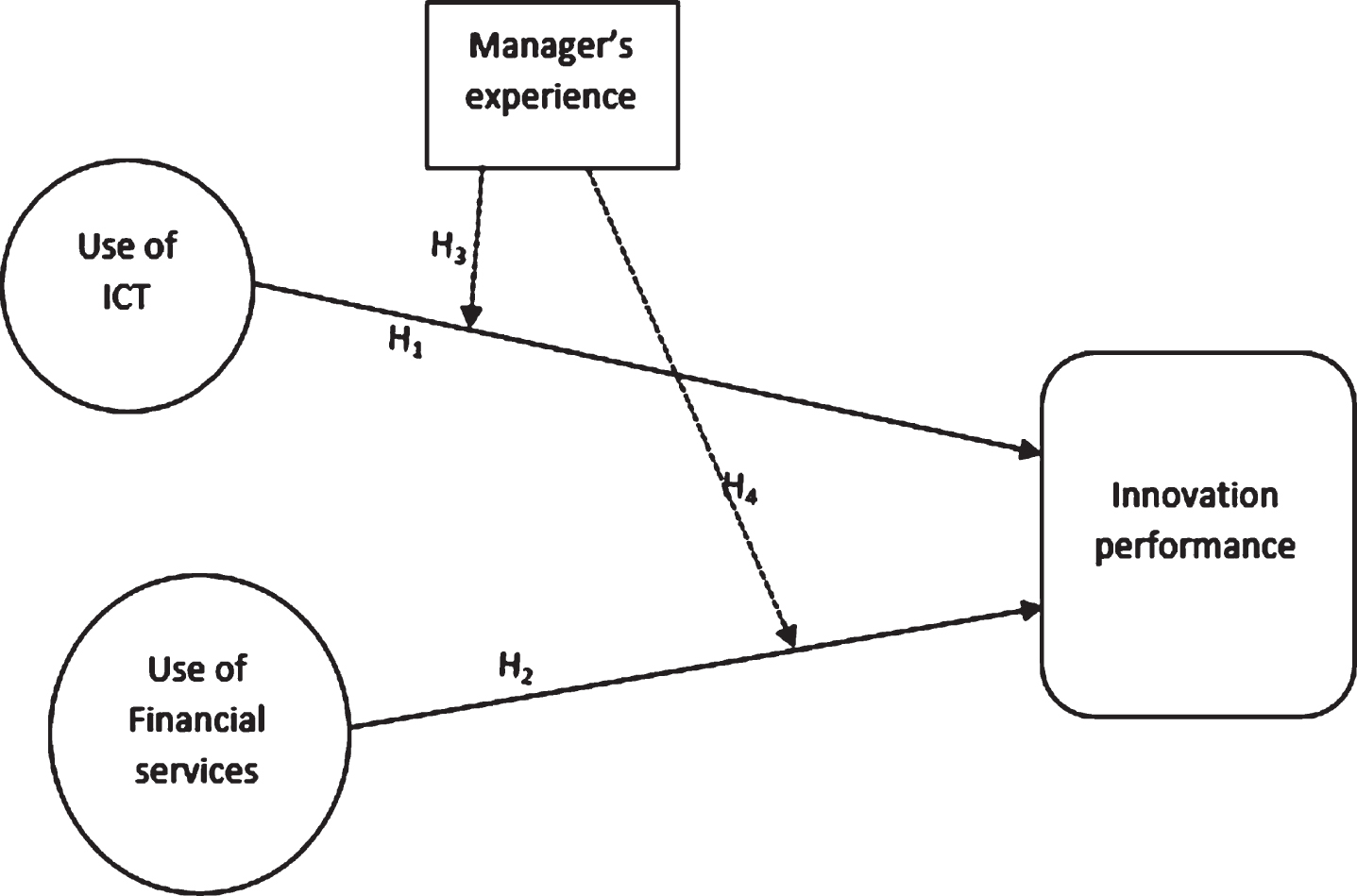

Figure 1 displays the conceptual model of the study. The figure maps the use of ICT and financial services variables influence on firm innovation performance. Also, it depicts the hypothesized mediating role of the SME manager’s experiences shown by the dotted lines.

The study model conceptual framework.

The study is motivated mainly by the dynamic capabilities view derived from the resource-based theory [32]. Teece et al (1997) defined dynamic capabilities as ‘the ability to integrate, build, and reconfigure internal and external competencies to address rapidly-changing environments.’ The theory expresses its focus on the environment of rapid changes and endeavors to specify the bases of value creation and value realization. The theory attempts to locate the capabilities that can lead the firm towards the attainment of competitive advantage. Moreover, the theory attempts to explain how such dynamic capabilities can enhance optimal resource allocation within the firm. This study brings together human, technology and financial resources that are important for firms to optimally allocate thereby attain innovation performance. The consideration of these resources on how they are developed integrated and managed within the firm is at stake. The dynamic capabilities view brings consideration of buffering on the effect of dynamism of the resources and the environments where they are being administered [33].

The use of information technology at the firm level can be depicted in two tiers, first, the technology that is used by finance firms in enhancing processes in business such as insurance, banking, and microfinance. Secondly, the technology that is applied for innovation and offering efficient services to customers [34]. Scholarly literature depicts internal and external factors for firm ICT adoption. The internal factors include firm characteristics, owner/manager characteristics, adoption, the perceived return on investment and implementation costs, and the external factors are social barriers, infrastructure, cultural barriers, political, legal and regulatory factors [35]. All these factors have an influence on firm-level use of technology. Innovation is considered to be an important pillar of firm competitive advantage and ICT introduces multiple ways of enhancing firm innovation capabilities, for instance, ICT can enhance designing speed but also can allow precise and comprehensive design actions [36, 37]. Firms have the ability to manage the internal factor by adopting new strategies but they may find difficulties in managing the external factors. [38] presents three distinct levels of firm adoption of ICT which include; basic assimilation, substantial and sophisticated assimilation. At the first level, the firm tends to have minimal usage of IT and its operations. The substantial assimilation entails several applications and machines that use ICT. The sophisticated assimilation means the integration of the numerous systems and the continuous use of technology in its processes. Most of the firms in Africa fall on the basic adoption category [39]. The factors for determine firm ICT adoption are categorized into factors related to firm staff potential use of ICT, the environment in which the organization operates and the characteristics of the firm [40]. In another viewpoint [41] identifies four groups that are affected by the adoption and use of technology. These include growth, performance, expansion, and introduction of new products. all of these achievable potential outcomes reflect product quality, efficiency, and productivity of the processes.

Innovation is defined in diverse ways and it can mean a minor renovation for existing products, processes, and services or advance transformation [42]. Innovation is concerned with interactions and of events and human resources at various levels and connected to the ongoing process of adapting to the new clinches. At firm-level innovation have two facets namely closed and open innovation. The closed innovation entails firms instituting their own ideas and then they create, market and distribute on self endeavors [21]. But open innovation accumulates internal and external ideas, and offer them to the market while still researching for potential innovative opportunities [43]. Digital innovation adopts new advanced technologies to meet customer desire for improved services/products relative to the existing ones in the market [44, 45]. The technology orientation philosophy reflects the technological push, which implies that customers will favor services and products with superior technology [46]. Technology-based firms are better placed to champion the use of the current technologies in inventing new products and services and substantial resources in research and development. Resulting in excelling in technical expertise, which is a critical derivation for break-through innovation [47].

When it comes to inter-firm innovative collaborations processes, ICT can become an inevitable conduit. There are many ICT tools currently available for firm knowledge management, for instance, there are tools that help in inter-firm R&D that improve the easiness, quality, and extent of knowledge sharing [36]. Besides of ICT enhancing R&D, it can make an information and knowledge base for easier sharing and facilitate the knowledge transfer in and outside the firm environments [48, 49]. ICT can effectively facilitate codification, integration and channel organization knowledge [50, 51].

Firm innovation performance can be contributed by a number of determinants, but the presence and use of new technology have an optimal amplification of innovation processes to achieve the best results [20] established that there is a specific market-oriented application of ICT by SMEs that display a vital potential to generate a competitive advantage in the firm product innovation [52] argues that SMEs’ ICT adoption in Malaysia brought a lower cost-effective tool for communication with customers. nevertheless, problems with security are extensive. The digital processes have greatly facilitated the implementation of novel ways of taming the current process and formation of new products and services. Furthermore, technology is known to be a cornerstone for firm innovation [53, 54]. Technology has brought about simplification and reshaping of the firm products resulting in the ability of the firm to access larger market share [55]. But technology-facilitated innovation may not be successfully achieved without proper access to financial services. The ability of the firm to integrate various sources of finances optimally can promote and facilitate the innovation process [24]. Other factors held constant; we argue that:

H 1 SMEs use of ICT has a positive impact on innovation performance for African firms

H 1a For African SMEs owning a website (OW) and communicating with clients using emails (CE) has a positive association with firm ability to introduce new products and services (INP)

H 1b For African SMEs owning a website and communicating with clients using emails has a positive association with firm ability to introduce or significantly improve its process (IMP)

Use of financial services and firm innovation

African financial sector is generally considered to be underdeveloped and the rural areas are the most vulnerable [56]. The banking sector in sub-Saharan Africa has penetrated to the extent lower than 35% and about 80% of African are constrained to access formal banking services [57]. Scholar empirical evidence from the enterprise survey indicates that 22% of firms have a line of credit or loan, and more than 455 firms still cite access to financial services as major obstacles to enterprise growth [58]. The connection of digital technology into financial interplay has come with the potential to provide, cheap, fast and accessible financial services to consumers and it is thought to bring better solutions in the African informal financial system dominated the market. The financial market is flourished with digital financial services that specifically target SMEs or they may be suitable for the circumstances that enable the consumer to take advantage of unexploited opportunities [59].

[30] on their study for foreign direct investment, access to finance, and innovation activity in chines enterprises found that the firms that have good access to domestic bank loans have more innovations than their counterparts. Therefore, access and actual use of financial services is an important factor for firm innovation activities. And [60] found that better access to stock market financing has a significant positive association with long-run levels of firms investing in R&D which are directly linked to the firm innovation performance and on the contrary access to credit service was found to be unimportant firm R&D activities. The actual use of financial services is considered among important factors that can lead to firm success [61]. Holding other factors constant financing availability can foster establishments to more technological-based innovations otherwise firm sustainability power is jeopardized. We, therefore, propose that:

H 2 SME extent of use of financial services has a positive association on innovation performance in Africa

H 2a For African SMEs having a current or savings account (CSA), having a loan from the financial institution (LOC) and having an overdraft facility (HOF) is positively associated to its ability to introduce new services/products

H 2b For African SMEs having a current or savings account, having a loan from the financial institution and having an overdraft facility is positively associated with its ability to introduce new/significantly improve its process

Role of firm manager’s experience

Considering the smallness and the nature of SME managers are viewed to be responsible for the mode, speed, and direction with which the company advance [62]. The shared characteristics of failed firms have been directly linked to personal decisions of their managers linked to their characteristics of deficiencies in management which may include inflexibility, lack of insight, much focus on technical skills [63]. The expertise of the manager in a particular can be attributed to previous functional experience, self-employment experience or venture creation, experience int eh sector, educational and/or family experience [64]. The influence of the entrepreneur’s experience is claimed to be positive or negative [65]. While experience can enable manager’s to easily tackle commonly experienced problems, they are in danger of inhibiting creativity due to lack of the degree of adaptability when confronted with new issues. When firm managers follow a conservative management style which is limited to products, services, and management that have already proven to work may inhibit firm innovativeness [66].

Scholarly literature confirms that there are a business turnover increases with entrepreneurs having more education and experience [67]. A need for a critical consideration in the managerial competence-performance matrix is the educational achievements and experiences of the owner/manager of the new venture startup. The managerial competencies as determined by the level of education, manager experience, start-up experience and acquaintance of the industry positively influence the performance of SMEs and education provides the knowledge base, logical and problem-solving skills [68]. The technical know-how to effectively deal with the entrepreneurship demands requires intellectual capital that is critical for effective management execution processes to be able to create sustained a firm competitive advantage.

However, in principle, the previous functional experience put the manager in a position of allowing developmental expertise that may result in firm growth. Some empirical studies have proved that management previous experience has a positive impact on firm growth [69]. We assume that a manager who has worked at the apex level of the firm has experience in the number of management areas. Confronted with consultations within and out of the sector environment he/she must have learned flexible management and has an orientation towards entrepreneurial tactics to improve the functionality of the firm [70]. With such characteristics, the manager is able to adapt to new technology and take advantage of the financial products that are accessible by the firm to introduce new products and processes or significantly improve the existing one. Linked to the manager’s experience the innovative managers are constantly seeking improvements and introducing changes, competitive, communicate and have good interpersonal skills [71].

H 3 For African SME’s managers’ experience mediate the use of ICT-innovation performance

H 3a for African SMEs manager’s experience mediate the relationship of OW and CE-INP

H 3b SMEs in Africa manager’s experience mediates the relationship OW and CE-IMP

H 4 For African SMEs Manager’s level of experience mediates the UFS-innovation performance relationship

H 4a For African SME manager’s experience mediate the CSA, HOF and LOC-INP relationship.

H 4b For African SMEs manager’s experience mediate the CSA, HOF, and LOC-IMP

Variables used in the study

This section describes the variables that are used in the study model and they entail the use of ICT, the use of financial services, firm innovations performance, manager experience, and control variables (age and ownership gender).

The use of information and communication technology was determined by the following indicator questions from the database. Do you currently communicate with clients by email? (CE), does the establishment have its own website (OW), Is the internet used to do research and develop a new idea of products and services? Do you use technology licensed by a foreign-owned company? Whether the firm has high speed, broadband internet connection on its premises

Was the internet used to order purchases for this establishment? Is the internet connection used to deliver services to your clients? Is the internet used to do research and develop ideas on new products and services? However, only two variables CE and OW had full responses, the remaining four either have no/or very few responses to render them suitable to feature in the analysis, therefore, they were excluded from the analysis.

The use of financial services (UFS) is the actual consumption of products or services offered by the financial system. And in this case, as per the nature of the data, the use of financial services is reflected by the extent to which firms utilize financial products offered by accessible financial institutions [72]. The questions that were identified as determinant variables for UFS include; Does this establishment have a checking and/ savings account? (CSA), At this time, does the establishment has an overdraft facility? (HOF), and Does the establishment have a line of credit or loan from a financial institution? (LOC). All the three indicators were used in the model analysis

Innovation at a firm-level entails the introduction of new products, services, and processes that add value to the organization; it also involves the improvement of the present products, services, and processes. In the enterprise survey questionnaire, two variables were identified to capture the SME innovation. Did the establishment introduce new products/services over the last 3 years? (INP), and During the last 3 years, did the establishment introduce a new/significantly improved process? (IMP). The same variables also were used by [73].

Manager’s Experience was identified by the question; How many years of experience working in this sector does the top manager have? (ME) and the control variables were the age of the establishment (Age) and ownership gender determined as a percentage of firms owned by women.

Methodology

The study employed data from the enterprise survey portal available at https://www.enterprisesurveys.org/. Enterprise survey is a survey portal at the firm level in various private-sector economies. The data are collected from standardized questionnaires filled by the top managers/owners of the businesses. The raw data are available free to download for researchers as long as you register with a research institution’s official email. The manufacturing and services sectors are the business sectors they feature in the survey.

As the focus of this study is on SMEs in Africa large firms were excluded from the analysis. Table 1, shows a total of 11504 SMEs from the manufacturing and service sector that was included in the analysis. The data were sorted such that they have to be within 5 years (2014–2018) old to maintain their timeliness and comparability. Therefore, after sorting only 27 countries’ features in the analysis. As it is seen in Table 1 the data depict a good blend of eastern, southern, northern, and west Africa rendering to be a better representation of the region. most of the left-out countries’ data were outdated and therefore, couldn’t fit into our range. Table 1 depicts 66.8% of the firms are small which is twice as much of medium. The scenario indicates the domination of small firms in the African context and of course in this analysis. The fact that there are many small firms than medium ones may explain the fact that most of the startups are for survival, inaccessibility to large capitals to start bigger ventures, lack of technical know-how, and stunted growth of ventures with considerable ages. The services firms are more than the manufacturing firms by 18.4%.

Sample characteristics

Sample characteristics

The study uses multiple regression analysis to analyze the model propositions. Statistical package for social science software (SPSS) version 23 was used. Moreover, the mediation analysis is done by using results from SPSS regression analysis input into the Sobel test of mediation.

Table 2, shows descriptive statistics of the data. The information presented comprises of means, standard deviations and correlation of variables. Age and manager’s experience show the highest level of standard deviation which reflects on how the age of the firms and the number of years SMEs manager’s experience under scrutiny have wide disparities from their mean. The linearity of the variable relationship is proved by the presence of positive and significant correlations among most variables except for just two instances where the variables have negative correlations.

Descriptive statistics and correlations

**=significant at p < 0.001 and * significant at p < 0.05.

Table 3, depicts four models that provide the hypothetical results from the multiple regression models related to the study hypothesis. Model 1, provides the results of the proposed influence of the use of ICT on the firm innovation performance. The results indicate for African SMEs owning a website has an insignificant influence on a firm ability to create and introduce a new product/service. However, the firm practice of communication with emails connoting the entire use of internet communications has demonstrated to have a positive significant impact on firm capability to introduce a new product/service. The results partly reject H1a and partly accept the hypothesis. Besides of the insignificant results in the first part, the significant result in the influence of CW on INP provides an important clue on the integrating ICT communication system in the SMEs operationalization that can foster creativity in designing new products and services that can suit the customer need.

Multiple regression results

Multiple regression results

**=significant at p < 0.001 and * significant at p < 0.05; Robust standard errors in parenthesis.

Model 2, examined the influence of the firm use of ICT on its ability to introduce new or significantly improve its process as one aspect of innovation performance. The results indicate that OW still has an insignificant association with IPM which partly denies our hypothesis H1b and accepts the other variable proposition of the influence of CE on IMP. Besides the insignificant results in the first part, the second part of the findings which is significant provides evidence of the usefulness of information technology within the firm to foster SMEs’ innovation capability. ICT enhances generation, development, integration, and improvement of key resources over a certain time lapse. ICT manifest possesses a dynamic feature that new production methods, new business models, e-commerce, new production methods, and better supply management, decision-making processes, new services, and customer relationship management can be fostered [74]. The results are consistent with the findings by [74–76].

In model 3, Table 3 depicts a significant influence of CSA, LOC, and HOF on firm INP in Africa. Among the three variables, HOF has the strongest association with INP. The results confirm our hypothesis H2a which states that for African SMEs having a current or savings account (CSA), having a loan from the financial institution (LOC) and having an overdraft facility (HOF) is positively associated to its ability to introduce new services/products.

Also, in the multiple regression analysis, model 4, confirms that CSA, LOC, and HOF have a significant influence on firm IMP. The result confirms the hypothetical proposition that H2b for African SMEs having a current or savings account, having a loan from the financial institution and having an overdraft facility is positively associated with its ability to introduce new/significantly improve its process. Access to and actual use of financial services is mentioned to be an important factor for efficient operations of SMEs. The availability of bank financing and debt financing can enable SMEs to utilize the available resource base optimally to introduce new products, services, and processes. These results are in tandem with the findings by [77, 78].

Besides the conceptual hypothetical results, the model also presents the results of some other variables associated with firm INP and IMP. The results indicate that age, gender and manager experience all have positive significant influence firm INP and IMP, except for the gender association with firm INP.

The study as depicted in the conceptual model, further examined the mediating effect of SME’s managers’ experience on the relationships of the use of ICT and the use of financial services with firm innovation performance. The procedure was done by using direct and indirect hypothetical regression of the variables results. Then, the ‘Z’ Sobel value was calculated using a Sobel test of mediation to determine whether the variable had a significant influence. Table 4, shows 10 various models that were devised to test the mediating influence of the manager’s experience. The first four models present the mediating role of SME manager’s experience on the use of ICT variables-INP/IMP relationships. The remaining 6 models present the hypothetical mediating influence of managerial experience on the use of financial services variables -INP/IMP relationships.

The mediating role of manager experience

The mediating role of manager experience

**=significant at < 0.001 and * significant at < 0.05. Whereby ‘a’=unstandardized regression coefficient for the association between the independent variable and the mediator in the model, ‘b’=the unstandardized regression coefficient between mediator variable and dependent variable, sa = standard error of ‘a’, and sb = standard error of ‘b’.

Model 1 in Table 4, shows an insignificant direct effect of OW on INP and also it provides the insignificant mediating influence of ME on the OW-INP relationship. The model results do not agree with the hypothesized proposition in H3a. But in model 3 CE has a significant direct association with INP, and ME has been confirmed to significantly mediate the CE-INP relationship. However, the fact that CE has a significant direct association, ME has partial mediation.

Model 2, and Model 4 presents the results relating to hypothesis H3b, which determines the influence of firm use of ICT on IMP. Model 2, depicts a significant direct association of OW and IMP. But, ME is displayed to insignificantly mediate the OW-IMP relationship. Nevertheless, model 4 shows ME significantly mediates the CE-IMP relationship. The mediation is partial since the direct relationship between CE and IMP is also significant. Besides of the insignificant results on ME mediating OW-IMP, the significant mediation role on CE-IMP finding adds new insights to the body of literature. The results imply that the fact that the firm owns its own website and communicates using emails has an impact on the firm ability to device new processes and significantly improve the existing ones gain more insights when managers have the relevant experiences.

Model 5, 7 and 9 generally depict the mediating role of ME on firm use of financial services-INP relationship. The results in all these three models indicate a significant mediating role of ME on SCA, LOC and HOF-INP relationships. All these mediations are partial since the direct relationships between SCA, LOC, and HOF with INP are all significant. The results confirm the hypothesis proposition H4a which states that ME mediates the SCA, LOC and HOF-INP relationship. The results add new insights to the body of knowledge such that the appropriate firm manager’s experience will exemplify more influence on the firm use of present and contemporary financial products to enhance the firm innovation capability.

Model 6, 8, and 10 display the results on the mediating role of ME on SCA, LOC, and HOF-IMP relationships. The results show a significant direct association between SCA, LOC, and HOF with IMP. ME is confirmed to have a significant mediation effect on SCA, LOC and HOF-IMP relationships. Such that, for the effect of the use of financial services on a firm’s ability to introduce new processes and/or significantly improve the existing ones is more explained when firm managers are experienced and competent to manage such innovative caprice. The results are in agreement with the study hypothesis H4b and they add to the body of literature new insights.

Reflecting on the challenges of waves of new information and technology applicability by African firms. The introduction of new financial products and changes in the financial landscape for SME’s financing, placing these factors under the umbrella of SME’s managers’ experience and competence. This study created a model that aimed at first, analyzing the impact of SMEs’ use of information and communication technology, and the use of financial services on innovation performance in African SMEs. The study further examined the mediating roles of manager’s experience on the use of ICT and the use of financial services -innovation performance relationship. As firms move from the challenges of access to information and technology and financial services more challenges unfold as to the applicability of these dynamic resourceful factors in an attempt to enhance their innovation performance. The study demonstrates how important for firms to emphasize fostering competence and relevant experience for SMEs future managers who will be more oriented to harness better results on integrating digital and contemporary financial services to improve the firm innovation performance.

Theoretical implications

The application of the theory of dynamic capabilities in our model, we attempted to analyze how dynamic capabilities of human capital, technology, and financial resources enhance firm innovation performance. and hence boost optimal resource allocation within the firm. The model results support the claim adding a basis and its applicability to firm dynamic operations. Resource-based literature emphasizes the capability of rearranging the resources in a configuration that can support the chosen organization strategy is critical than just having the resource itself [79]. The results of this study are in tandem with most of the study that has strived to analyze SMEs’ dynamic capabilities in configuring various resources for its sustainable performance (e.g. [80–82]. Because of the smallness of SMEs managers/owners are very close to the operations or operating personnel. The organization structure of SMEs is more likely to develop based on the interest of the owners/managers [83]. Therefore, this study has brought novelty of new insights into the body of resource-based theories of firm management by proving that the manager’s experience can significantly mediate the use of information technology-innovation performance relationships. Moreover, the study has demonstrated that the manager’s experience by African firms significantly mediates the use of financial services-innovation performance relationships. Moreover, the literature verify that most scholarly articles have tried to indicate the impact of financial services and innovations in terms of the supply side being able to create innovative services and product for their customers as it is in [84, 85]. By finding significant results on an association of the firm actual use of financial services with innovation performance, the study amplifies the notability of this insight in the literature which is dimly appreciated.

Practical implications

In the era of waves of changing technologies and the introduction of new and hybrid financial products gripping the SMEs’ operationalizations in Africa. Firm managers are called upon to emphasize acquiring competence and relevant experiences to enable them to strategize and integrated optimally the double arrays of new technologies and new financial services to foster firm innovation performance. These can be achieved by fostering learning orientated managers at a personal level which is translated onto entrepreneurial cognizance at a firm-level.

Limitations and further research

The study considered the firm’s data available from the enterprise survey that may be lacking some comprehensiveness in the variables that were eligible for analysis. For instance, the use of ICT considered two variables of the firm owning its website and communicating with email. Further study may wish to consider a comprehensive list of variables indicating the use of ICT by SMEs.

A similar limitation also can be observed while using the managerial experience to generally represent the manager’s characteristics and competency. This is because ME was the only variable featured to have compressive eligible data for analysis. Some relevant variables like level of education and at work skills development were either having no responses at all or having very low response percentage rendering them ineligible for analysis. Further studies may consider to compressively includes all the data for managerial experiences.